Multimodal Imaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

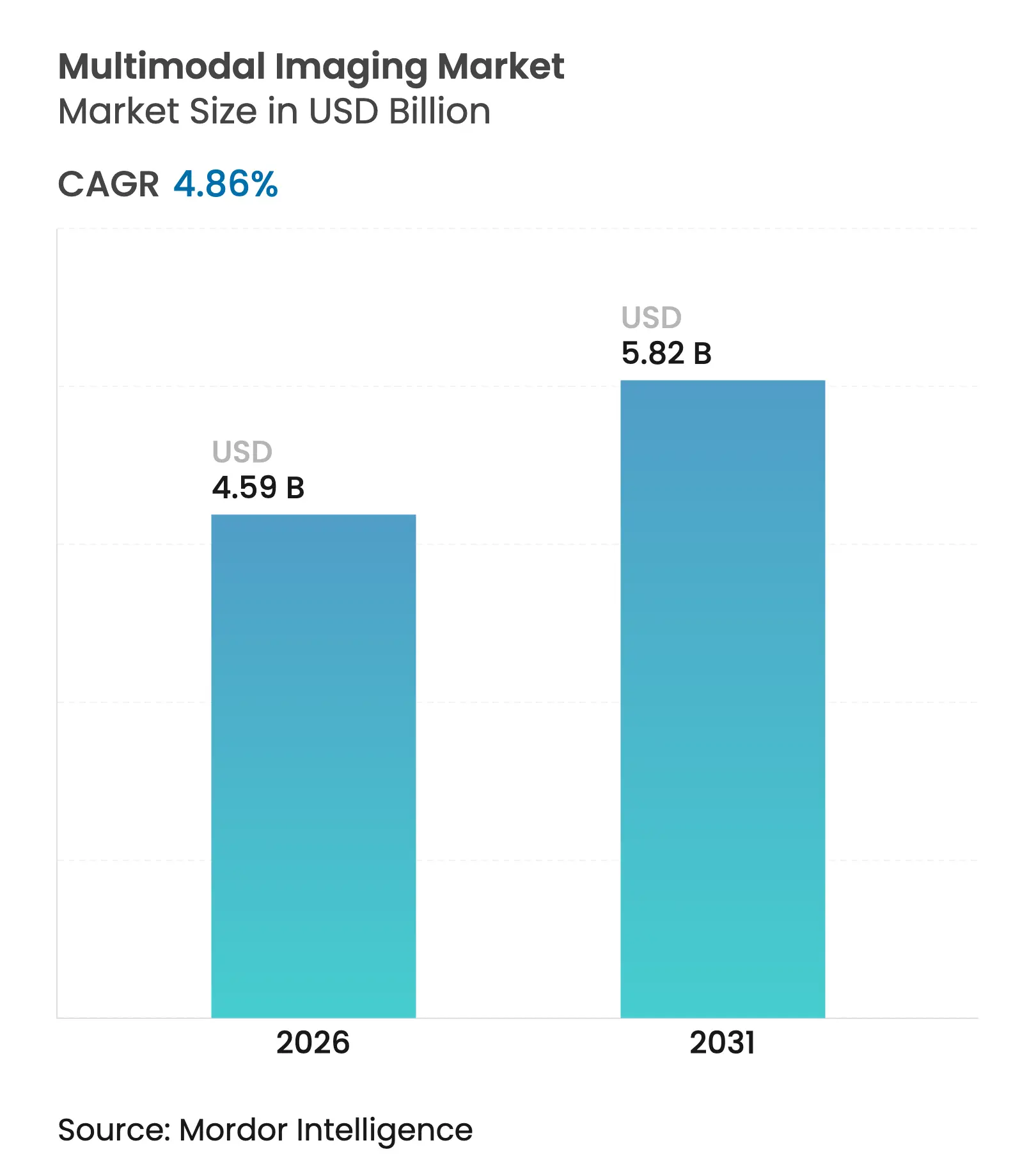

| Market Size (2026) | USD 4.59 Billion |

| Market Size (2031) | USD 5.82 Billion |

| Growth Rate (2026 - 2031) | 4.86 % CAGR |

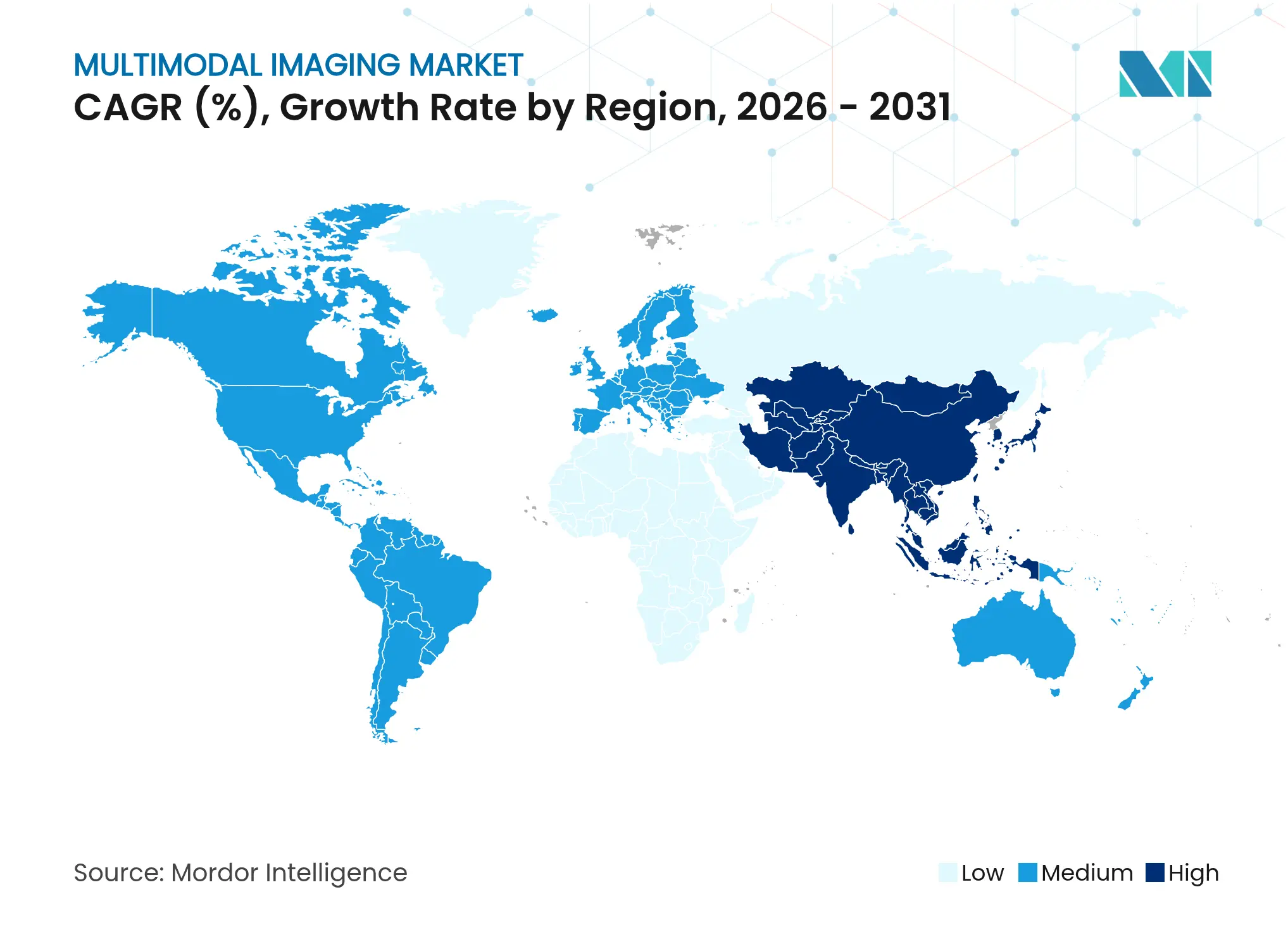

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Multimodal Imaging Market Analysis by Mordor Intelligence

The Multimodal Imaging market size is expected to grow from USD 4.38 billion in 2025 to USD 4.59 billion in 2026 and is forecast to reach USD 5.82 billion by 2031 at 4.86% CAGR over 2026-2031. Growth is shaped by health-system emphasis on hybrid diagnostic platforms that merge anatomical and functional data, strengthening early detection and treatment-monitoring accuracy in oncology and cardiology. Artificial-intelligence overlays automate scan protocols, shorten exam times, and elevate diagnostic confidence, while regulatory approvals for next-generation devices accelerate market adoption. North America retains leadership through robust reimbursement and wide theranostic radiopharmaceutical use, yet Asia-Pacific delivers the fastest trajectory on the back of hospital modernization, chronic-disease burden, and expanding private healthcare investment. The competitive field remains moderately consolidated around GE Healthcare, Siemens Healthineers, and Philips, each leveraging cloud-based analytics to differentiate performance and reduce ownership costs. Persistent headwinds—capital intensity, isotope-supply volatility, and data-integration hurdles—temper the otherwise positive outlook for the multimodal imaging market.

Key Report Takeaways

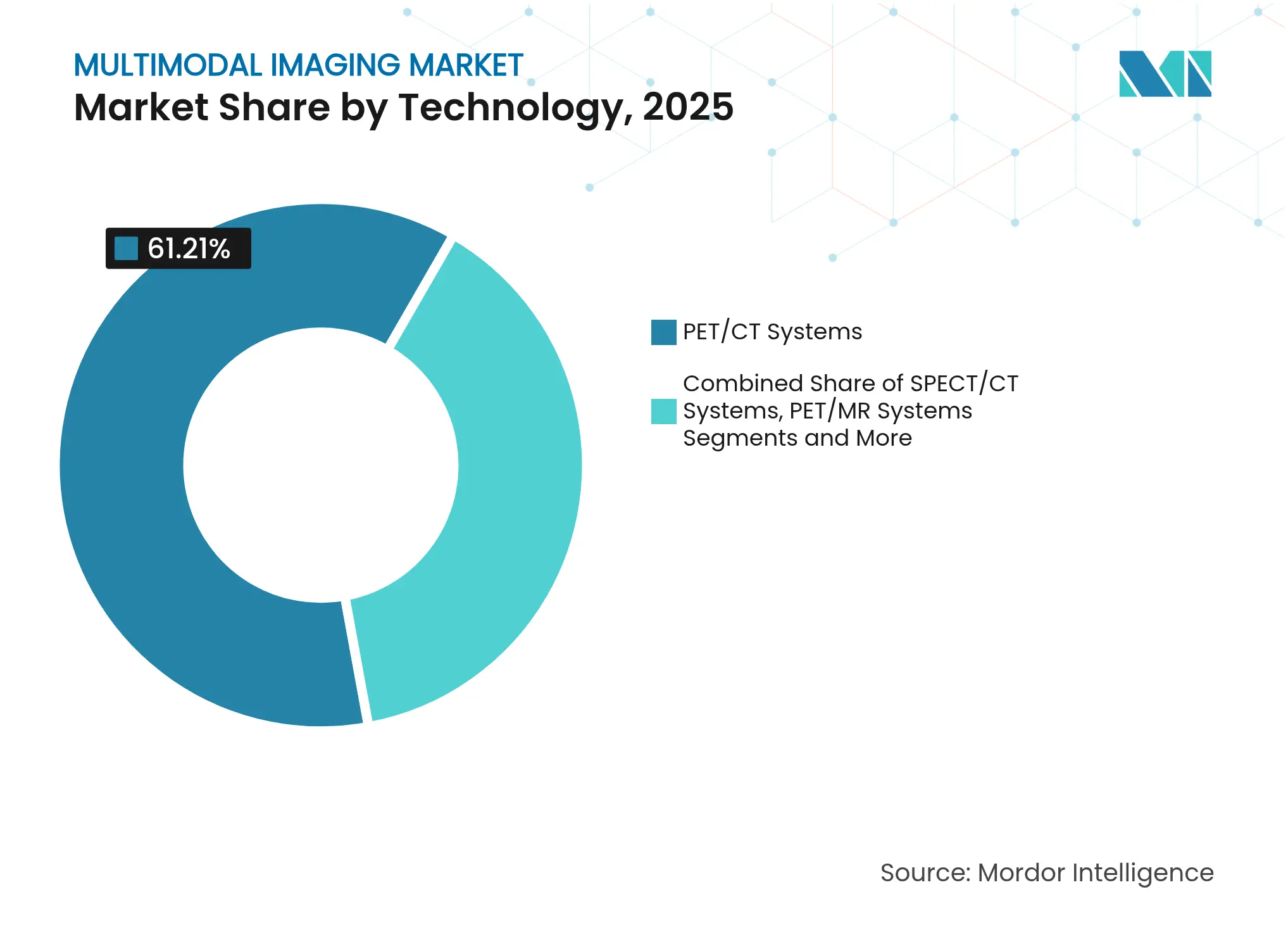

- By technology, PET/CT systems led with 61.21% of multimodal imaging market share in 2025, while PET/MR is forecast to expand at a 5.82% CAGR through 2031.

- By application, oncology captured 58.67% of the multimodal imaging market size in 2025 and cardiology is projected to advance at a 7.32% CAGR to 2031.

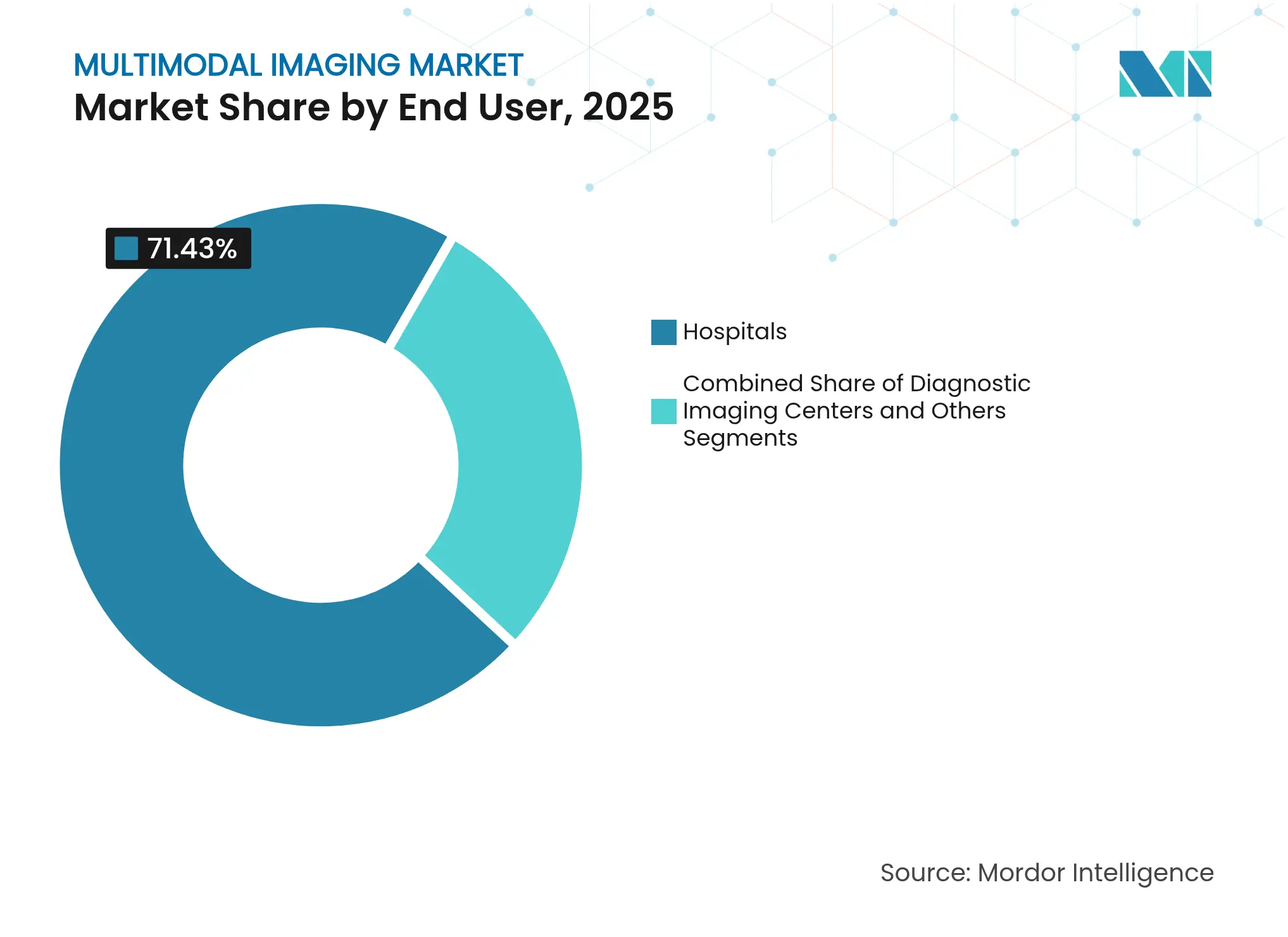

- By end-user, hospitals held 71.43% revenue share of the multimodal imaging market in 2025, while diagnostic imaging centers are growing the fastest at 6.05% CAGR.

- By geography, North America contributed 39.72% of the multimodal imaging market size in 2025; Asia-Pacific is advancing at a 6.47% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Multimodal Imaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing Prevalence of Chronic Diseases

Growing Prevalence of Chronic Diseases

| +1.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global, with concentration in North America & Europe

|

Impact Timeline

:

Long term (≥ 4 years)

|

Technological Advancements in Hybrid Modalities

Technological Advancements in Hybrid Modalities

| +0.8% | North America & EU leading, APAC adoption accelerating | Medium term (2-4 years) | |||

Rising Demand for Early Cancer Diagnosis

Rising Demand for Early Cancer Diagnosis

| +0.9% | Global, particularly strong in developed markets | Medium term (2-4 years) | |||

Increasing PET/CT Use in Cardiology Workflows

Increasing PET/CT Use in Cardiology Workflows

| +0.7% | North America & Europe core, expanding to APAC | Short term (≤ 2 years) | |||

Theranostic Radiopharmaceutical Expansion

Theranostic Radiopharmaceutical Expansion

| +0.6% | North America & EU leading, selective APAC markets | Long term (≥ 4 years) | |||

Portable Multimodal Systems for Remote Care

Portable Multimodal Systems for Remote Care

| +0.5% | Global, with early adoption in rural and underserved areas | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Prevalence of Chronic Diseases

Rising incidence of cancer and cardiovascular disorders keeps demand for sophisticated diagnostics high. Multimodal imaging delivers metabolic–anatomical correlation that single-modality exams cannot match, positioning the modality at the centre of preventive-care strategies. Cardiovascular MRI contributed measurable cost savings and outcome gains in a 361-patient study, underscoring health-economic value. Utilisation is projected to climb 27% in 30 years, reflecting demographic ageing and expanding clinical protocols rather than population growth alone. Oncology PET/CT volumes will benefit directly, as metabolic mapping improves early tumour detection and response assessment. The sustained rise in non-communicable disease prevalence therefore injects durable momentum into the multimodal imaging market.

Technological Advancements in Hybrid Modalities

Hybrid scanners now integrate AI to automate protocols and sharpen image clarity. Siemens Healthineers’ Biograph Horizon employs 4 × 4 mm LSO crystals and true time-of-flight, delivering high-resolution studies at reduced dose. Total-body PET enables dynamic acquisition, producing superior contrast while shrinking acquisition windows. Philips and NVIDIA jointly built MR foundation models that allow “zero-click” planning, promoting reproducibility and faster throughput. Such advances reduce technologist workload, increase scanner utilisation, and strengthen clinical-decision support—elements that fuel uptake across the multimodal imaging market.

Rising Demand for Early Cancer Diagnosis

Screening programmes now embed multimodal workflows to heighten accuracy. The FDA cleared Lumisight and Lumicell DVS fluorescence guidance for breast-conserving surgery, achieving 84% accuracy in detecting residual disease and cutting re-operation risk. PET/MRI in cervical cancer, augmented by parallel-encoder U-Net, reached a 0.726 Dice score for tumour segmentation. 18F-FES PET combined with 18F-FDG elevates confidence when staging estrogen-receptor-positive breast tumours. These breakthroughs reinforce the pre-eminence of hybrid modalities in oncology and expand the addressable base for the multimodal imaging market.

Increasing PET/CT Use in Cardiology Workflows

Cardiac PET/CT distinguishes viable from scarred myocardium, guiding revascularisation and raising quality-adjusted life years at acceptable thresholds. Long-axial field-of-view PET/CT reduces radiation while enabling faster whole-body studies, beneficial for unstable cardiac patients. AI-driven quantification packages accelerate perfusion analysis and standardise reporting. Together, these factors integrate cardiac PET/CT deeper into routine cardiology pathways, broadening revenue streams for the multimodal imaging market. Integration with AI-powered analysis platforms streamlines workflow efficiency while maintaining diagnostic accuracy standards required for clinical decision-making.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Capital and Maintenance Costs

High Capital and Maintenance Costs

| -0.9% | Global, particularly acute in emerging markets | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

-0.9%

|

Geographic Relevance

:

Global, particularly acute in emerging markets

|

Impact Timeline

:

Long term (≥ 4 years)

|

Inadequate Imaging Infrastructure (Emerging Markets)

Inadequate Imaging Infrastructure (Emerging Markets)

| -0.6% | APAC developing markets, MEA, parts of South America | Medium term (2-4 years) | |||

Medical-Isotope Supply-Chain Vulnerabilities

Medical-Isotope Supply-Chain Vulnerabilities

| -0.4% | Global, with regional variations in supply security | Short term (≤ 2 years) | |||

Interoperability & Data-Integration Hurdles

Interoperability & Data-Integration Hurdles

| -0.3% | Global, affecting all healthcare systems | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Capital and Maintenance Costs

Hybrid scanners require multi-million-dollar outlays and specialised upkeep, hampering acquisition in budget-constrained settings. Emergency-department studies show that although multimodal CT elevates diagnostic certainty for dizziness, economic burden deters blanket implementation.[1]Source: Long H. Tu, “Cost-Effectiveness of CT, CTA, MRI…,” PUBMED.NCBI.NLM.NIH.GOV Reimbursement frameworks often trail innovation, amplifying payback risk and limiting diffusion across the multimodal imaging market. The diagnostic imaging market faces consolidation pressures as providers seek economies of scale to manage these cost challenges while maintaining service quality standards.

Inadequate Imaging Infrastructure (Emerging Markets)

Power-supply variability, cooling requirements, and limited engineering workforces restrict hybrid technology roll-outs in developing economies. Regulatory diversity further complicates approvals, with decentralised EU pathways contrasting US FDA reviews.[2]Source: Long H. Tu, “Cost-Effectiveness of CT, CTA, MRI…,” PUBMED.NCBI.NLM.NIH.GOV Training gaps intensify deployment challenges, slowing growth in the multimodal imaging market across underserved geographies. These infrastructure gaps particularly affect rural and underserved populations where portable solutions offer the most significant potential impact.

Segment Analysis

By Technology: Hybrid PET/CT Remains Mainstay While PET/MR Accelerates

PET/CT systems accounted for 61.21% of the multimodal imaging market share in 2025, supported by broad clinical guidelines and mature reimbursement pathways. This technology underpins cancer staging, myocardial perfusion, and neurological metabolism evaluation, making it indispensable for hospital workflows. The multimodal imaging market size for PET/CT is growing closely with expanding oncology caseloads. Vendors differentiate via detector materials, longer axial field-of-view, and AI-assisted protocol optimisation to shrink radiation dose and speed throughput.

PET/MR, though currently smaller, records a 5.82% CAGR, buoyed by unparalleled soft-tissue contrast and reduced ionising exposure. Advances in deep-learning reconstruction, such as Philips SmartSpeed Precise, now cut exam times and improve SNR, making PET/MR more workflow-friendly. The multimodal imaging market size for PET/MR is projected to grow in the coming years as oncology centres adopt the modality for paediatric and neuro-oncology indications. SPECT/CT sustains demand in bone metastasis and cardiology perfusion, where isotope costs remain manageable. Niche combinations, including ultrasound/CT, hold specialised roles in interventional suites, rounding out the technology mix within the multimodal imaging market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Oncology Dominates, Cardiology and Neurology Gain Momentum

Oncology controlled 58.67% of the multimodal imaging market size in 2025, and a forward CAGR of 5.62%. Tumour-specific radiotracers, fluorescence-guided resection, and AI-driven segmentation expand clinical utility, reinforcing the value proposition of hybrid platforms. Cardiology follows, leveraging PET/CT to quantify perfusion and plaque inflammation, an approach forecast to capture a growth of 7.32% in the coming years from 2026 to 2031.

Neurology applications, from amyloid‐beta imaging to epilepsy focus localisation, register steady uptake as ageing populations boost dementia screening. Musculoskeletal applications demonstrate strong growth potential through PET/CT and PET/MRI capabilities in detecting bone metastases and inflammatory conditions, with nuclear medicine applications showing particular promise in MSK infection diagnosis. Ophthalmology and musculoskeletal segments, though smaller, employ multimodal retinal imaging and PET/MRI for inflammatory joint disease, respectively, illustrating diverse demand pockets that enrich the multimodal imaging market.

By End-User: Hospitals Anchor Demand While Imaging-Centre Networks Scale

Hospitals captured 71.43% of the multimodal imaging market share in 2025 thanks to integrated oncology and cardiology service lines that rely on in-house hybrid scanners for procedural planning and follow-up. The multimodal imaging market size within hospitals is expected to grow in the coming years as tertiary centres upgrade to total-body PET. These centers leverage focused expertise and streamlined operations to deliver cost-effective imaging services while maintaining quality standards comparable to hospital-based facilities.

Diagnostic imaging centres post a 6.05% CAGR, propelled by outpatient shift and payer preference for cost-efficient venues. Franchise models that deploy portable PET/CT and helium-free MRI broaden geographic reach, increasing scanner utilisation. Research institutions and ambulatory surgery centres contribute niche demand driven by clinical trials and intra-operative guidance, respectively, further diversifying the multimodal imaging market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America’s multimodal imaging market size reached USD 1.74 billion in 2025, equivalent to 39.72% global share, reflecting comprehensive insurance coverage and rapid AI workflow integration. Concentrated expertise at academic medical centres accelerates technology diffusion, while cross-border collaborations enhance Canadian capacity. Mexico’s private hospitals seize market openings generated by medical tourism, adding incremental demand for hybrid scanners.

Asia-Pacific posts the highest CAGR at 6.47%. China funds large-scale oncology and cardiology programmes that mandate PET/CT inclusion, whereas Japan upgrades ageing scanners to maintain diagnostic excellence for an elderly population. India’s private networks install digital PET/CT and 1.5T helium-free MRI in tier-1 cities, widening access. Australia and South Korea adopt cutting-edge platforms comparable to Western peers, reinforcing regional momentum.

Europe maintains a mature yet expanding base, with Germany spearheading innovation through local manufacturing and R&D. Unified valuation frameworks under the European Health Technology Assessment Regulation streamline procurement, underpinning continued adoption. Southern European nations deploy EU-funded tele-imaging initiatives that link rural clinics to urban centres, integrating portable PET/CT to extend reach. Collectively these dynamics keep Europe’s multimodal imaging market on a stable growth.

Competitive Landscape

Market Concentration

Three global conglomerates—GE Healthcare, Siemens Healthineers, and Philips—command the core hardware share, using scale to bundle scanners, informatics, and service. Each embeds AI toolkits such as Siemens’ AIDAN or Philips’ SmartSpeed to reduce exam times and automate triage, strengthening client lock-in. Capital-leasing models and usage-based financing mellow upfront-cost barriers, sustaining renewal cycles across the multimodal imaging market.

White-space entrants thrive by specialising. Positrigo secured FDA clearance for NeuroLF, a table-top brain PET scanner that targets neurology practices.[3]Source: Archana Rani, “FDA approves Positrigo's NeuroLF brain PET system,” MEDICALDEVICE-NETWORK.COM Cubresa advances pre-clinical PET/MR inserts for translational research, while Canon Medical promotes mobile DRFi hybrids to rural health providers. Software innovators layer decision-support algorithms over vendor-neutral archives, creating ecosystems that elevate the multimodal imaging market’s service dimension.

Strategic alliances intensify. Philips joined forces with NVIDIA to train MR foundation models, Siemens partnered with AWS for cloud-native reconstruction, and GE collaborates with Mayo Clinic to co-develop theranostic workflows. Such moves emphasise that future differentiation hinges on data analytics and workflow orchestration rather than scanner hardware alone. As a result, sustained R&D investment and collaboration will dictate competitive longevity within the multimodal imaging market.

Multimodal Imaging Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: RUHX launched a campaign to fund new PET/CT technology for the Royal United Hospitals Bath.

- March 2025: Under IAEA Rays of Hope, Al-Bashir Hospital (Jordan) installed PET-CT through a US-Jordan cost-sharing agreement, broadening access to nuclear medicine.

- May 2025: Mahajan Imaging unveiled North India’s first 128-slice digital PET-CT Omni Legend by GE Healthcare, coupled with a modern pathology lab.

Table of Contents for Multimodal Imaging Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing Prevalence of Chronic Diseases

- 4.2.2Technological Advancements in Hybrid Modalities

- 4.2.3Rising Demand for Early Cancer Diagnosis

- 4.2.4Increasing PET/CT Use in Cardiology Workflows

- 4.2.5Theranostic Radiopharmaceutical Expansion

- 4.2.6Portable Multimodal Systems for Remote Care

- 4.3Market Restraints

- 4.3.1High Capital and Maintenance Costs

- 4.3.2Inadequate Imaging Infrastructure (Emerging Markets)

- 4.3.3Medical-Isotope Supply-Chain Vulnerabilities

- 4.3.4Interoperability & Data-Integration Hurdles

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Technology

- 5.1.1PET/CT Systems

- 5.1.2SPECT/CT Systems

- 5.1.3PET/MR Systems

- 5.1.4Others (e.g., US/CT)

- 5.2By Application

- 5.2.1Oncology

- 5.2.2Cardiology

- 5.2.3Neurology

- 5.2.4Ophthalmology

- 5.2.5Musculoskeletal Disorders

- 5.2.6Others

- 5.3By End-User

- 5.3.1Hospitals

- 5.3.2Diagnostic Imaging Centers

- 5.3.3Others

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East and Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East and Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1GE Healthcare

- 6.3.2Siemens Healthineers

- 6.3.3Koninklijke Philips N.V.

- 6.3.4Canon Medical Systems Corp.

- 6.3.5United Imaging Healthcare

- 6.3.6Mediso Ltd.

- 6.3.7Neusoft Medical Systems Co. Ltd.

- 6.3.8Spectrum Dynamics Medical

- 6.3.9MILabs B.V.

- 6.3.10Bruker Corporation

- 6.3.11Cubresa Inc.

- 6.3.12Digirad Corporation

- 6.3.13Positron Corp.

- 6.3.14Shimadzu Corp.

- 6.3.15Carestream Health

- 6.3.16SurgicEye GmbH

- 6.3.17Agfa-Gevaert Group

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Multimodal Imaging Market Report Scope

As per the scope of the report, multimodal imaging systems describe to concurrent production of signals from more than one imaging technique. Multimodal imaging facilitates analyzing more than one molecule at a time so that cellular processes can be analyzed at the same time or the progression of these events can be monitored in present.