Foldable Gift Paperboard Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

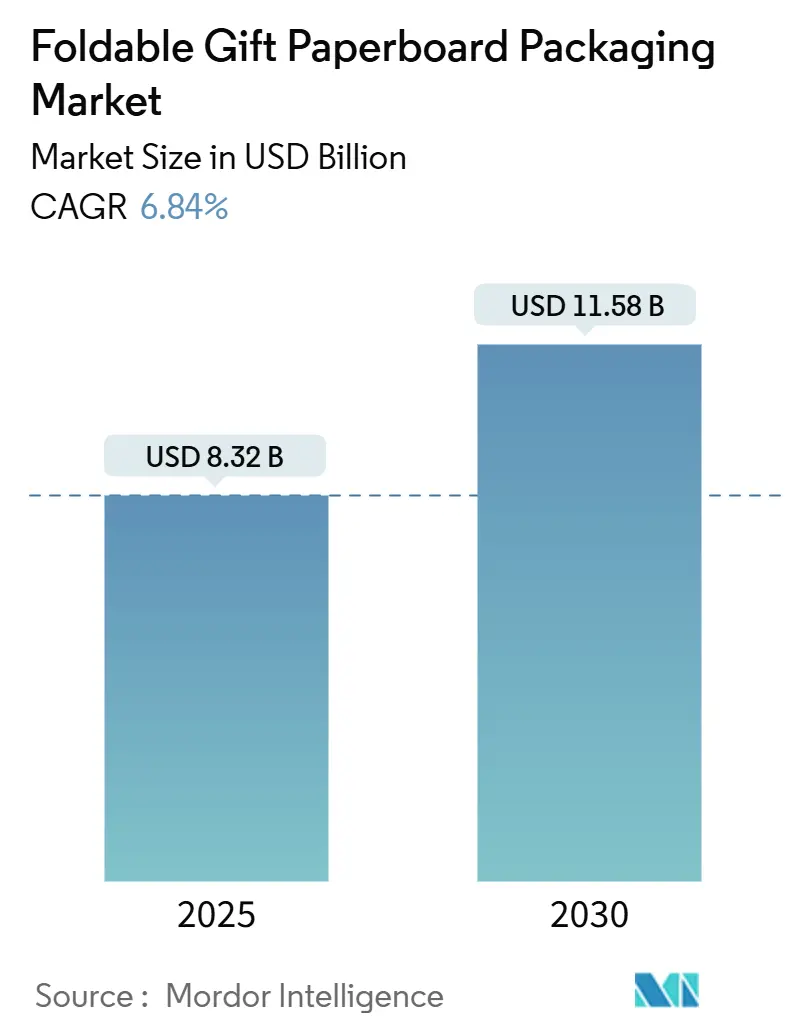

| Market Size (2025) | USD 8.32 Billion |

| Market Size (2030) | USD 11.58 Billion |

| Growth Rate (2025 - 2030) | 6.84% CAGR |

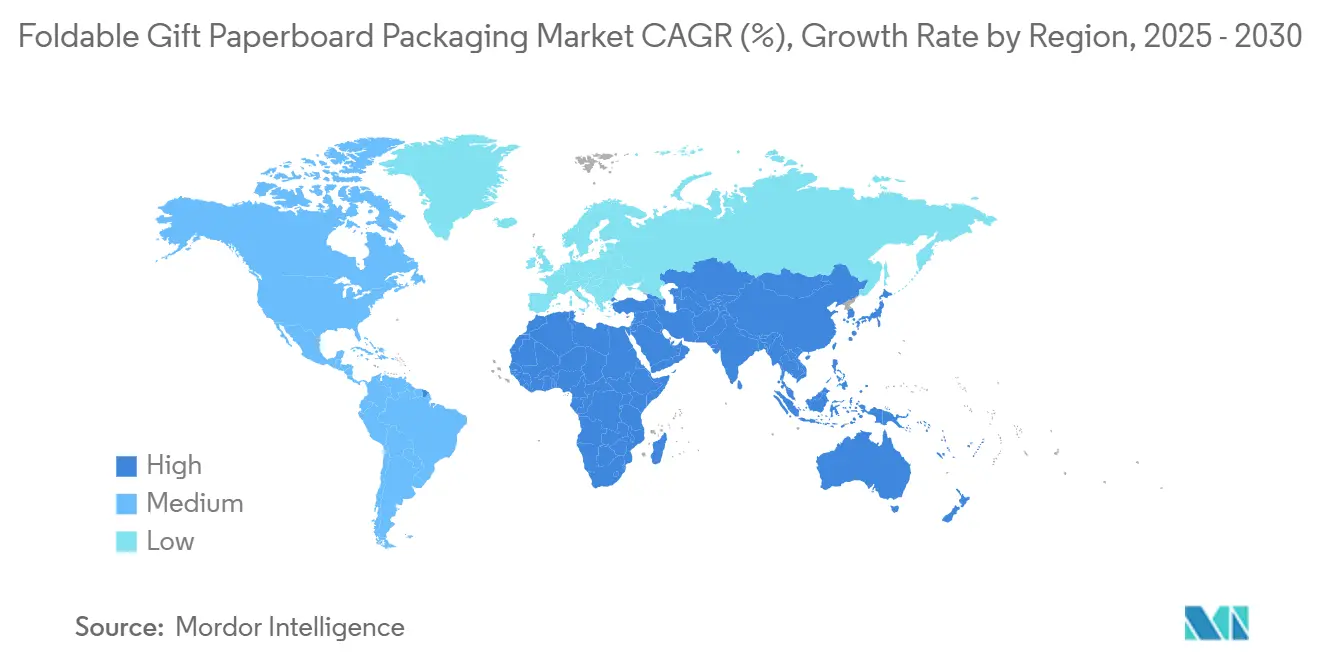

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Foldable Gift Paperboard Packaging Market Analysis by Mordor Intelligence

The foldable gift paperboard packaging market size stands at USD 8.32 billion in 2025 and is projected to reach USD 11.58 billion by 2030, reflecting a 6.84% CAGR. This trajectory underscores the sector’s resilience as brands replace single-use plastics, leverage premium positioning strategies, and fulfil surging e-commerce demand. Intensifying regulatory actions on plastic, brand-owner investment in premium unboxing, and advances in nano-clay barrier coatings collectively expand addressable volumes. Parallel mega-mergers deliver scale economies that temper cost pressures from volatile virgin fiber pricing and energy shocks. Regional momentum is led by Asia-Pacific, where rising middle-class consumption and new capacity underpin both the largest and fastest-growing share of the foldable gift paperboard packaging market.

Key Report Takeaways

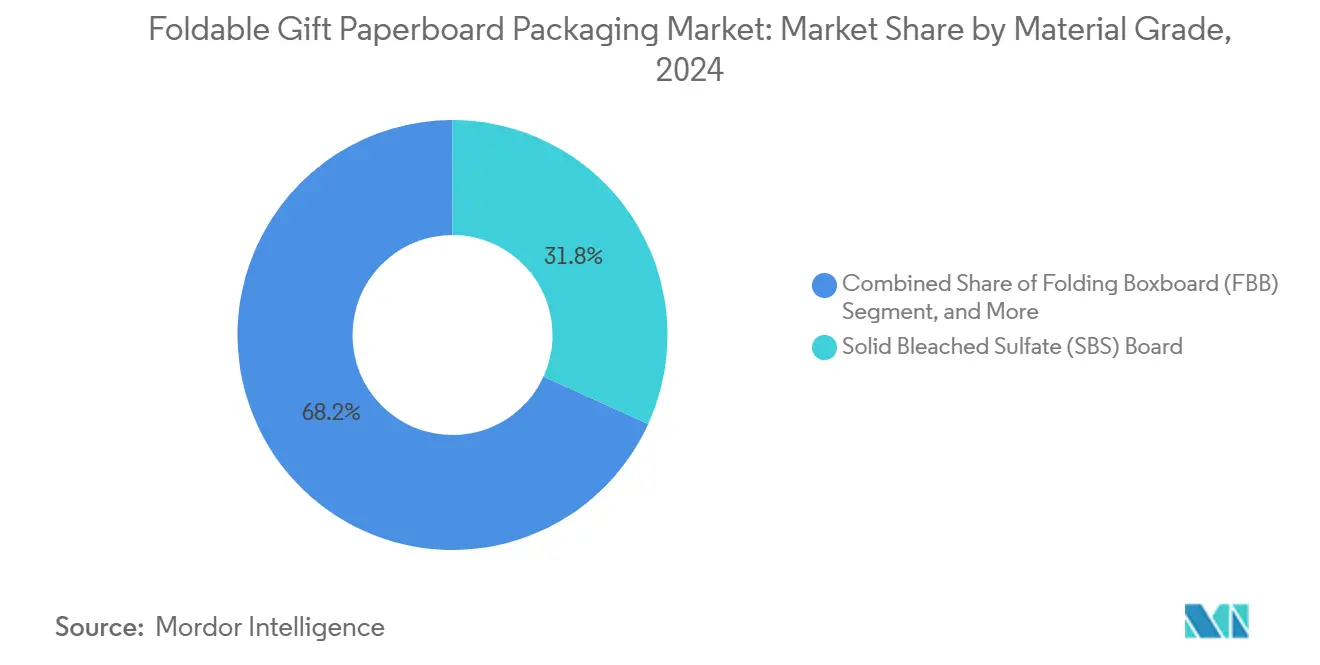

- By material grade, solid bleached sulfate board captured 31.79% of the foldable gift paperboard packaging market share in 2024.

- By end-use industry, the foldable gift paperboard packaging market size for the electronics and gadgets segment is projected to grow at a 7.47% CAGR between 2025-2030.

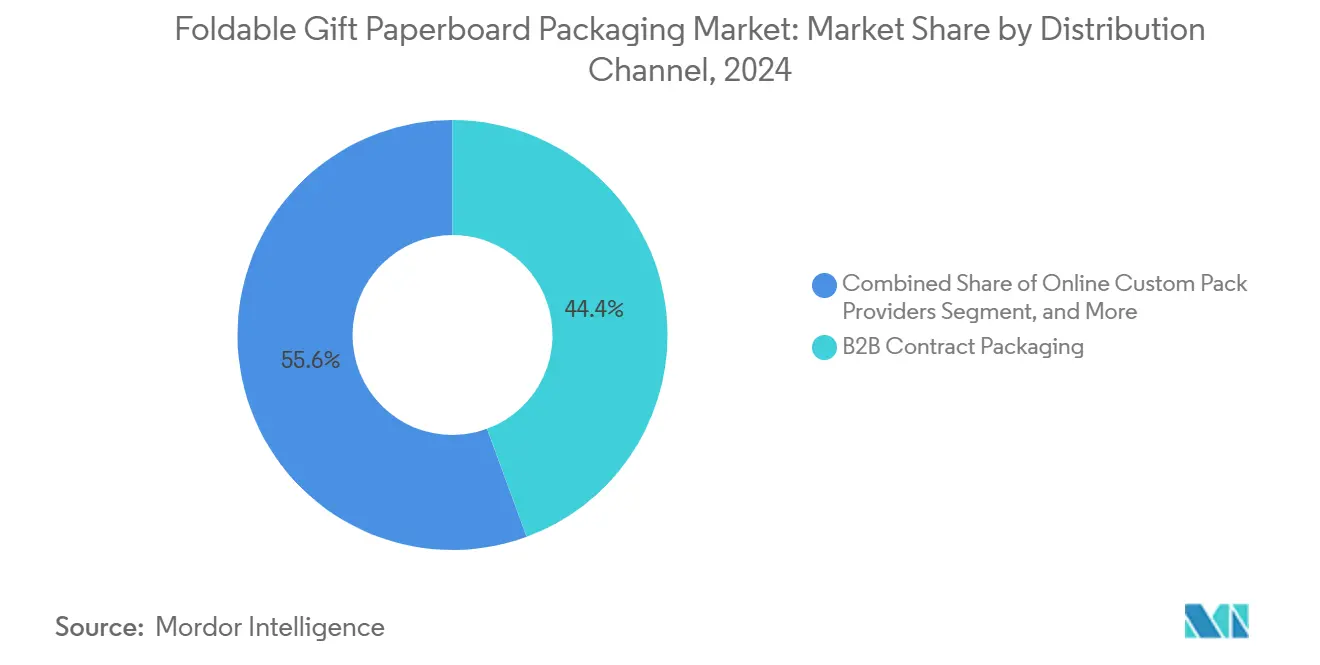

- By distribution channel, B2B contract packaging captured 44.38% of the foldable gift paperboard packaging market share in 2024.

- By geography, the foldable gift paperboard packaging market size for the Asia-Pacific segment is projected to grow at a 7.62% CAGR between 2025-2030.

Global Foldable Gift Paperboard Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating ban on single-use plastics | +1.2% | EU, North America, global spillover | Medium term (2-4 years) |

| Brand-owner push for premium unboxing experiences | +0.8% | North America, EU luxury, expanding APAC | Short term (≤2 years) |

| E-commerce demand for decorative protective mailers | +0.9% | Global; highest in APAC and North America | Short term (≤2 years) |

| Converters’ shift toward digital printing short-runs | +0.7% | North America and EU, technology transfer to APAC | Medium term (2-4 years) |

| Nano-clay barrier coatings enabling food-grade gift packs | +0.6% | Early adoption in developed markets | Long term (≥4 years) |

| Integration of NFC tags for experiential gifting | +0.5% | North America, EU, urban APAC | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Accelerating Ban on Single-Use Plastics

Global regulatory momentum is removing plastics from gift packaging lines. The EU’s Regulation 2025/40 mandates 100% recyclable packaging by 2030 while setting a 15% waste-reduction target by 2040.[1]European Commission, “Regulation 2025/40,” europa.eu The U.S. General Services Administration now prioritizes plastic-free options in federal procurement, explicitly citing corrugated and paperboard materials. Graphic Packaging replaced 450 million plastic packs with paperboard in 2023, underscoring the commercial shift. Industry compliance deadlines accelerate converter investment in barrier coatings that preserve recyclability. These frameworks collectively lift baseline demand in the foldable gift paperboard packaging market.

Brand-Owner Push for Premium Unboxing Experiences

Academic research shows complex packaging elevates perceived product quality and user satisfaction. Luxury and direct-to-consumer brands, therefore, deploy multi-sensory formats, textured substrates, magnetic closures, and layered reveals, best executed with high-graphics paperboard rather than plastic. Mayr-Melnhof Karton’s GreenPeel solution exemplifies the marriage of sustainability and aesthetics. Shareable unboxing moments drive organic social media amplification, validating incremental spend despite 15–25% higher material costs.

E-commerce Demand for Decorative Protective Mailers

The global shift to e-commerce calls for dual-purpose packs that shield products in transit yet delight on arrival. McKinsey identifies paper formats as the primary beneficiaries of this channel shift. Chinese folding boxboard already represents 80% of the nation’s USD 3.4 billion packaging exports in response to the requirement. Electronics brands in particular rely on engineered foldable gift paperboard structures that blend cushioning with premium presentation.

Converters’ Shift Toward Digital Printing Short-Runs

Digital presses unlock economical short runs critical for seasonal and personalized gifting. Stora Enso’s EUR 1 billion (USD 1.08 billion) consumer board upgrade in Finland highlights investment aimed at these high-mix requirements. Digital workflows support just-in-time production, cutting inventory and broadening access for small brands, thereby enlarging the foldable gift paperboard packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile virgin fiber prices | −0.9% | Global; highest in fiber-importing regions | Short term (≤2 years) |

| Supply-chain energy shocks inflating board costs | −0.7% | Europe and other energy-intensive regions | Medium term (2-4 years) |

| Competition from reusable fabric gift wraps | −0.4% | Sustainability-focused North America and EU | Long term (≥4 years) |

| M&A-driven SKU rationalization at big retailers | −0.3% | Global, concentrated in mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Virgin Fiber Prices

Eucalyptus pulp fell toward USD 545 per tonne in China after supply additions, yet remains prone to sharp swings. Smaller converters without long-term contracts face margin compression, whereas vertically integrated players hedge volatility, tilting competitive advantage within the foldable gift paperboard packaging market.

Supply-Chain Energy Shocks Inflating Board Costs

Electricity and natural gas account for a sizable share of mill costs. European producers pay a carbon premium on top of already higher energy tariffs. Billerud’s 2023 report targeted SEK 1.5 billion (USD 0.14 billion) in EBITDA savings partly through energy efficiency upgrades. Regional disparities shift production footprints toward lower-cost geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Grade: SBS Dominance Faces FBB Challenge

Solid Bleached Sulfate Board retained 31.79% of foldable gift paperboard packaging market share in 2024, thanks to superior graphics and barrier attributes suitable for luxury gifting. Folding Boxboard’s 7.59% CAGR through 2030, however, reflects a purchasing pivot toward cost-optimized substrates without sacrificing print quality. The foldable gift paperboard packaging market size for Folding Boxboard applications is on course to add USD 1.2 billion over the forecast window, aided by high e-commerce volumes. Recycled Kraft and White-lined Chipboard address lower-price tiers but seldom meet food-grade or premium branding requirements, capping their advance.

Price sensitivity is overtaking pure performance as converters analyze total cost-to-serve. Chinese exporters illustrate the shift, exporting USD 3.4 billion in folding boxboard during 2023, equivalent to 80% of total board exports.[2]Simon Matthis, “China’s Packaging Materials Exports Fall,” pulpandpapernews.com SBS remains the substrate of choice where tactile finishes, embossing, and specialty coatings command premium shelf appeal, yet mill investments increasingly favor FBB capacity expansion to balance margin and volume in the evolving foldable gift paperboard packaging market.

By End-use Industry: Electronics Disrupts Traditional Hierarchy

Personal care and cosmetics led with 26.51% share of the foldable gift paperboard packaging market size in 2024, driven by an entrenched premium presentation culture. Electronics and gadgets are catching up quickly, expanding at a 7.47% CAGR as product fragility and direct-to-consumer channels demand high-integrity packs that deliver memorable unboxing. Digital device launches often coincide with influencer campaigns, amplifying packaging design visibility and reinforcing shift in spend allocation.

Confectionery and gourmet food rely on seasonal gift cycles that favor rapid-turnover designs. Jewellery and watches sustain a high average revenue per unit, ensuring ample packaging budgets. Corporate promotional gifting emphasizes customization over material complexity, whereas alcohol and spirits navigate varied regulatory constraints yet maintain demand for ornate boxes during festive peaks. This diversity balances cyclical risk and enlarges the foldable gift paperboard packaging market addressable across disparate consumer occasions.

By Distribution Channel: Digital Disruption Accelerates

B2B contract packaging captured 44.38% of 2024 revenue by supplying turnkey solutions to global CPG majors. Online custom pack platforms are eroding incumbent share with a 7.34% CAGR, leveraging web-based design tools, auto-quoting and aggregated print networks to serve SMEs. The foldable gift paperboard packaging industry thus broadens its client base beyond multinationals, spurring incremental order frequency albeit at smaller average run sizes.

In-house brand packaging persists among top beauty and electronics multinationals that seek IP control and cost hurdle elimination. Nonetheless, capital intensity and rapid design cycles often steer mid-tier brands toward external partners. Digital marketplaces heighten competitive transparency on price and turnaround, compelling traditional converters to upgrade front-end interfaces and shorten lead-times to defend accounts.

Geography Analysis

Asia-Pacific’s 37.89% grip on 2024 revenue, combined with a 7.62% CAGR, highlights its dual status as a production epicenter and a consumption hotspot. Nine Dragons Paper’s expansion into Malaysia to 900,000 tonnes annually aligns with regional demand, tracking 4% growth. China’s export decline of 15% to USD 4.5 billion in 2023 signals rising local absorption rather than weakening fundamentals. Japan pursues premium sustainability niches, targeting JPY 650 billion (USD 4.29 billion) in sales from daily-life products by FY2030.[3]Nippon Paper Industries, “Management Briefing 2024,” nipponpapergroup.com India and fast-urbanizing ASEAN states contribute fresh volume, albeit constrained by logistics and fragmented regulation.

North America maintains a high per-capita spend rooted in e-commerce and luxury gifting culture. Federal procurement rules favor paperboard, further supporting the foldable gift paperboard packaging market. Europe mirrors those dynamics but overlays stringent recyclability mandates, driving innovation in barrier coatings and circular design. Energy costs remain a headwind that could catalyze the outsourcing of low-margin runs to Asia unless EU customers pay a sustainability premium.

South America and MEA collectively account for a single-digit share yet offer long-run upside as retail modernization progresses. Currency swings and regulatory unpredictability temper immediate investment. Nonetheless, global majors are positioning via partnerships to capture gradual premiumization, signaling long-range confidence in the foldable gift paperboard packaging market.

Competitive Landscape

Consolidation is reshaping rivalry. International Paper’s USD 7.8 billion purchase of DS Smith and the Smurfit Westrock merger, targeting USD 400 million in synergies, establish two scale leaders. TOPPAN’s USD 1.8 billion acquisition of Sonoco’s thermoformed and flexible assets widens its specialty portfolio. These moves integrate fiber sourcing, board production, and converting, securing cost leverage and cross-regional reach.

Technology is the new battleground. Early adopters of nano-clay coatings and NFC tagging command pricing power in food and luxury verticals. Digital printing lines differentiate through fast artwork swaps and reduced waste. Smaller independents succeed by niche specialization, short-run artistry, sustainability consulting, or rapid prototype turnaround, eschewing volume contests with conglomerates. Competitive intensity remains moderate, with switching costs rooted in design collaboration, supply-chain integration, and sustainability verification, elements that shield incumbents serving the foldable gift paperboard packaging market.

Foldable Gift Paperboard Packaging Industry Leaders

Smurfit Westrock PLC

Graphic Packaging Holding Company

International Paper Company

Mondi PLC

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Smurfit Westrock posted USD 7,656 million Q1 sales and outlined a 500,000-ton capacity closure plan alongside new converting plants to unlock USD 400 million synergies.

- April 2025: Stora Enso began output on its new Oulu consumer board line; Q1 sales rose 9% to EUR 2,362 million (USD 2,556 million) with adjusted EBIT up 17.7%.

- February 2025: Smurfit Westrock reported USD 7.5 billion Q4 sales and USD 319 million net income, confirming smooth integration.

- December 2024: TOPPAN Holdings agreed to buy Sonoco’s thermoformed and flexible business for USD 1.8 billion.

Global Foldable Gift Paperboard Packaging Market Report Scope

| Solid Bleached Sulfate (SBS) Board |

| Folding Boxboard (FBB) |

| Coated Unbleached Kraft (CUK) |

| White-lined Chipboard (WLC) |

| Recycled Kraft Board |

| Personal Care and Cosmetics |

| Confectionery and Gourmet Food |

| Jewellery and Watches |

| Electronics and Gadgets |

| Fashion and Accessories |

| Corporate and Promotional Gifts |

| Alcohol/Spirits |

| B2B Contract Packaging |

| In-house Brand Packaging |

| Online Custom Pack Providers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Material Grade | Solid Bleached Sulfate (SBS) Board | ||

| Folding Boxboard (FBB) | |||

| Coated Unbleached Kraft (CUK) | |||

| White-lined Chipboard (WLC) | |||

| Recycled Kraft Board | |||

| By End-use Industry | Personal Care and Cosmetics | ||

| Confectionery and Gourmet Food | |||

| Jewellery and Watches | |||

| Electronics and Gadgets | |||

| Fashion and Accessories | |||

| Corporate and Promotional Gifts | |||

| Alcohol/Spirits | |||

| By Distribution Channel | B2B Contract Packaging | ||

| In-house Brand Packaging | |||

| Online Custom Pack Providers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the foldable gift paperboard packaging market?

It is valued at USD 8.32 billion in 2025.

How fast is Asia-Pacific growing in foldable gift paperboard packaging?

The region is expanding at a 7.62% CAGR between 2025-2030.

Which material grade is gaining traction against SBS?

Folding Boxboard is the fastest-growing grade at 7.59% CAGR.

Why are electronics brands increasing spend on foldable gift boxes?

Fragile devices shipped direct-to-consumer need protective yet premium unboxing, fueling a 7.47% CAGR in the electronics segment.

How are mega-mergers changing competitive dynamics?

Deals such as International Paper-DS Smith and Smurfit Westrock create scale economies that lower cost per unit and expand global reach.

What technology is enabling food-grade applications in paperboard gifting?

Nano-clay barrier coatings deliver plastic-like moisture protection while remaining recyclable.

Page last updated on: