Mobile Medical Imaging Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

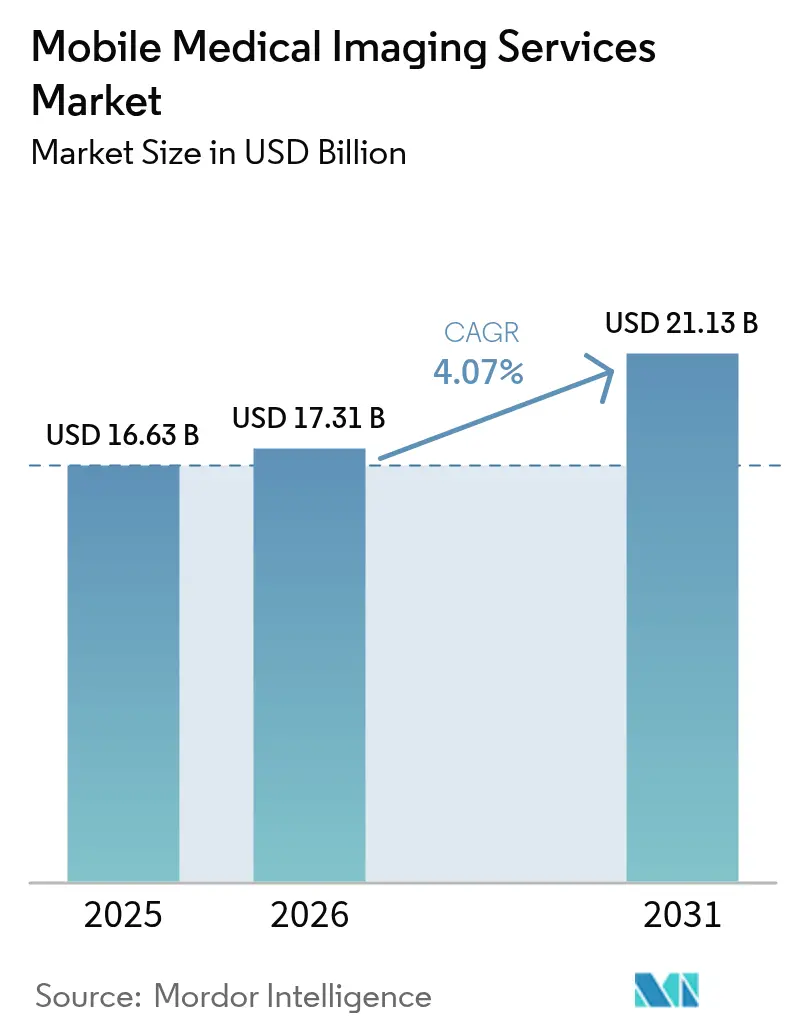

| Market Size (2026) | USD 17.31 Billion |

| Market Size (2031) | USD 21.13 Billion |

| Growth Rate (2026 - 2031) | 4.07% CAGR |

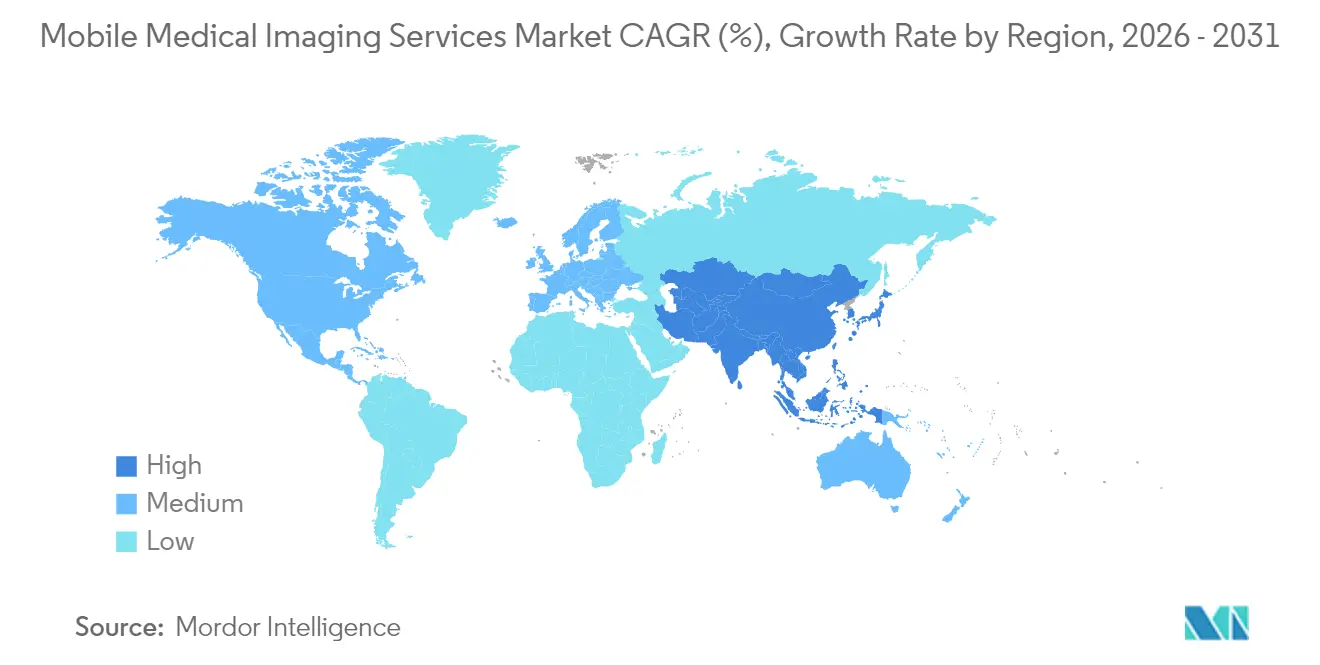

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

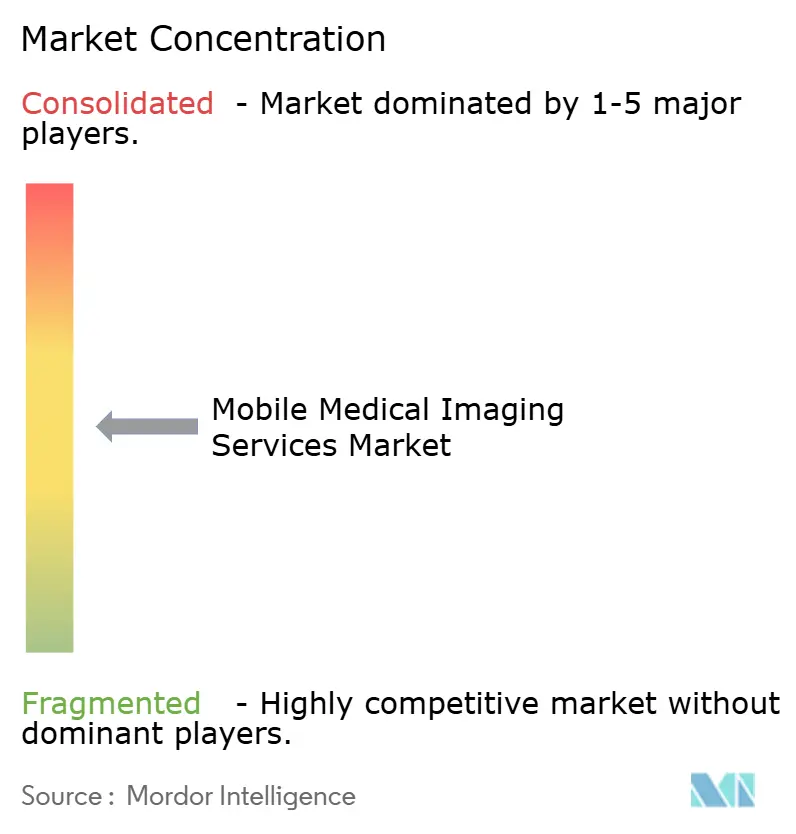

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Medical Imaging Services Market Analysis by Mordor Intelligence

The Mobile Medical Imaging Services market size is expected to grow from USD 16.63 billion in 2025 to USD 17.31 billion in 2026 and is forecast to reach USD 21.13 billion by 2031 at 4.07% CAGR over 2026-2031. Widespread decentralization of care, technological miniaturization and favorable reimbursement reforms keep demand rising, while point-of-care diagnostics continue to displace in-facility scans. Magnetic resonance imaging retains the largest revenue footprint, although positron-emission tomography/CT is expanding quickest as cardiac and oncology procedures migrate to mobile platforms. Provider strategies now integrate bedside scanning into hospital-at-home programs, trimming transport costs and boosting patient adherence. Growth is most pronounced in regions that combine supportive regulation, chronic disease burdens and infrastructure investments, particularly across North America and Asia-Pacific. Ongoing workforce constraints, cyber-security mandates and equipment capital outlays temper overall momentum but have not derailed the broader upward trajectory of the mobile medical imaging services market.

Key Report Takeaways

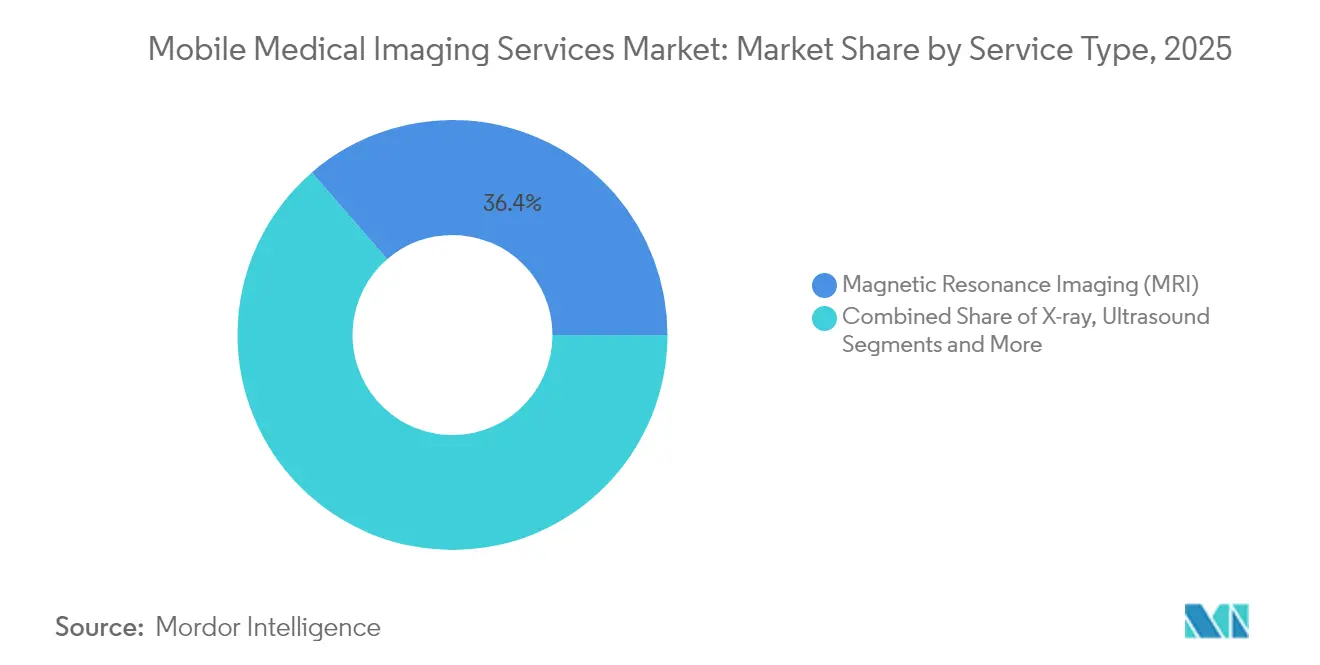

- By service type, magnetic resonance imaging led with 36.35% of mobile medical imaging services market share in 2025, while PET/CT is projected to grow at a 5.61% CAGR to 2031.

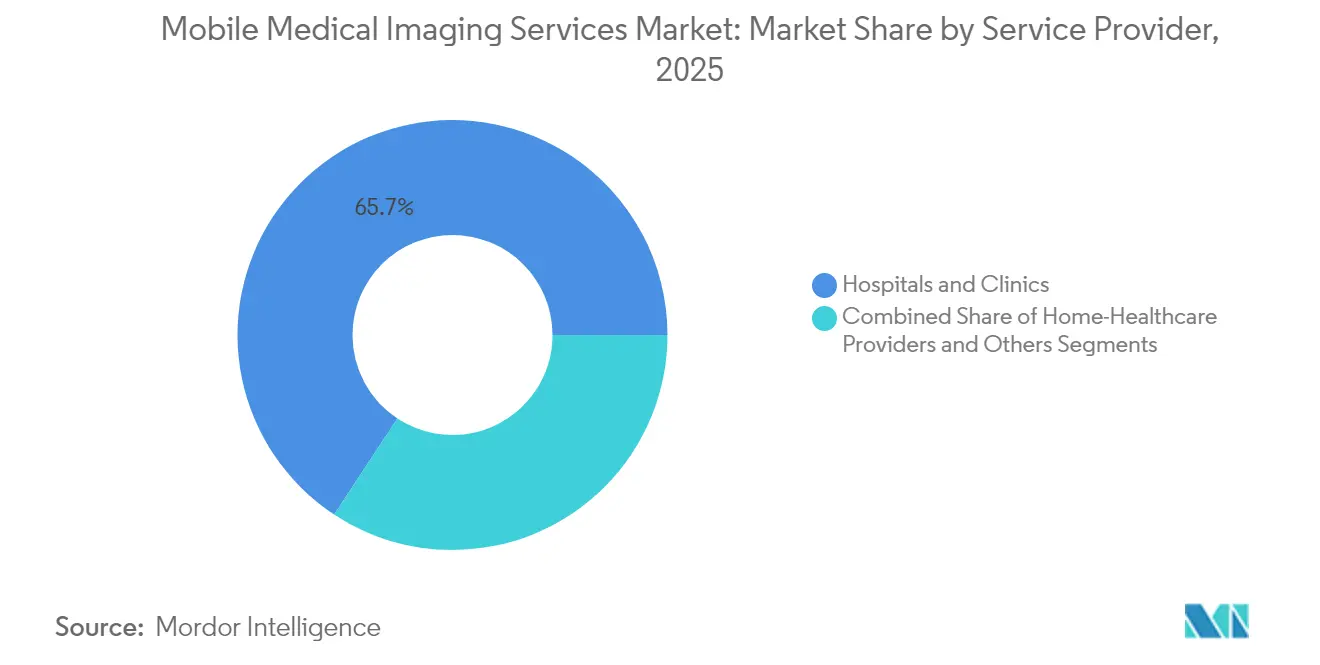

- By service provider, hospitals and clinics held 65.72% of revenue in 2025; home-healthcare providers are advancing at a 5.55% CAGR through 2031.

- By geography, North America captured 40.18% of revenue in 2025, while Asia-Pacific is growing the fastest at a 5.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mobile Medical Imaging Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in Demand for Portable Imaging Technology and Services | +1.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Growing Burden of Chronic Diseases | +0.8% | Global, particularly pronounced in APAC and North America | Long term (≥ 4 years) |

| Technological Advancements | +1.0% | North America & EU leading, APAC following | Short term (≤ 2 years) |

| Expansion of "Hospital-At-Home" Reimbursement Codes | +0.9% | North America, with EU pilot programs | Medium term (2-4 years) |

| Healthcare Infrastructure Expansion | +0.7% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Rising Adoption of Telemedicine and Teleradiology | +0.6% | Global, accelerated in rural and underserved areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise in Demand for Portable Imaging Technology and Services

Portable scanners now reach rural clinics, ambulances and intensive-care units without sacrificing image quality. The 2024 FDA clearance of Positrigo’s NeuroLF brain PET and Hyperfine’s AI-enhanced Swoop MRI confirmed regulatory confidence in ultra-compact formats. Handheld ultrasound platforms such as Exo Iris achieve up to 80% cost savings versus cart-based systems and slip into a clinician’s pocket, fostering everyday use in primary care.[1]Source: Exo, “Iris FDA-Cleared Applications,” explore.exo.inc Providers also note reductions in patient transfer times that cut adverse-event risk during critical care episodes. Point-of-care capabilities shorten diagnostic cycles, improving outcomes for stroke and trauma. Collectively, these shifts enlarge the mobile medical imaging services market by opening settings once considered unreachable.

Growing Burden of Chronic Diseases

Higher incidences of cardiovascular disease, cancer, and diabetes keep scan volumes climbing year after year. PET myocardial perfusion imaging grew 25% between 2018 and 2023, reflecting cardiologists’ preference for on-site assessments that speed intervention. Mobile mammography units targeted at population screening reduce travel burdens for seniors and improve compliance with annual checkups. Frequent imaging of diabetic foot complications through portable ultrasound provides early identification of ischemic tissue, lowering amputation rates. These clinical imperatives reinforce the structural expansion of the mobile medical imaging services market, particularly in aging regions.

Technological Advancements

Artificial-intelligence algorithms embedded inside scanners trim interpretation time by roughly 30%, while photon-counting detectors cut radiation dose and sharpen resolution. Cloud workstations offload processing, allowing vans and carts to remain lightweight and energy-efficient. Miniaturized gradient coils in next-generation MRI units eliminate the need for shielded rooms, letting providers wheel systems into emergency bays. Together, these upgrades raise productivity for radiologists and widen the application spectrum, cementing the competitiveness of early movers in the mobile medical imaging services market.

Expansion of "Hospital-At-Home" Reimbursement Codes

The 2025 Medicare Physician Fee Schedule grants parity for remote supervision of diagnostic procedures, removing long-standing financial deterrents. Private insurers have mirrored the policy, bundling mobile scans into home-care packages. Providers are capitalizing by launching turnkey imaging fleets that accompany nurses and virtual-care teams to patients’ homes. These reimbursements accelerate diffusion of services across suburban and rural counties, reinforcing revenue visibility for stakeholders in the mobile medical imaging services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Mobile Set-Ups and Scanners | -0.8% | Global, particularly impacting smaller providers | Medium term (2-4 years) |

| Radiation-Exposure Compliance Hurdles | -0.5% | Global, with stricter enforcement in EU and North America | Long term (≥ 4 years) |

| Cyber-Security Mandates for Mobile Endpoints | -0.4% | Global, with heightened focus in North America | Short term (≤ 2 years) |

| Shortage of Certified Mobile Technologists | -0.9% | Global, most acute in North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Mobile Set-Ups and Scanners

The substantial capital requirements for mobile imaging equipment create significant barriers to market entry and expansion. Acquiring a mobile PET/CT can cost USD 1.5 million–3 million, while mobile MRI frequently surpasses USD 2 million.[2]Source: Medco Blue, “How Much Does It Cost to Buy a Mobile MRI?,” medcoblue.com Rental fees for CT trailers approach USD 30,000 per month, excluding transport and shielding expenses. Refurbished units offer savings of 20–40% but availability is limited and may lag on AI upgrades. Financial constraints particularly impact rural and underserved markets where mobile imaging services are most needed, but economic viability is most challenging.

Shortage of Certified Mobile Technologists

The acute shortage of qualified imaging technologists severely constrains market growth. Radiologic technologist vacancy rates climbed to 18.1% in 2024 as retirements outpaced graduate inflows. Mobile assignments demand additional skills such as equipment rigging and lone-worker safety, pushing wages 15–25% above in-facility roles. Staffing agencies fill gaps but raise overhead, limiting smaller operators’ geographic reach and restraining capacity growth within the mobile medical imaging services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: MRI Dominance Amid PET/CT Acceleration

Magnetic resonance imaging retained 36.35% of revenue in 2025, underpinned by portable systems that bypass the need for shielded rooms and fixed cryogens. The modality’s versatility across neurology, orthopedics and cardiology cements its commanding role within the mobile medical imaging services market. PET/CT, however, is gaining momentum at a 5.61% CAGR, buoyed by surging cardiac perfusion studies and precision oncology diagnostics. PET scan volumes rose 10.2% year on year in 2023, indicating pent-up demand for real-time metabolic imaging in outpatient settings.

Ultrasound benefits from handheld transducers that cost a fraction of cart-based systems, democratizing access for primary-care physicians. Portable X-ray remains a workhorse in critical-care wards and nursing homes due to its speed and low radiation dose. A niche “Others” cohort—covering photon-counting CT and optical coherence tomography—illustrates the pipeline of next-generation tools set to enlarge the mobile medical imaging services market size for specialized scans over the next decade.

By Service Provider: Hospital Systems Lead While Home Care Accelerates

Hospitals and clinics generated 65.72% of 2025 revenue, translating existing referral streams into bedside imaging capacity. Integrated delivery networks fold mobile fleets into emergency and transplant pathways, capturing economies of scale and simplifying compliance documentation. These incumbents also leverage capital budgets to refresh scanners regularly, maintaining quality benchmarks that reinforce patient trust in the mobile medical imaging services market.

Home-healthcare providers are the fastest-growing cohort, advancing at 5.55% CAGR to 2031 as parity reimbursement legitimizes at-home diagnostics. DispatchHealth and similar players dispatch radiologic technologists alongside nurse practitioners, enabling acute evaluations that previously required ED transfers. A separate “Others” category spans urgent-care franchises, telemedicine hubs and dedicated mobile imaging vendors, each carving micro-niches based on geography or modality specialization. Momentum across these groups illustrates how diversification of provider types propels the broader mobile medical imaging services market.

Geography Analysis

North America retained 40.18% of 2025 revenue on the strength of early FDA clearances, CMS reimbursement innovation and established teleradiology networks. Capital inflows from private equity into imaging chains such as RadNet and RAYUS have reinforced equipment refresh cycles and accelerated fleet acquisitions. Workforce shortages pose headwinds, yet educational pipelines are expanding cohort sizes to moderate future vacancy rates. Overall, the mobile medical imaging services market size in North America is set to increase steadily through 2030 as hospital-at-home pilots transition into mainstream service lines.

Asia-Pacific represents the fastest-growing region at 5.88% CAGR, driven by rising chronic disease prevalence and large-scale infrastructure spending. Governments in China, India and Indonesia are subsidizing modular clinics equipped with point-of-care scanners to bridge urban-rural divides. Technology licensors such as Hyperfine and Positrigo have signed multi-country distribution agreements that shorten adoption lags. Domestic manufacturers are also scaling production of cost-effective ultrasound and X-ray units, fostering competitive pricing that broadens the mobile medical imaging services market across lower-income provinces.

Europe, the Middle East and Africa, and South America display mixed trajectories tied to differing reimbursement climates and currency volatility. European Union adherence to new MDR rules has lengthened product certification cycles but also instilled confidence in device quality. Middle Eastern health-city projects position mobile fleets as interim solutions while permanent facilities rise. Latin American adoption rates hinge on public-private financing partnerships that offset capex barriers. Collectively, these developments echo a global pivot toward decentralized diagnostics that amplifies the footprint of the mobile medical imaging services market.

Competitive Landscape

The field remains moderately fragmented, with regional specialists competing alongside national hospital networks. RadNet’s USD 103 million purchase of breast-AI vendor iCAD illustrates vertical integration that embeds analytics deeper into workflows. GE HealthCare’s acquisition of Intelligent Ultrasound for USD 51 million expands its ultrasound AI portfolio, signaling continued convergence between equipment and software providers.

Strategic alliances focus on cloud and artificial-intelligence enablement. GE HealthCare and Amazon Web Services cooperate on generative-AI imaging tools that promise faster triage and auto-reporting, raising the technology bar for all participants. Private equity is accelerating roll-ups: Affinity Equity Partners’ USD 658 million bid for a diagnostic imaging group reflects demand for scale benefits in procurement and compliance management. These moves consolidate market share but plenty of white space remains for agile entrants, especially in underserved rural pockets where the mobile medical imaging services industry continues to evolve.

Competition increasingly hinges on workforce models and cyber-security credentials. Operators that can recruit certified technologists and maintain zero-breach records win hospital contracts more readily. AI-driven maintenance schedules and remote diagnostics reduce downtime, enhancing utilization rates. Ultimately, differentiation rests on the seamless integration of hardware, software, staffing and reimbursement know-how, themes that will define leadership positions within the mobile medical imaging services market over the next five years.

Mobile Medical Imaging Services Industry Leaders

Akumin Inc (Alliance Healthcare Services)

DMS Health Technologies

Front Range Mobile Imaging

Accurate Imaging Inc

Cobalt Imaging Center

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Hyperfine presented clinical data at the International Stroke Conference confirming 90% diagnostic accuracy for acute ischemic stroke with its portable MRI platform.

- February 2025: TridentCare became the preferred network provider for Southwestern Health Resources, extending mobile imaging access to 790,000 patients across 16 Texas counties.

Global Mobile Medical Imaging Services Market Report Scope

As per the scope of this report, mobile medical imaging serive is a service in which special machines are used to perform imaging procedures on patients that are too sick to travel to a hospital. Mobile imaging provides comprehensive X-Ray, EKG and ultrasound services directly to medical facilities, homes and businesses. Mobile diagnostic imaging devices offer significant benefits to stakeholders by increased efficiency of healthcare services provision, better accessibility to healthcare and faster reaction time combined with their (usually) lower price. The Mobile Imaging Medical Services Market is Segmented By Service Type (X-Ray, PET/CT, Ultrasound, MRI, Others), End User (Hospitals and Private Clinics, Home Healthcare Service Providers, Others (Rehabilitation Centers, Geriatric Care, and Hospice Agencies) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| X-ray |

| Ultrasound |

| Magnetic Resonance Imaging (MRI) |

| PET/CT |

| Others |

| Hospitals and Clinics |

| Home-Healthcare Providers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | X-ray | |

| Ultrasound | ||

| Magnetic Resonance Imaging (MRI) | ||

| PET/CT | ||

| Others | ||

| By Service Provider | Hospitals and Clinics | |

| Home-Healthcare Providers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast CAGR for the mobile medical imaging services market to 2031?

The market is expected to expand at a 4.07% CAGR between 2026 and 2031.

Which service type currently commands the largest revenue share?

Magnetic resonance imaging leads with 36.35% of revenue in 2025.

Why is PET/CT the fastest-growing modality?

Growth is propelled by increasing demand for cardiac perfusion and oncology imaging, translating into a 5.61% CAGR through 2031.

How are reimbursement reforms influencing adoption?

Medicare parity for remote diagnostics and private-payer alignment enable providers to deploy mobile fleets without revenue penalties, accelerating uptake across home-healthcare settings.

What is the main operational challenge for providers?

A shortage of certified technologists, with vacancy rates exceeding 18%, is the principal bottleneck, raising labor costs and limiting fleet expansion.

Which region offers the highest growth potential?

Asia-Pacific is projected to achieve the fastest regional growth at a 5.88% CAGR, driven by healthcare infrastructure expansion and an aging population.

Page last updated on: