Reclaimed Lumber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

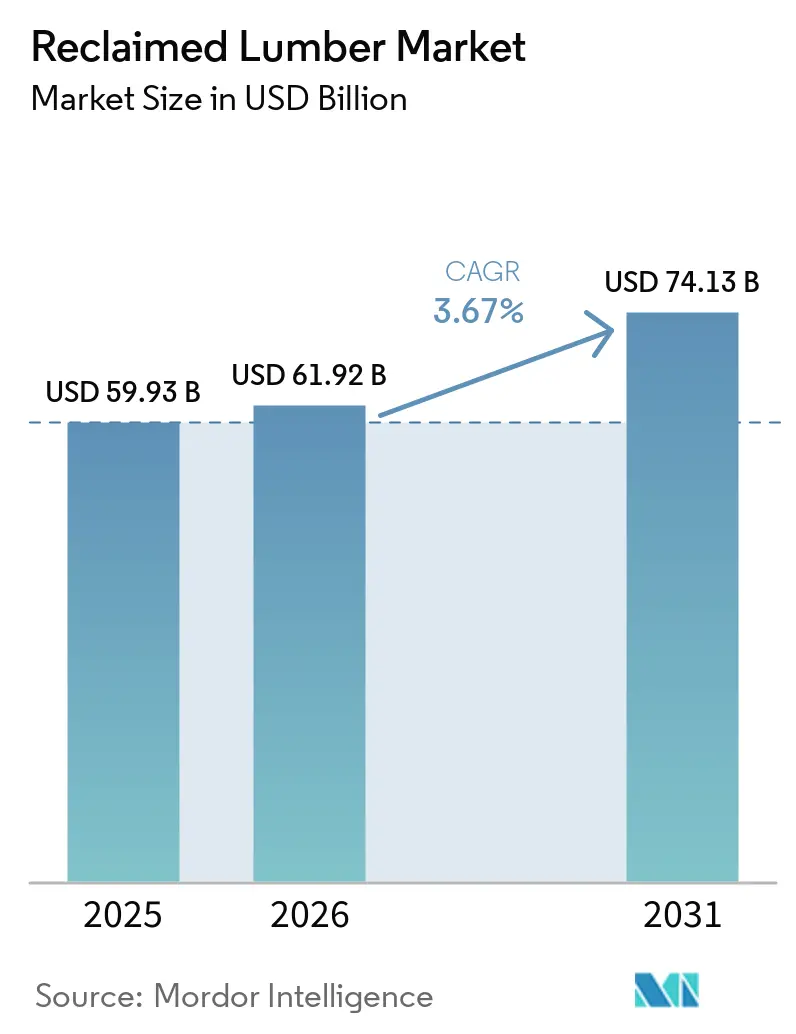

| Market Size (2026) | USD 61.92 Billion |

| Market Size (2031) | USD 74.13 Billion |

| Growth Rate (2026 - 2031) | 3.67% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Reclaimed Lumber Market Analysis by Mordor Intelligence

The Reclaimed Lumber Market size is expected to grow from USD 59.93 billion in 2025 to USD 61.92 billion in 2026 and is forecast to reach USD 74.13 billion by 2031 at 3.67% CAGR over 2026-2031. Mature demolition inventories and tightening deconstruction mandates are reshaping procurement, while carbon-accounting frameworks convert avoided embodied emissions into economic value. Japan's Circular Economy Promotion Law and lifecycle-carbon disclosure rules have driven a surge in demand. By the forecast period, commercial projects are projected to account for a dominant share, as hospitality and retail operators willingly pay significant price premiums for unique aesthetics and green credentials. While the competitive intensity remains moderate, the landscape is fragmented, with the top firms capturing a limited portion of the revenue. Notably, consolidation efforts have gained momentum, highlighted by Builders FirstSource's acquisition of Alpine Lumber and Cambium's successful funding to enhance artificial intelligence-driven logistics. White-space opportunities are emerging, particularly in mass-timber components and digitized chain-of-custody systems, ensuring compliance with Environmental Product Declaration mandates across multiple jurisdictions.

Key Report Takeaways

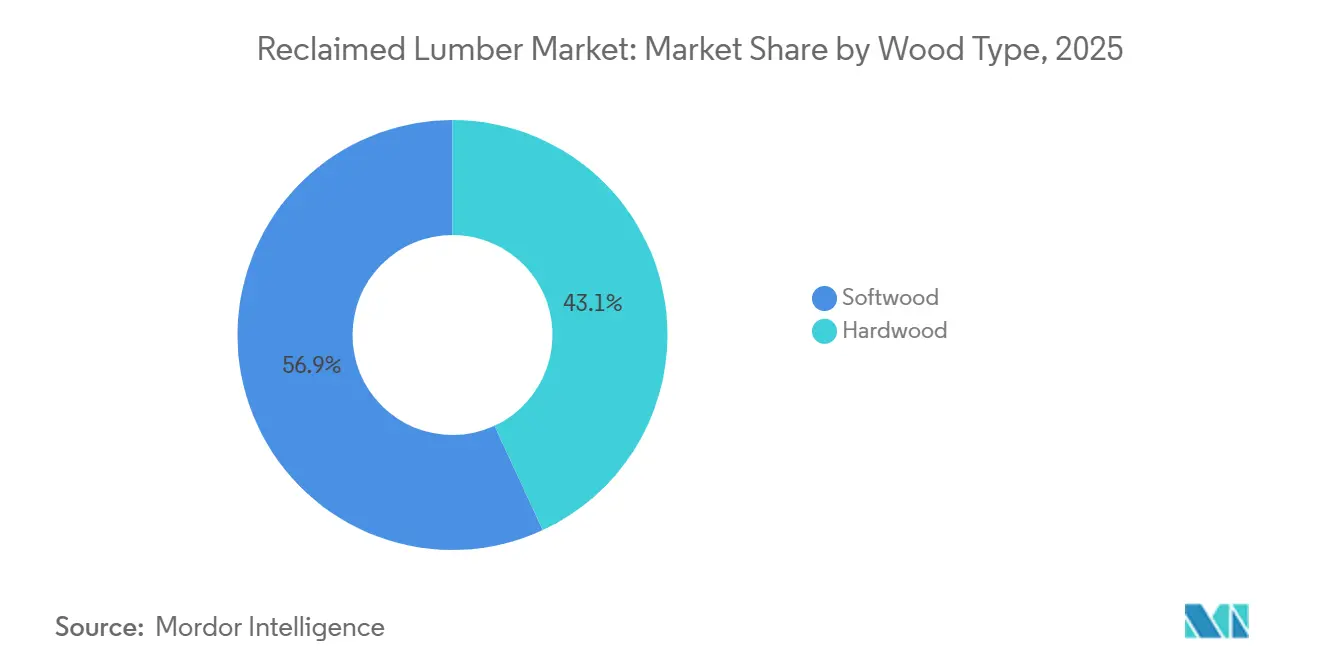

- By wood type, softwood held 56.90% global reclaimed lumber market share in 2025, while hardwood is forecast to register the fastest 4.44% CAGR between 2026 and 2031.

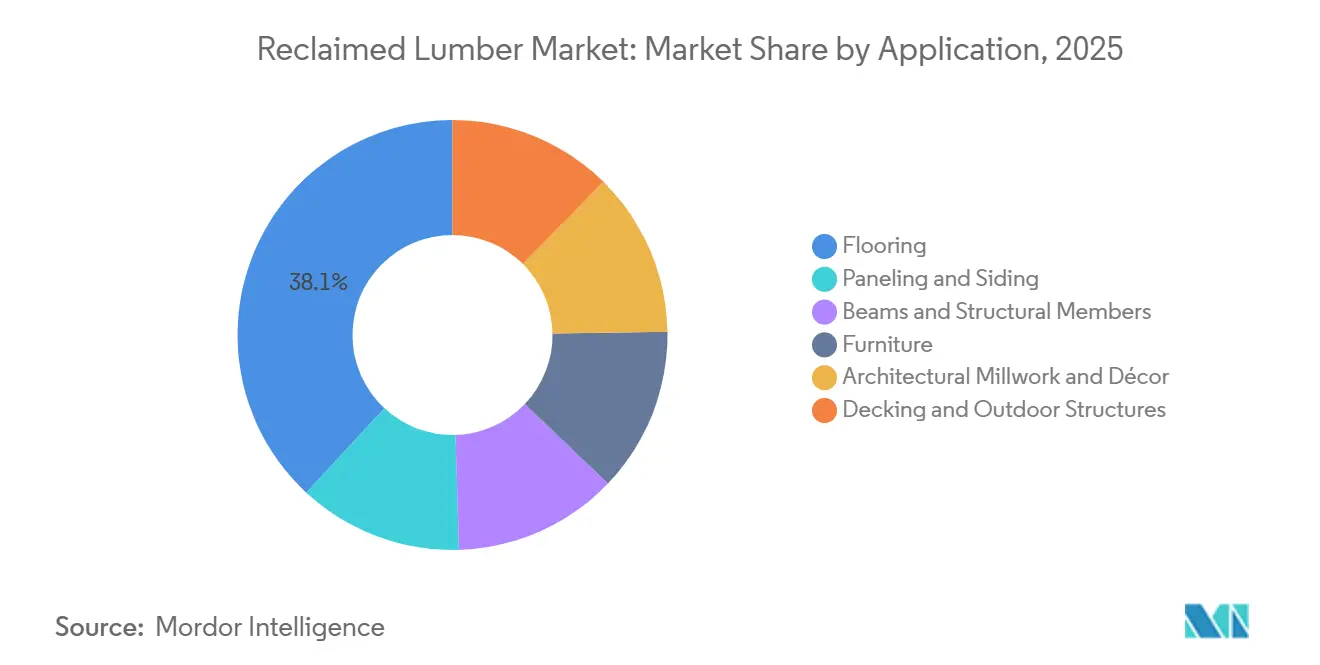

- By application, flooring accounted for 38.10% of the global reclaimed lumber market size in 2025 and is slated to post a 4.52% CAGR over 2026-2031.

- By end-user industry, commercial construction commanded 62.80% share in 2025; public and heritage restoration is projected to expand at a 4.67% CAGR between 2026 and 2031.

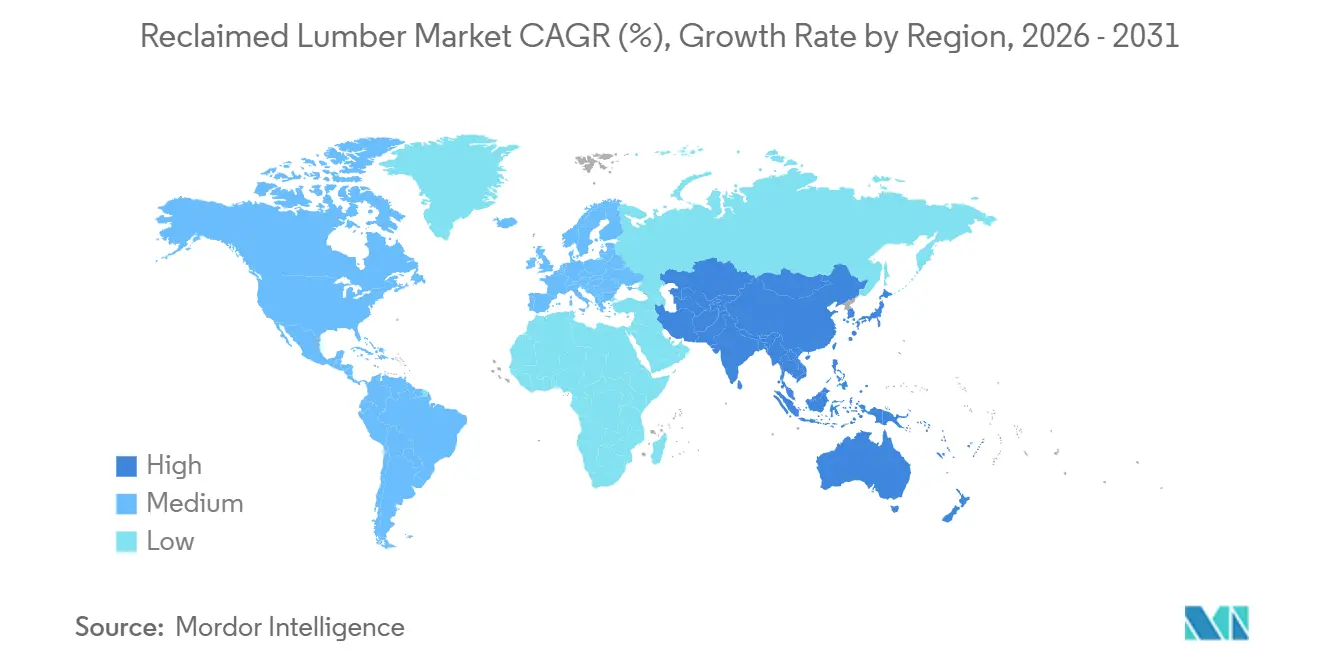

- By geography, Europe captured 37.30% of revenue in 2025, whereas Asia-Pacific is projected to advance at the highest 4.78% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Reclaimed Lumber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for sustainable construction materials | +1.20% | Global with clusters in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Rising interest in aesthetic and antique wood finishes | +0.70% | North America, Europe, and high-end projects in Asia-Pacific | Short term (≤2 years) |

| Increasing wood-waste management regulations | +0.90% | European Union, select US states, Japan | Long term (≥4 years) |

| Green-building certification incentives | +0.60% | Global, led by Leadership in Energy and Environmental Design (LEED) v5, Building Research Establishment Environmental Assessment Method (BREEAM), Green Star | Medium term (2-4 years) |

| AI-driven de-nailing and grading automation expanding supply | +0.50% | North America and Northern Europe are early adopters | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Sustainable Construction Materials

In eleven jurisdictions, including France's environmental regulations and Kenya's upcoming building code, lifecycle-carbon accounting has transitioned from a voluntary practice to a mandatory requirement for procurement [1]GlobalABC-UNEP, “Global Status Report for Buildings and Construction 2024/25,” globalabc.org. Studies referenced by Japan's Forestry Agency indicate that using reclaimed lumber can significantly reduce greenhouse gas emissions for entire buildings, provided the transport distance is kept within a reasonable range[2]林野庁, “木材産業の現状,” rinya.maff.go.jp . In Germany and France, public tenders are now evaluating bids based on their embodied-carbon intensity, giving an edge to those that can effectively translate carbon storage into bid advantages. Designs that replace steel or concrete with reclaimed wood can avoid high emission factors, enhancing the material's attractiveness. Builders lacking certification of provenance through Environmental Product Declarations face the risk of being sidelined from the rapidly expanding segment of institutional projects.

Rising Interest in Aesthetic and Antique Wood Finishes

In flagship hospitality projects, such as Equinox's Brooklyn Domino Sugar, interior designers are turning to "wood drenching." They blend weathered barn siding with polished concrete, showcasing flooring sourced from Cambium. In the United Kingdom, premium reclaimed oak and walnut are highly valued due to their genuine patinas and saw marks, which are difficult to replicate artificially. The once-favored Scandinavian herringbone layouts are making a comeback, driving up demand for narrow-width reclaimed boards. In a shift toward biophilic design standards, lighter matte finishes are now preferred over gloss coatings. Suppliers who curate their inventory based on species, age, and surface character are achieving higher margins, outpacing those who sell commodities.

Increasing Wood-Waste Management Regulations

Under the European Union's Waste Framework Directive, construction debris must be diverted from landfills. Meanwhile, Japan's Circular Economy Promotion Law mandates specific ratios for recycled materials. In the United States, King County (Washington), Massachusetts, Portland, and San Antonio have implemented deconstruction audits for older buildings, directing the resulting materials to certified processors. While subsidies in Japan help mitigate equipment costs, smaller operators face challenges with compliance expenses, such as lead-paint testing and traceability documentation. These challenges are driving many of them toward consolidation, often into larger, vertically integrated firms that have in-house laboratories.

Green-Building Certification Incentives

Pioneer Millworks received a significant grant from the Environmental Protection Agency to focus on documenting lifecycle impacts specific to their products. Leadership in Energy and Environmental Design (LEED) version 5, in a notable shift from version 4.1, now provides additional credits for third-party-verified Environmental Product Declarations. This change positions reclaimed lumber as a key asset for achieving higher certification levels, such as Gold or Platinum. Similarly, the Building Research Establishment Environmental Assessment Method (BREEAM), WELL Building Standard, and Australia's Green Star are encouraging reuse. As a result, uncertified competitors face increasing challenges, particularly as large-scale projects continue to prioritize proof of chain-of-custody.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited supply of high-quality reclaimed wood | -0.80% | Global, acute in Western Europe and the Eastern United States | Long term (≥4 years) |

| High cost and labor-intensive processing | -0.60% | Global, most severe in high-wage economies | Medium term (2-4 years) |

| Lack of global grading standards for structural reuse | -0.30% | Global | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Limited Supply of High-Quality Reclaimed Wood

The demolition of older structures containing old-growth lumber reached its peak in the past. As inventories dwindled, flows from the United Kingdom significantly decreased over the years. While heart pine and American chestnut have become highly valued, their scarcity persists, largely due to reforestation cycles that take several decades to complete. The practice of importing French oak into Britain, or sending United Kingdom stock to China for milling, not only contributes to freight emissions, thereby undermining environmental benefits, but also exposes buyers to the unpredictability of freight-rate fluctuations.

High Cost and Labor-Intensive Processing

Denailing requires a few minutes for each fastener, and since a single beam can conceal numerous nails, this adds several hours of labor before milling starts. With a significant yield loss, processors need to secure a larger quantity of raw stock to produce a smaller amount of finished boards. This requirement increases costs significantly. While retail prices for reclaimed flooring are considerably higher, virgin alternatives remain much cheaper. This price difference poses a challenge for widespread adoption. Although automation helps streamline the process, it cannot fully eliminate the labor inputs caused by product heterogeneity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Wood Type: Softwood Dominance Meets Hardwood Premiumization

Softwood commanded 56.90% global reclaimed lumber market share in 2025; salvaged Douglas fir and Southern yellow pine, sourced from warehouse teardowns, led the way. These species achieve an optimal moisture content suitable for interior installations, allowing for clean machining and maintaining a cost advantage. Hardwood, however, is forecast to grow at a 4.44% CAGR between 2026 and 2031. Reclaimed oak, walnut, and chestnut, celebrated for their antique patinas, are driving the surge in the global reclaimed lumber market. These woods, often unavailable in plantation forests, are leading the charge among wood types. A strategic move in this market involves engineered boards featuring thin hardwood veneers, maximizing surface area from limited stock. This tactic not only enhances the appeal of hardwood but also boosts its revenue share in the global reclaimed lumber market.

Designers are increasingly drawn to hardwood's intricate grain patterns, using them for feature walls, bar tops, and upscale retail shelving. In March 2025, Pioneer Millworks unveiled its Sunset Collection, specifically catering to restaurants in search of Forest Stewardship Council-certified engineered oak surfaces, complemented by eco-friendly, plant-based finishes. There is a growing preference for narrow-width planks, a choice that optimizes yield by extracting more boards from each salvaged beam. With automation reducing waste and blockchain technology enhancing provenance trust, hardwood prices are poised to maintain their premium, without narrowing the cost gap when compared to virgin exotic woods.

By Application: Flooring Leads, Furniture Surges

Flooring captured 38.10% of the global reclaimed lumber market size in 2025 and is projected to grow at 4.52% CAGR from 2026 to 2031, outpacing beams and paneling. Engineered planks compatible with underfloor heating transformed reclaimed stock from rustic niche to performance product. Herringbone and chevron layouts rose in popularity, and matte UV-cured finishes matched contemporary design palettes. Kiln drying guarantees dimensional stability, allowing hospitality chains and corporate offices to specify reclaimed floors without post-install movement risk.

Restaurant tables, hotel reception desks, and coworking communal benches are now telling sustainability stories to their guests. Specialty fabricators are embedding acoustic padding into these furnishings, effectively reducing ambient noise levels. This innovation addresses a common challenge faced by open-plan venues. While small-batch manufacturers are utilizing computer numerical control (CNC) engraving for branding, larger processors are turning to robotic sanding to handle increasing volumes. As commercial refits occur periodically, the share of furniture in the global reclaimed lumber market revenue is set to rise. This trend sees premium-priced pieces being recycled and transformed into fresh aesthetic statements.

By End-User Industry: Commercial Dominance, Residential Resilience

Commercial end-users accounted for 62.80% of market share in 2025, reflecting hospitality, retail, and corporate-office projects that absorb the 8-to-10-times cost premium over virgin lumber in exchange for differentiated aesthetics and sustainability storytelling. Equinox's Brooklyn Domino Sugar Building installed Cambium-supplied salvaged flooring, and restaurant chains specify reclaimed oak tables and walnut bar tops to create Instagram-ready interiors that drive foot traffic and brand differentiation. Residential applications, such as single-family homes, condominiums, and remodels, prioritize reclaimed flooring, accent walls, and ceiling beams, with demand concentrated in high-income coastal markets where sustainability credentials influence purchasing decisions. Industrial end-users deploy reclaimed timber for warehouse mezzanines, factory accent features, and office build-outs within manufacturing facilities, though volume remains modest relative to commercial and residential segments. Public and Heritage Restoration will grow at 4.67% CAGR from 2026 to 2031, the fastest among end-user categories, as government agencies and preservation societies restore historic buildings using period-appropriate reclaimed material to maintain architectural authenticity. Italy's systematic review of heritage-restoration projects documented the use of cross-laminated timber and fiber-reinforced polymer reinforcement to stabilize historic timber structures, techniques that extend service life while preserving original fabric.

Geography Analysis

Europe led the global reclaimed lumber market with a 37.30% revenue share in 2025. In the United Kingdom, Germany, France, and Italy, there is a notable blend of heritage preservation and established waste diversion mandates. Despite a decline in demolition volumes, premium pricing sustains the market's value; for instance, reclaimed flooring in the United Kingdom often commands high prices. In Germany, Hugo Kämpf offers Forest Stewardship Council (FSC) Recycled beams, reaching significant sizes. Meanwhile, Altholz Bayern's veneer slices are being utilized in adaptive-reuse projects, aiming for Building Research Establishment Environmental Assessment Method (BREEAM) or German Sustainable Building Council credits or German Sustainable Building Council credits. Within the European Union, cross-border transactions benefit from unified phytosanitary regulations. However, the lack of structural grading standards limits the use of beams in load-bearing applications.

Asia-Pacific will expand the fastest at 4.78% CAGR between 2026 and 2031. Japan's push for a circular economy, highlighted by its Circular Economy Promotion Law and a revamped Building Standards Act, is driving a surge in recycled wood usage. Domestic recycled wood circulation has been increasing, with a significant portion being utilized in construction. Misawa Homes introduced its M-Wood2, a blend of waste wood and plastics, with deliveries starting in August 2025. While Yamagen has been processing substantial amounts of industrial wood waste, the company is focusing on consolidating operations to improve efficiency. Despite facing fragmented supply chains, urban Tier 1 cities in China and India are increasingly opting for reclaimed flooring in their premium office towers, signaling a growth opportunity for regional processors.

North America is set for consistent growth, bolstered by initiatives like Leadership in Energy and Environmental Design (LEED) version 5 and new deconstruction mandates in states such as Massachusetts, Washington, and Oregon. Annandale Millwork's expansion in Virginia not only creates new jobs but also injects additional investment into local forest product purchases. Cambium, having processed a significant volume of salvaged wood, is channeling its recent funding into a foray into mass timber. While Canada and Mexico are still in the early stages, they stand poised to capitalize on cross-border flows of Douglas fir, contingent on the maturation of logistical corridors.

Competitive Landscape

The Reclaimed Lumber Market is moderately fragmented. Pioneer Millworks is utilizing a significant grant from the Environmental Protection Agency to develop Environmental Product Declarations, thereby boosting its appeal in Leadership in Energy and Environmental Design projects. Montana Reclaimed Lumber's operational efficiency has led to a throughput increase, resulting in notable annual savings on a modest capital outlay. However, smaller mills face challenges; those unable to finance certification audits or artificial intelligence scanners may see their margins shrink, especially as buyers increasingly demand Forest Stewardship Council Recycled or Truly Reclaimed labels.

Reclaimed Lumber Industry Leaders

Elmwood Reclaimed Timber

Longleaf Lumber Inc.

Carpentier

TerraMai

Pioneer Millworks

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Stora Enso showcased its circular approach to manufacturing high-performance Cross-Laminated Timber (CLT) panels using reclaimed timber, detailing processes and addressing challenges to ensure structural integrity and promote sustainable construction practices.

- February 2025: Cambium has raised USD 18.5 million in a Series A funding round to enhance its wood supply chain platform and introduce sustainable timber products. This initiative is likely to drive innovation and expand sustainable practices in the reclaimed lumber market.

Global Reclaimed Lumber Market Report Scope

Reclaimed lumber is wood salvaged from old buildings, barns, factories, or other structures and repurposed for new projects. Instead of being discarded, it is cleaned, processed, and reused, often prized for its durability, unique character, and environmental benefits. This sustainable practice reduces waste, preserves history, and provides distinctive materials for furniture, flooring, and construction, blending rustic charm with eco-conscious design.

The Reclaimed Lumber Market is segmented by wood type, application, end-user industry, and geography. By wood type, the market is segmented into softwood and hardwood. By application, the market is segmented into flooring, paneling and siding, beams and structural members, furniture, architectural millwork and décor, decking and outdoor structures. By end-user industry, the market is segmented into residential, commercial, industrial, public and heritage restoration. The report also covers the market size and forecasts for the Reclaimed Lumber Market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Softwood |

| Hardwood |

| Flooring | |

| Paneling and Siding | |

| Beams and Structural Members | |

| Furniture | Residential Furniture |

| Commercial and Hospitality Furniture | |

| Architectural Millwork and Décor | |

| Decking and Outdoor Structures |

| Residential |

| Commercial |

| Industrial |

| Public and Heritage Restoration |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle-East and Africa |

| By Wood Type | Softwood | |

| Hardwood | ||

| By Application | Flooring | |

| Paneling and Siding | ||

| Beams and Structural Members | ||

| Furniture | Residential Furniture | |

| Commercial and Hospitality Furniture | ||

| Architectural Millwork and Décor | ||

| Decking and Outdoor Structures | ||

| By End-user Industry | Residential | |

| Commercial | ||

| Industrial | ||

| Public and Heritage Restoration | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the reclaimed lumber market?

The reclaimed lumber market stands at USD 61.92 billion and is forecast to reach USD 74.13 billion by 2031 at a 3.67% CAGR from 2026 to 2031.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is projected to post the highest 4.78% CAGR, driven by Japan’s Circular Economy Promotion Law and stricter lifecycle-carbon disclosure rules.

What segment currently generates the most revenue?

Flooring led with 38.10% of 2025 application revenue and is expected to grow at a 4.52% CAGR as engineered planks meet underfloor-heating and herringbone standards.

Why do commercial builders favor reclaimed lumber despite higher prices?

Hospitality and retail projects accept an 8-to-10-times cost premium because reclaimed wood delivers unique aesthetics and helps secure Leadership in Energy and Environmental Design (LEED) or Building Research Establishment Environmental Assessment Method (BREEAM) certification credits.

What is the main supply-side challenge?

Western Europe and the Eastern United States are experiencing a decline in the availability of older demolition wood, which restricts access to high-quality feedstock and hampers long-term growth potential.

Page last updated on: