Consumer Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

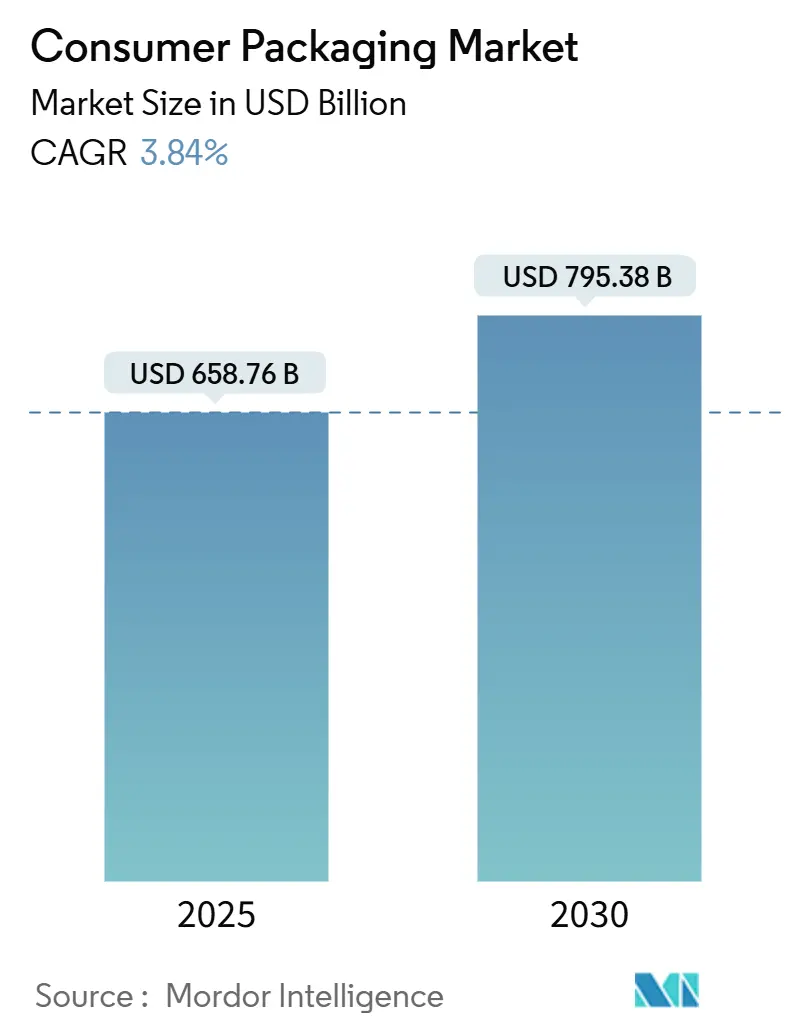

| Market Size (2025) | USD 658.76 Billion |

| Market Size (2030) | USD 795.38 Billion |

| Growth Rate (2025 - 2030) | 3.84% CAGR |

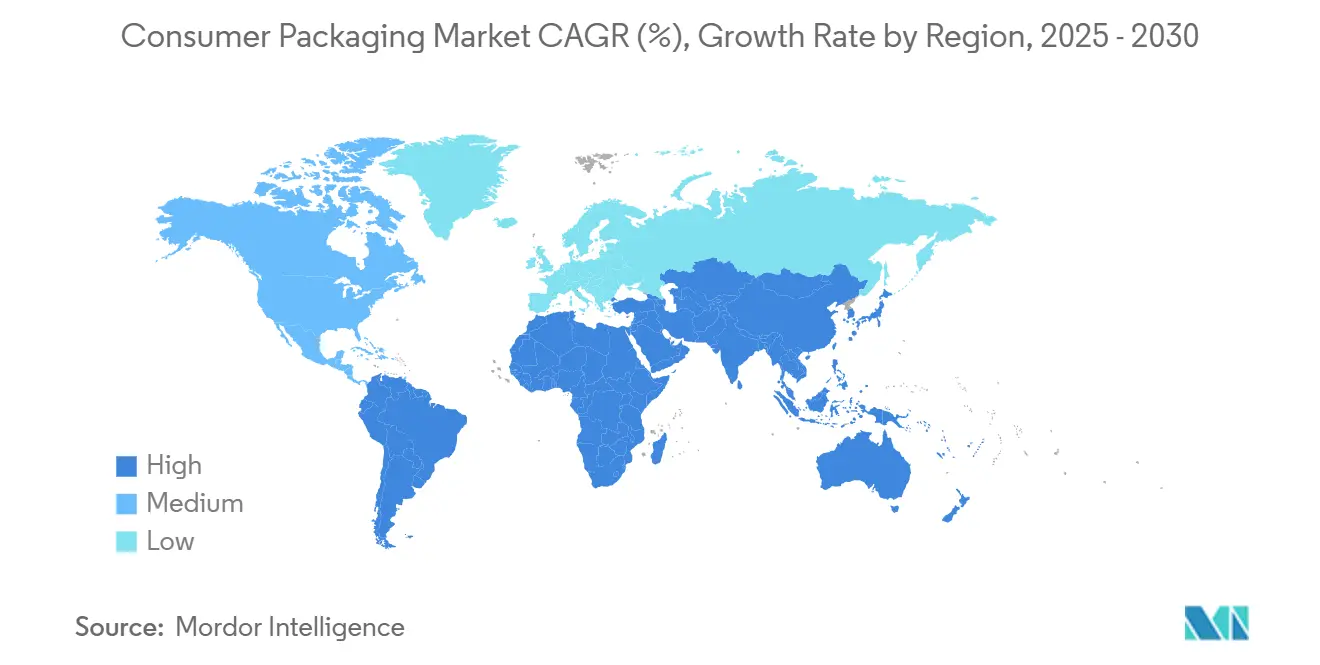

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Consumer Packaging Market Analysis by Mordor Intelligence

The consumer packaging market size reached USD 658.76 billion in 2025 and is projected to reach USD 795.38 billion by 2030, growing at a 3.84% CAGR. The modest growth rate signals a maturing arena in which sustainability mandates, e-commerce fulfillment demands, and regulatory scrutiny jointly reshape investments and operating models. Automated right-sizing tools deployed at large fulfillment centers are cutting corrugated and cushioning inputs by up to 15% without compromising protective performance. Fiber-based alternatives simultaneously gain ground as retailers seek packaging that aligns with recycling targets while maintaining shelf appeal. Raw-material volatility remains a near-term concern; however, manufacturers mitigate it by diversifying their supplier bases, incorporating price-escalation clauses, and accelerating lightweighting projects. Competitive intensity is steady rather than fierce because scale economies, long-term service contracts, and capital requirements maintain entry barriers at a moderate level.

Key Report Takeaways

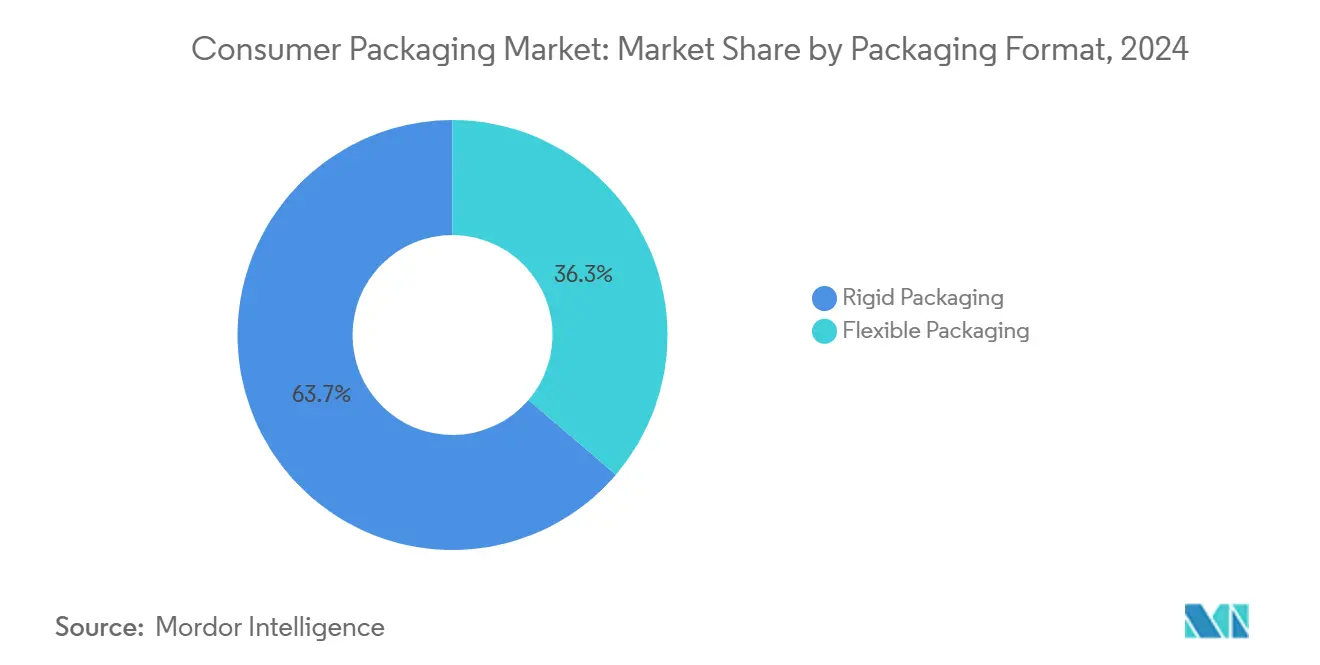

- By packaging format, the rigid packaging segment captured 63.74% of the Consumer Packaging Market share in 2024.

- By material type, the Consumer Packaging Market size for paper and paperboard is projected to grow at a 4.98% CAGR between 2025–2030.

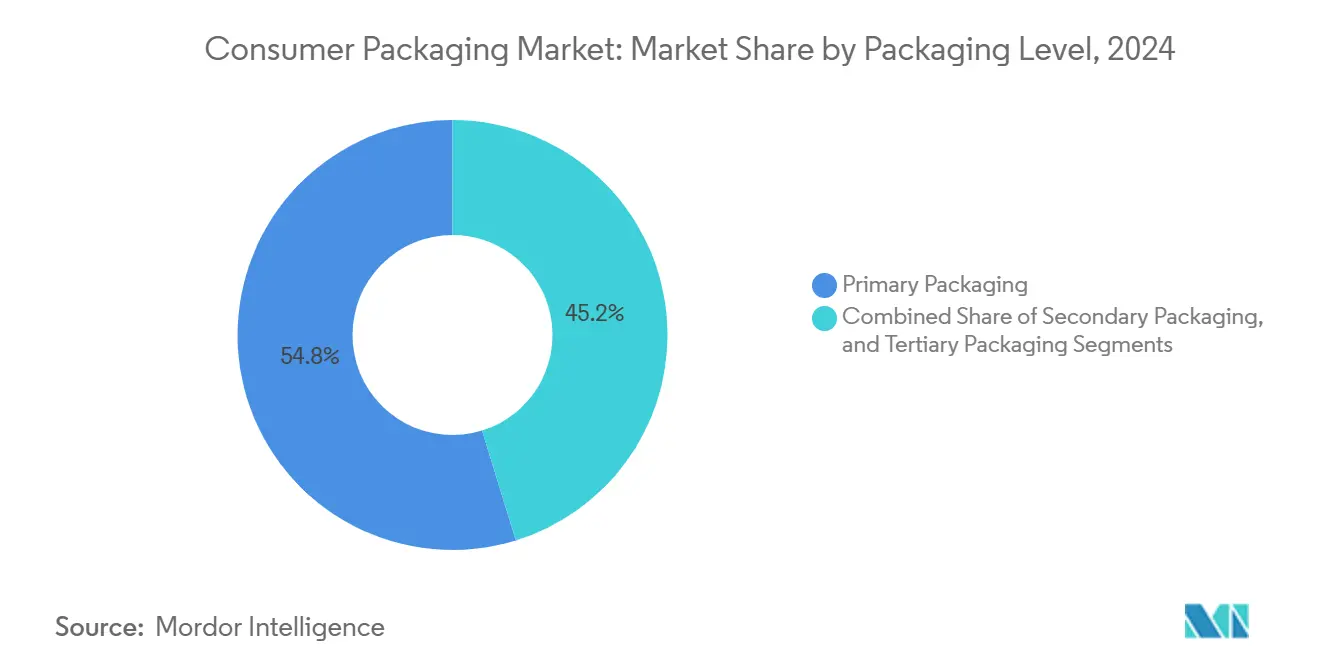

- By packaging level, the primary packaging segment captured 54.78% of the Consumer Packaging Market revenue share in 2024.

- By end-user industry, the Consumer Packaging Market size for pharmaceutical applications is projected to grow at a 4.63% CAGR between 2025–2030.

- By geography, the North America segment captured 41.69% of the Consumer Packaging Market share in 2024.

Global Consumer Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing e-commerce shipment volumes | +1.2% | Global, with a concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Premiumization in food and beverage packaging | +0.8% | North America and Europe, expanding to the Asia-Pacific | Long term (≥ 4 years) |

| Lightweighting and material-cost optimization | +0.6% | Global | Short term (≤ 2 years) |

| AI-driven "right-sizing" automation | +0.4% | North America and Europe, early adoption in the Asia-Pacific | Medium term (2-4 years) |

| National recycled-content quotas for FMCG brands | +0.7% | Europe and North America, emerging in the Asia-Pacific | Long term (≥ 4 years) |

| Returnable packaging subscription platforms | +0.3% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing e-commerce shipment volumes

Direct-to-consumer fulfillment requires packaging that is resilient enough to endure automated sortation, long-haul transportation, and porch drop-off, all while minimizing dimensional-weight charges that impact logistics budgets. Amazon’s machine-learning Package Decision Engine reduced overall packaging materials by 11% in 2024 while keeping damage rates below 0.5%.[1]Amazon, “2024 Sustainability Report,” sustainability.aboutamazon.com The success of large marketplaces prompts mid-tier retailers to adopt similar data-driven solutions, spurring a network effect that accelerates supplier innovation. Corrugated converters now offer modular inserts tailored to order profiles rather than static stock-keeping units. High-value electronics brands are increasingly trialing reusable shippers that integrate RFID tags, appealing to sustainability-minded consumers and reducing damage from reverse logistics. Cross-border e-commerce, projected to account for over 30% of global online sales by 2027, further amplifies demand for tamper-evident and multilingual labeling.

Premiumisation in food and beverage packaging

Shoppers associate specialized closures, tactile varnishes, and smart freshness indicators with higher product quality, enabling brand owners to command price premiums of 15-25%. Active labels that change color when the cold chain is breached gained traction among dairy and craft beer producers in 2024. Luxury confectionery houses turned to micro-flute corrugated sleeves enhanced with foil stamping to replace rigid tins, trimming weight by 22% while retaining giftability. Barrier-coated papers now rival multi-layer PET films in terms of oxygen and moisture resistance, allowing artisanal snack brands to market a “plastic-free” message without shelf-life penalties. Contract packers, responding to premiumization, have upgraded printing lines to 7-color capabilities, shrinking run sizes and enabling seasonally themed launches that boost velocity per stock-keeping unit.

AI-driven right-sizing automation

Robotic erect-fill-seal cells, connected to predictive algorithms, evaluate product geometry, shipping lane, and carrier-specific surcharges in real-time, selecting the smallest viable carton from an on-site blank library. FedEx reported that such right-sizing initiatives reduced packaging waste by 18% in 2024 and lowered the average shipping costs for merchants by 12%. Machine learning continuously refines dimension tables based on drop-test data and claims feedback, incrementally reducing void-fill requirements. Early adopters benefit from reduced freight emissions, an increasingly scrutinized CSR metric. Vendors are integrating computer vision into pick-and-place stations, enabling the same-line processing of irregular items, ranging from sporting goods to cosmetic kits. As capital costs fall, medium-volume facilities gain access to the technology, broadening the installed base and driving further algorithmic improvements.

National recycled-content quotas for FMCG brands

The European Union’s 2024 amendments mandate recycled content thresholds rising to 65% for paper-based formats and 25% for PET bottles by 2030. Parallel legislation has surfaced in three Canadian provinces and five U.S. states, widening the compliance footprint. Forward-looking converters secure long-term offtake agreements with material recovery facilities to lock in feedstock volumes, often at price premiums. To ensure traceability, blockchain pilots now document the origins of baled inputs, creating digital audits that satisfy retailer scorecards and mitigate the risk of greenwashing. Equipment suppliers are retrofitting extruders with advanced filtration systems to handle higher loads of recycled materials without gel defects. Brands that exceed minimum quotas feature on-pack logos that resonate with eco-conscious consumers, translating regulatory compliance into marketing advantage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile polymer and paper pulp prices | -0.9% | Global | Short term (≤ 2 years) |

| Tightening single-use plastic regulations | -0.6% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Additive disclosure rules hampering multilayer recycling | -0.4% | Europe and North America | Long term (≥ 4 years) |

| Cross-border e-commerce tariff shocks on packaging inputs | -0.5% | Global, concentrated in trade-dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile polymer and paper pulp prices

Polymer resin prices fluctuated by 23% in 2024 as unplanned cracker outages and energy price spikes disrupted supply chains. Hardwood pulp traded between USD 580 and USD 750 per metric ton during the same window, a variation that strained annual budgeting for medium-sized converters. To buffer risk, larger players adopted commodity hedging and dual-sourcing across continents, but smaller firms lacked the scale to secure favorable terms. Film extruders accelerated trials with calcium-carbonate masterbatches that reduce virgin-resin content by up to 12% without sacrificing tensile strength. Sheet-fed litho operations staggered order patterns to balance inventory carrying costs against potential spot-price escalations. Nonetheless, customer pushback on surcharges has intensified, highlighting the delicate balance between cost recovery and maintaining market share.

Tightening single-use plastic regulations

Europe’s Single-Use Plastics Directive transitioned from a framework to national enforcement in 2024, resulting in bans on certain polystyrene clamshells and the introduction of mandatory producer fees on other disposable items. Similar statutes emerged in California and New York, creating a patchwork that complicates multinational rollouts. Material substitutions often lift unit costs by 20-40% and necessitate capital spending on new forming machinery. Molded fiber trays, for instance, require pressing lines with higher tonnage and extended drying stages compared with thermoformed PET. Brand owners, therefore, face a trade-off between environmental commitments and price positioning. Enforcement agencies have begun auditing environmental claims, exposing firms to reputational risk if compostability or recyclability statements lack substantiation, further dampening near-term innovation speed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Format: Flexibles Outpace Legacy Rigid Offerings

Rigid containers held a 63.74% consumer packaging market share in 2024, driven by the dominance of metal cans, PET bottles, and glass jars in the market for carbonated beverages, sauces, and medical vials. Steady supermarket rotation and established filling lines anchor demand; yet, growth prospects are muted because lightweight substitutes are capturing incremental volume. Flexible alternatives, such as stand-up pouches and retort sachets, reached double-digit penetration in shelf-stable soups and single-serve pet food, a shift catalyzed by 30% logistics cost savings and increased brand billboard space. Converters ramped up high-barrier metalized films that withstand 135 °C retort sterilization and still maintain puncture resistance, unlocking categories once deemed exclusive to cans. E-commerce influences format choice by favoring flexible sachets that sag rather than shatter, lowering return rates for cosmetics and nutraceutical sachets.

Remarketing initiatives amplify the advantages of flexibles by touting reduced greenhouse-gas footprints compared with rigid benchmarks. Lifecycle assessments commissioned by brand owners reveal carbon reductions of up to 55% when switching from glass to pouch for cooking sauces, subject to regional electricity mixes. Co-packers now integrate digital printing for short-run lot codes and limited-edition graphics, enabling SKU proliferation without inventory blowouts. Heat-seal strength, formerly a weak point, has improved through laser-scored tear wings that deliver predictable opening force. Combined, these improvements sustain the 5.43% CAGR expected for flexibles and support premium pricing tiers that accentuate convenience and sustainability narratives across the consumer packaging market.

By Material Type: Paper and Paperboard Capture Sustainability Momentum

Plastic’s 44.68% share of the consumer packaging market size rests on its versatility, clarity, and cost efficiency, yet public sentiment and regulation steadily chip away at its unquestioned dominance. Paper and paperboard, projected to grow at a 4.98% CAGR, ride a perception wave that equates fiber with circularity. The transition accelerated after major quick-service restaurant chains switched from plastic clamshells to barrier-coated folding cartons that resist grease for four hours, which is sufficient for delivery windows. Technology advances, such as water-based dispersion coatings, confer moisture resistance without hindering repulpability, allowing mills to reclaim fiber through standard hydrapulpers.[2]TAPPI, “Barrier Coating Technology Advances,” tappi.org The consumer packaging industry is witnessing a growing demand for micro-fibrillated cellulose, which reinforces cup stock and reduces basis weight by 10-15%, while meeting strength specifications.

Plastic remains indispensable for high-clarity or high-barrier applications, such as vacuum-packed meats and carbonated soft drinks. Still, converters broaden their resin portfolios to include chemically recycled PET, granting them access to premium-priced contracts under recycled-content mandates. Glass and metal retain niche roles linked to product premiumization; craft distillers prefer glass flasks that accentuate brand heritage, whereas aluminum bottles gain market share in ready-to-drink cocktails due to their chill-speed advantages. Emerging biopolymers such as polylactic acid enter high-margin segments like single-serve coffee pods, but volume remains limited because processing windows differ from conventional equipment. Material diversification underpins resilience as brand owners pursue multi-path approaches to reduced environmental impact, reinforcing paper’s ascendance while plastic adapts to higher recycled loads within the consumer packaging market.

By Packaging Level: Secondary Solutions Gain E-commerce Traction

Primary packaging accounted for 54.78% of 2024 revenue and remains the face consumers see on shelves; yet, growth is pivoting to secondary formats that bridge the factory and doorstep. A surge in parcel shipments puts corrugated mailers, padded paper envelopes, and subscription boxes into the spotlight. Secondary solutions benefit from omnichannel strategies because retail display requirements now align with shipping durability tests, driving the development of multi-function designs, such as tear-strip displays that convert into shelf-ready trays. Automated case-packing lines integrate artificial intelligence to orient oddly shaped primary packs for optimal cube utilization, reflecting the 5.62% CAGR forecast for secondary layers of the consumer packaging market.

Cost pressures drive the development of nested designs that serve as both transit protection and countertop merchandising, resulting in an average 12% reduction in material inputs. Secondary suppliers partner with primary pack converters to pre-qualify sets for ISTA 6-Amazon tests, thereby shortening lead times for e-commerce rollouts. Universal recycling symbols printed on both layers align with municipal collection streams, easing consumer confusion and satisfying retailer scorecards that increasingly weigh recyclability metrics in listing decisions. The trend fortifies the notion that packaging levels are no longer siloed; instead, they form an integrated system tuned to cross-channel fulfillment realities.

By End-use Industry: Pharmaceuticals Accelerate Beyond the Base

Food and beverage continued to account for 46.67% of 2024 revenue through non-stop household replenishment and a fast-moving innovation pipeline. Yet, the pharmaceutical sector is poised to outpace all its peers at a 4.63% CAGR, driven by aging populations, biologic therapies, and home-based care. Vial trays capable of maintaining temperatures between 2-8 °C for up to 96 hours underpin the boom in temperature-sensitive drugs, while child-resistant, senior-friendly closures enhance adherence to chronic medicines. Legislation mandating serialization of prescription products across more than 50 jurisdictions further spurs demand for tamper-evident labels and machine-vision inspection systems.

Nutraceutical and over-the-counter brands leverage pharmaceutical advancements by incorporating blister packs with push-through laminates that limit moisture ingress to below 5% for up to two years. Meanwhile, food manufacturers are piloting antimicrobial sachets embedded in high-moisture bread packaging, borrowing pharmaceutical active-packaging know-how to extend shelf life. Beauty and personal-care companies integrate airless pumps initially designed for topical drugs to protect sensitive vitamin C serums. This cross-pollination confirms that pharmaceutical innovation ripples across adjacent categories, raising performance expectations and lifting value density within the broader consumer packaging market.

Geography Analysis

North America’s consumer packaging market leadership is underpinned by its 41.69% share and a forecast CAGR of 3.2%. High credit-card penetration fuels online spending, which in turn boosts demand for corrugated cases, bubble mailers, and protective inserts. The United States accounts for roughly four-fifths of regional revenue, with Canada adding specialized fiber-based formats aimed at quick-service dining chains and Mexico supplying cost-efficient corrugated exports into the Midwest. Federal and state plastics legislation promotes mono-material design, propelling innovations in paper mailers that replace bubble-lined poly envelopes. Large brands adopt advanced analytics to align package dimensions with real-time carrier surcharge tables, reinforcing operational efficiency.

Asia-Pacific’s rising middle class continues to reshape volume and value expectations. Surging urban e-grocery platforms in China and India require leak-proof, tamper-evident pouches that withstand cold-chain abuse yet open easily in domestic kitchens.[3]Asian Development Bank, “Consumer Market Growth in Asia,” adb.org Japan’s premium confectionery houses cling to ornate, rigid boxes but incorporate recycled PET windows to satisfy environmental guidelines without losing gift appeal. Australia leverages its forestry assets to export kraft linerboard, feeding Southeast Asian corrugators that serve local electronics assemblers. Cross-border harmonization of recycling symbols remains limited, prompting global consumer goods companies to print multilingual disposal instructions on outer cartons to avoid misclassification fines.

Europe combines regulatory rigor with consumer activism, driving the shift to fiber and chemically recycled polymers. The region invests heavily in collection and sortation infrastructure to close material loops, a prerequisite for meeting the 65% recycled-content goal by 2030. Germany and France lead pilot programs for reusable take-away cup schemes that integrate RFID tracking to optimize reverse logistics. The United Kingdom’s Plastic Packaging Tax increased in April 2025, raising the levy for non-compliant packs and encouraging converters to use coextruded films containing certified recycled feedstock. Southern Europe focuses on lightweight glass for olive oil exports, providing differentiation while reducing freight emissions, whereas the Nordics pioneer biopolymer-coated board for frozen pizza sleeves.

Mordor Intelligence provides coverage of the consumer packaging market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The consumer packaging market exhibits a moderate concentration profile anchored by multinational incumbents that collectively control an estimated one-third of global capacity. Amcor, Mondi, and Sealed Air remain top-tier players, each operating diversified portfolios that span rigid containers, flexible packaging, and protective solutions. Their competitive edge stems from multi-continent converting footprints that shorten delivery lead times while satisfying global key-account programs. Sustainability leadership remains the primary battlefield. Amcor’s 2024 commitment to shift all mainstream stock-keeping units to recyclable or reusable formats by 2027 compelled peers to accelerate similar pledges. Mondi invests EUR 180 million (USD 195 million) in high-barrier paper to pre-empt future plastic bans, whereas Sealed Air refines its automated mailer line to bolster its e-commerce credentials.

Regional specialists carve defensible niches by mastering local regulatory idiosyncrasies and offering high-touch service models. Examples include cartonboard converters in Poland catering to short-lead promotional runs for European discounters, and corrugated producers in Vietnam that deliver custom branding for cross-border marketplace sellers. Technology disruptors enter the market via software, offering AI-driven sizing engines on a subscription basis and partnering with third-party logistics hubs to pilot algorithms without incurring extensive capital outlay. Material innovators focus on bio-based films derived from agricultural by-products, gaining attention from personal-care brands seeking a differentiated sustainability narrative. Despite a steady trickle of mergers, antitrust authorities keenly monitor regional market shares, preventing any single firm from eclipsing 25% globally and thus keeping the consumer packaging market dynamic but structurally balanced.

A second tier of integrated fiber players such as Smurfit WestRock and International Paper flex muscle in containerboard self-sufficiency, granting pricing resilience during pulp spikes. Contract packagers diversify into design services, bundling structural engineering with manufacturing to capture value earlier in the project lifecycle. Start-ups exploit licensing models to place proprietary compostable resin blends into established extrusion lines, accelerating market entry. The interplay between scale and specialization ensures that no competitive advantage remains permanent; instead, continuous investment in materials science, automation, and circular-economy compliance defines long-term viability within the consumer packaging market.

Consumer Packaging Industry Leaders

Amcor plc

Mondi plc

Sealed Air Corporation

Smurfit WestRock plc

International Paper Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Amcor completed its USD 2.3 billion acquisition of Berry Global’s rigid packaging business, expanding food and beverage capacity across North America.

- September 2024: Mondi earmarked EUR 180 million (USD 195 million) to enlarge European barrier-coated paper output focused on chilled-food applications.

- August 2024: Sealed Air debuted an automated platform that links AI-guided right-sizing software with recycled-content mailers for e-commerce clients.

- July 2024: International Paper forged a USD 150 million joint venture with a Chinese partner to build corrugated capacity tailored to Asia-Pacific online retail.

Global Consumer Packaging Market Report Scope

| Rigid Packaging |

| Flexible Packaging |

| Plastic |

| Paper and Paperboard |

| Glass |

| Metal |

| Other Material Types |

| Primary Packaging |

| Secondary Packaging |

| Tertiary Packaging |

| Food and Beverage |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| Homecare and Household |

| Other End-use Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Format | Rigid Packaging | ||

| Flexible Packaging | |||

| By Material Type | Plastic | ||

| Paper and Paperboard | |||

| Glass | |||

| Metal | |||

| Other Material Types | |||

| By Packaging Level | Primary Packaging | ||

| Secondary Packaging | |||

| Tertiary Packaging | |||

| By End-use Industry | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| Pharmaceuticals | |||

| Homecare and Household | |||

| Other End-use Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the consumer packaging market in 2025, and how fast is it growing?

The consumer packaging market size stood at USD 658.76 billion in 2025 and is projected to expand at a 3.84% CAGR through 2030.

Which packaging format is expected to show the strongest growth trajectory through 2030?

Flexible formats, including stand-up pouches and retort sachets, are set to register a 5.43% CAGR, outpacing rigid alternatives.

What region is expected to deliver the highest growth for consumer packaging suppliers?

The Asia-Pacific region is forecast to advance at a 5.71% CAGR, driven by rising middle-class incomes and the adoption of e-commerce, which in turn is expected to boost packaged-goods consumption.

How are national recycled-content quotas influencing material choices?

Recycled-content mandates are accelerating investment in chemically recycled PET and high-barrier paper, prompting converters to secure feedstock and retrofit equipment for increased use of post-consumer resin.

Which end-use segment will grow the fastest to 2030?

Pharmaceutical applications are projected to grow at a 4.63% CAGR, driven by the adoption of cold-chain biologics, the implementation of serialization rules, and the aging demographics.

What role does AI play in packaging cost reduction?

AI-driven right-sizing systems optimize carton dimensions per order, cutting material use by up to 18% and lowering shipping costs by double-digit percentages.

Page last updated on: