Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 297.54 Billion |

| Market Size (2031) | USD 365.12 Billion |

| Growth Rate (2026 - 2031) | 4.17% CAGR |

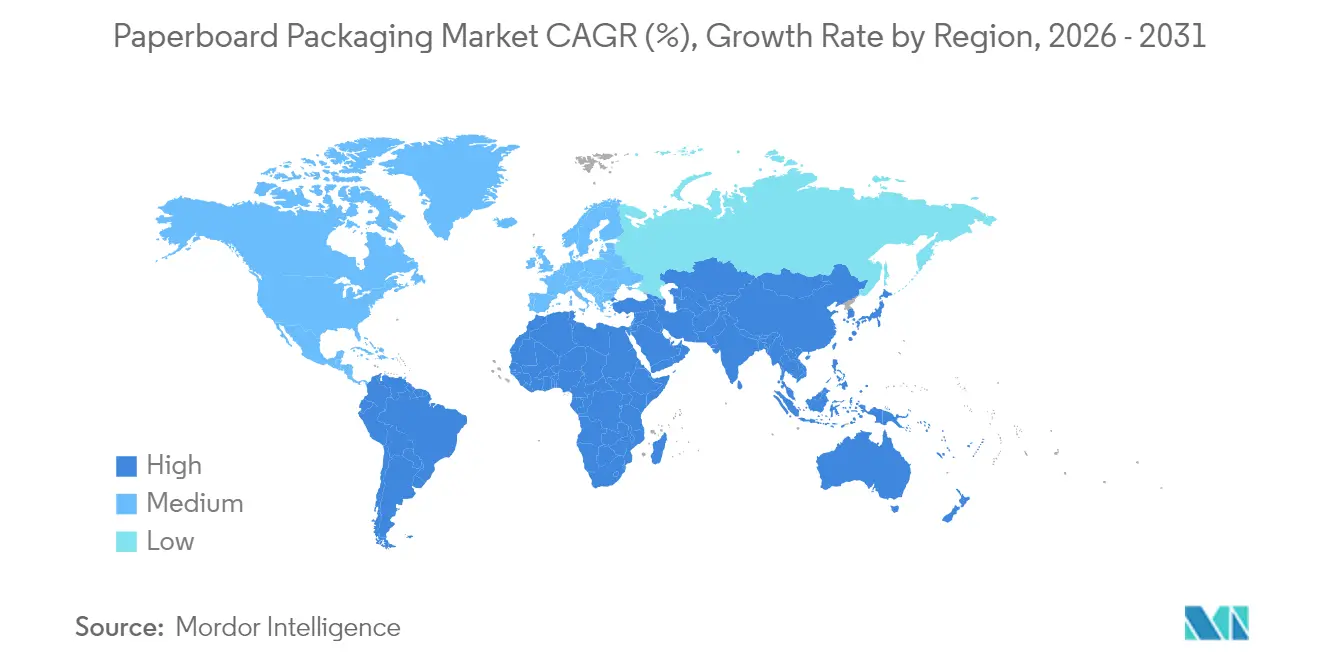

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paperboard Packaging Market Analysis by Mordor Intelligence

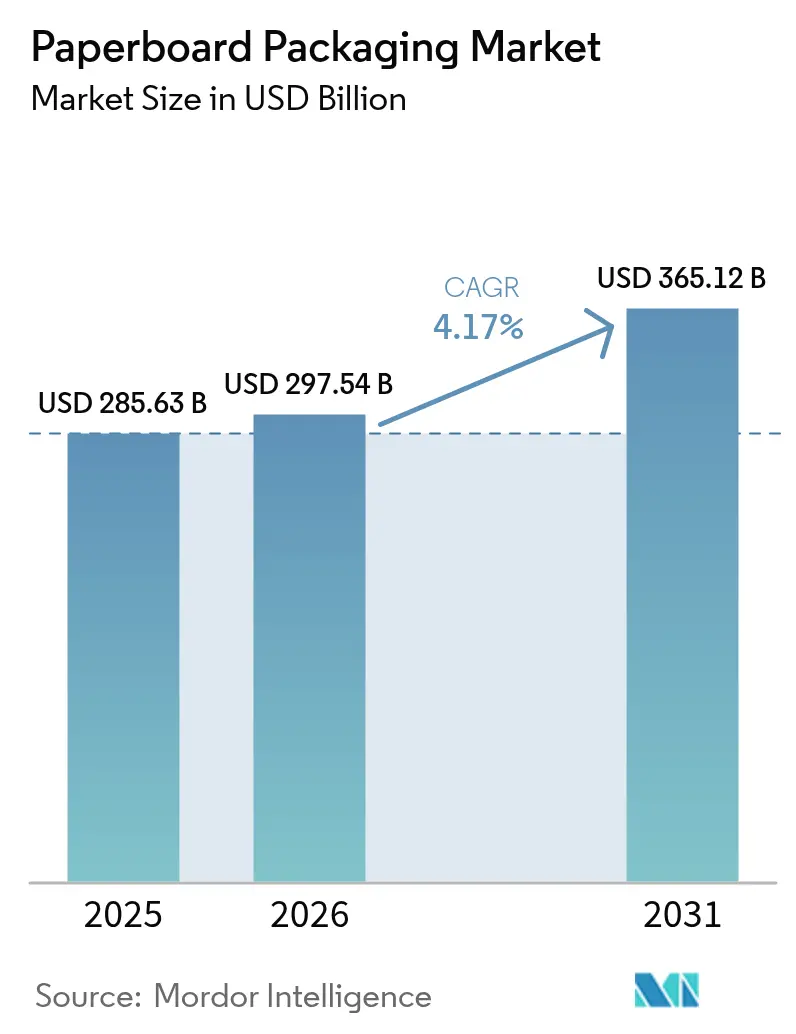

The Paperboard Packaging market size is expected to grow from USD 285.63 billion in 2025 to USD 297.54 billion in 2026 and is forecast to reach USD 365.12 billion by 2031 at 4.17% CAGR over 2026-2031.

Rising e-commerce volumes, regulatory momentum favoring fiber over plastic, and continuous improvements in lightweighting and digital converting technologies collectively propel expansion. Recycled fiber’s strong cost-to-performance profile complements retailer commitments to circular supply chains, sustaining demand despite raw-material cost swings. Corrugated formats remain the backbone of fulfillment networks, while folding cartons gain ground in premium consumer categories. Market participants counter mounting energy and recovered-paper price volatility by investing in vertical integration and pulp capacity in low-cost forestry regions.

Key Report Takeaways

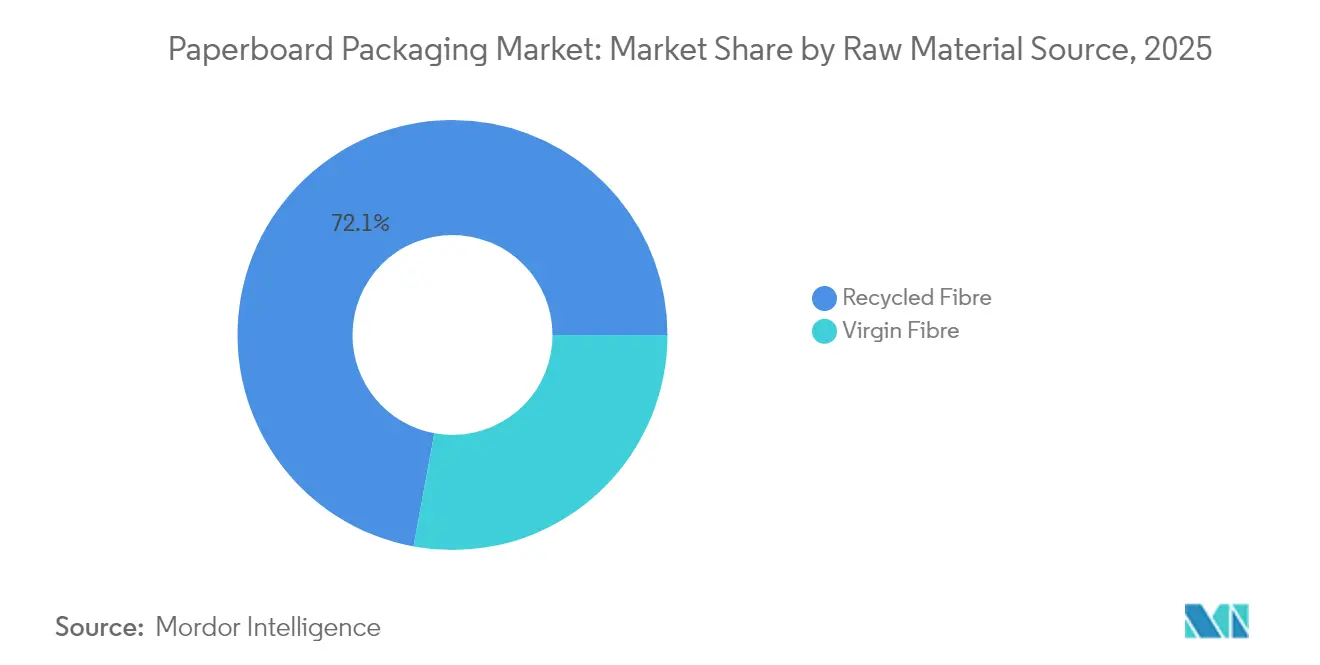

- By raw-material source, recycled fiber held 72.10% of the paperboard packaging market share in 2025, forecast to expand at a 6.65% CAGR to 2031.

- By product type, corrugated boxes led with 42.10% revenue share in 2025, while folding cartons are forecast to expand at a 5.55% CAGR to 2031.

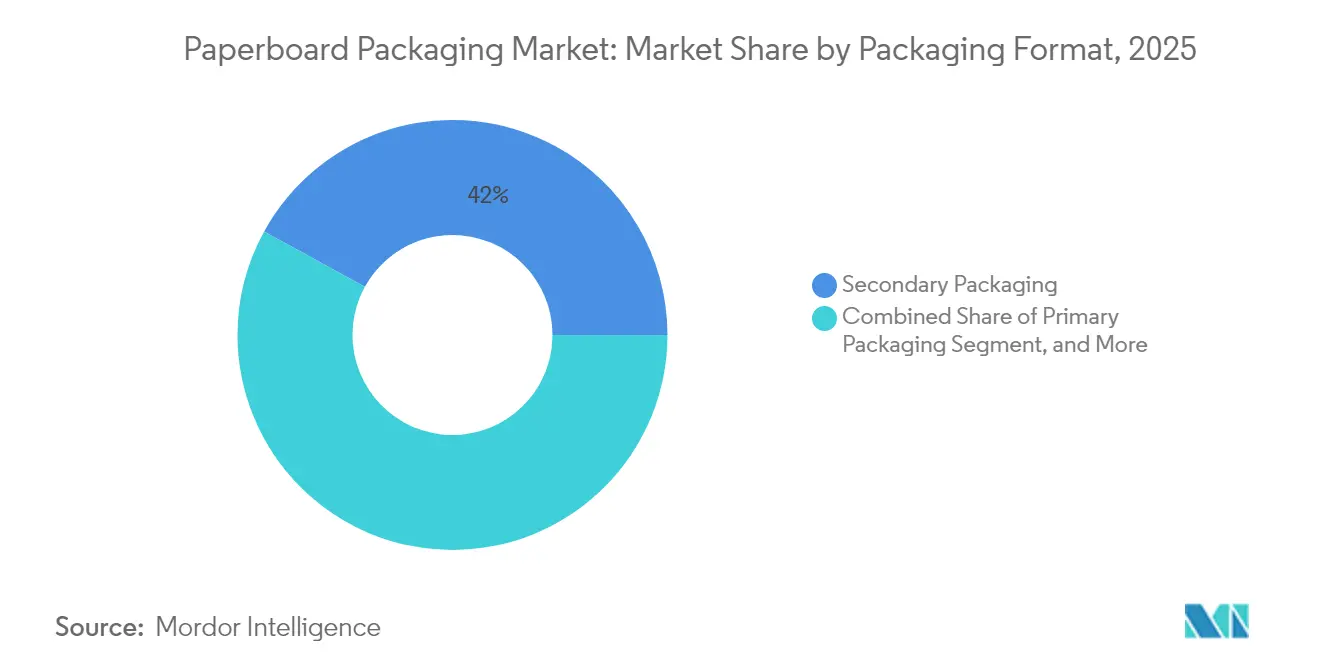

- By packaging format, secondary packaging accounted for 42.00% of the paperboard packaging market size in 2025 and is growing at a 4.95% CAGR through 2031.

- By end-user industry, personal care and cosmetics is advancing at a 5.90% CAGR through 2031, outpacing the food segment that retained a 28.10% revenue share in 2025.

- By Geography, Asia-Pacific is projected to post the fastest 6.78% CAGR to 2031, whereas North America commanded a 38.55% revenue share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Paperboard Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce surge boosting corrugated-shipping demand | +1.8% | Global (North America and Asia-Pacific focus) | Short term (≤ 2 years) |

| Plastic-substitution regulations favor fiber packaging | +0.5% | Europe and North America, spreading to Asia-Pacific | Medium term (2-4 years) |

| Light-weighting innovations lowering logistics cost | +0.7% | Global (early adoption in developed markets) | Medium term (2-4 years) |

| Rapid growth of packaged food and beverages in the Asia-Pacific | +1.2% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| AI-enabled on-demand custom printing | +0.8% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| LatAm eucalyptus pulp boom lowering virgin-fibre cost | +0.6% | Global supply impact, with regional production in South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce Surge Boosting Corrugated-Shipping Demand

Online retail penetration requires stronger, dimension-optimized shipping containers that withstand multiple touchpoints. Box producers captured surging orders by pairing high-performance flute profiles with real-time design tools that tailor packaging to SKU geometry. Packaging Corporation of America’s USD 70-per-ton price increase in early 2025 illustrated a tight demand-supply balance. Direct-to-consumer models further reinforce the need for branding space on outer packs, incentivizing converters to integrate high-graphics digital print modules. Smart-label technologies supporting location and shock monitoring now ship on corrugated liners, creating value beyond protection.

Plastic-Substitution Regulations Favor Fiber Packaging

The European Union’s Packaging and Packaging Waste Regulation mandates 90% recyclability by 2030, accelerating the shift from multilayer plastics toward recyclable fiber formats.[1]European Union, “Packaging and Packaging Waste Regulation,” eur-lex.europa.eu North American states replicate extended-producer-responsibility frameworks, while several Asia-Pacific markets draft similar statutes. Producers respond with dispersion-based barrier coatings and PFAS-free grease-proof chemistries that safeguard food while maintaining repulpability. Brand owners leverage these solutions to meet public sustainability pledges and evade upcoming plastic taxes.

Light-Weighting Innovations Lowering Logistics Cost

Micro-fluting, enhanced fiber orientation, and nanocellulose coatings cut board grammage by 15-20% without sacrificing stacking strength. Mill trials by Sappi confirm double-digit truckload-volume gains that translate into freight savings and lower carbon intensity. As carriers broaden dimensional-weight pricing, e-commerce shippers prioritize space-efficient secondary packs. Lightweighting thus offers dual incentives: immediate cost relief and progress toward emissions targets.

Rapid Growth of Packaged F&B in Asia-Pacific

Vietnam’s packaging demand is forecast to hit USD 3.5 billion by 2026 at a 9.73% CAGR, mirroring middle-class appetite for convenience foods.[2]Vietnam Packaging Association, “Vietnam Packaging Market Outlook 2026,” vietnampackaging.org Rising quick-service restaurant penetration amplifies single-use container volumes, while regional governments increasingly ban non-recyclable plastics. Paperboard manufacturers capitalize on this momentum by launching compostable noodle bowls and grease-resistant snack cartons tailored to tropical climates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deforestation and fiber-sourcing scrutiny | -0.6% | Global (tropical regions focus) | Medium term (2-4 years) |

| Volatile recovered-paper and energy costs | -0.4% | Global (regional variance) | Short term (≤ 2 years) |

| Brand-owner pull-back on sustainability pledges | -0.5% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Flexible plastic pouches eroding share | -0.3% | Global (food and beverage focus) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Deforestation and Fiber-Sourcing Scrutiny

Implementation of the European Union Deforestation Regulation compels mills to trace wood back to plots verified as deforestation-free after December 2020, adding auditing costs and exposing non-compliant supply chains to import bans.[3]Forest Stewardship Council, “European Union Deforestation Regulation Implementation,” fsc.org Multinationals extend the same protocols worldwide, effectively globalizing compliance. Smaller converters face disproportionate administrative burdens, nudging them toward certification pooling or vertical partnerships with plantation owners. Premiums paid for certified logs increase the break-even point for certain grades, compressing margins until chain-of-custody systems mature.

Volatile Recovered-Paper and Energy Costs

Recovered-fiber reference prices doubled in Q1 2024, while natural-gas volatility inflated pulping and drying expenses. Mills hedge through supply contracts and cogeneration projects, but input swings still distort quarterly earnings and complicate long-term pricing agreements. Some operators secure virgin eucalyptus pulp from Latin America to counterbalance recycled shortages, aided by Suzano’s INR 1.66 billion (USD 19 million) capacity expansion completed in January 2025.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material Source: Recycled Dominance Drives Sustainability

Recycled fiber secured a 72.10% share of the paperboard packaging market in 2025, underpinned by extensive curbside collection networks and maturing de-inking technologies. This segment is also projected to clock a 6.65% CAGR, outpacing virgin grades due to regulatory credits linked to circularity goals. The paperboard packaging market size for recycled grades is forecast to widen as brand owners mandate minimum post-consumer content for high-volume SKUs. Virgin fiber retains relevance where impeccable visual quality or high wet-strength is mandatory, such as cosmetics gift boxes and pharmaceutical blister cards.

Continuous investments in low-cost plantation forestry bolster recycled leadership. Suzano’s new Brazilian eucalyptus complex provides 2.55 million t/year of high-brightness pulp that blends seamlessly with recovered streams, lowering average furnish costs for global mills. Certification through FSC and PEFC further differentiates recycled sheets, enabling converters to add carbon-neutral claims that resonate with eco-conscious consumers. Resulting supply security and branding leverage keep recycled fiber at the forefront of the paperboard packaging market.

By Product Type: Corrugated Boxes Lead Digital Transformation

Corrugated boxes captured 42.10% revenue share in 2025, propelled by shipment frequency spikes tied to omnichannel retail. Embedded moisture barriers and crush-resistant micro-flutes allow these boxes to traverse automated sortation systems with minimal damage, reinforcing their indispensability. Folding cartons, though smaller in tonnage, promise the fastest 5.55% CAGR, as high-graphics capabilities align with premium food and personal-care placement. The paperboard packaging market size for folding cartons is projected to expand alongside demand for shelf-ready packs that combine vivid print with easier recyclability.

On the innovation front, Greif’s EnviroRAP™ showcases mono-material wrap formats that replace laminated mailers while retaining curbside recyclability. Parallel progress in digital corrugators lets converters print variable data at press speed, supporting localized holiday themes or influencer collaborations. Such flexibility differentiates corrugated solutions within the paperboard packaging market and sustains their lead as the workhorse of distribution.

By Packaging Format: Secondary Packaging Balances Function and Sustainability

Secondary packaging accounted for 42.00% of the paperboard packaging market size in 2025, reflecting its pivotal role in safeguarding goods through extended logistics chains. Growth continues at a 4.95% CAGR as shippers fine-tune case dimensions to slash fill rates and emissions. Innovations in package geometry and board caliper enable double-stacking of pallets without structural compromise, appealing to cost-sensitive FMCG firms. Conversely, primary packs face stiffer competition from lightweight pouches, pressing converters to add tactile varnishes and easy-open features to preserve shelf presence.

Ranpak’s NatureMailer and Climaliner Plus lines underscore transit packaging advancements that integrate insulation and void fill within curbside-recyclable wraps. E-commerce-specific SKUs marry smart-label sensors with QR-code consumer engagement portals, widening value propositions beyond containment. Such differentiated offerings fortify the secondary segment against incursions from alternative substrates in the paperboard packaging market.

By End-user Industry: Personal Care Drives Premium Innovation

Food retained the largest 28.10% slice of the 2025 revenue pool thanks to rigorous safety standards and rapid takeaway growth, yet CAGR momentum now tilts toward personal care and cosmetics at 5.90%. Beauty brands view tactile, embossed cartons as integral to unboxing rituals, rewarding converters able to embed metallic foils without compromising recyclability. Graphic Packaging’s coffee-capsule know-how migrated to fragrance sample sleeves, illustrating cross-category technology transfer.

Healthcare remains a steady contributor; serialization codes mandated on pharma blister wallets reinforce demand for pristine virgin board with exacting print tolerances. Electronics makers prioritize anti-static coatings and precision inserts that cushion devices while communicating sustainability credentials. Collectively, these dynamics diversify revenue streams and mitigate exposure to cyclical single-category swings, cementing end-market resilience within the paperboard packaging market.

Geography Analysis

North America commanded 38.55% revenue share in 2025, buoyed by integrated recovered-fiber networks and state-level plastic-reduction mandates that steer converters toward curbside-recyclable solutions. Packaging Corporation of America’s USD 1.8 billion containerboard acquisition bolsters regional capacity, evidencing consolidation that harnesses scale efficiencies. Retailers’ same-day delivery services further stimulate demand for right-sized corrugated shippers, helping the paperboard packaging market sustain mid-single-digit growth despite energy-cost headwinds.

Asia-Pacific represents the fastest-expanding arena, clocking a 6.78% CAGR through 2031 as urban households buy more packaged staples and quick-service meals. China’s export orders increasingly specify fiber-based transit wraps, while Vietnam’s local industry eyes USD 3.5 billion in packaging revenue by 2026. Regional governments embed circular-economy clauses in new waste directives, granting tariff concessions to importers of recycled sheets. These policy levers, coupled with low-cost labor and expanding online retail, turn Asia-Pacific into the growth engine of the paperboard packaging market.

Europe sustains material innovations underpinned by regulations such as the PPWR and the EUDR, which tighten recyclability and sourcing standards. Sappi’s EUR 500 million(USD 587.73 million) machine upgrade enhances lightweight coated capacity, while Mondi’s acquisition spree widens folding-carton footprints across consumer-goods clusters. High recovery rates and consumer receptiveness to eco-labels maintain a robust baseline, although sluggish macro demand tempers tonnage growth. Still, stringent compliance hurdles create a moat that favors established players inside the paperboard packaging market.

Competitive Landscape

The sector remains moderately fragmented, yet M&A velocity is climbing as leaders chase geographic reach and closed-loop raw-material access. International Paper’s EUR 8.2 billion (USD 9.64 billion) buyout of DS Smith strengthens European corrugated holdings, while the USD 20 billion Smurfit-WestRock merger births a transatlantic powerhouse with unprecedented mill-to-market breadth. Market entrants differentiate via specialty coatings and AI-enabled converting, but scale advantages in fiber procurement and freight still tilt cost curves in favor of multinationals.

Strategically, vertical integration is the prevailing theme. Pulp investments in Latin America feed North American mills, mitigating recovered-paper price spikes and ensuring quality consistency. Concurrently, converters automate line changeovers and deploy digital twins to optimize asset maintenance, lowering downtime and elevating output per labor hour. Intellectual-property filings for smart-packaging sensors surged at the USPTO in 2025, signaling a fresh competitive battleground rooted in data-rich features.[4]United States Patent and Trademark Office, “Smart Packaging Technology Patents,” uspto.gov

Regional specialty players remain relevant by mastering local regulation and customer intimacy, particularly in high-barrier niches like pharma inserts and temperature-controlled meal-kit sleeves. Yet consolidation momentum suggests the top five firms could exceed a combined 55% share by decade’s end, nudging the paperboard packaging market toward a more concentrated structure without eliminating room for agile innovators.

Paperboard Packaging Industry Leaders

International Paper Company

Smurfit WestRock

Mondi plc

Packaging Corporation of America

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Packaging Corporation of America posted Q1 2025 net sales of USD 2.0 billion, reflecting resilient corrugated demand.

- March 2025: Graphic Packaging announced Q1 2025 revenue of USD 2.2 billion on rising sustainable foodservice sales.

- February 2025: European regulators cleared International Paper’s EUR 8.2 billion (USD 9.64 billion) acquisition of DS Smith.

- January 2025: Suzano completed a R$1.66 billion (USD 1.88 billion) eucalyptus pulp expansion.

Global Paperboard Packaging Market Report Scope

The global paperboard packaging market study tracks the demand for major paperboard packaging products, such as corrugated boards, folding cartons, and other paper packaging products. The pricing for the raw material, that is, paper and paperboard for the paper products, is considered along with the consumption, import, and export trends and average prices to arrive at the market revenue.

Paperboard Packaging Solutions Market is Segmented by Grade (Carton Board, Containerboard and Other Grades), by Product Type (Folding Cartons, Corrugated Boxes and Other types), by End-User Industry (Food, Beverage, Healthcare, Personal Care, Household Care, Electrical Products and Other End-User Industries), and by Geography (North America (United States, Canada), Europe (Germany, United Kingdom, France, Italy, and Rest of Europe), Asia-Pacific (China, Japan, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, Mexico, Rest of Latin America) and Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa, Rest of Middle East and Africa)). The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Above Segments.

By Raw Material Source

| Virgin Fibre |

| Recycled Fibre |

By Product Type

| Folding Cartons |

| Corrugated Boxes |

| Rigid Boxes |

| Other Product types |

By Packaging Format

| Primary Packaging |

| Secondary Packaging |

| Transit / E-commerce Shipping |

By End-user Industry

| Food |

| Beverage |

| Healthcare |

| Personal Care and Cosmetics |

| Household Care |

| Electrical and Electronics |

| Other End-user Industries |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Raw Material Source | Virgin Fibre | ||

| Recycled Fibre | |||

| By Product Type | Folding Cartons | ||

| Corrugated Boxes | |||

| Rigid Boxes | |||

| Other Product types | |||

| By Packaging Format | Primary Packaging | ||

| Secondary Packaging | |||

| Transit / E-commerce Shipping | |||

| By End-user Industry | Food | ||

| Beverage | |||

| Healthcare | |||

| Personal Care and Cosmetics | |||

| Household Care | |||

| Electrical and Electronics | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the paperboard packaging market in 2026?

It is valued at USD 297.54 billion with a 4.17% projected CAGR to 2031.

Which material commands the highest share?

Recycled fiber holds 72.10% of 2025 revenue thanks to established collection systems and regulatory credits.

What drives rapid growth in Asia-Pacific?

Expanding middle-class consumption, e-commerce penetration, and government circular-economy policies push a 6.78% CAGR through 2031.

Why are corrugated boxes so dominant?

They support omnichannel fulfillment with structural strength, branding surfaces, and evolving smart-label integrations.

Which end-use segment is growing fastest?

Personal care and cosmetics packaging is advancing at 5.90% CAGR as brands seek premium yet sustainable cartons.

Page last updated on: