Medical Imaging Phantoms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

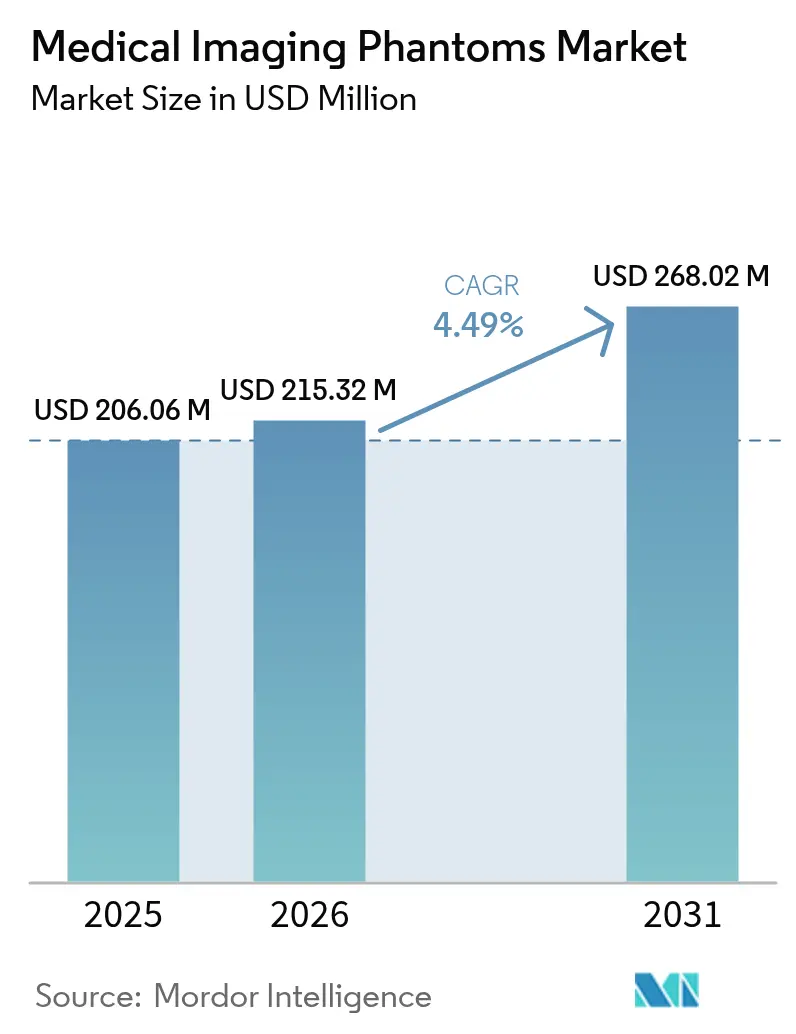

| Market Size (2026) | USD 215.32 Million |

| Market Size (2031) | USD 268.02 Million |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

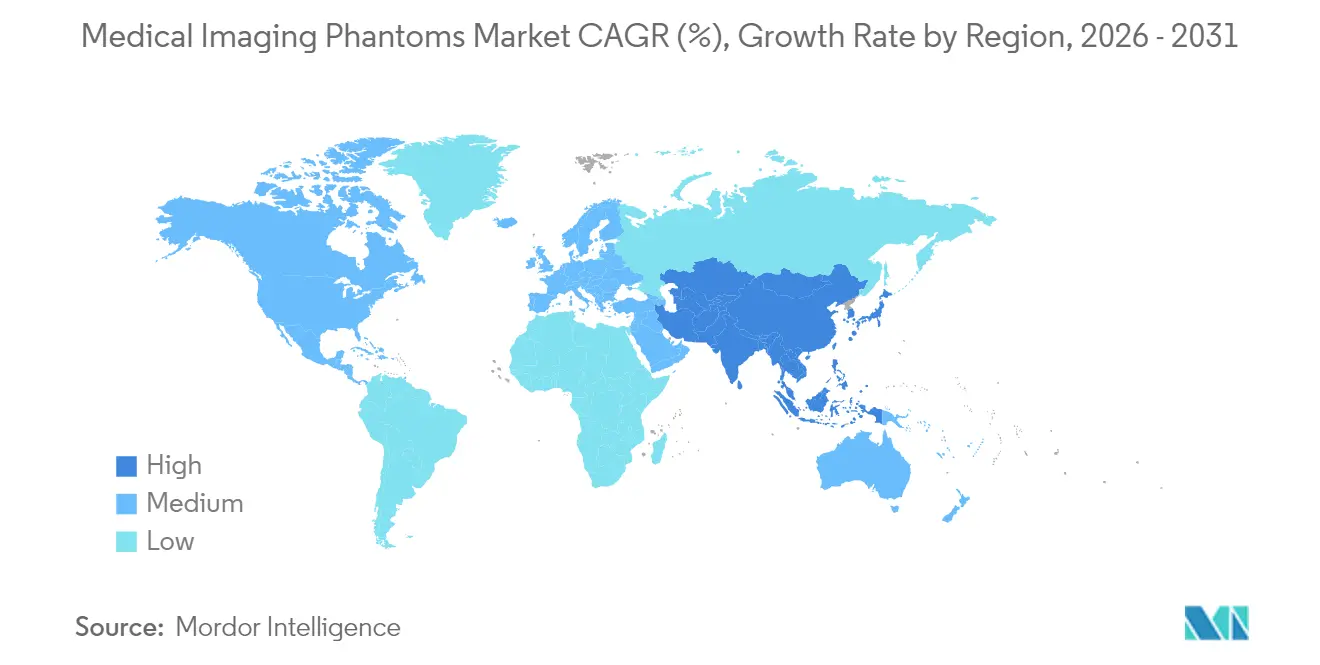

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

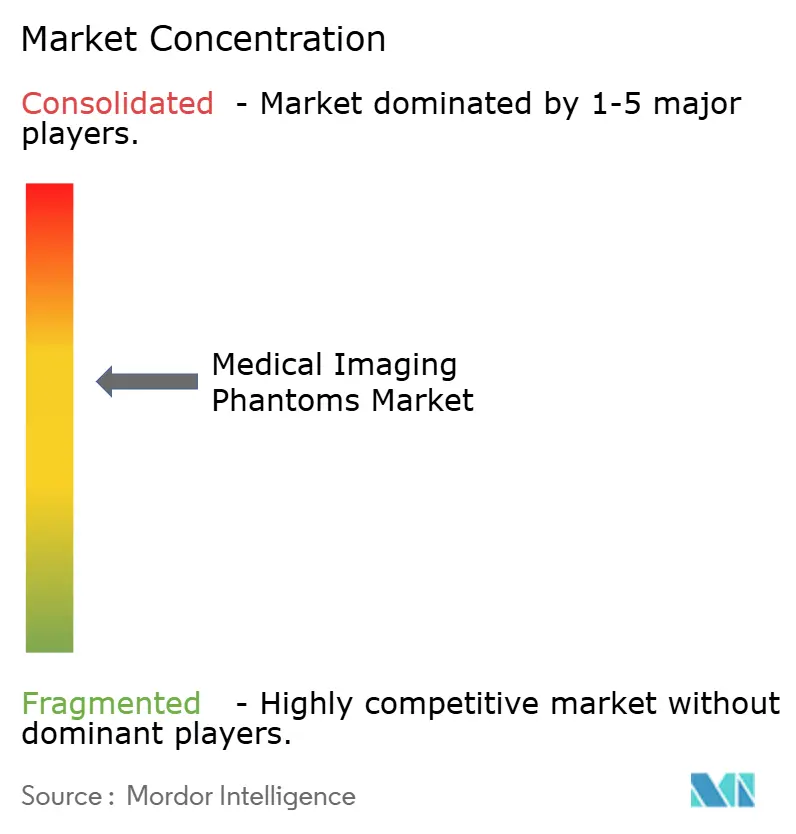

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Imaging Phantoms Market Analysis by Mordor Intelligence

The Medical Imaging Phantoms market size is expected to grow from USD 206.06 million in 2025 to USD 215.32 million in 2026 and is forecast to reach USD 268.02 million by 2031 at 4.49% CAGR over 2026-2031. Growing accreditation requirements that link reimbursement to documented image quality keep procurement budgets stable, while 3D printing and smart polymers expand the technical reach of manufacturers. Hospitals still account for most purchases, yet quality-focused ambulatory imaging providers are quickly scaling orders as value-based care shifts volumes away from inpatient settings. Rapid adoption of AI-enabled auto-QA software shortens test cycles and encourages more frequent phantom checks, raising replacement rates. Material innovation that spans CT, MRI, and ultrasound in a single object cuts inventory costs for radiology departments, spurring multimodality phantom demand. Supply-chain tightness for elastography-grade polymers and radioactive gels continues to push lead times higher, but 3D-printed alternatives partly offset the gap.

Key Report Takeaways

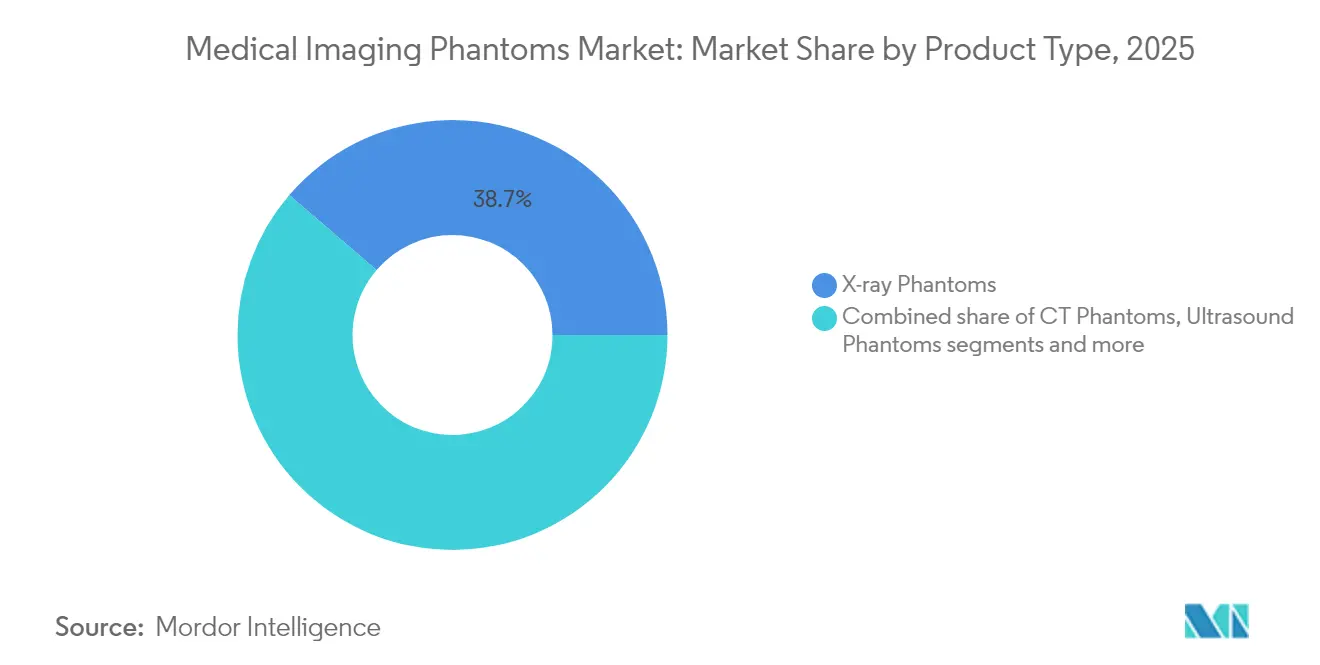

- By product type, X-ray phantoms led with 38.72% of the medical imaging phantoms market share in 2025, while CT phantoms are advancing at a 6.14% CAGR through 2031.

- By material, stimulating devices accounted for 56.14% of the medical imaging phantoms market size in 2025; false organs (anthropomorphic) phantoms post the fastest growth at 5.17% CAGR.

- By end user, hospitals captured 53.62% revenue share in 2025, whereas diagnostic imaging centers are expanding at a 5.86% CAGR to 2031.

- By geography, North America dominated with 36.74% of the medical imaging phantoms market share in 2025; Asia Pacific records the highest projected CAGR at 6.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Imaging Phantoms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating QA-stringency of value-based reimbursement programs | +1.2% | North America & EU | Medium term (2-4 years) |

| Surging adoption of 3-D printed, modality-agnostic phantoms | +0.8% | Global | Long term (≥ 4 years) |

| Rising installation of hybrid PET/CT & PET/MR scanners | +0.6% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Expanding radiology capacity in ambulatory imaging centers | +0.5% | North America & APAC | Short term (≤ 2 years) |

| AI-enabled auto-QA workflows cutting test-cycle time | +0.4% | Global | Long term (≥ 4 years) |

| Growing grant funding for photo-acoustic tomography validation | +0.3% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating QA-Stringency of Value-Based Reimbursement Programs

Mandatory CT phantom assessments that the Centers for Medicare & Medicaid Services will enforce from 2027 convert test objects from best-practice accessories into core compliance tools. The American College of Radiology ARCH-AI framework further embeds standardized phantom runs into AI validation workflows, tying algorithm reliability to phantom-verified metrics. Health systems now regard phantom purchases as revenue-protection spend, not discretionary outlays, anchoring the medical imaging phantoms market. Quality-based bonus pools in Medicare Advantage plans intensify uptake by rewarding documented imaging consistency.

Surging Adoption of 3-D Printed, Modality-Agnostic Phantoms

Additive manufacturing delivers patient-specific replicas within 0.1 mm geometric tolerance, while new PLA-PCL blends maintain CT, MRI, and ultrasound contrast in a single build.[1]Source: 3D Printing in Medicine, “Patient-Specific Implants Made of 3D Printed Bioresorbable Polymers at the Point-of-Care: Material, Technology, and Scope of Surgical Application,” threedmedprint.biomedcentral.com NIH support for an Industry-University Cooperative Research Center focused on optical imaging phantoms signals sustained federal backing. Production of complex anthropomorphic units now costs under USD 250 and finishes in days instead of months.[2]Source: Pharmaceuticals, “3D-Printed Organ-Realistic Phantoms to Verify Quantitative SPECT/CT Accuracy for 177Lu-PSMA-617 Treatment Planning,” mdpi.com Hybrid PET/MR and photoacoustic systems that need multi-energy calibration spur developers to design modality-agnostic phantoms, broadening the global medical imaging phantoms market footprint. The lower entry price of desktop stereolithography printers also empowers mid-tier radiology groups to fabricate on-site, shortening procurement cycles.

Rising Installation of Hybrid PET/CT & PET/MR Scanners

Asia Pacific hospital networks accelerate rollouts of PET/CT and PET/MR units in oncology and cardiology suites, increasing cross-calibration complexity. These integrated scanners require phantoms that align radiotracer distribution and MR signal uniformity within 2 mm spatial error across the full field of view.[3]Source: Journal of Nuclear Medicine, “Performance Characteristics of the NeuroEXPLORER, a Next-Generation Human Brain PET/CT Imager,” snmjournals.org Suppliers that combine low-attenuation plastics with MR-compatible shielding capture premium pricing. Regulators now reference phantoms in acceptance testing protocols for hybrid systems, making them a prerequisite for modality commissioning. The trend widens margins in the medical imaging phantoms market because hybrid systems carry larger service contracts that bundle QA consumables.

AI-Enabled Auto-QA Workflows Cutting Test-Cycle Time

Machine-vision algorithms now locate phantom markers and compute distortion metrics with sub-millimeter accuracy, reducing physicist review from hours to minutes. Continuous QA embedded in scanner firmware turns each patient scan into a quality check, lifting phantom wear rates and boosting reorder frequency. Early adopters report 40% fewer emergency maintenance calls because predictive analytics flag gradual performance drift. As AI becomes a standard feature, next-generation phantoms will ship with encrypted reference datasets that sync to AI dashboards, ensuring lock-step hardware-software validation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-intensive custom phantom prototyping | -0.7% | Global | Medium term (2-4 years) |

| Scarcity of elastography-grade tissue-mimicking polymers | -0.5% | Global | Long term (≥ 4 years) |

| Limited physicist bandwidth for advanced QA protocols | -0.4% | North America & EU | Short term (≤ 2 years) |

| Supply-chain volatility for high-purity radioactive gels | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Custom Phantom Prototyping

Developing a patient-specific anthropomorphic phantom can exceed USD 50,000 due to imaging, segmentation, multi-material printing, and validation costs.[4]Source: EJNMMI Physics, “Optimising Total Knee Replacement Imaging: A Novel 3D-Printed PET/CT Anthropomorphic Phantom for Metal Artefact Simulation,” springeropen.com Small suppliers find it difficult to recoup expenses in niche modalities, leading to consolidation and slower innovation. Academic teams often improvise do-it-yourself kits that vary in performance, undermining cross-site comparability. This capital barrier curbs the medical imaging phantoms market expansion in subspecialty domains.

Scarcity of Elastography-Grade Tissue-Mimicking Polymers

Replicating tissue stiffness from 1–200 kPa demands custom polymer blends, yet only a few vendors supply consistent batches at medical-grade purity. Disruptions in precursor chemicals compel manufacturers to stockpile, tying up working capital and extending delivery times. Research labs experiment with homemade silicones, but these variants often lack stable acoustic attenuation, limiting clinical acceptance. Growth in ultrasound and MR elastography therefore outpaces phantom availability, creating a drag on market volume.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: X-ray Phantoms Lead Despite CT Growth Acceleration

X-ray phantoms held 38.72% of the medical imaging phantoms market in 2025, a testament to mammography regulations that mandate routine test object scanning. Demand remains stable because the global installed base of digital radiography rooms vastly exceeds that of other modalities. The CT segment is picking up at a 6.14% CAGR as new dose-monitoring rules take effect, reflecting how evolving regulatory frameworks continuously reshape the medical imaging phantoms market size for slice-based imaging.

Manufacturers innovate with combination phantoms that house X-ray and CT inserts in one shell, lowering inventory requirements for smaller clinics. Ultrasound phantom makers focus on elastography features to match clinical expansion into liver, thyroid, and musculoskeletal assessments. MRI phantom demand remains uneven as helium supply challenges stall scanner installations, although quantitative imaging biomarkers spur interest in diffusion and T1/T2 calibration sets. Nuclear medicine phantoms chart steady orders tied to theranostic growth, where precise dosimetry becomes standard of care.

By Material: Stimulating Devices Dominate While Anthropomorphic Solutions Accelerate

Stimulating devices commanded 56.14% medical imaging phantoms market share in 2025 because they satisfy daily QA checklists with simple geometric targets that are easy to position and interpret. These phantoms are cost-effective and durable, which appeals to high-volume centers. Anthropomorphic solutions, buoyed by rapid 3D printing advances, are expanding at 5.17% CAGR as surgeons and interventional radiologists require lifelike simulations.

Hybrid filament formulations now blend PLA with soft thermoplastic elastomers, creating dual-durometer parts that mimic bone and soft tissue in a single print run. Academic-industry consortia fast-track standard test protocols so data collected with new materials remains comparable across sites. Niche materials such as graphite-doped silicones for photoacoustic imaging are entering pilot production, widening choice but adding qualification burdens for quality managers.

By End User: Hospitals Maintain Leadership as Diagnostic Centers Surge

Hospitals captured 53.62% of the medical imaging phantoms market size in 2025, owing to wide modality mix and in-house physicist teams that execute weekly QA routines. Their equipment breadth—from fluoroscopy to PET/CT—necessitates broad phantom inventories. Diagnostic imaging centers are growing at 5.86% CAGR because payers steer non-acute exams to lower-cost settings, and such facilities adopt phantoms early to secure ACR accreditation needed for payer contracts.

Bundled service models, where phantom providers include cloud analytics and periodic calibration, appeal to outpatient chains that prefer predictable operating costs. Research institutes and original-equipment manufacturers comprise a smaller slice yet drive high-spec orders, such as deep-brain stimulation MRI phantoms for device compatibility tests.

Geography Analysis

North America dominated with 36.74% of the medical imaging phantoms market in 2025, reflecting stringent FDA equipment performance rules and a dense imaging center network that completes frequent QA cycles. Hospitals invest in AI-linked phantoms to align with the ARCH-AI program, anchoring replacement demand. Government quality incentives compensate for higher labor costs, preserving healthy margins for suppliers.

Asia Pacific is the fastest-growing region at a 6.05% CAGR, supported by large-scale hospital build-outs and the transition of provincial centers to digital imaging. China funds hybrid PET/MR rollouts that need complex multimodality phantoms, while India’s National Accreditation Board for Testing mandates documented QA before licensure. Local manufacturing clusters in Shenzhen and Osaka lower import duties, yet premium inserts still rely on U.S. and European sources, sustaining international trade flows in the medical imaging phantoms market.

Europe posts steady gains as the Medical Device Regulation enforces traceability for QA accessories. Germany and the United Kingdom lead R&D partnerships that develop bio-resorbable phantom materials, while Scandinavian clinics pioneer remote phantom monitoring linked to centralized physics hubs. Middle East and Africa register emerging demand as Gulf hospitals position themselves as regional medical tourism centers, raising imaging quality benchmarks. South America grows more slowly due to fiscal constraints, although niche orders rise in Brazil’s private oncology sector.

Competitive Landscape

The market shows moderate fragmentation. Incumbents like CIRS, PTW Freiburg, Biodex Medical Systems, and Kyoto Kagaku specialize in discrete niches. Players differentiate through proprietary materials, software integration, and regulatory track record. Computerized phantoms bundled with AI analytics allow firms to command service premiums.

3D printing opens entry points for agile startups that deliver patient-specific products within 72 hours. Consolidation surfaces when radiation-therapy QA specialists acquire niche phantom assets to round out portfolios. Pricing pressure remains manageable because regulatory complexity and validation costs create natural moats, yet suppliers must invest continually in material science and software or face commoditization.

Supply-chain resilience becomes a differentiator. Companies securing elastography polymers through multi-year contracts or developing silicone alternatives avoid production delays that hurt smaller rivals. Strategic bottlenecks in radioactive gel sourcing prompt some vendors to pivot toward non-radioactive surrogates, positioning them for nuclear pharmacy shortages. Overall, competition favors firms that combine materials innovation, regulatory savvy, and data-centric software.

Medical Imaging Phantoms Industry Leaders

Gold Standard Phantoms

Biodex Medical Systems

Computerized Imaging Reference Systems (CIRS)

PTW Freiburg

Kyoto Kagaku

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Stratasys and Siemens Healthineers introduce patient-specific 3D-printed phantoms aimed at rapid CT algorithm development and precision imaging.

- December 2024: MedScan3D debuts a cross-modal phantom series with acoustical and mechanical realism for ultrasound, CT, and MRI validation.

- July 2024: RSD Radiology Support Devices previews multimodality phantoms designed for CT, MRI, and X-ray accreditation workflows.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the medical imaging phantom market as all synthetic objects that mimic specific tissue and organ properties across X-ray, CT, MRI, ultrasound, and nuclear imaging systems, and that are sold for routine calibration, quality assurance, training, or basic research.

Scope exclusion: Phantoms designed exclusively for high-energy radiotherapy dose verification are outside this scope.

Segmentation Overview

- By Product Type

- X-ray Phantoms

- CT Phantoms

- Ultrasound Phantoms

- MRI Phantoms

- Nuclear Imaging Phantoms

- Others

- By Material

- Stimulating Devices

- False Organs (Anthropomorphic)

- Other Materials

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed medical physicists, radiology QA supervisors, and phantom product managers across North America, Europe, and Asia Pacific to verify replacement cycles, typical stocking patterns, and recent price shifts. Follow-up surveys with diagnostic imaging centers helped us reconcile regional variations that secondary data alone could not clarify.

Desk Research

We began with open data sets from entities such as the US FDA 510(k) database, WHO Global Health Observatory, OECD Health Statistics, and the International Atomic Energy Agency diagnostic imaging registry, which offer baseline volumes of installed scanners and QA mandates. Trade association literature from the Radiological Society of North America and the American Association of Physicists in Medicine supplies modality-specific QA frequency norms, while patent analytics from Questel and company filings housed on D&B Hoovers illuminate material cost trends and supplier revenues. Additional insights come from peer-reviewed journals that test novel tissue-mimicking polymers and from the NIH 3D Print Exchange illustrating the adoption of printable phantoms. This list is illustrative; many other public and proprietary sources were consulted for gap filling and cross checks.

Market-Sizing & Forecasting

A top-down model starts with the global installed base of imaging systems by modality, multiplies it by recommended phantom usage per QA cycle, and adjusts for replacement life to estimate annual demand. Select bottom-up tests, such as rolling up shipment data from leading suppliers and checking sampled average selling prices, calibrate and fine-tune totals. Key variables in the model include new scanner installations, QA protocol frequency, modality mix shifts toward hybrid PET/CT, average phantom service life, and polymer cost inflation. Multivariate regression, supported by expert consensus on each driver, projects the market to 2030; scenario analysis captures rapid uptake of 3-D printed anthropomorphic models. When bottom-up evidence is thin for a region, proxy indicators like radiology procedure growth are applied with conservative load factors.

Data Validation & Update Cycle

Each draft output passes anomaly checks, variance reviews, and senior analyst sign-off before publication. The dataset refreshes annually, and interim updates are triggered by material events such as a new FDA QA guideline or a step change in scanner installations. A final live check is run just before release so clients receive the freshest viewpoint.

Why Our Medical Imaging Phantom Baseline Earns High Trust

Published values frequently diverge because firms select different product mixes, price ladders, and update cadences.

Key gap drivers include whether radiotherapy phantoms are counted, how aggressively 3-D printed units are forecast, and the currency conversion approach. Mordor reports only diagnostic phantoms, applies a weighted price curve validated with hospital buyers, and refreshes every twelve months, which limits drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 206.06 million (2025) | Mordor Intelligence | - |

| USD 181.5 million (2024) | Global Consultancy A | Focuses on CT only and projects a uniform 4% growth, undervaluing hybrid PET/MR demand |

| USD 190 million (2024) | Trade Journal B | Bundles radiotherapy dose phantoms and incorporates service contract revenue, inflating totals |

These comparisons show that when scope alignment and variable selection are not transparent, market values swing widely. By grounding estimates in scanner counts, QA practice norms, and price evidence reviewed with users, Mordor Intelligence delivers a balanced, reproducible baseline clients can depend on.

Key Questions Answered in the Report

Why are 3D-printed phantoms increasingly preferred over conventional models?

They can be produced in-house within days, closely replicate patient anatomy, and work across CT, MRI, and ultrasound, which improves quality checks and operator training while lowering logistics hurdles.

How is artificial intelligence changing phantom-based quality assurance?

AI software now automates image analysis of phantom scans, detecting subtle distortions in seconds and freeing physicists to focus on more complex performance issues.

What role do multi-modal phantoms play in the adoption of hybrid PET/CT and PET/MR scanners?

These phantoms validate spatial alignment and contrast consistency across integrated modalities, helping facilities maintain accreditation as hybrid imaging expands.

Why are outpatient imaging centers investing heavily in phantom testing?

Value-based reimbursement ties payment to documented image quality, so ambulatory facilities rely on routine phantom scans to secure favorable payer contracts.

Which supply-chain challenges most impact phantom availability?

Limited sources for elastography-grade polymers and high-purity radioactive gels can extend lead times and push manufacturers to explore alternative materials.

How do anthropomorphic phantoms enhance clinician training?

Their lifelike textures and anatomically accurate structures allow radiologists and surgeons to practice complex procedures in a controlled environment, reducing learning curves and improving patient safety.

Page last updated on: