Grain Alcohol Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

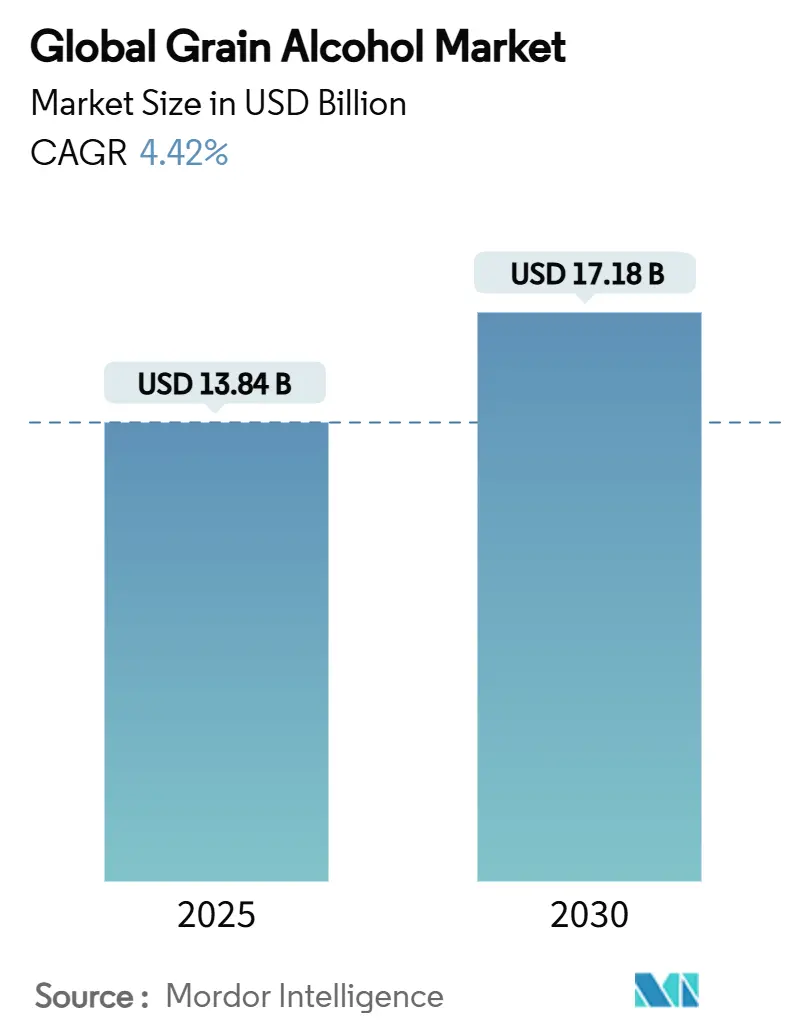

| Market Size (2025) | USD 13.84 Billion |

| Market Size (2030) | USD 17.18 Billion |

| Growth Rate (2025 - 2030) | 4.42% CAGR |

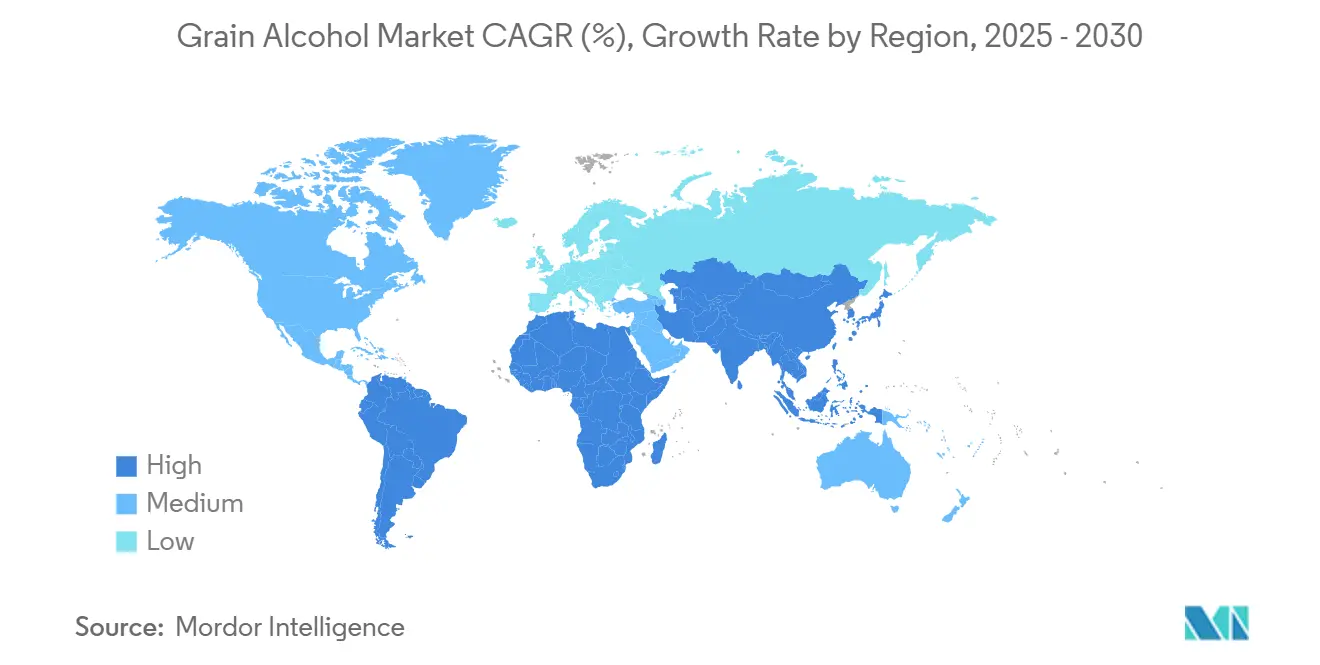

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Grain Alcohol Market Analysis by Mordor Intelligence

The global grain alcohol market size demonstrates robust financial performance, with projections indicating growth from USD 13.84 billion in 2025 to USD 17.18 billion by 2030, maintaining a steady compound annual growth rate (CAGR) of 4.42%. This market transformation reflects a significant shift in business dynamics, where manufacturers are moving away from traditional bulk production methods toward more sophisticated, high-purity applications. The pharmaceutical industry emerges as a key revenue driver, offering attractive profit margins through premium pricing structures. However, beverage manufacturers face increasing operational challenges as they navigate complex regulatory requirements, which impact their profit margins. This evolving landscape presents both opportunities and challenges for market participants as they adapt their business strategies to capitalize on higher-value segments while managing regulatory compliance costs [1]Source: Food and Drug Administration, “FDA Report on the Adoption of Advanced Manufacturing in Non-Medical Industries,” fda.gov.

Key Report Takeaways

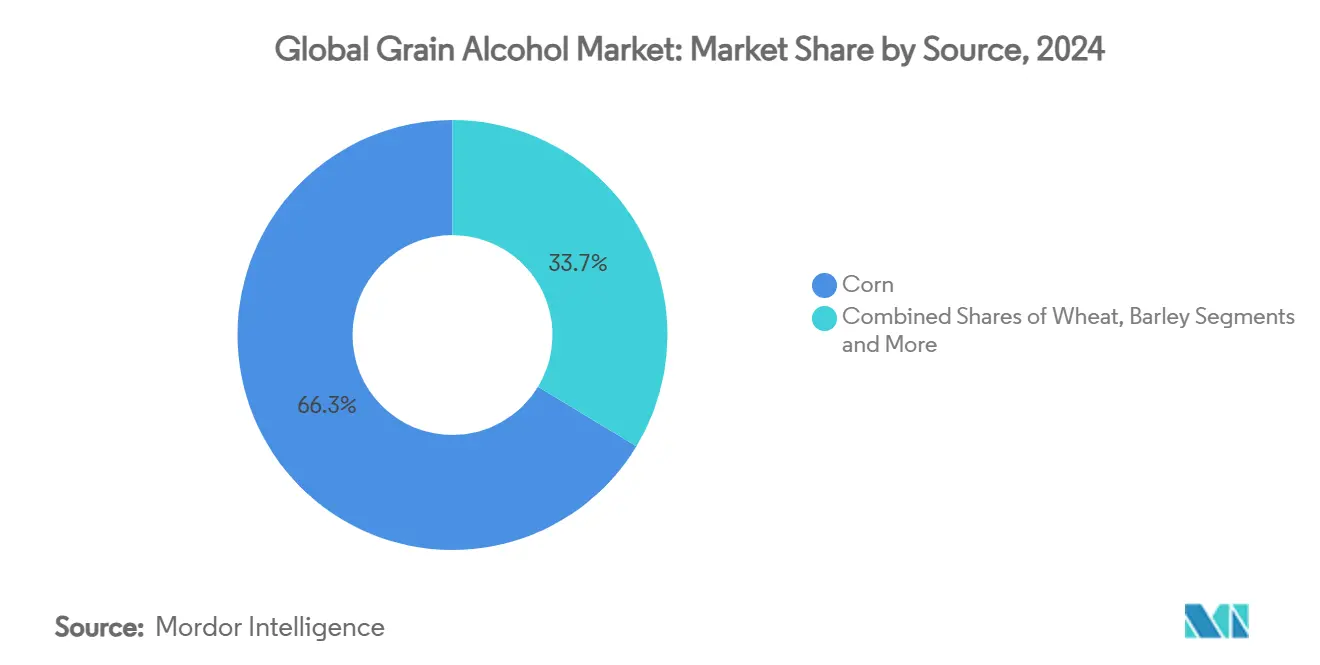

- By source, corn commanded 66.37% of the grain alcohol market share in 2024, whereas rye is forecast to expand at 5.74% CAGR through 2030 in response to craft distillery demand and gluten-free beverage regulations.

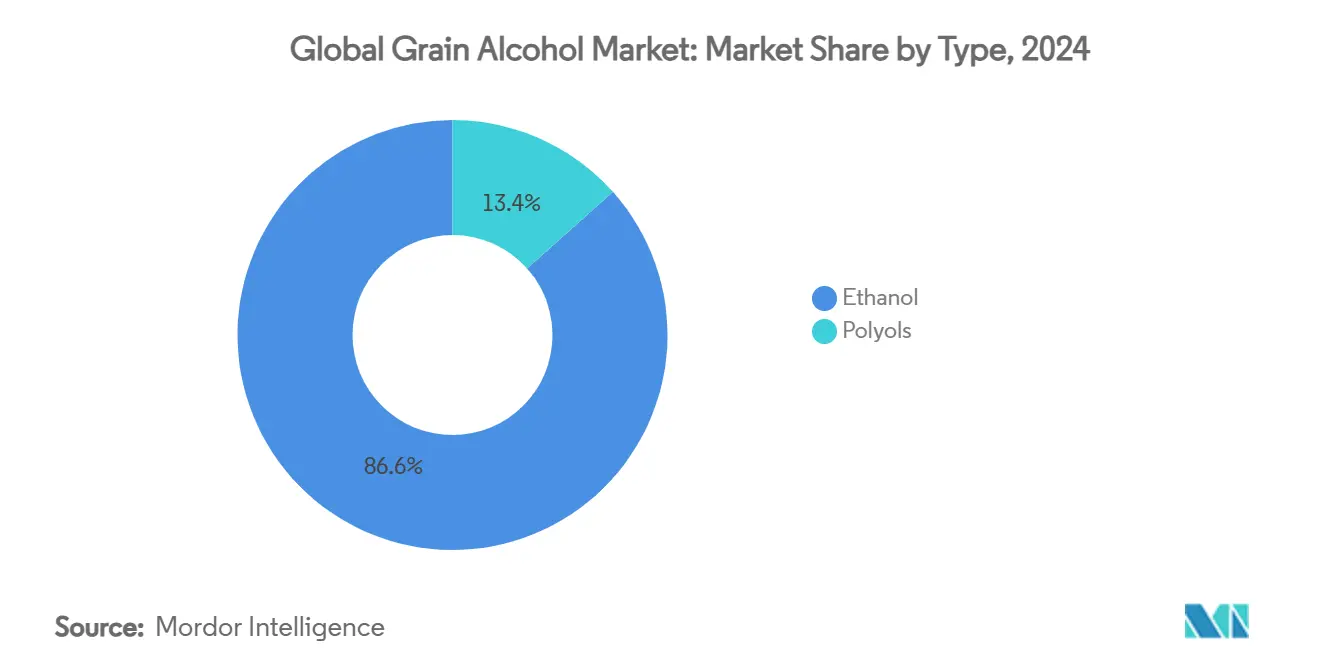

- By type, ethanol dominated with 86.37% of the grain alcohol market size in 2024; the polyols segment is projected to grow at 5.64% CAGR between 2025 and 2030, led by personal-care and pharmaceutical applications.

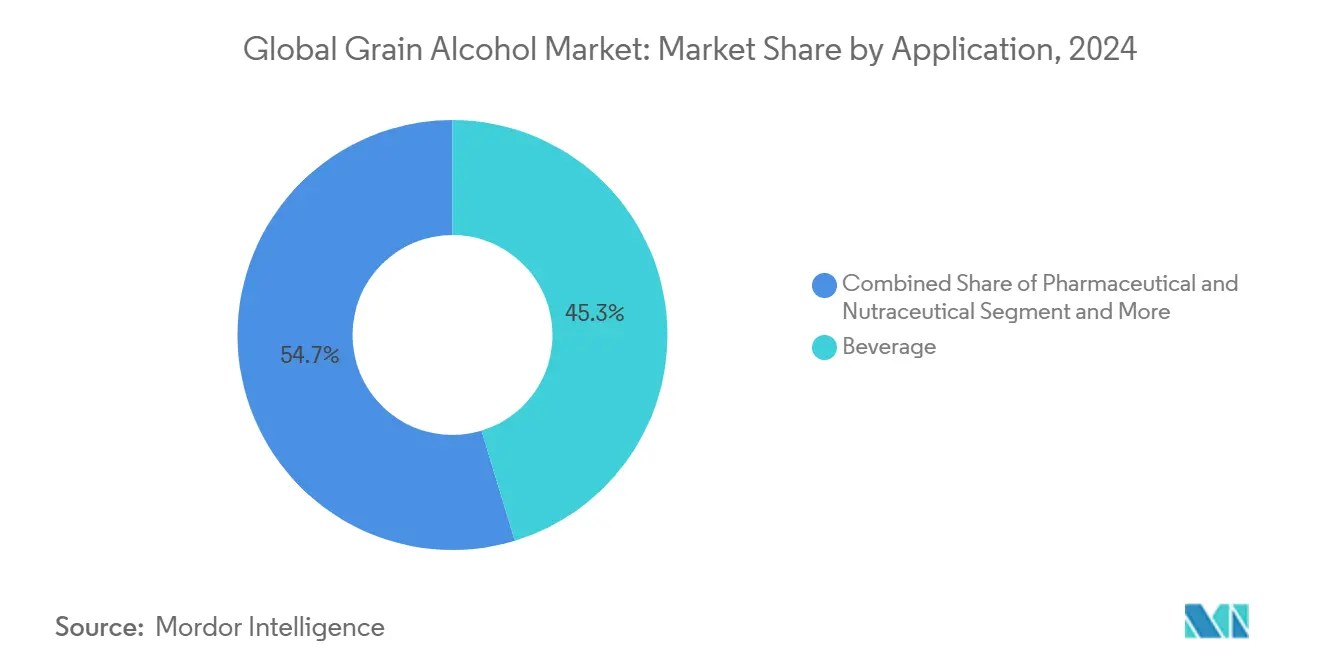

- By application, beverages accounted for a 45.36% share of the grain alcohol market size in 2024, while pharmaceutical and nutraceutical use is advancing at 5.82% CAGR through 2030 due to rising excipient demand.

- By geography, North America held 36.13% of the grain alcohol market share in 2024; Asia-Pacific is expected to grow at 5.39% CAGR over 2025-2030, underpinned by E10 and E20 blending mandates

Global Grain Alcohol Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for premium and craft grain-based alcoholic beverages | +0.8% | North America and Europe, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Expansion of craft distilleries producing artisanal spirits | +0.6% | Global, with early gains in North America, Europe | Short term (≤ 2 years) |

| Advances in distillation and purification technologies | +0.7% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Increasing consumer preference for natural and sustainable grain alcohol products | +0.5% | Europe & North America core, expanding to APAC | Medium term (2-4 years) |

| Expanding pharmaceutical and personal care applications | +0.9% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Demand for gluten-free and allergen-free alcoholic beverages | +0.4% | Europe & North America, emerging in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing demand for premium and craft grain-based alcoholic beverages

Premium craft spirits are reshaping the grain alcohol production landscape through their ability to command higher prices, as artisanal producers prioritize product excellence over mass production efficiencies. Koval Distillery demonstrates this evolution by successfully expanding its production capacity while preserving its premium market position. The company continues to achieve robust sales performance despite unfavorable market conditions. The premium craft segment's distinct requirements for specialty grain varieties and small-batch distillation processes create operational complexities that major industrial producers struggle to replicate efficiently. Through their commitment to premium pricing for heritage grains and specialized processing methods, craft producers establish a unique market position that shields them from fluctuations in commodity prices. A major investment by Staghorn in Kentucky's largest independent distillery underscores the institutional investment community's recognition of craft spirits' inherent advantages in capturing premium consumer segments. The craft distilling industry continues to discover promising expansion opportunities in Asian markets, specifically South Korea, Taiwan, and China, where premium domestic market segments remain relatively untapped.

Expansion of craft distilleries producing artisanal spirits

The expansion of craft distilleries continues to reshape grain sourcing dynamics, as these boutique producers establish meaningful partnerships with local farming communities rather than depending on traditional commodity markets. This evolution has generated specialized demand patterns for premium grains across different regions, which industrial ethanol manufacturers find challenging to accommodate within their high-volume business models, resulting in the emergence of parallel supply networks that emphasize grain quality and characteristics over production scale. Recent regulatory adjustments have removed previous production restrictions for craft distillers, intensifying market competition for superior grain supplies. This distributed manufacturing approach delivers logistical advantages through reduced transportation requirements while creating valuable price premiums that support local agricultural economies. The craft segment's commitment to supply chain visibility and product authenticity continues to boost demand for non-GMO and organic grain varieties, establishing distinct market segments that maintain premium pricing independently of broader commodity market fluctuations. These smaller producers now achieve production consistency through advanced technological implementations, including sophisticated fermentation processes and automated quality assurance systems, matching capabilities that were historically exclusive to large-scale industrial operations.

Advances in distillation and purification technologies

Technological advancements in distillation processes transform production economics by minimizing energy consumption and maximizing yield efficiency. Heat recovery systems in micro-distilleries deliver substantial reductions in both carbon emissions and water consumption per liter of pure alcohol produced, achieving rapid return on investment. Dividing-wall columns and hybrid process configurations provide significant economic benefits, particularly benefiting mid-scale producers competing with industrial facilities. The implementation of heat pump technology in carbon-neutral distilleries eliminates dependency on fossil fuels in production processes, creating competitive advantages in markets with established carbon pricing mechanisms. Enhanced enzymatic treatments optimize corn-to-ethanol conversion efficiency, minimizing feedstock requirements while improving financial returns for agricultural producers. The integration of carbon capture technologies enables producers to monetize their environmental initiatives while reducing operational expenses.

Increasing consumer preference for natural and sustainable grain alcohol products

Environmental regulations and corporate sustainability commitments fundamentally transform purchasing decisions across pharmaceutical, cosmetic, and beverage industries. Market dynamics reflect growing consumer demand for transparency in grain sourcing and processing methods, creating substantial opportunities for producers who implement and demonstrate sustainable agricultural practices. Forward-thinking companies that invest in renewable energy solutions for their distillation processes gain significant market advantages by offering carbon-neutral products to environmentally conscious consumers. Strategic agricultural initiatives, such as ADM's comprehensive regenerative farming program, effectively connect with premium market segments seeking robust and verifiable sustainability credentials throughout their entire supply chain network.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility and supply fluctuations in raw grain materials | -0.9% | Global, particularly acute in import-dependent regions | Short term (≤ 2 years) |

| Stringent and diverse regulatory policies on alcohol production | -0.6% | Global, most restrictive in Europe and North America | Long term (≥ 4 years) |

| Supply chain disruptions caused by geopolitical tensions | -0.7% | Global, concentrated in regions dependent on Ukrainian/Russian grains | Medium term (2-4 years) |

| High energy and water consumption for distillation and purification | -0.5% | Global, most impactful in regions with high energy costs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price volatility and supply fluctuations in raw grain materials

The grain market faces significant challenges as price volatility continues to squeeze profit margins, with smaller producers being particularly vulnerable due to their limited financial hedging capabilities. The USDA's projection of corn prices at USD 4.35 per bushel for 2025/26 represents a considerable decrease from recent peak levels, adding pressure on producer revenues [2]Source: United States Department of Agriculture, “World Agricultural Supply and Demand Estimates,” usda.gov. The industry also grapples with trade policy uncertainties, as potential reductions in U.S. agricultural exports of soybeans and corn under various tariff scenarios force producers to maintain higher inventory levels to manage risk. Additionally, weather-related production fluctuations in key growing regions introduce seasonal supply constraints, creating operational difficulties for producers with limited storage infrastructure. While the improving corn stocks-to-use ratio offers some reassurance regarding supply availability, the industry continues to face logistical hurdles in efficiently connecting areas of surplus production with processing facilities, highlighting the ongoing challenges in supply chain optimization.

Stringent and diverse regulatory policies on alcohol production

The intricate web of regulatory requirements across different jurisdictions imposes significant compliance costs, creating a distinct advantage for established large producers while effectively limiting market participation for smaller businesses. The stringent FDA pharmaceutical-grade ethanol standards, requiring a precise 99.2% purity level, necessitate extensive capital investments in sophisticated purification equipment and robust quality control systems. This challenge is further amplified by the U.S. "Alcohol Facts" labeling requirements, which demand detailed nutritional and alcohol content information, placing an additional burden on smaller producers who often operate without specialized regulatory compliance teams [3]Source: Federal Register, “Alcohol Facts Statements,” federalregister.gov. The situation becomes more complex in the European market, where varying standards for low-alcohol and non-alcoholic products across EU member states create market fragmentation, forcing companies to navigate multiple regulatory frameworks for product development and marketing strategies. The international trade landscape adds another layer of complexity through TTB import/export documentation requirements and diverse country-specific certification processes, resulting in administrative overhead that becomes particularly challenging for businesses operating at lower transaction volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Corn Dominance Faces Specialty Grain Challenge

The grain-based market landscape demonstrates corn's substantial market presence, commanding a 66.37% share in 2024. This significant market position is primarily attributed to corn's extensive processing infrastructure and operational efficiencies that have been developed over decades. While corn maintains its strong foothold in the market, there is a notable shift as specialty grains make inroads into premium market segments, presenting both opportunities and challenges for industry participants.

Among these emerging segments, rye stands out as the most dynamic performer, projected to grow at a 5.74% CAGR through 2030, driven by increasing demand from craft distillers who emphasize distinctive flavor profiles in their products. The industry is witnessing technological advancements, particularly in corn-to-ethanol conversion processes, where improved enzymatic treatments are enhancing production efficiency and reducing operational costs. In parallel market segments, wheat maintains its established position in pharmaceutical applications, where its unique gluten properties make it indispensable, while barley has successfully carved out its niche in the premium spirits market, catering to specialized production requirements.

By Type: Ethanol's Industrial Shift Toward High-Value Applications

The ethanol market, currently dominated by an 86.37% share in 2024, is experiencing a significant transformation. Traditional fuel applications are giving way to sophisticated industrial and pharmaceutical uses, where manufacturers can command higher prices. In the pharmaceutical sector, the growing requirement for high-purity ethanol variants (96% and 99.9% ABV) has established distinct market segments. These segments prioritize quality specifications over cost considerations, allowing producers to maintain stronger profit margins compared to conventional commodity markets. The polyols market is set to expand at 5.64% through 2030, primarily due to their increased integration into pharmaceutical and personal care formulations, where their unique functional properties justify premium pricing structures.

POET's innovative approach to bio-based purified alcohol production illustrates the industry's technological advancement. Their patented low-temperature fermentation processes effectively reduce impurities while maintaining FDA GMP compliance, creating a competitive edge in pharmaceutical applications. The technical ethanol segment has found success in industrial applications, particularly in cleaning solutions and paint solvents, where its renewable nature offers sustainable alternatives to petroleum-based products. However, manufacturers of extra neutral alcohol face increasingly stringent food defense requirements, resulting in higher compliance costs that particularly impact smaller producers' ability to enter the market.

By Application: Pharmaceutical Growth Reshapes Market Economics

The pharmaceutical and nutraceutical segment is projected to grow at a CAGR of 5.82% through 2030, emerging as the fastest-growing segment in the grain alcohol market. This remarkable growth is primarily attributed to the increasing incorporation of grain alcohol in drug formulations, medical-grade disinfectants, and homeopathic products, where manufacturers prioritize product purity over cost considerations. The segment's evolution has fundamentally reshaped the grain alcohol industry by creating substantial demand for specialized production facilities and stringent quality certifications, enabling manufacturers to command significant price premiums in the market.

The beverage segment continues to maintain its market leadership with a 45.36% share in 2024, reflecting long-established consumption patterns in the industry. However, the segment faces increasing challenges to its profit margins due to rising regulatory compliance requirements and associated costs. Additionally, the growing consumer preference for low-alcohol and alcohol-free alternatives has begun to impact traditional beverage market dynamics, prompting manufacturers to reassess their product portfolios and market strategies.

Geography Analysis

North America remains the undisputed market leader, commanding a significant 36.13% market share in 2024. This dominance stems from decades of investment in regulatory frameworks and production infrastructure that have created a robust and efficient market environment. The U.S. Energy Information Administration's projections highlight the market's stability, with ethanol production expected to reach 1.06 million barrels per day in 2025 and 1.05 million barrels per day in 2026. While the region faces export challenges, with projections showing a decline of 130,000 barrels per day, North American producers are actively adapting to market changes. The flourishing craft distillery segment has successfully created premium market niches, helping offset margin pressures in commodity ethanol. Furthermore, producers are strategically positioning themselves by adopting carbon capture technologies, enabling them to capitalize on environmental benefits in markets with established carbon pricing mechanisms.

Asia-Pacific has established itself as the market's growth powerhouse, demonstrating an impressive 5.39% growth rate through 2030. This remarkable expansion is primarily driven by progressive government policies supporting biofuel mandates and robust industrial demand growth. India has emerged as a key player in Asian ethanol production, with government initiatives ambitiously targeting E-20 blending by 2025. Despite experiencing a temporary 2% production decrease in 2024 due to feedstock constraints, the region continues to attract substantial capacity investments, fundamentally reshaping global market dynamics and setting new industry standards.

Europe maintains its strategic market position through a sophisticated regulatory landscape, particularly through EU Regulation 2019/787, which sets strict standards for agricultural-origin ethyl alcohol and protects geographical indications. The region's spirit drinks sector demonstrates significant economic impact, generating EUR 9.74 billion in exports and providing employment to approximately 1.2 million people. Despite facing challenges from elevated energy costs, the substantial economic benefits continue to drive production investments, underlining Europe's commitment to maintaining its established market presence and traditional production methods.

Competitive Landscape

The grain alcohol market shows a balanced level of consolidation, where larger companies benefit from their ability to meet regulatory requirements and invest in carbon capture technologies. These advantages create natural barriers for smaller companies trying to enter the market. We can see this trend in action through Bunge's USD 8 billion merger with Viterra, which has improved their ability to manage global food, feed, and fuel supply chains while strengthening their logistics and risk management capabilities.

Companies are increasingly using technology to stand out in the market. They are investing in better distillation methods, carbon capture systems, and advanced fermentation techniques to reduce costs and meet environmental standards. A practical example of this is ADM's new digital system for managing grain elevator transportation, which shows how established businesses are using new technology to maintain their competitive edge in logistics and supply chain operations.

New business opportunities are emerging in pharmaceutical-grade production and specialized grain processing, where strict regulations limit competition and companies can charge premium prices for high-quality products. The market's moderate concentration makes it easier for companies to work together, as shown by ADM's partnership with Mitsubishi Corp. This collaboration allows both companies to explore new opportunities in agricultural supply chains by combining their respective strengths.

Grain Alcohol Industry Leaders

Archer Daniels Midland

Green Plains Inc.

Cargill, Inc.

CropEnergies AG

Tereos S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Jagatjit Industries Limited commenced commercial production of ethanol at its newly commissioned 200 KLPD grain-based ethanol distillery plant in Punjab. This development marks a significant expansion into the ethanol segment, supporting India's green fuel initiatives.

- December 2024: Godavari Biorefineries Limited is investing INR 130 crore in a new corn and grain-based distillery to increase its ethanol production capacity. This dual-feedstock facility aligns with India's renewable energy objectives.

- September 2024: McDowell’s and Co launched its premium X Series, featuring single grain vodka, dry gin, citron rum, and dark rum. This range targets evolving consumer preferences and the growing cocktail culture in India, blending Indian and global ingredients for sophisticated drinking experiences.

Global Grain Alcohol Market Report Scope

| Corn |

| Wheat |

| Barley |

| Rye |

| Other |

| Ethanol |

| Polyols |

| Food |

| Beverage |

| Pharmaceutical and Nutraceutical |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Corn | |

| Wheat | ||

| Barley | ||

| Rye | ||

| Other | ||

| By Type | Ethanol | |

| Polyols | ||

| By Application | Food | |

| Beverage | ||

| Pharmaceutical and Nutraceutical | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the grain alcohol market?

The grain alcohol market size reached USD 13.84 billion in 2025 and is projected to hit USD 17.18 billion by 2030.

Which region is expanding fastest in grain alcohol demand?

Asia-Pacific is forecast to grow at 5.39% CAGR through 2030, propelled by E10 and E20 blending mandates and rising industrial use.

Why are pharmaceutical applications important for grain alcohol producers?

Pharmaceutical-grade ethanol commands higher prices due to 99.9% purity requirements, insulating producers from commodity swings and lifting overall margins.

Which grain is gaining traction beyond corn?

Rye is growing fastest at 5.74% CAGR as craft distillers seek distinctive flavor profiles and gluten-free positioning.

How are technology upgrades affecting production economics?

Heat-recovery and advanced column designs cut energy use by up to 23% and water draw by up to 55%, improving yields and lowering operating costs.

Page last updated on: