Recombinant Vaccines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

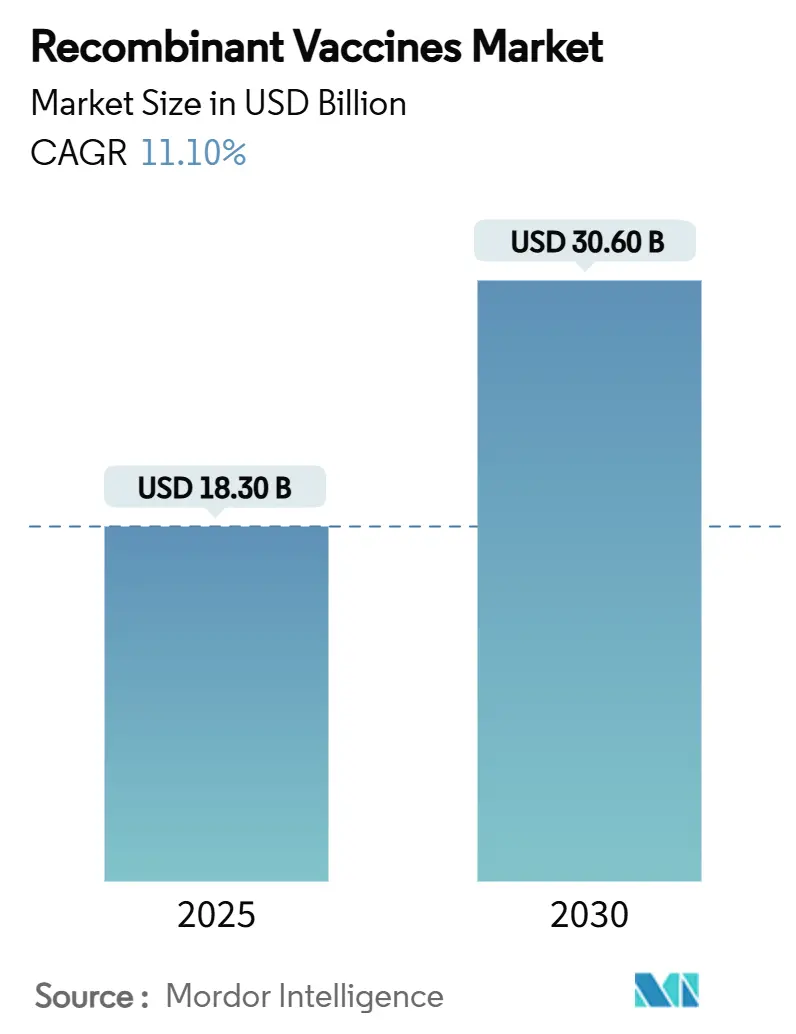

| Market Size (2025) | USD 18.30 Billion |

| Market Size (2030) | USD 30.60 Billion |

| Growth Rate (2025 - 2030) | 11.10% CAGR |

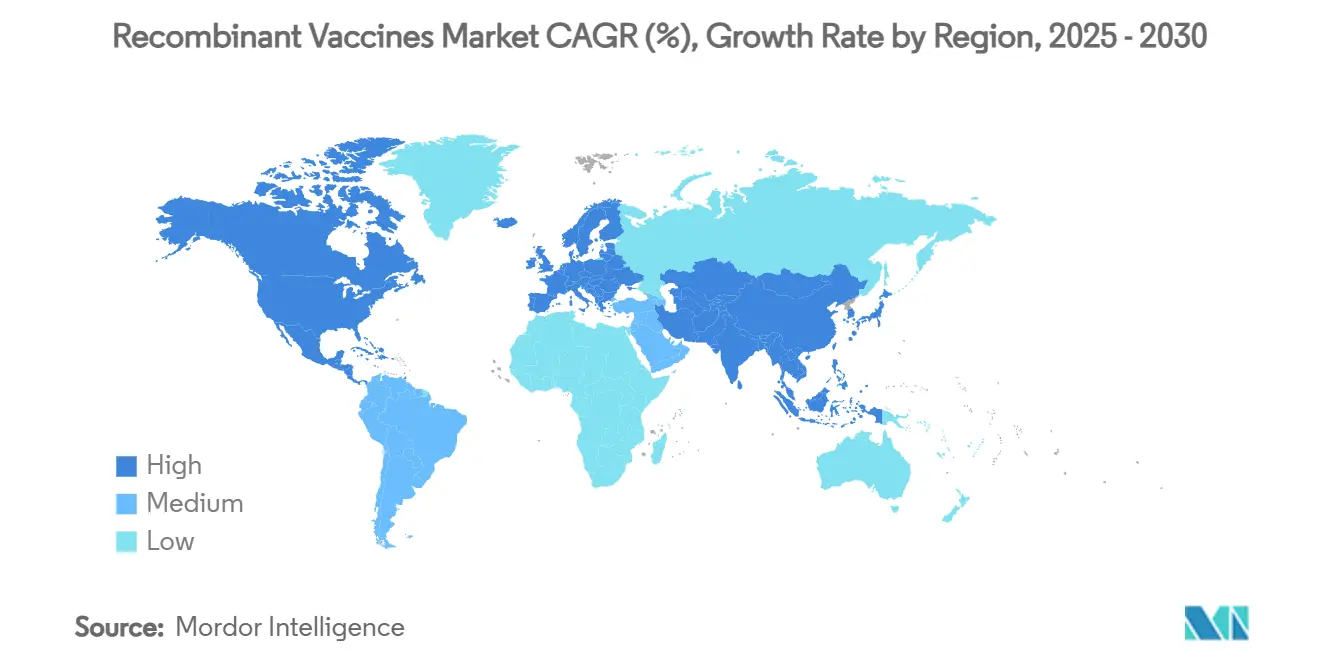

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recombinant Vaccines Market Analysis by Mordor Intelligence

The recombinant vaccines market size stands at USD 18.3 billion in 2025 and is projected to reach USD 30.6 billion by 2030, reflecting an 11.1% CAGR over the forecast period. Surging government mandates, especially for human papillomavirus (HPV) immunization, and sustained pandemic-preparedness funding keep capacity utilization high and improve scale efficiency across every major expression platform. Rising demand for thermostable formulations that limit cold-chain dependence, coupled with the rapid iteration advantages of messenger-RNA (mRNA) backbones, continues to pull investment away from legacy egg-based production toward precision synthetic biology. The recombinant vaccines market benefits from a globally diversified manufacturing footprint that now includes plant-based and yeast-based systems capable of sub-USD 1 per-dose economics, strengthening the commercial rationale for large adult-catch-up programs in low- and middle-income countries. Meanwhile, AI-guided epitope design and modular single-use bioreactors compress early development timelines, allowing faster pivoting to emerging pathogens and reinforcing the resilience of the recombinant vaccines market.

Key Report Takeaways

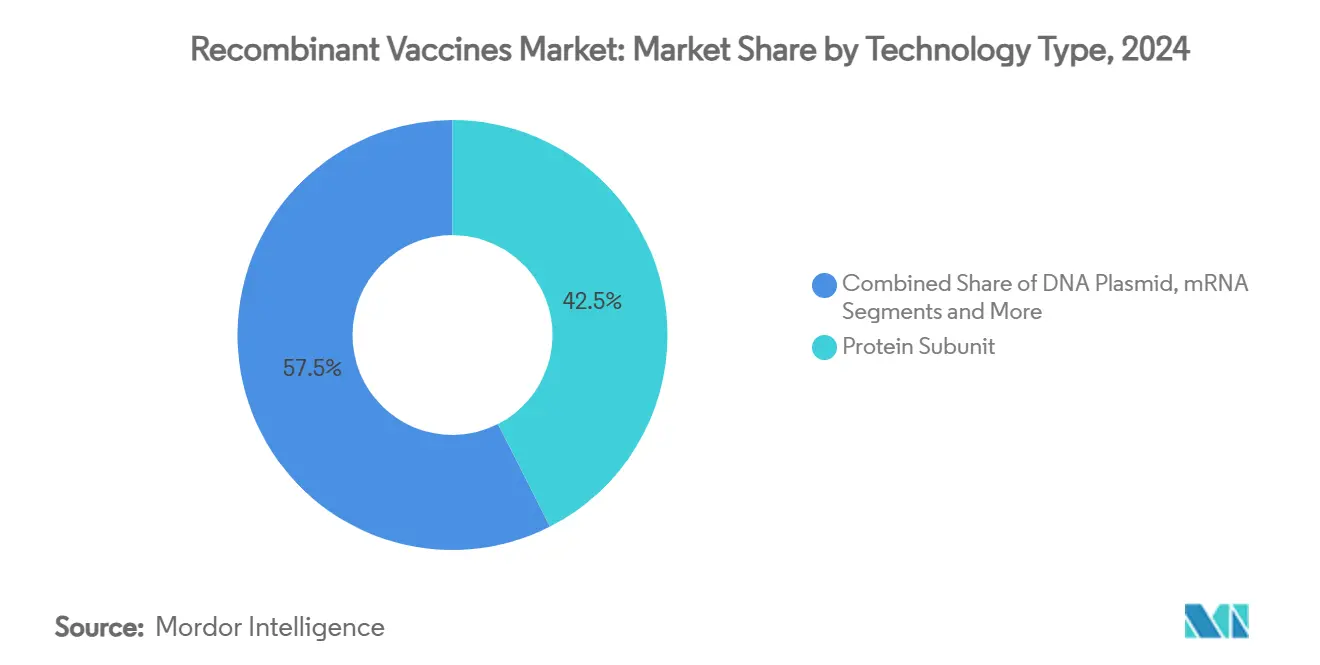

- By technology type, protein subunit products led with 42.5% revenue share in 2024, while mRNA platforms are poised for an 18.2% CAGR to 2030.

- By disease indication, HPV vaccines accounted for 47.8% of the recombinant vaccines market share in 2024, whereas dengue vaccines are advancing at a 16.5% CAGR through 2030.

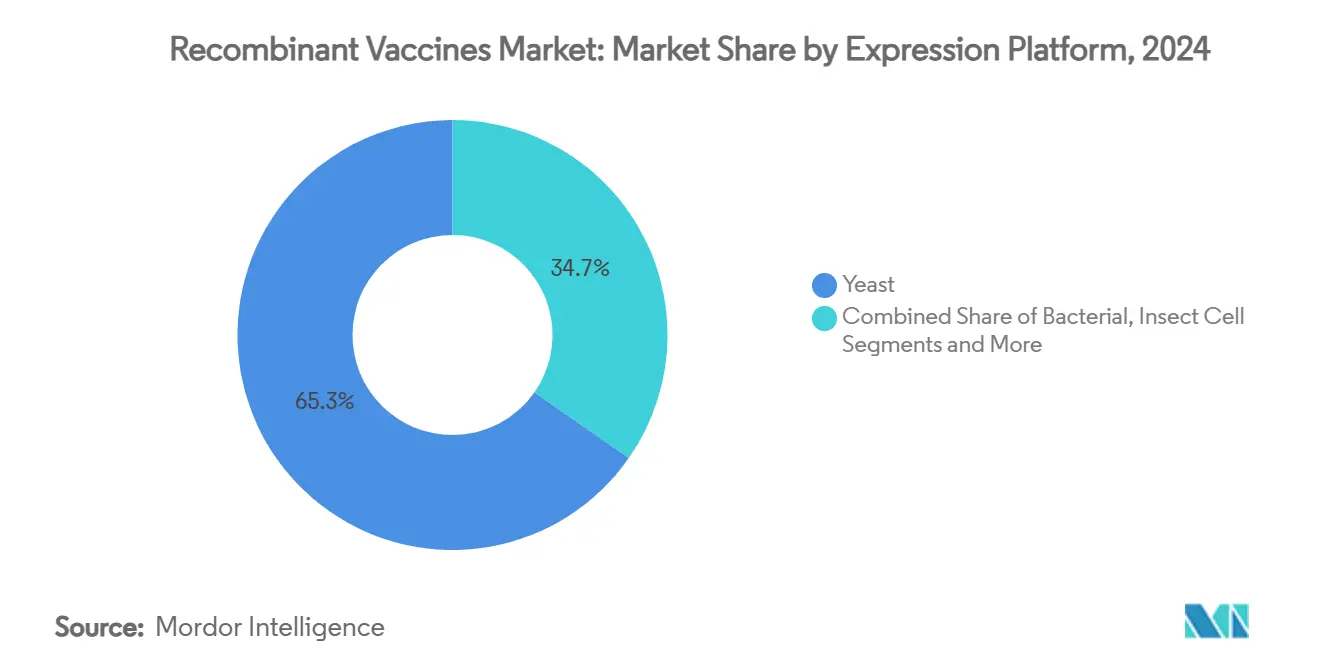

- By expression platform, yeast systems held 65.3% of the recombinant vaccines market size in 2024; plant-based systems are forecast to expand at a 21.0% CAGR.

- By end user, pediatric schedules captured 55.2% of total revenue in 2024, but geriatric applications are projected to grow at a 12.4% CAGR.

- By geography, North America commanded 35.8% of global sales in 2024, while Asia Pacific is on track for a 9.6% CAGR to 2030.

Global Recombinant Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HPV Vaccination Mandates Expanding Globally | +2.50% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Pandemic-Preparedness Funding For Rapid Platform Scale-Up | +1.80% | Global, concentrated in G7 nations | Short term (≤ 2 years) |

| Next-Gen mRNA / VLP Technologies With Superior Efficacy | +1.20% | North America & EU leading, APAC following | Long term (≥ 4 years) |

| Low-Cost Pichia Pastoris Platforms For LMIC Supply | +0.90% | APAC core, spill-over to MEA and South America | Medium term (2-4 years) |

| AI-Guided Antigen-Design Shortening Development Cycles | +0.80% | North America & EU, with expansion to APAC | Long term (≥ 4 years) |

| Thermostable Single-Dose Formulations Easing Cold-Chain | +0.60% | Global, with highest impact in MEA and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

HPV Vaccination Mandates Expanding Globally

Governments increasingly treat HPV shots as essential public-health infrastructure, widening programs beyond early adolescents to include adult catch-up cohorts. India’s 2024 approval of Cervavac by Serum Institute, an indigenous quadrivalent vaccine, reduced dose prices by more than 65%, enabling bulk procurement across multiple low-resource markets. As middle-income economies align national schedules with World Health Organization (WHO) elimination targets, volume contracts stretch the recombinant vaccines market and reward producers with agile multi-valent lines. Pending patent expirations in China have already catalyzed local entrants, prompting innovators to refresh formulations and explore alternative intranasal or microneedle routes to defend their share. Mandates now embed HPV coverage metrics in broader women's health outcome frameworks, ensuring stable, multi-year demand curves across the recombinant vaccines market.

Pandemic-Preparedness Funding for Rapid Platform Scale-Up

The Coalition for Epidemic Preparedness Innovations (CEPI) has allocated more than USD 3.5 billion to flexible manufacturing projects capable of shipping variant-specific lots within 100 days of sequence disclosure.[1]Coalition for Epidemic Preparedness Innovations, “100-Day Mission Strategy,” cepi.net Public advance-purchase commitments de-risk capacity expansions, keeping surge lines powered even during interpandemic lulls. Standardized single-use fermenters and digitally validated fill-finish skids let producers swap antigens with minimal downtime, enabling the recombinant vaccines market to respond quickly to evolving respiratory or vector-borne threats. Policymakers also channel funds into regional stockpiles that smooth demand cyclicality and strengthen revenue visibility for vertically integrated suppliers. Over-concentration of grants among legacy players, however, could compress innovation diversity unless funding windows broaden for smaller platform developers.

Next-gen mRNA/VLP Technologies With Superior Efficacy

Messenger RNA (mRNA) constructs and virus-like particle (VLP) assemblies consistently deliver stronger neutralizing titers and cross-variant breadth versus conventional protein subunits. Novavax’s Matrix-M adjuvant boosts immunogenicity for recombinant nanoparticle candidates while working at standard 2-8 °C supply chains, permitting deployment in settings where deep-freeze logistics remain impractical. AI-driven codon optimization tools shorten design-build-test loops, letting sponsors pivot candidate libraries within weeks. Capital-intensive lipid-nanoparticle (LNP) inputs and patent-protected ionizable lipid chemistries sustain high barriers to entry, reinforcing the competitive weight of firms that own integrated raw-material pipelines. Nevertheless, the faster variant-update cadence positions mRNA license-holders to capture incremental recombinant vaccines market revenue each respiratory-virus season.

Low-cost Pichia Pastoris Platforms for LMIC Supply

Yeast-based expression achieves end-to-end production costs below USD 1 per dose while meeting WHO prequalification standards. Bharat Biotech’s USD 75 million expansion into large-volume Pichia fermenters showcases the economic viability of microbial systems for mass immunization in price-sensitive settings. Distributed manufacturing hubs closer to demand centers reduce freight bottlenecks and hedge geopolitical supply risks, a decisive advantage after COVID-19 shipping disruptions. While yeast struggles with complex glycosylations, proprietary process tweaks are improving antigen fidelity, broadening the platform’s applicable disease spectrum. Sponsors mastering technology-transfer templates stand to claim substantial recombinant vaccines market share in donor-funded campaigns targeting diseases like cholera or typhoid.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX For GMP Biologics Manufacturing | -1.50% | Global, particularly acute in emerging markets | Long term (≥ 4 years) |

| Vaccine-Hesitancy & Misinformation | -0.80% | Global, with regional variations in intensity | Medium term (2-4 years) |

| Patent Cliffs Driving Low-Price Competition (E.g., HPV In China) | -0.60% | Global, with immediate impact in APAC markets | Short term (≤ 2 years) |

| Raw-Material Bottlenecks For Plasmid DNA & LNPs | -0.40% | Global, concentrated in North America & EU supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for GMP Biologics Manufacturing

Constructing a full-scale recombinant facility requires investments north of USD 500 million and entails stringent environmental-control specifications that exceed small-molecule norms twelve-fold.[2]National Institutes of Health, “Cost Drivers in Biologic Manufacturing,” pmcid.nih.gov Smaller biotechs lean on contract development and manufacturing organizations (CDMOs), yet peak-season demand can overrun available slots, delaying product launches. Continuous-processing skids and digital twins promise to shave batch failure rates, but their integration adds both upfront cost and validation complexity. Capital-intensive footprints tilt the recombinant vaccines market toward cash-rich incumbents, curbing the number of new clinical entrants and constraining price competition over the long term.

Vaccine Hesitancy & Misinformation

Global social-media echo chambers amplify safety myths, depressing adult coverage rates in several high-income markets, and adding volatility to procurement schedules. Regulatory agencies now mandate transparent post-market pharmacovigilance dashboards, which elevate compliance costs and extend time-to-approval for novel constructs. Manufacturers underwrite community-education initiatives and invest in geo-targeted digital campaigns, yet impact remains inconsistent across cultural contexts. Prolonged dips in uptake can translate into expired inventory write-offs, weighing on operating margins throughout the recombinant vaccines market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Type: mRNA Platforms Drive Innovation

mRNA candidates represent the fastest-moving segment, recording an 18.2% CAGR through 2030, while protein subunits remain the volume anchor with 42.5% of 2024 revenue. The recombinant vaccines market, therefore, balances reliability with agility as novel mRNA backbones inherit the manufacturing infrastructure bankrolled during the COVID-19 build-out. VLP programs bridge safety, potency, and moderate cold-chain requirements, making them attractive for developing-country rollouts. DNA plasmid vaccines stay niche due to delivery-device hurdles but gain momentum from nanoparticle and electroporation breakthroughs. Viral-vector programs, although clinically validated, face dose-limiting immunogenicity and complex, scalable purification, narrowing their competitiveness for rapid pandemic response.

Manufacturers increasingly hedge risk by combining technologies: mRNA for rapid variant updates, VLPs for broad antigen presentation, and protein subunits for pediatric schedules. Cross-licensing deals among platform owners have risen by 27% since 2024, enabling shared access to delivery reagents and reducing freedom-to-operate disputes. Agile platform pairing underpins more than a quarter of investigational filings, a trend that should expand recombinant vaccines market penetration into both endemic and emerging indications. Intellectual-property pooling is likely to intensify as regulators promote transfer agreements to accelerate future crisis responses.

By Disease Indication: Dengue Vaccines Emerge

HPV vaccines commanded 47.8% of 2024 receipts, driven by compulsory school-age schedules and adult catch-up extensions. Dengue products, however, are on a 16.5% CAGR trajectory through 2030 in response to Aedes aegypti range expansion and rising urban heat profiles. Hepatitis B continues to post steady procurement via birth-dose mandates, though ceiling prices have tightened under tender competition. Seasonal influenza keeps a lucrative annuity stream, but strain-selection uncertainty produces inventory risk. Meanwhile, shingles uptake climbs across high-income geriatric cohorts as awareness of post-herpetic neuralgia consequences improves.

Therapeutic cancer vaccines, including a personalized mRNA HPV-related trial now in Phase 2, represent a frontier that could re-classify prophylactic norms and add billions to the recombinant vaccines market by the late 2030s. COVID-19 boosters transition from crisis volumes to an endemic seasonal model, yet remain a material revenue pillar due to variant-specific rollouts. RSV vaccines for older adults secured inaugural approvals in 2024, creating a new respiratory franchise that capitalizes on immunosenescence-targeted adjuvants.

By Expression Platform: Plant-Based Systems Disrupt Manufacturing

Yeast retained 65.3% volume share in 2024, but plant-based expression logs the highest momentum, expanding at a 21.0% CAGR as transiently transformed Nicotiana leaves deliver recombinant proteins within seven days post-inoculation.[3]Nature Biotechnology, “Plant-Made Vaccines Gain Momentum,” nature.com Insect-cell baculovirus systems provide conformationally accurate VLPs yet carry elevated cost per gram owing to proprietary media and controlled bioreactors. Bacterial E. coli still excels at simple antigen fragments but lacks complex glycosylation capabilities, confining its scope. Mammalian Chinese-hamster-ovary (CHO) lines guarantee human-like post-translational modifications but face double-digit upstream cost marks and slower scale-out.

Plant-based lots often survive ambient shipping for four weeks after lyophilization, meeting WHO target-product profiles for low-resource campaigns. Sponsors are pairing AI-optimized codon libraries with high-throughput infiltration rigs to elevate yield beyond 5 g per kg of biomass, drawing venture capital into greenhouse biomanufacturing start-ups. The competitive stakes will sharpen as regulatory familiarity grows and dossier review cycles shorten, allowing plant systems to seize incremental recombinant vaccines market share across both pandemic stockpiles and routine pediatric schedules.

By End User: Geriatric Segment Expands

Pediatric formulations continued to dominate, accounting for 55.2% of global takings in 2024 thanks to entrenched national vaccination schedules that bundle hepatitis B, HPV, and combined diphtheria-tetanus-pertussis shots. The geriatric cohort, however, advances at a 12.4% CAGR, propelled by aging demographics in Japan, Germany, and the United States and new data on immunosenescence biomarkers. Adolescent boosters occupy a strategic midpoint that permits manufacturers to extend dose series and consolidate brand loyalty. Adult occupational and travel segments gain renewed policy attention after pandemic-era behavior shifts, further broadening the recombinant vaccines market base.

Age-targeted clinical trial designs now dominate Investigational New Drug (IND) submissions, driving the emergence of high-dose or adjuvanted vaccine SKUs labeled specifically for seniors. Digital reminder platforms integrate with national electronic health records, nudging compliance across retirement communities and long-term-care facilities. Even so, reimbursement fragmentation in multi-payer landscapes complicates forecasting and price positioning for adult programs. The COVID-19 experience strengthened public recognition of adult booster value, setting precedents that pipeline products for RSV, pneumococcal disease, and shingles aim to replicate.

By Route of Administration: Intranasal Delivery Gains Traction

Intramuscular (IM) injection maintained an 81.2% share in 2024, favored by entrenched clinical workflows and straightforward volume scaling. Intranasal sprays, projected to climb at 13.9% CAGR, promise mucosal IgA protection and eliminate needle-phobia barriers. Subcutaneous products remain largely confined to select therapeutic cancer vaccine trials, while intradermal micro-needle patches are in early commercialization stages pending cost-of-goods reductions. Oral delivery struggles with gastric degradation but sees incremental gains via enteric-coated nanoparticle work.

Thermostable intranasal powders are stable at 40 °C for up to 30 days, resulting in lower cold-chain expenditures, which account for nearly 20% of total program budgets in tropical immunization campaigns. However, multi-dose nasal devices introduce extra validation steps around dose consistency, adding roughly USD 0.30 per unit to manufacturing cost—a premium still palatable for pandemic stockpiles but challenging for routine childhood series. Over the forecast horizon, dual-format strategies—IM for infants, intranasal boosters for adolescents or adults—could maximize outreach and optimize supply allocation within the recombinant vaccines market.

Geography Analysis

North America led the recombinant vaccines market with 35.8% of 2024 revenue as the United States leveraged centralized stockpiles and premium Medicare reimbursement to sustain high average selling prices. Canada’s universal health system ensures broad pediatric coverage, while Mexico’s middle-class expansion boosts demand for dengue, rotavirus, and influenza shots. FDA accelerated-approval pathways and a dense CDMO ecosystem allow rapid pivoting to variant-specific mRNA lots, giving regional sponsors a first-mover edge. Investment in domestic lipid-nanoparticle manufacturing further shields the supply chain from geopolitical shocks, reinforcing North American market leadership.

Asia Pacific is the fastest-growing theater at a 9.6% CAGR through 2030, propelled by large-scale technology-transfer agreements, rising per-capita healthcare costs, and endemic disease burdens. China and India anchor regional momentum: China’s local mRNA start-ups file INDs at record pace, while India’s Serum Institute mobilizes multi-antigen campaigns under CEPI procurement contracts. Japan records steep uptake of geriatric shingles and RSV programs, and South Korea cultivates advanced LNP reagent supply chains that feed global mRNA pipelines. Southeast Asian nations prioritize dengue and Japanese encephalitis schedules, often backed by multilateral donor co-financing that secures sustained demand for the recombinant vaccines market.

Europe offers a mature yet innovative-friendly landscape where the centralized European Medicines Agency (EMA) approval process simplifies pan-regional launch. Still, stringent health-technology assessment (HTA) negotiations apply downward pressure on list prices. Germany and the United Kingdom foster cross-sector academic partnerships focused on modular mRNA and VLP workflows, and France’s historical protein-subunit know-how maintains a steady export surplus. Vaccine-hesitancy pockets in parts of Eastern Europe drive demand volatility, compelling suppliers to adopt just-in-time inventory models. EU pandemic-preparedness initiatives under HERA secure long-term offtake agreements, mitigating revenue risks for facilities built within the bloc.

Competitive Landscape

The recombinant vaccines market is moderately concentrated: the top five producers—Merck, GSK, Pfizer, Moderna, and Novavax—collectively command an estimated ~60% of worldwide revenue. Incumbents leverage vertically integrated supply chains, expansive regulatory dossiers, and multi-antigen franchises to defend their share against emerging platform specialists. Merck’s Gardasil HPV line, for example, still dominates premium segments even as India’s cost-efficient Cervavac undercuts per-dose pricing in developing regions. Pfizer capitalizes on its mRNA expertise, repurposing COVID-19 capacity for upcoming RSV and combined flu-COVID programs.

Strategic alliances proliferate: the USD 1.2 billion Novavax–Sanofi co-exclusive licensing deal provides Sanofi with a protein-based foothold in COVID-19 boosters and opens pathways for combination influenza-COVID products. Smaller innovators exploit synthetic biology and cell-free expression to bypass capital-intensive bioreactors, although downstream purification scalability remains a gating factor. Digital health add-ons—such as smartphone-linked smart-syringes—emerge as an ecosystem differentiator, letting firms track real-world safety data while boosting patient engagement.

Patent cliffs loom over first-generation HPV and hepatitis B constructs, intensifying generic pressure and triggering reformulation races. Companies buffer revenue impact by rolling out multi-valent upgrades or exploring alternative intranasal routes. Raw-material bottlenecks in specialty lipids and plasmid DNA spur backward integration as market leaders snap up niche suppliers, raising entry hurdles for start-ups. Competitive dynamics will intensify in white-space targets such as malaria, chikungunya, and personalized neoantigen vaccines, where platform versatility and regulatory agility will determine future recombinant vaccines market leaders.

Recombinant Vaccines Industry Leaders

Merck & Co.

GlaxoSmithKline plc

Pfizer Inc.

Sanofi

Moderna Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Novavax secured FDA approval for Nuvaxovid, the first recombinant protein COVID-19 shot approved for U.S. seniors and high-risk adolescents, triggering a USD 175 million milestone to partner Sanofi.

- February 2025: Novavax transferred U.S. commercial responsibility for Nuvaxovid to Sanofi for the 2025-2026 season, earning a USD 50 million pediatric-trial milestone while retaining over USD 1 billion in liquidity for pipeline assets.

- November 2024: FDA lifted the clinical hold on Novavax’s Phase 3 influenza and COVID-19 combination trials, allowing immediate enrollment resumption.

- September 2024: Novavax launched its 2024-2025 JN.1-specific COVID-19 vaccine nationwide at U.S. pharmacy chains, offering the only protein-based option for individuals above 12 years.

- May 2024: Novavax and Sanofi announced a USD 1.2 billion licensing agreement to co-commercialize COVID-19 vaccines and co-develop influenza-COVID combinations leveraging Matrix-M adjuvant science.

Global Recombinant Vaccines Market Report Scope

| Protein Subunit Vaccines |

| Virus-Like Particle (VLP) Vaccines |

| Viral Vector - Replicating |

| Viral Vector - Non-replicating |

| DNA Plasmid Vaccines |

| mRNA Vaccines |

| Human Papillomavirus (HPV) |

| Hepatitis B |

| Influenza |

| Shingles (Herpes Zoster) |

| Dengue |

| Malaria |

| Respiratory Syncytial Virus (RSV) |

| COVID-19 |

| Oncology (Therapeutic) |

| Yeast (Pichia, Saccharomyces) |

| Bacterial (E. coli) |

| Insect Cell (Baculovirus) |

| Mammalian Cell (CHO, HEK) |

| Plant-based |

| Cell-Free Synthetic |

| Pediatric |

| Adolescent & Adult |

| Geriatric |

| Intramuscular Injection |

| Subcutaneous Injection |

| Intradermal Injection |

| Oral |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology Type | Protein Subunit Vaccines | |

| Virus-Like Particle (VLP) Vaccines | ||

| Viral Vector - Replicating | ||

| Viral Vector - Non-replicating | ||

| DNA Plasmid Vaccines | ||

| mRNA Vaccines | ||

| By Disease Indication | Human Papillomavirus (HPV) | |

| Hepatitis B | ||

| Influenza | ||

| Shingles (Herpes Zoster) | ||

| Dengue | ||

| Malaria | ||

| Respiratory Syncytial Virus (RSV) | ||

| COVID-19 | ||

| Oncology (Therapeutic) | ||

| By Expression Platform | Yeast (Pichia, Saccharomyces) | |

| Bacterial (E. coli) | ||

| Insect Cell (Baculovirus) | ||

| Mammalian Cell (CHO, HEK) | ||

| Plant-based | ||

| Cell-Free Synthetic | ||

| By End User | Pediatric | |

| Adolescent & Adult | ||

| Geriatric | ||

| By Route of Administration | Intramuscular Injection | |

| Subcutaneous Injection | ||

| Intradermal Injection | ||

| Oral | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current recombinant vaccines market size and projected growth?

The recombinant vaccines market size is USD 18.3 billion in 2025 and is forecast to reach USD 30.6 billion by 2030, advancing at an 11.1% CAGR.

Which technology category is expanding fastest?

MRNA platforms are the fastest-growing, forecast to post an 18.2% CAGR as they leverage existing pandemic-era infrastructure for rapid antigen swapping.

Why are dengue vaccines attracting heightened investment?

Climate-driven mosquito range expansion and urban population density lift infection risk, propelling dengue vaccines at a 16.5% CAGR and expanding the recombinant vaccines market footprint.

How important is Asia Pacific to future sales?

Asia Pacific is projected to grow at 9.6% CAGR, underpinned by large-scale technology transfer, local manufacturing incentives, and high endemic disease burdens that increase vaccine volumes.

What are the primary obstacles manufacturers face?

High GMP plant capital costs and persistent vaccine-hesitancy dynamics remain the key restraints, potentially trimming growth by 1.5% and 0.8% of CAGR respectively.

Which companies currently lead the recombinant vaccines market?

Merck, GSK, Pfizer, Moderna, and Novavax collectively hold approximately 60% of global revenue, supported by extensive manufacturing networks and diversified technology portfolios.

Page last updated on: