RFID-Enhanced Recyclable Paperboard Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

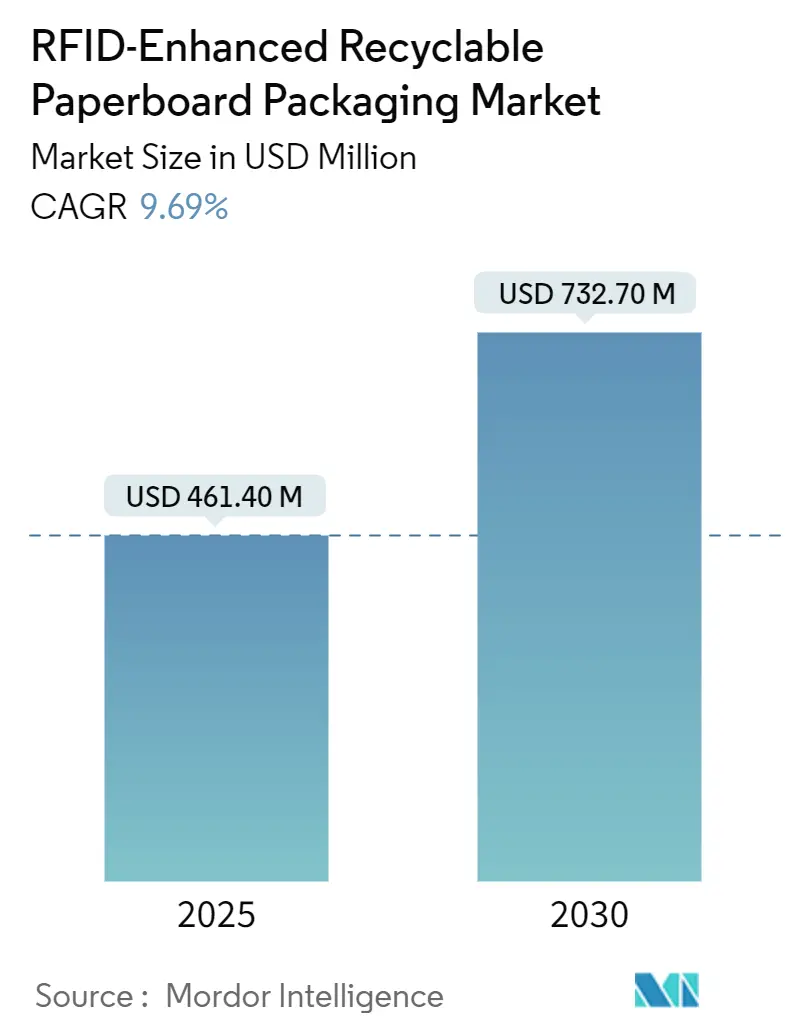

| Market Size (2025) | USD 461.40 Million |

| Market Size (2030) | USD 732.70 Million |

| Growth Rate (2025 - 2030) | 9.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

RFID-Enhanced Recyclable Paperboard Packaging Market Analysis by Mordor Intelligence

The RFID-Enhanced Recyclable Paperboard Packaging market size stands at USD 461.4 million in 2025 and is forecast to reach USD 732.7 million by 2030, reflecting a 9.69% CAGR over the period. The growth trajectory of the RFID-Enhanced Recyclable Paperboard Packaging market is propelled by retail mandates for item-level tagging, pharmaceutical anti-counterfeiting rules, and e-commerce requirements for real-time visibility. Asia-Pacific leads volume uptake, while European sustainability incentives accelerate fiber-based conversion. Corrugated boxes dominate adoption because their multilayer structure optimizes antenna performance, and ultra-high-frequency RAIN RFID holds the largest frequency share due to cost-efficient long-range reads. Producers are balancing functionality with recyclability by shifting from plastic-backed inlays to fiber-based or printed antennas that pass established repulpability tests.

Key Report Takeaways

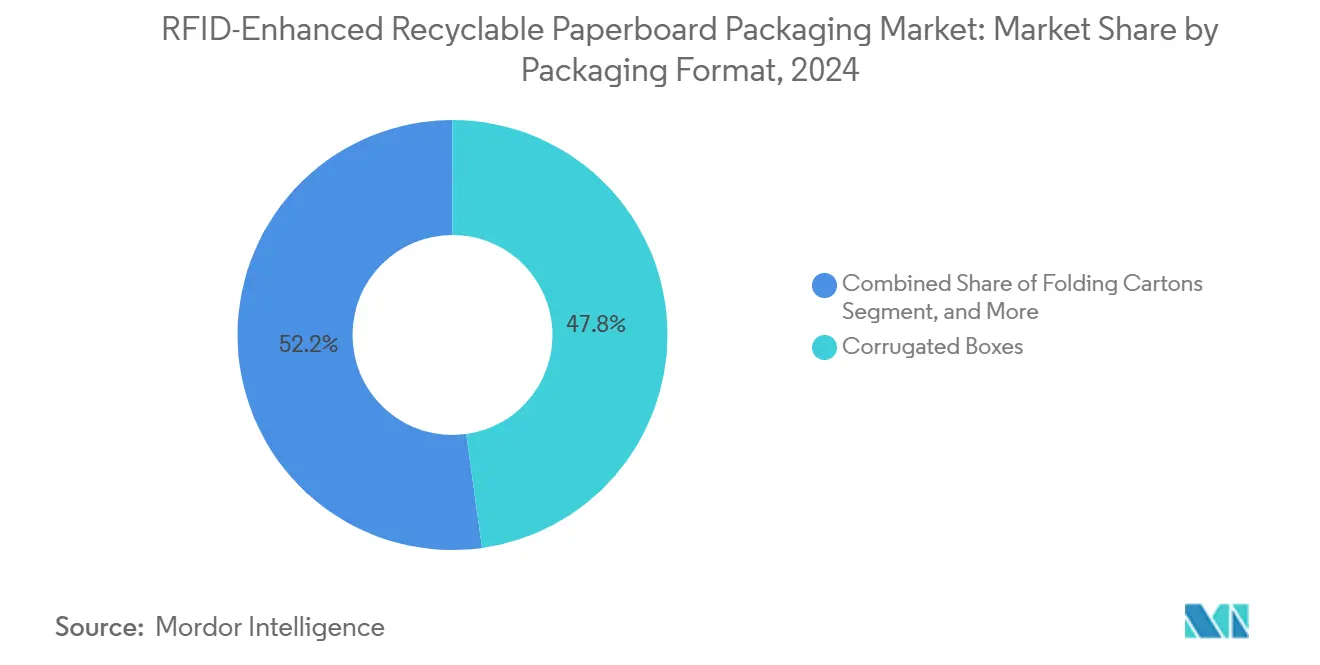

- By packaging format, corrugated boxes captured 47.81% of the RFID-enhanced recyclable paperboard packaging market share in 2024.

- By RFID frequency band, the RFID-enhanced recyclable paperboard packaging market size for NFC is projected to grow at a 9.84% CAGR between 2025-2030.

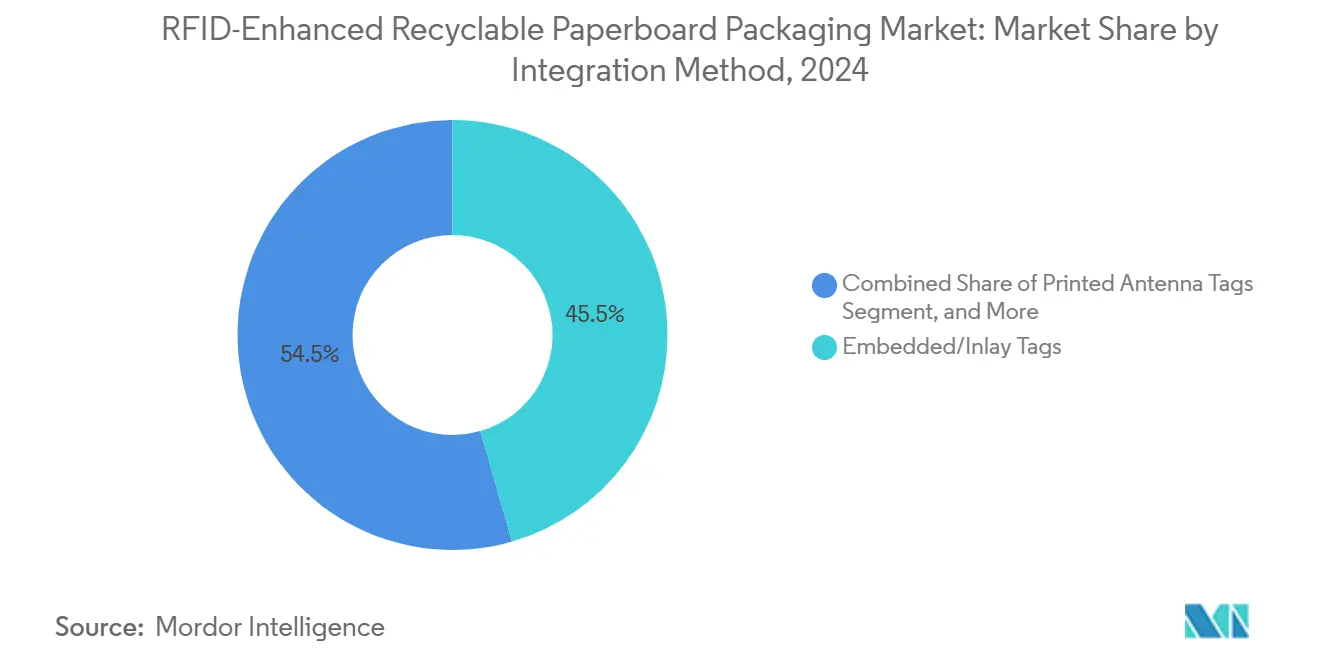

- By integration method, embedded and inlay solutions captured 45.53% of the RFID-enhanced recyclable paperboard packaging market share in 2024.

- By end-use industry, the RFID-enhanced recyclable paperboard packaging market size for healthcare and pharmaceuticals is projected to grow at a 10.81% CAGR between 2025-2030.

- By geography, Asia-Pacific captured 38.32% of the RFID-enhanced recyclable paperboard packaging market share in 2024.

Global RFID-Enhanced Recyclable Paperboard Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Retail mandates for item-level RFID tagging | +1.2% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Anti-counterfeiting regulations in pharmaceuticals and spirits | +1.8% | Global, led by FDA and EU regulatory frameworks | Medium term (2-4 years) |

| E-commerce push for real-time supply-chain visibility | +1.4% | Global, concentrated in APAC and North America | Short term (≤ 2 years) |

| Decarbonization credits for fiber-based connected packs | +1.1% | Europe and North America primarily | Long term (≥ 4 years) |

| AI-driven refill/return loops needing trackable cartons | +0.9% | APAC core, spill-over to developed markets | Medium term (2-4 years) |

| 5G Massive-IoT printable antennas on paperboard | +0.8% | APAC and Europe leading deployment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Retail Mandates for Item-Level RFID Tagging

Walmart expanded tagging requirements from apparel to general merchandise, forcing suppliers to embed RFID directly into primary and secondary packaging. Paris Corp. implemented custom inlays and encoding lines to meet the deadline, proving commercial feasibility for mass-volume stationery packs.[1]Packaging World, “Paris Corp. Meets Walmart RFID Tagging Mandate,” packworld.com Comparable mandates from Target and Decathlon are cascading through global supply networks, encouraging brand owners to standardize RFID across entire portfolios. The immediate benefit is higher on-shelf availability, but suppliers are also leveraging captured scan data for demand forecasting and shrinkage reduction. With omnichannel models relying on store-level fulfillment, accurate item visibility is now a revenue-critical capability, accelerating adoption throughout the RFID-Enhanced Recyclable Paperboard Packaging market.

Anti-Counterfeiting Regulations in Pharmaceuticals and Spirits

FDA serialization guidance endorses RFID to encode standardized numerical identifiers that authenticate every drug unit. Brand owners integrate the chip between paperboard plies, preserving tamper evidence while eliminating added plastic. The EU Falsified Medicines Directive and expanding regulations on premium spirits create parallel demand spikes. Beyond compliance, serialized RFID supports automated pharmacy dispensing and traceable cold-chain management. Healthcare providers report fewer medication errors when nurses validate bedside dosing via RFID-enabled cartons, reinforcing patient-safety drivers. As many generic producers update packaging lines, folding cartons with embedded inlays become the fastest-growing format inside the RFID-Enhanced Recyclable Paperboard Packaging market.

E-Commerce Push for Real-Time Supply-Chain Visibility

Online sellers rely on dark-store micro-fulfillment centers where cycle times are measured in minutes. Avery Dennison executed the largest single-wave RFID roll-out for a global logistics provider handling 2 billion parcels annually. Embedded UHF tags in corrugated shippers feed data lakes that power AI-driven slotting and routing decisions. Brands link serialized IDs to mobile-optimised landing pages, letting consumers confirm authenticity or arrange returns with one scan. This digital layer turns otherwise commoditized paperboard into an always-connected asset, raising switching costs and solidifying growth prospects for the RFID-Enhanced Recyclable Paperboard Packaging market.

Decarbonization Credits for Fiber-Based Connected Packs

EU taxonomy now recognises carbon benefits of replacing plastic labeling with fiber alternatives. Pulp and paper companies must renew 3.2% of capacity annually to meet 2050 net-zero scenarios, leading to large board-mill investments such as Stora Enso’s EUR 1 billion upgrade at Oulu. Corporate buyers claim scope-3 reductions when adopting recyclable RFID solutions. Carbon credit trading platforms have begun to differentiate between paperboard with metallised inlays and printed conductive ink antennas, steering demand toward low-impact designs. Finance-linked sustainability targets therefore directly increase tender volumes for RFID-ready recyclable packaging.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High incremental tag and conversion cost | -0.7% | Global, most acute in price-sensitive markets | Short term (≤ 2 years) |

| Signal attenuation from moisture and liquids | -0.5% | Global, particularly challenging in food and beverage | Medium term (2-4 years) |

| Recycling-stream contamination by metallic antennas | -0.4% | Europe and North America with strict recycling standards | Medium term (2-4 years) |

| Lack of global RFID kill/deactivation standards | -0.3% | Global, hindering cross-border implementations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Incremental Tag and Conversion Cost

Passive UHF inlays fell below USD 0.05, yet tag plus application still adds meaningful unit cost for low-margin SKUs. Wiley research shows copper antennas can halve material expense, but commercial converters need volume commitments to switch tooling. Small brands lack capex to retrofit lines, slowing penetration in emerging markets. Consolidation around global suppliers like Avery Dennison enables scale economies, but also leaves buyers exposed to supply imbalance risk. Over the forecast horizon, cost declines partially offset the restraint, yet pricing remains a gating factor for the RFID-Enhanced Recyclable Paperboard Packaging market in price-sensitive regions.

Signal Attenuation from Moisture and Liquids

Water absorbs radio waves, reducing read reliability on fresh produce, meat, and dairy packs. Controlled trials in refrigerated sea containers showed read rates sliding to 57.1% on frozen bread versus 97.6% on canned vegetables. Printed low-dielectric spacers and antenna tuning improve performance, but require application-specific design, increasing engineering effort. Until universal moisture-robust designs mature, some food processors will delay full conversion, muting near-term upside for the RFID-Enhanced Recyclable Paperboard Packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Format: Corrugated Dominance Drives Market Structure

Corrugated boxes contributed 47.81% of RFID-Enhanced Recyclable Paperboard Packaging market size in 2024, reflecting their prevalence in e-commerce shipping. Corrugated flutes provide a natural spacer that improves coupling efficiency between tag and reader. WestRock documented successful repulping of fiber-backed inlays, mitigating contamination worries. Folding cartons, used widely in pharmaceuticals, post a 10.43% CAGR, powered by serialized drug mandates. The segment benefits from thinner substrates that still permit embedding conductive paths without compromising crease lines. Sleeve and tray formats serve quick-service outlets seeking anti-theft and quick scan at point-of-sale. Point-of-purchase displays emerge as experiential touchpoints where NFC enables gamified promotions. Together, these developments reinforce the central role of corrugated yet diversify revenue sources within the RFID-Enhanced Recyclable Paperboard Packaging market.

Corrugated users now specify printed antennas to avoid aluminium waste, while premium spirits adopt high-frequency NFC overlays for consumer storytelling. Logistics firms require dual-frequency packs combining UHF for warehouse sweeps and NFC for customer interaction. As costs fall, hybrid multilayer designs gain traction, accelerating addressable volume. Consequently, corrugated keeps value leadership, but folding cartons harvest the fastest incremental gains, positioning both as complementary growth engines for the RFID-Enhanced Recyclable Paperboard Packaging market.

By RFID Frequency Band: UHF Dominance Reflects Performance Advantages

UHF held 58.04 of % RFID-Enhanced Recyclable Paperboard Packaging market share in 2024 due to long read range and EPCglobal alignment. Warehouses deploy portal readers that capture hundreds of tags every second, unlocking labor savings. NFC rises fastest at 9.84% CAGR, appealing to brand marketers who value direct phone engagement. Luxury labels encode origin certificates into cartons to fight counterfeits. LF remains niche for metal-heavy environments but secures loyal demand in tools and automotive spares. Hybrid designs allow the same tag to communicate in both UHF and HF, creating new user stories while optimising SKU consolidation.

Complementary advances in 5G and edge computing spur interest in mid-band sub-6 GHz sensors integrated into paperboard, yet commercial rollout lags research prototypes. For the forecast period, UHF sustains volume dominance, NFC claims interactive packaging opportunities, and printed antennas push cost boundaries, ensuring balanced expansion of the RFID-Enhanced Recyclable Paperboard Packaging market.

By Integration Method: Embedded Solutions Lead Market Adoption

Embedded or inlay-sandwiched tags controlled 45.53% of RFID-Enhanced Recyclable Paperboard Packaging market size in 2024.[2]Sappi, “Sappi and ISBC bring together digital and paper sectors,” sappi.com The approach protects chips from mechanical stress, suits high-speed die-cutting, and maintains surface print quality. Printed antennas, though fastest with 9.37% CAGR, confront variability in conductive ink uniformity. Advances in primer coatings and sintering now deliver near-metal performance, closing the gap. External labels persist as retrofit options for legacy lines but hinder recyclability and aesthetics.

Growing sustainability scrutiny shifts procurement towards fiber-based ISBC® paper where antenna conductors deposit directly onto cellulose. Converter trials demonstrate throughput parity with standard flexo, suggesting printed solutions will cross the cost inflection point by 2027. Nevertheless, mission-critical items like pharma blister wallets stay with embedded inlays for assured readability. This dual-track evolution keeps the integration landscape dynamic in the RFID-Enhanced Recyclable Paperboard Packaging market.

By End-Use Industry: Food and Beverage Leadership Reflects Scale Advantages

Food and beverage accounted for 32.67% of RFID-Enhanced Recyclable Paperboard Packaging market size in 2024, fueled by omnichannel grocery and convenience chains. RFID allows automatic stock rotation, reducing markdowns. Japan’s METI pilot cut food waste while raising inventory accuracy above 98%. Healthcare shows 10.81% CAGR as unit-level drug traceability and temperature logging converge. Serialization timelines in the United States and EU anchor long-term demand visibility. Apparel, consumer electronics, and third-party logistics contribute diversified revenue hedges, each exploiting RFID for shrink reduction and speed.

As retail subscription models flourished, beverage brands trial trackable multipack sleeves that notify hubs when empties are ready for collection, embedding circular flows. Healthcare pilots add humidity sensors to folding cartons for biologics. The heterogeneity of use cases ensures balanced exposure across defensive and discretionary sectors, supporting resilience in the RFID-Enhanced Recyclable Paperboard Packaging market.

Geography Analysis

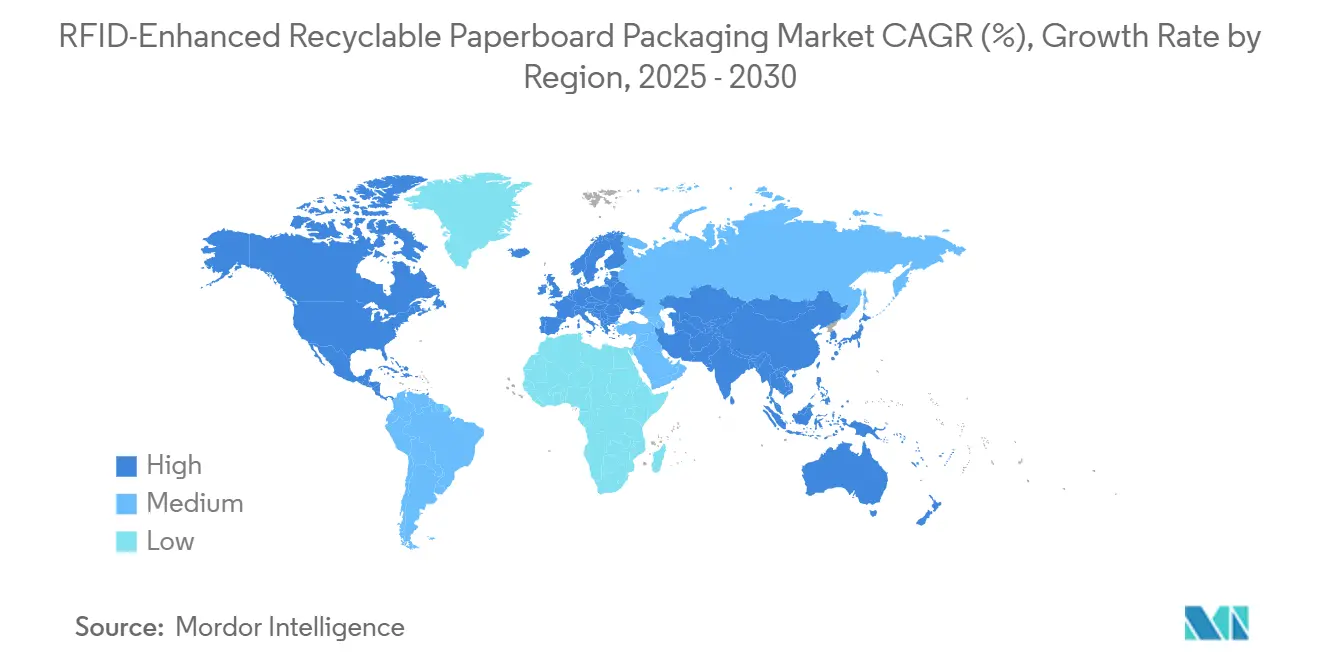

Asia-Pacific captured 38.32% revenue in 2024 and posts the highest 11.14% CAGR, driven by manufacturing scale, supportive policy, and 5G infrastructure. China hosts most tag fabrication capacity, lowering costs and accelerating adoption. Japan’s convenience chains embed RFID in every rice ball sleeve, proving high-volume economics. South Korea commercializes printable antennas aligned with its updated semiconductor roadmap.

North America secures a strong position, underpinned by Walmart’s sweeping mandate and the FDA’s clear serialization playbook.[3]Office of Regulatory Affairs, “CPG Sec. 400.210,” fda.gov Retailers leverage existing EPCIS data layers to integrate sustainability metrics. Converters partner with recyclers to certify tag removability, aligning with state-level extended producer responsibility laws.

Europe remains the sustainability vanguard. EU carbon pricing and circular-economy directives drive fiber-based smart packaging. Stora Enso’s Oulu conversion underpins regional supply, while GS1 guidance harmonizes pulp product identification. Government subsidies for 5G testbeds in Germany and Finland nurture next-gen printed antenna ventures.

Growth in South America, the Middle East, and Africa accelerates from low bases as e-commerce expands. Multinationals roll out off-the-shelf folded-carton kits with pre-encoded inlays, avoiding on-site capex. As import duties ease and recycling regulations strengthen, these regions become future growth corridors for the RFID-Enhanced Recyclable Paperboard Packaging market.

Competitive Landscape

The RFID-Enhanced Recyclable Paperboard Packaging market remains moderately fragmented. Avery Dennison, Stora Enso, Smurfit WestRock, Sappi, and CCL Industries anchor top-tier positions, together holding under 40% combined revenue, which leaves room for mid-sized innovators. Avery Dennison’s Intelligent Labels segment reached USD 850 million and grew nearly 20% organically, benefiting from apparel and logistics roll-outs. Its vertically integrated antenna printing and IC-mounting lines deliver cost leadership.

Stora Enso leverages renewable board chemistry to differentiate. The Oulu site conversion gives it 750 kiloton annual capacity dedicated to high-barrier cartonboard compatible with embedded RFID, positioning the firm as a one-stop partner to CPGs targeting plastic-free pledges. WestRock funnels material insights from its repulping studies into design guidelines that reassure brand owners on recyclability.

CCL Industries captured closed-loop opportunities by integrating RFID into reusable quick-service trays. Sappi advances 100% fiber-based ISBC paper, while specialized start-ups like PragmatIC Print pioneer flexible ICs that conform to thin-wall sleeves. Competitive intensity centers on lowering tag cost, improving recycled fiber yield, and integrating environmental sensing, ensuring continuous innovation throughout the RFID-Enhanced Recyclable Paperboard Packaging market.

RFID-Enhanced Recyclable Paperboard Packaging Industry Leaders

Stora Enso Oyj

Smurfit WestRock plc

International Paper Company

Avery Dennison Corporation

R.R. Donnelley & Sons Company (RRD)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Stora Enso began ramp-up of its EUR 1 billion consumer board line at Oulu, targeting full capacity by 2027 and embedding RFID-ready surface characteristics.

- October 2024: Avery Dennison posted 17% adjusted EBITDA margin in Intelligent Labels after large apparel and general merchandise expansions.

- September 2024: Avery Dennison Investor Day highlighted material science plus digital ID roadmap for waste reduction and recycling-ready labels.

- August 2024: Paris Corp. deployed RFID across stationery ranges to satisfy Walmart tagging rules in collaboration with FineLine Technologies.

Global RFID-Enhanced Recyclable Paperboard Packaging Market Report Scope

| Corrugated Boxes |

| Folding Cartons |

| Paperboard Sleeves and Trays |

| Point-of-Purchase Displays |

| Low Frequency (LF) |

| High Frequency / NFC |

| Ultra-High Frequency (UHF / RAIN) |

| Embedded/Inlay Tags |

| Printed Antenna Tags |

| External RFID Labels/Stickers |

| Food and Beverage |

| Healthcare and Pharmaceuticals |

| Consumer Electronics |

| Apparel and Footwear |

| Logistics and 3PL |

| Other End-Use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Packaging Format | Corrugated Boxes | ||

| Folding Cartons | |||

| Paperboard Sleeves and Trays | |||

| Point-of-Purchase Displays | |||

| By RFID Frequency Band | Low Frequency (LF) | ||

| High Frequency / NFC | |||

| Ultra-High Frequency (UHF / RAIN) | |||

| By Integration Method | Embedded/Inlay Tags | ||

| Printed Antenna Tags | |||

| External RFID Labels/Stickers | |||

| By End-Use Industry | Food and Beverage | ||

| Healthcare and Pharmaceuticals | |||

| Consumer Electronics | |||

| Apparel and Footwear | |||

| Logistics and 3PL | |||

| Other End-Use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the RFID-Enhanced Recyclable Paperboard Packaging market by 2030?

The market is forecast to reach USD 732.7 million by 2030, expanding at a 9.69% CAGR.

Which region leads adoption of RFID-enabled recyclable paperboard?

Asia-Pacific holds 38.32% share and posts the fastest 11.14% CAGR due to manufacturing concentration and supportive policy.

Why are corrugated boxes central to RFID packaging roll-outs?

Corrugated structure optimises antenna performance and represents 47.81% of 2024 revenue, making it the dominant format.

How do regulations influence uptake in pharmaceuticals?

FDA serialization rules endorse RFID at unit level, driving a 10.81% CAGR for healthcare applications.

What technology trend will most reduce tag cost?

Printed conductive ink antennas on paperboard are advancing toward large-scale production, promising sub-USD 0.03 tags and improved recyclability.

Page last updated on: