PLA-Laminated Paperboard Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

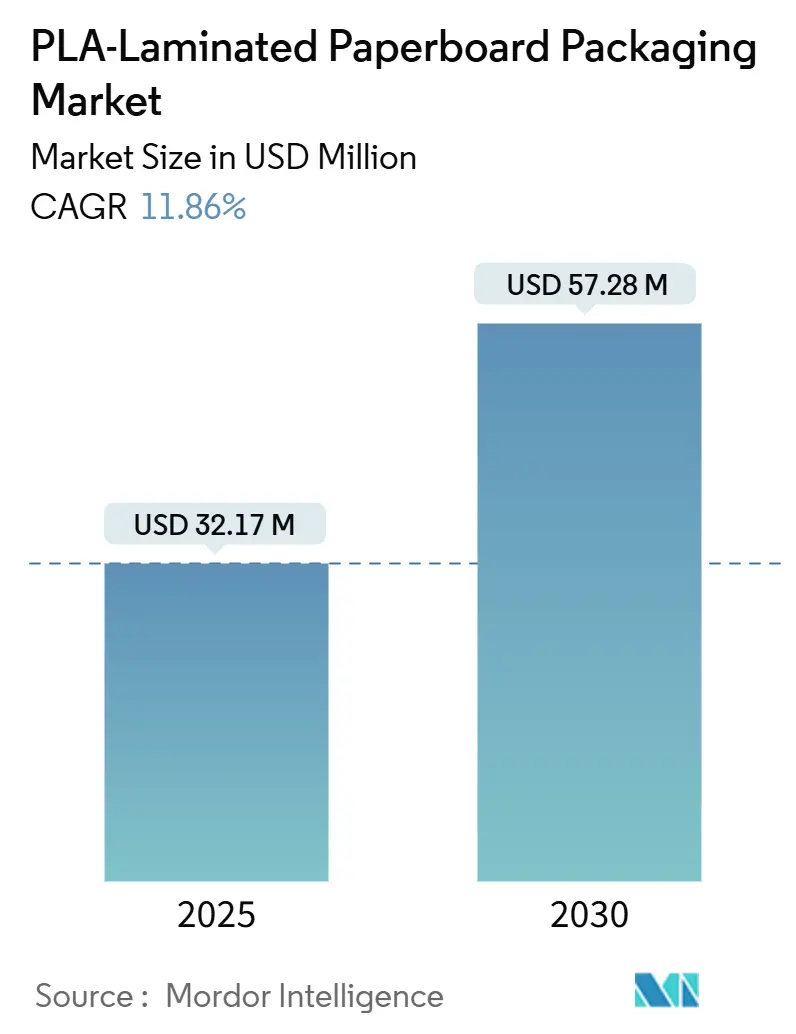

| Market Size (2025) | USD 32.17 Million |

| Market Size (2030) | USD 57.28 Million |

| Growth Rate (2025 - 2030) | 11.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PLA-Laminated Paperboard Packaging Market Analysis by Mordor Intelligence

The PLA-Laminated Paperboard Packaging market size reached USD 32.71 billion in 2025 and is forecast to hit USD 57.28 billion by 2030, registering an 11.86% CAGR over the period. Regulatory crack-downs on per- and polyfluoroalkyl substances (PFAS) and single-use plastics, corporate net-zero mandates, and a post-pandemic surge in food-service demand are aligning in favor of PLA-coated substrates, displacing petroleum-based coatings across multiple end-uses. Europe’s early adoption of the EU Packaging and Packaging Waste Regulation (PPWR) anchors near-term compliance investment, while NatureWorks’ new Thai PLA complex ensures upstream security of supply in the fastest-growing Asia-Pacific markets. Brand owners’ science-based decarbonization targets are translating into long-term supply contracts, improving utilization rates for recently installed extrusion-coating lines. Technological gains such as microwave-stable high-heat grades and ultra-thin reactive-extrusion barriers are widening the performance window, enabling the PLA-Laminated Paperboard Packaging market to penetrate applications previously locked to fossil polymers. Price volatility in lactic-acid monomer and the uneven build-out of composting infrastructure remain headwinds, yet the overall demand signal continues to strengthen as governments and corporations converge on circular-economy principle.

Key Report Takeaways

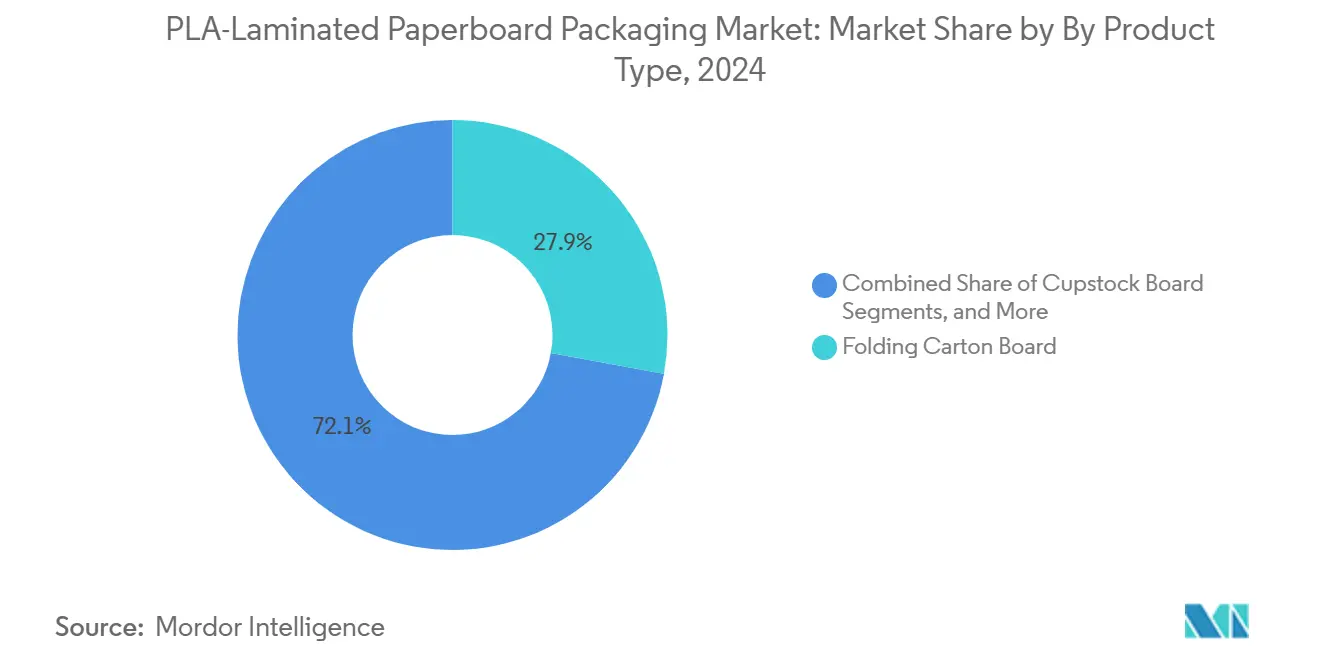

- By product type, folding carton board captured 27.89% of the PLA-laminated paperboard packaging market share in 2024.

- By application, the PLA-laminated paperboard packaging market size for the ready-meal and take-away trays segment is projected to grow at a 12.84% CAGR between 2025-2030.

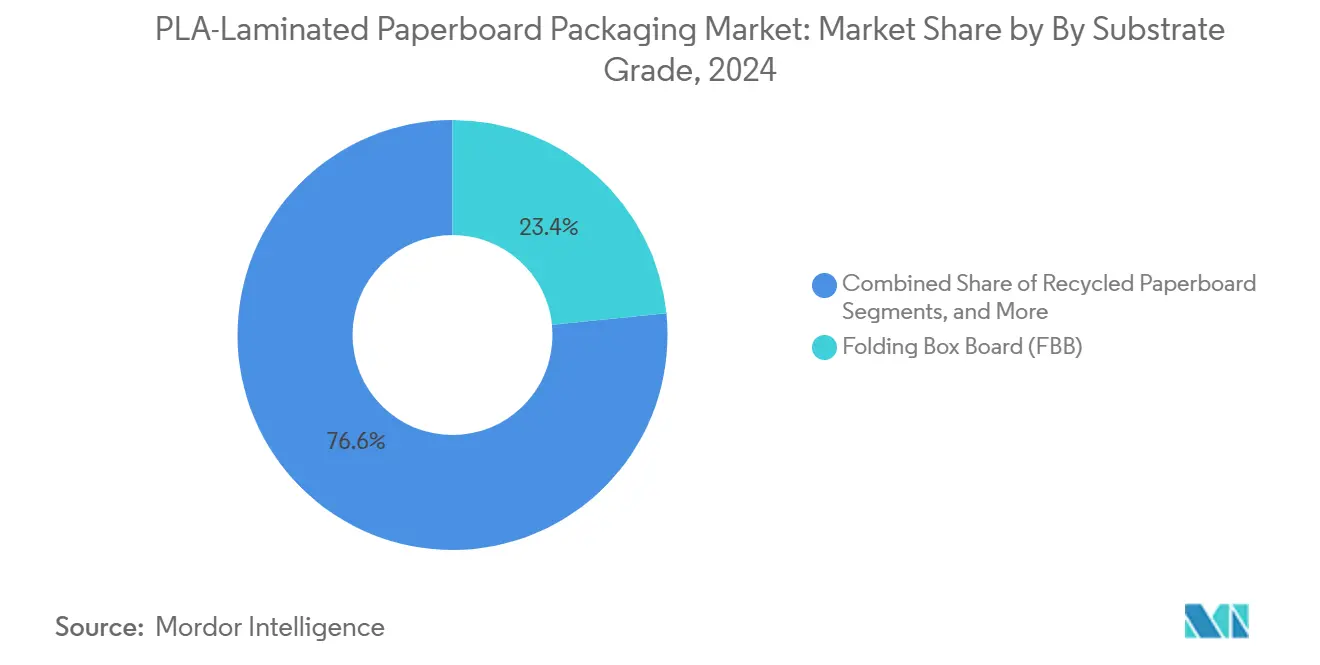

- By substrate grade, folding box board captured 23.38% of the PLA-laminated paperboard packaging market share in 2024.

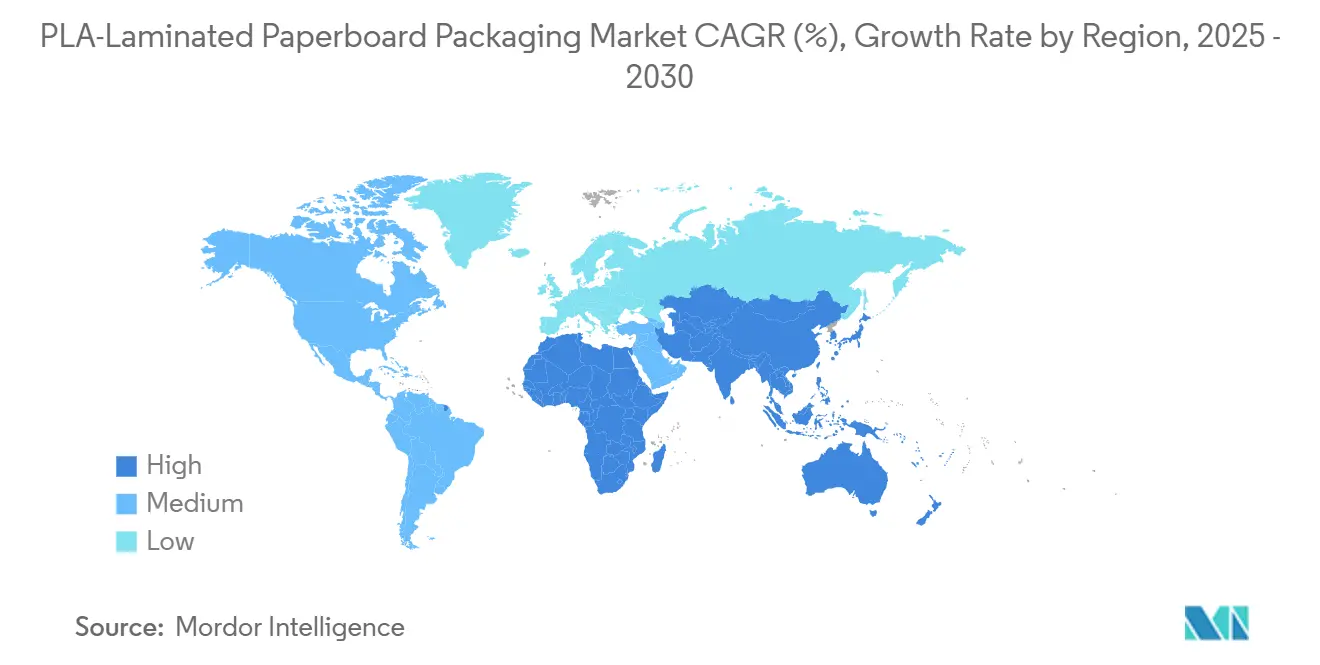

- By geography, the PLA-laminated paperboard packaging market share for the Asia-Pacific region is projected to grow at a 13.02% CAGR between 2025-2030.

Global PLA-Laminated Paperboard Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans on PFAS and SUP plastics | +2.1% | Global, led by NA and EU | Short term (≤ 2 years) |

| Corporate zero-carbon packaging targets | +1.8% | Global, NA and Europe | Medium term (2-4 years) |

| Surge in takeaway/QSR cup demand post-COVID | +1.5% | Global, high in APAC | Short term (≤ 2 years) |

| High-heat PLA grades enable microwaveable trays | +1.2% | NA and Europe, rising APAC | Medium term (2-4 years) |

| Ultra-thin reactive-extrusion PLA barriers | +0.9% | Advanced manufacturing | Long term (≥ 4 years) |

| Composting-infrastructure build-outs | +0.8% | NA and EU core, select APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory bans on PFAS and SUP plastics

Global legislation is rapidly outlawing fluorinated additives and single-use plastics, converting PLA coating from a green premium to a compliance prerequisite. Minnesota’s January 2025 PFAS ban spans 11 packaging categories. At EU level, the PPWR caps PFAS at 25 ppb for individual compounds by August 2026. Parallel Congressional proposals would prohibit intentional PFAS use nationwide in US food packaging.[1]SGS, “US Congress Intends to Ban PFAS in Food Packaging,” SGS.COM Together, these measures eradicate cost-driven competition from polyethylene-coated board, opening a structural advantage for the PLA-Laminated Paperboard Packaging market.

Corporate zero-carbon packaging targets

Brand owners are translating net-zero pledges into binding procurement criteria. Nestlé requires 100% recyclable or reusable packaging by 2025 and a one-third cut in virgin plastic. Mondelez is targeting 96% recyclability and deforestation-free fiber sourcing. Such mandates secure multi-year off-take agreements, underpinning capital outlays for new extrusion coaters and reducing unit costs across the PLA-Laminated Paperboard Packaging industry.

Surge in takeaway/QSR cup demand post-COVID

Online ordering and delivery platforms embedded disposable formats into daily routines, lifting cup and lid volumes to historic highs. Huhtamaki’s 2024 trends report confirms enduring preference for convenience paired with compostability. The PLA-Laminated Paperboard Packaging market harnesses this volume surge as conventional wax or plastic-lined board faces rapid de-selection by quick-service restaurants.

High-heat PLA grades enable microwaveable trays

Bio-based copolyesters now deliver melting points above 200 °C, breaking the thermal ceiling that once confined PLA to ambient uses. Ready-meal trays, therefore, shift from CPET toward coated paperboard, improving brand sustainability scores without sacrificing microwavability. The performance leap broadens the addressable PLA-Laminated Paperboard Packaging market across convenience food channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PLA resin price volatility vs. PE | -1.4% | Global, acute in EMs | Short term (≤ 2 years) |

| Limited industrial composting in EMs | -0.7% | APAC, Latin America, Africa | Long term (≥ 4 years) |

| Potential EU curbs on bioplastic SUP items | -0.6% | European Union | Medium term (2-4 years) |

| Nano-plastic shedding concerns at high temp. | -0.5% | Food-safety-sensitive markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PLA resin price volatility vs. PE

Quarterly swings of 15-20% in spot PLA relative to polyethylene unsettle converters’ cost models. Feedstock availability and logistics bottlenecks heighten variability, especially in regions lacking local lactic-acid capacity. Pricing turbulence narrows adoption in cost-critical fast-moving consumer goods, tempering PLA-Laminated Paperboard Packaging market growth in emerging economies.

Limited industrial composting in EMs

Many municipalities in Asia and Africa still rely on landfills; industrial composting penetration remains low. Without downstream recovery, brand owners hesitate to pay sustainability premiums, stalling conversion projects. This infrastructure gap continues to cap the potential of the PLA-Laminated Paperboard Packaging market until regional waste-management upgrades materialize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialty Papers Drive Innovation

The segment generated the highest revenue from Folding Carton Board, which controlled 27.89% PLA-Laminated Paperboard Packaging market share in 2024. Mass-market carton producers leveraged existing press lines to overlay PLA, giving brand owners drop-in compliance with minimal line change. Specialty Papers, however, are racing ahead at a 13.14% CAGR as pharmaceutical leaflets and technical inserts demand biocompatibility alongside barrier performance.

Growth in Specialty Papers signals a shift toward value-added niches within the PLA-Laminated Paperboard Packaging market. High-heat trays and aluminum-free blister substrates exemplify how tailored coatings on fine-paper bases unlock premium price points. Investments by Dai Nippon Printing in aluminum-free PTP structures confirm this pivot to monomaterial design.[2]Dai Nippon Printing, “Aluminum-Free PTP Film,” PRTIMES.JP

By Application: Ready-Meals Accelerate Growth

Food-service Disposable Cups and Lids accounted for 54.61% of the PLA-Laminated Paperboard Packaging market size in 2024, underpinned by the lasting expansion of quick-service restaurant channels. Consumer preference for recyclable or compostable on-the-go formats supports stable baseline demand.

The fastest mover is Ready-Meal and Take-away Trays, advancing at 12.84% CAGR on the back of high-heat PLA grades that sustain microwave cycles without warping. NatureWorks’ tie-up with IMA for compostable coffee pods illustrates how function-critical formats migrate to PLA-coated paperboard when performance hurdles fall.

By Substrate Grade: Recycled Content Gains Momentum

Folding Box Board commanded 23.38% of the 2024 PLA-Laminated Paperboard Packaging market size owing to its stiffness-to-weight ratio and print surface suited to consumer goods. Brands seeking shelf appeal have favored FBB with PLA coatings to meet dual goals of design and sustainability.

Recycled Paperboard is the fastest-expanding substrate, growing 13.23% CAGR as procurement policies score both renewable barriers and post-consumer fiber. Mondi’s EUR 200 million recycled containerboard mill in Duino, Italy underlines the scale of capital channeled into circular fiber capacity.

Geography Analysis

Europe topped the regional leaderboard with 33.45% PLA-Laminated Paperboard Packaging market share in 2024. The PPWR’s PFAS threshold and monomaterial rules delivered regulatory certainty, prompting Stora Enso to start up the Oulu consumer-board line that propelled 17.7% EBIT growth in Q1 2025.[3]Stora Enso, “Interim Report Q1 2025,” STORAENSO.COM Mature composting systems, evidenced by an 81.5% paper-recycling rate, enhance the end-of-life proposition that justifies brand premiums.

Asia-Pacific is the growth engine, forecast to register a 13.02% CAGR to 2030. Thailand’s 75,000 tpa PLA complex moves feedstock closer to converters, cutting freight and import-duty exposure while aligning with regional bio-circular-green policies. China’s zero-waste city initiatives couple infrastructure funding with bans on non-degradable food-service ware, accelerating PLA uptake.

North America shows resilient growth anchored by early state-level PFAS bans. Billerud’s first US-made containerboard shipments in 2024 signal supplier localization, while the USDA compost grants reduce disposal-phase uncertainty. Latin America and MEA remain nascent; progress hinges on regulatory harmonization and organics-recovery investments.

Competitive Landscape

The PLA-Laminated Paperboard Packaging market is moderately fragmented. Legacy board producers such as Stora Enso, Smurfit WestRock, and Graphic Packaging retrofit extrusion coaters to apply PLA, leveraging mill scale and customer reach. Smurfit WestRock’s closure of 500,000 tons of legacy paper capacity and simultaneous investment in high-efficiency converting plants encapsulate this strategic redeployment.

Horizontal moves are matched by vertical plays as NatureWorks and Total Corbion explore joint technology centers with converters, blurring supplier–customer lines. Mid-tier firms exploit application niches pharma, technical, or luxury goods, using proprietary coatings with differentiated crystallinity or barrier chemistries.

Competition is intensifying around integrated solutions that merge recycled fiber with renewable barriers. Producers capable of guaranteeing both carbon-footprint reduction and traceable post-consumer content are winning multi-year preferred-supplier status with multinational FMCGs, reshaping bargaining power across the PLA-Laminated Paperboard Packaging industry.

PLA-Laminated Paperboard Packaging Industry Leaders

Stora Enso Oyj

Metsä Board Corporation

Huhtamäki Oyj

Graphic Packaging Holding Company

Smurfit WestRock PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: NatureWorks completed its USD 350 million Ingeo PLA facility in Thailand, adding 75,000 tpa of regional capacity aimed at packaging converters across Asia-Pacific.

- April 2025: Stora Enso reported EUR 175 million (USD 189 million) EBIT in Q1 2025 on the back of its Oulu consumer-board line start-up and reorganized into seven business areas to sharpen focus on renewable packaging.

- March 2025: International Paper closed a USD 9.9 billion acquisition of DS Smith, creating the world’s largest fiber-based packaging company with combined USD 24 billion revenue.

- June 2024: Billerud logged its inaugural sale of US-produced containerboard and began trials of Tribute and Voyager grades targeting sustainable packaging.

- May 2024: UPM teamed with Pentawards to promote the Sustainable Design category, spotlighting BioPura and BioVerno naphtha as drop-in fossil alternatives.

Global PLA-Laminated Paperboard Packaging Market Report Scope

| Cupstock Board |

| Folding Carton Board |

| Liquid Packaging Board |

| Food Tray and Plate Board |

| Specialty Papers |

| Food-service Disposable Cups and Lids |

| Dairy and Beverage Cartons |

| Ready-Meal and Take-away Trays |

| Fresh Produce and Confectionery Packs |

| Other Application (Pharma, Personal Care) |

| Solid Bleached Sulfate (SBS) |

| Folding Box Board (FBB) |

| Unbleached Kraft Board (UKB) |

| Recycled Paperboard |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Thailand | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Cupstock Board | ||

| Folding Carton Board | |||

| Liquid Packaging Board | |||

| Food Tray and Plate Board | |||

| Specialty Papers | |||

| By Application | Food-service Disposable Cups and Lids | ||

| Dairy and Beverage Cartons | |||

| Ready-Meal and Take-away Trays | |||

| Fresh Produce and Confectionery Packs | |||

| Other Application (Pharma, Personal Care) | |||

| By Substrate Grade | Solid Bleached Sulfate (SBS) | ||

| Folding Box Board (FBB) | |||

| Unbleached Kraft Board (UKB) | |||

| Recycled Paperboard | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Thailand | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the PLA-Laminated Paperboard Packaging market?

The PLA-Laminated Paperboard Packaging market size stood at USD 32.71 billion in 2025 and is on track to reach USD 57.28 billion by 2030.

Which region holds the largest market share?

Europe leads with 33.45% market share, supported by stringent PFAS restrictions and mature composting networks.

What application segment is growing the fastest?

Ready-Meal and Take-away Trays are projected to register the highest 12.84% CAGR through 2030 due to microwave-safe high-heat PLA grades.

How volatile are PLA prices compared with polyethylene?

PLA resin prices have shown 15-20% quarterly swings versus polyethylene, posing short-term cost risk for converters.

Why is Asia-Pacific considered the growth engine?

A new 75,000 tpa PLA plant in Thailand, rapid urbanization, and expanding food-service channels combine to drive a 13.02% regional CAGR.

Page last updated on: