Viral Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

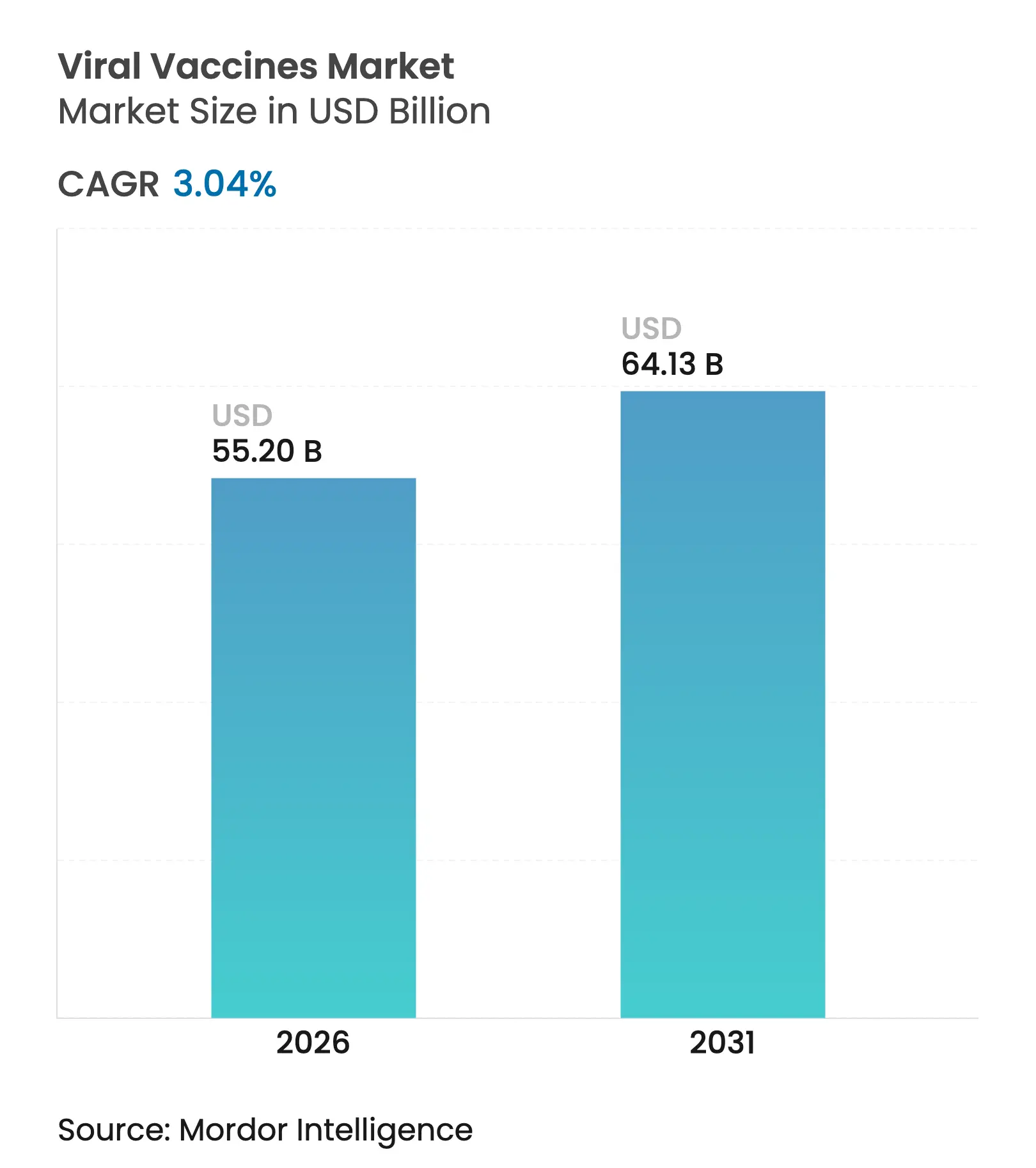

| Market Size (2026) | USD 55.2 Billion |

| Market Size (2031) | USD 64.13 Billion |

| Growth Rate (2026 - 2031) | 3.04 % CAGR |

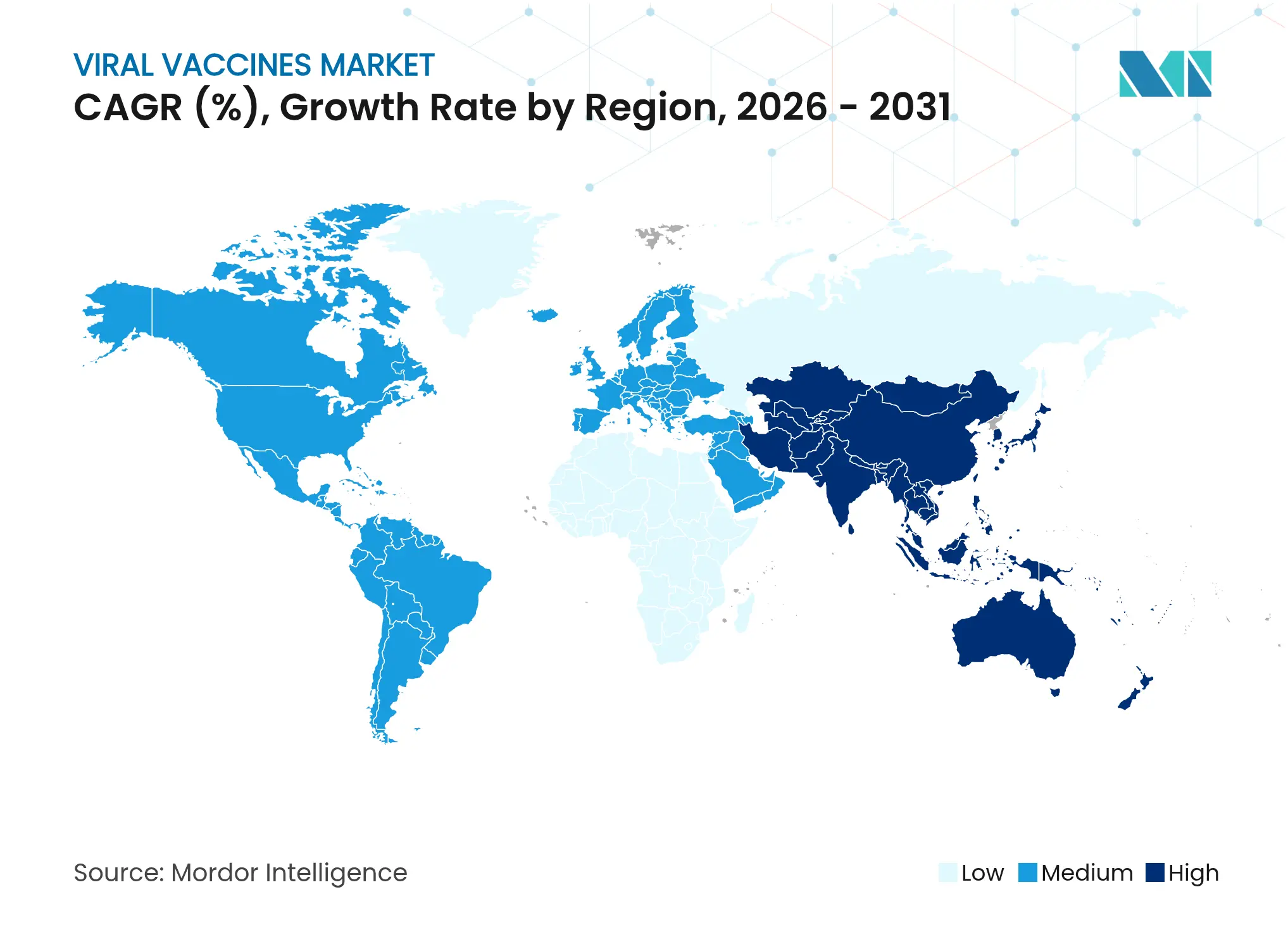

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Viral Vaccines Market Analysis by Mordor Intelligence

The viral vaccines market size is expected to grow from USD 53.57 billion in 2025 to USD 55.2 billion in 2026 and is forecast to reach USD 64.13 billion by 2031 at 3.04% CAGR over 2026-2031. The shift from volume-driven expansion to platform-based differentiation reflects sustained pandemic-preparedness funding, rapid-response technology adoption, and re-shoring of production capacity. Government programs such as the USD 5 billion Project NextGen and the USD 590 million HHS allocation for next-generation mRNA influenza vaccines are steering capital toward speed-to-market capabilities that surpass traditional development timelines. Manufacturers are recalibrating supply chains around regional security goals, evidenced by Sanofi’s USD 595 million Singapore expansion and Lotte Biologics’ USD 3.3 billion South Korean plant that anchor Asia-Pacific hubs. Liquid formulations retain demand leadership, yet freeze-dried products grow fastest as governments pay premiums for shelf-stable stockpiles. Platform technologies now set the competitive pace; mRNA candidates out-grow legacy subunit and conjugate products while therapeutic pipelines unlock higher-value treatment niches. Public procurement still commands the majority of doses, but private channels capture the fastest growth as employer immunization programs and travel requirements expand adult uptake.

Key Report Takeaways

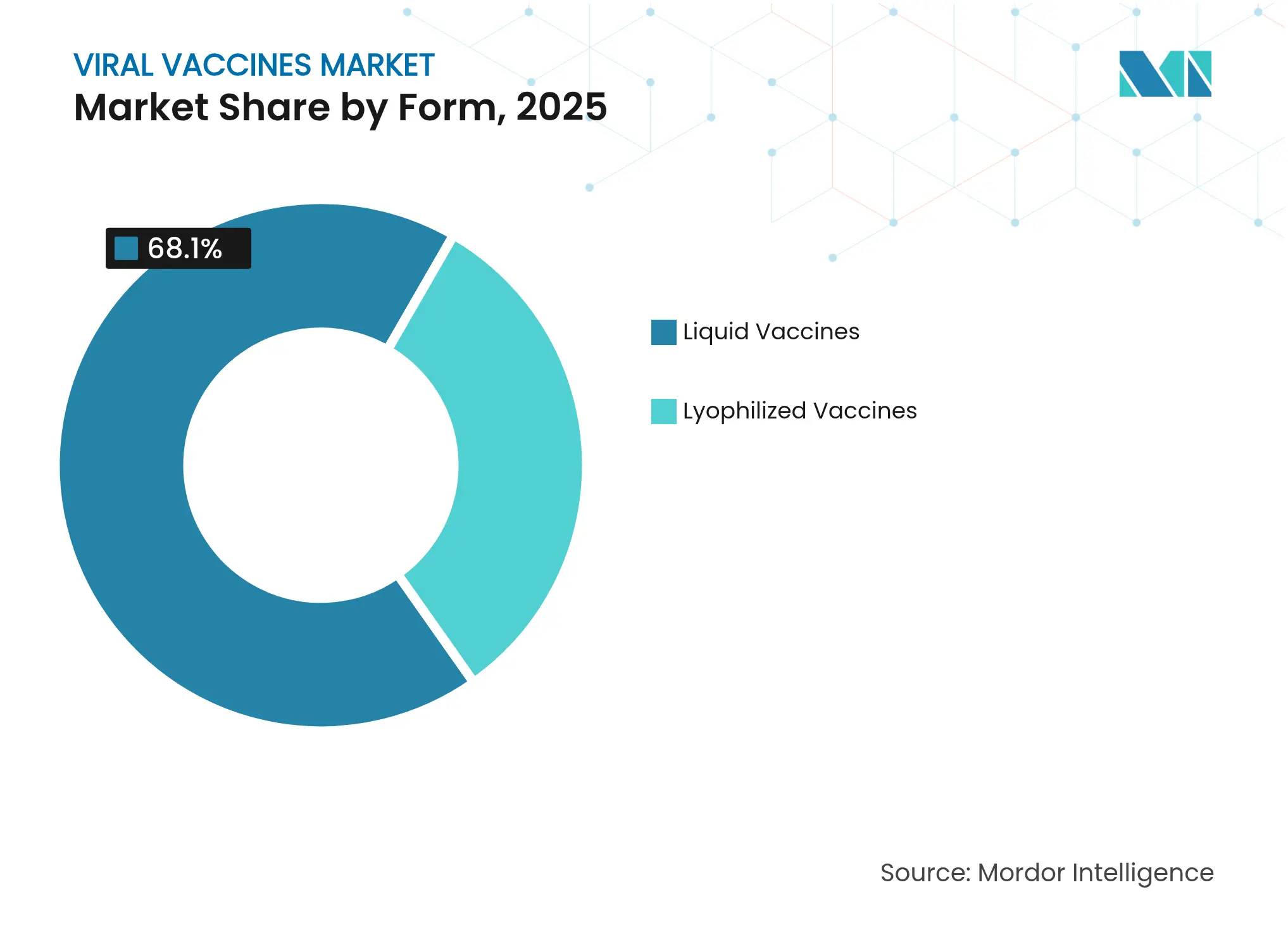

- By form, liquid vaccines accounted for 68.10% of viral vaccines market share in 2025, while lyophilized products are advancing at a 4.18% CAGR through 2031.

- By type, subunit and conjugate vaccines led with 40.78% revenue share in 2025; mRNA platforms record the highest projected CAGR at 4.39% through 2031.

- By approach, preventive products dominated with 77.85% share in 2025, yet therapeutic candidates are pacing growth at 4.63% CAGR to 2031.

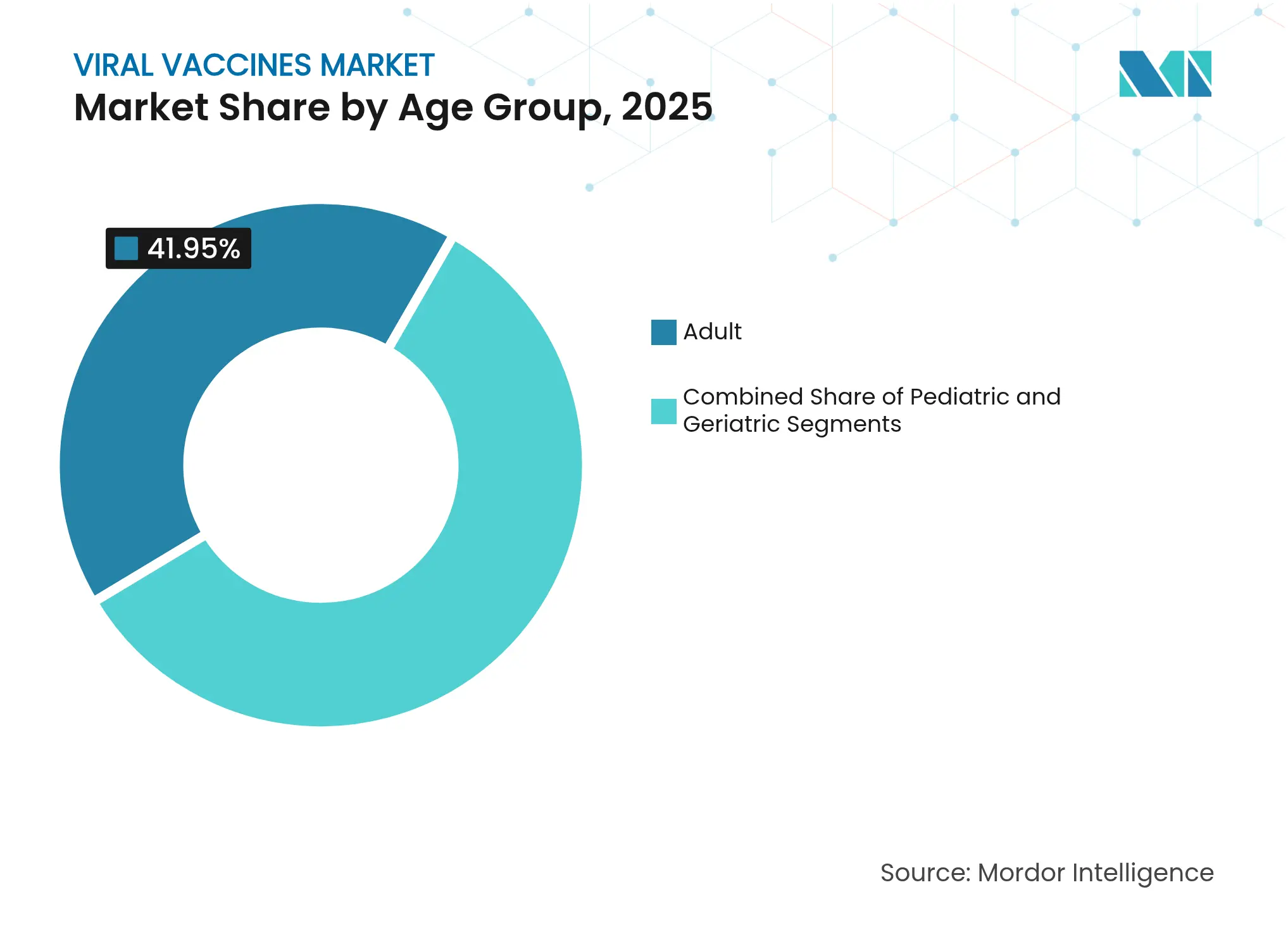

- By age group, adults held 41.95% share of the viral vaccines market size in 2025; pediatric formulations are expanding at a 4.21% CAGR through 2031.

- By distribution channel, the public sector controlled 69.20% of 2025 volumes, while private channels post a 4.12% growth rate through 2031.

- By geography, North America captured 40.75% of 2025 revenue; Asia-Pacific is forecast to grow the fastest at 4.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Viral Vaccines Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Government immunization funding surge

Government immunization funding surge

| +1.2% | North America, EU | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

North America, EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Rising incidence of viral outbreaks

Rising incidence of viral outbreaks

| +0.8% | APAC, MEA | Short term (≤ 2 years) | |||

Rapid-response platform technologies

Rapid-response platform technologies

| +0.6% | North America, EU | Long term (≥ 4 years) | |||

Pandemic-preparedness stockpiling

Pandemic-preparedness stockpiling

| +0.4% | High-income nations | Medium term (2-4 years) | |||

Expanding LMIC manufacturing hubs

Expanding LMIC manufacturing hubs

| +0.3% | APAC core | Long term (≥ 4 years) | |||

Demand for combination vaccines

Demand for combination vaccines

| +0.2% | Developed markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Government Immunization Funding Surge

Large-scale public budgets shift procurement from episodic purchases to rolling contracts that stabilize cash flows and de-risk R&D. The USD 79.5 billion 2024 PHEMCE allocation anchors multi-year demand, letting manufacturers plan capacity expansions without fearing demand cliffs. Japan’s USD 8.5 billion 100-day vaccine program sets new global speed benchmarks that regulators elsewhere will likely mirror. As sovereign buyers insist on accelerated timelines, platform agility becomes an entry ticket, raising technical hurdles for late adopters. Steady public funding also crowds-in private investment, widening the resource gap between frontier technologies and conventional approaches. Ultimately, predictable procurement fortifies the viral vaccines market against cyclical shocks while intensifying the race for innovative modalities.

Rising Incidence of Viral Outbreaks

Zoonotic transmission risks and resurgent endemic diseases create a baseline need for flexible production. USDA clearance for mass H5N1 poultry immunization underscores cross-species dynamics that pull veterinary and human pipelines closer. Recurrent measles spikes reveal how lapses in community coverage quickly translate into new sales opportunities for suppliers with surge capacity. Outbreak-driven purchasing favors manufacturers capable of moving from sequence to shipment within months, eroding the advantage of pure scale. The convergence of animal and human vaccine markets further rewards firms with multipurpose platforms that can amortize R&D costs across broader portfolios.

Rapid-Response Platform Technologies

mRNA and viral-vector systems reduce design-to-clinical timelines, making speed the principal differentiation lever. Moderna’s mNEXSPIKE approval validates variant-targeted programs that pivot quickly as viral evolution advances [1]Moderna, Inc., "Moderna Receives U.S. FDA Approval for COVID-19 Vaccine mNEXSPIKE," modernatx.com. Wacker’s USD 102 million German mRNA hub, sized for 200 million doses annually, shows how shared infrastructure boosts multi-asset output. Investors now judge portfolios by adaptive capacity, incentivizing firms to prioritize modular facilities and digitalized QC. Consequently, platform leaders can secure advance-purchase commitments that underwrite expansion well before phase III readouts, compressing traditional product-launch curves.

Pandemic Preparedness Stockpiling by High-Income Nations

Governments stockpile broad-spectrum or shelf-stable vaccines, granting premium status to lyophilized and multivalent products. Germany’s reservation of half the Wacker plant’s output for strategic reserves exemplifies guaranteed off-take that mitigates commercial volatility [2]Wacker Chemie AG, “Wacker Secures German Pandemic-Preparedness Contract,” wacker.com . The European Union’s EUR 750 million African Vaccines Manufacturing Accelerator pledges to procure 800 million doses, linking foreign-aid budgets to reliable demand signals. Such commitments smooth manufacturing utilization rates, encourage dual-use facilities, and cap market cyclicality.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High clinical & scale-up costs

High clinical & scale-up costs

| -0.7% | Global | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

-0.7%

|

Geographic Relevance

:

Global

|

Impact Timeline

:

Long term (≥ 4 years)

|

Cold-chain & last-mile logistics gaps

Cold-chain & last-mile logistics gaps

| -0.5% | APAC, MEA | Medium term (2-4 years) | |||

Regulatory complexity for novel platforms

Regulatory complexity for novel platforms

| -0.4% | North America, EU | Medium term (2-4 years) | |||

Social-media-driven vaccine hesitancy

Social-media-driven vaccine hesitancy

| -0.3% | Developed markets | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Clinical & Scale-Up Costs

Novel platforms carry elevated R&D and facility requirements that exceed conventional budgets three- to five-fold, restricting participation to capital-rich firms. Therapeutic vaccine trials often surpass USD 100 million due to longer follow-up and specialized endpoints, straining early-stage biotech cash flows. Specialized lipid nanoparticle lines and validated RNA suites further inflate outlays, anchoring competitive advantage with conglomerates that can amortize costs across broader pipelines.

Cold-Chain & Last-Mile Logistics Gaps

Ultra-low-temperature needs for select mRNA products strain distribution in regions where grid stability is uncertain. Rural APAC and parts of MEA remain underserved, tipping purchasing in favor of lyophilized or ambient-temperature alternatives. Consequently, suppliers unable to furnish thermal-stable formats risk exclusion from sizeable tenders despite clinical efficacy. Investments in portable coolers and solar-powered freezers are growing, yet infrastructure parity is several years away.

Segment Analysis

By Form: Lyophilized Formulations Elevate Access

Lyophilized doses, though a minority today, chip away at the liquid stronghold with a 4.18% CAGR through 2031. Liquid vaccines held 68.10% of viral vaccines market share in 2025, but freeze-dried products capture procurement preference where cold chain reliability is questionable. The viral vaccines market size for lyophilized offerings is projected to expand steadily as humanitarian agencies prioritize long-shelf-life stock. Asahi Kasei’s Planova FG1 filter accelerates virus removal sevenfold, cutting cycle times and improving yield.

Process innovations such as controlled nucleation preserve antigen conformation, allowing room-temperature shipping without potency loss. Manufacturers that master excipient optimization unlock distribution to last-mile clinics, converting previously inaccessible populations into addressable demand. Over the forecast horizon, liquid fill-finish lines will still dominate urban markets, yet dry-powder formats are expected to expand territory coverage and smooth seasonal volume fluctuations.

Note: Segment shares of all individual segments available upon report purchase

By Type: Platform Diversification Reshapes Portfolios

Subunit and conjugate products provided 40.78% of 2025 revenue, reinforcing their regulatory familiarity. However, mRNA candidates post a 4.39% CAGR, gradually eroding incumbent margins. The viral vaccines market size attached to mRNA is buoyed by adaptive design that compresses preclinical work. Meiji Seika’s self-replicating mRNA prototype illustrates next-wave efficiencies that could lower dose requirements and reduce raw-material spend.

Legacy inactivated and viral-vector categories supply risk-averse regulators and markets with lower cold-chain budgets, maintaining relevance as portfolio ballast. Yet sponsors increasingly hedge by maintaining at least two modality capabilities, ensuring continuity if safety signals or supply disruptions hit a single platform. Cross-training of manufacturing staff and harmonized digital QC systems permit operational flexibility that aligns with unpredictable pathogen emergence.

By Approach: Therapeutics Challenge Prophylaxis Supremacy

Preventive injections captured 77.85% revenue in 2025, but therapeutic programs targeting chronic infections grow at 4.63% CAGR. HPV therapeutic vaccine trials focusing on E6/E7 oncoproteins demonstrate potential to shift cancer management paradigms . Revenue models differ; treatment courses command higher price points offsetting smaller eligible populations. The viral vaccines market share for therapeutics remains modest today yet is poised to rise as proof-of-concept successes expand indications.

Preventive regimens still underpin national schedules and school mandates, locking in recurring demand streams. Nonetheless, regulatory agencies begin crafting distinct pathways for therapeutic candidates, potentially shortening approval times once surrogate endpoints become validated. Companies that integrate both preventive and therapeutic lines can arbitrage manufacturing overheads while diversifying risk across policy and epidemiology uncertainties.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Age Group: Pediatric Doses Drive Schedule Expansion

Adult use retained the highest 41.95% share in 2025, yet pediatric demand is advancing fastest at 4.21% CAGR. Expanded childhood schedules and combination shots reduce clinic visits while improving compliance. The viral vaccines market size allocated to pediatric cohorts benefits from government bulk purchasing that stabilizes annual production plans. Simultaneously, adult boosters against respiratory syncytial virus and shingles represent lucrative private-pay niches.

Geriatric demand grows as clinicians seek immunosenescence-friendly adjuvants, creating micro-segments with willingness to pay for enhanced protection. Developers tailor dosage and formulation strategies per demographic, recognizing that a uniform approach overlooks physiological and socioeconomic nuances that influence uptake.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Private Options Gain Momentum

Public procurement delivered 69.20% of 2025 volume, ensuring base-load factory utilization. Yet private outlets are registering 4.12% CAGR as employer programs and retail clinics promote convenience. The viral vaccines market size flowing through private channels is still small but generates attractive margins given reduced tender pricing pressure. Manufacturers craft dual-pricing strategies that meet government affordability mandates while capturing discretionary premium segments.

Engagement of digital pharmacies and on-site employer events shortens purchase cycles, lending agility that public tenders lack. Firms that align packaging, messaging, and service levels with consumer expectations will out-perform peers reliant on institutional buyers alone.

Geography Analysis

North America commanded 40.75% of 2025 revenue owing to entrenched R&D clusters, advanced cold chains, and strategic federal outlays such as Project NextGen. Merck’s USD 1 billion North Carolina fill-finish expansion and Moderna’s trio of plants under construction highlight how domestic capacity scales to match guaranteed off-take. Regulatory frameworks like FDA Fast Track accelerate first-in-class entrants, preserving the region’s innovation premium despite rising global competition.

Asia-Pacific posts the fastest 4.08% CAGR as governments embed bioscience in industrial policy. China’s multi-billion-dollar 2024 bioprocessing investments and South Korea’s Lotte Biologics megasite illustrate state-backed ambitions to dominate contract manufacturing. Japan’s 1.1 trillion-yen rapid-response initiative nurtures mRNA self-sufficiency, coupling funding with streamlined approvals. Regional suppliers leverage lower capital costs and abundant engineering talent to bid aggressively for multinational tech-transfer deals, redrawing supply-chain maps.

Europe leverages harmonized regulation and public-private financing to sustain capacity. Sanofi, Pfizer, and AstraZeneca pledged EUR 2.5 billion for new French facilities that benefit from talent pools and centralized quality frameworks. Wacker’s German mRNA hub, locked into national reserve commitments, underscores governmental drive for sovereignty. The EU’s African accelerator funds extend geopolitical reach by underwriting export pipelines that also cushion domestic demand swings. BioNTech’s GBP 1 billion UK expansion, aided by targeted grants, shows how flexible post-Brexit incentives can attract long-horizon R&D spending.

Competitive Landscape

Market Concentration

Competition mixes scale champions with platform specialists. Pfizer, Sanofi, and GSK rely on diversified portfolios and extensive tender networks to defend incumbency. Yet agility leaders such as Moderna, BioNTech, and CureVac exploit mRNA know-how to secure variant-specific approvals in record time. AstraZeneca’s USD 1.1 billion Icosavax acquisition and Novavax’s USD 1.2 billion tie-up with Sanofi highlight the premium placed on proprietary antigen-design engines.

White-space plays center on therapeutic and combination formulations, where pricing freedom offsets narrower patient pools. AI-guided immunogen discovery and digital twins for process modeling are emerging weapons that cut cycle times and derisk scale-up.

Still, high capital requirements and regulatory hurdles curb fragmentation, keeping bargaining power with a tight cohort of global producers. In this environment, partnership optionality becomes as crucial as internal innovation, with co-development deals spreading risk while opening regional access pathways.

Viral Vaccines Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Moderna received FDA approval for mNEXSPIKE (mRNA-1283) for adults 65+ and at-risk individuals 12-64.

- May 2025: BioNTech committed GBP 1 billion over 10 years for two UK R&D centers, backed by GBP 129 million in government grants.

- March 2025: Curevo closed a USD 110 million Series B to advance amezosvatein, a non-mRNA shingles candidate.

- June 2024: Wacker opened a USD 102 million mRNA competence center in Halle, Germany with 200 million-dose annual capacity.

Table of Contents for Viral Vaccines Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Government Immunization Funding Surge

- 4.2.2Rising Incidence of Viral Outbreaks

- 4.2.3Rapid?Response Platform Technologies

- 4.2.4Pandemic Preparedness Stockpiling by High-Income Nations

- 4.2.5Expanding LMIC Vaccine Manufacturing Hubs

- 4.2.6Demand For Combination Viral Vaccines

- 4.3Market Restraints

- 4.3.1High Clinical & Scale-Up Costs

- 4.3.2Cold-Chain & Last-Mile Logistics Gaps

- 4.3.3Regulatory Complexity for Novel Platforms

- 4.3.4Social-Media-Driven Vaccine Hesitancy

- 4.4Regulatory Landscape

- 4.5Porters Five Forces Analysis

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Form

- 5.1.1Liquid Vaccines

- 5.1.2Lyophilized Vaccines

- 5.2By Type

- 5.2.1Live-attenuated

- 5.2.2Inactivated

- 5.2.3Subunit and Conjugate

- 5.2.4mRNA

- 5.2.5Viral Vector

- 5.2.6Others

- 5.3By Approach

- 5.3.1Preventive

- 5.3.2Therapeutic

- 5.4By Age Group

- 5.4.1Pediatric

- 5.4.2Adult

- 5.4.3Geriatric

- 5.5By Distribution Channel

- 5.5.1Public

- 5.5.2Private

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4Australia

- 5.6.3.5South Korea

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East and Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1Pfizer Inc.

- 6.3.2AstraZeneca plc

- 6.3.3Serum Institute of India Pvt Ltd

- 6.3.4Dynavax Technologies Corp.

- 6.3.5Moderna Inc.

- 6.3.6Bavarian Nordic A/S

- 6.3.7CSL Ltd (Seqirus)

- 6.3.8Valneva SE

- 6.3.9Emergent BioSolutions Inc.

- 6.3.10GSK plc

- 6.3.11Bharat Biotech Intl. Ltd

- 6.3.12Merck & Co., Inc.

- 6.3.13Sanofi SA

- 6.3.14Johnson & Johnson (Janssen)

- 6.3.15BioNTech SE

- 6.3.16Novavax Inc.

- 6.3.17Sinovac Biotech Ltd

- 6.3.18Sinopharm (CNBG)

- 6.3.19CanSino Biologics Inc.

- 6.3.20Inovio Pharmaceuticals Inc.

- 6.3.21Zydus Lifesciences Ltd

- 6.3.22Clover Biopharma

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Viral Vaccines Market Report Scope

Viral vaccines can be made from live viruses, killed viruses, or subunits of viruses. Common viral vaccines protect against diseases such as measles, rubella, mumps, hepatitis B, rabies, and human papillomavirus, among others. Viral vaccines play a crucial role in safely combating the spread of various viruses, including the variola virus, poliovirus, and rabies viruses.

The viral vaccine market is segmented into form, type, approach, and geography. By form, the market is segmented into liquid vaccines and lyophilized vaccines. By type, the market is segmented into live-attenuated vaccines, killed or inactivated vaccines, subunit and conjugate vaccines, mRNA vaccines, viral vector, and others (combination vaccines, toxoids, and others). By approach, the market is segmented into therapeutic and preventive. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also offers the market size and forecasts for 17 countries across the region. For each segment, the market sizing and forecasts have been done based on value (USD).