Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.67 Billion |

| Market Size (2026) | USD 7.90 Billion |

| Market Size (2031) | USD 9.17 Billion |

| Growth Rate (2026 - 2031) | 3.03% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Wine Market Analysis by Mordor Intelligence

The South America wine market was valued at USD 7.67 billion in 2025 and is expected to reach USD 7.90 billion in 2026, with projections indicating it will grow to USD 9.17 billion by 2031, registering a CAGR of 3.03% during the forecast period. Key factors driving this growth include increasing premiumization, an expanding export footprint supported by tariff-reducing trade agreements, and rising female participation in wine consumption. Currency depreciation in Argentina and Chile has enhanced export competitiveness, although adverse weather conditions and water scarcity pose operational risks for growers. To address these challenges, producers are investing in water-efficient drip irrigation systems, direct-to-consumer sales channels, and wine-route tourism to mitigate the impact of rising input costs. Additionally, sparkling wine and rosé styles are emerging as faster-growing segments, reflecting global premium-occasion trends that have reached South America later than Europe or North America.

Key Report Takeaways

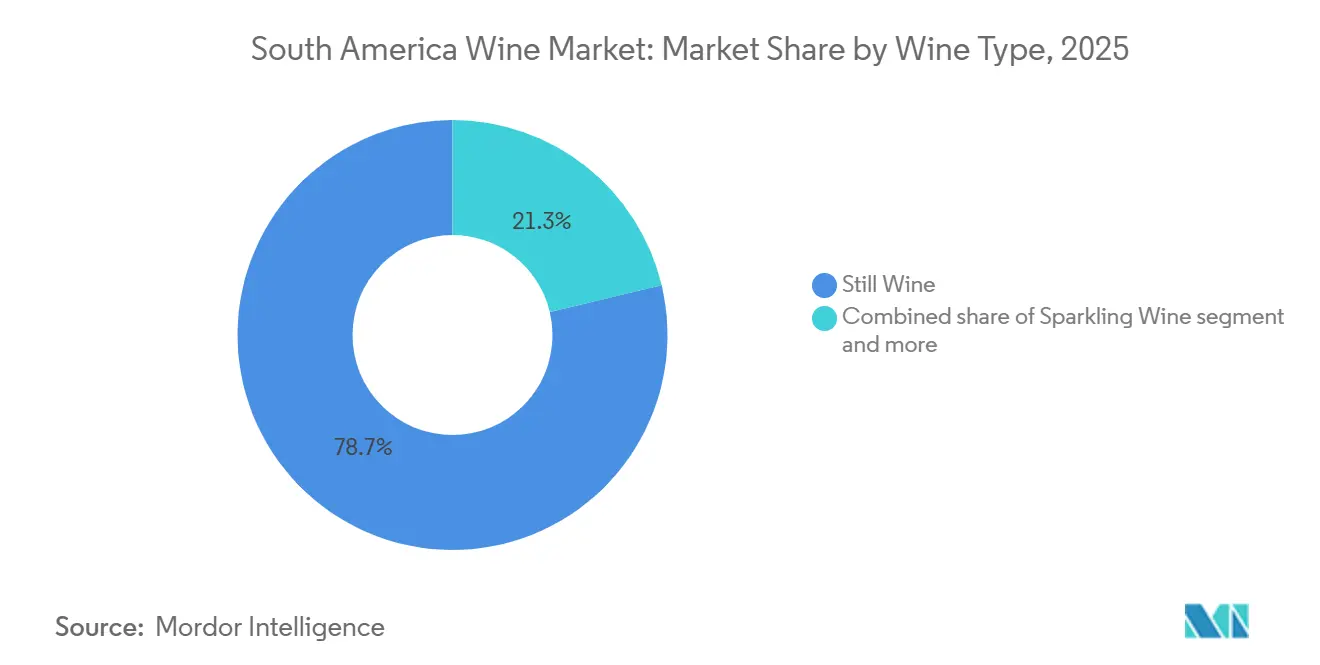

- By wine type, still wine led with 78.71% of the South America wine market share in 2025, while sparkling wine is forecast to post the fastest 3.95% CAGR through 2031.

- By color, red wine accounted for 56.10% share of the South America wine market size in 2025; rosé is on track for a 5.09% CAGR between 2026 and 2031.

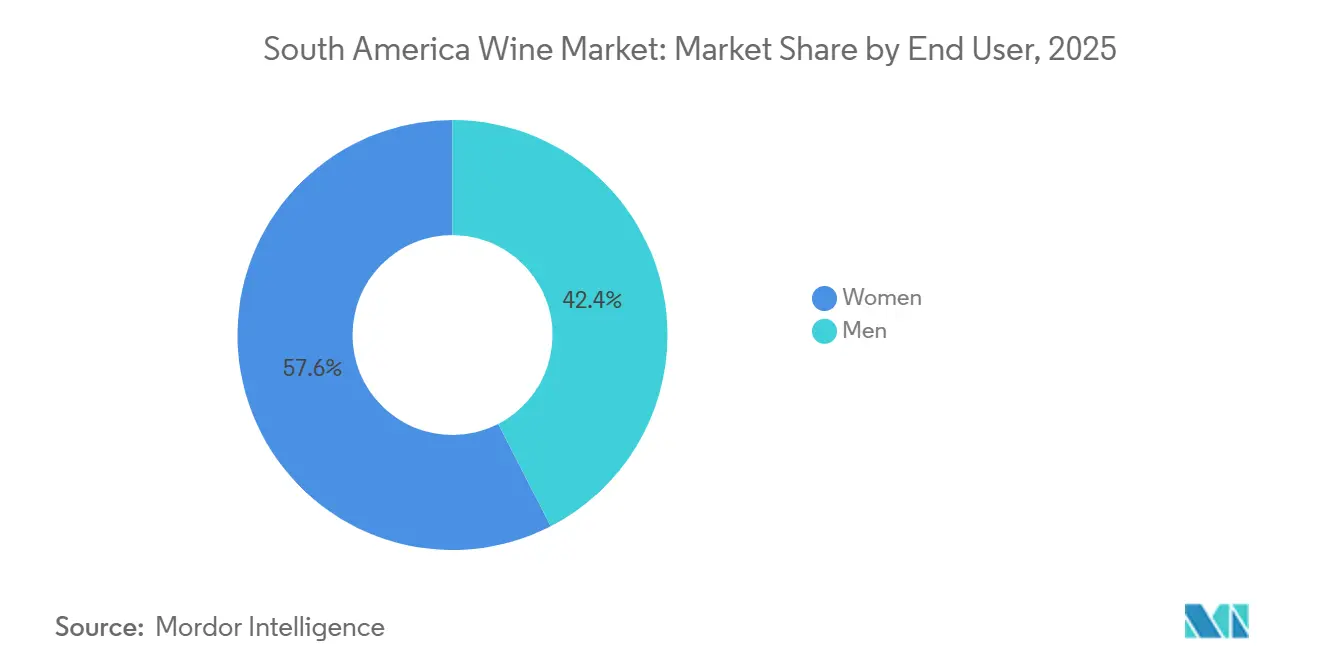

- By end user, women represented 57.56% of volume in 2025, and the men segment is projected to expand at a 3.89% CAGR to 2031.

- By distribution channel, off-trade captured a 70.38% share in 2025, yet on-trade is set to rebound at a 4.45% CAGR through 2031.

- By geography, Argentina held 39.95% of regional revenue in 2025, whereas Colombia is anticipated to deliver the quickest 4.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Wine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing domestic tourism and wine-route programs | +0.6% | Argentina, Chile, Brazil | Medium term (2-4 years) |

| Growing interest in premium and boutique wines | +0.8% | Argentina, Chile, Brazil, Colombia | Long term (≥ 4 years) |

| Adoption of sustainable and organic wines | +0.5% | Chile, Argentina, Brazil | Long term (≥ 4 years) |

| Ethical packaging and convenience formats | +0.3% | Brazil, Chile | Short term (≤ 2 years) |

| Rise of export-oriented free-trade deals | +0.7% | Argentina, Brazil, Uruguay, Paraguay, Chile | Medium term (2-4 years) |

| Influence of social media and wine influencers | +0.4% | Urban centers across South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing domestic tourism and wine-route programmes

Wine tourism is increasingly being utilized as a strategy by producers to mitigate the impact of rising climate-related costs and currency fluctuations. In 2024, Mendoza welcomed over 1.5 million visitors, generating approximately USD 300 million in additional revenue through activities such as tastings, lodging, and direct sales [1]Source: Wines of Argentina Organization, "Argentina", winesofargentina.org. This growth highlights the region's ability to attract both domestic and international tourists, driven by its reputation for high-quality wines and scenic landscapes. In Chile, the Colchagua and Casablanca valleys have established formal wine-route consortia, combining vineyard tours with culinary experiences. These initiatives capitalize on Chile's reputation for sustainability, offering a competitive edge over traditional Old World wine regions. By integrating eco-friendly practices and promoting local gastronomy, these regions are enhancing their appeal to environmentally conscious consumers. The strategic benefit is evident: direct-to-consumer channels reduce reliance on distributor margins and foster brand loyalty, providing producers with protection against retail price competition, particularly in markets where off-trade discounting is diminishing per-bottle profitability.

Growing interest in premium and boutique wines

Premiumization is gaining momentum, even as mass-market segments experience volume declines. Brazil's craft wine movement, primarily based in Rio Grande do Sul's Serra Gaúcha region, is drawing investment from urban entrepreneurs who view boutique wineries as lifestyle ventures with export opportunities to niche markets in the United States and Europe. This movement is characterized by small-scale production, a focus on high-quality grapes, and an emphasis on unique, handcrafted wines that appeal to discerning consumers. Chile's export strategy has shifted toward bottles priced above USD 10, with Carmenere and Syrah emerging as key varieties, as producers move away from bulk shipments that rely solely on cost competitiveness. This strategic pivot includes targeted marketing campaigns, partnerships with international distributors, and efforts to highlight the premium quality of Chilean wines. This trend highlights a broader development: as middle-income groups grow across South America, wine is evolving from a commodity to a status symbol, benefiting brands that focus on storytelling, terroir differentiation, and engagement with sommeliers.

Adoption of sustainable and organic wines

The growing adoption of sustainable and organic wines is a significant driver in the South American wine market. This trend is fueled by increasing consumer awareness regarding health, environmental impact, and ethical production practices. Wineries in Argentina, Chile, and Uruguay are responding by investing in organic vineyards, biodynamic methods, and eco-friendly production processes to cater to the rising demand for clean-label and sustainably produced wines. In 2025, 42% of consumers in Latin America preferred organic options, while 34% prioritized products made with locally sourced ingredients [2]Source: Kerry, "How LATAM Consumers Are Redefining Food and Beverage Functionality", kerry.com. This indicates a strong market preference for environmentally conscious and provenance-focused products. As a result, producers are innovating in vineyard management, reducing chemical inputs, and emphasizing transparency and traceability. These efforts position sustainable and organic wines as both a premium offering and a socially responsible choice for modern consumers in the region.

Ethical packaging and convenience Formats

Packaging innovation is transforming distribution economics and enhancing consumer accessibility. Aluminum cans and bag-in-box formats, previously considered less premium, are gaining popularity in Brazil and Chile as producers focus on younger consumers who value portability and portion control over traditional bottle designs. The Moreira Salles family's planned takeover of Verallia, a French glass bottler, in March 2025 highlights the strategic importance of supply chain integration. Controlling packaging inputs helps producers mitigate commodity price fluctuations and facilitates the quicker adoption of sustainable formats. This trend is advancing as convenience packaging reduces barriers for wine-curious consumers who may find 750ml bottles either intimidating or inefficient, thereby broadening the market beyond traditional fine-dining and home-entertaining scenarios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency volatility impacting imported inputs | -0.4% | Argentina, Brazil, Chile | Short term (≤ 2 years) |

| High competition from beer and spirits | -0.5% | Brazil, Colombia, Peru | Medium term (2-4 years) |

| High production costs for organic certification | -0.3% | Argentina, Chile, Brazil | Long term (≥ 4 years) |

| Climate-change-driven water scarcity | -0.6% | Chile, Argentina, Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Currency volatility impacting imported inputs

Currency volatility poses a significant challenge for the South American wine market, particularly for producers dependent on imported inputs such as barrels, machinery, yeast cultures, and specialized packaging materials. Fluctuating exchange rates lead to unpredictable increases in production costs, reducing profit margins and complicating budgeting and long-term planning for wineries. Smaller and mid-sized producers are particularly affected, as they often lack access to hedging mechanisms or viable local alternatives for essential imported inputs. This financial instability can hinder investment in innovation, expansion, or premium wine production, thereby slowing growth in both domestic and export markets and impacting the global competitiveness of South American wines.

High competition from beer and spirits

High competition from beer and spirits serves as a significant restraint on the South American wine market, restricting growth in both consumption and market share. In Chile, for example, beer is the most consumed alcoholic beverage, representing 77% of total alcoholic beverage sales by volume as of 2025, according to USDA reports [3]Source: USDA, "Beer and Ingredients Opportunities in Chile", usda.gov. This strong preference for beer, coupled with the prominent presence of spirits, limits shelf space, marketing focus, and consumer interest in wines, particularly during casual or on-premise drinking occasions. Consequently, wine producers encounter difficulties in expanding their market penetration, especially among younger or price-sensitive consumers, and must focus on innovation or differentiation to compete effectively with the established consumption patterns of beer and spirits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Wine Type: Sparkling Variants Gain Celebratory Share

Still wine maintained a dominant market share of 78.71% in 2025, driven by its widespread use in everyday consumption, restaurant offerings, and export activities. However, sparkling wine is expected to grow at a compound annual growth rate (CAGR) of 3.95% through 2031, indicating a shift toward celebratory and premium consumption occasions. Fortified and dessert wines remain niche products, primarily concentrated in regions influenced by Portuguese traditions, such as Brazil and Argentina's Salta province. These wines, including late-harvest Torrontés and fortified Malbecs, cater to collectors and sommeliers rather than the broader mass market.

Additionally, other wine types, such as pét-nat and orange wines, are gaining traction in boutique portfolios as producers explore natural fermentation and extended skin contact to stand out in competitive retail markets. Historical context highlights that South America's sparkling wine tradition developed later than Europe's. However, rising disposable incomes and the increasing acceptance of wine as a lifestyle product are narrowing this gap. The strategic implication is that the growth of sparkling wine is driven more by the expansion of consumption occasions than by replacing still wine. Producers who position sparkling wine as an everyday indulgence rather than a product reserved for special events can tap into incremental consumption opportunities without significantly impacting still wine sales.

By Color: Rosé's Premiumization Defies Red Dominance

Red wine held 56.10% of the market share in 2025, driven by Argentina's Malbec exports and Chile's shipments of Carmenere and Cabernet Sauvignon. However, rosé wine, with a compound annual growth rate (CAGR) of 5.09% through 2031, highlights a trend of premiumization that is influencing producer portfolios and retail assortments. While white wine lags behind red and rosé in growth, it remains a critical component for producers aiming to maintain portfolio balance and achieve geographic diversification. Argentina's Torrontés and Chile's Sauvignon Blanc dominate white wine exports, particularly to tropical markets in Central America and the Caribbean, where the climate favors chilled, aromatic styles over tannic red wines.

In Brazil, white wine production is concentrated in Rio Grande do Sul, where Italian immigrant communities have historically cultivated Trebbiano and Moscato. Recent plantings of Chardonnay and Riesling indicate a shift toward international varieties that can command higher export premiums. The segmentation by wine color reflects a broader strategic dynamic: red wine continues to deliver volume and margins in established markets, while rosé and white wines present growth opportunities in emerging demographics and occasions where traditional red wines face cultural or climatic challenges.

By End User: Women Drive Premiumization and Format Innovation

In 2025, women accounted for 57.56% of the wine market in South America, indicating a demographic shift that is shaping marketing strategies and product development priorities. Female consumers tend to purchase wine primarily for home consumption, place greater emphasis on health and sustainability claims, and are willing to explore new varietals and formats. This makes them a key target for premiumization strategies. In contrast, the male segment, which is projected to grow at a CAGR of 3.89% through 2031, constitutes a smaller but strategically important group. Men are characterized by higher spending per occasion in on-trade channels and exhibit stronger brand loyalty to established labels. This gender disparity is particularly pronounced in Brazil and Colombia, where wine culture is relatively new. Women in these countries are adopting wine more rapidly than men, who continue to prefer beer and spirits.

The impact of these trends extends to product design and distribution strategies. Women's preferences for lighter alcohol content, smaller serving sizes, and eco-friendly packaging are driving the adoption of formats such as 375ml bottles, aluminum cans, and bag-in-box packaging, which were previously considered less premium. On the other hand, men's dominance in on-trade channels underscores the importance of restaurant and bar placements for building brand awareness and encouraging trial, even as off-trade channels account for the majority of volume. Producers that tailor messaging and packaging by gender, while avoiding outdated stereotypes, can achieve incremental margins by aligning product attributes with consumer preferences rather than adopting a one-size-fits-all approach.

By Distribution Channel: On-Trade Rebounds as Experience Trumps Convenience

Off-trade accounted for 70.38% of the market share in 2025, highlighting the structural advantages of supermarkets, specialty liquor stores, and e-commerce platforms. These channels provide a wide selection, price transparency, and convenience. However, on-trade is expected to grow at a CAGR of 4.45% through 2031, reflecting a post-pandemic recovery driven by experiential consumption and premiumization. Restaurants, wine bars, and hotels generate higher per-bottle margins and serve as key venues for brand-building. Sommeliers and servers play a significant role in influencing consumer trials, making on-trade placements critical for producers aiming to establish premium positioning.

Within the off-trade channel, specialty liquor stores hold a dominant position by offering curated selections and staff expertise, bridging the gap between mass-market supermarkets and the expertise of on-premise sommeliers. Other off-trade channels, such as e-commerce and direct-to-consumer shipments, are experiencing the fastest growth in absolute terms. This growth is driven by digital-native consumers who prioritize convenience and personalized recommendations over in-store browsing. In Argentina, the devaluation of the peso has made restaurant wine prohibitively expensive for domestic consumers, accelerating a shift toward off-trade channels. This trend may persist even if the currency stabilizes, creating a structural challenge for the recovery of on-premise sales in the region's largest market.

Geography Analysis

In 2025, Argentina accounted for 39.95% of South America's wine revenue. The country's RVA sustainability protocol now encompasses over 100 wineries, positioning Argentina as a climate-resilient alternative to drought-affected regions like California and Australia. This strategic positioning is gaining traction among European buyers who prioritize ESG compliance. Colombia, with a 4.14% CAGR projected through 2031, is the region's fastest-growing wine market. This growth is driven by increasing affluence, urbanization, and the emergence of a wine culture that is attracting import-focused distributors. Although wine represents a small share of Colombia's alcohol market, which is dominated by beer and aguardiente, the USD 15-plus wine segment is expanding at double-digit rates as Bogotá and Medellín's middle class shifts from mass-market beverages.

Brazil's wine market is experiencing a divide between craft producers in Rio Grande do Sul and mass-market cooperatives facing challenges such as cost inflation and consumer trading-down. Chile, the region's second-largest wine producer, is contending with water scarcity and stagnant domestic demand. However, Wines of Chile's sustainability certification now covers over 80% of vineyard areas, providing a compliance advantage that appeals to European retailers demanding verified ESG credentials.

Peru and other South American countries remain minor contributors to the region's wine revenue. In Peru, pisco production dominates the grape-based alcohol industry, leaving wine as an import-dependent niche primarily found in Lima's upscale restaurants. Paraguay and Bolivia's wine sectors are minimal, limited by climate, infrastructure, and cultural preferences for beer and spirits. The Mercosur-EU trade agreement, ratified in 2024, grants GI protections to 350 South American labels, including Uruguay's Tannat and Brazil's Vale dos Vinhedos. This agreement establishes a legal framework for terroir-based branding, which could enhance the visibility of smaller producers over time.

Competitive Landscape

The South America wine market exhibits a moderately fragmented structure. Opportunities for growth are emerging in three key areas: the premiumization of underutilized varietals such as Carmenere and Torrontés, the adoption of direct-to-consumer models that eliminate distributor margins, and wine tourism initiatives that transform vineyard visits into high-margin revenue streams. The premiumization trend is driven by increasing consumer interest in unique and high-quality wines, while direct-to-consumer models enable producers to establish closer relationships with customers and improve profit margins. Wine tourism, on the other hand, not only boosts revenue but also enhances brand loyalty by offering immersive experiences to consumers.

Smaller producers in regions like Uco Valley, Casablanca, and Serra Gaúcha are utilizing platforms such as Instagram and TikTok to enhance brand visibility without requiring large marketing budgets. These digital platforms allow producers to reach a broader audience, particularly younger consumers, through engaging content and storytelling. Additionally, craft wineries are differentiating themselves in competitive retail spaces by experimenting with natural fermentation techniques and extended skin contact. These methods cater to the growing demand for artisanal and sustainable products, helping smaller players carve out a niche in the market.

Technology adoption within the market is uneven. While precision viticulture and drip irrigation are widely implemented by large estates to optimize yields and resource efficiency, cooperatives and family-owned growers often face financial barriers to adopting these technologies due to high upfront costs. The Mercosur-EU agreement's Geographical Indication (GI) protections provide a regulatory advantage for established appellations, safeguarding the authenticity and reputation of regional wines. However, inconsistent enforcement of these protections allows counterfeit labels to threaten the premium positioning of exports in international markets, undermining the efforts of legitimate producers to maintain quality standards and brand integrity.

South America Wine Industry Leaders

-

Concha y Toro

-

Viña Santa Rita

-

Bodega Catena Zapata

-

VSPT Wine Group (Viña San Pedro)

-

Grupo Penaflor (Bodega Trapiche)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Brazilian wine group Miolo completed the acquisition of the renowned Argentine winery Renacer. This move significantly expanded Miolo's presence in Argentina and strengthened the cross-border consolidation of South American wine producers.

- November 2024: Chilean producer Viña Ventisquero announced plans to expand its vineyard holdings in Patagonia. This expansion will increase the size of what is considered the world’s southernmost commercial vineyard, supporting future production growth and investments in terroir.

- January 2023: La Celia, the oldest winery in Argentina’s Uco Valley, introduced a new trio of terroir-driven wines that highlight the distinct characteristics of its diverse estate. The estate spans the sub-regions of Paraje Altamira, La Consulta, and Eugenio Bustos. After nearly a decade of collaboration with soil and geology experts to understand site-specific expressions, the winery released three single-parcel wines, including, a Malbec from Paraje Altamira, a Cabernet Franc from La Consulta, and a Cabernet Sauvignon from Eugenio Bustos. Each wine reflects the unique soil and climatic influences of its respective region.

South America Wine Market Report Scope

Wine is an alcoholic drink typically made from fermented grape juice. The South America Wine market is segmented by product type, color, distribution channel, and geography. Based on product type market is segmented into still wine, sparkling wine, fortified wine, and vermouth. Based on the color market is segmented into red wine, rose wine, and white wine, By distribution channel, the market is divided into on-trade and off-trade. Off-trade is further segmented into supermarkets/hypermarkets, specialty stores, online retailers, and other distribution channels. Based on geography market is segmented into Brazil, Argentina, and Rest of South America. For each segment, the market sizing and forecast have been done based on value (in USD million).

By Wine Type

| Fortified/Dessert Wine |

| Still Wine |

| Sparkling Wine |

| Other Wine Types |

By Color

| Red Wine |

| White Wine |

| Rosé Wine |

By End User

| Men |

| Women |

By Distribution Channel

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Other Off-Trade Channels |

By Geography

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Wine Type | Fortified/Dessert Wine | |

| Still Wine | ||

| Sparkling Wine | ||

| Other Wine Types | ||

| By Color | Red Wine | |

| White Wine | ||

| Rosé Wine | ||

| By End User | Men | |

| Women | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Other Off-Trade Channels | ||

| By Geography | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the South America wine market?

The South America wine market size stands at USD 7.90 billion in 2026.

Which country is the largest revenue contributor?

Argentina generated 39.95% of regional revenue in 2025.

Which wine type is growing fastest?

Sparkling wine is expanding at a 3.95% CAGR through 2031.

How will the Mercosur-EU trade deal affect exporters?

The agreement eliminates tariffs over seven years and grants GI protection to 350 South American labels, improving EU market access.

Page last updated on: