MRI Guided Neurosurgical Ablation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

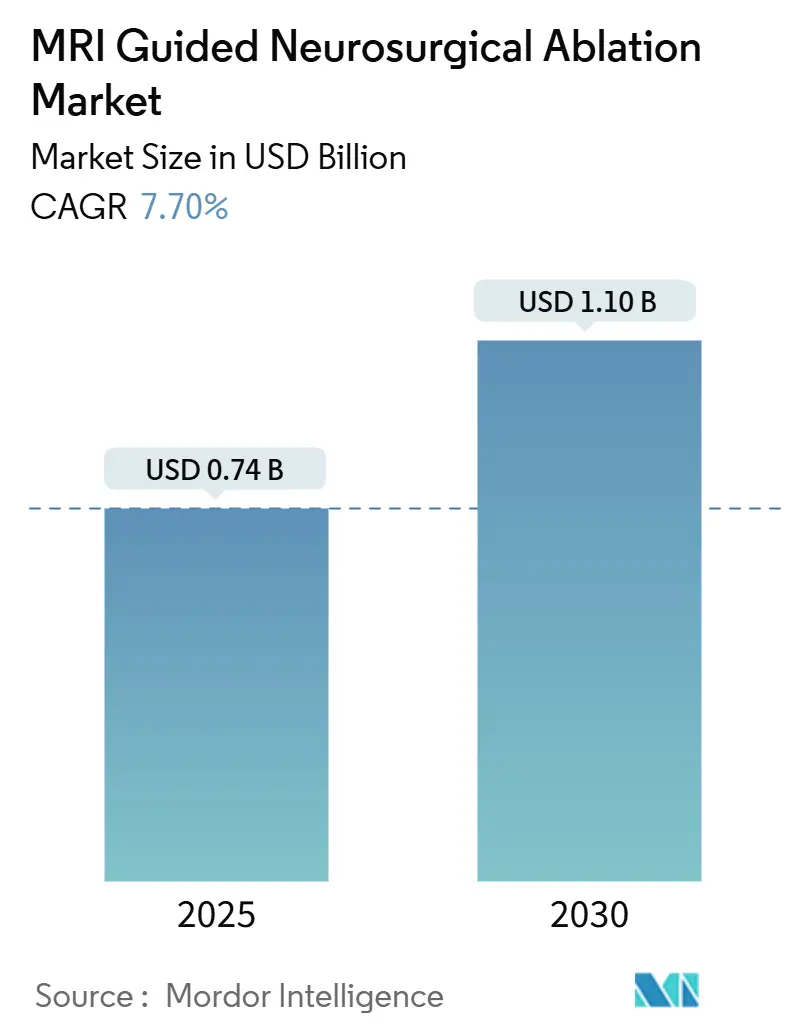

| Market Size (2025) | USD 0.74 Billion |

| Market Size (2030) | USD 1.10 Billion |

| Growth Rate (2025 - 2030) | 7.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MRI Guided Neurosurgical Ablation Market Analysis by Mordor Intelligence

The MRI-guided neurosurgical ablation market size is projected to reach USD 1.10 billion in 2030, up from USD 0.74 billion in 2025, advancing at a 7.7% CAGR between 2025 and 2030. Continuous gains in brain-tumor incidence reporting, the clinical shift from open craniotomy to laser or focused ultrasound, and supportive reimbursement codes in the United States and leading European Union economies sustain the topline trajectory. Device makers are widening disposable portfolios to capture steady revenue from every procedure, while hospital groups leverage outcome data to negotiate higher payer rates. The ecosystem is further buoyed by collaborations between imaging majors and software start-ups that shorten planning times and cut capital payback cycles. Intensifying competition among magnet vendors, coupled with cross-licensing of novel cooling technologies, also helps keep price escalation muted for high-volume purchasers, creating a virtuous cycle of adoption in both mature and emerging centers.

Key Report Takeaways

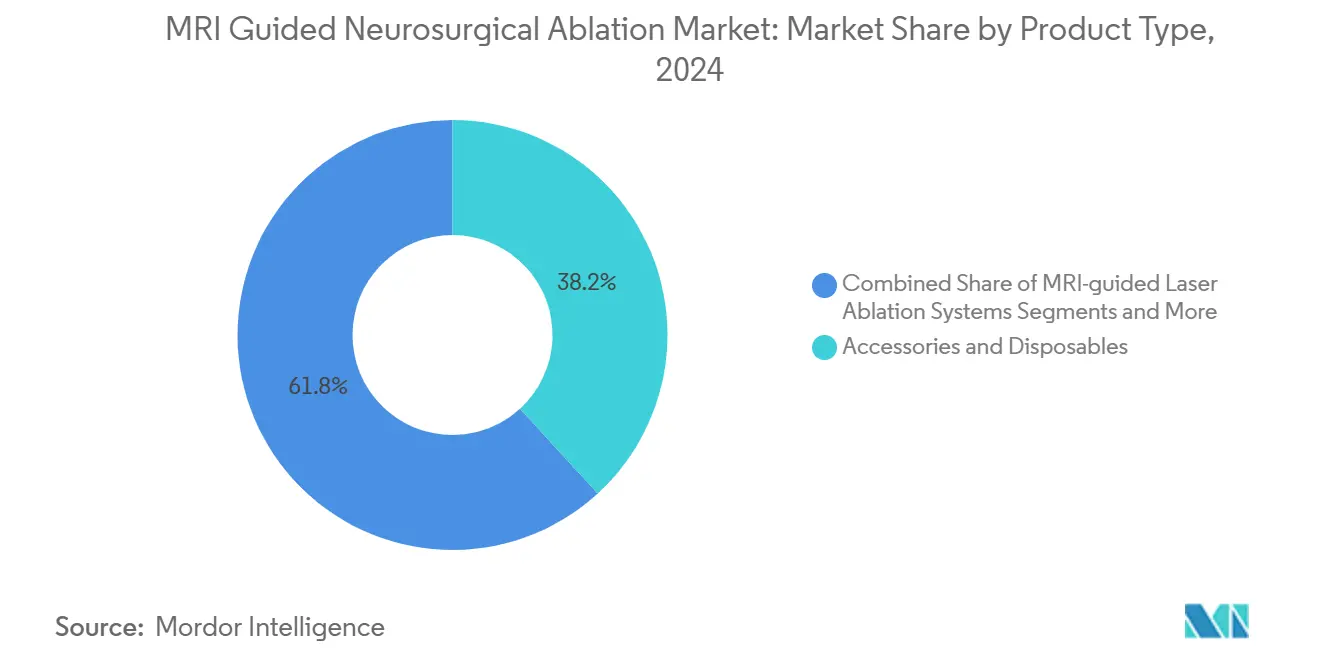

- By product type, accessories and disposables commanded a 38.2% share of the MRI-guided neurosurgical ablation market in 2024, whereas planning and navigation software is forecast to compound at a 7.4% CAGR through 2030.

- By application, brain-tumor ablation accounted for 55.8% of the MRI-guided neurosurgical ablation market size in 2024; psychiatric disorders are poised for the fastest 8.1% CAGR over the same period.

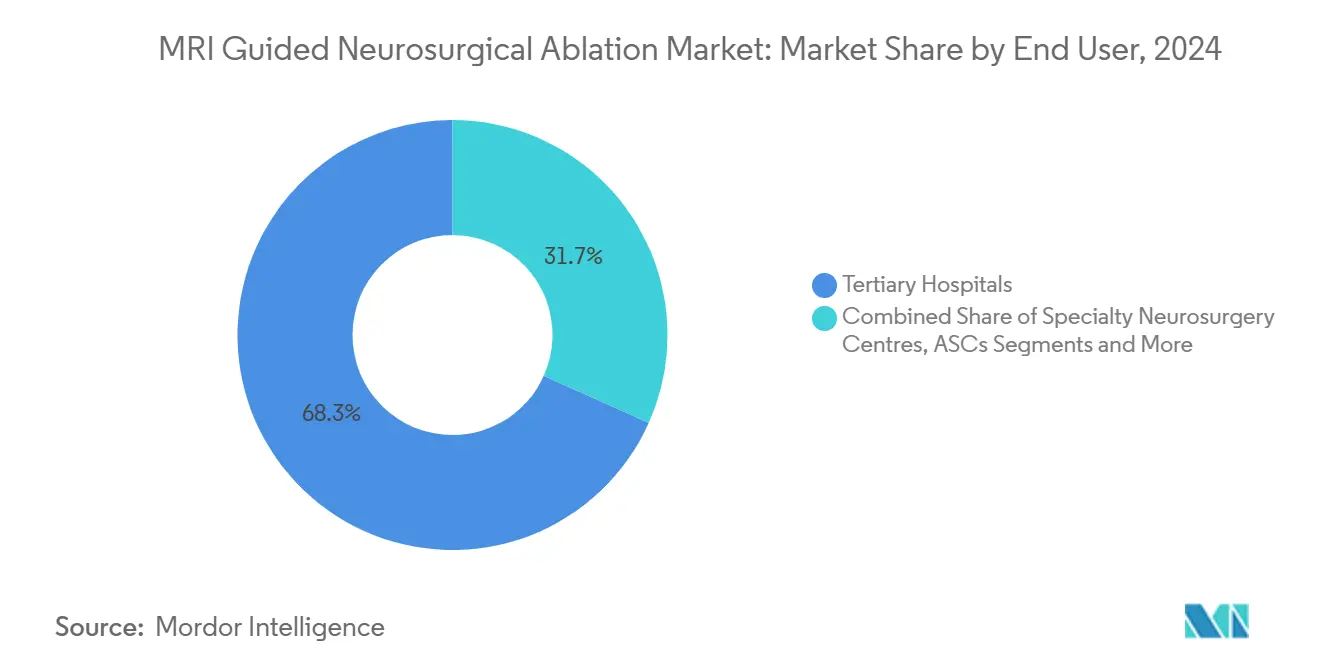

- By end user, tertiary hospitals led with 68.3% revenue share in 2024, while ambulatory surgical centers are projected to expand at a 6.9% CAGR between 2025 and 2030.

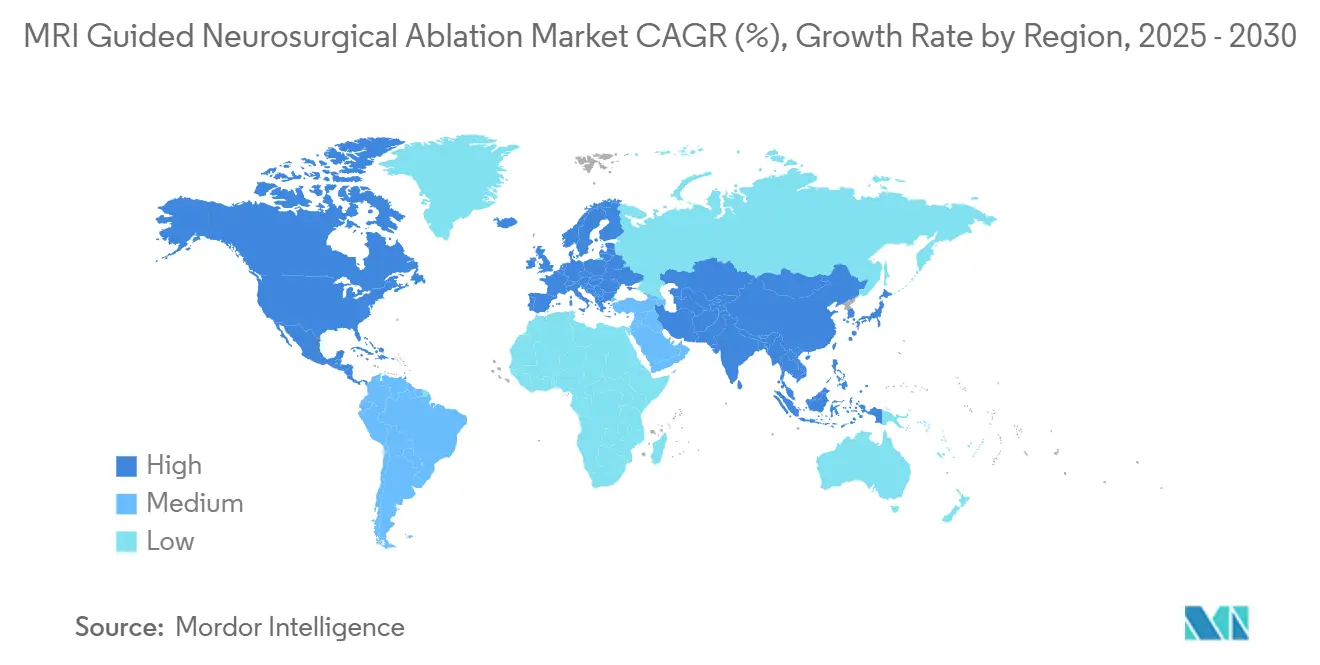

- By geography, North America held 45.6% of the MRI-guided neurosurgical ablation market share in 2024; Asia Pacific is set to grow at an 8.4% CAGR to 2030.

Global MRI Guided Neurosurgical Ablation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Brain Tumours & Drug-Resistant Epilepsy | +2.10% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Growing Preference For Minimally Invasive Neurosurgery | +1.80% | Global, led by developed markets | Short term (≤ 2 years) |

| MRI-Compatible System & Thermometry Advances | +1.40% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Expanding Reimbursement Approvals In US & EU | +1.20% | North America & Europe primarily | Medium term (2-4 years) |

| BBB-Disruption Synergy For Drug Delivery | +0.90% | Global research centers, early clinical adoption | Long term (≥ 4 years) |

| 7-T MRI & AI-Driven Planning Adoption | +0.80% | North America & Europe, selective APAC centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Brain Tumors & Drug-Resistant Epilepsy

Brain-tumor cases and medically refractory epilepsy have risen steadily since 2024, leading to greater neurosurgical case volumes. Laser interstitial thermal therapy and transcranial focused ultrasound reduce operative morbidity and shorten intensive-care stays, making them first-line options in specialized centers. Leading academic hospitals now publish two-year seizure-freedom rates beyond 70%, which reinforces payer confidence. Patient advocacy groups lobby for early surgical referral, translating into faster pipeline conversion for device vendors. The trend keeps procedure revenue resilient during broader capital budget slowdowns, sustaining the MRI-guided neurosurgical ablation market.[1]National Cancer Institute, “Brain Tumor Statistics, 2025 Update,” National Cancer Institute, nci.nih.gov

Growing Preference for Minimally Invasive Neurosurgery

Surgeons underscore smaller incisions, reduced hospital stays, and rapid neurological recovery as key determinants of patient satisfaction. Marketing teams have responded with simulation-based workshops that upskill residents in laser trajectory planning within 30 minutes. Insurance databases from the United States show an average USD 7,500 decrease in total episode-of-care cost versus open craniotomy, prompting value-based purchasing teams to favour ablation. Government quality-metrics programs reward centers that cut readmission rates, creating further pull. This convergence keeps the MRI-guided neurosurgical ablation market on a double-digit utilization path in the short term.[2]Centers for Medicare & Medicaid Services, “Hospital Outpatient Prospective Payment System 2025,” Centers for Medicare & Medicaid Services, cms.gov

MRI-Compatible System & Thermometry Advances

Vendors have shifted from passive fiber-optic sensors to real-time proton-resonance frequency monitoring, ensuring temperature accuracy within 1 °C. The upgrade permits surgeons to halt energy delivery immediately before eloquent-cortex thresholds are reached. Compact laser generators now fit inside 1.5-T scanner rooms, eliminating the need for separate C-arms. Technology harmonization across coils, shields, and navigation hubs simplifies procurement and drives multiprocedure discounts, lifting the MRI-guided neurosurgical ablation market in cost-sensitive institutions.[3]Richard Ehman, “Advances in MR Thermometry,” Radiological Society of North America, rsna.org

Expanding Reimbursement Approvals In US & EU

In 2025, the Centers for Medicare & Medicaid Services assigned APC-5165 status to laser interstitial therapy for brain lesions, raising facility fees by 12%. Germany’s Institut für das Entgeltsystem im Krankenhaus included MR-guided focused ultrasound for tremor under OPS-8-980.4, ensuring full Diagnosis-Related Group funding. France adjusted its Liste des Produits et Prestations Remboursables to add disposable laser applicators, guaranteeing 100% coverage under public insurance. These policy wins provide predictable cash flow that offsets capital amortization, reinforcing supplier order books and enlarging the MRI-guided neurosurgical ablation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Procedural Costs | -1.90% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Limited MRI Suite / Neurosurgeon Availability | -1.30% | Global, acute in rural and developing regions | Medium term (2-4 years) |

| Thermal-Safety Issues Near MR-Conditional Implants | -0.80% | Global, concentrated in markets with high implant penetration | Medium term (2-4 years) |

| Reimbursement Gaps For Psychiatric/Off-Label Uses | -0.60% | North America & Europe primarily, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Procedural Costs

A 3-Tesla installation with laser capabilities can exceed USD 3 million, while single-use applicators are priced at USD 8,000. Budget-constrained hospitals delay purchase decisions until case load certainty is reached. Secondary centers often outsource complex ablations, limiting geographic diffusion. Vendor financing packages help, but require minimum volume commitments that not all sites can meet. These factors collectively subtract growth momentum from the MRI-guided neurosurgical ablation market.

Limited MRI Suite / Neurosurgeon Availability

Wait times for elective scanners average 42 days in non-urban United States regions, delaying procedure scheduling. According to the World Federation of Neurosurgical Societies, the global neurosurgeon workforce remains below 23,000, against a projected demand for 50,000. Fellowships specializing in MRI-guided techniques are available at fewer than 15 centers worldwide. Staff limitations compel hospitals to cap daily ablation slots, suppressing throughput and thereby restraining the MRI-guided neurosurgical ablation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Accessories dominance alongside software acceleration

Accessories and disposables accounted for 38.2% of the MRI-guided neurosurgical ablation market share in 2024, driven by the need to replace laser sheaths and focused ultrasound membranes after each procedure. The stable consumables stream secures recurring revenue, enabling vendors to bundle starter kits with new console placements. Single-use items also face minimal regulatory barriers, promoting rapid iteration in cooling line design and the integration of fiber-optic sensors. Growing regulatory scrutiny over infection prevention adds further impetus, as disposable kits guarantee sterility without the time-intensive reprocessing required for reusable kits.

Planning and navigation software is forecast to expand at a 7.4% CAGR, the quickest among product categories. Cloud-based modules that automatically segment lesions and overlay trajectory risk maps reduce planning time by 40%. Deep-learning engines learn from prior cases and adjust safety margins in real time, creating a feedback loop that improves outcomes. Hospitals capitalize on software upgrades to extend the life cycles of their hardware, deferring large-ticket replacements. Competitive licensing models, where costs scale with usage rather than fixed seats, underpin adoption in mid-size centers.

By Application: Brain-tumor preeminence with psychiatric momentum

Brain-tumor ablation captured 55.8% of the MRI-guided neurosurgical ablation market in 2024, driven by higher lesion volumes and clear survival endpoints. Surgeons increasingly prefer laser therapy for deep-seated gliomas, achieving gross-total ablation while sparing eloquent cortex. The modality demonstrates reduced intensive-care unit time and faster steroid tapering, enhancing quality-of-life metrics. Strong dataset publication accelerates guideline inclusion, reinforcing the segment’s lead. Device makers tailor applicator lengths to varied tumor geometries, thereby consolidating procedural confidence.

Psychiatric indications such as obsessive-compulsive disorder and treatment-resistant depression are forecast to register an 8.1% CAGR until 2030. Early pilot data reveal symptom reduction scores exceeding 45% at six-month follow-up, stoking demand in academic psychiatry units. Regulatory bodies in Canada and Australia have granted compassionate-use approvals, allowing physicians to treat select cases while broader trials continue. Advocacy organizations lobby for permanent procedural codes, which would establish a stable reimbursement framework. Manufacturers collaborate with mental health specialists to refine targeting algorithms, thereby strengthening future growth prospects in the MRI-guided neurosurgical ablation market.

By End User: Tertiary dominance balanced by ambulatory rise

Tertiary hospitals owned 68.3% of the MRI-guided neurosurgical ablation market share in 2024, primarily due to the integration of imaging suites, extensive critical-care support, and multidisciplinary tumor boards. Capital budgets at these institutions often accommodate high-field magnets and proprietary lasers under academic grants. Risk management teams favor in-house capacity, as it controls quality scores and maximizes downstream radiology revenue. The concentration also helps vendors justify service contracts, ensuring optimal uptime and reliability.

Ambulatory surgical centers are on track for a 6.9% CAGR through 2030 as procedural times fall below 90 minutes and anesthesia protocols shift toward monitored care. The freestanding format appeals to payers that seek lower facility fees. Device manufacturers respond with cart-based laser generators that slide into mobile MRI trailers. Partnerships with third-party imaging providers enable ambulatory centers to schedule high-volume weekend cases, thereby improving asset utilization. Patient preference for same-day discharge further accelerates this trend, broadening the market for MRI-guided neurosurgery ablation.

Geography Analysis

North America accounted for 45.6% of global revenue in 2024, anchored by early FDA clearances and well-established payer frameworks. The United States Medicare system increased outpatient payment rates for MR-guided focused ultrasound by 5% in 2025, prompting adoption across community hospitals. Canada’s provincial health authorities funded four additional laser systems under targeted epilepsy programs. Research consortia in Boston and Toronto supply high-quality evidence, reinforcing clinician confidence and keeping the MRI-guided neurosurgical ablation market on a robust path.

Europe follows with steady but heterogeneous uptake. Germany and Italy deploy focused ultrasound primarily for movement disorders, while the United Kingdom emphasizes laser therapy for cerebral metastases within National Health Service innovation clusters. Cross-border collaborative studies harmonize outcome metrics, aiding reimbursement negotiations. European Union medical device regulation requires post-market surveillance reports, which compel vendors to maintain robust clinical support teams. These coordinated efforts sustain the MRI-guided neurosurgical ablation market size across the continent.

Asia Pacific is forecast to post the fastest 8.4% CAGR through 2030. China’s tier-one hospitals integrate 7-Tesla scanners with domestic laser probes, while Japanese centers exploit high-precision robotics to streamline burr-hole placement. India witnesses a private-sector push as large hospital chains market ‘scar-less brain surgery’ packages. Regional governments channel public health funds towards neurological disorders due to demographic aging, creating fertile ground for grant installations. The growing demand for minimally invasive options among medical tourists further strengthens Asia’s contribution to the MRI-guided neurosurgical ablation market.

Competitive Landscape

The supplier ecosystem consists of diversified conglomerates, pure-play laser firms, and focused ultrasound specialists. Medtronic leverages its global neurosurgery salesforce to bundle laser systems with external ventricular drains, thereby penetrating new oncology accounts. Monteris Medical concentrates on dedicated brain-tumor centers and reports a 20% increase in disposable sales in 2025 following the release of its NeuroBlate Optic fiber. ClearPoint Neuro deepens integration with 3-Tesla scanners through its platform upgrade that shortens planning cycles by 15%.

Imaging multinationals such as Siemens Healthineers, GE Healthcare, and Philips extend competitive pressure by embedding proprietary temperature-mapping algorithms in their premium scanner lines. These embedded solutions enable turnkey offerings that appeal to capital committees keen on single-vendor procurement. Start-ups like Lunit apply convolutional neural networks to refine lesion segmentation accuracy, triggering collaboration agreements with device manufacturers. This blend of hardware, software, and artificial intelligence capabilities defines the next frontier in the MRI-guided neurosurgical ablation market.

Strategic moves during 2024–2025 include Insightec’s partnership with Boston Scientific to co-promote focused ultrasound for essential tremor, and Abbott Laboratories’ minority investment in NeuroOne to access thin-film electrode technology. Elekta AB entered a distribution arrangement with CLS to deploy laser applicators in Nordic markets. Profound Medical received Conformité Européenne mark for its next-generation trans-cranial system in June 2025. These initiatives collectively heighten competitive rivalry while accelerating procedure innovation within the MRI-guided neurosurgical ablation market.

MRI Guided Neurosurgical Ablation Industry Leaders

Medtronic plc

Monteris Medical Inc.

Insightec Ltd.

ClearPoint Neuro, Inc.

Boston Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Insightec's Exablate Neuro pallidotomy received FDA approval, expanding its use to treat Parkinson's disease. This milestone opens new possibilities for addressing movement disorders and highlights the technology's precision in targeting deep brain structures.

- December 2024: NeuroOne Medical Technologies achieved a significant breakthrough by completing its first human implant procedure at University Hospitals using the OneRF ablation system. This success marks the system's transition from development to real-world clinical use in MRI-guided thermal ablation.

- October 2024: NeuroOne Medical Technologies strengthened its global presence by expanding its distribution partnership with Zimmer Biomet for the OneRF thermal ablation system. This collaboration leverages Zimmer Biomet's established neurosurgical network to accelerate international market growth.

Global MRI Guided Neurosurgical Ablation Market Report Scope

As per the scope of the report, MRI-guided neurosurgical ablation is a minimally invasive surgical procedure that uses magnetic resonance imaging (MRI) to precisely target and destroy abnormal brain tissue, such as tumors, epileptic foci, or other neurological lesions.

The segmentation for the MRI-guided neurosurgical ablation market is categorized by product type, application, end user, and geography. By product type, it includes MRI-guided laser ablation systems, MRI-guided focused ultrasound systems, accessories and disposables, planning/navigation software, and service and maintenance contracts. By application, it covers brain tumor ablation, drug-resistant epilepsy, movement disorders (ET, Parkinson's), psychiatric disorders (OCD, depression), and radiation necrosis and other indications. By end user, the segmentation comprises tertiary hospitals, specialty neurosurgery centers, ambulatory surgical centers, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| MRI-guided Laser Ablation Systems |

| MRI-guided Focused Ultrasound Systems |

| Accessories & Disposables |

| Planning / Navigation Software |

| Service & Maintenance Contracts |

| Brain Tumour Ablation |

| Drug-Resistant Epilepsy |

| Movement Disorders (ET, Parkinson's) |

| Psychiatric Disorders (OCD, Depression) |

| Radiation Necrosis & Other Indications |

| Tertiary Hospitals |

| Specialty Neurosurgery Centres |

| Ambulatory Surgical Centres |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | MRI-guided Laser Ablation Systems | |

| MRI-guided Focused Ultrasound Systems | ||

| Accessories & Disposables | ||

| Planning / Navigation Software | ||

| Service & Maintenance Contracts | ||

| By Application | Brain Tumour Ablation | |

| Drug-Resistant Epilepsy | ||

| Movement Disorders (ET, Parkinson's) | ||

| Psychiatric Disorders (OCD, Depression) | ||

| Radiation Necrosis & Other Indications | ||

| By End User | Tertiary Hospitals | |

| Specialty Neurosurgery Centres | ||

| Ambulatory Surgical Centres | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the MRI-guided neurosurgical ablation market?

The market is valued at USD 0.74 million in 2025 and is forecast to reach USD 1.10 million by 2030.

Which application category contributes the most revenue?

Brain-tumor ablation delivers 55.8% of total revenue, driven by high prevalence and clear surgical indications.

Which region is growing the fastest in MRI-guided neurosurgical ablation?

Asia Pacific is expected to grow at an 8.4% CAGR from 2025 to 2030.

What product segment posts the highest growth rate?

Planning and navigation software shows the fastest expansion at a 7.4% CAGR.

What is the main restraint limiting wider adoption?

High capital expenditure coupled with limited specialized staffing constrains procedural expansion, especially in emerging markets.

Page last updated on: