Packaging LCA And Eco-Design Advisory Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.15 Billion |

| Market Size (2030) | USD 1.76 Billion |

| Growth Rate (2025 - 2030) | 8.97% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Packaging LCA And Eco-Design Advisory Services Market Analysis by Mordor Intelligence

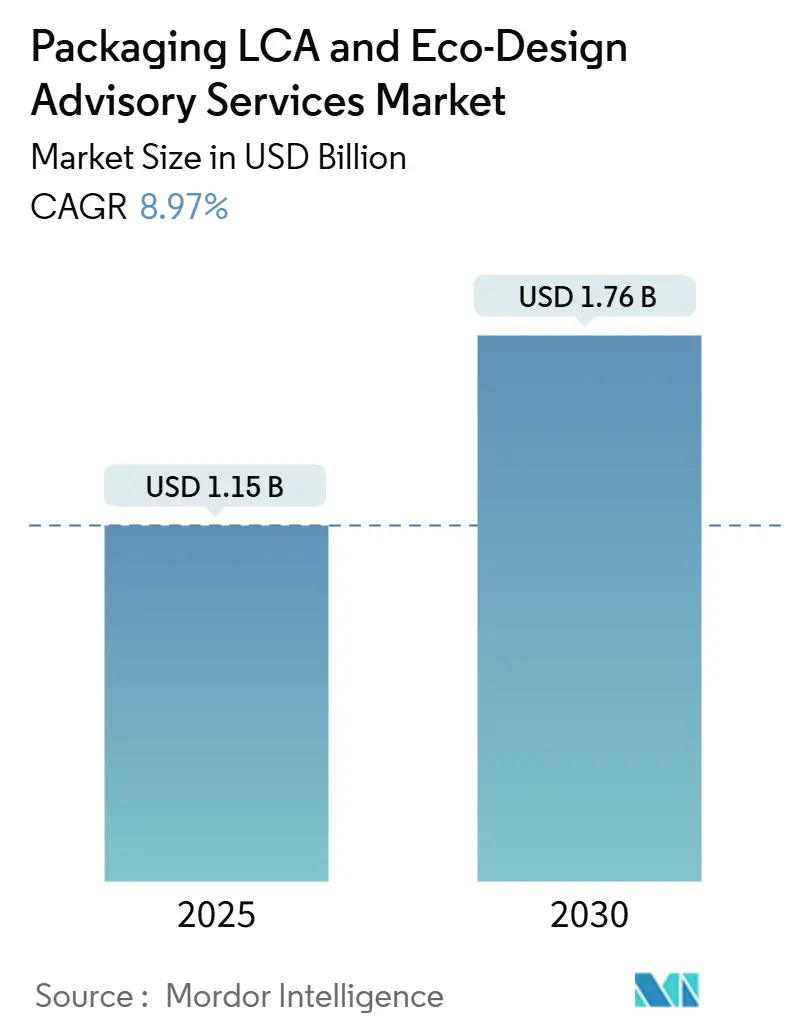

The Packaging LCA and Eco-Design Advisory Services market size reached USD 1.15 billion in 2025 and is projected to advance at an 8.97% CAGR, increasing the value to USD 1.76 billion by 2030. Rising Extended Producer Responsibility rules, corporate net-zero roadmaps, and real-time cloud assessment tools converge to push life-cycle metrics into day-to-day packaging decisions. Consulting demand intensifies as multinational brands harmonize global specifications with local plastic taxes, while AI-enabled scenario engines shorten assessment cycles from months to days. Europe remains the compliance epicenter, yet Asia-Pacific accelerates on the back of stringent single-use bans and multinational procurement shifts. Competitive intensity remains moderate, with software-first specialists gaining market share by embedding APIs within product design suites and converting one-off studies into subscription services.

Key Report Takeaways

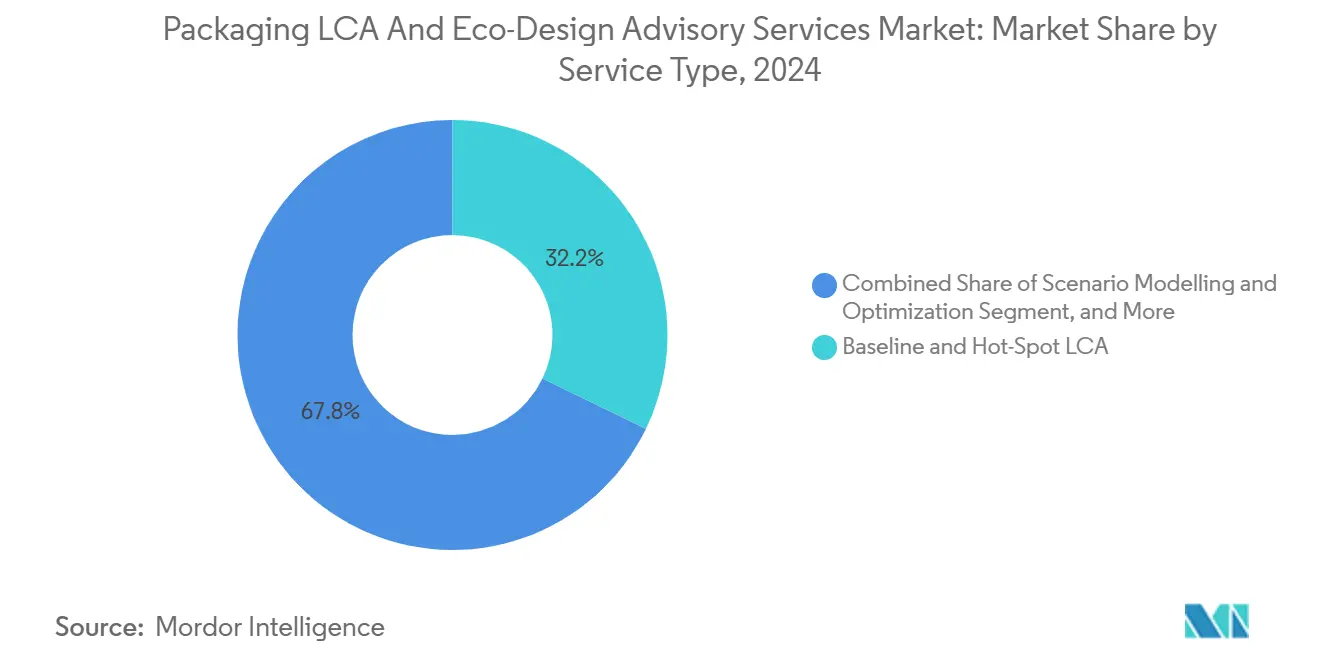

- By service type, Baseline and Hot-Spot LCA captured 32.18% of the Packaging LCA and Eco-Design Advisory Services Market share in 2024.

- By material type, Packaging LCA and Eco-Design Advisory Services Market size for compostable materials is projected to grow at a 10.68% CAGR between 2025–2030.

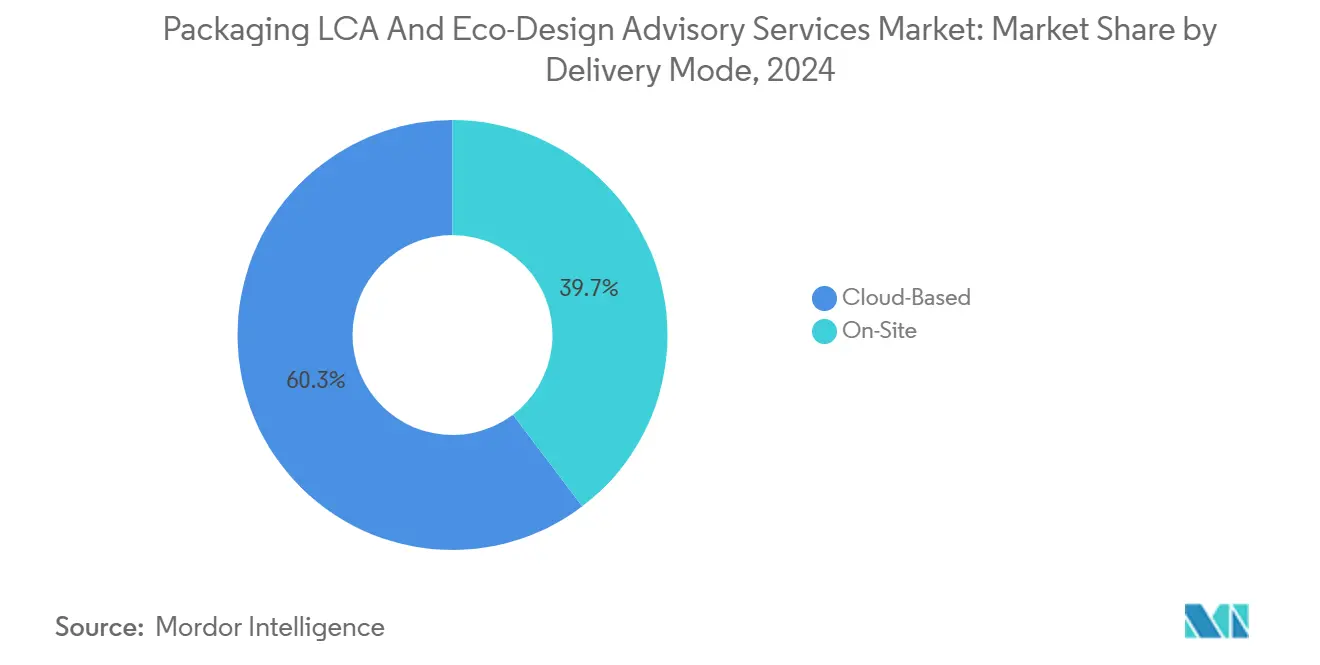

- By delivery mode, cloud platforms captured 60.32% of the Packaging LCA and Eco-Design Advisory Services Market share in 2024.

- By end-user, Packaging LCA and Eco-Design Advisory Services Market size for e-commerce and retail is projected to grow at 11.09% CAGR between 2025–2030.

- By geography, Europe captured 34.62% of the Packaging LCA and Eco-Design Advisory Services Market share in 2024.

Global Packaging LCA And Eco-Design Advisory Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing EPR and Plastics Taxes | +2.1% | Europe and North America, expanding to the Asia-Pacific | Medium term (2-4 years) |

| Corporate Net-Zero Pledges | +1.8% | Global, strongest at multinational headquarters | Short term (≤2 years) |

| Digitization of LCA Data Flows | +1.4% | Global, early adoption in tech-forward regions | Long term (≥4 years) |

| Retailers’ Private-Label Eco-Score Rollouts | +1.2% | Europe and North America, and selective Asia-Pacific markets | Medium term (2-4 years) |

| Material Circularity KPIs Embedded in Investor ESG Ratings | +0.9% | Global, emphasis on public company domiciles | Medium term (2-4 years) |

| Brand-Owner Race For "Recyclable-By-Design" Patents | +0.7% | Global, concentrated in innovation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing EPR and Plastics Taxes

Extended Producer Responsibility laws shift end-of-life costs from municipalities to brand owners, making eco-design a financial lever. France now mandates recyclability scores, Germany requires granular material disclosure, and the Netherlands applies a EUR 0.80-per-kilogram plastics levy. Advisory firms secure steady revenue as brands seek ongoing monitoring, scenario modelling, and design tweaks to stay within fee thresholds and avoid escalating penalties.

Corporate Net-Zero Pledges

Science-based targets compel manufacturers to account for packaging emissions inside corporate carbon budgets. Unilever earmarked EUR 1 billion (USD 1.13 billion) for packaging projects, and Nestlé allocated CHF 2 billion (USD 2.15 billion) toward circular materials.[1]Unilever, “Annual Report and Accounts 2024,” unilever.com As climate disclosure rules from the United States Securities and Exchange Commission and the European Union broaden, brands demand auditable LCA data that withstands investor scrutiny.

Digitization of LCA Data Flows

Cloud platforms replace static spreadsheets with live databases that feed design software through APIs. Sphera Solutions logged 40% year-over-year growth in integrations during 2024, slashing average study times by 60% and driving recurring subscription uptake. Continuous monitoring transforms the service model from project-based billing to enterprise licenses, appealing to procurement and R&D teams under time pressure.

Retailers’ Private-Label Eco-Score Rollouts

Large retailers publicize environmental ratings across thousands of stock-keeping units, forcing suppliers to validate superior scores or risk relegation to the shelf. Carrefour expanded its eco-score to 15,000 items, while Walmart embeds packaging metrics in Project Gigaton supplier dashboards. Manufacturers respond with comparative LCAs and rapid-cycle optimizations that align with retailer benchmarks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Qualified LCA Professionals | -1.3% | Global, acute in emerging markets | Short term (≤2 years) |

| Fragmented Regional Ecolabel Standards | -0.8% | Global, complexity varies by region | Medium term (2-4 years) |

| High Cost of Primary Data Collection for SMEs | -0.6% | Global, disproportionate impact on developing markets | Medium term (2-4 years) |

| IP Concerns Over Disclosing Full Packaging Formulations | -0.4% | Global, concentrated in competitive sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing EPR and Plastics Taxes

Extended Producer Responsibility laws shift end-of-life costs from municipalities to brand owners, making eco-design a financial lever. France now mandates recyclability scores, Germany requires granular material disclosure, and the Netherlands applies a EUR 0.80-per-kilogram plastics levy. Advisory firms secure steady revenue as brands seek ongoing monitoring, scenario modelling, and design tweaks to stay within fee thresholds and avoid escalating penalties.

Corporate Net-Zero Pledges

Science-based targets compel manufacturers to account for packaging emissions inside corporate carbon budgets. Unilever earmarked EUR 1 billion (USD 1.13 billion) for packaging projects, and Nestlé allocated CHF 2 billion (USD 2.15 billion) toward circular materials. As climate disclosure rules from the United States Securities and Exchange Commission and the European Union broaden, brands demand auditable LCA data that withstands investor scrutiny.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Scenario Modelling Shapes Strategic Decisions

Baseline and Hot-Spot assessments represented 32.18% of 2024 revenues, underscoring the continuing need for footprint baselines across vast packaging portfolios. Through 2030, Scenario Modelling and Optimisation will outpace all other offerings at a 10.96% CAGR as procurement and innovation teams weigh carbon, cost, and circularity trade-offs in parallel. The Packaging LCA and Eco-Design Advisory Services market size associated with Scenario Modelling is projected to reach USD 0.54 billion by 2030. Brands adopt iterative workshops where LCA experts, designers, and logistics planners model shifts from virgin plastic to fiber, or from air to sea freight, within hours instead of weeks.

Eco-Design Strategy Consulting gains traction because clients want holistic recommendations rather than isolated footprint tables. Software Implementation and Training services grow steadily as firms build in-house capability to execute routine studies, while Compliance and Reporting become commoditized once templates stabilize. Competitive differentiation, therefore, centers on agile scenario engines that can ingest multi-variable inputs and deliver clear cost-impact curves without manual recalculation.

By Material Type: Compostables Accelerate Amid Plastic Scrutiny

Plastics held 42.25% of the 2024 analysis spend, reflecting both volume dominance and regulatory scrutiny. Yet, compostable materials exhibit the sharpest rise, with a 10.68% CAGR, moving from a niche to a mainstream market as governments incentivize organic waste collection and ban certain fossil-based resins. The Packaging LCA and Eco-Design Advisory Services market share linked to plastics will gradually decline as taxation and design constraints prompt brands to shift toward paper, pulp, and bio-based polymers.

Paper and paperboard maintain solid demand owing to the recyclability infrastructure, whereas glass studies focus on lightweighting to offset transport emissions. Emerging bio-polymer blends create data-scarcity headaches, driving demand for custom primary data collection to confirm degradation rates and microplastic profiles. Advisory providers that expand proprietary databases or partner with academic labs secure a competitive advantage by shortening their data collection cycles.

By Delivery Mode: Cloud Platforms Enable Always-On Footprinting

Cloud delivery accounted for 60.32% of 2024 billings and is forecast to climb at a 10.84% CAGR. Packaging engineers now click a plug-in inside computer-aided design tools and receive live impact readouts, bringing life-cycle accounting into sprint-based product development. The Packaging LCA and Eco-Design Advisory Services market size for cloud-based offerings is projected to surpass USD 1 billion by 2030.

Continuous monitoring shifts revenue models toward annual licenses, with tiered access based on user volume and data-refresh frequency. On-site consulting still appeals for confidential formulations and heavily regulated sectors such as pharmaceuticals, where data never exists in secure networks. Hybrid setups emerge, allowing sensitive inputs to reside locally while reference databases update through encrypted channels.

By End-user Industry: E-Commerce Spurs Innovative Solutions

Food and beverage clients generated 37.71% of 2024 spend, driven by strict single-use rules and consumer pressure on grocery packaging. E-commerce and retail are expected to post the highest 11.09% CAGR as the sector navigates the cushion-versus-carbon dilemma for shipped parcels. Beauty brands continue to invest in refillable and lightweight formats to appease activist scrutiny, whereas household chemical makers focus on concentrated formulas that reduce bottle sizes.

Pharmaceutical companies commission complex trade-off studies that balance sterility, child-resistance, and recyclability, often requiring assessments of blended primary and secondary packaging. Consultants who can simulate drop-test performance alongside footprint metrics gain an edge, particularly in omnichannel supply chains.

Geography Analysis

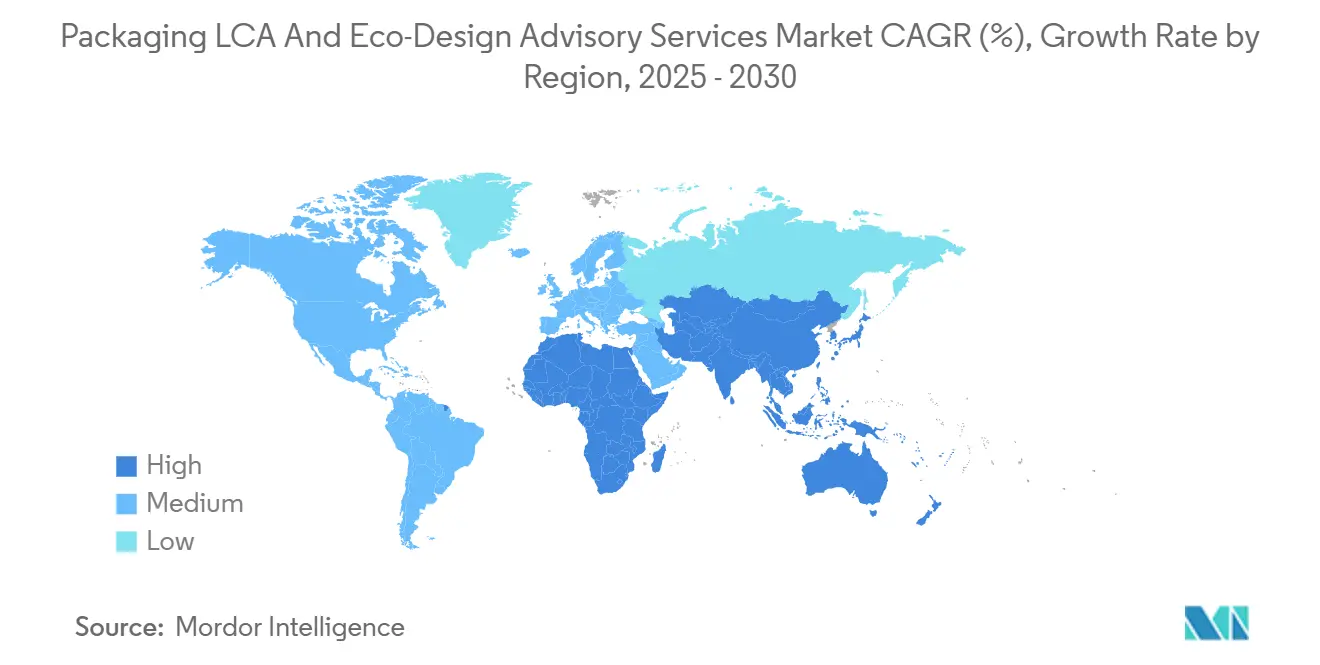

Europe retained 34.62% revenue share in 2024 on the back of the European Union Packaging and Packaging Waste Regulation, France’s AGEC law, and German VerpackG reporting. The region’s uniform adoption of ISO-aligned methods cements a high baseline for consultancy rigor. English, Dutch, and German professional hubs supply robust talent pools that feed cross-border projects. Brands operating across 27 member states prefer single-provider frameworks that streamline documentation against harmonized standards.

The Asia-Pacific region is the growth engine, with an 11.34% CAGR projected through 2030. China’s ban on foreign waste imports, Japan’s Plastic Resource Circulation Act, and India’s Extended Producer Responsibility rules fuel advisory uptake. Local governments are increasingly enforcing modulated fees tied to recyclability scores, forcing exporters to adjust their packaging formats to accommodate domestic recycling infrastructure. Manufacturing density in coastal China, Vietnam, and Thailand positions the region as a hotspot for supply-chain-integrated LCA engagements, including inbound raw-material impacts and outbound logistics optimization.[2]World Bank, “Plastic Waste Management in Asia,” worldbank.org

North America posts steady expansion as California SB 54, New York packaging EPR legislation, and Canadian federal plastic bans tighten reporting obligations. Clients value scenario models that weigh multilayer mono-material pouches against recyclable rigid formats under differing state mandates. Federal climate-disclosure requirements further embed LCA in Securities and Exchange Commission filings, raising the bar for audit-ready methodologies. Latin America and the Middle East and Africa remain nascent but fast-growing; multinationals often lead voluntary projects there to de-risk future regulations and secure first-mover reputational benefits.

Competitive Landscape

The marketplace remains moderately fragmented, with the top five players accounting for roughly 25% of combined revenue. Global management consultancies leverage existing C-suite ties to cross-sell packaging services; however, specialized software vendors such as Sphera Solutions and PRé Sustainability capture market share through their technological depth. Boutique advisories compete on sector focus, for instance, pharmaceutical or luxury goods packaging. Patent filings for automated impact calculators indicate an escalating trend in tech investment, with Ecochain Technologies alone filing 12 software patents in 2024.[3]United States Patent and Trademark Office, “Patent Application Database Search,” uspto.gov

Testing laboratories integrate LCA modules to deliver one-stop validation, while certification bodies offer digital passports that bundle traceability with impact scores. Market entrants from the enterprise software sector are seeking to commoditize footprint calculations, which threatens traditional billable-hour models. Mergers and acquisitions focus on unifying databases, regional presence, and subject-matter expertise, as evidenced by Sphera’s 2025 acquisition of SimaPro and Intertek’s acquisition of a laboratory, which links physical and environmental testing.

Pricing models evolve toward subscription plus value-added analytics, rather than per-study fees. The shift benefits clients with high SKU volumes, notably fast-moving consumer goods and e-commerce retailers. Providers differentiate via sector-specific datasets, AI-driven hotspot detection, and the ability to meet third-party assurance standards under ISO 14044. Given the fragmented share distribution, the sector scores 6 on the 10-point concentration scale.

Packaging LCA And Eco-Design Advisory Services Industry Leaders

Boston Consulting Group

Sphera Solutions, Inc.

Anthesis Group

PRé Sustainability B.V.

Ramboll Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Boston Consulting Group opened a Global Packaging Sustainability Center in Singapore with a USD 25 million commitment.

- September 2025: Carbon Trust Advisory partnered with Walmart’s Project Gigaton to deliver standardized LCAs for 5,000 suppliers.

- August 2025: Intertek Group acquired Kiwa for EUR 180 million (USD 203 million) to combine its test labs with eco-design audits.

- July 2025: WSP Global established a 150-strong Circular Economy Practice, focusing on packaging optimization.

Global Packaging LCA And Eco-Design Advisory Services Market Report Scope

| Baseline and Hot-Spot LCA |

| Scenario Modelling and Optimisation |

| Eco-Design Strategy Consulting |

| Software Tool Implementation and Training |

| Packaging Compliance and Reporting |

| Plastic |

| Paper and Paperboard |

| Metal |

| Compostable |

| Glass |

| Other Material Type |

| On-Site |

| Cloud-Based |

| Food and Beverage |

| Personal Care and Cosmetics |

| Household Chemicals |

| E-commerce and Retail |

| Pharmaceuticals |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Baseline and Hot-Spot LCA | ||

| Scenario Modelling and Optimisation | |||

| Eco-Design Strategy Consulting | |||

| Software Tool Implementation and Training | |||

| Packaging Compliance and Reporting | |||

| By Material Type | Plastic | ||

| Paper and Paperboard | |||

| Metal | |||

| Compostable | |||

| Glass | |||

| Other Material Type | |||

| By Delivery Mode | On-Site | ||

| Cloud-Based | |||

| By End-user Industry | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| Household Chemicals | |||

| E-commerce and Retail | |||

| Pharmaceuticals | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Packaging LCA and Eco-Design Advisory Services market?

The market reached USD 1.15 billion in 2025 and is forecast to hit USD 1.76 billion by 2030.

Which region is expanding the fastest?

Asia-Pacific shows the highest growth, rising at an 11.34% CAGR due to tightening local regulations and multinational procurement shifts.

Which service category is growing quickest?

Scenario Modelling and Optimisation leads with a projected 10.96% CAGR through 2030, reflecting demand for strategic trade-off analysis.

Why are cloud platforms gaining share?

Cloud APIs embed real-time life-cycle metrics within design systems, reducing study time by 60% and converting one-off projects into recurring subscriptions.

Which end-user sector drives the most spending?

Food and beverage accounts for 37.71% of 2024 revenues, pushed by strict single-use rules and consumer expectations.

What limits faster market growth?

A global shortage of certified LCA professionals and fragmented ecolabel standards adds cost and complexity, dampening near-term expansion.

Page last updated on: