Regulatory Advisory Services For Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

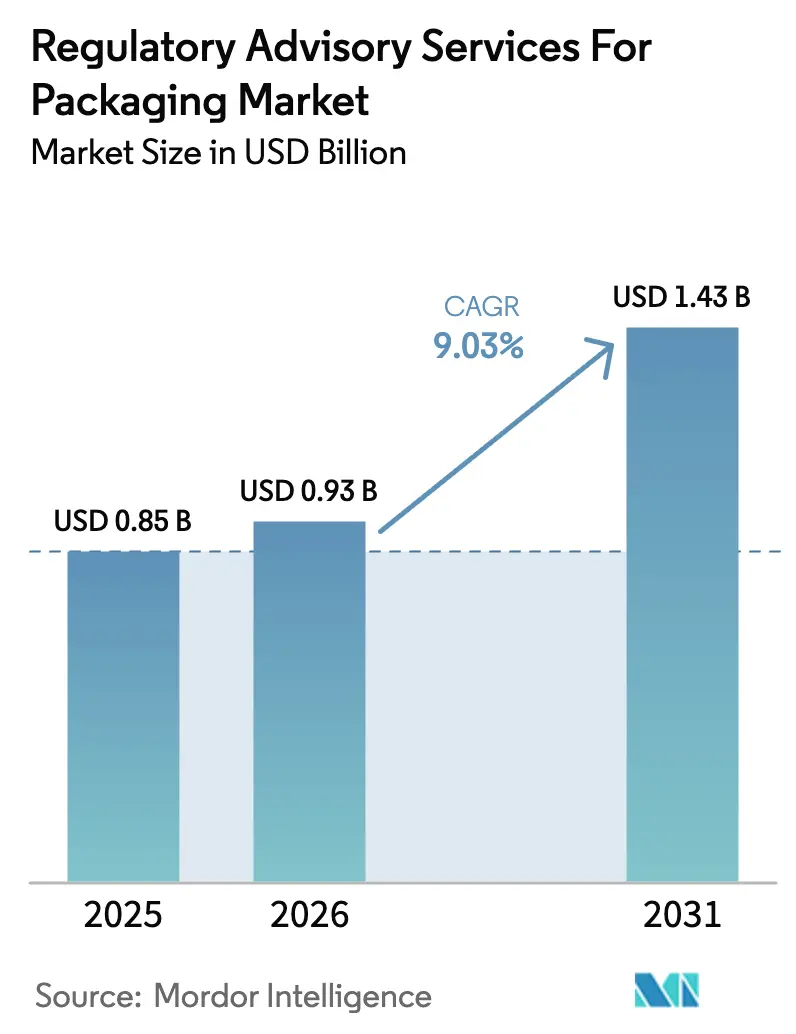

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.43 Billion |

| Growth Rate (2026 - 2031) | 9.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

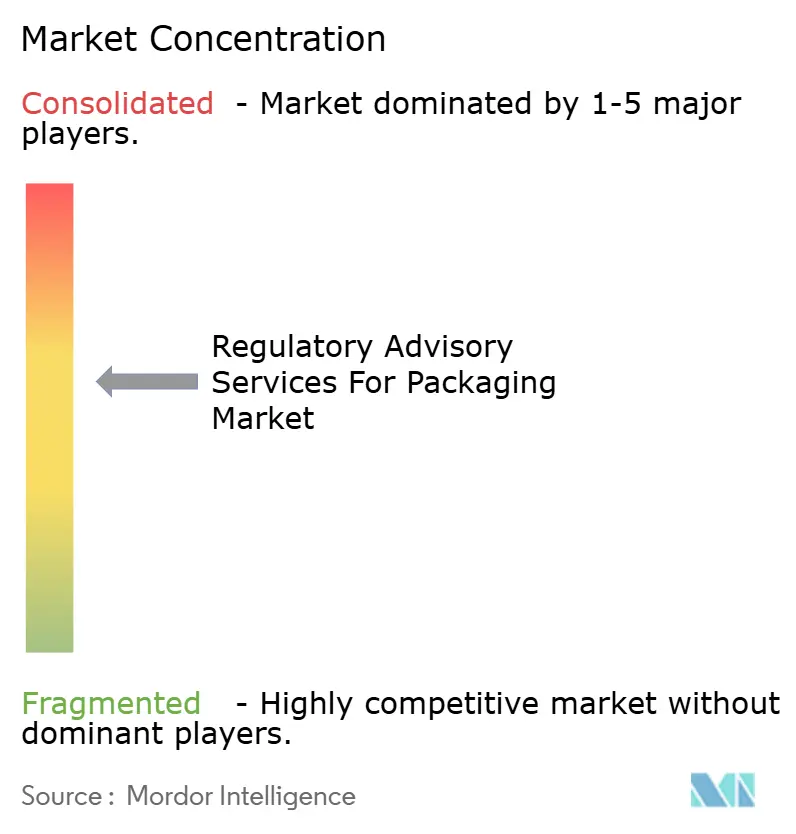

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Regulatory Advisory Services For Packaging Market Analysis by Mordor Intelligence

The regulatory advisory services market size in 2026 is estimated at USD 0.93 billion, growing from 2025 value of USD 0.85 billion with 2031 projections showing USD 1.43 billion, growing at 9.03% CAGR over 2026-2031. Converging regulatory pressures from the EU Packaging and Packaging Waste Regulation (PPWR), proliferating extended producer responsibility (EPR) schemes, stricter FDA food-contact materials (FCM) pathways, and accelerating digital passport requirements are sustaining demand for specialist guidance. Brand owners now treat compliance data as a competitive asset, shifting spending toward predictive regulatory intelligence and automated documentation workflows. Mid-sized packaging converters increasingly outsource dossier preparation, realizing that fragmented fee structures and overlapping submission portals make in-house compliance cost-prohibitive. Digitalization mandates, such as EU product passports and U.S. Customs import gate data filings, further elevate advisory spend as companies race to harmonize data flows between enterprise resource planning systems and regulatory portals. Meanwhile, the global shortage of senior regulatory toxicologists and qualified packaging auditors tightens service capacity, supporting premium bill-out rates across all regions.

Key Report Takeaways

- By service type, compliance documentation and dossier preparation captured 28.33% of the Regulatory Advisory Services for Packaging Market share in 2025.

- By material, the Regulatory Advisory Services for Packaging Market size for biobased/compostable materials is projected to grow at a 11.12% CAGR between 2026-2031.

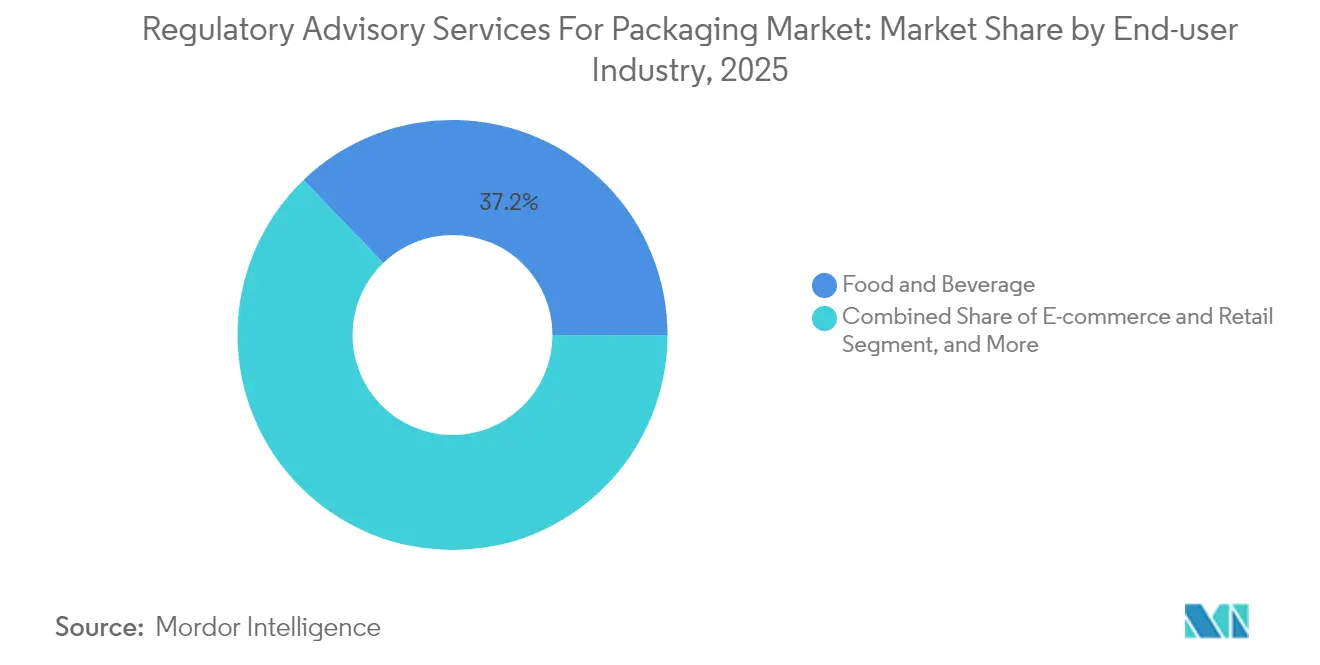

- By end-user, food and beverage companies captured 37.18% of the Regulatory Advisory Services for Packaging Market share in 2025.

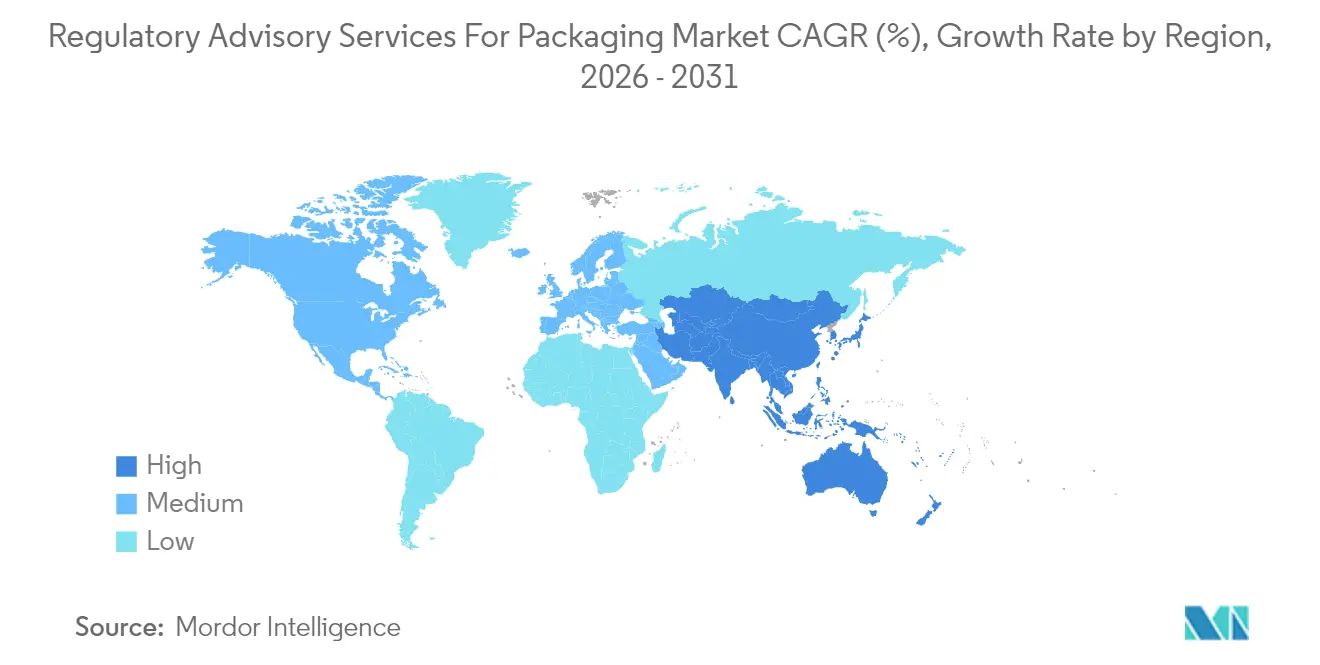

- By geography, the Regulatory Advisory Services for Packaging Market size in Asia-Pacific is projected to grow at 11.58% CAGR between 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Regulatory Advisory Services For Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU PPWR Compliance Deadlines Accelerating Advisory Spend | +2.1% | Europe, with spillover to North America and Asia-Pacific | Medium term (2-4 years) |

| Global Proliferation of EPR Schemes for Packaging | +1.8% | Global, with early gains in Asia-Pacific, Europe, North America | Long term (≥ 4 years) |

| Stricter FDA Pathways for Food-Contact Materials | +1.4% | North America, with regulatory influence on global FCM standards | Medium term (2-4 years) |

| Brand-Owner Race to Validated "Non-HFSS / PFAS-Free" Claims | +1.2% | Global, with a concentration in North America and Europe | Short term (≤ 2 years) |

| AI-Driven Compliance-Cloud Platforms Preferred by SMEs | +1.6% | Global, with early adoption in Europe and North America | Short term (≤ 2 years) |

| Import-Gate Digital Product-Passport Requirements in CBP ACE | +1.0% | North America, with an influence on global supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU PPWR compliance deadlines accelerating advisory spend

Mandatory recyclability assessments, enforced in January 2025, and digital product passports, due in July 2025, have spurred a surge in documentation projects, particularly among consumer-packaged-goods multinationals that outsource dossier preparation. Companies unable to validate design-for-recycling metrics risk distribution bans, so advisory firms report three-fold spikes in European service backlogs. SMEs lean on subscription platforms that scrape PPWR annex updates daily, yet still require experts to interpret exemptions for multilayer laminates.[1]European Environment Agency, “PPWR Compliance Requirements and Technical Criteria,” eea.europa.eu Material suppliers, meanwhile, commission recyclability test protocols to defend sales with conversion customers. The result is heightened, time-sensitive demand across Europe, rippling into North American exporters that ship into the single market.

Global proliferation of EPR schemes for packaging

Forty-seven jurisdictions operated active packaging EPR frameworks in 2024, and a further 23 announced or expanded schemes through 2025, multiplying report templates and fee calculators that multinational manufacturers must master. The Asia-Pacific region leads the count, with Japan focusing on e-commerce parcels, South Korea expanding to biobased formats, and India setting a 70% producer responsibility target by 2030. Advisory specialists now bundle tariff simulations with EPR strategy to help brands model fee exposure and redesign SKU portfolios. Harmonization is unlikely before 2030, ensuring steady, recurring consulting revenue as every rule change triggers data re-submission.

Stricter FDA pathways for food-contact materials

The FDA’s January 2025 rule requires more comprehensive toxicology and migration datasets before new packaging polymers, coatings, or recycled resins can win approval. Over 200 PFAS substances were subject to immediate review, prompting a rush of filings and retainer contracts with toxicology-focused advisers. Biobased resin developers face the longest timelines because bio-sourced impurities require additional risk assessment. As federal scrutiny tightens, guidance requests now include parallel EU and Mercosur dossiers to avoid dual regulatory surprises, thereby lifting cross-regional advisory volumes.

Brand-owner race to validated "non-HFSS / PFAS-free" claims

Retailers elevated chemical-safety scorecards in 2025, compelling suppliers to remove PFAS coatings while maintaining barrier functionality. Detection thresholds below 10 ppb drive lab complexity, prompting companies to seek third-party validation to avoid greenwash litigation. Packaging lines are converted to alternative barriers, such as silicon oxide or water-based acrylics, yet they require comparative migration data, which extends project timelines. Advisory demand spikes earliest in snack, dairy, and fast-food categories, where grease resistance is critical.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Fragmentation of National EPR Fee Structures | -1.3% | Global, with a concentration in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Shortage of Senior Regulatory Toxicologists and Auditors | -1.1% | Global, with acute shortages in North America and Europe | Medium term (2-4 years) |

| Uncertainty Around Recycled-Content Mass-Balance Verification | -0.8% | Global, with regulatory influence from the EU and North America | Medium term (2-4 years) |

| Hidden Liability Exposure From "Scope-Creep" ESG Claims | -0.6% | Global, with a concentration in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High fragmentation of national EPR fee structures

Divergent eco-modulation formulas across EU states mean the same pouch can incur a five-fold fee variance, undermining portfolio-wide cost predictability. Asia-Pacific adds another layer of fragmentation, with weight-based schedules in Japan and recyclability-bonus models in South Korea. Advisory firms must recalibrate databases monthly, driving internal cost overheads that limit scalable margin capture. Brands, in turn, hesitate to accelerate packaging redesign when fee algorithms shift annually, thereby tempering service growth potential.

Shortage of senior regulatory toxicologists and auditors

Vacancy rates for senior toxicologists reached 45% in 2024, and average hiring cycles exceeded nine months. Certification backlogs compel consultancies to prioritize projects, thereby lengthening the turnaround time for complex FCM assessments. Training pipelines lag, with only 400 board-eligible professionals graduating annually worldwide. The shortage inflates labor rates, raising project bids, and deters some price-sensitive SMEs from entering full-service retainers, thus capping addressable demand growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Advisory digitalization unlocks scale

The regulatory advisory services market size for compliance documentation reached USD 0.24 billion in 2025, underscoring its role as a foundational revenue pillar in the industry. Digital platforms, though smaller, accelerated at 10.61% CAGR as cloud-native engines harvest legislation feeds, flag obligations, and auto-populate reporting templates. Large enterprises embed these feeds into governance dashboards, whereas SMEs prefer subscription portals with embedded chat and consultant support. Testing and certification workstreams gained momentum in response to PFAS and recyclability test mandates, while training services underperformed due to constrained instructor capacity.

A structural shift is underway: firms are now blending traditional advisory retainers with platform licenses to reduce the number of manual hours per project. The regulatory advisory services market is therefore transitioning to outcome-based billing that ties fees to dossier approvals or EPR cost savings. Providers with proprietary rules engines secure higher renewal rates than pure-play consultants, which explains the rising M&A activity as incumbents purchase reg-tech startups.

By Material: Biobased formats amplify complexity

Plastics retained the lion’s share amid overlapping EPR fees, FDA FCM reviews, and audits for verifying recycled content. Within the plastics industry, chemical recycling claims trigger intensive mass-balance verification projects, each priced at premium hourly rates. Paper-based formats continue to see sustained demand for PFAS substitution guidance and fit-for-purpose testing of recycled fiber. The regulatory advisory services market share for biobased and compostable materials, while still modest, is expanding fastest as brand owners pilot PLA, PHA, and fiber-blend substrates.

Compliance hurdles for biobased options include inconsistent biodegradability test methods, country-specific labeling icons, and competing performance thresholds between industrial and home composting. Advisory engagements often span material science, life-cycle assessment, and consumer-facing claim substantiation. As a result, firms with multidisciplinary teams capture a higher wallet share per client, thereby reinforcing their competitive differentiation.

By End-user Industry: E-commerce raises the innovation bar

Food and beverage companies dominate advisory spending because every FCM change requires an FDA or EU risk assessment, whereas supermarket chains impose PFAS-free and recyclability scorecards. Pharmaceutical and cosmetics players rely on niche toxicology support, but they represent a lower volume overall. E-commerce retailers, however, recorded the fastest spend growth as extended producer responsibility laws now cover mailers, fillers, and return-ready packaging.

E-commerce also confronts emerging digital product passport obligations for cross-border shipments. Integrating barcode systems into warehouse management software requires IT-savvy advisory teams comfortable mapping packaging data to customs filings. Early adopters see logistics savings once harmonized identifiers replace multiple national labels. This fuels double-digit growth for providers that couple regulatory guidance with systems integration know-how, signaling a lucrative niche over the forecast horizon.

Geography Analysis

Europe remained the epicenter of regulatory activity, generating 35.40% of global revenue in 2025, driven by imminent PPWR milestones and advanced national EPR overlays. Germany and France lead demand due to their complex eco-modulation and stringent recyclability scoring rubrics. Scandinavia’s digital-first governance accelerates the uptake of cloud reporting platforms, fostering advisory opportunities in data integration. Eastern European members, newly subject to harmonized PPWR rules, engage external consultants to translate directives into local implementation roadmaps, further broadening regional workload.

The Asia-Pacific region is forecasted to lead growth at a 11.58% CAGR, driven by the rollout of second-generation EPR frameworks in Japan, South Korea, and India. Local brand owners often lack historical compliance teams, so regional advisory firms fill knowledge gaps on reporting cadences and fee optimization. [2]Asia-Pacific Economic Cooperation, “Regional EPR Scheme Development Updates,” apec.org . China’s policy pilots on chemical recycling credits create experimental advisory assignments, yet are tempered by uncertain national-level rollout timelines. Australia and New Zealand maintain smaller volumes but exhibit high platform adoption ratios, preferring self-service dashboards with periodic expert audits.

North America features a fragmented state-by-state EPR rollout plus a single federal FCM pathway, producing a demand mix skewed toward strategic roadmap consulting and toxicology retainers. U.S. importers simultaneously prepare for Customs and Border Protection digital passport data uploads via the ACE portal, compelling integration projects between enterprise systems and customs filings. Canada’s federal plastics registry and provincial EPR statutes intensify cross-border data-harmonization needs. Mexico’s nascent regulatory push offers first-mover opportunity for bilingual advisory teams specializing in harmonizing North American Supply Chain Act requirements with local standards.

Competitive Landscape

The regulatory advisory services market is moderately fragmented, with no single company controlling more than 8% of global revenue. Testing conglomerates, such as SGS, Intertek, and Bureau Veritas, utilize their extensive worldwide laboratory footprints and brand credibility to secure contracts for recyclability and migration tests.

Niche consultancies excel in tackling biobased safety dossiers or AI risk-screening algorithms, often partnering with larger players for laboratory execution. Digital newcomers deliver subscription-based rule-engines that notify clients of regulatory changes, monetized through tiered access models. Consolidation is intensifying as incumbents acquire reg-tech outfits to embed automated data scraping and fee calculators, evident in Intertek’s 2025 purchase of Regulatory Science Associates.[3]McKinsey and Company, “Regulatory Technology Adoption in Packaging Industry,” mckinsey.com

Talent scarcity also drives mergers that add scarce toxicologists, while private equity funds target platform providers with sticky annual recurring revenue. Price competition remains muted because project outcomes hinge on interpretive expertise rather than commodity deliverables. Providers able to prove accelerated dossier clearance or EPR fee savings secure multi-year master service agreements, building annuity-style revenue streams.

Regulatory Advisory Services For Packaging Industry Leaders

SGS SA

Intertek Group plc

Bureau Veritas SA

UL Solutions Inc.

TÜV SÜD AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: SGS SA invested EUR 15 million (USD 16.95 million) to automate recyclability assessments across five European labs.

- September 2025: Intertek Group plc acquired Regulatory Science Associates for USD 45 million to bolster FCM toxicology depth.

- August 2025: Bureau Veritas SA introduced an AI-enabled EPR fee platform covering 23 schemes under a subscription model.

- July 2025: UL Solutions Inc. opened a German biobased packaging certification center following a USD 12 million capital outlay.

Global Regulatory Advisory Services For Packaging Market Report Scope

The study on the Regulatory Advisory Services for Packaging Market Report is Segmented by Service Type (Regulatory Monitoring and Intelligence, Compliance Documentation and Dossier Preparation, Testing and Certification Support, Training and Capacity-Building, and Digital Compliance Platforms), End-user Industry (Food and Beverage, Consumer Goods, Pharmaceuticals, Cosmetics and Personal Care, E-commerce and Retail, and Other End-user Industries), Material (Plastics, Paper and Paperboard, Metal, Glass, and Biobased/Compostables), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

The market comprises consulting firms and compliance specialists that offer services to ensure packaging products meet legal requirements for safety, labeling, and traceability across various global jurisdictions. This covers advisory services that help packaging companies comply with international and regional regulations, such as those from the FDA (United States), EFSA (Europe), and APAC-specific standards. It includes audits, documentation, and certification support for packaging materials and processes.

| Regulatory Monitoring and Intelligence |

| Compliance Documentation and Dossier Preparation |

| Testing and Certification Support |

| Training and Capacity-Building |

| Digital Compliance Platforms |

| Food and Beverage |

| Consumer Goods |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| E-commerce and Retail |

| Other End-user Industries |

| Plastics |

| Paper and Paperboard |

| Metal |

| Glass |

| Biobased / Compostables |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Regulatory Monitoring and Intelligence | ||

| Compliance Documentation and Dossier Preparation | |||

| Testing and Certification Support | |||

| Training and Capacity-Building | |||

| Digital Compliance Platforms | |||

| By End-user Industry | Food and Beverage | ||

| Consumer Goods | |||

| Pharmaceuticals | |||

| Cosmetics and Personal Care | |||

| E-commerce and Retail | |||

| Other End-user Industries | |||

| By Material | Plastics | ||

| Paper and Paperboard | |||

| Metal | |||

| Glass | |||

| Biobased / Compostables | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the PPWR/EPR/FDA/FCM regulatory advisory services market by 2031?

The market is expected to reach USD 1.43 billion by 2031, growing at a 9.03% CAGR.

Which region will grow fastest through 2031?

Asia-Pacific is forecast to expand at an 11.58% CAGR, fueled by new EPR schemes in Japan, South Korea, and India.

Which service type is expanding most quickly?

Digital compliance platforms are set to grow at a 10.61% CAGR as SMEs adopt AI-powered monitoring tools.

Why are biobased materials driving advisory demand?

Biobased formats face inconsistent biodegradability standards and complex safety dossiers, creating an 11.12% CAGR growth niche for specialist consultants.

How fragmented is the competitive landscape?

No firm controls more than 8% of revenue; the top five hold roughly 40%, yielding a market concentration score of 4.

Page last updated on: