Tamper Evident Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

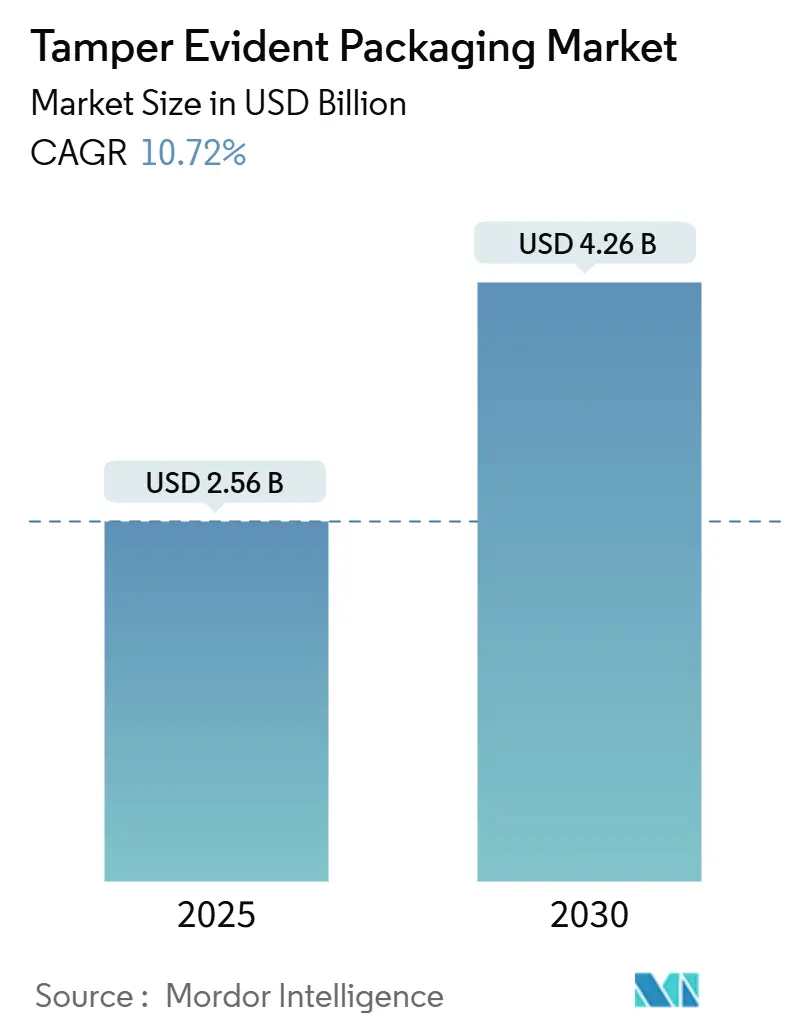

| Market Size (2025) | USD 2.56 Billion |

| Market Size (2030) | USD 4.26 Billion |

| Growth Rate (2025 - 2030) | 10.72% CAGR |

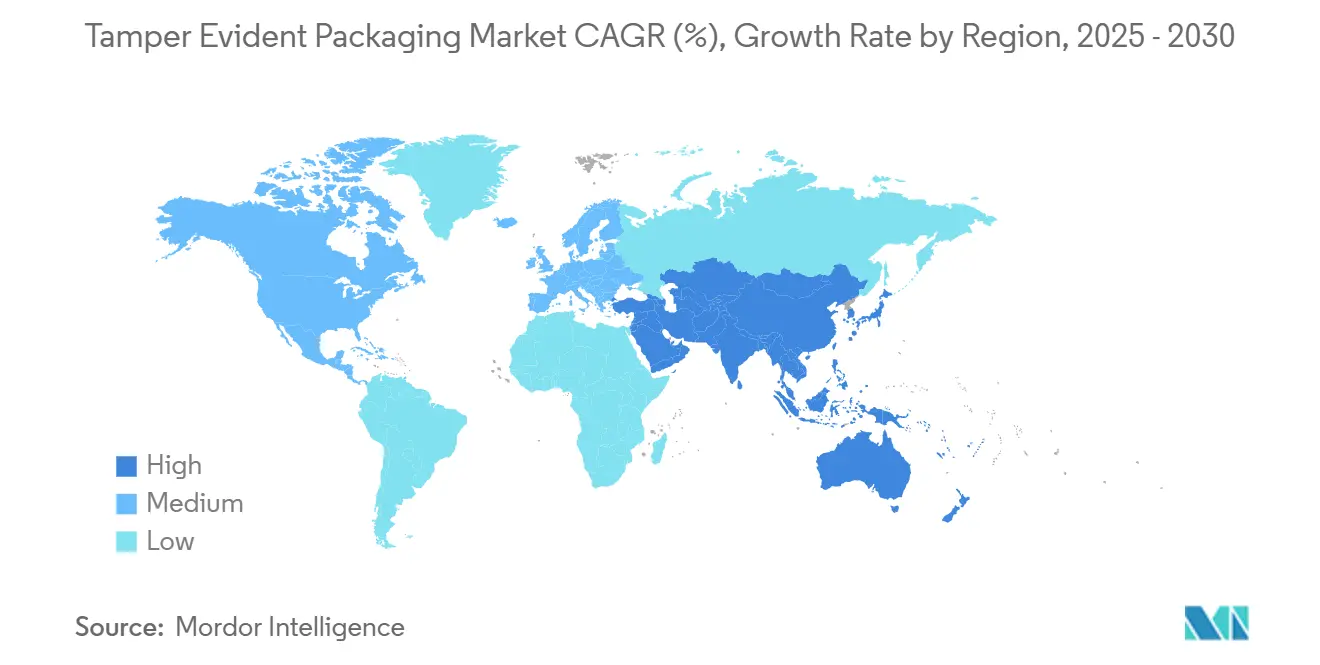

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tamper Evident Packaging Market Analysis by Mordor Intelligence

The tamper-evident packaging market size is USD 2.56 billion in 2025 and is projected to reach USD 4.26 billion by 2030, representing a 10.72% CAGR during the forecast period. Regulatory mandates have turned packaging integrity into a compliance prerequisite, moving procurement conversations away from cost and toward brand protection, data capture, and supply-chain transparency. Unit-level pharmaceutical serialization, rising e-commerce volumes, and highly publicized counterfeiting incidents are amplifying investment in visible and digital seals that reassure regulators and consumers alike. Brands are also pairing tamper evidence with sustainability storytelling, driving innovation in recyclable barrier coatings and mono-material structures. Competitive dynamics now hinge on who can integrate NFC, blockchain, and serialization into cost-effective formats at an industrial scale, particularly in the Asia-Pacific region, where OEM and private-label volumes create early-mover advantages.

Key Report Takeaways

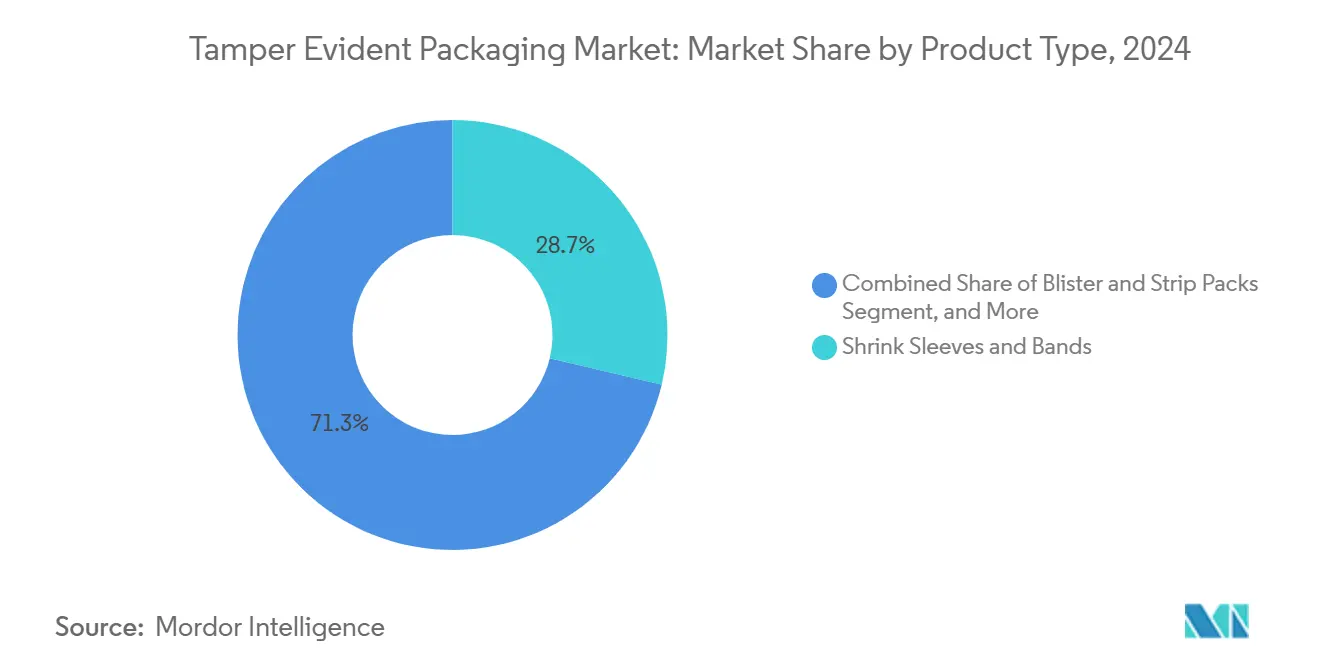

- By product type, shrink sleeves and bands captured 28.72% of the tamper-evident packaging market share in 2024.

- By material, the tamper-evident packaging market size for paper and paperboard is projected to grow at a 12.53% CAGR between 2025–2030.

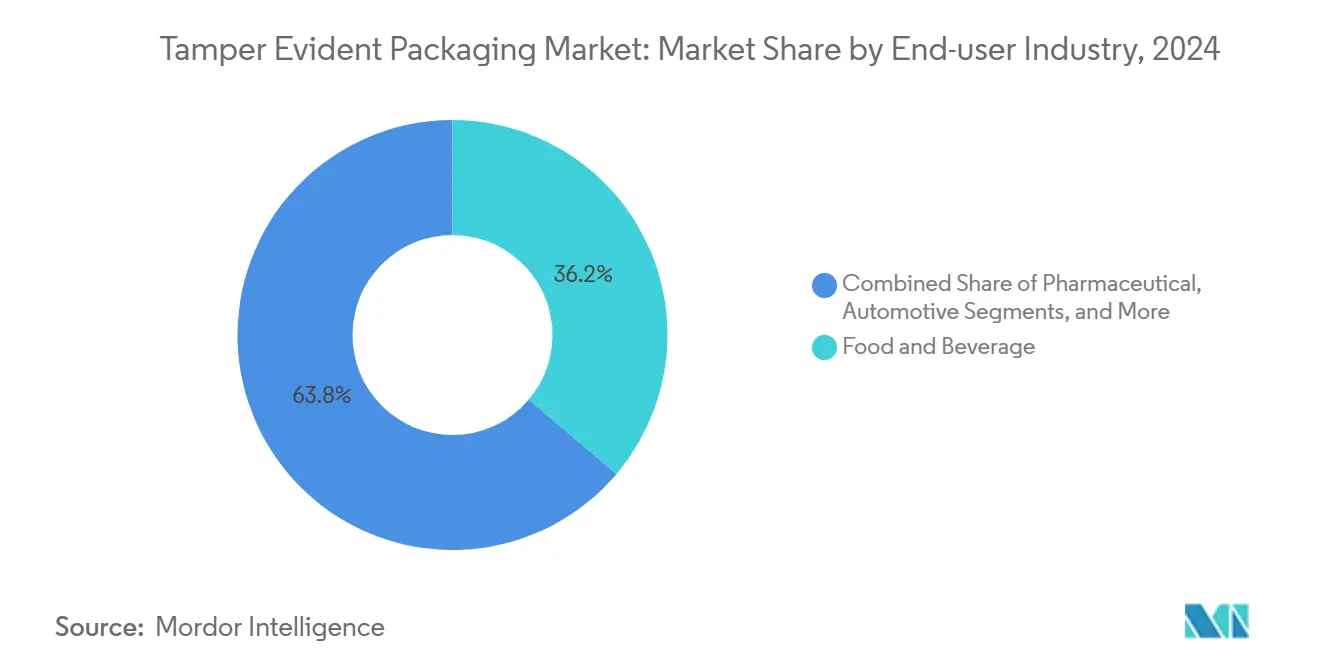

- By end-user, the pharmaceutical sector captured 36.18% of the tamper-evident packaging market share in 2024.

- By geography, the tamper-evident packaging market size in the Asia-Pacific region is projected to grow at a 11.28% CAGR between 2025–2030.

Global Tamper Evident Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising regulatory mandates for pharmaceutical serialization | +2.8% | Global, early gains in North America and the EU | Medium term (2-4 years) |

| Growth of e-commerce and last-mile delivery needs | +2.1% | Global, Asia-Pacific core with spill-over to the Middle East and Africa | Short term (≤ 2 years) |

| Counterfeit incidents in food and beverage supply chains | +1.9% | Asia-Pacific core, South America emerging | Medium term (2-4 years) |

| Smart tamper-evident features (NFC, blockchain) adoption | +1.7% | North America and the EU early adoption, Asia-Pacific following | Long term (≥ 4 years) |

| Net-zero commitments driving recyclable solutions | +1.4% | EU leading, North America, and Asia-Pacific adoption | Long term (≥ 4 years) |

| Expansion of injectable biologics packaging | +1.3% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Regulatory Mandates for Pharmaceutical Serialization

Global drug-traceability laws have matured from voluntary pilots into binding frameworks that dictate unit-level tracking and anti-tamper features. Full U.S. Drug Supply Chain Security Act enforcement in 2024 placed serialization and visible tamper evidence on every prescription unit, while the EU Falsified Medicines Directive sets identical obligations across 27 markets. Contract and generic manufacturers face direct purchasing consequences if they fail audits, creating a cascading demand wave among suppliers of seals, labels, and blister formats certified under ISO 12931. The surge is no longer limited to prescription therapeutics; nutraceuticals and high-value medical devices are mirroring pharmaceutical compliance to streamline distribution approvals. Large brands now treat tamper evidence as a top-five spend category in packaging budgets because audit penalties outweigh incremental seal costs.

Growth of E-Commerce and Last-Mile Delivery Needs

Parcel volumes rose by double digits in 2024, exposing packages to multiple hand-offs in vans, lockers, and doorsteps where pilferage risks multiply. Amazon’s program requiring tamper-evident seals on electronics and pharmaceuticals created a de facto industry baseline that other global merchants have copied.[1]Amazon, “Package Security Enhancement Program Annual Report,” Amazon.com Logistics providers now rate shippers based on the evidence of seal integrity at delivery, prompting brands in the beauty and personal care sectors to upgrade from basic tuck-in boxes to tear-strip mailers with irreversible adhesives. Package-theft losses topping USD 12 billion in 2024 persuaded insurers to reduce deductibles only for parcels shipped in compliant, track-and-trace pouches. The immediate revenue bump benefits low-cost films and fibers that print warning text and expiration data in a single pass, yet it also introduces headroom for premium NFC seals that capture open-time stamps. Because online volumes skew toward the Asia-Pacific region, incremental demand is highest in the region’s megacities, where courier networks remain fragmented.

Counterfeit Incidents in Food and Beverage Supply Chains

The discovery of falsified infant formula across Southeast Asia pushed nutrition regulators to mandate tamper-evident foil seals on powdered products starting in late 2024. Alcohol brands followed suit after high-margin spirits were diluted and resealed, eroding consumer trust across key nightlife hubs. Diageo’s NFC-enabled closures enable buyers to confirm provenance via their smartphone, transforming every package into a customer-engagement touchpoint. Liability payouts exceeding USD 50 million for a single tampering episode have reframed packaging from expense to risk-mitigation asset. Demand extends upstream to contract fillers and co-packers, which now specify tamper-evident over-wraps to protect multiple brand customers within shared lines. Asia-Pacific remains the epicenter, but Latin American authorities are fast-tracking similar rules after high-profile beverage scandals, setting a medium-term uplift of nearly two percentage points in regional CAGR.

Smart Tamper-Evident Features (NFC, Blockchain) Adoption

Brands are moving beyond passive visual cues toward digital verification that couples one-time seals with encrypted data. Novartis piloted blockchain-linked blister packs for oncology therapies, giving pharmacists and patients a cloud-verified authenticity record. NFC tags embedded inside tear-off closures unlock marketing content post-purchase, converting security spend into brand-engagement ROI. Investment economics favor medicines and luxury categories where unit margins exceed USD 5, offsetting incremental tag costs of USD 0.15-0.45 per pack. European and U.S. pilots now feed Asia-Pacific rollouts, as global brands seek harmonized SKUs. Scaling remains constrained by electronics recycling rules and privacy regulations, yet momentum signals a long-term value shift toward data-rich packaging, positioning tamper-evidence as an on-ramp to the Internet of Packs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced tamper-evident technologies | -1.8% | Global, more pronounced in emerging markets | Short term (≤ 2 years) |

| Environmental rules against multilayer plastics | -1.4% | EU leading, North America following | Medium term (2-4 years) |

| Specialty-resin supply shortages | -1.1% | Global, concentrated in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Consumer usability complaints | -0.9% | Developed markets, elderly demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Tamper-Evident Technologies

Incorporating NFC or blockchain technology raises the per-unit packaging cost by 25%-40%, a premium that many food and personal-care brands cannot absorb, given category margin ceilings. While pharmaceutical buyers accept CFO approval for USD 0.30 digital seals, fast-moving consumer goods struggle to justify the outlay, as packaging historically accounts for less than 5% of the cost of goods. Small and medium enterprises face further hurdles because specialty suppliers impose minimum order quantities exceeding USD 100,000 to reach volume pricing. Capital outlays also rise: machines that apply smart labels run 15% slower and require integration with cloud serialization software, resulting in productivity dips during the ramp-up period. As a result, adoption skews heavily toward premium SKUs, capping near-term penetration potential and subtracting almost two percentage points from the overall tamper-evident packaging market CAGR in price-sensitive regions.

Environmental Rules Against Multilayer Plastics

The European Union’s Single-Use Plastics Directive and Extended Producer Responsibility fees penalize insecure packaging that relies on non-recyclable composites. Traditional shrink sleeves, which are made from PVC, PET-G, and inks, often fail recyclability tests, forcing converters to redesign or pay escalated eco-modulation fees. Line-conversion costs range from USD 2 million to USD 8 million per plant, an expenditure that many mid-tier suppliers defer amid uncertain future rules. Paper-based tear-strips address recyclability yet can compromise moisture and oxygen barriers, prompting skepticism among brands selling shelf-stable foods. Regulatory uncertainty, particularly regarding the acceptance of chemical recycling, delays investment decisions across Europe and increasingly in North America, reducing forecast growth by at least 1.4 percentage points until clear, harmonized guidance emerges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Blister Packs Anchor Pharmaceutical Evolution

Blister and strip formats generated USD 810 million of the tamper-evident packaging market size in 2025 and are projected to accelerate at an 11.79% CAGR, as injectable biologics and personalized therapies require unit-dose integrity. The visibility of ripped lidding foil aligns with ISO 11607 sterility guidelines, enabling pharmacists to detect interference instantly. Rising demand for cold-chain biologics drives innovation in barrier films that protect sensitive actives from moisture while providing a clear peel indicator. Pharmaceutical lines converting from bulk bottles to calendar packs report an 8% reduction in wastage and increased patient adherence, reinforcing the financial logic behind higher unit costs. Brands also print serialized 2D codes under the foil, creating dual visual-digital authentication without altering dispenser workflows.

Shrink sleeves and bands continue to dominate retail shelf presence, accounting for 28.72% of the tamper-evident packaging market in 2024, as they deliver full-body branding and entry-level security for food, beverage, and OTC categories. Their unit cost remains under USD 0.02 when sourced at scale, keeping them the go-to solution for volume SKUs. However, shrinking versatility meets performance limits in high-temperature logistics, steering temperature-sensitive pharmaceuticals toward foil-plastic hybrids. Pouches and sachets address e-commerce performance gaps through lightweight, puncture-resistant laminates that lower dimensional weight in courier networks. Induction seals, heat-shrink bands and pull-tab lids complement the blister surge by safeguarding liquid nutraceuticals and premium dairy products, demonstrating that multi-format portfolios are now table stakes for converters seeking cross-category relevance.

By Material Type: Sustainability Reshapes Procurement Logic

Plastic maintained a 48.59% revenue share in the tamper-evident packaging market in 2024, as its seal strength and clarity underpin cost-effective protection. Polyolefin and polyethylene terephthalate films, which run on legacy equipment, adapt easily to heat-shrink or induction sealing, explaining their persistent dominance despite policy headwinds. Yet, Extended Producer Responsibility fees up to USD 1,800 per metric ton in several EU states now tilt the total cost of ownership in favor of recyclable mono-material options. Converters respond with PET-based shrink sleeves that deactivate inks at 205 °C, easing delamination during recycling without losing shrink ratios. Bio-based resins, notably polylactic acid, have entered pilot production for coffee capsules and single-use nutrition packs, marrying compostability claims with tamper-evident features at niche volumes.

Paper and paperboard are registering a 12.53% CAGR off a smaller base as brands position fiber seals as visible proof of sustainability alignment. Tear-out fiber voids signal interference, while compatible barrier coatings repel oils and limit moisture. Glass and aluminum regain their selective appeal among premium spirits and ophthalmic drugs, where oxygen and taste neutrality justify heavier formats. Supply-chain shocks in specialty resins during 2024 prompted global brands to dual-source between plastic and paperboard, reducing single-material dependency. Future winners will likely offer modular seal layers that migrate between substrates without retooling adhesive chemistries, reducing downtime and inventory risk for copackers.

By End-user Industry: Pharmaceuticals Remain the Innovation Catalyst

Pharmaceuticals contributed USD 925 million to the tamper-evident packaging market size in 2025 and are projected to grow at an annual rate of 11.49% as oncology and cell therapies demand serialized, temperature-verified packaging. FDA 21 CFR Part 211 container-closure integrity rules quantify leak-rate thresholds, prioritizing seals that combine deterministic testing with visible breach evidence. Unit-dose blister packaging supports medication adherence programs reimbursed by insurers, resulting in payback periods of under 12 months for chronic care drugs. Medical device makers piggyback on pharmaceutical lines, adopting foil-pouch formats that protect sterile implants yet open in sterile fields with a single peel. The sector’s scale and compliance culture make it a proving ground for digital seals, accelerating spin-offs into adjacent consumer categories.

Food and beverage commands the second-largest revenue block as counterfeit scares push tamper-evident requirements from premium spirits into mainstream nutrition staples. Alcoholic spirits embed tamper rings and NFC chips in composite closures, while functional beverages opt for pull-ring foil diaphragms that maintain carbonation. Cosmetics and personal-care players are integrating invisible tamper slits around pump collars to avoid disrupting shelf aesthetics, a trade-off that values brand experience as much as barrier properties. Automotive and industrial users remain niche but fast-rising, shielding high-value electronic control units and lithium-ion cells during global transit. Direct-to-consumer subscription models across all these verticals amplify repeat exposure to seals, embedding consumer expectation that every delivery arrives visibly secure.

Geography Analysis

The Asia-Pacific region provides the largest and fastest-growing demand pool, driven by China’s expansion of prescription drugs and India’s ambitions to export generics. Regional regulators accelerated their alignment with EU Falsified Medicines guidelines in 2024, triggering bulk orders for serialized blister packs that are compliant with both domestic and export lanes. Contract packers in Malaysia and Vietnam leverage cost advantages to supply multinational brands, and regional e-commerce giants prefer high-visibility tear strips that deter in-transit pilferage. Coupled with rising middle-class scrutiny of product authenticity, these factors support an 11.28% CAGR through 2030 and cement the region’s 36.29% 2024 revenue share lead.

North America exhibits high per-capita spending on advanced seals because the FDA now audits tamper-evidence alongside serialization files, turning compliance gaps into recall triggers.[2]U.S. Food and Drug Administration, “21 CFR Part 211 Current Good Manufacturing Practice,” FDA.gov Smart labels featuring NFC have earned early retail acceptance thanks to widespread smartphone penetration, while sustainability initiatives focus on curbside recyclability programs under the U.S. Plastics Pact. Canada’s pharmaceutical rules mirror U.S. standards, allowing suppliers to amortize regulatory investments across a contiguous market that prioritizes quality over price in critical health products.

Europe continues to direct innovation toward recyclable tamper-evident solutions to satisfy eco-design tenets embedded in its Packaging and Packaging Waste Directive. German beverage deposit systems already require closures that remain attached after opening, influencing tamper feature geometry. Simultaneously, European value chains champion digital product passports that link visible seals to cloud-based lifecycle data, effectively turning each pack into an audit node. Middle East and Africa plus Latin America compose the remaining revenue slices, each posting high-single-digit growth as local regulators strengthen traceability rules and multinational brands extend risk-mitigation policies to export plants.

Competitive Landscape

The tamper-evident packaging industry is characterized by a moderately fragmented state, with the top five suppliers controlling roughly 45% of global sales. Incumbents such as Amcor, Sealed Air, 3M, Mondi, and WestRock expand through strategic acquisitions, targeted capacity increases, and patent filings around hybrid plastic-fiber seals. Amcor’s USD 150 million commitment to NFC-enabled closures underscores a pivot toward integrating electronics inside conventional caps, a signal to contract packers that the company can bundle security with data analytics.[3]Amcor, “Smart Packaging Technology Investment Announcement,” Amcor.com Sealed Air’s USD 85 million buy-out of a European barrier-coating specialist augments recyclable fiber capacity while broadening IP around moisture-barrier chemistries. 3M leverages its heritage in adhesives and RFID to penetrate the automotive and high-value electronics markets, diversifying its end-market exposure beyond healthcare.

Technology entrants, blockchain consortia, printed-electronics startups, and authentication app providers exploit white-space by bundling software subscriptions with physical seals. Their ability to convert tamper evidence from a cost center into a data monetization asset threatens traditional converters lacking digital roadmaps. Patent activity jumped 32% year-on-year in 2024, with filings clustering around destruct-on-peel adhesives, color-change inks and flexible printed circuits. Converters able to license or co-develop with electronics firms appear best positioned to ride digital adoption curves without diluting capital returns.

Price competition remains contained because regulatory audits penalize substitution failures, allowing premium suppliers to defend margins. Yet consolidation pressure grows in specialty niches where compliance costs create high barriers to entry. Private-equity investors are bundling regional label converters to build scale ahead of a potential wave of serialization-related outsourcing, setting the stage for medium-term share shifts once standardized digital architectures emerge.

Tamper Evident Packaging Industry Leaders

Amcor plc

Sealed Air Corporation

3M Company

Smurfit WestRock plc

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Amcor announced a USD 150 million investment in smart packaging technologies, including NFC-enabled tamper-evident closures for pharmaceutical products.

- September 2025: Sealed Air Corporation completed the USD 85 million acquisition of specialized tamper-evident assets from a European competitor to bolster barrier-coating IP and sustainable formats.

- August 2025: 3M Company introduced RFID-embedded tamper-evident labels targeting electric vehicle component verification.

- July 2025: Mondi revealed a EUR 120 million (USD 132 million) expansion of paper-based, tamper-evident capacity across European plants.

- June 2025: WestRock Company formed a joint venture with a blockchain provider to co-develop serialization-ready tamper-evident solutions for regulated pharmaceuticals.

Global Tamper Evident Packaging Market Report Scope

| Shrink Sleeves and Bands |

| Blister and Strip Packs |

| Induction and Heat-Seal Lids |

| Tamper-Evident Closures and Caps |

| Pouches, Bags and Sachets |

| Film Over-wraps and Wrap-Around Labels |

| Other Products |

| Plastic |

| Paper and Paperboard |

| Glass |

| Metal Foils |

| Other Materials |

| Pharmaceutical |

| Food and Beverage |

| Cosmetics and Personal Care |

| Automotive |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product | Shrink Sleeves and Bands | ||

| Blister and Strip Packs | |||

| Induction and Heat-Seal Lids | |||

| Tamper-Evident Closures and Caps | |||

| Pouches, Bags and Sachets | |||

| Film Over-wraps and Wrap-Around Labels | |||

| Other Products | |||

| By Material | Plastic | ||

| Paper and Paperboard | |||

| Glass | |||

| Metal Foils | |||

| Other Materials | |||

| By End-user Industry | Pharmaceutical | ||

| Food and Beverage | |||

| Cosmetics and Personal Care | |||

| Automotive | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What drives current demand for tamper-evident packaging?

Regulatory serialization, e-commerce shipping risks, and high-profile counterfeiting incidents create an urgent need for visible and digital seals that protect brand integrity.

Which region leads to adoption?

Asia-Pacific leads with a 36.29% 2024 revenue share and an 11.28% CAGR to 2030, combining global manufacturing scale with rising consumer awareness.

How big is the pharmaceutical contribution?

Pharmaceuticals accounted for 36.18% of the 2024 revenue pool and remain the fastest-growing end-user, with a 11.49% CAGR through 2030.

Are sustainable materials gaining ground?

Yes, paper and paperboard seals are advancing at a 12.53% CAGR as Extended Producer Responsibility fees push brands toward recyclable alternatives.

What is the main barrier to smart tamper-evident features?

Upfront unit cost premiums of USD 0.15-0.45 restrict adoption to high-margin categories, though scale and regulatory pressure are narrowing the gap.

How fragmented is the supplier landscape?

The market is moderately fragmented, with the top five players controlling roughly 45% of sales. However, intense patent activity and digital disruptors are reshaping the competitive landscape.

Page last updated on: