Tequila Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

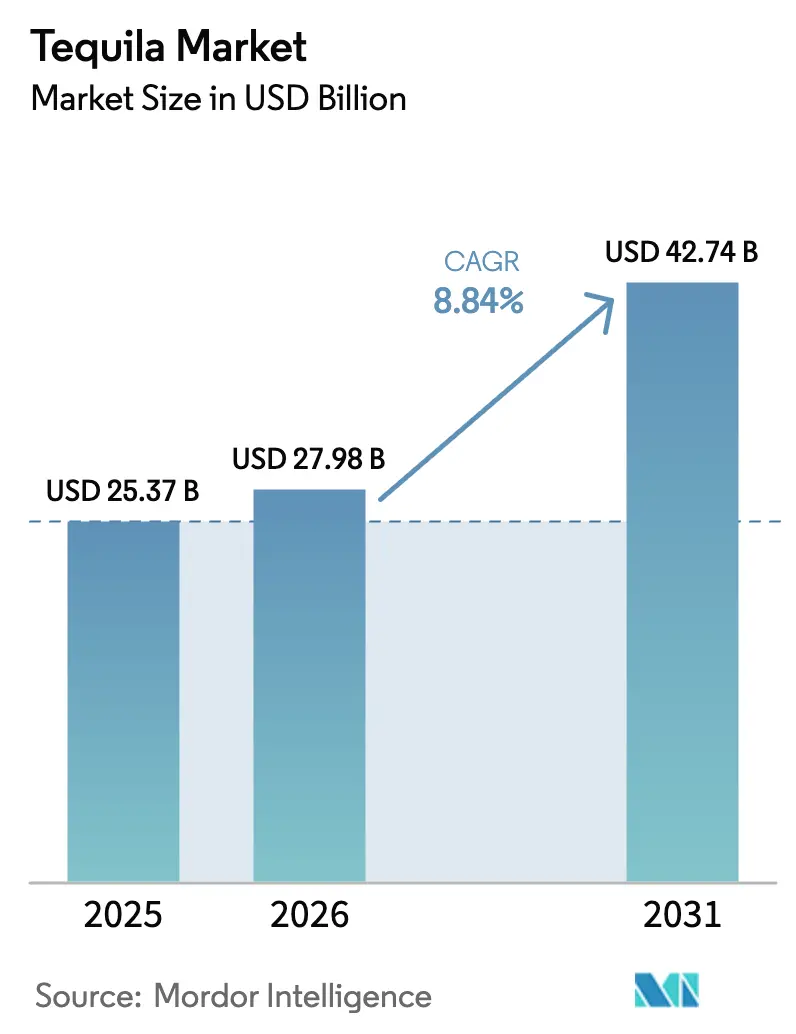

| Market Size (2026) | USD 27.98 Billion |

| Market Size (2031) | USD 42.74 Billion |

| Growth Rate (2026 - 2031) | 8.84% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

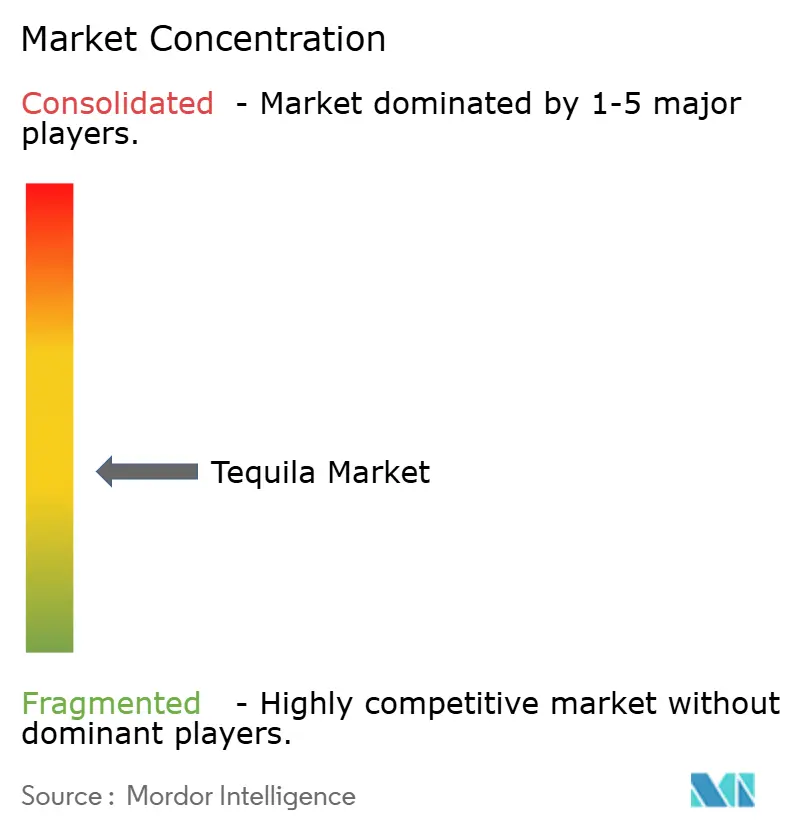

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Tequila Market Analysis by Mordor Intelligence

The Tequila Market size is expected to increase from USD 25.37 billion in 2025 to USD 27.98 billion in 2026 and reach USD 42.74 billion by 2031, growing at a CAGR of 8.84% over 2026-2031. The market's evolution is being shaped by shifting consumer preferences, as aged agave spirits gain popularity as refined sipping alternatives to traditional options like whiskey or cognac. This transformation is primarily driven by an increasing demand for premium products, the rising influence of cocktail culture, and accelerated growth in the Asia-Pacific region. The United States remains the largest market, accounting for over three-fifths of global tequila consumption. However, the fastest growth is being observed in urban centers across India, China, and Southeast Asia, where higher disposable incomes and a growing culture of social drinking are fueling demand. Additionally, the tequila category is experiencing a surge in momentum due to celebrity-backed product launches, which elevate bottles into aspirational lifestyle symbols. Vertical integration strategies are also playing a critical role by ensuring a consistent supply of raw agave and mitigating the impact of price fluctuations. Over the next five years, the tequila market is expected to expand further, supported by the recovery of on-trade channels, innovations in ready-to-drink tequila products, and increasing adoption of additive-free certifications, all of which are creating new growth opportunities.

Key Report Takeaways

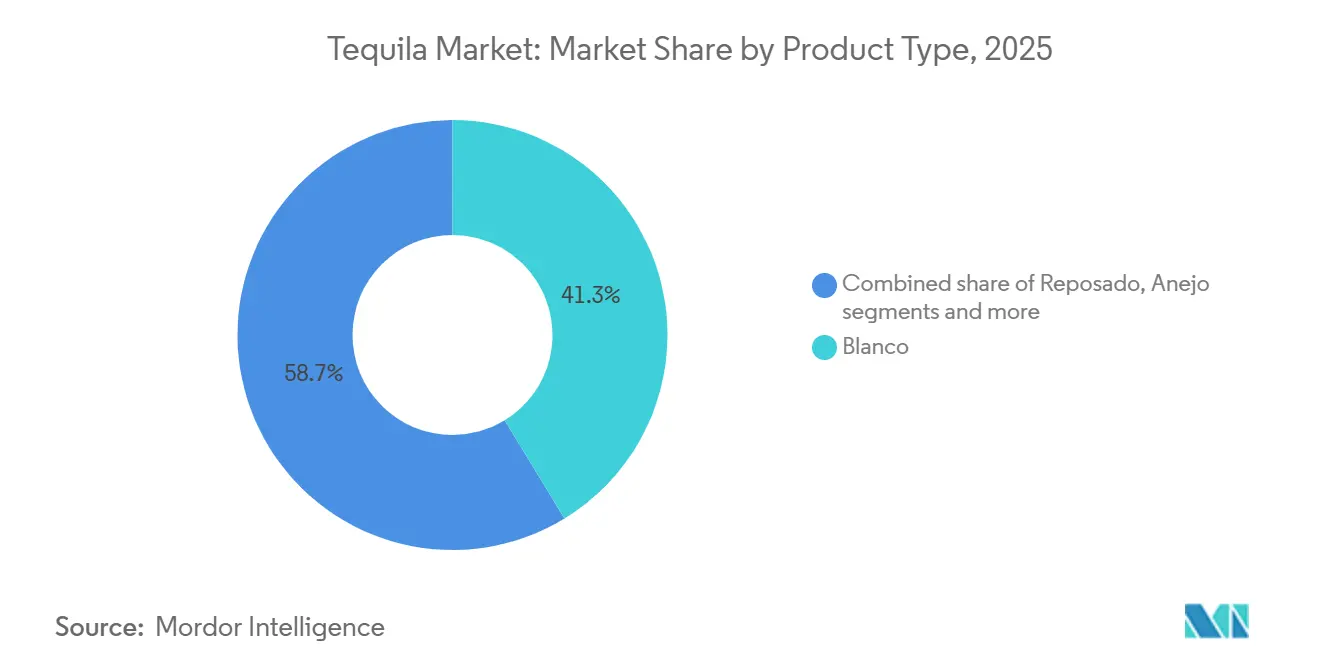

- By product type, blanco led with 41.27% of the tequila market share in 2025, while reposado is on track to grow at a 9.27% CAGR through 2031.

- By category, the mass tier commanded 67.17% of value in 2025; the premium tier is forecast to expand at a 9.36% CAGR to 2031.

- By end user, men represented 56.85% of 2025 consumption, but the women’s segment is advancing at a 9.62% CAGR through 2031.

- By distribution channel, off-trade delivered 59.32% of 2025 sales, whereas on-trade is rebounding at a 10.02% CAGR as hospitality spending returns.

- By geography, North America accounted for 62.38% of the tequila market in 2025, and Asia-Pacific is expected to lead global growth with a projected CAGR of 10.14% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tequila Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer preference for high-quality, artisanal, and aged tequilas | +2.1% | Global, with premium concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Cocktail culture and mixology boom support the market | +1.8% | North America, Europe, and emerging Asia-Pacific urban centers | Short term (≤ 2 years) |

| Effective marketing and branding strategies | +1.5% | Global, celebrity-brand influence strongest in North America and Europe | Short term (≤ 2 years) |

| Sustainability and ethical sourcing drive the market | +0.9% | Europe, North America, and premium segments in Asia-Pacific | Long term (≥ 4 years) |

| Innovation in production and aging | +1.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Growing tourism and hospitality sector | +0.7% | Mexico (Jalisco), North America, and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing consumer preference for high-quality, artisanal, and aged tequilas

The tequila category is evolving as consumers increasingly seek complexity and sipping experiences similar to those of whiskey or cognac. This trend, known as "premiumization," is driving a shift from blanco to reposado and añejo expressions. Reposado, with a forecasted 9.27% CAGR through 2031, is growing faster than blanco. Its adaptability in both cocktails and neat servings stands out. With an aging period of 2-11 months, reposado enables quicker inventory turnover compared to añejo while offering oak-derived vanilla and caramel flavors that appeal to spirits enthusiasts. Brands like Código 1530 and Calirosa are adopting wine-barrel finishing as a differentiation strategy. By utilizing French oak Cabernet and California red-wine barrels, they introduce berry and citrus notes along with a smoother mouthfeel. These tequilas, priced above USD 90, are attracting oenophiles. Cristalino tequilas, which are aged expressions filtered for clarity, combine blanco's visual appeal with añejo's depth. IWSC judges have praised this innovation as a demonstration of high-level craftsmanship, broadening its consumer base. The ultra-premium segment, defined by bottles priced over USD 50, has been the fastest-growing tier for nearly a decade. Limited-edition offerings, such as Clase Azul Ultra, aged for 5 years and featuring hand-painted ceramic, platinum, and 24-karat gold detailing, are positioning tequila as a form of collectible art.

Cocktail culture and mixology boom support the market

Bartenders are significantly expanding tequila's cocktail repertoire, moving beyond the traditional boundaries of margaritas and palomas. Reposado and añejo tequilas are now being creatively incorporated into espresso martinis, Old Fashioneds, and other spirit-forward cocktails, showcasing the versatility of agave when paired with vermouth and aged spirits. Despite the margarita maintaining its position as the most popular cocktail in the United States, mixologists are increasingly experimenting with aged tequilas to enhance flavor profiles by adding depth and oak tannins. This approach is broadening tequila's appeal, particularly among whiskey enthusiasts who appreciate complex and robust flavors. Additionally, the ready-to-drink tequila cocktail segment is leveraging the growing demand for convenience. Products such as canned margaritas and palomas are gaining traction in off-trade channels, appealing to younger consumers who prioritize portability, ease of consumption, and portion control.

Effective marketing and branding strategies

Celebrity-backed tequila brands are transforming traditional marketing approaches by leveraging the power of social media, creating demand through scarcity-driven product launches, and positioning their offerings as lifestyle statements that merge the worlds of spirits and fashion. In September 2025, Kendall Jenner's 818 Tequila unveiled "818 Minis," 50-milliliter bottles designed as bag charms and collectible items, aiming to appeal to Gen Z consumers aged 18-29. Dwayne Johnson's Teremana expanded its presence globally in 2024, while Megan Thee Stallion introduced Chicas Divertidas in February 2025. Both brands utilized influencer-driven campaigns, exclusive product releases, and packaging inspired by fashion trends to capture consumer attention in an increasingly competitive retail environment. Although critics argue that these celebrity brands exploit Mexican heritage and redirect profits away from traditional producers to foreign marketers, their significant impact on the market cannot be overlooked. These brands have successfully driven consumer trials, expanded distribution networks, and elevated price points across the tequila category, reshaping the competitive landscape.

Sustainability and ethical sourcing drives the market

As sustainability becomes a key factor in consumer decision-making, particularly among millennials, the agave cultivation and distillery industries are undergoing transformative changes. Consumers are increasingly seeking environmentally and socially responsible products, prompting major companies like Diageo and Pernod Ricard to invest in sustainable agave initiatives. These programs include the implementation of advanced water treatment systems, the adoption of fair-trade sourcing practices, and the promotion of organic farming methods. Such efforts aim to mitigate reputational risks while aligning with evolving consumer values. Additionally, bat-friendly tequila programs have emerged as a critical strategy to protect pollinator species that are vital for maintaining agave's genetic diversity. These programs address the ecological challenges posed by monoculture farming, which has significantly reduced genetic variation in agave plants, leaving them more vulnerable to pests and climate-related shocks. The demand for organic tequila certifications is also growing, with brands increasingly emphasizing additive-free production processes and greater transparency. This shift directly counters the allowances under NOM-006-SCFI-2012 standards, which permit the inclusion of up to 1% undisclosed additives, such as glycerin, oak extract, caramel coloring, and sugar syrup. By focusing on transparency and sustainability, brands are positioning themselves to meet the expectations of environmentally conscious consumers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent government regulations limit growth | -0.8% | Global, with enforcement concentrated in Mexico | Long term (≥ 4 years) |

| Consumers' inclination toward healthy beverages | -0.6% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Limited penetration in traditional markets | -0.5% | Asia-Pacific (excluding Japan), Middle East, Africa, and South America | Long term (≥ 4 years) |

| High production costs impact market growth | -0.4% | Global, with acute impact on small producers in Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent government regulations limits the growth

Regulatory complexities in tequila production and international trade pose significant challenges, particularly for smaller producers and new entrants to the market. The Tequila Regulatory Council (CRT) enforces strict denomination of origin requirements, specifying that tequila must be made using Blue Agave sourced from designated regions in Mexico. While these regulations ensure product authenticity, they also create supply chain limitations that restrict production scalability. Additionally, United States import regulations require a Certificate of Authenticity for tequila imports, issued by the CRT, which increases administrative costs and can lead to delays. In 2024, the United States remained the largest importer of tequila from Mexico, with imports totaling 334,573.91 thousand liters, according to the Tequila Regulatory Council[1]Source: Tequila Regulatory Council, “Informacion Estadistica”, crt.org.mx. While the regulatory framework ensures the quality and authenticity of tequila, it inadvertently creates an oligopolistic market. This structure favors established producers, especially those with robust CRT ties and distribution networks. These challenges intensify during agave shortages. In such times, limited supply and stringent production mandates exert cost pressures, hitting smaller producers the hardest.

Consumers’ inclination toward healthy beverages

Health-conscious consumers are reducing their alcohol intake or choosing low-calorie, organic, and functional beverages, creating challenges for spirit categories that lack a wellness focus. Tequila brands have adapted by promoting their lower calorie content compared to beer and sugary cocktails. They also market 100% agave tequilas as "cleaner" options, free from additives and non-agave sugars. While organic certifications and additive-free claims address transparency demands, tequila still faces competition from hard seltzers, non-alcoholic spirits, and functional beverages that align more closely with wellness trends. Approximately one-third of alcohol consumers now prioritize quality over quantity, favoring premium spirits consumed in moderation over high-volume, low-cost alternatives. This trend benefits super-premium tequila brands but creates challenges for mass-market mixto brands. Flavored tequilas and ready-to-drink cocktails, while appealing to younger consumers, risk being perceived as sugary and less healthy, creating a conflict between accessibility and wellness positioning. Additionally, the "sober curious" movement and the growing popularity of alcohol-free social events in North America and Europe present structural challenges. Younger demographics are increasingly experimenting with reduced alcohol consumption and adopting alternative social rituals that often exclude spirits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reposado Outpaces Blanco Despite Lower Share

Blanco accounted for 41.27% of the tequila market in 2025, driven by its position as the preferred cocktail base and its appeal to consumers seeking the fresh agave flavor without oak influence. However, Reposado is expected to grow at a 9.27% CAGR through 2031, marking the fastest growth among product types. This growth is fueled by consumers shifting toward aged variants that combine agave purity with vanilla, caramel, and spice notes developed during 2-11 months of oak barrel aging. This trend highlights a broader premiumization movement: bartenders are increasingly using reposado in espresso martinis and other spirit-forward cocktails, while consumers are choosing to enjoy aged tequilas neat or on the rocks instead of taking shots with lime and salt. Extra Añejo, aged for more than 3 years, represents the ultra-premium segment with its deep amber color and rich chocolate and coffee notes. Retail prices often exceed USD 150, making it a popular choice for collectors and special occasions.

Other product types include Joven, a blend of blanco and aged tequila, sometimes softened with caramel color or glycerin, and Cristalino, a high-growth innovation where añejo or extra añejo is charcoal-filtered to remove color while retaining oak-derived complexity. Wine-barrel finishing is gaining popularity, with brands like Código 1530 and Calirosa using French oak Cabernet and California red-wine barrels. These methods produce pink-hued "Rosa" blancos and añejos with berry and citrus notes, priced above USD 90 and appealing to wine enthusiasts. The shift toward aged variants is also influenced by barrel sourcing economics. The United States bourbon industry supplies ex-bourbon American oak barrels, which impart bold vanilla and caramel flavors. Meanwhile, French oak barrels, previously used for wine, cognac, or Armagnac, offer more subtle and refined flavor profiles, supporting premium pricing.

By End User: Female Segment Fastest-Growing Despite Male Dominance

Male consumers accounted for 56.85% of tequila's volume in 2025, reflecting historical consumption trends and the spirit's traditional association with masculine party rituals. Data from the World Health Organization highlights a stark contrast in alcohol consumption: men averaged 8.2 liters per capita, while women lagged at 2.2 liters[2]Source: World Health Organization, "Alcohol", who.int. However, the female demographic is expected to grow at a CAGR of 9.62% through 2031, the fastest among end-user groups. This growth is driven by the popularity of flavored tequila variants, celebrity-endorsed brands targeting women, and marketing campaigns that reframe tequila as a sophisticated sipping option rather than a party drink. Megan Thee Stallion's "Chicas Divertidas," launched in February 2025, capitalized on her extensive social media influence to appeal to younger female consumers who identify with her brand.

Flavored tequila is particularly popular among younger consumers, and this group skews more female compared to traditional blanco or añejo drinkers. Additionally, women's increasing involvement in agave farming, jimador roles, and master blending has provided brands with authenticity narratives that highlight female leadership and craftsmanship. The slower growth of the male segment reflects market maturity in North America, where male tequila consumption is already high, and limited penetration in traditional spirits markets like whiskey and beer, where male loyalty remains strong. Female-focused marketing strategies include smaller 50-milliliter mini bottles, pastel or pink packaging, partnerships with social media influencers, and cocktail recipes emphasizing fresh ingredients and lower alcohol content. These efforts aim to reduce barriers to trial and promote regular consumption occasions beyond parties and celebrations.

By Category: Premium Segment Accelerates Despite Mass Dominance

The mass category accounted for 67.17% of the tequila market in 2025, highlighting the sustained popularity of value-priced mixto tequilas and entry-level 100% agave blancos priced under USD 40. However, the premium segment is experiencing significant growth, with a 9.36% CAGR projected through 2031. This growth is driven by celebrity-endorsed brands, innovations such as cristalino, wine-barrel finishes, and exclusive limited-edition releases. These premium products typically start at prices above USD 50 and often exceed USD 100. Consequently, the competitive landscape is evolving. Multinational corporations like Diageo, Pernod Ricard, and Brown-Forman are heavily investing in super-premium portfolios to capitalize on higher margins and align with consumers' shift toward premiumization.

Celebrity-backed brands are heavily concentrated in the premium segment, leveraging social media influence, scarcity-driven product launches, and lifestyle branding to secure shelf space and attract consumer attention. For instance, Kendall Jenner's 818 Tequila, priced at approximately USD 45 for standard bottles, introduced 50-milliliter "Mini" bottles priced between USD 4-5. Marketed as bag charms and collectible accessories, these "Minis" appeal to Gen Z's preference for self-expression and the "little-treat" economy. While the mass segment faces challenges, such as health-conscious consumers perceiving mixto tequilas as lower quality and criticism of the 1% additive allowance under NOM-006-SCFI-2012 standards, it continues to lead in volume. This is primarily due to price sensitivity in emerging markets and the high demand for cocktails in bars and restaurants.

By Distribution Channel: On-Trade Rebounds as Hospitality Recovers

Off-trade channels represented 59.32% of tequila sales in 2025, driven by pandemic-era trends favoring at-home consumption, the growth of e-commerce, and the emergence of specialty liquor stores and direct-to-consumer models. However, the on-trade channel is expected to grow at a 10.02% CAGR through 2031, the fastest among distribution channels. This growth is attributed to the recovery of bars, restaurants, and nightclubs from pandemic disruptions, alongside the reintroduction of super-premium pours and cocktail programs that emphasize aged tequilas and artisanal brands. Tequila achieved a significant milestone in Q1 2025 by surpassing vodka to claim the largest revenue share in the U.S. spirits market. This was driven by on-premise premiumization and bartender innovations that expanded tequila's cocktail repertoire beyond margaritas and palomas. While the margarita remains the most popular cocktail in the U.S., mixologists are now incorporating reposado and añejo tequilas into espresso martinis, Old Fashioneds, and other spirit-forward cocktails, increasing check averages and driving volume growth in on-trade venues.

The off-trade's leading share highlights the advantages of retail pricing, convenience, and the growing popularity of ready-to-drink tequila cocktails in cans and bottles. These products appeal to younger consumers who prioritize portability and portion control. E-commerce platforms and direct-to-consumer models have enhanced access to limited-edition and super-premium tequilas. By bypassing traditional three-tier distribution systems, brands achieve higher margins and gain access to valuable consumer data. Specialty liquor stores, along with other off-trade channels, such as supermarkets and convenience stores where regulations permit, benefit from impulse purchases, promotional displays, and the ability to offer a wide range of price points and product types. On the other hand, on-trade venues provide unique experiential benefits. Bartender recommendations, cocktail customization, and social settings encourage trials of new brands and aged expressions. The post-pandemic recovery of tourism and hospitality, particularly in tequila-producing regions like Jalisco, further strengthens these dynamics. Distillery tours and tequila trails in these regions attract international visitors and drive on-site sales.

Geography Analysis

North America accounted for 62.38% of the tequila market in 2025, driven by the United States being the primary destination for Mexican tequila exports and the spirit's strong integration into American cocktail culture. Tequila surpassed vodka to become the top revenue-generating spirit in the United States market during Q1 2025, propelled by premiumization, the rise of celebrity-backed brands, and the margarita's popularity as the nation's favorite cocktail. While Canada and Mexico hold smaller shares within North America, both markets are growing. Mexico's tequila consumption is increasing due to a recovery in tourism and hospitality, while Canada's multicultural urban centers are fostering interest in premium agave spirits. Mexico's tequila supply chain, encompassing agave cultivation to bottling, operates under strict regulations and is limited to specific regions. The National Institute of Statistics and Geography reported that Mexico produced 13.36 million liters of tequila blanco in April 2025[3]Source: National Institute of Statistics and Geography, "Economic Information Bank (BIE)", inegi.org.mx. Canada, meanwhile, is emerging as a key growth market within North America.

Asia-Pacific is expected to lead global growth with a projected CAGR of 10.14% through 2031, driven by rising disposable incomes, urbanization, and the growing adoption of cocktail culture in countries such as China, Japan, India, Thailand, and Singapore. Following pandemic-related disruptions, China is reclaiming its position as a leading global tequila importer. Japan, a mature market for premium tequila, continues to value aged varieties and terroir-focused narratives. In Thailand, Singapore, and Indonesia, tequila-based drinks are gaining traction in cocktail bars and nightlife venues. Australia and New Zealand benefit from well-established spirits cultures and high per-capita consumption of premium imports. In the Middle East, cultural and religious norms in countries like the UAE and Saudi Arabia limit tequila's reach. However, expatriate communities and tourism-driven hospitality sectors in cities such as Dubai and Riyadh are creating niche demand for super-premium brands.

Europe, South America, and the Middle East and Africa, while holding smaller market shares, exhibit varied growth trends. Spain is the world's second-largest tequila importer after the United States, with Germany, the United Kingdom, France, and Italy also ranking among the top importers, driven by premiumization and the rise of cocktail culture. However, compliance with the European Union's spirits regulations, requiring origin labeling and additive disclosure, poses challenges. At the same time, these regulations enhance the quality perception of 100% agave tequilas. In South America, rising disposable incomes are encouraging urban consumers in Brazil, Argentina, Colombia, and Chile to explore imported spirits. However, growth is constrained by limited distribution infrastructure and high import duties. In the Middle East and Africa, alcohol regulations in predominantly Muslim countries present structural barriers. Nevertheless, established spirits markets in South Africa, Nigeria, and Morocco, along with growth opportunities in Turkey's urban centers, indicate potential. Tequila's Denomination of Origin status provides legal protection and brand value, but its limited penetration in traditional markets highlights the need for customized marketing strategies, strategic distribution partnerships, and effective regulatory navigation to unlock long-term growth.

Competitive Landscape

The tequila market is moderately fragmented, with production concentrated in Mexico and consumption concentrated in Mexico and the United States. Key players, such as Bacardi Limited, Diageo PLC, Pernod Ricard SA, Constellation Brands, Inc., and Suntory Holdings Limited, are focusing on product innovation and strengthening distribution networks to reach a wider global consumer base. Additionally, these industry leaders are forming strategic alliances with e-commerce platforms to expand their digital presence and engage with online consumers in emerging markets.

These companies are prioritizing premiumization, expanding their footprint across diverse geographic regions, and differentiating themselves through robust environmental, social, and governance (ESG) initiatives. Their dedication to innovation and sustainability is reflected in the adoption of advanced technologies, including drone-enabled agave mapping for precision agriculture, water-reuse systems to improve resource efficiency, and additive-free certifications to align with evolving consumer demands.

Consumer resistance to the 1% additive allowance under the NOM-006-SCFI-2012 standards is driving demand for transparency and "True" tequila positioning, creating opportunities for additive-free certifications. Cross-category consolidation is emerging, as demonstrated by Tito's Vodka acquiring a majority stake in Lalo Tequila in September 2025, signaling the diversification efforts of single-brand spirits houses. Although technology adoption remains limited, Ford Motor Company's partnership with Jose Cuervo to develop agave bioplastics for automotive components highlights the industry's potential for innovation in sustainability and byproduct utilization. While regulatory compliance with the Consejo Regulador del Tequila's certification processes and NOM-006-SCFI-2012 standards poses challenges for new entrants, the growth of contract distilleries (maquiladoras) provides an alternative. These distilleries enable celebrity brands and startups to enter the market without significant capital investments in facilities, reducing entry barriers and accelerating brand expansion.

Tequila Industry Leaders

-

Diageo PLC

-

Constellation Brands, Inc.

-

Suntory Holdings Limited

-

Pernod Ricard SA

-

Bacardi Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: FINO Tequila, co-founded by Yuvraj Singh and a group of Indian American entrepreneurs, has debuted in India. This ultra-premium, award-winning tequila combines the traditional craftsmanship of Jalisco's Highlands in Mexico with a forward-thinking global vision.

- April 2025: UXCO, Inc. introduced Escasa, a new tequila brand, to the United States market. The portfolio features both Blanco and Reposado variants. Escasa Tequila emphasizes the authentic flavors of Jalisco, Mexico.

- March 2025: Meanwhile Drinks, a London-based company, unveiled its inaugural Tequila brand, Desdeya. In crafting Desdeya Tequila, Meanwhile Drinks collaborated with Grupo Tequilero México, located in Arandas, in the Highlands of Jalisco.

- December 2024: Louis Vuitton Moët Hennessy expanded its portfolio by launching the luxury tequila brand 'Volcan de Mi Tierra' in India. Featuring a premium range that includes Blanco, Reposado, Cristalino, and the distinguished Volcan X.A., this launch underscores the company's commitment to elevating standards of sophistication and craftsmanship in the spirits industry.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the tequila market as every 100 % blue-agave and mixto spirit distilled in Mexico, bottled either at source or in international bulk-bottling facilities, and sold through on-trade and off-trade channels worldwide at producer-level values that are adjusted to account for direct brand-owned retail operations.

Scope Exclusion: Ready-to-drink agave cocktails, mezcal, sotol, and other non-tequila agave spirits are not included.

Segmentation Overview

-

By Product Type

- Blanco

- Reposado

- Anejo

- Other Types

-

By End User

- Men

- Women

-

By Category

- Mass

- Premium

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Specialty/Liquor Stores

- Others Off Trade Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Thailand

- Singapore

- Indonesia

- South Korea

- Australia

- New Zealand

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Saudi Arabia

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview agave farmers, master distillers, regional distributors, duty-free buyers, and bar managers across North America, Europe, and key Asia-Pacific metros. These conversations validate production run rates, channel mark-ups, and emerging premiumization patterns before we finalize assumptions.

Desk Research

We start by mapping supply using open data from the Consejo Regulador del Tequila, Mexico's Secretaría de Economía export filings, UN Comtrade shipment codes, DISCUS shipment surveys, and consumer panel updates from sources such as Statista and Euromonitor. Trade journals and filings accessed through Dow Jones Factiva and D&B Hoovers give us company-level shipment, capacity, and price moves. Supplementary checks draw on Eurostat import dashboards, Volza container-level export alerts, and patent activity scraped via Questel for process innovations that signal capacity shifts. This list is illustrative; additional public and proprietary repositories feed the desk stage.

Market-Sizing & Forecasting

A top-down reconstruction begins with CRT certified production, subtracts domestic bulk transfers, adds verified export volumes, and applies channel-specific average selling prices. Results are cross-checked through selective bottom-up roll-ups of listed producer revenues and sampled distributor mark-ups. Variables that feed the model include blue-agave farm-gate prices, premium segment share, on-trade footfall indices, disposable income growth, agave maturation cycles, and new brand launch counts. A multivariate regression blends these drivers with historical volume to project demand, while scenario analysis bridges data gaps in emerging markets.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, anomaly checks against external shipment and price trackers, and peer audit before release. We refresh the full dataset each year and trigger interim updates whenever agave price spikes, tariff changes, or major capacity additions occur.

Why Mordor's Tequila Baseline Commands Reliability

Published estimates often diverge because firms vary scope, price points, and refresh timing; understanding those levers is vital before decisions are made.

Key gap drivers stem from whether on-trade revenue is counted, how premium bottles are priced, and if bulk-exported tequila bottled offshore is included, which is where Mordor's disciplined variable set delivers a fuller picture.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 25.67 B (2025) | Mordor Intelligence | - |

| USD 11.43 B (2024) | Global Consultancy A | Excludes on-trade and offshore bottling, applies factory-gate ASPs |

| USD 11.69 B (2024) | Industry Publication B | Uses shipment volumes only, omits super-premium tier, static FX rates |

| USD 12.38 B (2025) | Regional Consultancy C | Covers limited geographies, conservative premiumization share |

Taken together, the comparison shows that our wider channel coverage, live ASP tracking, and annual refresh cadence give decision-makers a market baseline that is both transparent and dependable.

Key Questions Answered in the Report

Which product type is expanding fastest within the tequila market?

Reposado is forecast to grow at a 9.27% CAGR through 2031, outpacing other expressions.

How large will the tequila market size be in 2031?

The tequila market size is projected to reach USD 42.74 billion by 2031.

What drives premium growth in the tequila market?

Celebrity branding, cristalino innovation, and barrel-finishing techniques propel premium-tier sales.

Which region is expected to deliver the highest tequila CAGR?

Asia-Pacific is projected to register a 10.14% CAGR through 2031 due to rising disposable income and cocktail adoption.

Page last updated on: