Compostable Paperboard Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 32.71 Billion |

| Market Size (2030) | USD 57.28 Billion |

| Growth Rate (2025 - 2030) | 11.86% CAGR |

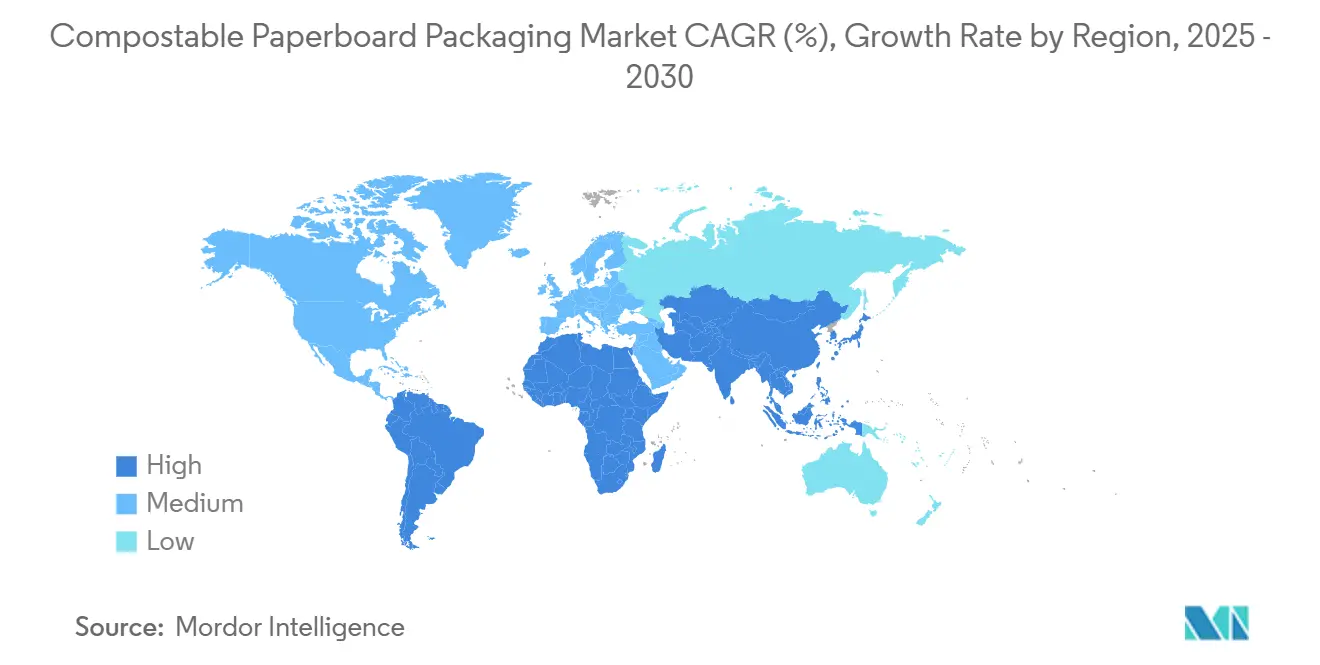

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

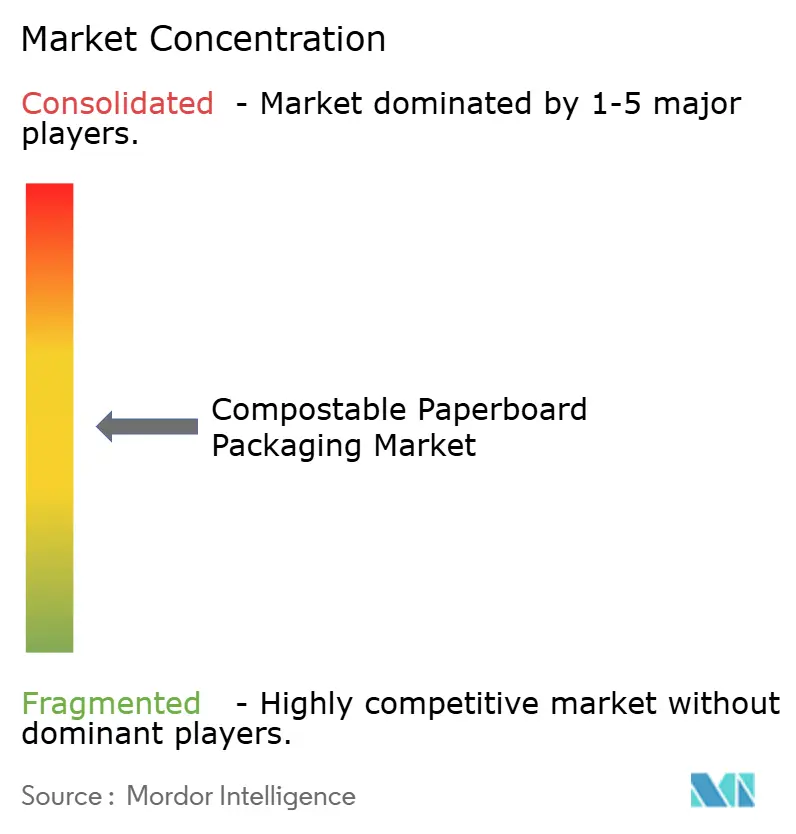

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compostable Paperboard Packaging Market Analysis by Mordor Intelligence

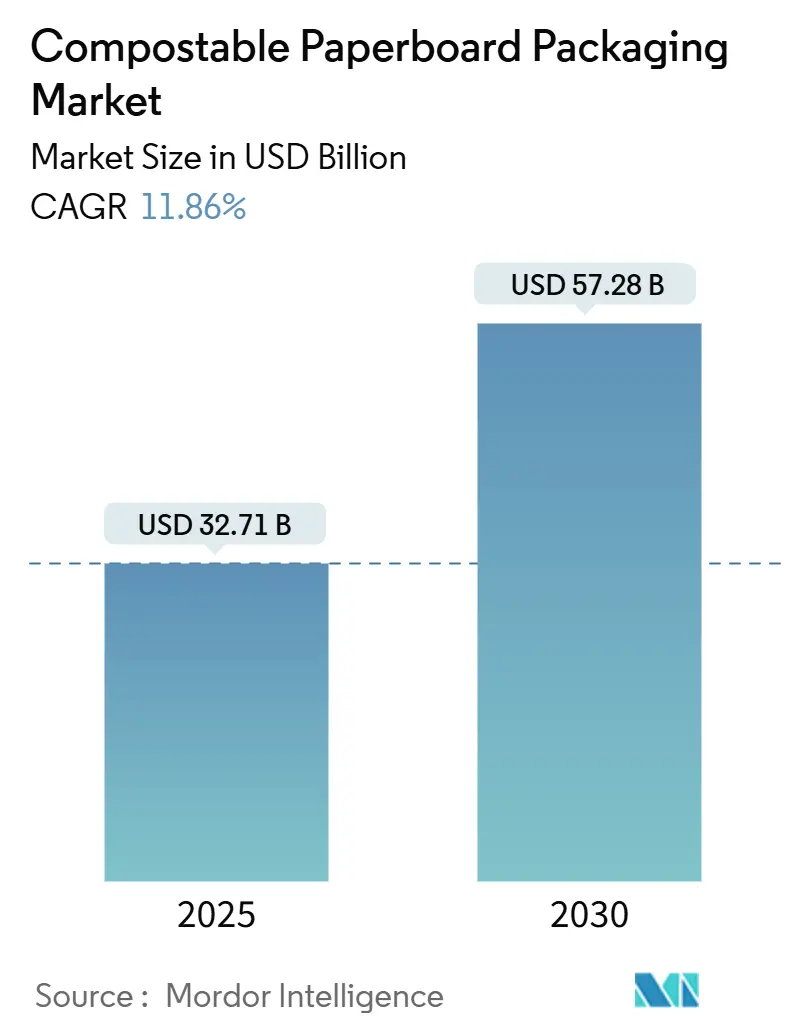

The compostable paperboard packaging market size stood at USD 32.71 billion in 2025 and is forecast to reach USD 57.28 billion by 2030, advancing at an 11.86% CAGR. This expansion stems from regulatory cost internalization on plastics, breakthrough dry-forming technology that cuts fiber processing costs, and brand-owner carbon targets. Demand accelerates as Extended Producer Responsibility (EPR) regimes mature, while aqueous barrier chemistry and nanocellulose coatings close historical performance gaps. Europe presently dominates, yet Asia-Pacific’s 12.95% CAGR signals a geographic pivot where first-mover investments in composting infrastructure enable scale benefits. Competitive strategies now prioritize vertical integration, recovered-fiber hedging, and proprietary coating formulations, positioning fiber solutions as mainstream replacements for poly-lined board.

Key Report Takeaways

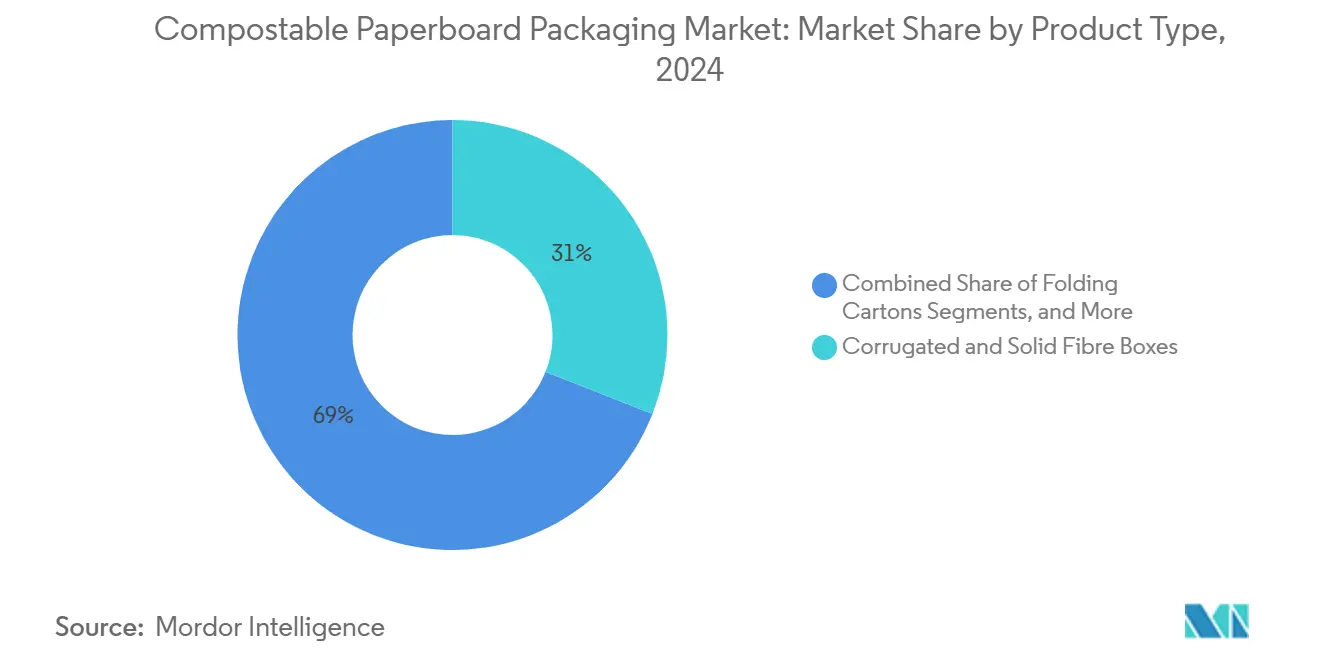

- By product type, corrugated and solid fiber boxes held 27.89% of the compostable paperboard packaging market share in 2024.

- By end-user industry, the compostable paperboard packaging market size for the personal care and cosmetics segment is projected to grow at a 12.67% CAGR between 2025-2030.

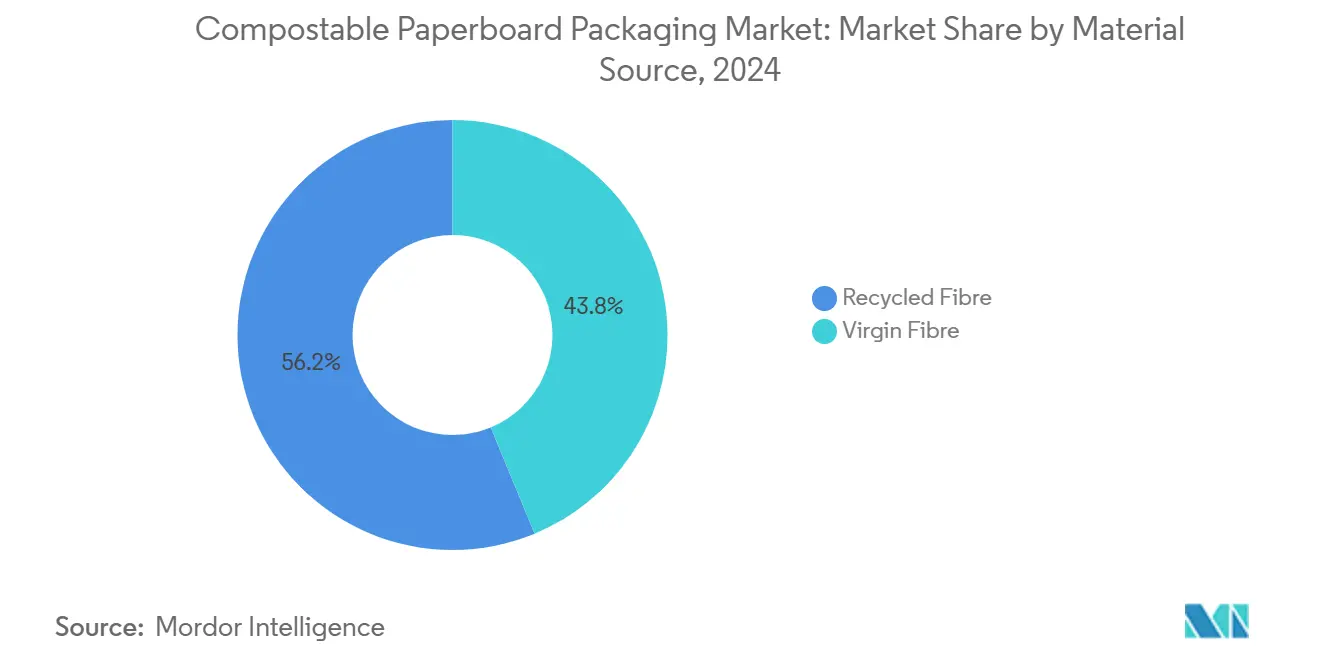

- By material source, recycled fiber held 56.23% of the compostable paperboard packaging market share in 2024.

- By functional coating, PLA and bio-polymer products retained 44.82% of the compostable paperboard packaging market share in 2024.

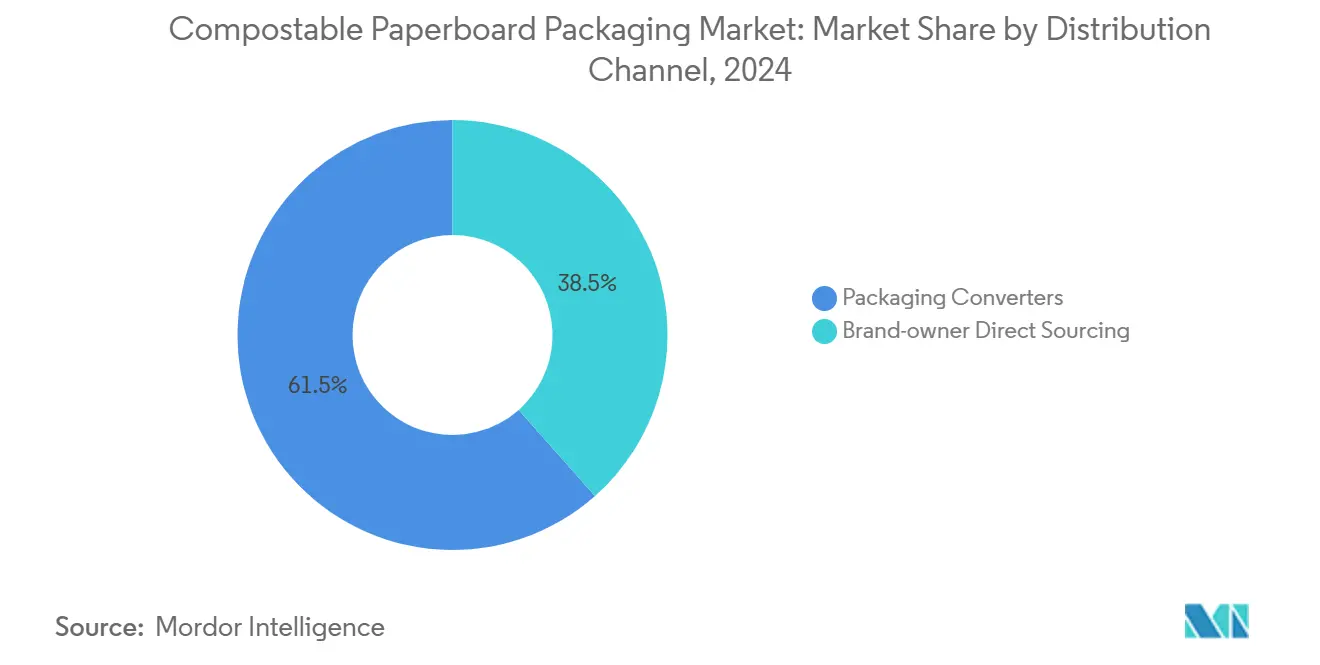

- By distribution channel, the compostable paperboard packaging market size for direct brand-owner sourcing is projected to grow at a 12.89% CAGR between 2025-2030.

- By geography, the compostable paperboard packaging market size for Asia-Pacific region is projected to grow at a 12.95% CAGR through 2030.

Global Compostable Paperboard Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans on single-use plastics and EPR laws | +2.8% | Global, with early gains in EU, California, Australia | Medium term (2-4 years) |

| Food-delivery boom driving sustainable take-out formats | +2.1% | North America & APAC core, spill-over to Europe | Short term (≤ 2 years) |

| Brand owner carbon-neutral packaging targets | +1.9% | Global, concentrated in Fortune 500 companies | Medium term (2-4 years) |

| Dry-forming molded-fiber cost breakthroughs | +1.7% | North America & EU manufacturing hubs | Long term (≥ 4 years) |

| Home-compostability labeling by retailers | +1.4% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Cold-chain e-grocery fiber chill-box adoption | +1.2% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory bans on single-use plastics and EPR laws

Global EPR mandates re-price packaging by shifting disposal charges from municipalities to producers, placing mainstream plastics at a structural cost disadvantage. The EU’s Packaging and Packaging Waste Regulation in effect since February 2025 sets compostability requirements for items such as tea bags and carrier bags, while California’s SB 54 compels a 25% material reduction by 2032. Australia’s 2024 reform blueprint raises recycled-content obligations on paperboard and accelerates landfill levies, creating a regulatory floor under fiber demand.[1]Department of Climate Change, Energy, the Environment and Water, “Australia launches comprehensive packaging regulations reform,” Enviliance.com, ENVILIANCE.COM South Australia’s targeted bans on non-certified produce stickers illustrate how granular rules unlock niche compostable volumes. Together, these actions cushion the compostable paperboard packaging market against cyclical downturns and reinforce a compliance-driven growth baseline.

Food-delivery boom driving sustainable take-out formats

Rapid urbanization and the visibility of delivery waste intensify scrutiny of single-use plastics in take-out channels. Restaurants migrating to molded-fiber trays enjoy brand lift while meeting municipal waste fees tied to plastic reduction. Huhtamaki has already shifted more than 80% of its food-service portfolio to renewable or recycled substrates, signalling supplier alignment with this demand surge. Consumer willingness to pay for eco-friendly packaging mitigates price premiums, and app-based ordering platforms now highlight “planet-friendly” icons, reinforcing pull-through. Cold-chain delivery of ready-to-cook meals opens additional space for fiber-based chill-boxes that can displace expanded polystyrene without compromising temperature control.

Brand owner carbon-neutral packaging targets

Corporate net-zero roadmaps elevate packaging as a visible Scope 3 lever. WestRock reports that 96% of its portfolio is already recyclable, compostable, or reusable, inching toward a 100% target by 2025. Ahold Delhaize intends to trim virgin primary plastic by 5% this year while ensuring full recyclability or compostability, sending clear signals down the supply chain.Lifecycle assessments reveal compostable paperboard yields markedly lower end-of-life emissions than landfill-bound multilayer plastics, making it an attractive decarbonization pathway for brand portfolios. Public ESG disclosures convert these technical gains into tangible investor confidence.

Dry-forming molded-fiber cost breakthroughs

Advances in orientation control and low-energy drying slash molded-fiber cycle times and unit costs, moving the format from premium niche to mainstream choice. The International Molded Fiber Association projects the segment to surpass USD 15 billion by 2034 on a 6% CAGR, anchored in these process gains. Patented nanocrystalline cellulose additives boost tensile strength and grease resistance while preserving compostability, enabling fiber to compete head-to-head with polystyrene in electronics cushioning. Stora Enso’s multi-year USD 1.1 billion investment in Oulu is emblematic of global scale-up aimed at meeting this new demand. As volume ramps, procurement savings cascade throughout the compostable paperboard packaging market, narrowing the historical price gap relative to poly-lined board.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price premium over poly-lined board | -1.8% | Global, most pronounced in price-sensitive segments | Short term (≤ 2 years) |

| Patchy industrial composting infrastructure | -1.5% | North America & developing APAC markets | Long term (≥ 4 years) |

| Barrier-fatigue for high-oil foods | -1.2% | Global food service and retail applications | Medium term (2-4 years) |

| Recovered fiber supply volatility | -0.9% | Global, concentrated in regions with limited virgin fiber | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price premium over poly-lined board

Compostable coatings still command 15-30% price uplifts versus polyethylene laminates, squeezing converter margins in value-sensitive categories. Smurfit Westrock’s 2024 earnings call flagged difficulties in passing higher recovered-fiber costs to corrugated customers. Yet aqueous barrier breakthroughs such as Cascades Sonoco’s FlexSHIELD, certified both by BPI and TÜV, cut the cost delta while meeting food-contact demands. As EPR fees escalate on plastic, the economic equation steadily tilts toward fiber, shrinking the restraint’s bite over the medium term.

Patchy industrial composting infrastructure

The US Environmental Protection Agency estimates USD 14-16 billion is needed to modernize organic-waste capacity, underscoring the processing gap. Regional disparities see the Pacific states well-served while the Midwest lags, limiting PLA-coated product end-markets. The Environmental Research & Education Foundation notes Northeast facilities average under 25,000 tonnes per year versus triple that in the West, affecting haul-distance economics.[2]Environmental Research & Education Foundation, “USCC, EREF Release Report on Composting Practices in the U.S.,” Compostingcouncil.org, COMPOSTINGCOUNCIL.ORG Progressive mandates in Washington and California, however, catalyze private-sector build-outs, foreshadowing long-term relief.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Molded fiber accelerates displacement of rigid plastics

The compostable paperboard packaging market size for corrugated and solid fiber boxes retained leadership at USD 9.14 billion in 2024. Growing e-commerce kept volumes high, yet growth slowed to single digits as adopters optimized pack-out ratios. Molded fiber trays and clamshells, in contrast, posted double-digit expansion, leveraging dry-forming efficiencies and fast-food conversions. Their superior cushioning, stackability, and print quality now satisfy both electronics OEMs and quick-service restaurants, challenging legacy polystyrene. Folding cartons continue serving premium confectionery and cosmetics, while nascent paper bottles attract beverage trials seeking brand differentiation. Specialty formats, including paperboard canisters and fiber drums, capture niche technical demands such as moisture-sensitive powders.

Second-order impacts ripple through supply contracts; converters adding in-house thermo-forming to address clamshell demand report utilization rates above 85%. Capex deployment tilts toward automation lines capable of switching between food-service and electronics skus, minimizing downtime. Regionalized tool-making further accelerates design iterations, shortening customer qualification cycles. Collectively, these shifts amplify molded fiber’s 13.16% CAGR advantage, sustaining its share climb within the broader compostable paperboard packaging market.

By End-User Industry: Consumption patterns drive premiumization

Food and beverage firms accounted for USD 13.6 billion in 2024, leveraging existing filler infrastructure compatible with fiber-based cartons. Retailers cite reduced landfill fees and positive consumer sentiment as deciding factors. Personal care and cosmetics, although smaller, outpaced overall market growth, gaining traction in skin-care kits that use molded fiber inserts to replace plastic trays. Online subscription boxes further amplify demand in this segment. Food-service operators pivot under municipal bans and consumer pushback, migrating hot-cup lids, bowls, and cutlery toward certified compostability. Household care lags due to detergent compatibility issues with aqueous barriers, yet pilots using mineral-coating technology show promise in powder formats.

Marketing teams harness narrative value; brand storytelling around renewable inputs resonates with eco-conscious demographics, allowing premium pricing in discretionary categories. Meanwhile, industrial users migrate slowly because mechanical robustness still favors standard corrugated. Bridging this gap requires hybrid structures fiber outer shells paired with minimalist bio-films currently under joint development among converters and chemical suppliers.

By Material Source: Virgin fiber regains favor for performance-critical packs

While recycled grades comprised more than half of 2024 volumes, virgin fiber shipments expanded faster, driven by barrier and food-contact specifications that recycled pulp struggles to meet. Nordic producers leverage sustainably managed forests to supply virgin kraft with chain-of-custody certification, commanding price premiums of 8-12%. Australia’s rising recycled-content mandates sustain demand for post-consumer fiber, yet brand owners of infant-nutrition and premium confectionery prefer virgin stock to eliminate contamination risk. Certification wins, such as Metsä Board’s DIN CERTCO home-compostability rating, further bolster virgin positioning. [3]Metsä Board, “Home Compostability Certification for Metsä Board Paperboards,” Metsagroup.com, METSAGROUP.COM

Supply strategies now balance cost, performance, and regulatory optics. Some multinationals adopt dual-spec approaches: recycled content for outer shipping cases, virgin for direct-food contact. The compostable paperboard packaging market thus bifurcates into commodity and premium tiers, each with distinct sourcing ecosystems.

By Functional Coating: Aqueous dispersion gains momentum

PLA and bio-polymer laminates generated USD 14.6 billion in 2024 underpinned by mature food-service channels, yet face scrutiny over industrial composting needs. Aqueous and mineral dispersion coatings, registering the highest 13.28% CAGR, win share by enabling home compostability and aligning with PFAS restrictions. Multilayer silicon-oxide barrier systems extend shelf life for high-oil snacks without compromising recyclability. Un-coated grades remain viable for dry commodities, although moisture-sensitive goods increasingly demand performance films.

Innovation cycles compress as converters co-develop chemistries with specialty chemical partners, accelerating certification pipelines. Cost parity with poly-laminate is in sight once scale passes 500 million m² annually, a milestone expected by 2027 in Europe. This trajectory threatens PLA’s current leadership, especially in regions where industrial composting remains scarce.

By Distribution Channel: Direct sourcing reshapes value capture

Converters shipped more than USD 20 billion of compostable paperboard in 2024, yet brand-owner direct procurement is climbing swiftly. Fast-moving consumer-goods companies sign multi-year supply agreements to secure capacity amid tightening fiber markets. Graphic Packaging’s investment in Waco boosts recycled board output earmarked for such direct deals. Meanwhile, e-commerce giants pilot on-site corrugators paired with proprietary design software, reducing reliance on third-party converters. The trend redistributes margin upstream to fiber producers and downstream to brand owners, pressuring mid-tier converters to specialize or consolidate.

Hybrid models emerge converters offer design and certification services while allowing customers to own tooling. This collaboration mitigates capital risk yet keeps technical expertise with the converter, ensuring mutual dependency. Vertical integration will likely advance further as compostable paperboard packaging market participants chase security of supply.

Geography Analysis

Europe controlled USD 11.8 billion, equal to 35.94% of 2024 revenue, supported by harmonized EPR rules and dense composting networks. Germany’s Green Dot fees and France’s AGEC law force retailers to switch formats, while Nordic mills provide competitively priced virgin kraft sourced from certified forests. Inflationary energy costs pinch margins but stimulate energy-efficient dry-forming investments, reinforcing regional technology leadership.

Asia-Pacific, advancing at a 12.95% CAGR, will eclipse Europe in absolute growth by 2027 as Japan’s renewable-plastic roadmap and China’s circular-economy statutes converge. Large population centers amplify volume upside, and government grants underwrite composting infrastructure, mitigating the processing bottleneck. Emerging Southeast Asian economies piggyback on manufacturing relocations, feeding regional converter clusters that export to Europe and North America.

North America shows heterogeneous progress. California’s SB 54 and Washington’s labeling law produce demand hotspots, whereas central states lag amid infrastructure gaps. Federal recycling-modernization grants totaling up to USD 43 billion prioritise organics facilities, potentially unlocking a second-wave growth cycle once projects come online. Canada aligns closely with US standards, while Mexico’s near-shoring surge incentivizes export-oriented plants to choose compostable solutions for tariff-favored goods entering the United States.

Competitive Landscape

Industry concentration remains moderate as the top five suppliers capture roughly 38% revenue, leaving room for disruptors. The Smurfit Westrock merger yields a diversified giant with USD 34 billion in pro-forma 2024 sales and an R&D war-chest exceeding USD 300 million, enabling rapid barrier-coating development. International Paper’s DS Smith acquisition extends its European footprint and deepens corrugated expertise aligned with compostable mandates.

Mid-cap firms pursue specialization; Cascades Sonoco scales its FlexSHIELD aqueous line, carving a niche in PFAS-free food service. Stora Enso restructured around four renewable-packaging divisions, dedicating 60% of revenue to fiber innovation.Patent filings in nanocellulose and mineral-hybrid coatings climb, signaling knowledge-based defensibility. Nevertheless, capital intensity and certification hurdles create barriers that partly shield incumbents from new entrants, sustaining stable yet dynamic competition in the compostable paperboard packaging market.

Compostable Paperboard Packaging Industry Leaders

Smurfit WestRock PLC

Stora Enso Oyj

Mondi Group PLC

Huhtamaki Oyj

Graphic Packaging International LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Stora Enso finalized its renewable-packaging realignment and accelerated Oulu board-line ramp-up toward 2027 full capacity.

- February 2025: International Paper closed its purchase of DS Smith, enhancing global sustainable-packaging coverage.

- July 2024: Mondi allocated EUR 1.2 billion to organic growth, debuting TrayWrap kraft paper and FlexiBag Reinforced solutions.

- March 2024: California’s CalRecycle initiated SB 54 rulemaking, obligating producer-responsibility group enrollment by Jan 2024.

Global Compostable Paperboard Packaging Market Report Scope

| Folding Cartons |

| Corrugated and Solid Fibre Boxes |

| Foodservice Take-Out Containers |

| Molded Fibre Trays and Clamshells |

| Paper Bottles and Canisters |

| Specialty / Other |

| Food and Beverage Manufacturing |

| Foodservice and Delivery |

| Personal Care and Cosmetics |

| Household and Home-care |

| Healthcare and Pharmaceuticals |

| Industrial and Other |

| Virgin Fibre |

| Recycled Fibre |

| PLA / Bio-polymer Coated |

| Aqueous and Mineral Dispersion |

| Un-coated / No-added-PFAS |

| Packaging Converters |

| Brand-owner Direct Sourcing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Thailand | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Folding Cartons | ||

| Corrugated and Solid Fibre Boxes | |||

| Foodservice Take-Out Containers | |||

| Molded Fibre Trays and Clamshells | |||

| Paper Bottles and Canisters | |||

| Specialty / Other | |||

| By End-user Industry | Food and Beverage Manufacturing | ||

| Foodservice and Delivery | |||

| Personal Care and Cosmetics | |||

| Household and Home-care | |||

| Healthcare and Pharmaceuticals | |||

| Industrial and Other | |||

| By Material Source | Virgin Fibre | ||

| Recycled Fibre | |||

| By Functional Coating | PLA / Bio-polymer Coated | ||

| Aqueous and Mineral Dispersion | |||

| Un-coated / No-added-PFAS | |||

| By Distribution Channel | Packaging Converters | ||

| Brand-owner Direct Sourcing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Thailand | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the compostable paperboard packaging market?

The compostable paperboard packaging market size reached USD 32.71 billion in 2025 and is projected to grow to USD 57.28 billion by 2030.

Which region is expanding fastest in compostable paperboard packaging?

Asia-Pacific is forecast to register a 12.95% CAGR through 2030, outpacing all other regions due to strong regulatory momentum and rapid urbanization.

Why are molded fiber trays gaining share over traditional corrugated boxes?

Dry-forming breakthroughs lower production costs and improve strength, enabling molded fiber trays to meet food-service and electronics cushioning requirements while offering compostability.

How do regulatory bans influence demand for compostable packaging?

Extended Producer Responsibility laws in the EU, California, and Australia raise compliance costs for plastics, creating a structural shift toward fiber-based, compostable alternatives.

What coating technologies are displacing PLA laminates?

Aqueous and mineral-dispersion barriers are scaling quickly because they enable home compostability and eliminate PFAS, addressing emerging health and regulatory concerns.

What is the primary constraint to broader adoption of compostable paperboard?

Limited industrial composting capacity in several regions hampers end-of-life processing for certain coated products, though infrastructure investment is accelerating to close this gap.

Page last updated on: