Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.22 Trillion |

| Market Size (2031) | USD 1.44 Trillion |

| Growth Rate (2026 - 2031) | 3.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Packaging Market Analysis by Mordor Intelligence

The global packaging market size in 2026 is estimated at USD 1,220.36 billion, growing from 2025 value of USD 1,180 billion with 2031 projections showing USD 1,443.9 billion, growing at 3.42% CAGR over 2026-2031. This steady expansion demonstrates how the global packaging market continues to mature while absorbing regulatory costs linked to circular-economy mandates and shifting consumer expectations that favor sustainability over pure cost–performance metrics. Demand resilience arises from packaging’s irreplaceable protection, brand-building, and compliance functions across food, beverage, pharmaceuticals, and e-commerce channels. Asia-Pacific keeps capital intensity low through large-scale manufacturing, whereas developed regions invest in advanced recycling, mono-material films, and digital printing that enable near-real-time SKU launches. Meanwhile, e-commerce parcel growth, regulatory bans on single-use plastics, and corporate sustainability targets reinforce capital flows toward lighter materials, bio-based feedstocks, and on-demand customization platforms. Brands pursuing differentiation increasingly embed digital identifiers that support traceability, consumer engagement, and compliance with evolving extended producer responsibility (EPR) schemes.

Key Report Takeaways

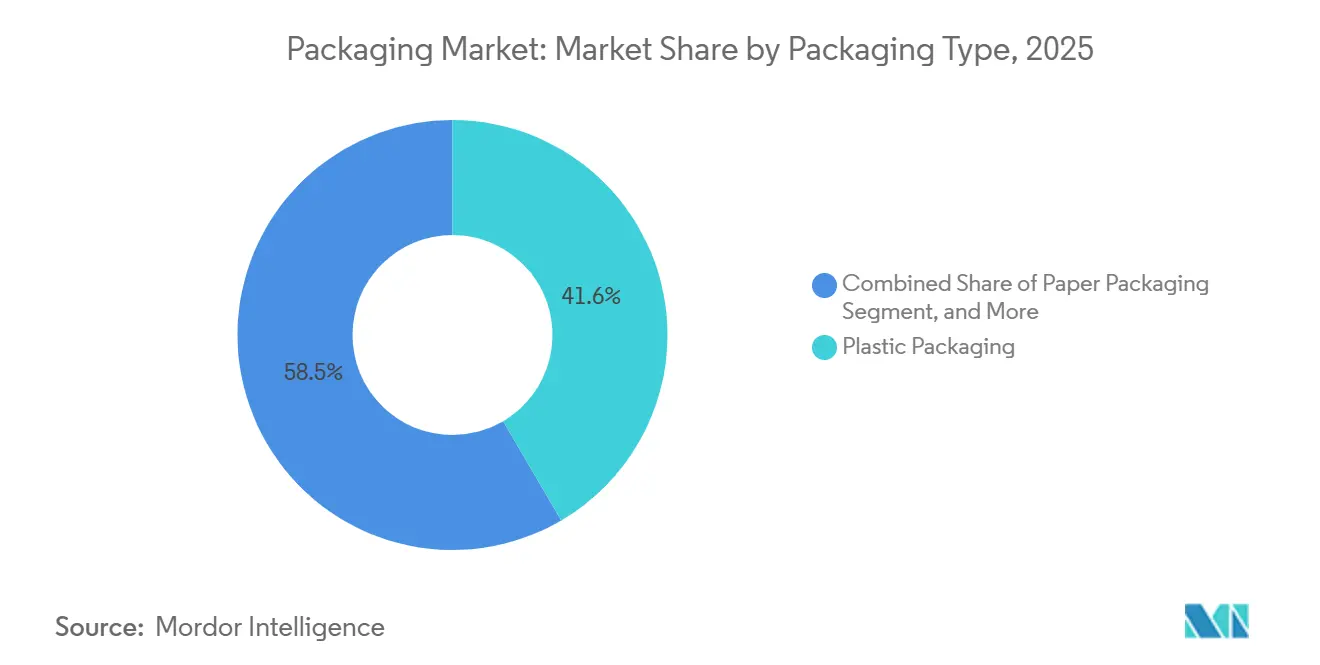

- By packaging type, plastic held 41.55% of the global packaging market share in 2025, while paper is the fastest-expanding packaging type, growing at a 4.62% CAGR to 2031.

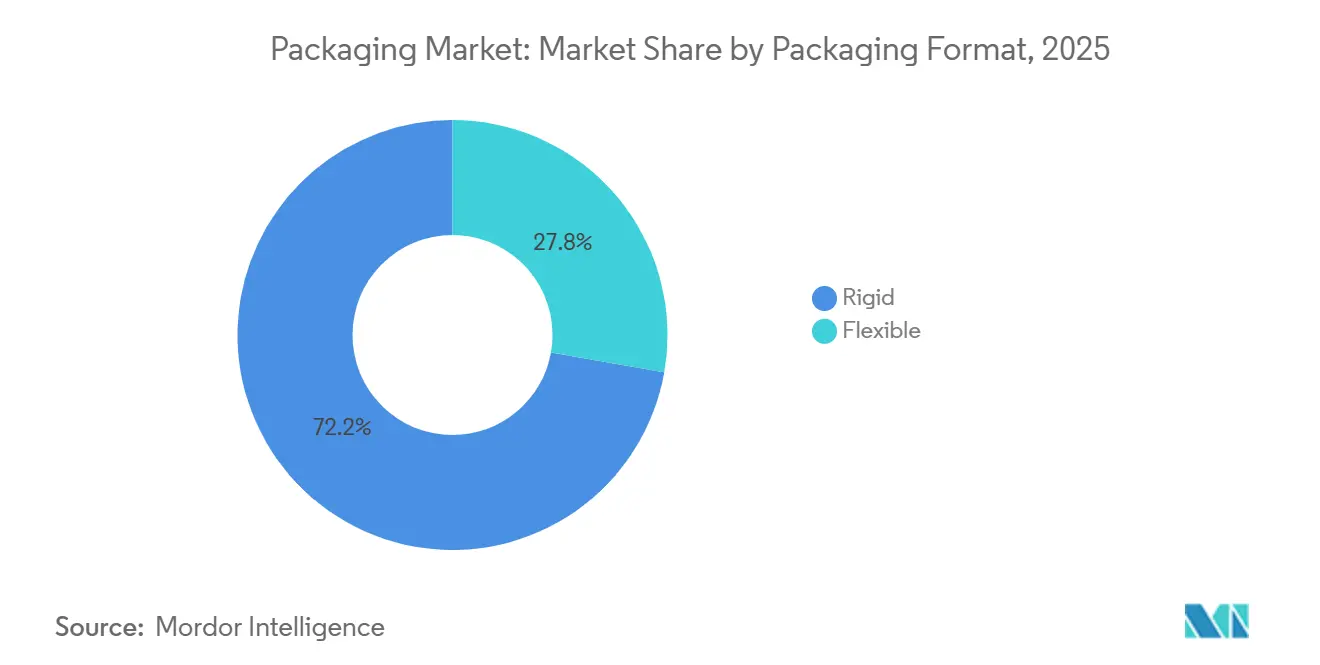

- By packaging format, rigid solutions captured 72.22% of the global packaging market revenue share in 2025. Whereas, flexible formats trail rigid ones in growth, with flexible packaging forecast to rise at a 4.26% CAGR through 2031.

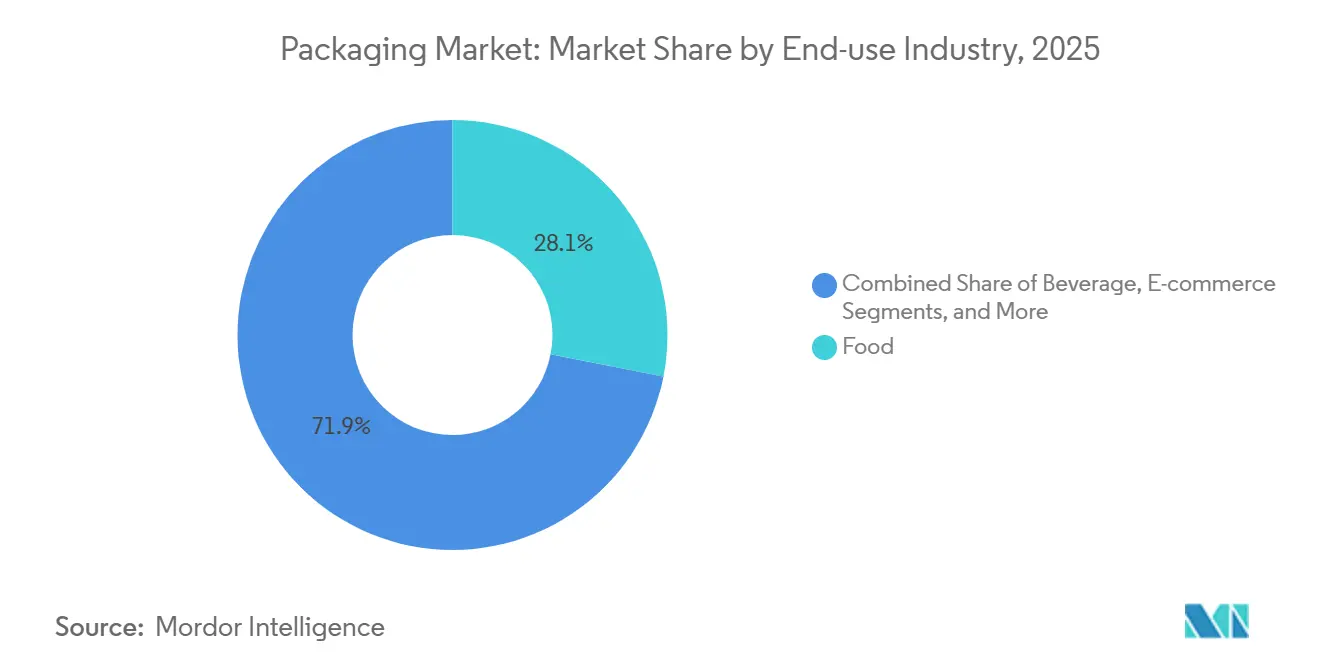

- By end-use industry, food accounted for 28.10% of the global packaging market size in 2025, while E-commerce leads growth, climbing at a 4.86% CAGR between 2026 and 2031.

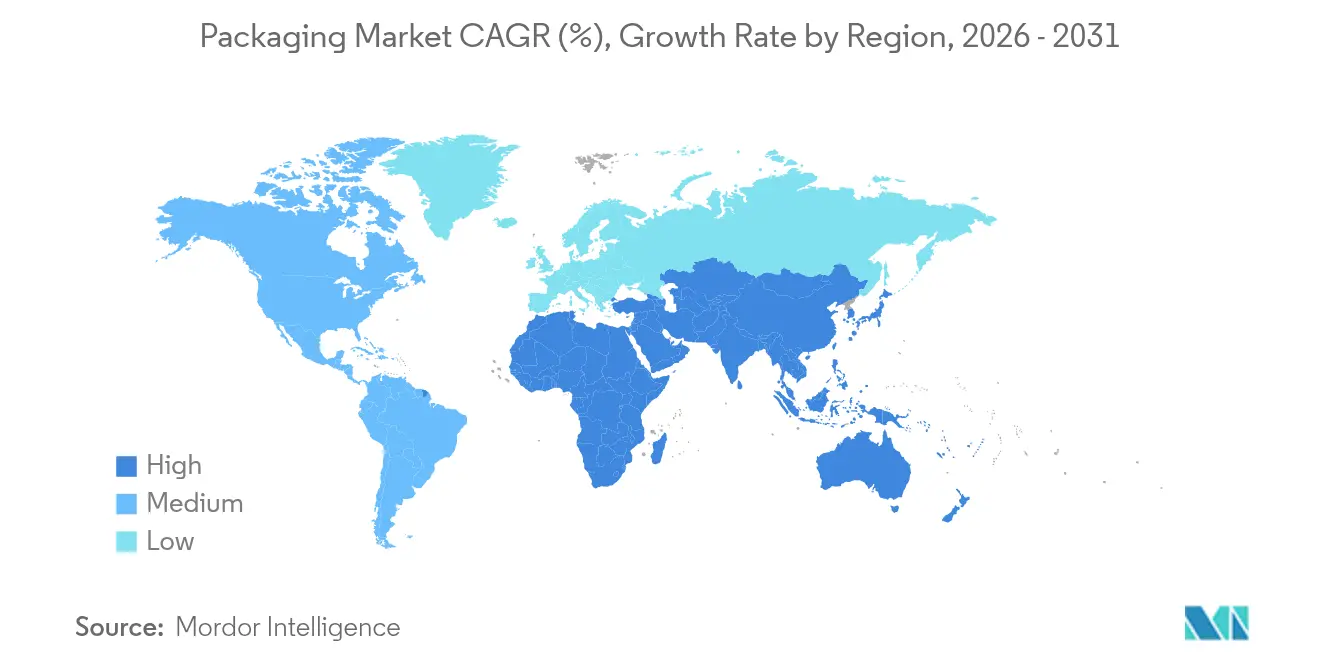

- By geography, Asia-Pacific accounted for 39.72% of the global packaging market in 2025. Whereas, the Middle East and Africa are projected to post the fastest regional CAGR at 3.89% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability-linked purchasing commitments | +1.0% | Global; EU & North America lead | Medium term (2-4 years) |

| E-commerce parcel volume explosion | +0.8% | Global; urban hubs | Short term (≤ 2 years) |

| Brand-owner shift to mono-material films | +0.5% | Europe & North America | Medium term (2-4 years) |

| Regulatory bans on single-use plastics | +0.7% | EU; selected U.S. states; emerging APAC | Long term (≥ 4 years) |

| On-site digital print enabling SKU proliferation | +0.4% | Developed markets | Short term (≤ 2 years) |

| Adoption of smart and connected packaging (IoT, QR, NFC-enabled solutions) | +0.6% | Global; strongest in North America, Europe, and advanced APAC | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Sustainability-Linked Purchasing Commitments Drive Material Innovation

Corporate mandates now specify minimum recycled content and confirmed recyclability, accelerating investment in molecular recycling plants and bio-based resins. Estée Lauder reached 71% compliance with its “5 Rs” packaging framework in 2024, illustrating how premium brands monetize sustainability narratives. Procurement teams embed carbon and recyclability metrics into supplier scorecards, a trend that aligns with forthcoming EPR fees that penalize hard-to-recycle formats. Certification programs such as the Association of Plastic Recyclers’ design-for-recycling guidelines supply technical blueprints that shorten development cycles. As a result, resin suppliers scale depolymerization units that return PET and polyamide to virgin-grade feedstock, letting converters hit recycled-content targets without compromising shelf life. Investors reward companies that link executive bonuses to packaging footprint reductions, further institutionalizing sustainable-material adoption.[1]Amcor plc, “Amcor Completes Merger with Berry Global,” amcor.com

E-Commerce Parcel Volume Explosion Reshapes Protective Packaging

Urban fulfillment centers ship billions of single-item orders that face more handling steps than traditional store deliveries, heightening damage-prevention needs. Amazon’s AI-driven pack-line optimization removed 95% of plastic air pillows, substituting paper cushioning that maintains product integrity and improves curbside recyclability. [2]Amazon, “Amazon Eliminates 95% of Plastic Air Pillows,” amazon.com Automated right-sizing machinery now cuts custom corrugated blanks per order, trimming material use by up to 30% while slashing dimensional-weight fees. These volume dynamics elevate demand for lightweight flexible mailers with integrated tear strips and return seals. Digital presses print small-batch graphics that reinforce brand storytelling during unboxing. Consequently, converters capable of integrating data analytics with converting assets capture growing e-commerce wallet share, while traditional bulk shippers retrofit plants with new forming and sealing technologies.

Brand-Owner Shift to Mono-Material Films Simplifies Recycling

Barrier performance traditionally required laminated PET, aluminum, and PE layers that standard sortation equipment cannot separate. Moving to mono-material structures eases collection and reprocessing, aligning with supermarket chains that publicly commit to recycling-ready private-label packaging. High-barrier PE and PP films now incorporate EVOH tie layers or plasma-deposited coatings that preserve oxygen and moisture barriers yet remain sortable in existing streams. Pilot projects show recycling yields improve 20-30 percentage points when mixed-material laminates exit the waste stream. Equipment suppliers introduce blown-film lines optimized for all-PE pouches, while ink makers develop de-inkable systems that leave no optical residue after washing. This platform approach reduces EPR levies and supports retailers’ closed-loop plastic targets, guiding capital budgets toward mono-material capacity additions in Europe and North America.

Regulatory Bans on Single-Use Plastics Accelerate Alternatives

The EU Packaging and Packaging Waste Regulation (PPWR 2025/40) prohibits non-recyclable formats above defined plastic content thresholds, pushing brands to switch to paper, compostable fiber, or recyclable PP solutions. California extends the ban to PFAS-laden wrappers, forcing quick-service chains to trial fluorine-free grease barriers. Start-ups commercialize seaweed-based films and cellulose coatings that meet food-contact regulations while offering backyard-compostable end-of-life options. Beverage brands hedge aluminum tightness by piloting fiber bottles fitted with thin-film barrier liners. Compliance deadlines concentrate R&D spending, creating a pipeline of alternative-material stock-keeping units scheduled for 2026-2027 launches. Retailers add recyclability icons and disposal instructions on front panels to satisfy consumer demand for clear sustainability signaling.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-oil price volatility impacting resin costs | -0.7% | Global; resin-dependent regions | Short term (≤ 2 years) |

| Rising anti-plastic sentiment in developed economies | -0.5% | North America & Europe | Medium term (2-4 years) |

| Aluminum can sheet supply tightness | -0.3% | Global beverages | Medium term (2-4 years) |

| Container-glass furnace energy inflation | -0.4% | Europe; energy-intensive hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil Price Volatility Impacts Resin Budgets

Polyethylene, polypropylene, and PET prices correlate strongly with Brent crude, creating unpredictable margin swings for converters on quarterly contracts. Sudden USD 10 per-barrel spikes in 2024 translated into double-digit resin surcharges inside four weeks, straining small extruders that lack hedging tools. Brand owners demanded fixed-price agreements, shifting cost risk downstream and prompting converters to accelerate recycled-content usage that follows a different price curve. Paperboard prices also climbed because higher diesel rates elevated transport costs and chemical inputs. The volatility steers capital toward regional resin suppliers and shortens supply chains, although capacity gaps persist in high-purity rPET pellets needed for food-grade applications.

Rising Anti-Plastic Sentiment Shapes Brand Decisions

Consumer surveys show more than half of shoppers in the United States and Europe actively avoid plastic-wrapped goods when alternatives exist. Media coverage of ocean debris elevates reputational stakes, causing retailers to delist packs deemed “over-packaged.” Personal-care brands adopt refill pods or glass jars to signal eco-leadership, despite higher breakage risk and weight. Marketing budgets now earmark life-cycle assessment disclosures as core message elements. However, functional requirements sometimes necessitate plastic; therefore, brands emphasize mono-material recyclability and chemical-recycling partnerships to counter perception gaps. This sentiment acts as a drag on volume growth for conventional plastic formats, even as specialty polymers grow in high-value medical and barrier applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Paper Gains Momentum Despite Plastic Dominance

Plastic packaging retained 41.55% of the global packaging market share in 2025 on the strength of its versatility, sealing speed, and cost efficiency. Yet paper packaging’s 4.62% CAGR through 2031 outpaces overall global packaging market growth as regulators and brand charters privilege renewable fiber over petroleum-based substrates. The global packaging market size allocated to paper formats widens, supported by barrier coatings that now survive freezer-to-microwave cycles. Corrugated converters invest in digital single-pass presses that enable shelf-ready graphics, letting retailers skip additional display trays. Material substitution accelerates in quick-service food, where fiber bowls replace expanded polystyrene, and in confectionery multipacks that migrate from oriented polypropylene to recyclable coated paper.

The rigid plastics segment preserves traction via innovations in mono-material PET jars and HDPE bottles compatible with mechanical recycling, sustaining share in sauces, dairy, and home-care. Flexible plastic films enjoy e-commerce tailwinds owing to their low weight and tamper-evident seals. Meanwhile, metal cans face supply-chain limits as aerospace and automotive demand collide with packaging orders, driving cost pressure. Glass maintains niche roles in premium beverages but absorbs energy-price shocks that encourage light-weighting. Fiber growth continues as mills ramp high-performance linerboards capable of replacing bleached polyethylene-coated cartons, creating new value pools inside the global packaging market.

By Packaging Format: Flexible Solutions Drive Efficiency Gains

Rigid formats captured 72.22% of the global packaging market in 2025, remaining critical for industries requiring stackability, dosing precision, and tamper resistance. PET bottles are transitioning to tethered caps to comply with EU directives, while returnable glass pool systems are re-emerging in regional beverage markets. Corrugated boxes, a mainstay in transport packaging, are experiencing volume shifts to paper mailers and molded fiber cushioned sleeves. Additionally, hybrid formats, such as paper-based tubes with thin polymer linings, are gaining traction by combining rigidity and flexibility, unlocking growth opportunities in the premium personal-care kit segment of the global packaging market.

Flexible formats are projected to achieve a 4.26% CAGR through 2031, offering comparable protection with up to 70% less material than rigid alternatives. This growth aligns with the increasing shift toward online fulfillment, where parcel dimensions directly impact logistics costs, driving demand for mailers, pouches, and sachets. Companies are capitalizing on the "billboard effect" of high-definition flexographic and digital prints on films, delivering sharp graphics without requiring secondary labels. Retort pouches are expanding their presence in wet-food and ready-meal categories, capturing market share from traditional metal cans and glass jars while enhancing sustainability through a reduced carbon footprint.

By End-Use Industry: E-Commerce Disrupts Traditional Hierarchies

Food maintained 28.10% of the global packaging market size in 2025, reflecting unbroken demand for safe, shelf-stable products across every region and income bracket. Multilayer barrier films, aseptic cartons, and thermoformed trays anchor this volume, while recyclable mono-material solutions gain ground. Beverage applications face aluminum sheet shortages, prompting craft brewers to pilot fiber bottles and fill-in lines compatible with tethered caps.

E-commerce, though smaller today, grows fastest at 4.86% CAGR, redirecting design priorities from shelf visibility to dimensional optimization. Parcel movement multiplies drop-tests, so cushioned mailers and inflation-on-demand systems proliferate. Personal-care brands leverage the unboxing moment with digitally printed tissue and branded tape, reinforcing loyalty despite minimal touchpoints. Pharmaceutical packaging accelerates smart-label adoption to meet DSCSA traceability deadlines, incorporating serialized 2D codes that authenticate every saleable unit. Industrial packaging introduces returnable drums and foldable IBCs that align with circular-logistics mandates, rounding out heterogeneous demand drivers inside the global packaging market.

Geography Analysis

Asia-Pacific’s 39.72% share reflects unparalleled manufacturing density plus rising disposable incomes that expand packaged food, beverage, and personal-care consumption. China dominates flexible film extrusion capacity, while India’s blister-pack output meets growing pharmaceutical demand and exports to Africa. Mature markets like Japan and South Korea add value through high-precision converting, antimicrobial coatings, and digital embellishment. Indonesia and Vietnam scale corrugated plants to support electronics export hubs, fueling steady cartonboard demand.

Europe maintains leadership in eco-design, leveraging PPWR-driven mandates that incentivize source-reduced and recyclable solutions. Germany’s closed-loop PET system achieves collection rates near 98%, offering a blueprint for other member states. France and Italy expand producer-responsibility schemes that reward post-consumer resin usage with fee discounts. Eastern Europe attracts flexible-packaging investments that balance wage competitiveness with EU market proximity, giving converters cost and compliance advantages.

North America’s mature consumption drives consistent replacement demand, yet growth pockets emerge in omnichannel fulfillment. U.S. converters automate corrugated factories with robotics, meeting Amazon Frustration-Free guidelines for damage-free delivery. Canada’s deposit systems support high-quality glass recycling that supplies craft beverage fillers, while Mexico’s resin plants feed both domestic and U.S. markets, hedging against supply shocks.

Middle East and Africa accelerates as Saudi Arabia and UAE diversify economies; new megacities attract modern retail formats requiring sophisticated primary and secondary packaging. South Africa’s collection infrastructure upgrades enable rPET availability, feeding regional bottle loops and embedding circular practices into the expanding global packaging market.

Competitive Landscape

Moderate concentration characterizes the global packaging market, where scale, material breadth, and regulatory expertise differentiate leading suppliers. Amcor, International Paper, and Crown Holdings leverage geographically dispersed plants and integrated raw-material access to serve multinational brand owners under multi-year contracts. Amcor’s merger with Berry Global created a super-scale entity emphasizing recycled-content platforms and down-gauging technology. International Paper invests in containerboard mills that feed e-commerce tailwinds, while Crown divested its European beverage can unit to sharpen focus on high-growth segments.

Strategic moves concentrate on sustainability credentials and value-added services. Sonoco’s USD 3.9 billion Eviosys acquisition expands metal packaging scale and grants access to advanced peel-off ends used in ready meals. [3]Sonoco Products Company, “Sonoco Completes Eviosys Acquisition,” sonoco.comSealed Air reorganized around Food and Protective units, freeing resources for paper-based cushioning and smart-label development. Private-equity investors fund specialty converters in molded fiber, refill systems, and anticounterfeit labels, exerting competitive pressure on incumbents with slower innovation cycles.

Technological differentiation escalates. Players integrate data platforms that predict pack-line downtime, automate pallet configuration, and embed GS1 Digital Link 2D codes for consumer engagement. Converters cross-license barrier-coating patents to keep pace with PPWR recyclability standards. Rapid prototyping hubs near brand-owner design centers collapse concept-to-launch timelines, a critical advantage when promotional cycles compress. Overall, competition hinges on who can balance cost, compliance, and creativity while scaling alternative materials inside the evolving global packaging market.

Packaging Industry Leaders

International Paper Company

Mondi plc

Oji Holdings Corporation

UFlex Limited

Smurfit Westock

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Xampla partnered with Huhtamaki to supply Bunzl UK & Ireland with plant-based coated hot-food boxes featuring Morro coating technology.

- July 2025: Pulpex equipped Evolve Organic Beauty with fiber-based refillable shower bottles.

- June 2025: APC Packaging launched airless refillable systems for sustainable cosmetic applications.

- May 2025: Albéa Tubes provided Laboratoires SVR with recyclable makeup-remover balm packaging featuring 95% polyethylene construction.

Global Packaging Market Report Scope

Packaging refers to wrapping or bottling products to protect them from damage during transportation and storage. It keeps a product safe and marketable and helps to identify, describe, and promote it.

The packaging market is segmented by packaging type (plastic packaging (rigid plastic packaging (material type (polyethylene (PE - high-density polyethylene (HDPE) and low-density polyethylene (LDPE)), polypropylene (PP), polyethylene terephthalate (pet), polyvinyl chloride (PVC), polystyrene (PS) and expanded polystyrene (eps) , other material types ), product type (bottles and jars (containers), caps and closures, bulk-grade products - IBC, crates, pallets, drums, other product types), end-user industry (food, beverage, industrial and construction, automotive, cosmetics and personal care, other end-user industries), flexible plastic packaging ((material type (polyethylene (PE)), biaxially oriented polypropylene (BOPP), cast polypropylene (CPP), other material types), product type (pouches, bags, films and wraps), end user industry (food, beverage, pharmaceutical, cosmetics and personal care, other end-user industries), region (North America, Europe, Asia Pacific, Middle East And Africa, Latin America), paper and paperboard (product type (folding carton and rigid boxes, corrugated boxes and containers, single-use paper products (bags and pouches, cups, and trays among others), end-user industry (food, beverage, industrial and electronics, cosmetics and personal care, healthcare, other end-user industries), region (North America, Europe, Asia Pacific, Middle East And Africa, Latin America), metal packaging (product type (cans (food, beverage, aerosols, and others), caps and closures, other product types )), region (North America, Europe, Asia Pacific, Middle East And Africa, Latin America), container glass (end-user industry (food, beverage (alcoholic and non-alcoholic), personal care and cosmetics, pharmaceuticals)), region (North America, Europe, Asia Pacific, Middle East And Africa, Latin America). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

By Packaging Type

| Plastic Packaging | By Type | Rigid Plastic Packaging | By Material Type | Polypropylene (PP) |

| Polyethylene Terephthalate (PET) | ||||

| Polyvinyl Chloride (PVC) | ||||

| Polystyrene (PS) and Expanded Polystyrene (EPS) | ||||

| Other Material Types | ||||

| By Product Type | Bottles and Jars | |||

| Caps and Closures | ||||

| Trays and Containers | ||||

| Other Product Types | ||||

| By End-use Industry | Food | |||

| Beverage | ||||

| Pharmaceutical | ||||

| Cosmetics and Personal Care | ||||

| Industrial | ||||

| Other End-use Industries | ||||

| Flexible Plastic Packaging | By Material Type | Polyethylene (PE) | ||

| Biaxially Oriented Polypropylene (BOPP) | ||||

| Cast Polypropylene (CPP) | ||||

| Other Material Types | ||||

| By Product Type | Pouches and Bags | |||

| Films and Wraps | ||||

| Other Product Types | ||||

| By End-use Industry | Food | |||

| Beverage | ||||

| Pharmaceutical | ||||

| Cosmetics and Personal Care | ||||

| Industrial | ||||

| Other End-use Industries | ||||

| By Product Type | Bottles and Jars | |||

| Pouches and Bags | ||||

| Bulk-Grade Products | ||||

| Other Product Types | ||||

| By End-use Industry | Food | |||

| Beverages | ||||

| Cosmetics and Personal Care | ||||

| Pharamceuticals | ||||

| Industrial | ||||

| Other End-use Industries | ||||

| Paper Packaging | By Product Type | Folding Carton | ||

| Corrugated Boxes | ||||

| Liquid Paperboard | ||||

| Other Product Types | ||||

| By End-use Industry | Food | |||

| Beverages | ||||

| E-commerce | ||||

| Other End-use Industry | ||||

| Container Glass | By Color | Green | ||

| Amber | ||||

| Flint | ||||

| Other Colors | ||||

| By End-use Industry | Food | |||

| Alcoholic | ||||

| Non-Alcoholic | ||||

| Personal Care and Cosmetics | ||||

| Pharmaceuticals (excluding Vials and Ampoules) | ||||

| Perfumery | ||||

| Metal Cans and Containers | By Material Type | Steel | ||

| Aluminum | ||||

| By Product Type | Cans | |||

| Drums and Barrels | ||||

| Caps and Closures | ||||

| Other Product Types | ||||

| By End-use Industry | Food | |||

| Beverage | ||||

| Chemicals and Petroleum | ||||

| Industrial | ||||

| Paints and coatings | ||||

| Other End-use Industries | ||||

By Packaging Format

| Rigid |

| Flexible |

By End-Use Industry

| Food |

| Beverage |

| Pharmaceuticals and Healthcare |

| Personal Care and Cosmetics |

| Industrial |

| E-commerce |

| Other End-use Industry |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Mexico | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Thailand | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Packaging Type | Plastic Packaging | By Type | Rigid Plastic Packaging | By Material Type | Polypropylene (PP) |

| Polyethylene Terephthalate (PET) | |||||

| Polyvinyl Chloride (PVC) | |||||

| Polystyrene (PS) and Expanded Polystyrene (EPS) | |||||

| Other Material Types | |||||

| By Product Type | Bottles and Jars | ||||

| Caps and Closures | |||||

| Trays and Containers | |||||

| Other Product Types | |||||

| By End-use Industry | Food | ||||

| Beverage | |||||

| Pharmaceutical | |||||

| Cosmetics and Personal Care | |||||

| Industrial | |||||

| Other End-use Industries | |||||

| Flexible Plastic Packaging | By Material Type | Polyethylene (PE) | |||

| Biaxially Oriented Polypropylene (BOPP) | |||||

| Cast Polypropylene (CPP) | |||||

| Other Material Types | |||||

| By Product Type | Pouches and Bags | ||||

| Films and Wraps | |||||

| Other Product Types | |||||

| By End-use Industry | Food | ||||

| Beverage | |||||

| Pharmaceutical | |||||

| Cosmetics and Personal Care | |||||

| Industrial | |||||

| Other End-use Industries | |||||

| By Product Type | Bottles and Jars | ||||

| Pouches and Bags | |||||

| Bulk-Grade Products | |||||

| Other Product Types | |||||

| By End-use Industry | Food | ||||

| Beverages | |||||

| Cosmetics and Personal Care | |||||

| Pharamceuticals | |||||

| Industrial | |||||

| Other End-use Industries | |||||

| Paper Packaging | By Product Type | Folding Carton | |||

| Corrugated Boxes | |||||

| Liquid Paperboard | |||||

| Other Product Types | |||||

| By End-use Industry | Food | ||||

| Beverages | |||||

| E-commerce | |||||

| Other End-use Industry | |||||

| Container Glass | By Color | Green | |||

| Amber | |||||

| Flint | |||||

| Other Colors | |||||

| By End-use Industry | Food | ||||

| Alcoholic | |||||

| Non-Alcoholic | |||||

| Personal Care and Cosmetics | |||||

| Pharmaceuticals (excluding Vials and Ampoules) | |||||

| Perfumery | |||||

| Metal Cans and Containers | By Material Type | Steel | |||

| Aluminum | |||||

| By Product Type | Cans | ||||

| Drums and Barrels | |||||

| Caps and Closures | |||||

| Other Product Types | |||||

| By End-use Industry | Food | ||||

| Beverage | |||||

| Chemicals and Petroleum | |||||

| Industrial | |||||

| Paints and coatings | |||||

| Other End-use Industries | |||||

| By Packaging Format | Rigid | ||||

| Flexible | |||||

| By End-Use Industry | Food | ||||

| Beverage | |||||

| Pharmaceuticals and Healthcare | |||||

| Personal Care and Cosmetics | |||||

| Industrial | |||||

| E-commerce | |||||

| Other End-use Industry | |||||

| By Geography | North America | United States | |||

| Canada | |||||

| Mexico | |||||

| South America | Brazil | ||||

| Argentina | |||||

| Mexico | |||||

| Rest of South America | |||||

| Europe | Germany | ||||

| France | |||||

| United Kingdom | |||||

| Italy | |||||

| Spain | |||||

| Poland | |||||

| Rest of Europe | |||||

| Asia-Pacific | China | ||||

| India | |||||

| Japan | |||||

| Thailand | |||||

| Australia | |||||

| South Korea | |||||

| Rest of Asia-Pacific | |||||

| Middle East and Africa | Middle East | Saudi Arabia | |||

| United Arab Emirates | |||||

| Turkey | |||||

| Rest of Middle East | |||||

| Africa | South Africa | ||||

| Nigeria | |||||

| Egypt | |||||

| Rest of Africa | |||||

Key Questions Answered in the Report

How large is the global packaging market in 2026?

The global packaging market size stands at USD 1.22 trillion in 2026.

What CAGR is forecast for worldwide packaging demand through 2031?

Market value is projected to rise at a 3.42% CAGR between 2026 and 2031.

Which packaging format is expanding fastest?

Flexible formats are growing at a 4.26% CAGR thanks to material efficiency and e-commerce adoption.

Which end-use sector shows the strongest growth momentum?

E-commerce packaging leads with a 4.86% CAGR through 2031 as parcel volumes soar.

What region is expected to post the highest growth rate?

Middle East and Africa is forecast to expand at a 3.89% CAGR, outpacing all other regions.

How are leading companies responding to sustainability mandates?

Market leaders pursue mergers, recycled-content expansion, and mono-material innovation to meet strict regulatory and brand-owner targets.

Page last updated on: