Recycled Carbon Fiber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

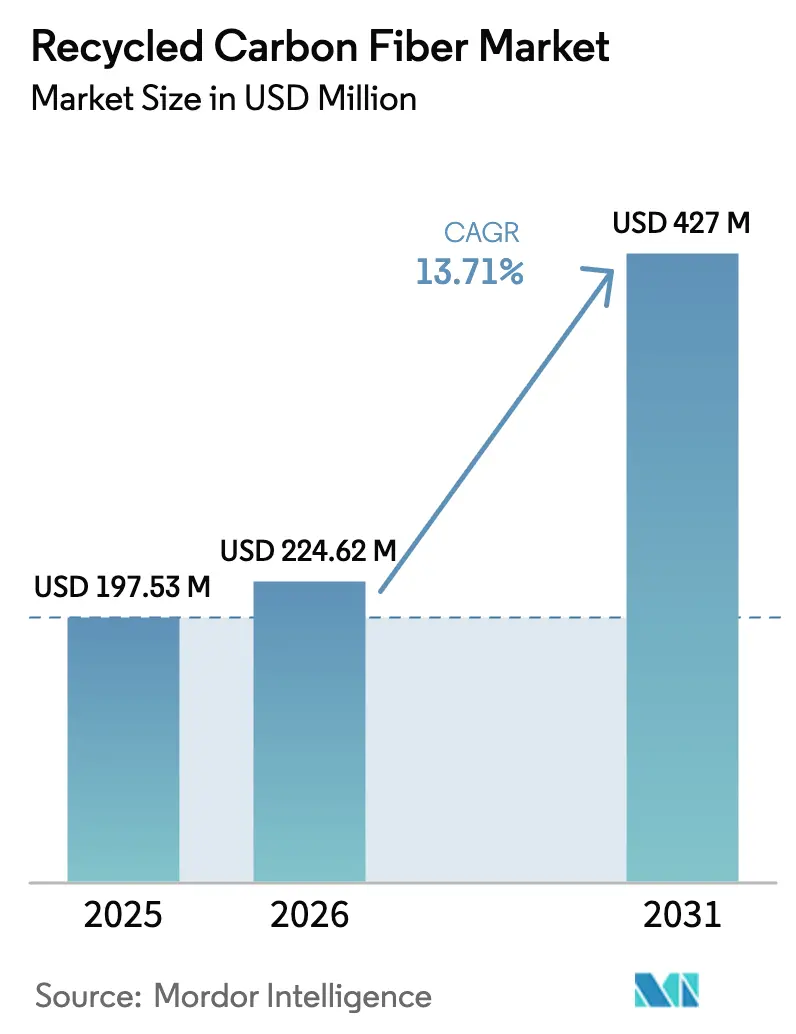

| Market Size (2026) | USD 224.62 Million |

| Market Size (2031) | USD 427 Million |

| Growth Rate (2026 - 2031) | 13.71% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recycled Carbon Fiber Market Analysis by Mordor Intelligence

The Recycled Carbon Fiber Market size was valued at USD 197.53 million in 2025 and is estimated to grow from USD 224.62 million in 2026 to reach USD 427 million by 2031, at a CAGR of 13.71% during the forecast period (2026-2031). Demand is rising as aerospace and automotive manufacturers race to cut embodied carbon while safeguarding the stiffness-to-weight ratio that virgin fiber provides. Chopped grades dominate because they drop straight into injection and compression molding lines already qualified for glass fiber. At the same time, energy-positive pyrolysis plants are driving processing costs below USD 8 per kilogram and pushing recycled carbon fiber market adoption into high-volume platforms. Net-zero commitments, Extended Producer Responsibility rules, and decommissioned wind-turbine blades are converging to secure a predictable scrap supply that tempers price volatility and underpins multi-year offtake contracts with OEMs.

Key Report Takeaways

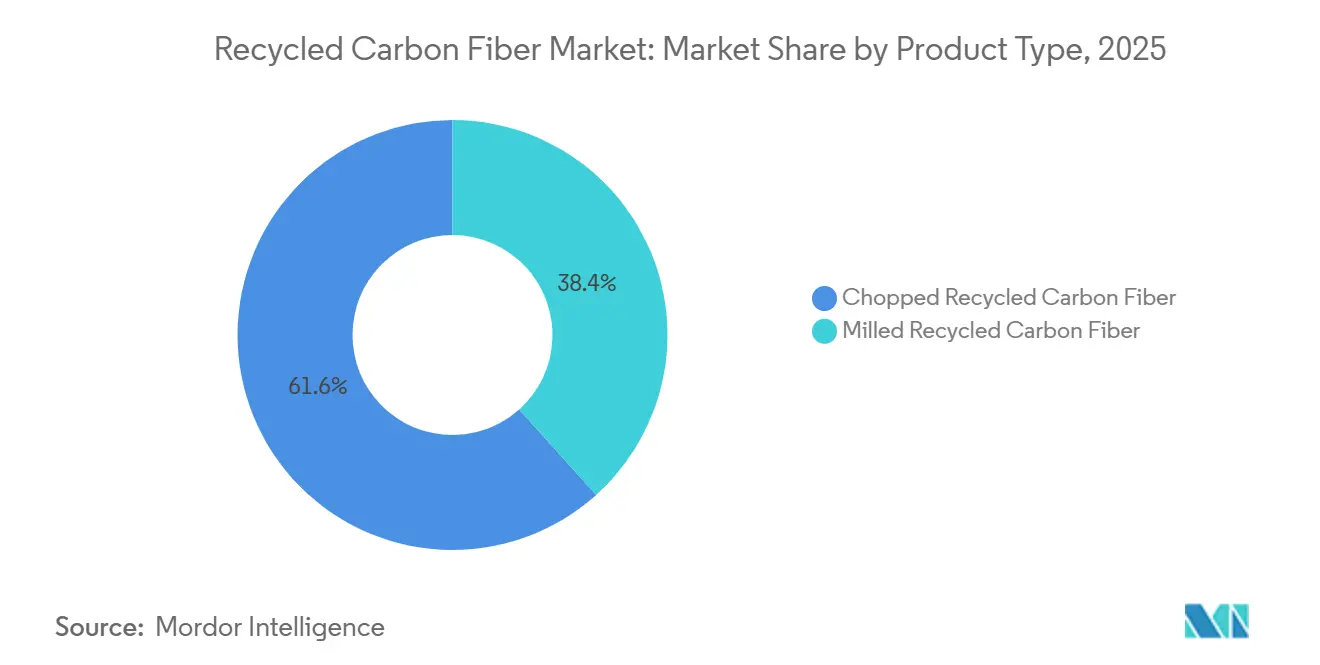

- By product type, chopped recycled carbon fiber led with 61.65% revenue share in 2025 and is forecast to expand at a 13.91% CAGR through 2031.

- By source, aerospace scrap captured 45.82% of the recycled carbon fiber market share in 2025, and the same segment is projected to grow at a 14.44% CAGR through 2031.

- By the recycling process, pyrolysis controlled 70.45% of the market in 2025, while solvolysis records the highest projected CAGR at 15.66% to 2031.

- By matrix, thermoset composites accounted for 67.29% of the recycled carbon fiber market size in 2025; thermoplastic composites are advancing at a 15.08% CAGR through 2031.

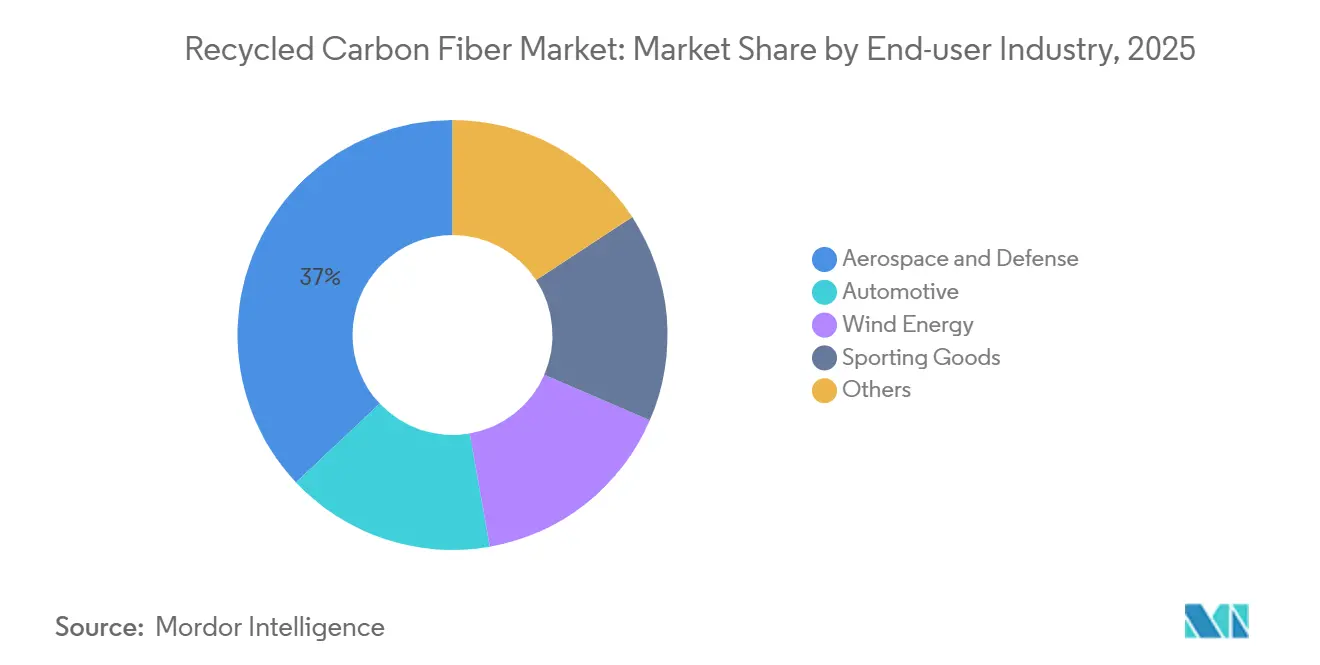

- By end-user industry, aerospace and defense dominated with a 37.01% share in 2025; automotive is expected to post the fastest 14.82% CAGR to 2031.

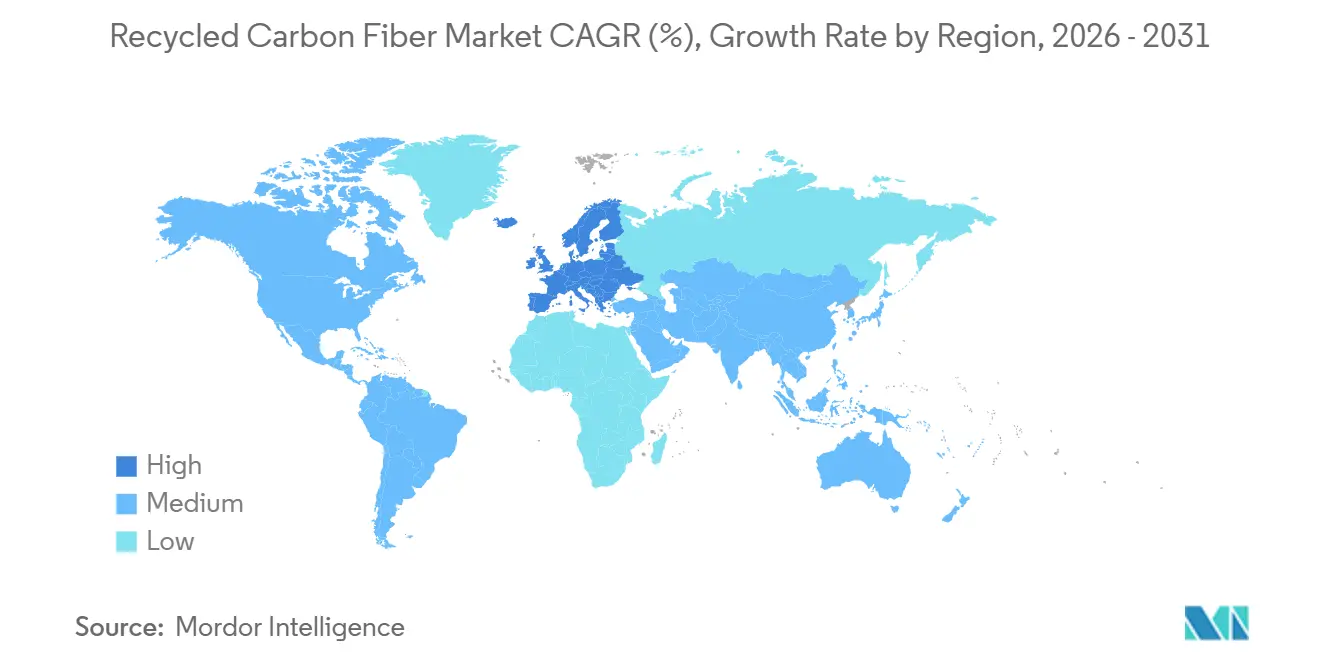

- By region, North America held a 38.15% share in 2025; Europe is poised to expand at a 14.99% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Recycled Carbon Fiber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Circular-economy mandates in Europe and America | +2.8% | Europe (Germany, France, UK), North America (US, Canada) | Medium term (2-4 years) |

| OEM net-zero targets boosting rCF content in EVs | +3.2% | Global, with concentration in Europe and North America | Long term (≥ 4 years) |

| End-of-life wind-turbine blades creating high-grade scrap | +2.1% | Europe (Nordic countries, Germany, Spain), North America | Medium term (2-4 years) |

| Accelerating aircraft retirements in Asia-Pacific unlocking aerospace scrap | +2.5% | Asia-Pacific (China, Japan, South Korea), spill-over to North America | Short term (≤ 2 years) |

| Break-even cost parity as energy-positive pyrolysis plants scale | +3.1% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Circular-Economy Mandates in Europe and America

Extended Producer Responsibility directives are forcing composite producers to finance take-back schemes. The EU Waste Framework Directive, revised in 2024, requires a 30% recycling rate for carbon-fiber composites by 2030, and Germany’s VerpackG collects a EUR 120 per-ton levy on non-compliant products. In the United States, California Senate Bill 54 compels manufacturers to close the loop on 25% of carbon-fiber content by 2028. These measures raise landfill tipping fees to EUR 95 per ton in Western Europe, tilting the cost equation in favor of certified recyclers. As a result, processors report a 40% jump in long-term scrap-supply contracts since Q4 2025[1]European Commission, “Waste Framework Directive 2024 Revision,” europa.eu.

OEM Net-Zero Targets Boosting rCF Content in EVs

Automakers are embedding recycled carbon fiber into battery enclosures and body-in-white parts to hit Scope 3 goals. BMW’s iX uses 15% recycled carbon fiber, trimming embodied carbon by 2.3 kg CO₂-eq per vehicle, while Mercedes-Benz plans 40% recycled composite across EQ models by 2030. Tesla’s Berlin plant started underbody shield trials with chopped recycled carbon fiber sourced from a local pyrolysis operator that processes aerospace scrap. Recycled grades command USD 18 per kilogram, a 35% discount to virgin tow, making them cost-competitive with aluminum extrusions when tooling consolidation is factored in[2]BMW Group, “Sustainability Report 2025,” bmwgroup.com.

End-of-Life Wind-Turbine Blades Creating High-Grade Scrap

Europe’s first-generation onshore turbines are entering decommissioning, yielding 45,000 t of blade waste annually through 2026. Vestas and Siemens Gamesa teamed with ReFiber to open a 12,000 t solvolysis plant in Denmark, achieving 90% fiber yield and lengths suited to automotive compression molding. Germany earmarked EUR 50 million in 2025 for regional dismantling hubs, lowering transport costs for remote turbines. Blade skins use unidirectional carbon plies, so post-pyrolysis fiber retains more than 85% of virgin tensile strength, attracting compounders that supply structural brackets to European EV platforms.

Accelerating Aircraft Retirements in Asia-Pacific Unlocking Aerospace Scrap

Asia-Pacific airlines retired over 320 wide-body jets in 2025, releasing high-modulus scrap into the recycling chain. China’s aviation regulator now requires that 50% of composite waste flow to certified recyclers by 2027, guaranteeing feedstock volumes. Mitsubishi Chemical raised capacity at Toyohashi to process 1,800 t of fuselage scrap annually, supplying sporting goods and auto customers that prize 250 GPa modulus fibers. South Korea’s Korean Air joint venture dismantles 777 airframes and exports chopped fiber to US compounders, capturing a USD 12 per-kg margin over landfill.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of substitute lightweight materials (Al, Mg, GF) | -1.9% | Global, with higher impact in cost-sensitive automotive segments | Medium term (2-4 years) |

| Fragmented scrap-collection logistics | -1.4% | North America, Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Variable fiber-length distribution impacting quality control | -1.2% | Global, particularly affecting automotive and sporting goods | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of Substitute Lightweight Materials

Aluminum, magnesium, and glass fiber still undercut recycled carbon fiber on price in cost-sensitive automotive programs. Aluminum 6000-series extrusions stood at USD 4.20 per kilogram in 2025, roughly one-fifth of recycled carbon fiber. Magnesium die-castings grew 18% in North America last year, filling EV battery-enclosure orders once earmarked for composites. Glass-fiber sheet-molding compounds at USD 2.80 per kilogram satisfy crash-energy needs in non-structural panels, limiting recycled carbon fiber market penetration to parts where its 40% density advantage offsets the premium. The substitution threat is magnified in Asia, where lifecycle-carbon metrics carry less weight in sourcing decisions.

Fragmented Scrap-Collection Logistics

Lack of standardized collection networks inflates transport costs and introduces contamination that devalues scrap. A 2025 industry survey found 60% of European carbon-fiber off-cuts still enter municipal waste streams, with average haul distances topping 450 km. North American aerospace scrap often travels over 1,200 km to reach Midwest pyrolysis plants, adding USD 50 per ton in freight and eroding recycled carbon fiber market economics. Small sporting goods makers generate sub-50 t volumes that are too costly to consolidate, steering material to landfills. Asia-Pacific faces similar issues as airframe teardowns outpace collection infrastructure, driving 25% rejection rates at recyclers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chopped Grades Sustain Lead While Milled Grades Nudge Up

Chopped fiber commanded 61.65% of the recycled carbon fiber market share in 2025 and is projected to climb at a 13.91% CAGR, reinforcing its status as the go-to reinforcement for injection and compression molding. Most pyrolysis lines naturally produce 3–12 mm fibers that flow easily in thermoplastic compounds, allowing automotive tier-ones such as Magna to cut 15–20% weight versus glass-fiber parts without retooling.

Milled fiber remains a niche, feeding coatings, adhesives, and 3D-printing filaments that value uniform dispersion over tensile performance. Growth depends on additive-manufacturing demand and on solvolysis breakthroughs that can deliver longer fibers suitable for semi-structural parts. If 15–25 mm retention scales, chopped fiber may face stiffer competition, particularly in battery-enclosure ribs where designers seek higher modulus without continuous-fiber lay-up.

By Source: Aerospace Scrap Maintains Quality Premium

Aerospace scrap delivered 45.82% of feedstock and will grow at a 14.44% CAGR through 2031, buoyed by Asia-Pacific fleet retirements and steady trimming waste from Boeing’s 787 and Airbus A350 lines. Aerospace prepregs carry resin contents below 35%, which raises fiber yield above 92% after pyrolysis and justifies a 25–30% price premium.

Automotive and wind-energy scrap offer higher tonnage but lower purity, saddling recyclers with pre-processing to strip contaminants. Blade waste will rise sharply as European turbines reach end-of-life, creating volume but challenging small operators that lack high-temperature pyrolysis or solvolysis lines. Sporting goods scrap is dispersed and small-batch, though brand take-back programs initiated in 2025 could improve aggregation over the forecast period.

By Recycling Process: Pyrolysis Dominates, Solvolysis Gains Momentum

Pyrolysis held a 70.45% share in 2025, thanks to its versatility with thermoset scrap and its maturing cost profile. Gen 2 Carbon’s Lake City plant runs at 14.2 MWh per ton, recovering 90% fiber yield and supplying automotive customers at USD 7.20 per kilogram.

Solvolysis, though smaller, will outpace with a 15.66% CAGR as operators like Mitsubishi Chemical prove 50 mm fiber-length retention and 95% tensile-strength preservation using lower-temperature solvent systems. Mechanical shredding keeps a foothold in conductive fillers and bulk-molding compounds but will cede share as customers demand higher structural performance at marginally higher price points.

By Matrix Compatibility: Thermoset Share Mirrors Installed Base

Thermoset composites accounted for 67.29% of the recycled carbon fiber market size in 2025, reflecting the epoxy dominance in aerospace and wind applications. Pyrolysis easily strips cured resin, yet re-impregnation adds a compounding step that raises total part cost, limiting uptake in price-sensitive brackets.

Thermoplastic demand will rise at a 15.08% CAGR as EV makers exploit the re-melt capability that enables genuine closed-loop recycling. BMW demonstrated that polyamide-6 battery enclosures granulated at end-of-life can be injection-molded into new parts without property loss, smoothing the path to mass-volume adoption and broadening recycled carbon fiber market appeal beyond niche programs.

By End-User Industry: Automotive Emerges as Growth Engine

Aerospace and defense retained 37.01% of 2025 revenue by leveraging recycled carbon fiber in cabin interiors, cargo liners, and non-primary structures cleared by regulators in 2024. Certification cycles and long aircraft lifespans temper rapid volume shifts, but maintenance, repair, and overhaul scrap keeps supply predictable.

Automotive will grow at a 14.82% CAGR through 2031 as EV platforms chase every kilogram saved to extend range. Mercedes-Benz’s EQS sedan integrates recycled carbon fiber in its front-end carrier, cutting 8 kg and 18 kg CO₂-eq per unit. Sporting goods and consumer electronics remain small but steady, tapping recycled fiber for environmental branding and modest weight reduction.

Geography Analysis

North America led with 38.15% revenue in 2025, underpinned by aerospace hubs that feed high-grade scrap and federal tax credits that subsidize new recycling capacity. Boeing diverted 68% of its composite waste to recyclers, and the US Department of Energy granted USD 85 million to co-fund pyrolysis and solvolysis projects, accelerating the transition away from mechanical shredding. Canada’s tier-one suppliers started molding recycled carbon fiber battery trays, while Mexico’s aerospace cluster funnels production off-cuts into US furnaces.

Europe is on track for a 14.99% CAGR as Extended Producer Responsibility rules bite and blade decommissioning accelerates. Germany expanded pyrolysis capacity to 18,000 t per year, France forged closed-loop supply chains for EV parts, and the UK demonstrated solvolysis fiber suitable for Airbus cabin partitions. Nordic nations monetize blade waste by exporting chopped fiber to Italian and German compounders, while Spain scales sporting-goods recycling around bicycle hubs.

Asia-Pacific sits at the nexus of scrap generation and demand. China’s draft standards for recycled carbon fiber in rail and auto parts, Japan’s 35% capacity hike, and South Korea’s qualification of recycled grades for the Ioniq 6 underpin regional momentum. However, fragmented collection and limited processing capacity in Southeast Asia and India delay full-scale deployment, creating white-space for new entrants that can aggregate scrap across borders.

Competitive Landscape

The Recycled Carbon Fiber market shows moderate concentration. Technology leadership is tightening competitive gaps. Vartega’s energy-positive plant sells 1.8 MWh surplus electricity per ton into Colorado’s grid, while Carbon Fiber Remanufacturing filed a two-stage pyrolysis patent that restores surface energy via plasma treatment, chasing tensile properties near virgin T700. White-space persists in thermoplastic-composite recycling and additive manufacturing. Start-ups are developing bio-based resins that simplify end-of-life separation, and digital platforms are emerging to coordinate scrap pickups, lowering rejection rates.

Recycled Carbon Fiber Industry Leaders

Carbon Conversions

Gen 2 Carbon Limited

TORAY INDUSTRIES, INC.

Mitsubishi Chemical Group Corporation

SGL Carbon

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Toray Industries, Inc. unveiled a groundbreaking recycling technology capable of decomposing various carbon fiber reinforced plastics (CFRP) derived from thermosetting resins. Notably, this process preserves both the strength and surface quality of the fibers. Leveraging this innovation, Toray produced a nonwoven fabric crafted from recycled carbon fibers.

- March 2025: In Imola, Italy, the Hera Group launched FIB3R, a facility focused on the industrial-scale recycling of carbon fiber composites. Currently, FIB3R aims to produce 160 tonnes of recycled carbon fiber (rCF) annually, achieving a notable 75% energy savings compared to traditional virgin fiber.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the recycled carbon fiber (rCF) market as the global trade of post-industrial or post-consumer carbon fiber that is reclaimed through physical, thermal, or chemical processes and resold in chopped, milled, or mat form for use in composites, textiles, and allied applications. The valuation covers only revenue generated from the first sale of rCF into end-use industries across automotive, aerospace and defense, wind energy, sporting goods, and other niche sectors.

Scope exclusion: fibers recovered as furnace ash, carbon black derived additives, and any reuse of un-cured prepreg scrap are not counted within this study.

Segmentation Overview

- By Product Type

- Chopped Recycled Carbon Fiber

- Milled Recycled Carbon Fiber

- By Source

- Aerospace Scrap

- Automotive Scrap

- Other Sources

- By Recycling Process

- Pyrolysis

- Solvolysis / Chemical Recycling

- Mechanical Shredding and Milling

- By Matrix Compatibility

- Thermoset Composites

- Thermoplastic Composites

- By End-user Industry

- Automotive

- Aerospace and Defense

- Wind Energy

- Sporting Goods

- Others

- By Geography

- Asia

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordic Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle-East and Africa

- Asia

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interview recycling plant managers, aerospace material buyers, and tier-one auto suppliers in North America, Europe, and East Asia, using structured questionnaires to validate scrap availability, conversion yields, and realistic average selling prices. Follow-up surveys with composite compounders test demand growth assumptions and reveal substitution thresholds versus virgin fiber.

Desk Research

In desk work, we tap freely available yet authoritative datasets such as Eurostat's End-of-Life Vehicle statistics, United States EPA solid-waste tables, UN Comtrade trade codes for carbon scrap, and IEA tallies of wind-turbine retirements. Industry associations, for example, the Carbon Fiber Circular Alliance or the American Composites Manufacturers Association, provide technical papers on scrap yields, while academic journals offer process-yield coefficients. Company 10-Ks, investor decks, and patent filings complement these public sources and help our team benchmark pricing spreads. Select paid databases like D&B Hoovers for financials and Questel for patent intensity round out the evidence base. This list is illustrative; many additional references are screened to cross-check every datapoint.

Market-Sizing & Forecasting

The market value baseline starts with a top-down reconstruction that multiplies region-wise scrap generation (tons) by realistic recovery rates and average selling prices, which are then adjusted with import-export balances. Results are corroborated with selective bottom-up checks, sampled recycler revenues and compounder procurement volumes, before the figures are finalized. Key variables inside the model include aircraft retirements per year, end-of-life wind-blade tonnage, average rCF price discount to virgin fiber, penetration of rCF in under-hood automotive parts, and regional landfill fees that influence recycling economics. Forecasts use multivariate regression blended with scenario analysis to sense-test how policy shifts or commodity-price swings might nudge demand.

Data Validation & Update Cycle

Model outputs pass through variance scans against independent scrap pricing curves, peer market ratios, and historical trajectories. Senior reviewers sign off only after anomalies are resolved. We refresh the dataset every twelve months, with interim revisions triggered by large plant start-ups, policy mandates, or step changes in fiber pricing.

Why Mordor's Recycled Carbon Fiber Baseline Earns Trust

Published estimates differ because analysts may select unlike product mixes, apply varying discount curves, or roll forecasts less frequently. By anchoring on physically observable scrap flows and calibrating yields with field interviews, our baseline stays transparent and replicable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 197.63 million (2025) | Mordor Intelligence | - |

| USD 179.44 million (2025) | Regional Consultancy A | Excludes milled rCF grades and wind-energy uptake |

| USD 160.00 million (2025) | Global Consultancy A | Counts only automotive and industrial uses; omits Asia scrap flows |

| USD 193.00 million (2024) | Trade Journal B | Uses generic fiber price proxy without process-yield adjustments |

These contrasts show that when scope, unit pricing, and refresh cadence vary, totals drift. Mordor's disciplined variable list, annual refresh, and dual validation steps give decision-makers a balanced, dependable point of reference.

Key Questions Answered in the Report

How large is the recycled carbon fiber market in 2026?

How large is the recycled carbon fiber market in 2026?

Which end-user sector is growing fastest for recycled carbon fiber?

Which end-user sector is growing fastest for recycled carbon fiber?

Why does aerospace scrap command a premium?

Why does aerospace scrap command a premium?

Which recycling process is gaining share over the forecast period?

Which recycling process is gaining share over the forecast period?

Page last updated on: