Cross Laminated Timber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

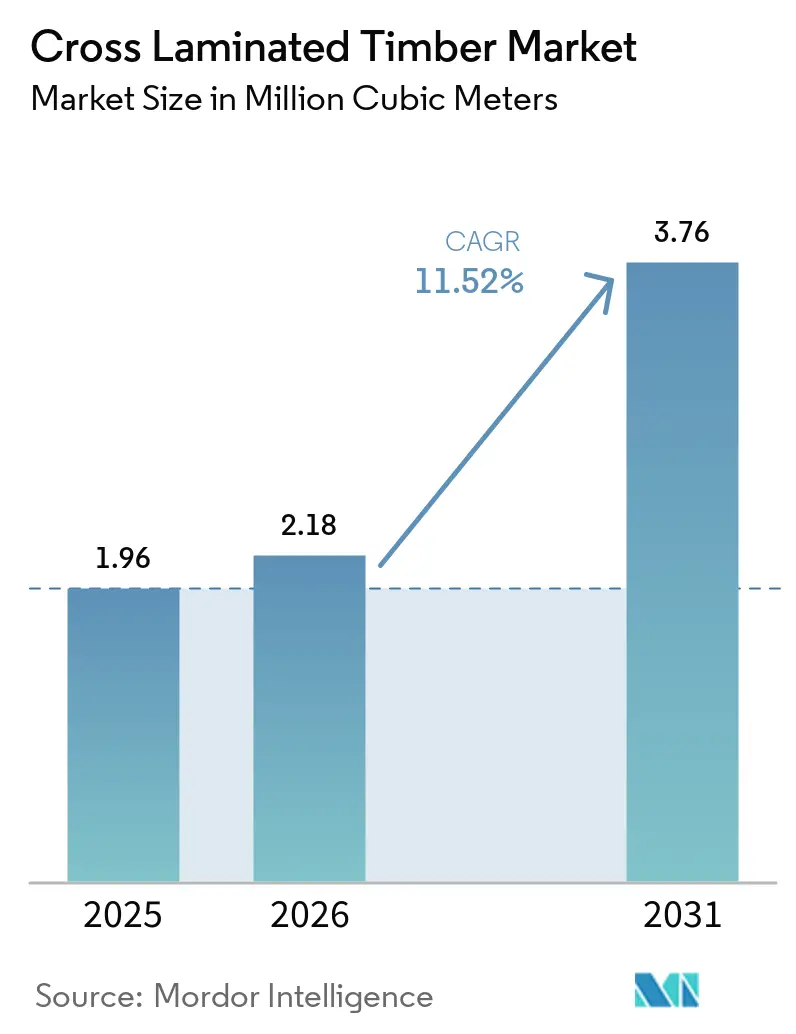

| Market Volume (2026) | 2.18 Million cubic meters |

| Market Volume (2031) | 3.76 Million cubic meters |

| Growth Rate (2026 - 2031) | 11.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

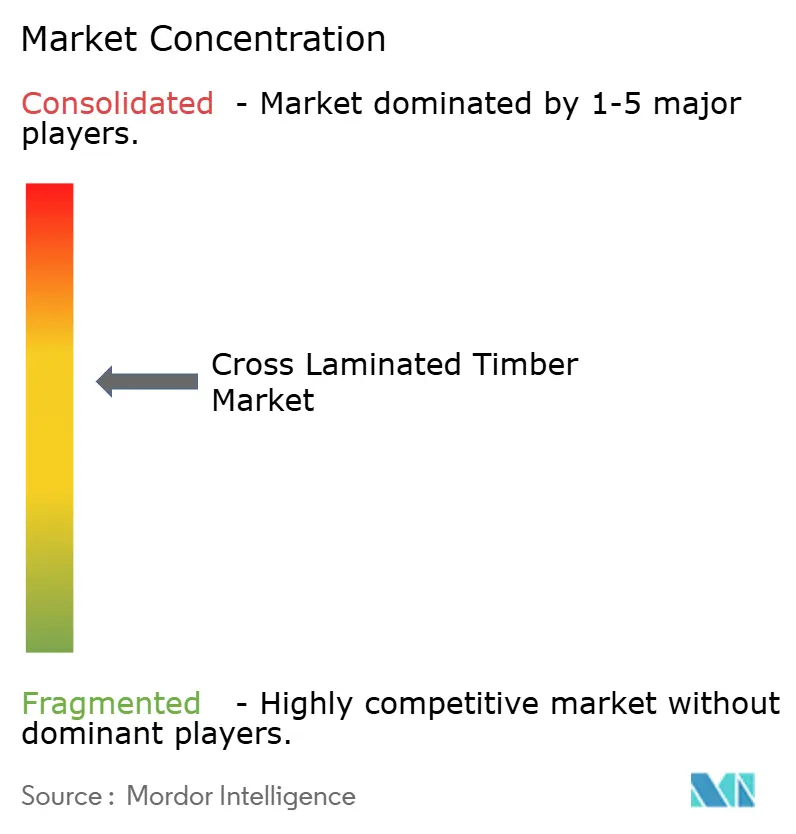

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cross Laminated Timber Market Analysis by Mordor Intelligence

The Cross Laminated Timber Market size is projected to expand from 1.96 Million cubic meters in 2025 and 2.18 Million cubic meters in 2026 to 3.76 Million cubic meters by 2031, registering a CAGR of 11.52% between 2026 to 2031. Developers are shifting toward bio-based structural systems as the European Union’s carbon-removal certification and North America’s Buy Clean mandates reward low-embodied-carbon procurement. Fabricators with digitized design-for-manufacture platforms now deliver project-specific life-cycle assessments in under three days, compressing bid cycles and widening adoption. North American mills capitalize on Douglas-fir’s higher density to serve seismic markets, while European incumbents scale capacity through vertical forest-to-fabrication integrations. Headline risks include feedstock cost spikes, moisture-driven durability challenges, and the still-limited universe of fire-rated adhesive chemistries that meet Annex B char-rate tests.

Key Report Takeaways

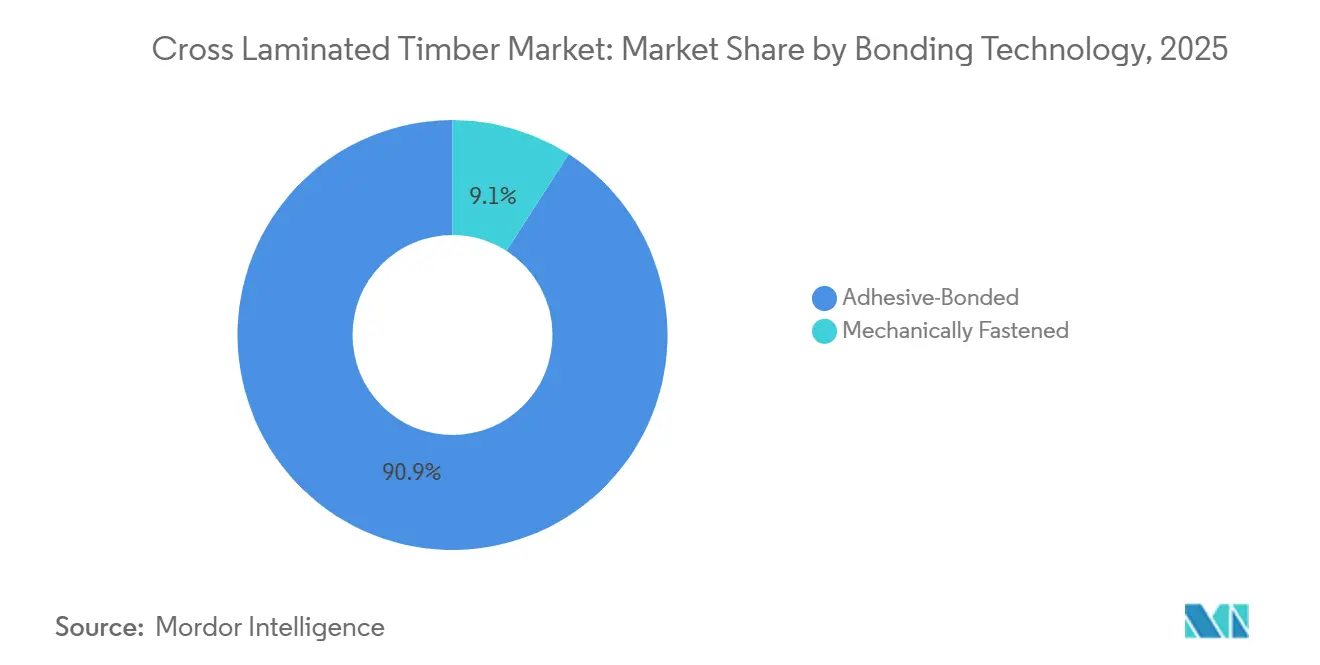

- By bonding technology, adhesive-bonded commanded 90.91% cross laminated timber market share in 2025 and is forecast to expand at a 12.16% CAGR through 2031.

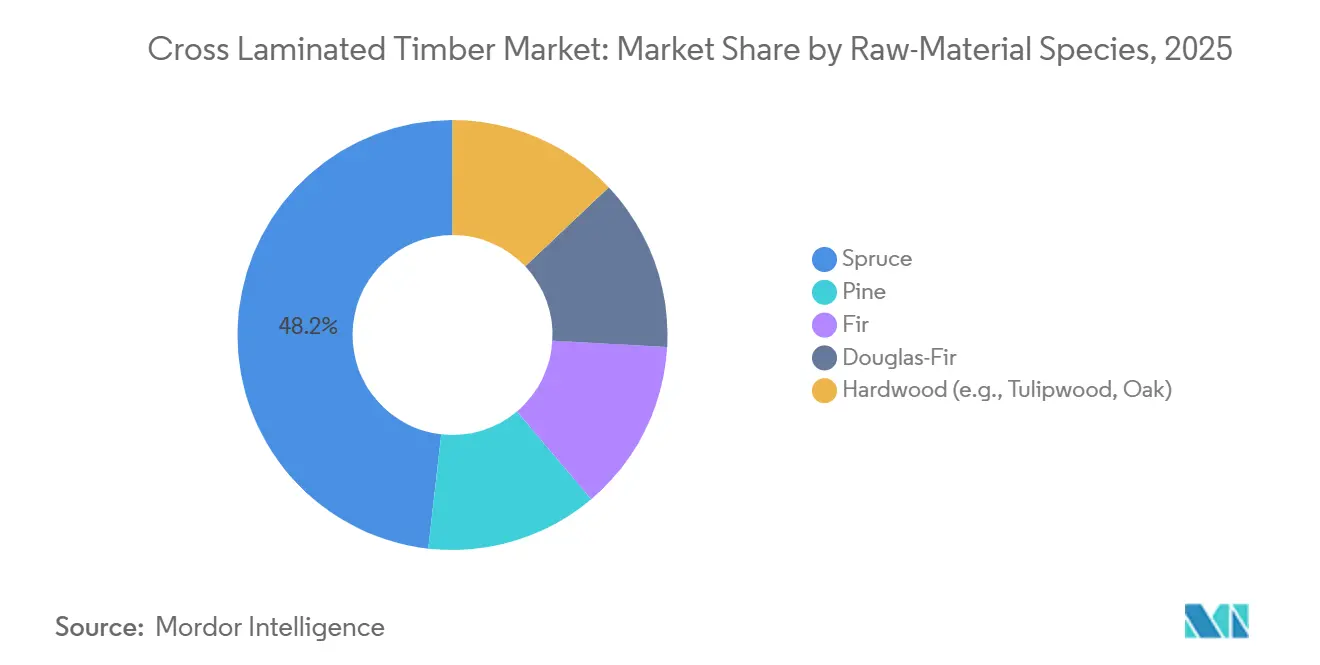

- By raw-material species, spruce captured 48.21% share of the cross laminated timber market size in 2025 and Douglas-fir is projected to advance at a 12.60% CAGR between 2026-2031.

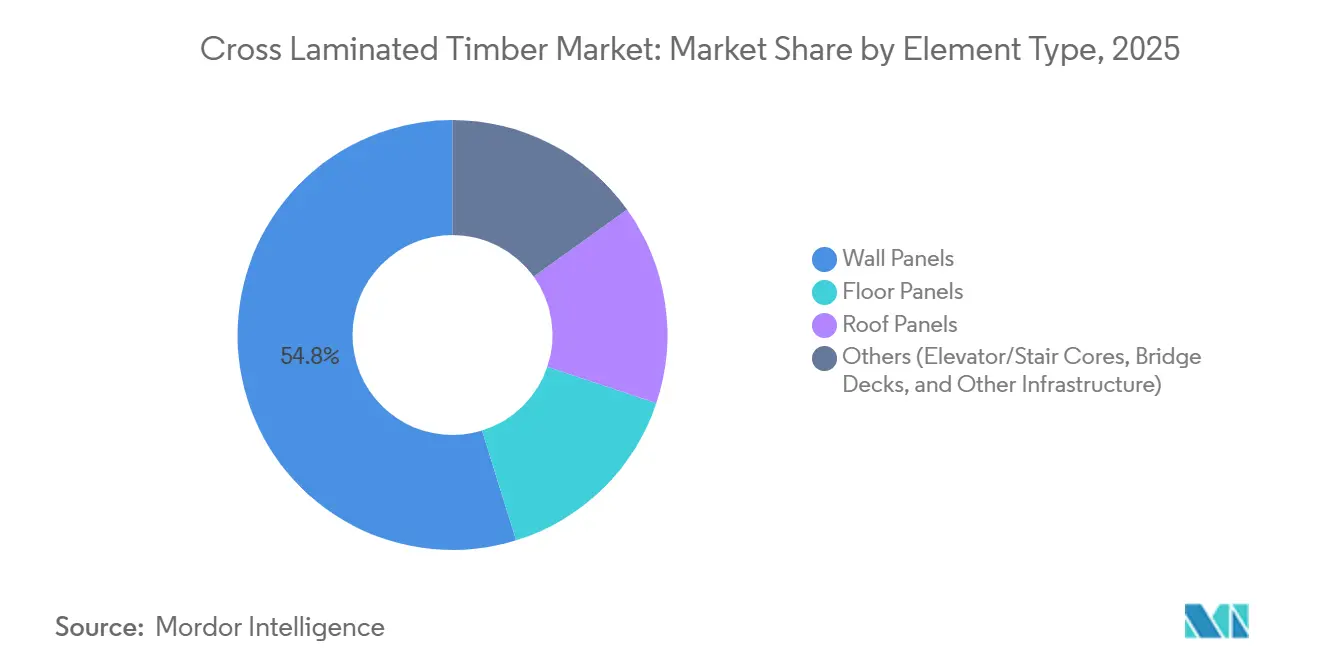

- By element type, wall panels held 54.78% share of the cross laminated timber market size in 2025 and roof panels are on track for a 13.15% CAGR through 2031.

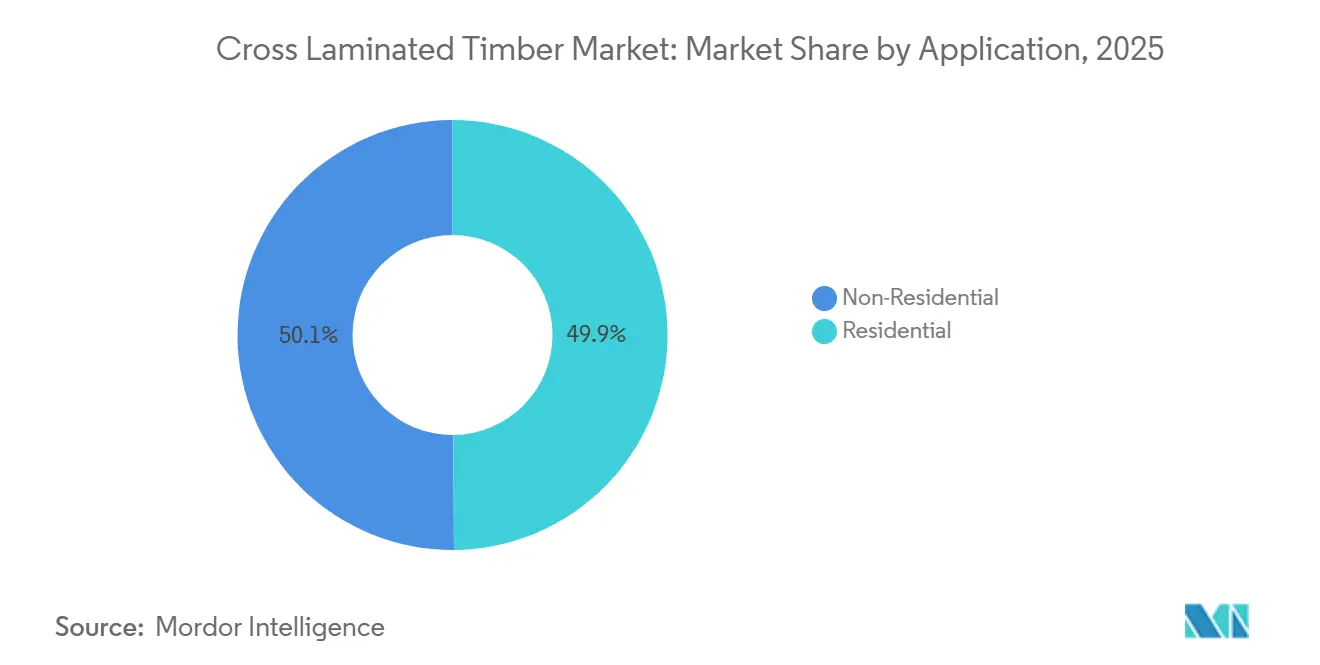

- By application, non-residential led with 50.12% cross laminated timber market share in 2025, while residential is forecast to post a 12.45% CAGR to 2031.

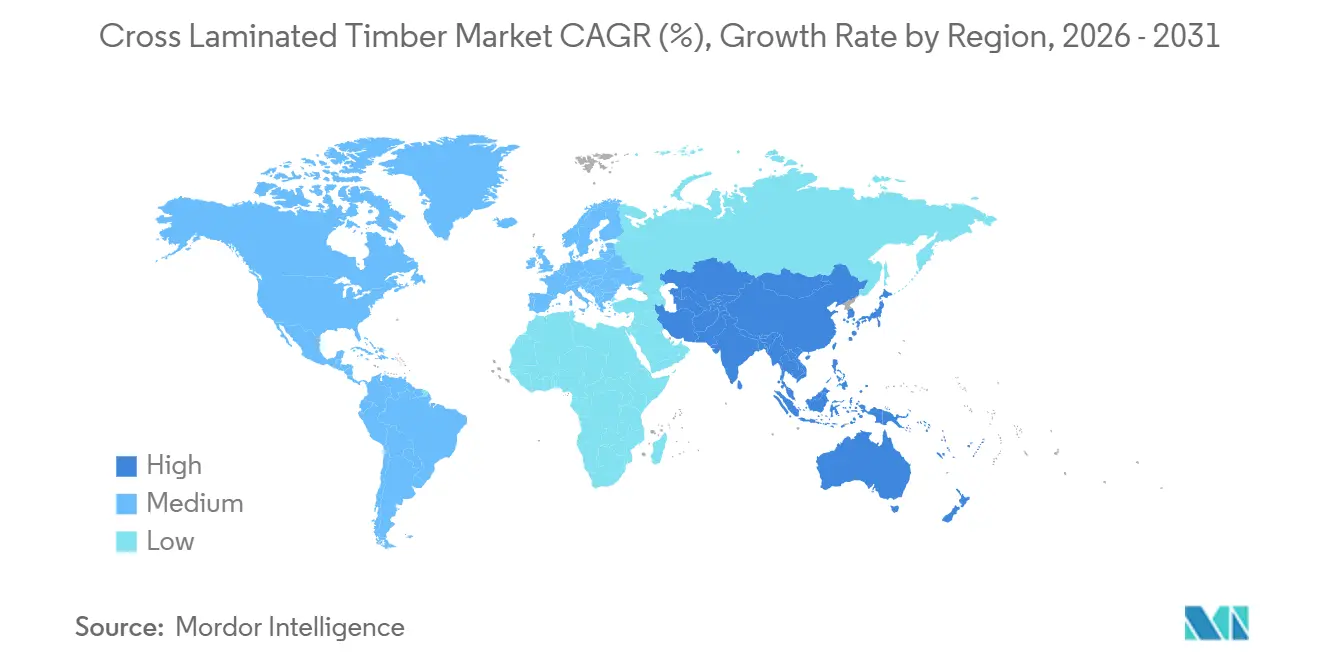

- By geography, Europe accounted for 54.33% of 2025 volume, while Asia-Pacific is projected to register a 17.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cross Laminated Timber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Incentives and Low-Carbon Building Codes in the European Union and North America | +3.2% | Europe (Germany, France, Nordic), North America (California, Oregon, British Columbia) | Medium term (2-4 years) |

| Growing Modular and Off-Site Mid-rise Construction Demand | +2.8% | Global, with concentration in Europe and North America urban centers | Short term (≤ 2 years) |

| Carbon-Pricing Escalation in Europe Favouring Low-Embodied-Carbon Cross-Laminated Timber | +2.1% | Europe (EU ETS jurisdictions), early spillover to UK and Switzerland | Long term (≥ 4 years) |

| Adoption of Long-Span CLT Rib / Hybrid Floor Systems (more than 12 M) Unlocking New Use-Cases | +1.6% | North America and Europe commercial projects, emerging in Asia-Pacific | Medium term (2-4 years) |

| AI-Driven Design for Manufacture Platforms Cutting Engineering Lead-Times | +1.3% | Global, led by digitally mature markets in North America and Northern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Incentives and Low-Carbon Building Codes in the European Union and North America

Mandatory whole-life-carbon assessments for buildings above 2,000 m² from 2028 under EU Directive 2024/1275 are prompting specifiers to prioritize timber systems that cut global-warming potential by up to 75% versus steel-concrete frames. California’s 2024 Buy Clean update extends environmental-product-declaration rules to mass-timber in public projects above USD 5 million, effectively gating non-compliant suppliers. British Columbia’s Step Code offers emissions credits for bio-based structures, accelerating CLT uptake in Vancouver and Victoria multifamily schemes. Because fabricators can now deliver verified carbon footprints within 72 hours, developers gain a compliance edge in permitting queues. Resulting demand underpins the cross laminated timber market’s rapid volume gains.

Growing Modular and Off-Site Mid-rise Construction Demand

Factory-built CLT modules trim on-site labor needs by 30-40% and shorten schedules 20-25%, a decisive benefit in high-wage urban centers. A Stockholm development reached weathertight status in 11 weeks using prefabricated CLT cassettes versus 18 weeks for concrete, saving USD 1.8 million in preliminaries. Germany’s modular housing output climbed 18% during 2024-2025; acoustic-performing CLT panels meeting DIN 4109 standards enable thinner floor assemblies. Japan earmarked JPY 12 billion to subsidize rural CLT modular homes, targeting 5,000 units by 2028 and reinforcing Asia-Pacific growth.

Carbon-Pricing Escalation in Europe Favouring Low-Embodied-Carbon Cross-Laminated Timber

EU ETS allowances averaged EUR 85 tCO₂e in 2025, inflating embodied-carbon liabilities for steel and cement by 12-15%[1]European Energy Exchange, “EU ETS Pricing 2025,” eex.com . A typical 8-story concrete frame now incurs EUR 102,000-127,500 in carbon costs, while an equivalent CLT structure pays roughly one-fourth, boosting project IRRs by up to 1.2 percentage points. The Carbon Border Adjustment Mechanism, fully effective in 2026, further widens the gap by pricing imported metals.

Adoption of Long-Span CLT Rib / Hybrid Floor Systems (more than 12 M) Unlocking New Use-Cases

Hybrid rib panels spanning 12-16 m allow column-free offices and retail floors once reserved for post-tensioned concrete. A Helsinki office delivered in 2025 eliminated 18 interior columns and gained 9% net leasable area using Stora Enso’s Sylva Rib system. Hybrid CLT-steel frames meeting Canadian seismic Category IV are expanding into U.S. West Coast projects, enlarging the cross laminated timber market addressable base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Spruce and Fir Prices Post-Russia-Ukraine Conflict Raising EU Costs | -1.8% | Europe (Central and Eastern Europe most affected), spillover to Nordic region | Short term (≤ 2 years) |

| Moisture Absorption Related Durability Risks | -1.2% | Tropical and subtropical regions (Southeast Asia, Middle East, South America), coastal zones globally | Medium term (2-4 years) |

| Limited Fire Rated Adhesive Options That Pass Annex B Tests (U.S.) | -0.9% | North America (U.S. jurisdictions enforcing IBC Chapter 6), limited impact in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Spruce and Fir Prices Post-Russia-Ukraine Conflict Raising EU Costs

Central European spruce and fir prices jumped 22-28% between early 2022 and mid-2024 following sanctions on Russian timber, trimming large fabricator EBITDA by 2.3 points and forcing seven mid-sized plants to shutter or merge. Fixed-price bid requirements of 9-12 months exacerbate risk, delaying project awards and tempering capacity expansions within the cross laminated timber market.

Moisture Absorption Related Durability Risks

University of Queensland testing showed uncoated CLT panels in Brisbane exceeded safe moisture thresholds by the third wet season, necessitating USD 15-22 m² protective finishes and five-year recoats. A Dubai pilot incorporated vapor membranes and mechanical dehumidifiers, adding 11% to structural costs. These premiums dampen competitiveness in Southeast Asia despite strong sustainability demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bonding Technology: Adhesive Systems Maintain Dominance

Adhesive-bonded represented 90.91% of 2025 volume, underpinned by polyurethane and MUF chemistries that deliver 6-8 MPa shear strength and global code acceptance. This segment is forecast to grow at 12.16% CAGR, keeping the cross laminated timber market size firmly aligned with code-driven high-rise demand. Mechanically fastened alternatives are also expanding as circular-economy projects prize disassembly.

DLT’s Living Building Challenge credentials entice niche adopters, yet 20-25% thicker panels raise material outlays by 15-18%. Emerging bio-based adhesives derived from lignin promise 40-50% fossil-carbon reduction while retaining PRG 320 performance, reinforcing adhesive-bonded leadership. Mechanically fastened systems will remain a valuable niche for heritage retrofits and temporary structures rather than a broad substitute.

By Raw-Material Species: Spruce Leads; Douglas-Fir Accelerates

Spruce captured 48.21% of 2025 volume thanks to abundant Central European supply and favorable stiffness-to-weight attributes, securing the largest slice of cross laminated timber market share. Pine and fir follow, serving cost-sensitive or low-rise applications. Douglas-fir records a 12.60% CAGR as U.S. Pacific mills exploit its 15-20% superior shear resistance for seismic zones.

Douglas-fir CLT has gained traction in Oregon and California where updated codes favor high-density species. Hardwood CLT - principally tulipwood - commands premium boutique projects due to intrinsic Class D fire ratings and visual appeal.

By Element Type: Wall Panels Still Predominate; Roof Panels Surge

Wall panels held 54.78% of 2025 volume and continue to anchor structural loads in mid-rise buildings. Roof panels post the fastest 13.15% CAGR by enabling lightweight vertical extensions in dense cities. Paris now permits two-story CLT rooftop additions that add no more than 15% structural weight, a condition easily met by CLT’s 400-500 kg/m³ density.

Hybrid CLT-beech floors introduced by Binderholz lift bending stiffness 18% without thickness increases, widening floor-plate spans for office use. Elevator cores, stair modules, and bridge decks - signal emerging infrastructure diversification that could raise installed volumes beyond buildings by 2031.

By Application: Residential Growth Outpaces Non-Residential

Non-residential led with 50.12% cross laminated timber market share in 2025, buoyed by corporate net-zero targets and institutional retrofits. Yet residential demand is set to climb 12.45% CAGR, surpassing non-residential by decade’s end. Germany allocated EUR 14.5 billion to subsidize low-carbon housing, 40% ring-fenced for CLT projects.

Sweden’s municipal landlords aim for 15,000 CLT apartments by 2028. California’s wildfire-impacted housing shortage accelerated CLT adoption in 2025, with a 120-unit Oakland project realizing 18% cost savings over concrete. Institutional and commercial segments will continue to anchor volume, but residential modular schemes drive the fastest incremental growth in the cross laminated timber market.

Geography Analysis

Europe maintained 54.33% of 2025 volume, supported by Germany’s 18-meter height allowance for standard timber approvals and Nordic vertical integration that feeds domestic and export demand. Finland’s 2025 output grew owing to shipping panels to the UK, where net-zero pathways drive imports. Southern Europe shows rapid catch-up as seismic retrofits and heritage rooftop conversions adopt lightweight CLT systems.

North America’s share concentrates in the United States in the Pacific and Californian corridors, where the 2021 IBC permits 18-story mass-timber buildings. Canada’s CleanBC program reserved CAD 50 million for mass-timber pilots, elevating British Columbia’s provincial demand. Growth is tempered by still-limited fire-rated adhesive options and intermittent feedstock volatility, yet Douglas-fir supply advantages sustain momentum.

Asia-Pacific is the fastest-growing cross laminated timber market region at 17.38% CAGR. Japan’s revised Building Standard Law allows four-story CLT structures without ministerial approval, unlocking rural housing subsidies and mid-rise urban projects[2]Ministry of Land, Infrastructure, Transport and Tourism Japan, “Building Standard Law Revision 2024,” mlit.go.jp . China’s pilot builds in Shenzhen and Hangzhou test domestic panels, but adhesive certification delays restrain volume. Green-building credits drive South Korea’s share, while Southeast Asia remains nascent because of humidity-related durability costs. South America and the Middle East trail with global share apiece, though Brazil’s 2024 plant investment hints at latent regional adoption.

Mordor Intelligence provides coverage of the cross laminated timber market across other key regional markets, including Asia, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The global market remains moderately concentrated. European leaders, including Stora Enso, Binderholz, Mayr-Melnhof Holz, HASSLACHER Holding GmbH, and KLH, command advantages in scale, multi-plant networks, and long-standing architect ties. North American challengers such as SmartLam and Nordic Structures leverage proximity to Douglas-fir forests and high-growth residential corridors to erode European share.

Strategies bifurcate: large players deepen vertical integration to mitigate feedstock price swings, evidenced by Binderholz’s 45,000-hectare Romanian forest acquisition in 2025. Mid-sized firms differentiate through digital design tools and specialty panels, Pfeifer’s REI-90 fire-rated system and HASSLACHER’s dowel-fastened CLT secure niche sustainability projects. Hardwood CLT specialists target premium hospitality, while Asia-Pacific entrants scale domestic capacity to local codes, intensifying competitive dynamics across the cross laminated timber market.

Technology adoption is a decisive moat. Binderholz’s AI-optimization cuts lead-time variability 22% and material waste by 14%, enabling four-week delivery commitments. Stora Enso’s EUR 120 million Gruvön expansion adds a 16-m CNC line and AI-driven QC, adding 250,000 m³ capacity by late 2026. Patent activity around hybrid rib systems and bio-based adhesives signals next-wave differentiation that could reset cost curves.

Cross Laminated Timber Industry Leaders

Binderholz GmbH

HASSLACHER Holding GmbH

KLH Massivholz GmbH

Mayr-Melnhof Holz Holding AG

Stora Enso

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Microsoft constructed two data centers in Northern Virginia, utilizing cross laminated timber for part of the construction. Since CLT was prefabricated offsite, it allowed for faster and safer installation compared to corrugated steel commonly used in large commercial buildings.

- June 2024: Binderholz GmbH introduced Decorative Micro cross laminated timber, a 3-layer solid wood panel made of spruce, featuring a tongue and groove connection designed for interior and timber construction applications. This product was engineered to facilitate high-quality and efficient processing while meeting both visual and technical standards.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the cross-laminated timber (CLT) market as factory-made structural panels built from three or more layers of sawn lumber arranged at right angles and bonded into large, dimension-stable slabs used in load-bearing walls, floors, and roofs. Units are expressed in cubic meters of finished CLT delivered from mills to construction projects.

Scope Exclusion: laminated veneer lumber, glue-laminated beams, and other engineered wood products are not counted.

Segmentation Overview

- By Bonding Technology

- Adhesive-Bonded

- Mechanically Fastened

- By Raw-Material Species

- Spruce

- Pine

- Fir

- Douglas-Fir

- Hardwood (e.g., Tulipwood, Oak)

- By Element Type

- Wall Panels

- Floor Panels

- Roof Panels

- Others (Elevator/Stair Cores, Bridge Decks, and Other Infrastructure)

- By Application

- Residential

- Non-Residential

- Commercial

- Industrial / Institutional

- Other Applications (Military Housing, Emergency Shelters, Event Structures)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Vietnam

- Malaysia

- Indonesia

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- South Africa

- Nigeria

- Egypt

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

We interview mill operators, timber-frame contractors, structural engineers, and code officials across Europe, North America, and fast-growing Asian hubs. Discussions verify typical line utilization, reject rates, price realization, and the pace at which mid-rise and modular builders substitute CLT for concrete. Short online surveys with architects give us adoption-probability curves that desk data cannot reveal.

Desk Research

Mordor analysts start with reputable public records, annual production reports from FAO-Forestry and UNECE Timber Committee, Eurostat trade files, U.S. Forest Service mill surveys, and building-permit dashboards from Statistics Canada and the Australian Bureau of Statistics. Company filings, investor decks, and environmental-product declarations then clarify mill capacities and panel size mixes. Paid resources such as D&B Hoovers (mill revenues) and Volza (export shipment counts) let us benchmark output against cross-border flows. These sources illustrate market depth, yet do not alone answer every sizing question; many additional references inform background checks and data cleaning.

Market-Sizing & Forecasting

A combined top-down and bottom-up model is built. National sawn-wood production, CLT mill nameplate capacity, average capacity utilization, and export-import balances reconstruct 2025 demand pools; supplier roll-ups and sampled ex-factory prices validate volumes and value. Key variables include: 1. Mill capacity additions announced through 2027, 2. Regional carbon-price trajectories, 3. Building permits for multi-story timber structures, 4. Average panel thickness trends, 5. Exchange-rate outlook affecting price parity. Multivariate regression projects each driver through 2030, while scenario analysis tests high-carbon-price and low-housing-start cases. Where supplier disclosures are partial, we interpolate using historical utilization bands cross-checked against shipment data.

Data Validation & Update Cycle

Outputs face three layers of review: variance checks against independent trade and permitting metrics, peer review by a senior analyst, and a final refresh before publication. The dataset is updated yearly, with interim revisions triggered by new mill start-ups, code changes, or material events flagged during continuous news monitoring.

Why Mordor's Cross Laminated Timber Baseline Earns Investor Trust

Published estimates often diverge because firms mix engineered wood types, use different price decks, or freeze models for years.

Key gap drivers include: some studies convert square-foot project data directly to revenue without verifying panel thickness; others model only Europe and stretch that ratio globally; a few adopt optimistic carbon-credit price paths that inflate value. Mordor Intelligence fixes scope to finished CLT panels, refreshes all variables annually, and aligns carbon-pricing assumptions with enacted policy, yielding a balanced baseline users can retrace.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 2.15 Mn m³ (2025) | Mordor Intelligence | |

| USD 1.81 Bn (2025) | Global Consultancy A | revenue only; excludes Asia-Pacific volume |

| USD 1.33 Bn (2023) | Research Publisher B | older base year; applies single global ASP |

| USD 1.17 Bn (2024) | Industry Journal C | omits mechanically-fastened panels |

In sum, Mordor's disciplined scope selection, live driver tracking, and cross-check routine deliver a dependable reference point for planners who need transparent, reproducible numbers.

Key Questions Answered in the Report

How large is the cross laminated timber market in 2026 and where is it headed?

The Cross Laminated Timber Market size is projected to expand from 1.96 Million cubic meters in 2025 and 2.18 Million cubic meters in 2026 to 3.76 Million cubic meters by 2031, registering a CAGR of 11.52% between 2026 to 2031.

Which bonding technology dominates commercial projects?

Adhesive-bonded held 90.91% of 2025 volume because of code familiarity and high shear strength.

Why is Douglas-fir gaining share in seismic regions?

Douglas-fir’s higher density and shear capacity meet stringent seismic codes in the U.S. Pacific Northwest, driving a 12.60% CAGR through 2031.

Which element type is expanding the fastest?

Roof panels are forecast to increase at 13.15% CAGR as cities allow lightweight CLT rooftop additions.

Page last updated on: