Blockchain-Enabled Paperboard Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

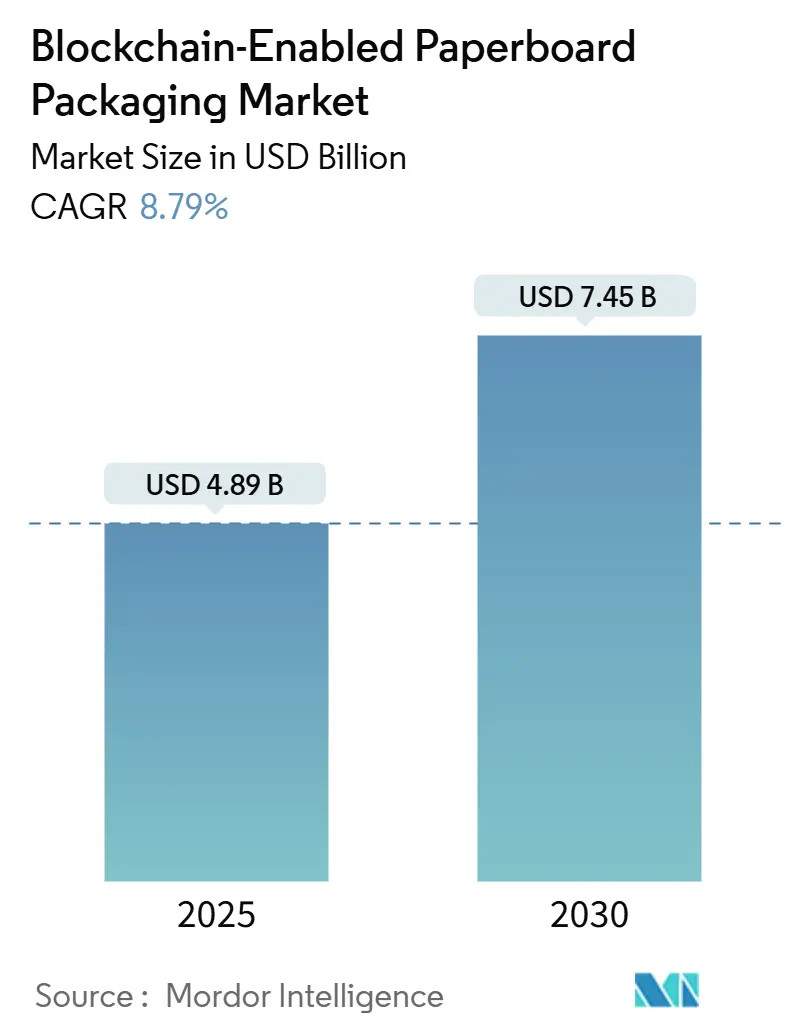

| Market Size (2025) | USD 4.89 Billion |

| Market Size (2030) | USD 7.45 Billion |

| Growth Rate (2025 - 2030) | 8.79% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

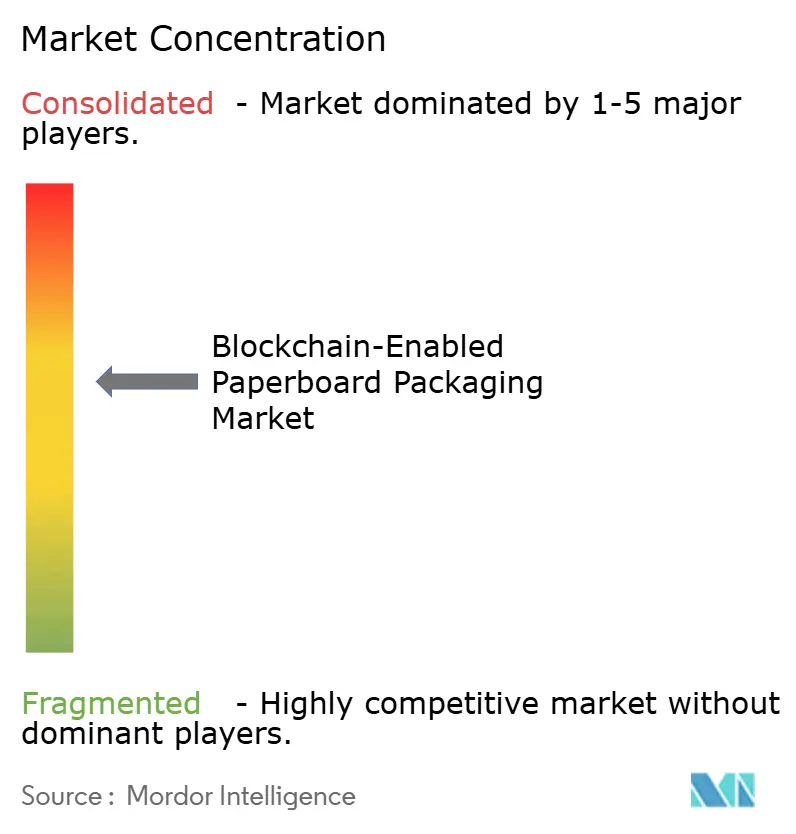

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blockchain-Enabled Paperboard Packaging Market Analysis by Mordor Intelligence

The blockchain-enabled paperboard packaging market size stands at USD 4.89 billion in 2025 and is forecast to reach USD 7.45 billion by 2030, reflecting an 8.79% CAGR. Momentum comes from the European Union’s Digital Product Passport mandate, the United States Food Safety Modernization Act (FSMA 204) traceability rule, and rising e-commerce parcel volumes. Brand owners view distributed-ledger cartons as a practical way to prove recycled-content claims, deter counterfeits, and automate customs documentation. Large converters are consolidating to spread integration costs, while pure-play technology firms escalate watermark and RFID innovation. Investments continue to shift toward cloud-native platforms that minimize blockchain energy consumption and improve recycling sortation accuracy.

Key Report Takeaways

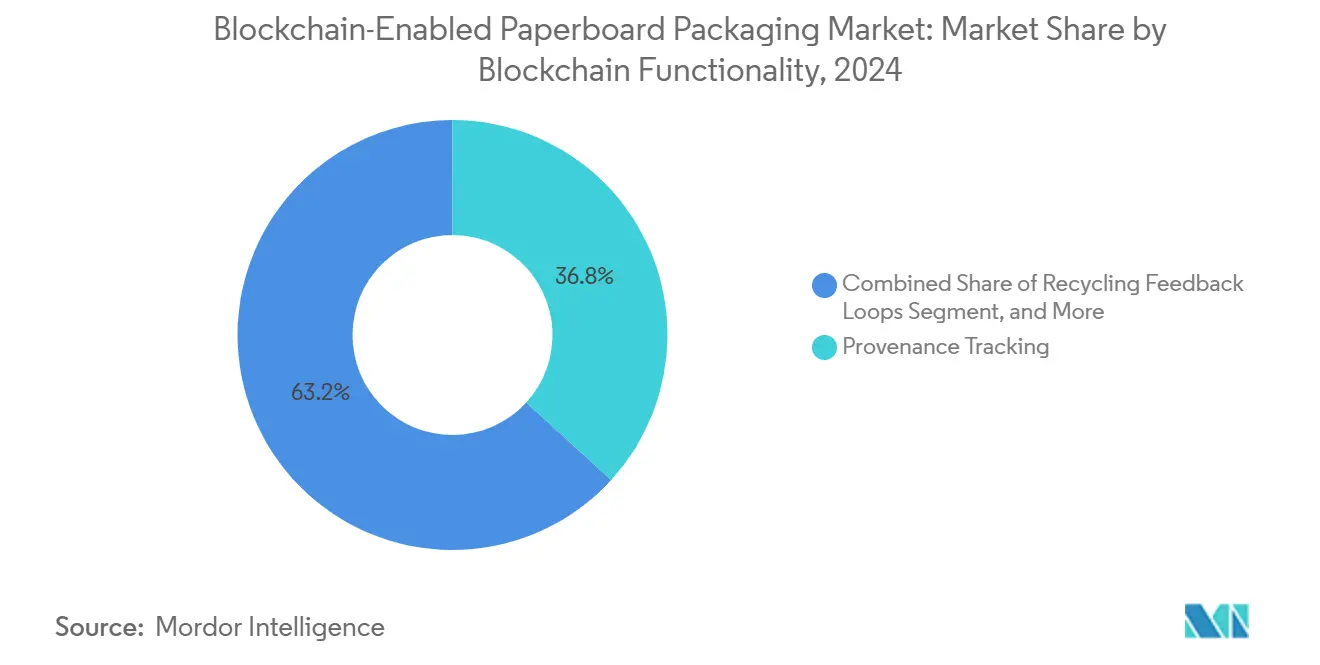

- By blockchain functionality, provenance tracking captured 36.79% of the blockchain-enabled paperboard packaging market share in 2024.

- By paperboard grade, the blockchain-enabled paperboard packaging market size for folding boxboard is projected to grow at a 9.52% CAGR between 2025-2030.

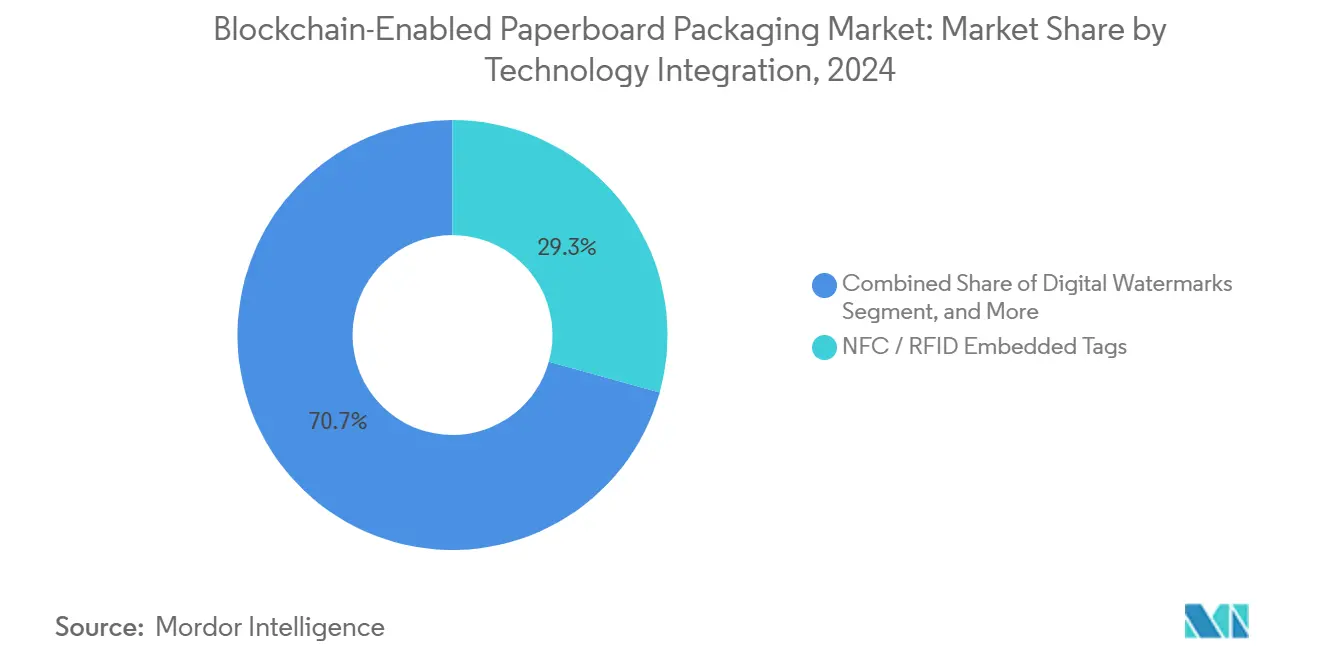

- By technology integration, NFC/RFID tags captured 29.31% of the blockchain-enabled paperboard packaging market share in 2024.

- By end-use, the blockchain-enabled paperboard packaging market size for e-commerce retail is projected to grow at a 9.36% CAGR between 2025-2030.

- By geography, North America captured 31.67% of the blockchain-enabled paperboard packaging market share in 2024.

Global Blockchain-Enabled Paperboard Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability-driven shift from plastic to recyclable paperboard packaging | +2.1% | Global, with strongest impact in EU and North America | Medium term (2-4 years) |

| E-commerce boom demands robust track-and-trace cartons | +1.8% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Brand demand for end-to-end supply-chain transparency | +1.5% | Global, particularly EU and North America | Medium term (2-4 years) |

| EU Digital Product Passport rules for packaging traceability | +1.3% | EU primary, with spillover to global exporters | Short term (≤ 2 years) |

| Voluntary carbon-credit traceability in fiber packaging projects | +0.9% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Luxury goods anti-counterfeit adoption of blockchain-secured cartons | +0.7% | Global, concentrated in luxury market hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sustainability-driven shift from plastic to recyclable paperboard packaging

Legislation curbing single-use plastics is accelerating migration toward fiber substrates that carry verifiable environmental credentials. International Paper reports that 98% of its corrugated and paperboard formats now meet curbside recyclability guidelines, allowing brands to comply with stringent waste-reduction laws.[1]International Paper, “Unboxing 2025's Sustainable Packaging Trends,” internationalpaper.com By coupling these cartons with distributed-ledger identifiers, manufacturers can document recycled-content percentages, chain-of-custody history, and carbon-footprint reductions. Certified data helps retailers substantiate eco-labels and justifies premium shelf pricing. Government-backed extended-producer-responsibility schemes further reinforce the need for immutable audit trails so that levies reflect genuine recovery rates. As compliance reporting shifts from voluntary disclosure to mandatory filings, converters able to supply ledger-ready board enjoy a growing order pipeline.

E-commerce boom demands robust track-and-trace cartons

Online retail volumes produce complex fulfillment networks where parcel integrity and delivery confirmation are critical. WestRock’s BornDigital cartons embed NFC tags that register custody transfers on blockchain nodes, lowering fraud, returns, and lost-in-transit disputes. Last-mile couriers scan the tag to confirm arrival, while consumers verify authenticity using smartphones. Cross-border merchants utilize the same data packet to pre-populate customs declarations, easing clearance delays. High-frequency parcel flows push warehouses to automate checking; immutable package IDs replace manual inspection and minimize labor. As holiday peak seasons strain capacity, the technology demonstrates tangible ROI through reduced chargebacks and faster dock-to-door cycles.

Brand demand for end-to-end supply-chain transparency

Stakeholders increasingly scrutinize source forests, mill practices, and labor conditions. DNV’s My Story QR labels convert technical provenance records into consumer-friendly narratives while preventing tampering through public-key cryptography. ESG-oriented investors reward suppliers that disclose verifiable metrics on deforestation and carbon intensity. Downstream retailers use the same ledger entries to validate responsible sourcing commitments during vendor audits. As litigation over greenwashing escalates, immutable documentation becomes a defensive requirement rather than a marketing add-on. Trade finance institutions also begin to link credit terms to transparent supply data, reinforcing the economic case for adoption.

EU Digital Product Passport rules for packaging traceability

Commencing 2027, the regulation obliges most goods sold in the bloc to carry a unique digital identity detailing repair, recycling, and sustainability attributes. Digimarc and IOTA have demonstrated an open-standard architecture that decentralizes storage yet permits authorized access across the chain. Carton converters must encode Global Trade Item Numbers plus serial identifiers directly on board surfaces or tags, ensuring compatibility with EU customs and recycling systems. As global brands adjust production lines to serve Europe, the blueprint is expected to become the de-facto global norm, spurring parallel deployments in export-oriented Asian plants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-front costs of blockchain and IoT integration in mills | -1.4% | Global, particularly impacting smaller manufacturers | Short term (≤ 2 years) |

| Data privacy and interoperability concerns across partners | -1.1% | Global, with stricter requirements in EU and Asia-Pacific | Medium term (2-4 years) |

| RFID/digital-watermark recyclability contamination risk | -0.8% | Global, especially in markets with advanced recycling infrastructure | Long term (≥ 4 years) |

| Energy footprint of public blockchains vs sustainability claims | -0.6% | Global, with heightened scrutiny in environmentally conscious markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Up-front costs of blockchain and IoT integration in mills

Capital outlays for sensors, cloud nodes, and training stretch thin cash flows at small and mid-size paperboard plants. Installation disrupts production, and ongoing maintenance introduces unfamiliar cybersecurity tasks. Transaction fees, data-storage subscriptions, and periodic hardware refresh escalate total cost of ownership. Scale advantages allow majors such as Smurfit Westrock to amortize investments, accelerating consolidation as smaller players seek alliances or exit. Although cloud-native ledgers reduce hardware burden, budget constraints still delay near-term rollouts in emerging markets.

Data privacy and interoperability concerns across partners

Ledgers thrive on shared visibility, yet suppliers hesitate to expose pricing, factory yields, or forest-source maps that competitors might mine. Jurisdictional patchworks from Europe’s GDPR to South Korea’s Digital Assets Basic Act enforce varied consent rules, raising compliance complexity. Inconsistent data models across competing blockchain platforms further inhibit seamless exchange. To mitigate, consortia now publish open APIs and allow selective disclosure of sensitive fields. Still, negotiations over ownership of analytics derived from shared data prolong deployment cycles and weigh on adoption rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Blockchain Functionality: Provenance tracking underpins early compliance

Provenance modules commanded 36.79% of 2024 revenue as regulators and consumers seek immediate visibility into fiber origin and custody events. The blockchain-enabled paperboard packaging market benefits because converters can integrate QR or NFC IDs without reinventing box designs. Recycling feedback loops, though smaller, will grow fastest at 9.65% CAGR by enabling deposit-return verification and curbside sortation incentives. Anti-counterfeit coding remains vital in luxury spirits and pharma vials, whereas consumer-engagement smart coupons add loyalty value for mainstream brands. Carbon accounting is gaining ground as cloud platforms, such as atma.io on Hedera, track emissions at the individual-item level, supplying auditors with immutable Scope 3 data. Over the outlook, blended applications are expected, where a single tag supports provenance, recycling credits, and loyalty points simultaneously to optimize unit economics.

The future mix will hinge on regulatory layering. As Digital Product Passport requirements widen, provenance becomes a baseline feature, pushing suppliers to differentiate via circular metrics and consumer interaction add-ons. Because each extra ledger field marginally increases data storage costs, brands will prioritize modules with clear financial payback, such as reduced recall liability or fraud losses. Meanwhile, open-source smart-contract libraries lower development barriers, letting SME brands pilot feedback-loop incentives without deep coding expertise. This democratises access but intensifies competition among platform vendors for value-added analytics subscriptions.

By Paperboard Grade: SBS retains premium share, FBB gains pace

Solid Bleached Sulfate held 32.56% of the blockchain-enabled paperboard packaging market share in 2024, owing to its smooth print surface that supports high-density watermarks and embedded antennas. SBS dominates cosmetics, pharma, and gift spirits cartons where pristine aesthetics justify added tag costs. Folding Boxboard is projected to post a 9.52% CAGR, lifted by frozen-food and meal-kit demand that values FBB’s freezer tolerance and lighter grammage. Coated Unbleached Kraft and White-lined Chipboard address budget segments, often adopting lower-cost QR coding rather than embedded electronics.

Substrate selection influences tag type; thicker corrugated liners can house RFID inlays without compromising bending stiffness, whereas thin micro-flute retail packs favor discreet digital watermarks. Sappi’s ISBC RFID Paper illustrates how electronic components can be laminated into fiber layers without plastic films, aligning with recyclability targets. This innovation narrows performance gaps between premium SBS and workhorse kraft grades, potentially redistributing share toward mid-priced options by 2030.

By Technology Integration: NFC/RFID mature, watermarks accelerate

NFC and passive UHF RFID tags captured 29.31% revenue in 2024 through proven reliability and smartphone compatibility. They power interactive campaigns: consumers tap to see provenance or claim loyalty tokens. Cost, however, remains a constraint for low-margin food cartons. Digital watermarks, imperceptible patterns printed across the substrate, are on track for a 9.48% CAGR. They require no silicon and no visible codes, reducing unit cost and protecting brand aesthetics. Digimarc’s GPU-optimized sortation engine reads these marks at belt speeds, slashing recycling‐plant labor spend by almost 50%.[2]Digimarc, “Revolutionizes Recycling with GPU-Optimized Sortation Software,” digimarc.com

Molecular markers are emerging for high-risk pharmaceuticals, embedding chemical signatures detectable with handheld scanners. Hybrid deployments mix visible GS1 Digital Link codes for retail with invisible watermarks for MRF identification. Tag choice increasingly aligns with end-of-life pathways; municipalities that invest in optical sorters favor watermark adoption to meet circular‐economy quotas.

By End-use Industry: Food and beverage dominate, e-commerce surges

Food and beverage applications accounted for 38.94% revenue in 2024 as the FSMA 204 rule compels high-risk product traceability by January 2026. Blockchain cartons log farm identifiers, processing dates, and temperature excursions, enabling rapid recall when pathogens emerge. E-commerce parcels will register a 9.36% CAGR through 2030 because shoppers expect proof of authenticity and secure proof-of-delivery. Personal-care brands deploy ledger tags to disclose ingredient sourcing and affirm cruelty-free claims, while electronics components rely on serialization to guard against counterfeit parts.

Healthcare packaging demands the highest security; IBM and boards of pharmacy operate consortia where tamper-evident NFC chips authenticate each dose. Luxury maison houses leverage the Aura consortium’s QR chips to certify exclusivity, reducing chargebacks on secondary markets. Collectively, these verticals diversify revenue, cushioning converters from cyclical demand in any single sector.

Geography Analysis

North America led the blockchain-enabled paperboard packaging market with a 31.67% revenue share in 2024, underpinned by mature tracing statutes and robust technological infrastructure. Large integrated mills partner with cloud providers to roll out item-level IDs across grocery packaging. The region’s high e-commerce penetration drives merchant adoption, while consumer litigation risks incentivize immutable food safety data. State sustainability bills under debate could tighten disclosure rules further, sustaining investment momentum.

Europe follows closely, driven by the Digital Product Passport and plastic-reduction directives. Regional converters pilot board-level QR coding to meet 2027 compliance deadlines. Luxury goods clusters in Italy and France implement NFC chips to elevate brand experience and deter counterfeits. Public recycling systems collaborate with Digimarc watermark trials to achieve 2030 circular targets. Government grants offset SME integration costs, helping diffuse the technology across mid-tier folding carton plants.

Asia-Pacific represents the fastest-growing opportunity, forecast at 9.71% CAGR. Hong Kong’s stablecoin ordinance offers regulatory certainty for ledger tokenization of supply data. China’s Ministry of Commerce pilots blockchain customs corridors, signaling an eventual scale deployment once standards settle. Japanese electronics exporters deploy RFID-enhanced corrugated shippers to authenticate high-value modules. In India, Asahi Kasei’s Akliteia platform authenticates specialty films packaged in digitally marked cartons, reflecting rising anti-counterfeit demand.[3]Asahi Kasei, “Akliteia™ Digital Platform in India,” asahi-kasei.com

Competitive Landscape

The competitive field is moderately fragmented, with incumbents and tech specialists converging. Smurfit Westrock integrates NFC modules through joint ventures while maintaining cost leadership across commodity grades. Its USD 7.7 billion quarterly sales illustrate scale leverage in absorbing digital-conversion expenses. Digimarc focuses on watermark IP, reporting subscription revenue of USD 23.9 million and forging alliances with Avery Dennison and HP to evangelize code standards.

Avery Dennison’s atma.io manages more than 30 billion serialized items, anchoring a growing SaaS recurring base while extending carbon-credit functionality via the Hedera network ATM A.IO. Security Matters commercializes invisible molecular marking, targeting beverage bottlers seeking plastic-free authentication. Start-ups that master low-energy ledger protocols and recyclable tag designs attract venture capital, while smaller carton printers ally with platform vendors to avoid sunk R&D costs. Patent races center on energy-efficient consensus algorithms and fiber-embedded antenna methods, indicating intensifying innovation cycles up to 2030.

Blockchain-Enabled Paperboard Packaging Industry Leaders

Smurfit Westrock plc

International Paper Company

Mondi plc

Graphic Packaging Holding Company

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Smurfit Westrock posted net sales of USD 7,656 million and net income of USD 382 million, citing sustained capital spending on digital carton plants.

- February 2025: Digimarc announced FY 2024 subscription revenue of USD 22.4 million and set a target of positive net income by Q4 2025 through expanded authentication uses.

- December 2024: Digimarc partnered with Picadeli to integrate watermarking in fresh-food packaging for tamper protection during self-checkout.

- December 2024: Digimarc released GPU-optimized recycling sortation software that halves operating costs at material recovery facilities.

- May 2024: Avery Dennison’s atma.io integrated Hedera ledger services to tokenise carbon accounts across 22 billion items.

Global Blockchain-Enabled Paperboard Packaging Market Report Scope

| Provenance Tracking |

| Anti-Counterfeit Authentication |

| Consumer Engagement / Smart Loyalty |

| Carbon Footprint Accounting |

| Recycling Feedback Loops |

| Solid Bleached Sulfate (SBS) |

| Coated Unbleached Kraft (CUK) |

| Folding Boxboard (FBB) |

| White-lined Chipboard (WLC) |

| Containerboard / Corrugated |

| QR / GS1 Digital Link Codes |

| NFC / RFID Embedded Tags |

| Digital Watermarks |

| Invisible Molecular Markers |

| Food and Beverage |

| Personal Care and Cosmetics |

| Healthcare and Pharmaceuticals |

| Luxury Goods and Spirits |

| E-commerce Retail |

| Industrial and Electronics |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Blockchain Functionality | Provenance Tracking | ||

| Anti-Counterfeit Authentication | |||

| Consumer Engagement / Smart Loyalty | |||

| Carbon Footprint Accounting | |||

| Recycling Feedback Loops | |||

| By Paperboard Grade | Solid Bleached Sulfate (SBS) | ||

| Coated Unbleached Kraft (CUK) | |||

| Folding Boxboard (FBB) | |||

| White-lined Chipboard (WLC) | |||

| Containerboard / Corrugated | |||

| By Technology Integration | QR / GS1 Digital Link Codes | ||

| NFC / RFID Embedded Tags | |||

| Digital Watermarks | |||

| Invisible Molecular Markers | |||

| By End-use Industry | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| Healthcare and Pharmaceuticals | |||

| Luxury Goods and Spirits | |||

| E-commerce Retail | |||

| Industrial and Electronics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the blockchain-enabled paperboard packaging market in 2025?

The blockchain-enabled paperboard packaging market size is USD 4.89 billion in 2025.

What CAGR is expected through 2030 for blockchain-enabled paper cartons?

The market is projected to grow at an 8.79% CAGR between 2025 and 2030.

Which blockchain functionality currently generates the most revenue?

Provenance tracking leads, holding 36.79% of 2024 revenue.

Which end-use segment is expanding the fastest?

E-commerce retail packaging is forecast to advance at 9.36% CAGR to 2030.

Why is Europe important for blockchain carton adoption?

The EU Digital Product Passport mandates unique digital identities from 2027, driving continent-wide deployment and influencing global exporters.

What technology type offers cost-effective item-level tracking?

Digital watermarks provide low-cost, silicon-free serialization and are growing at 9.48% CAGR.

Page last updated on: