COVID-19 Vaccine Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

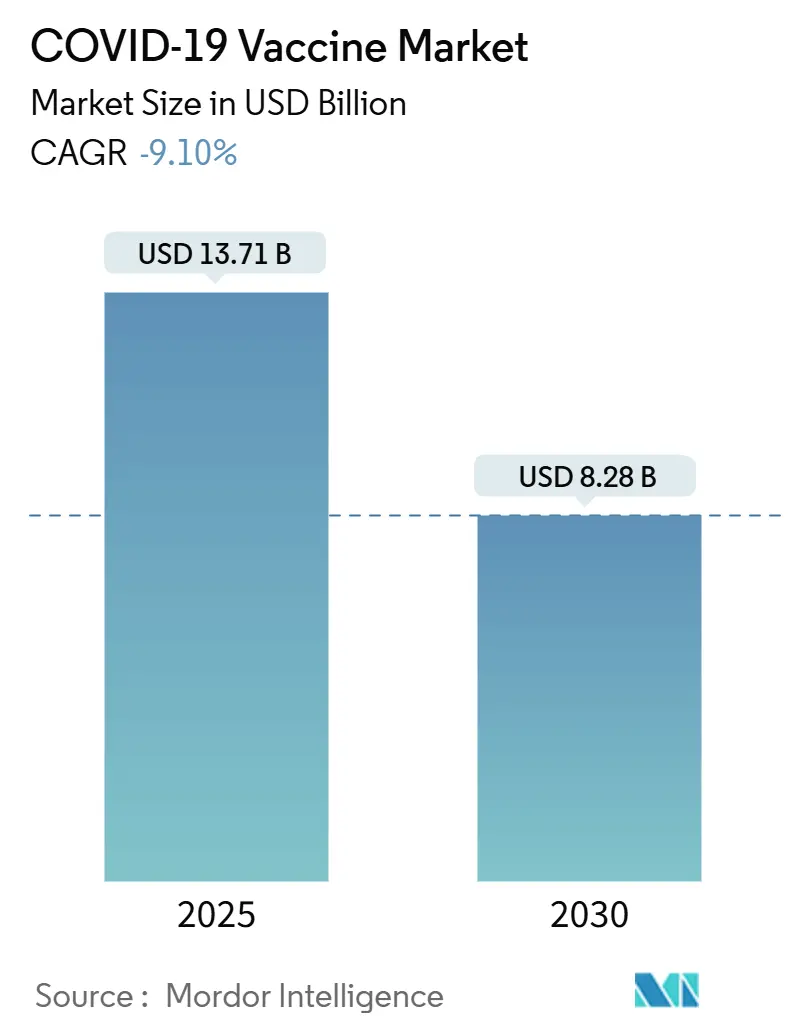

| Market Size (2025) | USD 13.71 Billion |

| Market Size (2030) | USD 8.28 Billion |

| Growth Rate (2025 - 2030) | -9.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

COVID-19 Vaccine Market Analysis by Mordor Intelligence

The COVID-19 vaccine market size stood at USD 13.71 billion in 2025 and is projected to contract to USD 8.28 billion by 2030, reflecting a –9.10% CAGR during the forecast period. The downturn follows the global shift from emergency mass immunization toward routine, risk-based programs for older adults and immunocompromised populations. Demand now hinges on government booster funding, variant-adapted formulations, and combination respiratory shots that promise operational efficiencies for overstretched health budgets. Competitive dynamics are characterized by accelerating portfolio diversification, strategic alliances that merge platform know-how with commercial reach, and expanding Asia-Pacific production capacity that counterbalances Western volume declines. Meanwhile, political headwinds against mRNA platforms in parts of the United States underscore the rising regulatory complexity that manufacturers must navigate to safeguard revenues.

Key Report Takeaways

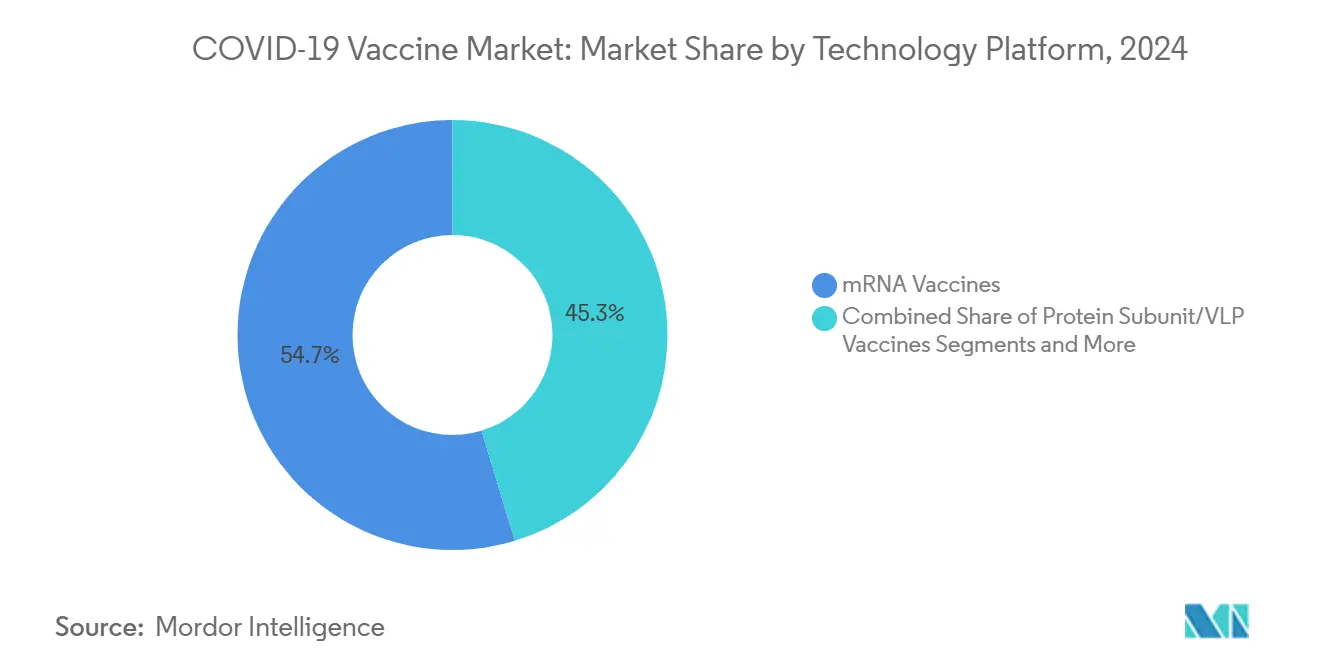

- By technology platform, mRNA retained 54.7% of the COVID-19 vaccine market share in 2025, while protein subunit vaccines recorded the fastest relative growth trajectory among non-mRNA competitors despite the broader market contraction.

- By valency, bivalent formulations led with a 61.2% revenue share in 2024; multivalent candidates are projected to exhibit the highest CAGR at 14.2% through 2030, as manufacturers pursue universal coronavirus protection strategies.

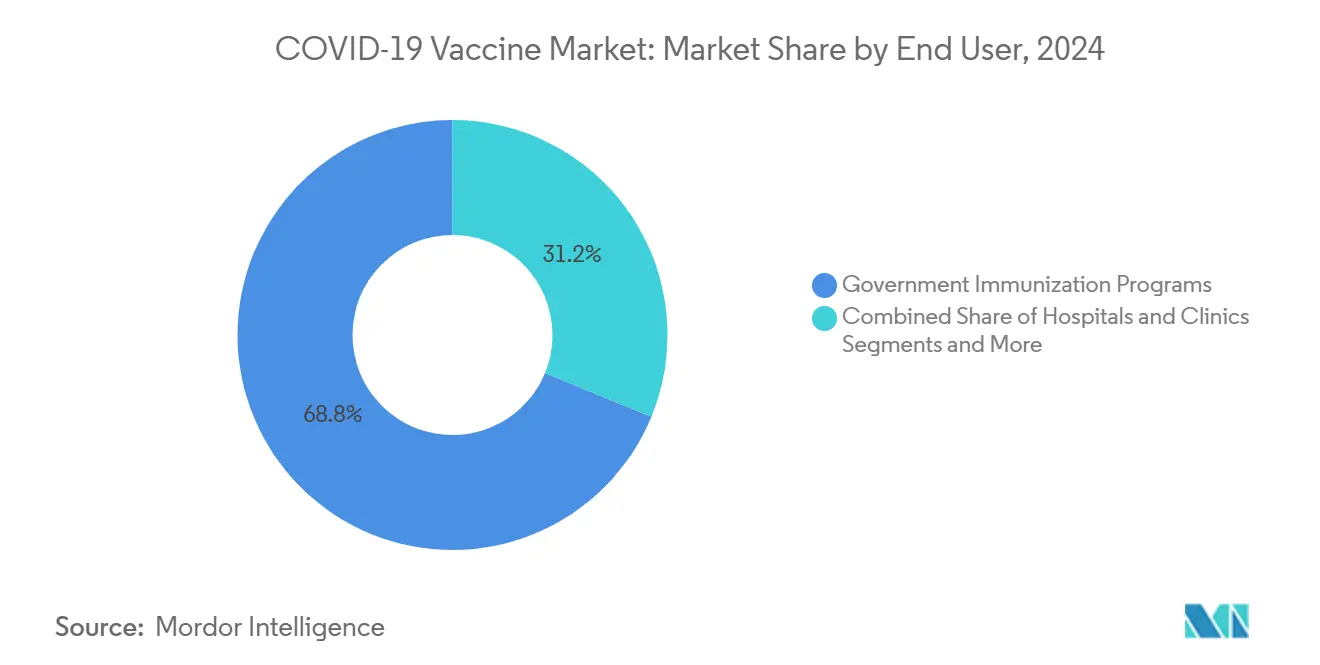

- By end user, government immunization programs accounted for 68.8% of the COVID-19 vaccine market size in 2024, whereas retail pharmacies demonstrated the most stable performance with a –7.4% CAGR forecast to 2030.

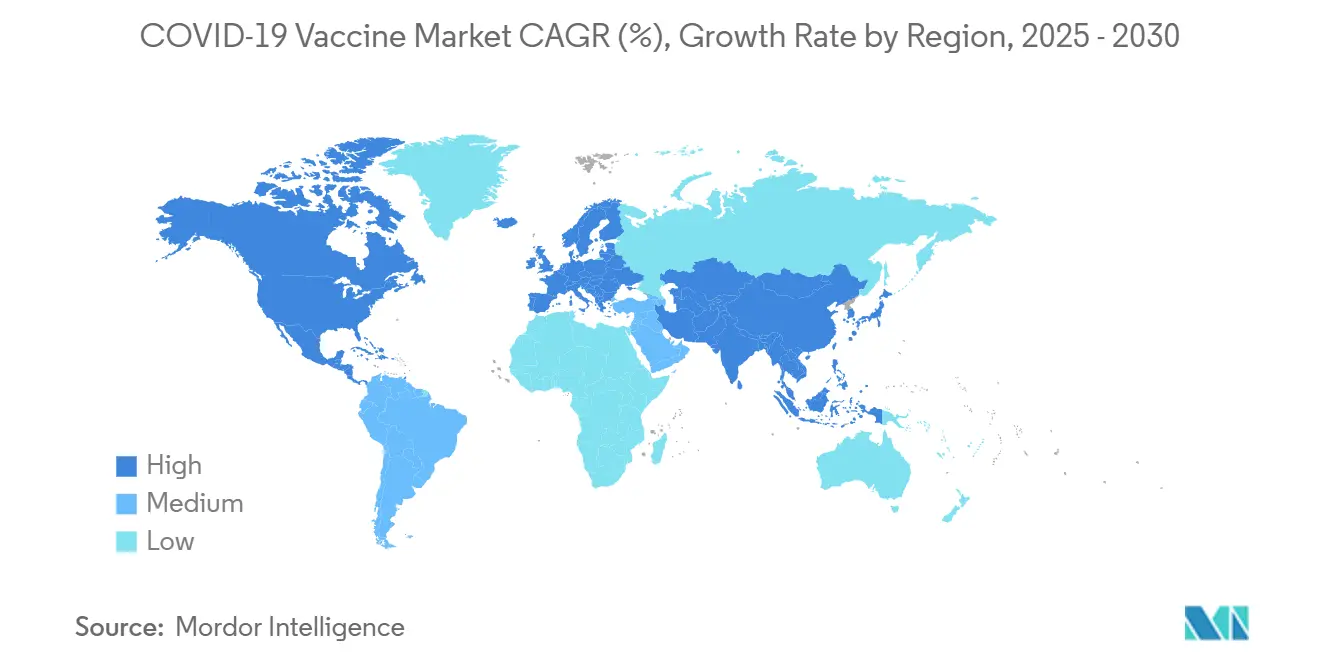

- North America commanded 38.2% of the global COVID-19 vaccine market in 2024; the Asia-Pacific region shows the smallest contraction at a –3.7% CAGR through 2030, buoyed by sustained public procurement and local manufacturing expansion.

Market Trends and Insights

Drivers Impact Analysis of COVID-19 Vaccine Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government booster-program funding & procurement commitments | +2.30% | Global; strongest in North America and EU | Medium term (2-4 years) |

| Variant-adapted & combo respiratory vaccine upgrades | +1.80% | Global; led by developed markets | Short term (≤2 years) |

| Integration into routine immunization schedules for high-risk groups | +1.50% | APAC core with spill-over to developed markets | Long term (≥4 years) |

| Advances in mRNA stabilization & lyophilized formulations | +1.20% | Global; amplified in emerging markets | Medium term (2-4 years) |

| Microneedle patch & intradermal delivery cut cold-chain costs | +0.90% | Emerging markets; rural health settings | Long term (≥4 years) |

| OPMR & blockchain verification improve booster compliance | +0.70% | National systems with early adoption in developed countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Booster-Program Funding & Procurement Commitments

Sustained public funding supplies a predictable revenue floor as private demand wanes. The U.K. allocated GBP 1 billion (USD 1.33 billion) for its 2025 autumn booster campaign that prioritizes adults 75+ and the immunocompromised, guaranteeing minimum national volume for Pfizer-BioNTech’s Comirnaty.[1]Department of Health and Social Care, “COVID-19 Autumn 2025 Vaccination Programme,” gov.uk In the United States, the USD 5 billion Project NextGen fund underwrites late-stage trials for next-generation vaccines, converting R&D risk into future procurement options.[2]U.S. Department of Health and Human Services, “Project NextGen,” hhs.gov Similar multi-year purchase agreements across Canada, Germany, and Japan foster supply-chain continuity and incentivize continued platform innovation despite revenue headwinds.

Variant-Adapted & Combo Respiratory Vaccine Upgrades

Fast-cycle regulatory clearance for strain-matched shots has become the new competitive yardstick. In August 2024, the FDA simultaneously authorized KP.2-targeted mRNA vaccines from Moderna and Pfizer and a JN.1-targeted protein subunit vaccine from Novavax, marking the first dual-variant season in U.S. history. Efficacy data published in the Lancet showed Moderna’s next-generation mRNA-1283 candidate delivering 9.3% higher relative protection than its predecessor against Omicron sub-lineages. As influenza-COVID combination shots proceed through late-stage trials, companies anticipate supply-chain synergies and greater patient adherence, supporting incremental volume even within a contracting COVID-19 vaccine market.

Integration Into Routine Immunization Schedules for High-Risk Groups

Guideline bodies pivoted from universal recommendations to risk-based dosing patterns that align with influenza program logic. The CDC now advises adults 65 years or older and people with immunocompromising conditions to receive an additional 2024-2025 dose six months after their last shot. The Joint Committee on Vaccination and Immunization (JCVI) embedded formal cost-effectiveness thresholds into U.K. COVID-19 policy, reserving public reimbursement for populations where economic modeling confirms net benefit. These frameworks institutionalize demand for annual or biannual boosters, underpinning long-term volume visibility for manufacturers.

Advances in mRNA Stabilization & Lyophilized Formulations

Process innovation is reducing cold-chain dependency, broadening access in resource-constrained regions, and lowering inventory write-offs. Researchers funded by CEPI are developing heat-stable lipid nanoparticle chemistries capable of maintaining potency for six months at 25 °C, slashing logistics costs by up to 70%. A trans-amplifying mRNA construct from the University of Pittsburgh requires 40-fold less active ingredient, cutting both raw-material cost and reactogenicity risk.[3]Science Daily, “New mRNA Vaccine Is More Effective,” sciencedaily.com Commercial adoption of lyophilized vials is forecast to accelerate share retention for mRNA leaders while enabling regional fill-finish partnerships throughout Asia Pacific and Latin America.

Restraints Impact Analysis of COVID-19 Vaccine Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Waning pandemic urgency dampens demand | –4.2% | Global; most pronounced in developed markets | Short term (≤2 years) |

| Politicization & hesitancy toward mRNA platforms | –2.8% | North America; selective EU regions | Medium term (2-4 years) |

| State-level legislative restrictions on mRNA use | –1.9% | United States; potential spill-over to other federal systems | Medium term (2-4 years) |

| Insufficient ultra-cold-chain capacity in low-income regions | –1.6% | Sub-Saharan Africa, rural Asia, Latin America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Waning Pandemic Urgency Dampens Demand

Public perception of COVID-19 as a manageable endemic disease undercuts vaccination intent even among high-risk cohorts. Pfizer’s COVID portfolio revenue fell 52% year-over-year to USD 5.4 billion in 2024 amid sharply reduced contracted volumes. CDC surveillance from the VISION and IVY networks estimated 22.8% adult uptake of the 2024-2025 updated booster despite 44% vaccine effectiveness against hospitalization. Such behavioral shifts create inventory volatility and prompt manufacturers to trim production capacity, reinforcing negative growth momentum across the COVID-19 vaccine market.

Politicization & Hesitancy Toward mRNA Platforms

Partisan attitudes increasingly dictate vaccine decisions. Draft bills in Montana and Idaho propose bans on mRNA technology, threatening to fracture U.S. market access and complicate supply-chain planning. Political realignment of public-health agencies elevated debate over federal advisory processes, injecting uncertainty into seasonal recommendation timelines. Resultant hesitancy depresses booster uptake, particularly in rural counties, muting revenue trajectories even in regions with ample vaccine availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

COVID-19 Vaccine Market Segment Analysis

By Technology Platform:

mRNA Maintains Dominance Despite Eroding Growth ProspectsmRNA vaccines captured 54.7% of the COVID-19 vaccine market share in 2024, anchored by the scale advantages of Pfizer-BioNTech and Moderna and their established real-time variant update capabilities. Protein subunit platforms, however, are rapidly positioning themselves to share gains through strategic alliances. Sanofi’s USD 1.2 billion co-commercialization deal with Novavax grants global reach to a technology historically constrained by marketing bandwidth. Even with a –11.1% CAGR forecast for protein subunits, the category remains the fastest-evolving mRNA alternative and could see volume stabilization as cost-conscious procurement agencies seek lower-price options.

Historically, viral vector and inactivated platforms filled supply gaps in 2021-2022 but now reside in maintenance niches, especially in countries with emergency authorizations still in place. Novel constructs such as self-amplifying mRNA and circular RNA candidate vaccines promise dose-sparing benefits and extended durability, hinting at long-term disruption potential after 2028. As combination vaccines enter commercial rollout, technology decisions will increasingly hinge on compatibility with multivalent payloads, potentially recalibrating COVID-19 vaccine market size allocation among platforms.

By Valency:

Bivalent Formulations Bridge Present Needs as Multivalent R&D AcceleratesBivalent shots represented 61.2% of global volume in 2024, reflecting regulators' preference for two-strain coverage that balances manufacturing feasibility with immunological breadth. Monovalent original-strain doses are being phased out across Europe and North America, with emergency-use extensions mostly reserved for humanitarian aid channels. Polyvalent and pan-coronavirus programs gather momentum, notably a CEPI-sponsored consortium exploring mosaic nanoparticle designs capable of neutralizing pre-emergent SARS-CoV-2. Although multivalent products account for less than 2% of the COVID-19 vaccine market size today, their 14.2% projected CAGR through 2030 positions them as the primary growth engine in an otherwise shrinking segment.

Adoption timelines hinge on validation of breadth without efficacy trade-offs and on the capacity of regulatory frameworks to accommodate complex potency assays. Manufacturers investing early in high-throughput variant screening and adaptive clinical trial designs may secure first-mover advantages, particularly in procurement tenders that bundle influenza and coronavirus protection.

By End User:

Government Programs Anchor Demand Amid Retail Channel ResilienceGovernment programs generated 68.8% of the COVID-19 vaccine market size in 2024 as ministries leveraged bulk purchasing to secure supply for targeted boosters. However, volume guarantees have narrowed around defined risk categories, compelling manufacturers to renegotiate minimum-purchase clauses. Retail pharmacies, supported by insurance reimbursement and consumer preference for convenience, show the shallowest decline at –7.4% CAGR to 2030, positioning them as critical last-mile hubs. Hospitals retain a role for complex patients requiring pre-vaccination evaluation, while occupational health programs remain uneven, flourishing in sectors such as aviation yet lagging in small-business settings.

Longitudinally, retail demand proved negligible during the 2021 mass-vaccination peak but now offers a defensive hedge against public-budget volatility. Manufacturers that optimize single-dose vial formats and extend shelf life for pharmacy channels may capture incremental volume otherwise lost to expirations in centralized stockpiles.

Geography Analysis

North America COVID-19 Vaccine Market

North America accounted for 38.2% of global revenue in 2024, underpinned by strong payer mechanisms and dense vaccination infrastructure. Nevertheless, mounting political opposition in certain U.S. states threatens to fragment procurement. Bills proposing to restrict mRNA vaccine use create planning uncertainty for suppliers and could prompt a geographical reallocation of manufacturing capacity toward jurisdictions with stable uptake. Canada’s science-driven National Advisory Committee on Immunization provides steadier demand signals, while Mexico leverages proximity to U.S. production hubs to diversify its respiratory vaccine supply chain.

Europe COVID-19 Vaccine Market

Europe exerts an outsized influence on antigen-composition decisions through the coordinated actions of the European Medicines Agency. The region’s transition toward cost-effectiveness-driven booster policies is exemplified by the United Kingdom’s age-stratified program, which reduces volume but enhances predictability. France and Germany remain among the largest single-country purchasers, although both report lower booster coverage compared with 2022 peaks.

APAC and Africa COVID-19 Vaccine Market

Asia Pacific demonstrates the greatest resilience with a –3.7% CAGR forecast through 2030. China’s Sinovac and Sinopharm vaccines dominate domestic allocation, with export deals across Southeast Asia enhancing production economies of scale. India’s Serum Institute capitalizes on fill-finish versatility to serve both domestic and African volume. Japan granted full approval to Arcturus Therapeutics’ self-amplifying mRNA candidate, confirming its openness to novel platforms that could offset declining imports of first-generation doses. Australia’s risk-based booster framework mirrors its long-standing influenza strategy, preserving modest but reliable tender demand.

South America and the Middle East COVID-19 Vaccine Market

Latin America and the Middle East see heterogeneous trajectories. Brazil benefits from Butantan Institute’s tech-transfer agreements that localize protein subunit production. In contrast, several Gulf states shifted procurement toward combination COVID-influenza candidates for adult boosters, anticipating efficiency gains within overstretched primary-care systems.

Competitive Landscape

Market concentration remains moderate. Pfizer, Moderna, and Novavax collectively held a 71% share in 2024. Still, downward revenue pressure is catalyzing portfolio diversification and selective M&A. Pfizer’s COVID franchise posted USD 3.4 billion in 2024, down 38% year-over-year, prompting renewed emphasis on partner-led R&D collaborations. Moderna is repositioning itself as a broad respiratory player; FDA approval of its RSV vaccine mRESVIA in April 2025 underscores growing dependence on a multi-pathogen strategy to stabilize cash flow.

Strategic alliances accelerate. Sanofi’s co-exclusive licensing accord with Novavax integrates protein subunit innovation with established distribution muscle to commercialize both stand-alone and combination vaccines beginning in 2025. AstraZeneca’s USD 1.1 billion acquisition of Icosavax strengthens its advanced-platform credentials, dovetailing with a USD 50 billion U.S. manufacturing expansion that will add a Virginia plant dedicated to respiratory biologics. Regional firms in China, India, and South Korea are scaling fill-finish capacity and exploring microneedle delivery partnerships, further diluting incumbent dominance over the forecast horizon.

Intellectual-property cross-licensing gains prominence as patent cliffs loom. BioNTech’s GBP 1 billion, decade-long R&D collaboration with the U.K. government secures shared rights to emerging genomic and infectious-disease platforms, hedging against margin erosion in single-indication franchises. GSK, meanwhile, teamed with Flagship Pioneering on a USD 150 million discovery program targeting novel RNA modalities that could later feed combination shot pipelines. Competitive strategy thus centers on integrating platform breadth, manufacturing scale, and payer-aligned evidence to defend or win COVID-19 vaccine market share amid structural contraction.

COVID-19 Vaccine Industry Leaders

Pfizer Inc.

Moderna Inc.

AstraZeneca plc

Sinovac Biotech Ltd.

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

COVID-19 Vaccine Market Companies Covered in this Report

- Pfizer

- BioNTech

- Moderna

- AstraZeneca

- Johnson & Johnson

- Sinovac Biotech

- Sinopharm (CNBG)

- Serum Institute of India

- Bharat Biotech International Ltd.

- Novavax

- CanSino Biologics Inc.

- GlaxoSmithKline

- Sanofi

- Valneva

- Anhui Zhifei Longcom Biopharm.

- Clover Biopharmaceuticals

- Daiichi Sankyo Co., Ltd.

- CureVac N.V.

- SK Bioscience Co., Ltd.

- CSL Ltd. (Seqirus)

Recent Industry Developments in COVID-19 Vaccine Market

- July 2025: Sanofi acquired Vicebio for USD 1.15 billion to strengthen its vaccine pipeline in respiratory diseases.

- July 2025: AstraZeneca announced plans to construct its largest global manufacturing facility in Virginia as part of a USD 50 billion expansion strategy.

- June 2025: Moderna introduced mNEXSPIKE, a next-generation COVID-19 vaccine for older adults and high-risk individuals, employing lower antigen doses to enhance safety.

- May 2024: Novavax and Sanofi unveiled a USD 1.2 billion co-commercialization agreement for COVID-19 vaccines and next-generation flu-COVID combinations.

Global COVID-19 Vaccine Market Report Scope

Segmentation Overview

| mRNA Vaccines |

| Viral Vector Vaccines |

| Protein Subunit / VLP Vaccines |

| Inactivated Vaccines |

| DNA / Other Novel Platforms |

| Monovalent (Original) |

| Bivalent (Dual Strain) |

| Polyvalent / Multivalent |

| Pan-Coronavirus Candidates |

| Government Immunization Programs |

| Hospitals & Clinics |

| Retail & Chain Pharmacies |

| Occupational Health Centres & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology Platform | mRNA Vaccines | |

| Viral Vector Vaccines | ||

| Protein Subunit / VLP Vaccines | ||

| Inactivated Vaccines | ||

| DNA / Other Novel Platforms | ||

| By Valency | Monovalent (Original) | |

| Bivalent (Dual Strain) | ||

| Polyvalent / Multivalent | ||

| Pan-Coronavirus Candidates | ||

| By End User | Government Immunization Programs | |

| Hospitals & Clinics | ||

| Retail & Chain Pharmacies | ||

| Occupational Health Centres & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the COVID-19 vaccine market?

The COVID-19 vaccine market size reached USD 13.71 billion in 2025 and is projected to fall to USD 8.28 billion by 2030.

How fast is the COVID-19 vaccine market expected to shrink?

The market is forecast to decline at a -9.1% CAGR between 2025 and 2030 as universal mass vaccination ends.

Which platform holds the largest share today?

MRNA vaccines led with 54.7% COVID-19 vaccine market share in 2025 due to rapid variant update capabilities.

Why is Asia Pacific showing stronger stability than other regions?

Asia Pacific benefits from sustained public procurement, local manufacturing expansion, and relatively lower political resistance to vaccines, resulting in only a 3.7% CAGR decline.

What role will combination vaccines play going forward?

Influenza-COVID combination vaccines are advancing through late-stage trials and are expected to moderate volume erosion by integrating COVID boosters into existing respiratory immunization programs.

How concentrated is the competitive landscape?

The top five manufacturers hold a little over 60% of global revenue, giving the market a moderate concentration score of 6.

Page last updated on: