Antibody Discovery Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

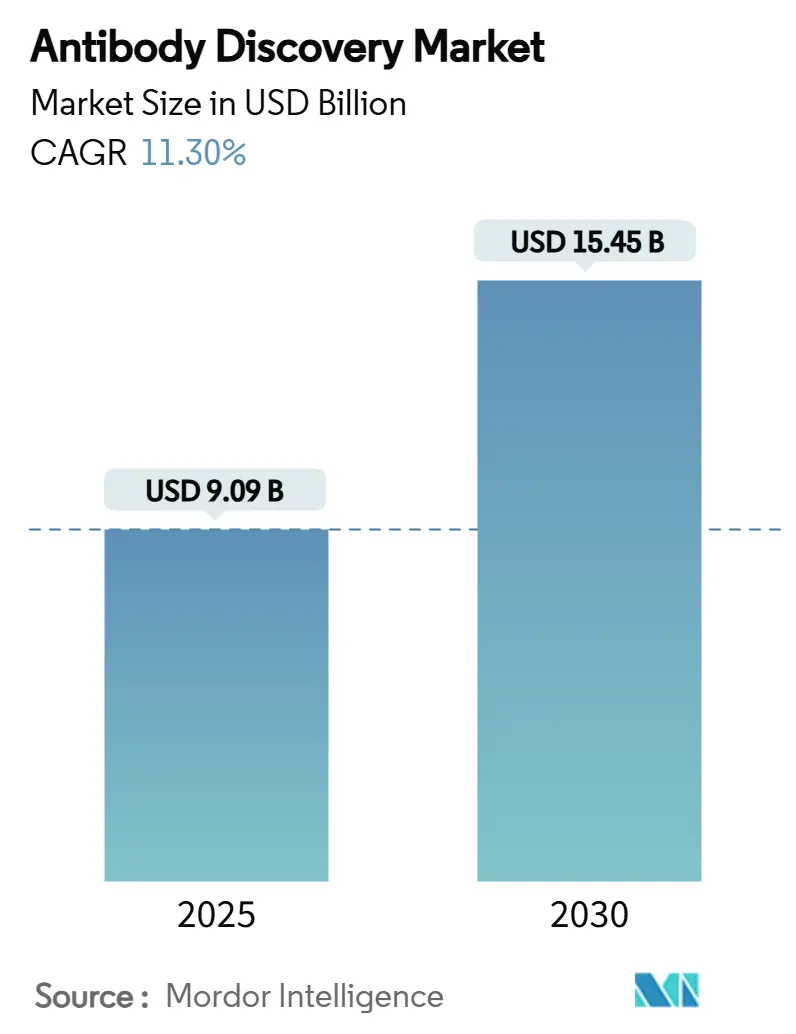

| Market Size (2025) | USD 9.09 Billion |

| Market Size (2030) | USD 15.45 Billion |

| Growth Rate (2025 - 2030) | 11.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antibody Discovery Market Analysis by Mordor Intelligence

The antibody discovery market size stands at USD 9.09 billion in 2025 and is projected to reach USD 15.45 billion by 2030, translating into an 11.3% CAGR across the forecast period. Uptake is propelled by a decisive shift toward precision biologics, with pharmaceutical pipelines reallocating resources from small-molecule leads to antibody programs that address challenging or previously undruggable targets. Artificial-intelligence design suites and high-throughput screening technologies are compressing time-to-hit identification, cutting early-stage timelines from months to weeks, and lowering attrition in downstream developability testing. Multiple blockbuster monoclonal antibodies nearing patent expiry create room for follow-on assets, while biosimilar pressure forces originators to double down on differentiated next-generation constructs. In parallel, regulatory agencies have issued guidance for bispecific and multispecific formats, providing clearer development pathways that de-risk investments in innovative scaffolds.

Key Report Takeaways

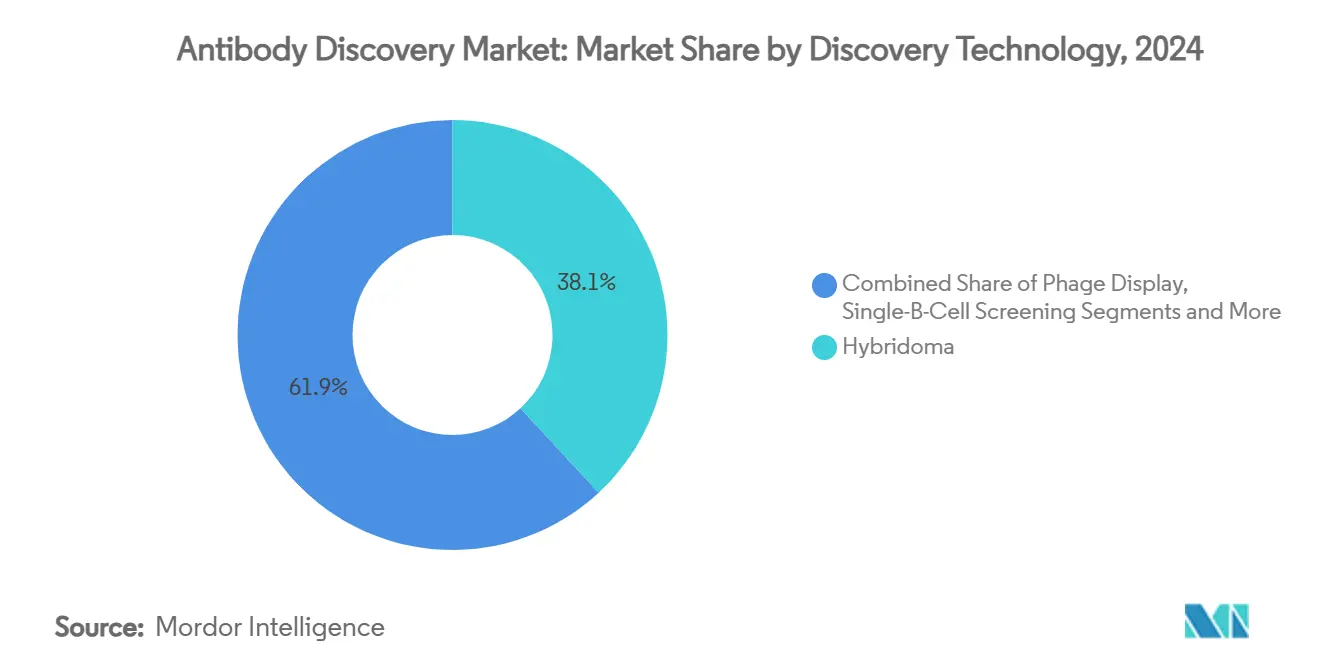

- By discovery technology, hybridoma technology captured 38.1% of antibody discovery market share in 2024, whereas AI/ML-enabled platforms are forecast to expand at a 22.4% CAGR between 2025 and 2030.

- By service model, in-house discovery held 52.6% of the antibody discovery market share in 2024, while contract and outsourced models exhibit the highest projected CAGR at 17.3% through 2030.

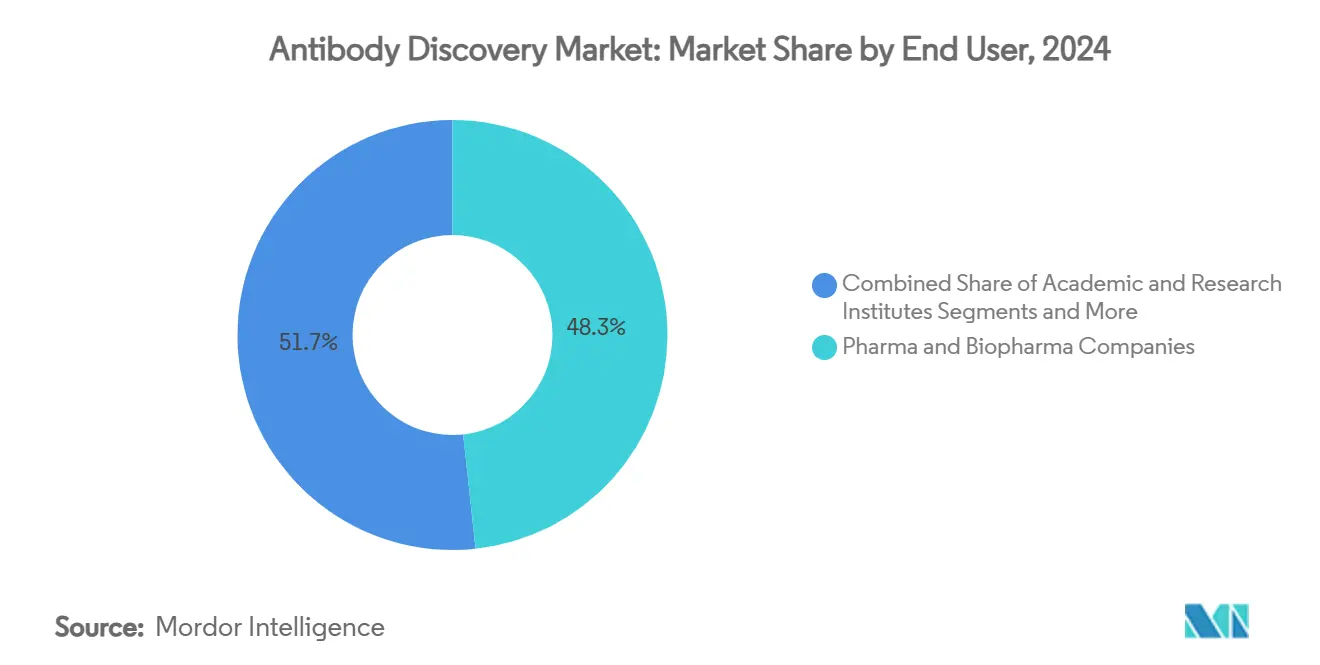

- By end user, pharmaceutical and biopharmaceutical companies accounted for 48.3% of the antibody discovery market size in 2024; biotechnology start-ups are advancing at a 14.8% CAGR to 2030.

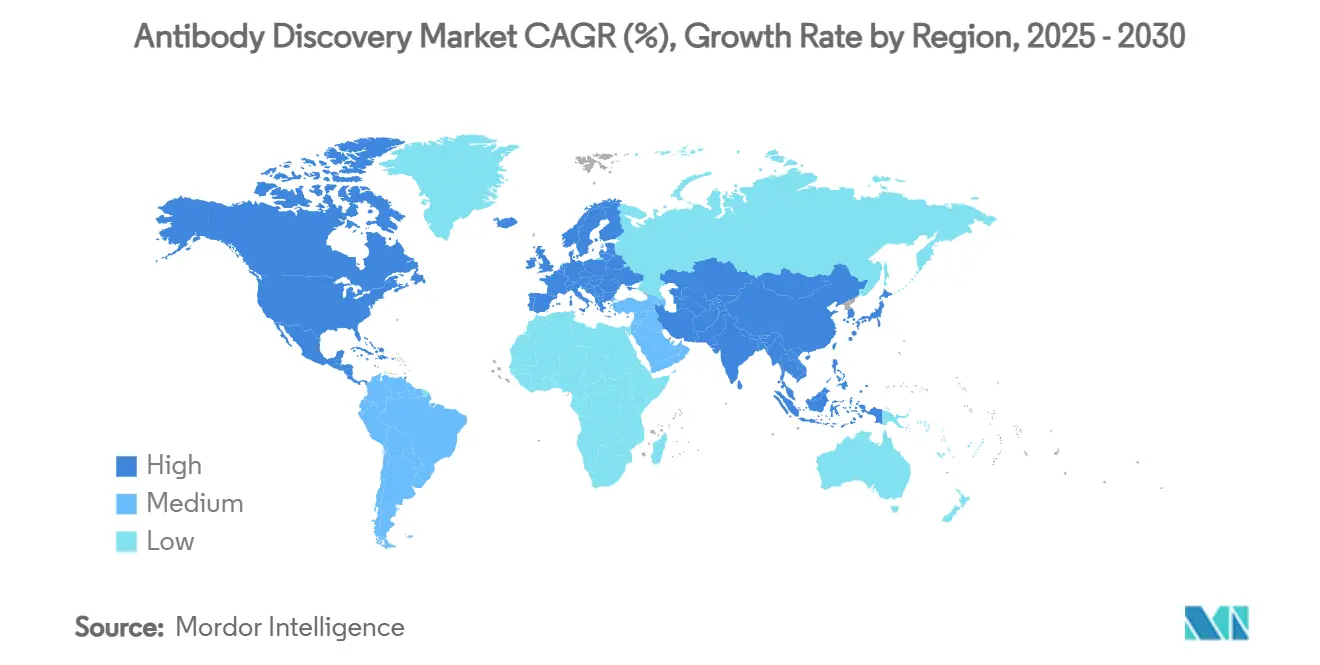

- Geographically, North America commanded 41.5% of the antibody discovery market size in 2024, although Asia Pacific is projected to log the fastest expansion at 13.5% CAGR over the same horizon.

Global Antibody Discovery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand For Monoclonal Antibody (MAb) Therapeutics | +3.20% | Global, with North America & EU leading adoption | Medium term (2-4 years) |

| Technological Advances In Phage Display & Single-B-Cell Screening | +2.80% | Global, concentrated in biotech hubs | Short term (≤ 2 years) |

| Expanding Pharma/Biotech R&D Budgets & Outsourcing | +2.10% | APAC core, spill-over to North America & EU | Medium term (2-4 years) |

| Growing Chronic & Oncologic Disease Burden Globally | +1.90% | Global, with aging populations in developed markets | Long term (≥ 4 years) |

| AI/ML-Driven In-Silico Discovery Shortening Timelines | +1.80% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Blockbuster MAb Patent Cliffs Unlocking "Follow-On" Discovery | +1.40% | Global, with regulatory variations by region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Monoclonal Antibody Therapeutics

More than 200 marketed antibody products generated sustained clinical validation that now steers discovery priorities toward biologics addressing oncology, autoimmune, infectious, and neurologic conditions. Four of the 10 highest-selling drugs in 2024 were monoclonal antibodies, reinforcing the commercial case for continued pipeline expansion. Late-stage pipelines demonstrate diversification, with 45% of candidates aimed at cancer and 27% targeting immune-mediated disorders. Patent expirations on earlier wave blockbuster antibodies further stimulate “follow-on” programs that leverage known mechanisms while integrating improved specificity or half-life. Combined, these factors create a durable influx of projects that sustains the antibody discovery market well beyond the forecast horizon.

Technological Advances in Phage Display & Single-B-Cell Screening

Iterative enrichment protocols and computationally guided selection strategies now deliver antibodies against membrane proteins and conformational epitopes that traditionally resisted hybridoma approaches.[1]Muhammad A. Khan et al., “Phage Display Derived Monoclonal Antibodies: From Bench to Bedside,” PubMed Central, ncbi.nlm.nih.gov Microfluidic single-B-cell screening interrogates millions of clonotypes while preserving natural heavy–light pairing, directly improving downstream developability.[2]A. C. Gray, “Animal-Derived Antibody Generation Faces Strict Reform,” Nature Methods, nature.com Hybrid workflows integrating mammalian display with phage display capture the volumetric scalability of bacterial systems alongside the folding fidelity of eukaryotic hosts, thereby raising hit quality and reducing back-end engineering requirements. These advances increase discovery success rates, democratize access to high-value targets, and lower the cost per validated lead, all of which accelerate revenue growth for the antibody discovery market.

Expanding Pharma/Biotech R&D Budgets & Outsourcing

Raised biologics allocation inside big-pharma R&D portfolios intersects with a broad willingness to outsource specialized upstream steps to contract development and manufacturing organizations (CDMOs). In 2024, 84.6% of biomanufacturers reported outsourcing analytical testing—an indicator of comfortable reliance on external partners for technically demanding tasks. Asia Pacific CDMO hubs combine cost advantages with upgraded GMP facilities, making the region attractive for discovery as well as development. For small and mid-sized biotechnology firms, outsourced discovery eliminates the need for USD 10 million-plus capital outlays on automated screening or next-gen sequencing, reallocating scarce funds toward clinical proof-of-concept instead.

AI/ML-Driven In-Silico Discovery Shortening Timelines

Generative models trained on millions of antibody–antigen pairs now achieve 16% binding rates in de-novo design campaigns, with at least one confirmed hit for half of the targets tested.[3]Chai Discovery, “Zero-Shot Antibody Design in a 24-Well Plate,” bioRxiv, biorxiv.org Structure-conditioned sequence generation coupled with atomic-level refinement enables simultaneous optimization of affinity, stability, and manufacturability, replacing sequential test cycles with a single integrated design step. Closed-loop experimental validation further accelerates learning, compounding improvements in each successive iteration. These gains cut early-stage discovery from 12 months to under six weeks, markedly improving internal rate of return for new programs and cementing AI as a central pillar of the antibody discovery market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost & Technical Complexity Of Discovery Platforms | -2.10% | Global, particularly affecting smaller biotechs | Short term (≤ 2 years) |

| Stringent Multi-Jurisdictional Regulatory Validation For Novel Formats | -1.70% | Global, with varying regional requirements | Medium term (2-4 years) |

| Scarcity Of High-Quality Antigens For Next-Gen Targets | -1.40% | Global, concentrated in advanced research centers | Medium term (2-4 years) |

| Escalating IP Litigation Over Antibody Sequence Claims | -1.20% | North America & EU, with spillover to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost & Technical Complexity of Discovery Platforms

Cutting-edge AI engines, high-throughput cytometers and long-read sequencing decks routinely lift greenfield budgets past USD 10 million, rendering full in-house buildouts unattainable for many venture-financed companies. Skilled labor shortages in computational biology and protein engineering add persistent operational expenses that frequently exceed initial hardware outlays. Technology refresh cycles average 24 months, forcing continual reinvestment to maintain competitive benchmarks. Collectively, these economics push early-stage innovators toward fee-for-service or partnership models, which in turn restrain absolute revenue growth for pure in-house solutions within the antibody discovery market.

Stringent Multi-Jurisdictional Regulatory Validation for Novel Formats

Guidance documents for bispecific antibodies issued by the FDA lay out bespoke quality, non-clinical, and clinical expectations that differ from traditional monoclonals, adding extra studies and time to development programs. Europe imposes separate requirements for biosimilar comparability, while its push toward animal-free research mandates additional in-vitro justification for transgenic platforms. Intellectual-property uncertainties, highlighted by rising disclosure thresholds for sequence-based claims, further cloud the risk–reward calculus for nontraditional constructs. These hurdles collectively temper uptake of advanced formats, limiting short-term revenue capture despite evident therapeutic promise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Discovery Technology: Computational Acceleration Redraws the Landscape

Hybridoma systems held 38.1% of the antibody discovery market share in 2024, supported by decades of regulatory familiarity and an installed base that handles routine immunogenic targets efficiently. However, hybridoma campaigns struggle with membrane proteins and conformational epitopes that are becoming more commercially relevant, prompting users to supplement with display-based or computational methods. In value terms, hybridoma workflows accounted for the most considerable absolute portion of the antibody discovery market size in 2024 but are projected to cede ground to faster alternatives throughout the forecast horizon.

AI/ML-enabled in-silico platforms are set to log a 22.4% CAGR through 2030, the fastest clip among all technologies. Performance proof points, such as 16% de-novo binding success across 52 targets, underline the ability to transcend empirical screening limits. Phage display remains indispensable for library diversity and rapid affinity maturation, while microfluidic single-B-cell platforms bring high-value pairing information that reduces downstream re-engineering. Industry feedback indicates that future competitive advantage will stem less from owning a single modality and more from integrating computational design, display selection, and high-resolution analytics into one continuous pipeline, positioning platform integration as a key focus for new capital deployment within the antibody discovery market.

By Service Model: Outsourcing Momentum Builds on Complexity Economics

In-house discovery commanded 52.6% of the antibody discovery market in 2024, reflecting large pharmaceutical groups’ preference for end-to-end control and intellectual-property consolidation. These organizations integrate discovery with process development and clinical translation, enabling tight feedback loops that can rescue borderline assets through rapid engineering cycles. However, the steep cost of platform upkeep and the need for specialized staff limit expansion to companies with deep capital pools.

Contract and outsourced discovery services are forecast to post a 17.3% CAGR between 2025 and 2030 as complexity economics favor external expertise. CDMOs now provide target identification, AI-assisted design, high-throughput screening, and developability analytics in modular or turnkey formats. Asia Pacific vendors lead on cost-adjusted throughput, while North American specialists differentiate on AI toolkits and regulatory track records. Mixed models—where discovery seeds are generated externally and then transferred in-house for optimization—are gaining traction, especially for bispecific programs that require both advanced engineering and tight clinical alignment. This evolution keeps outsourcing below majority volume but systematically raises its revenue contribution inside the antibody discovery market.

By End User: Start-Ups Fuel Innovation Velocity

Pharmaceutical and biopharmaceutical companies accounted for 48.3% of the antibody discovery market share in 2024, leveraging established screening platforms, GMP infrastructures, and global regulatory networks. Within these firms, strategic focus is shifting toward bispecifics, antibody–drug conjugates, and other complex modalities that demand sophisticated early-stage analytics. The ability to press assets through late-stage trials and global launches remains a unique advantage that anchors their spending power.

Biotechnology start-ups are projected to grow at a 14.8% CAGR, the fastest among all end-user groups. Venture investors increasingly back AI-native platforms that promise lower capital intensity and shorter discovery cycles, enabling lean teams to generate clinically relevant leads without heavy wet-lab footprints. Academic and research institutes continue to generate target biology and early antibody prototypes, often out-licensing to commercial entities for clinical advancement. As a result, collaboration models that blend academic novelty, start-up agility, and pharmaceutical scale are likely to dominate new program launches, ensuring diversified demand across the antibody discovery market.

Geography Analysis

North America represented 41.5% of the antibody discovery market size in 2024, anchored by a mature venture capital ecosystem, concentrated biotech clusters in Boston and the Bay Area, and early regulatory engagement from the FDA that lowers uncertainty for novel constructs. Deep AI talent pools and proximity to leading academic centers accelerate computational innovation, sustaining the region’s leadership in early-stage technology breakthroughs. Rising labor costs and competitive pricing from offshore providers, however, motivate large firms to offload routine screening or sequence-liability testing to external partners located elsewhere.

Asia Pacific is forecast to register a 13.5% CAGR from 2025 to 2030, the highest across all regions. Government incentives in China, India, South Korea, and Singapore range from tax credits to purpose-built bioclusters, and have attracted multinational CDMOs that co-locate with domestic innovators. Regional players increasingly launch proprietary formats and form outbound partnerships, indicating a transition from cost-center to innovation hub. Regulatory authorities are harmonizing guidelines with ICH standards, shortening review timelines for clinical trial applications and thereby stimulating local demand for discovery platforms.

Europe remains a pivotal market rooted in historic pharmaceutical strongholds across Germany, Switzerland, and the United Kingdom. The European Medicines Agency’s guidance on monoclonal antibodies and biosimilars supplies regulatory clarity for traditional formats. Simultaneously, the bloc’s movement toward animal-free science accelerates investment in in-vitro display and computational design, opening niche opportunities even as overall growth trails North America and Asia Pacific. Brexit has introduced administrative overhead for cross-border studies. Still, London-based financial markets continue to fund biotech spinouts, ensuring that the region stays integral to the antibody discovery market’s global footprint.

Competitive Landscape

The antibody discovery market is moderately fragmented. Established life-science suppliers such as Thermo Fisher Scientific, Sartorius AG, and WuXi Biologics maintain large installed bases across cell line development, analytics, and pilot-scale production. Their scale supports continuous reinvestment in automation, high-content imaging, and machine-learning pipelines that sustain client retention. Mid-tier players differentiate by owning niche technologies—example platforms include transgenic mice that yield fully human sequences or display systems tailored for G-protein-coupled receptors.

AI-centric entrants like Chai Discovery and MAbSilico deliver purpose-built design engines that skip labor-intensive immunization steps, compressing go-to-hit timelines by an order of magnitude. These challengers usually partner with CDMOs for wet-lab validation, effectively inserting themselves as digital layer specialists rather than full-service rivals. Intellectual-property filings exceed 1,000 antibody-related applications annually, underscoring a race to stake claims around novel scaffolds, developability prediction algorithms, and manufacturing cell lines.

Strategic deal activity confirms platform convergence trends. In February 2025, Harbour BioMed allied with Insilico Medicine to merge AI design with a human antibody mouse system, while March 2025 witnessed BioNTech’s USD 800 million acquisition of Biotheus, adding Chinese manufacturing depth for bispecific programs. Such moves illustrate how incumbents seek technological breadth and geographic reach to counterbalance pure-play disruptors. Over the next five years, convergence between computational engines, specialized wet-lab capabilities, and global manufacturing footprints is expected to redefine what constitutes full-service competitiveness within the antibody discovery market.

Antibody Discovery Industry Leaders

GenScript Biotech

WuXi Biologics

Abcam plc

Thermo Fisher Scientific

Cytiva (Danaher)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Chai Discovery unveiled Chai-2, reporting 16% de-novo binding across 52 targets and reducing discovery cycles to weeks.

- February 2025: Harbour BioMed partnered with Insilico Medicine to accelerate AI-powered antibody discovery, combining Harbour Mice and Pharma.AI platforms.

- January 2025: Antibody Analytics secured a strategic investment from NorthEdge to scale antibody characterization services.

- October 2024: Rapid Novor demonstrated REpAb sequencing that recovered functional antibodies from vaccinated human serum.

Global Antibody Discovery Market Report Scope

| Hybridoma Technology |

| Phage Display |

| Single-B-Cell Screening |

| Transgenic Animal Platforms |

| Yeast Display |

| Mammalian / Ribosome Display |

| AI/ML-Enabled In-Silico Design |

| In-house Discovery |

| Contract / Outsourced Discovery Services |

| Hybrid Co-development Partnerships |

| Pharmaceutical & Biopharmaceutical Companies |

| Biotechnology Start-ups |

| Academic & Research Institutes |

| Contract Research Organizations (CROs) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| APAC | China |

| Japan | |

| India | |

| South Korea | |

| Australia & New Zealand | |

| Rest of APAC | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Discovery Technology | Hybridoma Technology | |

| Phage Display | ||

| Single-B-Cell Screening | ||

| Transgenic Animal Platforms | ||

| Yeast Display | ||

| Mammalian / Ribosome Display | ||

| AI/ML-Enabled In-Silico Design | ||

| By Service Model | In-house Discovery | |

| Contract / Outsourced Discovery Services | ||

| Hybrid Co-development Partnerships | ||

| By End User | Pharmaceutical & Biopharmaceutical Companies | |

| Biotechnology Start-ups | ||

| Academic & Research Institutes | ||

| Contract Research Organizations (CROs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| APAC | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia & New Zealand | ||

| Rest of APAC | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the antibody discovery market?

The antibody discovery market size is USD 9.09 billion in 2025.

What annual growth rate is expected for the market through 2030?

The market is projected to register an 11.3% CAGR over the 2025–2030 period.

Which discovery technology segment is growing the fastest?

AI/ML-enabled in-silico design is forecast to expand at a 22.4% CAGR, the highest among all technology categories.

Why are pharmaceutical companies increasingly outsourcing antibody discovery?

Rising platform complexity and capital intensity make external CDMOs attractive for specialized tasks, enabling cost savings and faster project turnaround.

Which region is expected to show the strongest growth?

Asia Pacific is anticipated to grow at a 13.5% CAGR, propelled by government incentives, upgraded technical capabilities and competitive pricing.

Page last updated on: