NFC-Embedded Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

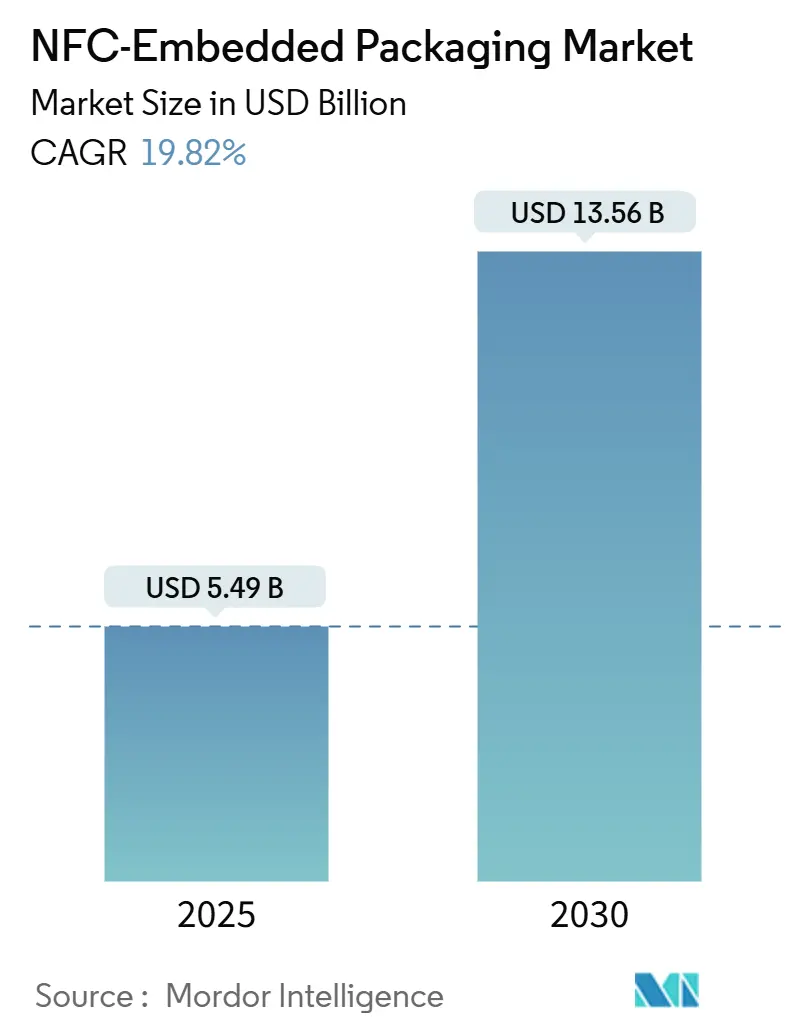

| Market Size (2025) | USD 5.49 Billion |

| Market Size (2030) | USD 13.56 Billion |

| Growth Rate (2025 - 2030) | 19.82% CAGR |

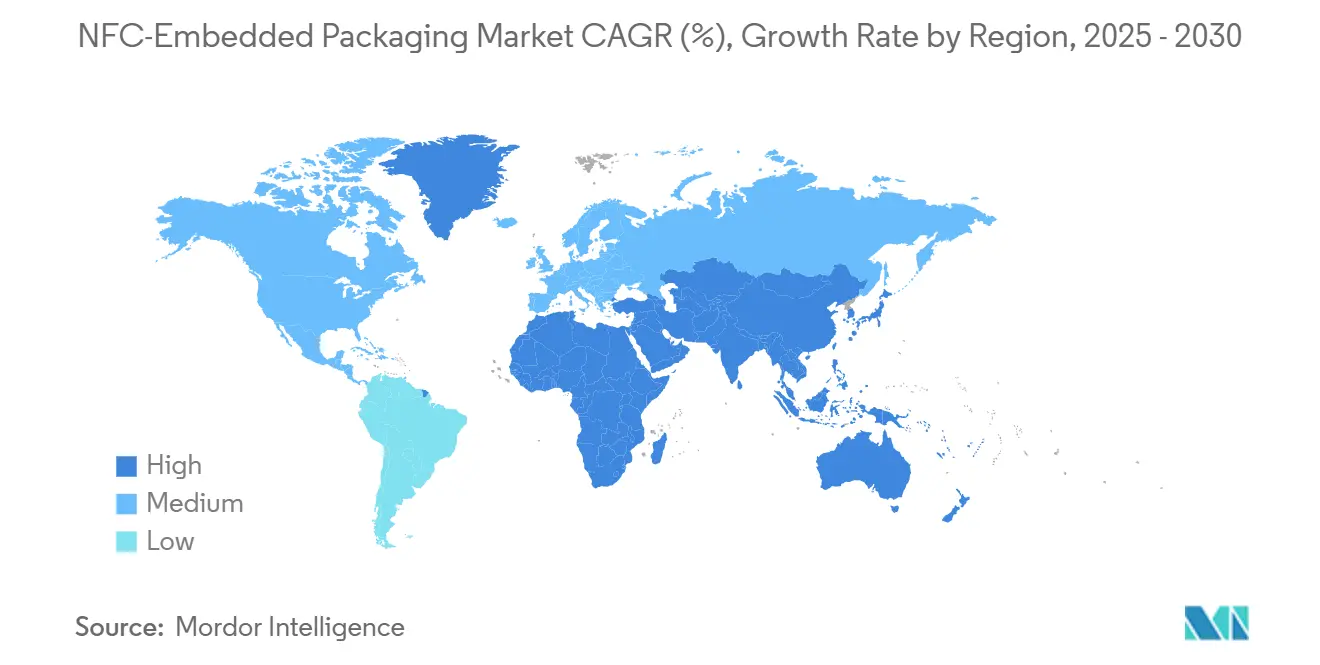

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

NFC-Embedded Packaging Market Analysis by Mordor Intelligence

The NFC-embedded packaging market size stands at USD 5.49 billion in 2025 and is projected to reach USD 13.56 billion by 2030, translating into a sturdy 19.82% CAGR. Persistent demand for item-level visibility, smartphone-driven consumer engagement, and increasingly stringent anti-counterfeiting laws are combining to drive this growth. Ultra-thin printed electronics continue to push unit costs below mass-adoption thresholds, while cloud analytics platforms intensify the need for in-pack data streams. Early adoption across North America and rapid manufacturing scale-up in Asia-Pacific sustain the market’s upward trajectory, and sustainability mandates are steering material innovation toward compostable substrates. Intensifying M&A activity underscores a race to bundle tag hardware with analytics and compliance services.

Key Report Takeaways

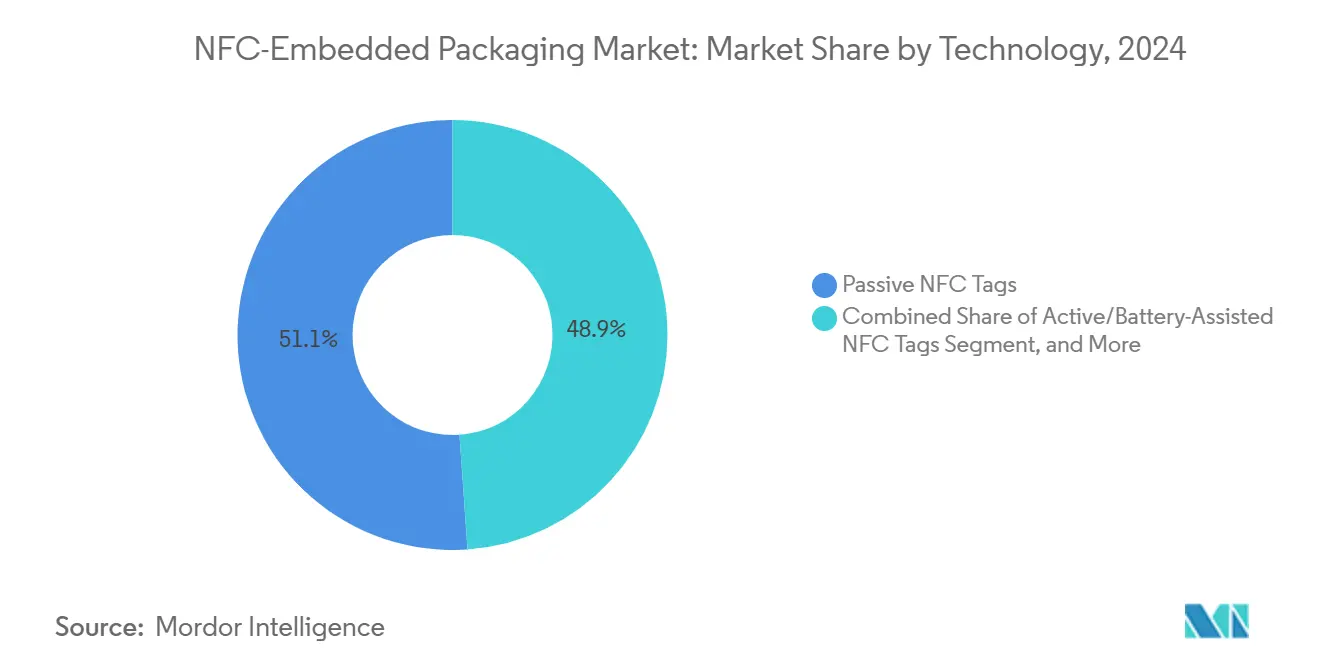

- By technology, passive NFC tags captured 51.12% of the NFC-embedded packaging market share in 2024.

- By end-user industry, the NFC-embedded packaging market size for pharmaceuticals and healthcare is projected to grow at a 20.59% CAGR between 2025-2030.

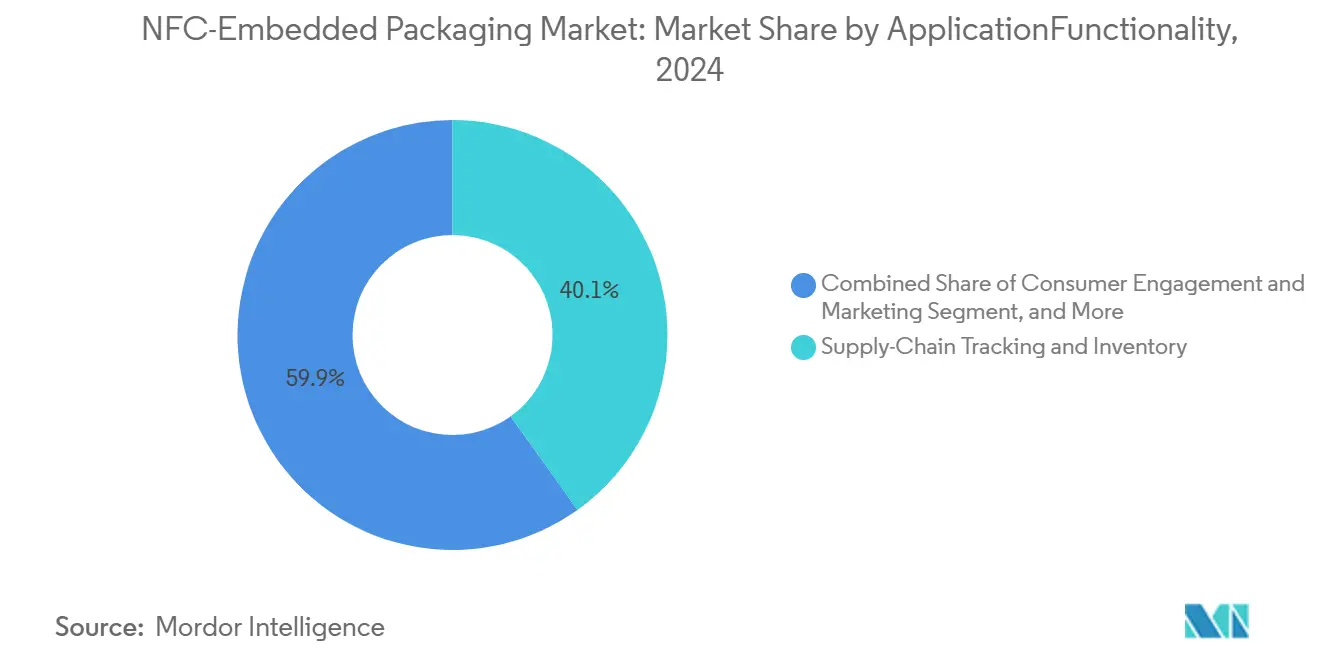

- By functionality, supply-chain tracking captured 40.12% of the NFC-embedded packaging market share in 2024.

- By material, the NFC-embedded packaging market size for biodegradable and compostable substrates is projected to grow at a 23.14% CAGR between 2025-2030.

- By geography, North America captured 34.93% of the NFC-embedded packaging market share in 2024.

Global NFC-Embedded Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone ubiquity enabling tap-and-go packaging interaction | +4.2% | Global with APAC leading adoption | Short term (≤ 2 years) |

| Retailers’ shift to omnichannel inventory accuracy | +3.8% | North America and Europe | Medium term (2-4 years) |

| Stringent pharma anti-counterfeiting mandates (FMD, DSCSA) | +3.5% | EU and North America | Long term (≥ 4 years) |

| IoT analytics demand for real-time in-pack data | +3.1% | Global developed markets | Medium term (2-4 years) |

| Ultra-thin printed electronics reducing tag cost | +2.9% | APAC manufacturing hubs | Short term (≤ 2 years) |

| Emergence of crypto-secured NFC tags for luxury goods | +2.4% | Premium markets worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Smartphone Ubiquity Enabling Tap-and-Go Packaging Interaction

More than 6.8 billion active smartphones create a universal reader infrastructure that allows packaging to become an interactive touchpoint, negating the need for dedicated scanners.[1]GSMA, “The Mobile Economy 2024,” gsma.com Rising contactless habits, reinforced during the pandemic, continue to sustain consumer preference for simple, tap-driven experiences. The Asia-Pacific region benefits most because high smartphone penetration aligns with cost-efficient electronics manufacturing. As brands add NFC labels to everyday items, they unlock real-time authentication, ingredient transparency, and dynamic content updates. These capabilities deepen customer trust and open data pipelines previously inaccessible through static barcodes. Brands gain an owned engagement channel without additional hardware investment, accelerating ROI.

Retailers’ Shift to Omnichannel Inventory Accuracy

Omnichannel models hinge on reliable item-level visibility across stores, warehouses, and last-mile delivery. NFC tags enable instant, line-of-sight-free reads, increasing stock accuracy to 99.5% and reducing shrinkage by up to 15% in high-volume environments. Automated inventory updates during customer handling enable BOPIS fulfillment, dynamic shelf pricing, and fast returns processing. Retailers avoid costly infrastructure overhauls because existing smartphones or handhelds double as readers. Competitive pressures for ever-faster order cycles make real-time data a baseline expectation rather than an optimization layer. Consequently, NFC-embedded packaging becomes both an operational necessity and a customer-experience differentiator.

Stringent Pharma Anti-Counterfeiting Mandates (FMD, DSCSA)

EU and U.S. legislation mandates end-to-end traceability, making NFC-enabled security features compulsory components for prescription drugs.[2]European Medicines Agency, “Falsified Medicines Directive,” ema.europa.eu Tag-level cryptography authenticates products at the patient interface, mitigating a counterfeit medicine trade valued in the billions. Timelines for full compliance extend through 2027, locking in long-term demand. Patient-facing apps add value beyond regulation by enabling dosage reminders and adverse-event reporting, further boosting pharmaceutical interest. As penalties for non-compliance escalate, pharma firms are prioritizing NFC adoption despite higher unit costs.

IoT Analytics Demand for Real-Time In-Pack Data

Enterprises are increasingly integrating packaging into their broader IoT ecosystems to monitor location, temperature, and consumer interactions. NFC-generated data feeds predictive algorithms that drive automated reordering, dynamic pricing, and cold-chain assurance. For perishable pharmaceuticals and foods, maintaining accurate temperature records reduces spoilage and liability exposures. In manufacturing, tags track work-in-process components, improving takt-time measurement. This data granularity elevates operational agility and drives system-wide optimization. Accordingly, NFC-embedded packaging shifts from a functional label to a strategic data node in enterprise networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront system integration costs | -2.8% | Global SME markets | Short term (≤ 2 years) |

| Data-privacy / GDPR compliance concerns | -2.1% | EU and other privacy-regulated regions | Medium term (2-4 years) |

| Global semiconductor substrate shortages | -1.9% | Global supply chains | Short term (≤ 2 years) |

| Fragmented standards for HF-NFC interoperability | -1.6% | Worldwide cross-platform uses | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront System Integration Costs

A full NFC deployment often requires new middleware, analytics dashboards, and ERP connectors that can exceed USD 500,000 for mid-sized operations. Added expenses for staff training and customization inflate the total cost of ownership and delay payback periods. Smaller enterprises, although volume-rich, hesitate to commit capital amid uncertain ROI timelines. Vendors are responding with SaaS-based subscription models to reduce upfront barriers; however, perceived complexity still hinders adoption.

Data-Privacy / GDPR Compliance Concerns

NFC packaging collects consumer interaction data that falls under strict consent protocols in Europe and other privacy-focused jurisdictions. Brands must embed opt-in workflows and anonymization features, adding design overhead. Failure to secure consent risks fines up to 4% of global revenue, deterring risk-averse adopters. While privacy-by-design architecture is emerging, balancing seamless engagement with regulatory rigor remains a delicate task.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Passive Dominance and Active Momentum

Passive NFC labels accounted for a commanding 51.12% share of the NFC-embedded packaging market in 2024, reflecting their cost edge and maintenance-free design. At a median unit price of less than USD 0.10, passives enable broad deployment across everyday consumer goods. Active and battery-assisted tags, although more expensive, are growing at a 22.15% CAGR. These variants harvest energy, extend read ranges, and integrate sensors that unlock cold-chain telemetry and tamper detection. The NFC-embedded packaging market size for active solutions is projected to more than quadruple by 2030 as the cost of printed batteries falls. Hybrid NFC-UHF platforms remain a niche but valuable bridge between retail point-of-sale engagement and warehouse automation, enhancing omnichannel sync efficiency. Manufacturing advances in flexible substrates from APAC lower activation thresholds and help active tags approach cost parity. Consequently, suppliers are tailoring portfolios to tiered functionality, ensuring that every price point carries a clear value proposition.

The competitive dynamic centers on silicon miniaturization and antenna innovation. Foundries are squeezing die areas below 0.3 mm², while roll-to-roll printing tunes impedance to thin paper backings. NXP’s latest NTAG series, for example, couples 128-bit AES encryption with temperature logging, winning multiple design awards in pharma supply chains.[3]NXP Semiconductors, “NFC in Packaging Applications,” nxp.com Start-ups are layering blockchain certificates onto tag memory blocks, targeting high-margin luxury goods. As functionalities multiply, interoperability testing has emerged as a de-facto gatekeeper, with GS1 and ISO standards bodies accelerating certification cycles.

By End-User Industry: Retail Clout Meets Pharma Urgency

Retail and FMCG retained 32.41% revenue share in 2024, benefiting from broad SKU counts that magnify efficiency gains. Supermarkets utilize NFC to minimize self-checkout friction, while apparel chains employ it to prevent return fraud. The NFC-embedded packaging market share for retail is expected to decline slightly by 2030 as other verticals catch up, yet absolute spend will increase due to SKU proliferation. Pharmaceuticals, already advancing at 20.59% CAGR, will narrow the gap quickly as compliance deadlines approach. The NFC-embedded packaging market size for pharma authentication is forecast to hit USD 2.8 billion by 2030, driven by unit-level serialization mandates.

Consumer electronics leverage NFC labels for one-tap warranty activation and quick-start tutorials, trimming support call volumes. Logistics operators insert tags into pallets and totes, enabling automated reconciliation that slashes handling time. Across various verticals, sustainability metrics are now influencing tag adoption, as end-users prefer bio-based substrates that align with ESG goals. Consequently, solution suppliers must speak both operational and sustainability languages to win RFPs.

By Application / Functionality: Tracking Leads, Engagement Surges

Supply-chain tracking retained a leading 40.12% share in 2024, because real-time location data sits at the heart of omnichannel and compliance workflows. Brands pursuing 360-degree visibility integrate NFC reads into WMS, TMS, and ERP layers, shrinking reconciliation cycles from days to seconds. Authentication and anti-counterfeiting sit in second place but carry outsized strategic weight in pharmaceuticals and luxury goods. Meanwhile, consumer engagement applications will log a brisk 21.01% CAGR as marketers replace static QR codes with richer, secured NFC calls to action. The NFC-embedded packaging market size devoted to engagement is expected to cross USD 3 billion by 2030 as app fatigue drives users toward frictionless tap interactions.

Temperature-monitoring tags gain traction as regulators tighten cold-chain audits in biologics. Elsewhere, reusable container tracking enables circular economy models, particularly in the beverage and automotive parts industries. Vendors increasingly offer modular tag designs, allowing brands to layer multiple functionalities, such as tracking, engagement, and sensing, onto a single label, thereby improving economies of scope.

By Material / Substrate: Paper Leadership Faces Green Disruption

Paper labels remain the workhorse substrate, with a 46.81% share in 2024, prized for their low cost, printability, and alignment with curbside recycling streams. However, biodegradable and compostable films often PLA or cellulose blends are sprinting ahead at 23.14% CAGR, propelled by corporate net-zero commitments and legislative bans on single-use plastics. The NFC-embedded packaging market size attributable to compostable substrates is expected to more than triple by 2030, albeit from a relatively small baseline.

Polymer labels still dominate harsh-environment use cases, such as those on refrigerated or oily surfaces. Metal-foil constructions are suitable for tamper-evident pharmaceuticals and high-EMI environments. Innovations in solvent-free conductive inks and laser-cut antennas now allow eco-substrates to achieve comparable read ranges, narrowing the performance gap. Converters are scaling multi-layer lamination lines that sandwich antennas between compostable layers, protecting circuitry while preserving end-of-life degradability.

Geography Analysis

North America captured 34.93% of global revenue in 2024, underpinned by omnichannel retail pioneers, stringent DSCSA pharmaceutical rules, and a dense ecosystem of NFC solution providers. Retailers operationalized tap-based checkout to trim labor costs, while drugmakers prepared for 2027 serialization deadlines. State-level sustainability statutes also sparked early pilots for compostable NFC labels. Growth remains steady as enterprises migrate from pilot to full fleet deployments.

The Asia-Pacific region is the clear acceleration hub, forecasted to grow at a 20.51% CAGR through 2030. China’s dominance in printed electronics compresses tag prices, while India and Southeast Asia supply the fast-growing consumer base that craves smartphone-centric engagement. Governments’ Made-in-Asia digitization drives funnel subsidies into smart manufacturing nodes, ensuring local availability of passive and active chips. The region consequently serves both as a production powerhouse and an expanding end-market.

Europe sustains mid-teens growth, driven by the Falsified Medicines Directive and ambitious circular economy targets. Luxury goods clusters in France and Italy are integrating crypto-secure NFC tags into packaging to combat grey-market leakage. GDPR compliance adds complexity but simultaneously builds consumer trust. The European Commission’s extended producer responsibility rules further incentivize smart labels that demonstrate recycling outcomes, making NFC a lever for regulatory reporting.

Competitive Landscape

The field remains moderately fragmented. Electronics majors, such as NXP Semiconductors and Avery Dennison, secure high-volume contracts, while packaging converters, like Multi-Color Corporation, integrate tag insertion at scale. Recent consolidation, Multi-Color’s USD 85 million takeover of Starport Technologies in October 2024, signals a race to bundle hardware with cloud analytics and design services. Start-ups specializing in crypto-secured tags target luxury and art authentication niches, bringing blockchain APIs to mainstream CPG workflows.

Technology roadmaps converge on power harvesting, sensor fusion, and eco-substrate compatibility. Avery Dennison’s Smartrac Cosmos platform marries tag IDs with a cloud SaaS layer, lowering integration hurdles for mid-tier brands. Identiv’s alliance with Tapwow embeds cryptographic handshakes into luxury perfumery cartons, underscoring security as a differentiator. Meanwhile, capacity expansions at Xerafy and Thinfilm address supply bottlenecks, signaling confidence in multi-year volume growth.

In the longer term, competitive edges will hinge on vertical integration, from antenna ink formulation to data analytics dashboards. Companies that bridge physical tags with actionable insights are well-positioned to capture more durable, recurring revenue streams. Sustainability credentials now appear in RFQs alongside unit price and memory specs, forcing incumbents to invest in R&D for biodegradable materials.

NFC-Embedded Packaging Industry Leaders

Avery Dennison Corporation

NXP Semiconductors N.V.

Impinj, Inc.

CCL Industries Inc. (Checkpoint Systems)

Zebra Technologies Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Multi-Color Corporation completed its USD 85 million acquisition of Starport Technologies, integrating smart packaging capabilities into its global label portfolio.

- September 2024: Fedrigoni purchased BoingTech for EUR 45 million (USD 50 million), combining premium substrates with NFC expertise for luxury goods.

- August 2024: Identiv partnered with Tapwow to launch crypto-secured NFC authentication for high-value packaging.

- July 2024: NXP Semiconductors reported 18% year-over-year revenue growth in NFC packaging solutions.

Global NFC-Embedded Packaging Market Report Scope

| Passive NFC Tags |

| Active/Battery-Assisted NFC Tags |

| Hybrid NFC + UHF RFID Tags |

| Food and Beverage |

| Pharmaceuticals and Healthcare |

| Retail and FMCG |

| Consumer Electronics |

| Logistics and Supply Chain |

| Authentication and Anti-Counterfeiting |

| Supply-Chain Tracking and Inventory |

| Consumer Engagement and Marketing |

| Temperature/Condition Monitoring |

| Asset Management |

| Paper-Based Labels |

| Plastic Polymer Labels |

| Metal-Foil and Durable Labels |

| Biodegradable/Compostable Substrates |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Technology | Passive NFC Tags | ||

| Active/Battery-Assisted NFC Tags | |||

| Hybrid NFC + UHF RFID Tags | |||

| By End-User Industry | Food and Beverage | ||

| Pharmaceuticals and Healthcare | |||

| Retail and FMCG | |||

| Consumer Electronics | |||

| Logistics and Supply Chain | |||

| By Application/Functionality | Authentication and Anti-Counterfeiting | ||

| Supply-Chain Tracking and Inventory | |||

| Consumer Engagement and Marketing | |||

| Temperature/Condition Monitoring | |||

| Asset Management | |||

| By Material/Substrate | Paper-Based Labels | ||

| Plastic Polymer Labels | |||

| Metal-Foil and Durable Labels | |||

| Biodegradable/Compostable Substrates | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

Which region is expected to grow fastest in NFC-enabled packaging adoption?

Asia-Pacific is projected to post the highest 20.51% CAGR through 2030, fueled by manufacturing scale and smartphone ubiquity.

Which application currently holds the largest revenue share?

Supply-chain tracking and inventory management dominate with 40.12% of 2024 revenue.

How are anti-counterfeiting regulations influencing adoption?

EU and U.S. directives require end-to-end traceability, turning NFC labels into compulsory compliance tools across pharmaceutical supply chains.

What materials are gaining traction for sustainable NFC tags?

Biodegradable and compostable substrates are advancing at a 23.14% CAGR as brands align with circular-economy goals.

Who are the key players shaping competitive dynamics?

Avery Dennison, NXP Semiconductors, Multi-Color Corporation, Identiv, and several niche start-ups drive innovation through acquisitions and security-focused partnerships.

Page last updated on: