Ruminant Vaccines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

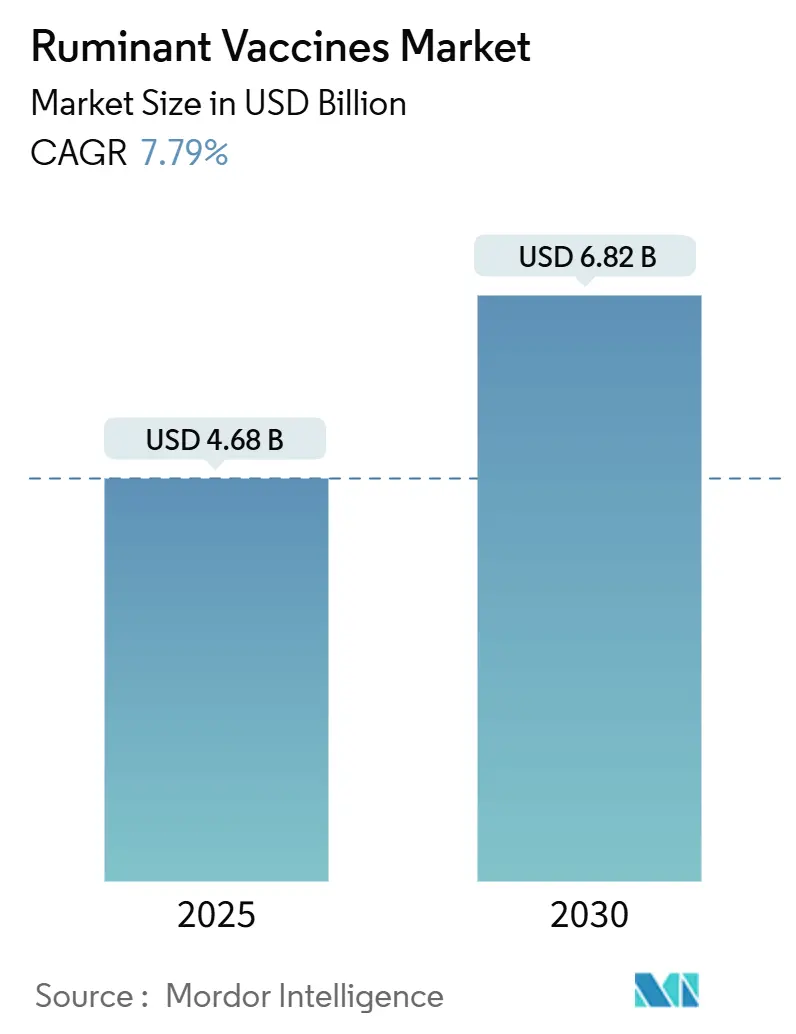

| Market Size (2025) | USD 4.68 Billion |

| Market Size (2030) | USD 6.82 Billion |

| Growth Rate (2025 - 2030) | 7.79% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ruminant Vaccines Market Analysis by Mordor Intelligence

The ruminant vaccine market size stood at USD 4.68 billion in 2025 and is forecast to reach USD 6.82 billion by 2030, advancing at a 7.79% CAGR. This strong trajectory reflects sustained government spending on foot-and-mouth disease (FMD) preparedness, rapid adoption of mRNA vaccine platforms, and expanding small-holder dairy intensification programs in emerging Asia-Pacific economies. Strategic vaccine banks such as Canada’s USD 57.5 million reserve and the Global Foot and Mouth Disease Research Alliance’s five-year mandate illustrate the scale of public-sector commitment to preventive immunization.[1]Animal Health Canada, “Foot-and-Mouth Disease (FMD) – Forward Plans,” animalhealthcanada.ca Private-sector innovation is equally pivotal, with Zoetis alone reporting USD 2.898 billion in 2024 livestock revenue, while venture-backed startups accelerate nanoparticle and recombinant delivery systems. Vaccine distribution is improving through digitized cold-chain networks in tropical regions, and regulatory agencies are drafting specific quality guidelines for veterinary mRNA products, laying the groundwork for faster approvals.

Key Report Takeaways

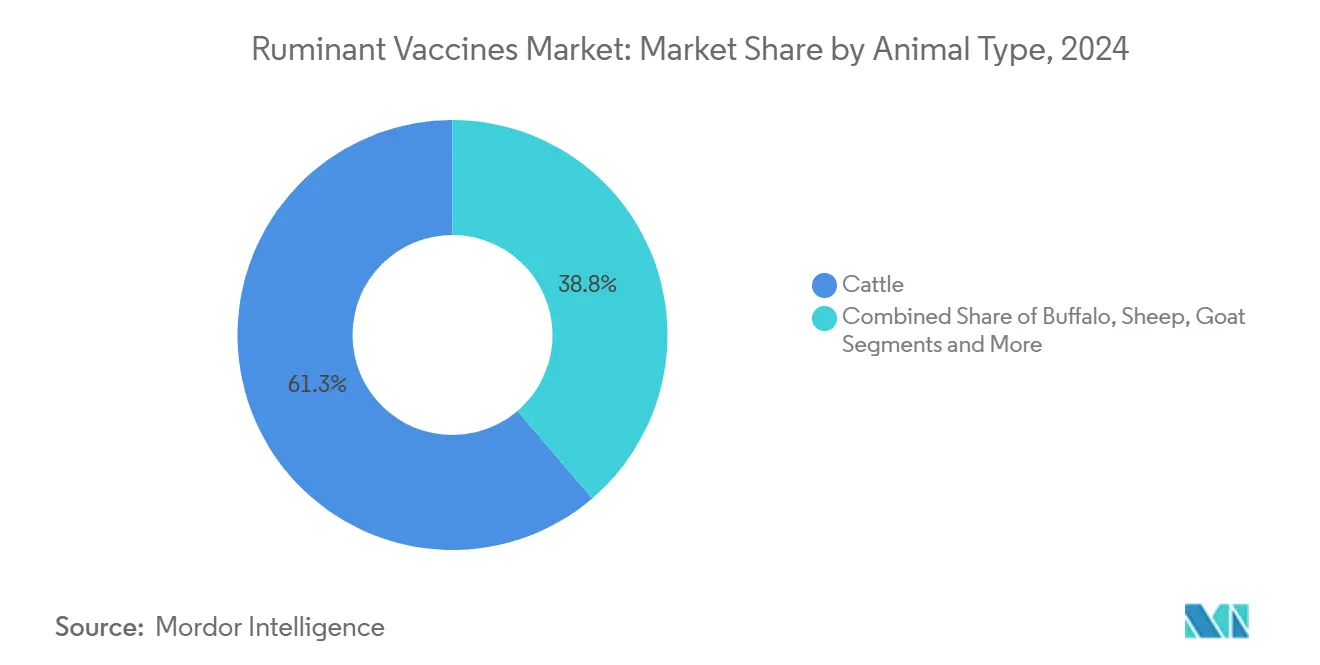

- By animal type, cattle vaccines led the ruminant vaccine market with 61.25% of the share in 2024; goat and sheep products are projected to grow at a 10.58% CAGR to 2030.

- By vaccine type, inactivated platforms commanded 47.53% of the ruminant vaccine market size in 2024, while DNA formulations are set to post the highest 11.78% CAGR through 2030.

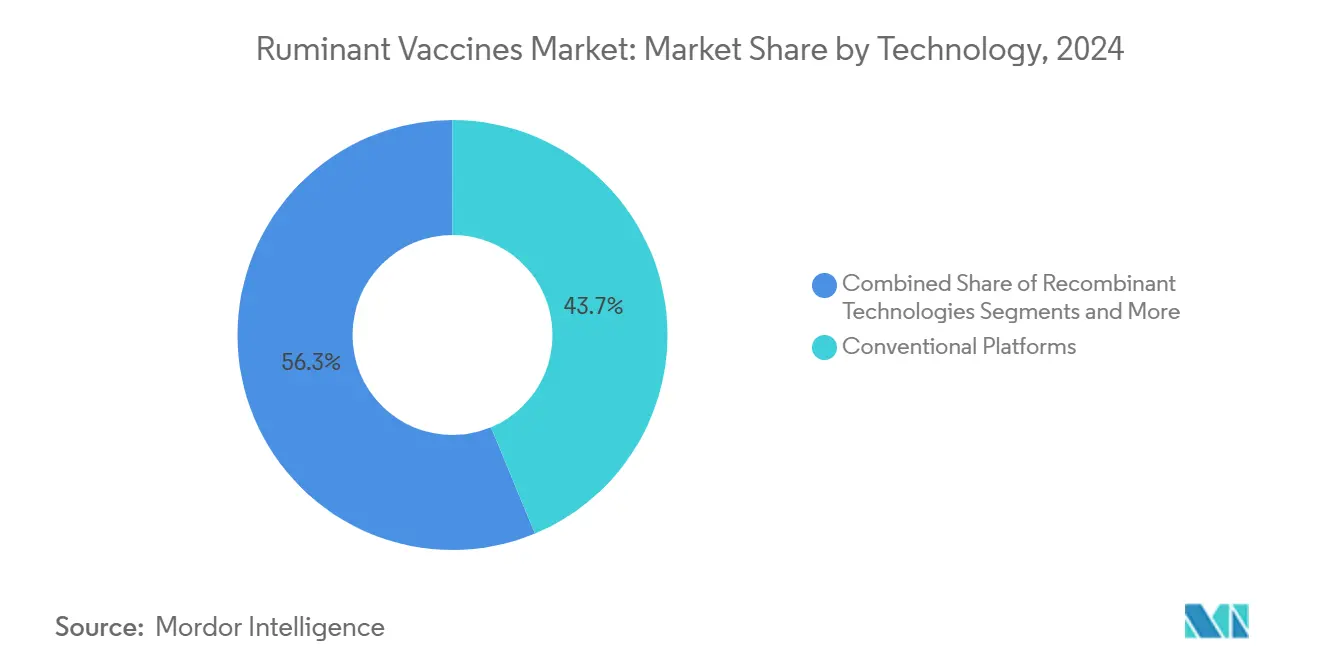

- By technology, conventional platforms generated 43.73% of 2024 revenue; recombinant vectors represent the fastest-growing track at an 11.84% CAGR.

- By route of administration, parenteral delivery captured 71.36% market share in 2024; intranasal products will expand at a 10.42% CAGR between 2025-2030.

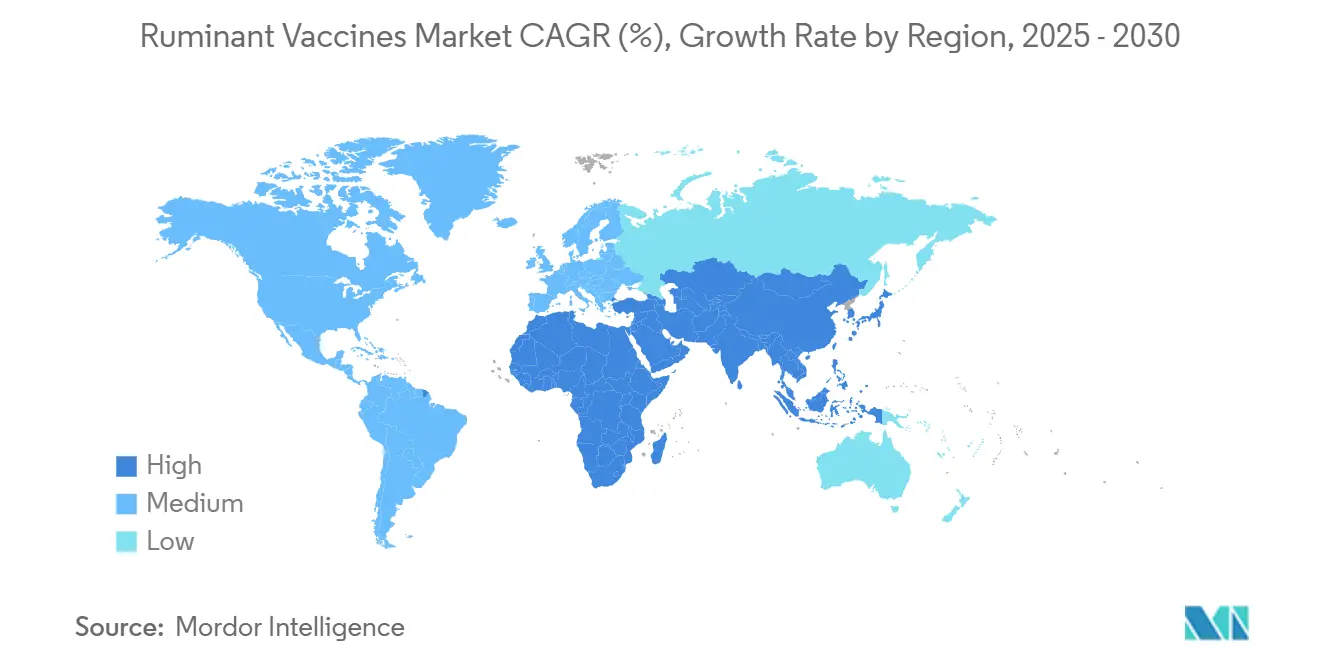

- By geography, Asia-Pacific accounted for 31.84% of 2024 revenue, while the Middle East and Africa are set to post the highest 9.62% CAGR.

Global Ruminant Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying FMD eradication programs | +1.8% | Global; focus on Asia-Pacific & MEA | Medium term (2-4 years) |

| Rising small-holder dairy intensification | +1.5% | Emerging Asia; spill-over to South America | Long term (≥ 4 years) |

| Demand for differentiated milk & meat labels | +1.2% | North America & EU; spreading to APAC | Medium term (2-4 years) |

| EU “Green Deal” push for preventive health | +0.9% | Europe; shaping global standards | Long term (≥ 4 years) |

| Emergence of mRNA vector cattle shots | +1.4% | North America & EU lead; global rollout | Short term (≤ 2 years) |

| Digitized cold-chain networks in Africa | +0.8% | MEA; potential in other tropical regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying FMD Eradication Programs

Government-backed FMD elimination strategies now mandate herd-wide immunization, fund strategic vaccine stockpiles, and integrate outbreak simulation exercises. Canada’s USD 57.5 million national vaccine bank exemplifies proactive procurement, while USDA’s Global Foot and Mouth Disease Research Alliance accelerates next-generation antigen discovery. Recent African field studies show vaccinated cattle experience a 69.3% lower infection risk, reinforcing the economic logic of mass immunization.[2]Wubshet A.K. et al., “FMD Vaccine Efficacy in Africa,” frontiersin.org Mandatory certification is also tightening export requirements, motivating producers to maintain up-to-date vaccination records for market access.

Rising Small-Holder Dairy Intensification in Emerging Asia

Small-scale dairy farms are shifting from subsistence to commercial models, boosting demand for preventive health solutions. Digital herd-management tools in Indonesia correlate with higher vaccination rates, while Indian cross-breeding initiatives improve milk yields by more than 110%, heightening awareness of disease prevention. Cooperative membership is critical; farmers in organized groups secure easier financing for vaccines and demonstrate stronger compliance.

Growing Demand for Differentiated Milk & Meat Quality Labels

Retail and export channels now reward vaccinated herds with 10-15% price premiums, linking animal health practices to product quality certifications.[3]European Commission, “EU Delegated Regulation 2024/1159,” eur-lex.europa.eu Major grocery chains require suppliers to present full vaccination logs, and organic labels increasingly integrate preventive health metrics. Traceability platforms connect immunization data with on-pack QR codes, giving consumers transparency into herd management.

Emergence of mRNA Vector Platforms for Multivalent Cattle Shots

Adaptation of mRNA technology cuts development cycles from 12-18 months to roughly 3 months. Experimental bovine viral diarrhea mRNA candidates achieved antibody titers comparable to licensed inactivated shots, validating the platform’s promise. University-led consortia are building dedicated mRNA pilot plants, and regulatory guidance from the European Medicines Agency is streamlining dossier requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sub-optimal strain matching in trans-boundary diseases | -1.1% | Global; acute in Asia-Pacific & MEA | Medium term (2-4 years) |

| Chronic under-reporting of small-ruminant morbidity | -0.8% | MEA & South America | Long term (≥ 4 years) |

| Anti-vaccination sentiment among pastoralists | -0.6% | MEA & parts of Asia-Pacific | Medium term (2-4 years) |

| Limited freeze-drying capacity for thermostable doses | -0.9% | Global; critical in tropical climates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sub-Optimal Strain Matching in Trans-Boundary Diseases

Rapid viral evolution often outpaces surveillance, undermining vaccine efficacy. Immunogenicity trials in the Middle East confirm that tetravalent FMD formulations offer variable protection when field strains drift, necessitating more frequent antigen updates. The financial burden rises when boosters become necessary, eroding producer confidence in vaccination programs.

Anti-Vaccination Sentiment Among Pastoral Communities

Nomadic herders in Kenya and Ethiopia voice skepticism based on historical vaccine failures. Gender dynamics complicate uptake, as male household heads control decisions despite women handling daily animal care.[4]Irene N. Mutambo, “Building Resilience to Rift Valley Fever in Kenya,” plos.org Limited veterinary extension services and insufficient multilingual outreach further depress coverage, creating disease reservoirs that threaten broader eradication goals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Cattle Vaccines Anchor Global Demand

The cattle segment generated 61.25% of the ruminant vaccine market size in 2024, driven by the high economic stakes associated with bovine respiratory and reproductive diseases. Intensive feedlot and dairy operations depend on wide vaccine portfolios that cover FMD, bovine viral diarrhea, and clostridial pathogens. Producers value the predictable returns on preventive spending, reinforcing steady uptake across developed regions. Conversely, water-buffalo vaccines serve niche dairy pockets in South and Southeast Asia but are gaining ground as genetic improvement programs lift yield targets. Goat and sheep vaccines remain the fastest climbers at a 10.58% CAGR, primarily because combined PPR-sheep pox formulations lower administration costs by as much as 40% while maintaining efficacy. Demand is underpinned by food-security imperatives in rural economies where small ruminants provide crucial household income.

Growth in goat and sheep immunization is reshaping the competitive landscape, attracting venture capital toward thermostable multivalent candidates. Camelid vaccines sit in a nascent phase yet command attention in arid regions that view these animals as vital protein and transport resources. Regulatory agencies are harmonizing dossier requirements across species, encouraging platform technologies that can be rapidly adapted from cattle to small ruminants. These dynamics sustain robust volume expansion even as cattle products retain the largest absolute share of the ruminant vaccine market.

By Vaccine Type: Inactivated Platforms Retain Lead While DNA Breaks Out

Inactivated formulations captured 47.53% of the ruminant vaccine market share in 2024, benefiting from mature manufacturing ecosystems and well-documented safety profiles. Large public-tender programs default to these products because cold-chain infrastructure is already tuned to their storage parameters. Live-attenuated shots remain essential where rapid, single-dose immunity is mandatory, especially during outbreaks. Toxoid vaccines maintain relevance for clostridial coverage in intensive grazing systems. Recombinant vector products combine safety with vigor but currently face higher production costs.

DNA vaccines are the breakout category, forecast to grow at an 11.78% CAGR through 2030, as lipid-nanoparticle delivery systems overcome historical potency hurdles. The ruminant vaccine market size for DNA solutions is small today, yet collaborations such as Ceva-Touchlight highlight industry confidence in enzymatic plasmid manufacturing. mRNA candidates remain early-stage but promise unrivaled speed. Subunit and virus-like particle platforms round out a diverse pipeline, fueling competition for next-generation differentiation.

By Technology: Conventional Platforms Hold Tradition; Recombinant Vectors Sprint Ahead

Conventional Platforms accounted for 43.73% of 2024 revenue, prized for robust, long-lasting immunity. Producers favor single-hit protection that minimizes labor, particularly in extensive grazing setups. Conventional inactivated technology follows, leveraging decades of production refinement. Toxoid approaches fill bacterial niches such as blackleg prevention.

Recombinant vectors now form the fastest-growing technology track at an 11.84% CAGR. Advances in bovine adenoviral vectors have unlocked efficient gene loading and expression, allowing multi-pathogen payloads without live pathogen risks. Virus-like particle and nanoparticle platforms increase antigen density and thermostability, directly addressing distribution constraints in tropical regions. Manufacturers are expanding capacity; Ceva’s new 7,000 m² plant underscores long-term bets on platform diversification. These shifts push the ruminant vaccine market toward more versatile, rapid-response technologies.

By Route of Administration: Parenteral Dominance Faces Intranasal Momentum

Parenteral routes generated 71.36% of 2024 revenue, reflecting entrenched veterinary practice and dose accuracy. Feedlot managers trust intramuscular and subcutaneous injections for systemic immunity in high-value herds. Needle-free jet injectors are gaining visibility but remain grouped within parenteral delivery.

Intranasal vaccination is the fastest mover with a 10.42% CAGR, celebrated for mucosal immunity that curbs maternal antibody interference in neonates. Field trials in pre-weaned calves show strong priming potential, and the ease of administration suits large herd dynamics. Oral baits support wildlife control programs, while transdermal microneedle patches are targeting small-ruminant producers seeking animal-welfare gains. Each modality enriches the ruminant vaccine market portfolio, widening choice based on on-farm logistics.

Geography Analysis

Asia-Pacific led the ruminant vaccine market in 2024 with a 31.84% revenue share, buoyed by expanding dairy herds in China and India, supportive government immunization subsidies, and rising middle-class protein demand. Digitized cold-chain pilots in Indonesia and Vietnam reduce wastage and improve last-mile delivery, while Australia’s advanced veterinary networks promote premium prophylaxis purchasing. Regional progress is accelerated by local biotech partnerships that shorten supply chains and adapt formulations to indigenous strains.

North America remains a mature yet innovative arena. The United States channels significant R&D funding into mRNA and recombinant technologies, supported by clear FDA guidance that favors agile developers. Canada’s FMD vaccine bank demonstrates federal readiness, while Mexico’s integrated livestock trade network benefits from harmonized vaccine standards under USMCA frameworks. Consistent demand arises from stringent traceability laws and retailer procurement codes mandating full vaccination documentation.

Europe wields outsized regulatory influence through the Green Deal, which rewards preventive health practices that reduce antibiotic dependence. Germany, France, and the United Kingdom sustain high per-animal spending, encouraging adoption of advanced adjuvant systems. The European Medicines Agency’s draft mRNA guidance illustrates policy commitment to next-generation immunization. Eastern European members deploy EU structural funds for cold-chain upgrades, boosting coverage in former under-served zones.

Middle East & Africa posts the fastest 9.62% CAGR, propelled by international development grants and growing veterinary education capacity. Digitized cold-chain startups tackle thermal challenges, and regional vaccine-fill facilities reduce import dependence. South America capitalizes on large commercial cattle operations that require full FMD vaccination for export eligibility to Asian markets. Cross-border harmonization projects among MERCOSUR states aim to streamline vaccine licensing and distribution, enhancing market fluidity.

Competitive Landscape

The ruminant vaccine market is moderately concentrated. Zoetis leverages scale in both R&D and distribution, while Merck Animal Health’s USD 1.3 billion acquisition of Elanco’s aqua business signals portfolio diversification into broader biologicals. Ceva accelerates nucleic-acid manufacturing through its partnership with Touchlight, revealing a strategic pivot toward genetic platforms.

Disruptors include academic spin-offs, commercializing nanoparticle adjuvants, and biotech firms engineering thermostable formulations suited to tropical logistics. Investors target white-space opportunities where combined vaccines reduce administration labor in mixed-species herds. Regulatory programs like the FDA’s Veterinary Innovation Agenda entice agile developers by offering consultative pathways and conditional approvals. Capacity expansions, exemplified by MSD’s USD 220 million Austrian plant, reflect confidence in sustained demand growth.

Digital integration is emerging as a competitive differentiator. Platform providers bundle vaccine supply contracts with herd-management software and tele-veterinary services, locking in customer loyalty through data analytics. Overall, incumbents defend share through breadth and capital, whereas newcomers exploit speed and specialization, together ensuring continuous innovation in the ruminant vaccine market.

Ruminant Vaccines Industry Leaders

Zoetis

Merck Co & Inc

Boehringer Ingelheim

Ceva Santé Animale

Elanco Animal Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: L-PRES set a target to manufacture 850 million vaccine doses annually to meet surging livestock demand.

- January 2025: Ceva partnered with Touchlight to co-develop enzymatic dbDNA vaccines under upfront-and-royalty terms.

- January 2025: The European Medicines Agency issued draft quality guidelines for veterinary mRNA products, clarifying dossier expectations.

Global Ruminant Vaccines Market Report Scope

| Cattle |

| Buffalo |

| Sheep |

| Goat |

| Camelids (Llama, Alpaca, etc.) |

| Inactivated (Killed) |

| Live Attenuated |

| Toxoid |

| Recombinant Vector |

| Subunit |

| DNA |

| mRNA |

| Conventional Platforms |

| Recombinant Technologies |

| Genetic Vaccines |

| Other Emerging Platforms |

| Parenteral | Intramuscular |

| Subcutaneous | |

| Intranasal | |

| Oral | |

| Transdermal (Microneedle/Jet) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Animal Type | Cattle | |

| Buffalo | ||

| Sheep | ||

| Goat | ||

| Camelids (Llama, Alpaca, etc.) | ||

| By Vaccine Type | Inactivated (Killed) | |

| Live Attenuated | ||

| Toxoid | ||

| Recombinant Vector | ||

| Subunit | ||

| DNA | ||

| mRNA | ||

| By Technology | Conventional Platforms | |

| Recombinant Technologies | ||

| Genetic Vaccines | ||

| Other Emerging Platforms | ||

| By Route of Administration | Parenteral | Intramuscular |

| Subcutaneous | ||

| Intranasal | ||

| Oral | ||

| Transdermal (Microneedle/Jet) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the ruminant vaccine market in 2025?

It reached USD 4.68 billion in 2025 and is projected to climb to USD 6.82 billion by 2030 at a 7.79% CAGR.

Which animal segment brings in most vaccine sales?

Cattle vaccines dominate with 61.25% of 2024 revenue, reflecting their central role in global protein production.

What technology is growing fastest?

Recombinant vector platforms show the highest growth, advancing at an 11.84% CAGR through 2030.

Which administration route is gaining traction?

Intranasal delivery is the fastest-expanding route, expected to grow at a 10.42% CAGR between 2025-2030.

Which region is projected to grow quickest by 2030?

Middle East & Africa leads regional expansion with a 9.62% CAGR, supported by development-funded veterinary infrastructure.

How are regulators treating mRNA livestock vaccines?

The European Medicines Agency released draft guidance in 2025 that clarifies quality requirements and accelerates the approval pathway for veterinary mRNA products.

Page last updated on: