Market Overview

| Study Period | 2021 - 2031 |

|---|---|

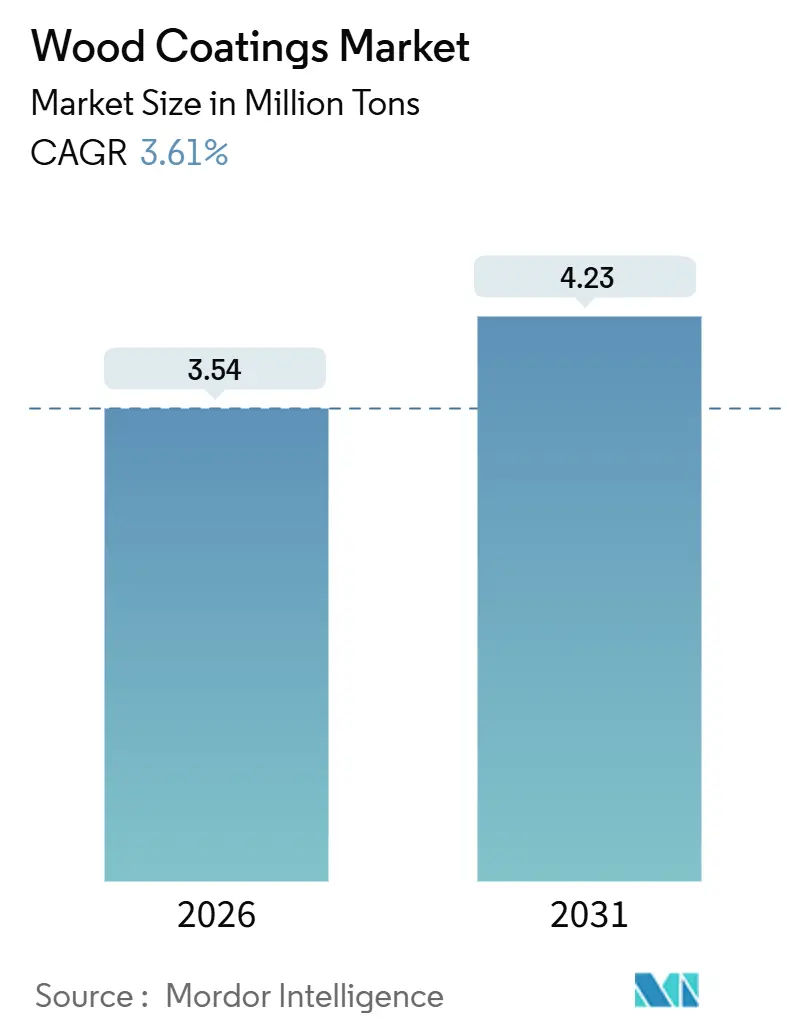

| Market Volume (2026) | 3.54 Million tons |

| Market Volume (2031) | 4.23 Million tons |

| Growth Rate (2026 - 2031) | 3.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wood Coatings Market Analysis by Mordor Intelligence

The Wood Coatings Market size is estimated at 3.54 million tons in 2026, and is expected to reach 4.23 million tons by 2031, at a CAGR of 3.61% during the forecast period (2026-2031). Solvent-borne lines still dominate finishing halls, yet regulatory pressure in Europe and California and the cost advantage of ready-to-assemble (RTA) furniture in the Asia-Pacific are steering investments toward waterborne and UV-cured chemistries. Asia-Pacific furniture exporters continue to absorb higher resin prices through plant automation and inline quality control, while North American remodelers sustain demand for premium low-sheen polyurethane clears. Abrasion-resistant polyurethane resins remain the backbone of mass-timber interiors, and the rollout of AI-enabled pigment dosing is trimming waste and offsetting the 15-20% price premium attached to waterborne dispersions. Competitive intensity stays moderate, with the top five suppliers controlling 38% of global tonnage and regional specialists exploiting niches that reward formulation tweaks for local wood species.

Key Report Takeaways

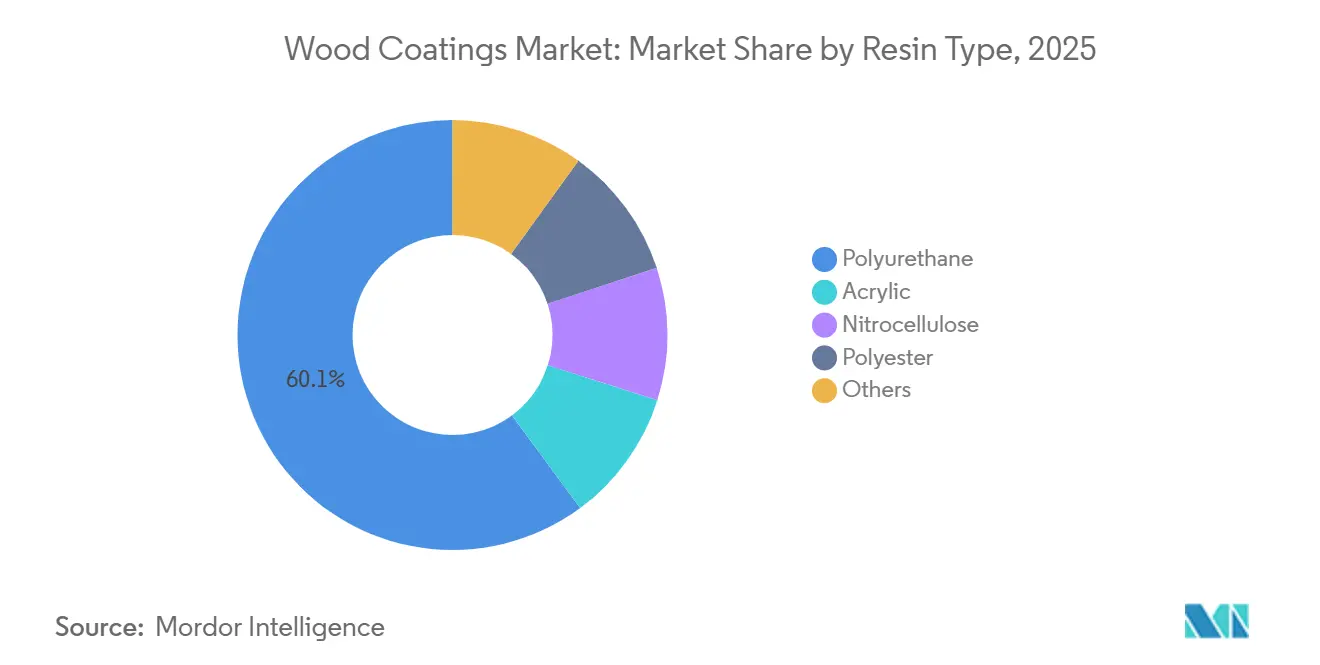

- By resin type, polyurethane held a 60.14% Wood Coatings market share in 2025, and it is projected to expand at a 3.82% CAGR through 2031.

- By technology, solvent-borne finishes commanded 78.12% of the Wood Coatings market size in 2025, while waterborne systems are on track for the fastest 4.35% CAGR to 2031.

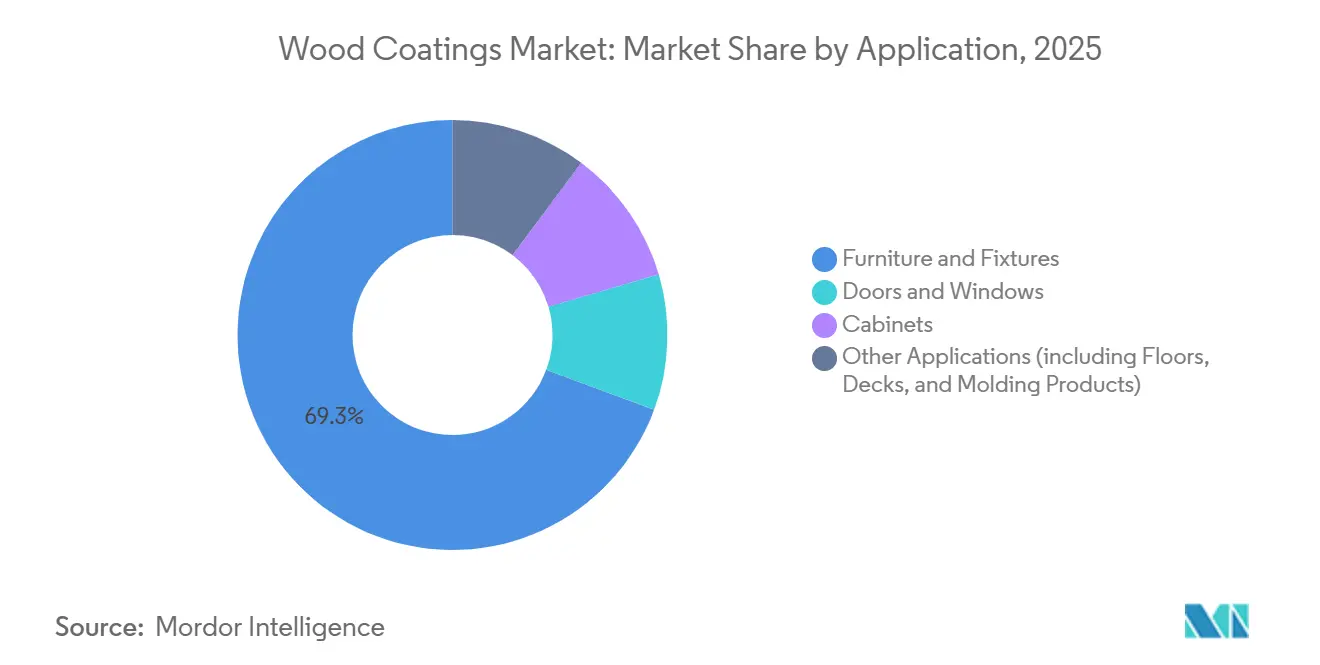

- By application, furniture and fixtures led with 69.34% of Wood Coatings market share in 2025; the segment is forecast to rise at 3.75% CAGR through 2031.

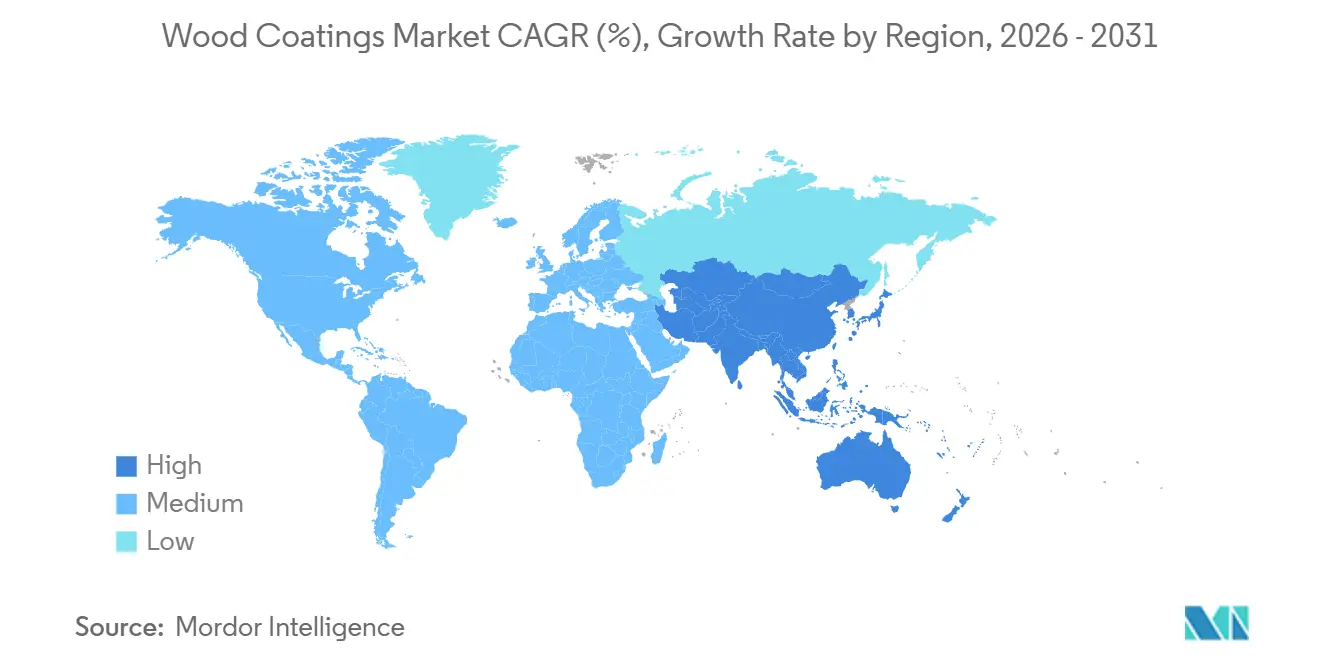

- By geography, Asia-Pacific accounted for 56.68% of the Wood Coatings market size in 2025 and is set to post the quickest 3.91% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wood Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Modular and RTA furniture boom in Asia-Pacific | +0.8% | China, India, Vietnam, Indonesia, Thailand | Medium term (2-4 years) |

| EU-led shift to low-VOC waterborne formulations | +0.6% | Europe, California, Northeast U.S. | Long term (≥4 years) |

| Premium interior décor trend in North America | +0.4% | United States, Canada | Short term (≤2 years) |

| Mass-timber high-rise adoption elevating clear UV demand | +0.5% | North America, Nordic Europe, Germany, Austria | Medium term (2-4 years) |

| AI-enabled inline color matching | +0.3% | Early adoption in Europe and North America, global rollout post-2028 | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Modular and RTA Furniture Boom in Asia-Pacific

Ready-to-assemble formats now account for 60–70% of India’s organized furniture sales, pushing finishing lines toward fast-curing waterborne topcoats that tolerate flat-pack boxing within 24 hours[1]Ministry of Commerce & Industry India, “Furniture Export Trends 2024,” commerce.gov.in. Vietnam’s wood and furniture exports jumped 21% in 2024 to USD 16.3 billion, and the local association targets USD 18 billion in 2025 as EU buyers seek EUDR-compliant suppliers. Thailand produced 6.63 million wooden furniture pieces in 2024, up 14.46%, while Indonesia shipped USD 2.02 billion of furniture, keeping wooden articles above 50% of export value. China’s coastal clusters generated CNY 535.52 billion (USD 73.9 billion) in furniture revenue during the first ten months of 2024, with exports climbing 7.2% to USD 54.932 billion. These production hubs favor two-component polyurethane clears that hit ≥2H pencil hardness at ambient cure, positioning the driver to add 0.8 percentage points to the regional CAGR.

EU-Led Shift to Low-VOC Waterborne Formulations

Directive 2004/42/EC caps VOC content at 400 g/L for interior and 300 g/L for exterior wood finishes, forcing a reevaluation of solvent-heavy alkyds and nitrocellulose lacquers[2]European Union, “Directive 2004/42/EC,” eur-lex.europa.eu. Regulation (EU) 2023/1464 also limits formaldehyde release to 0.062 mg/m³, tightening material specs for panel producers. The EU Ecolabel now requires interior coatings below 30 g/L VOC, a threshold only waterborne dispersions reliably meet. Akzo Nobel disclosed that 60% of its 2024 sales stemmed from sustainable products, and PPG opened a waterborne plant in Rayong, Thailand, to serve EU-bound furniture exporters. California Air Resources Board mirrors the restriction with a 550 g/L limit for clear finishes, reinforcing the 0.6 point uplift in long-term CAGR.

Premium Interior Décor Trend in North America

U.S. homeowners spent USD 485 billion on remodeling in 2024, with kitchen and bath upgrades claiming 42%. Low-sheen polyurethane and acrylic-polyurethane hybrids dominate cabinetry specs because they resist yellowing under LED lighting. Sherwin-Williams posted USD 6.16 billion in third-quarter 2024 net sales, citing mid-single-digit growth in wood stains and clears. Benjamin Moore launched a zero-VOC interior finish in 2025 that meets Greenguard Gold and helps projects score LEED v4.1 credits. Canadian housing starts averaged 240,000 units in 2024–25, feeding demand for factory-finished doors and window frames. This décor upswing lifts short-term CAGR by 0.4 points.

Mass-Timber High-Rise Adoption Accelerating Clear UV Finish Demand

North America added 1.2 million m² of cross-laminated timber floor area in 2024, including the University of Toronto’s 14-story Academic Wood Tower. Nordic countries approved 87 mass-timber buildings in 2024, together consuming about 42,000 tons of UV-curable acrylate coatings. Germany eased code barriers to expose CLT up to 22 m heights, provided fire-retardant finishes are applied. Austria’s Lifecycle Tower ONE used 2,800 m³ of CLT coated with waterborne UV acrylics emitting under 10 g/L VOC. Rapid-cure UV clears that reach ≥3H hardness within 10 seconds explain the 0.5 point CAGR boost expected between 2027 and 2029.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resin and solvent price volatility | -0.5% | Acute in Europe and North America, global spillover | Short term (≤2 years) |

| Stricter formaldehyde / VOC caps | -0.4% | Europe, North America, China | Medium term (2-4 years) |

| PFAS phase-out threatening performance additives | -0.3% | Regulatory leadership in EU and United States | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Resin and Solvent Price Volatility

Toluene diisocyanate averaged CNY 14,700/ton (USD 2,041/ton) and polymeric MDI hit CNY 15,200/ton (USD 2,110/ton) in Q3 2025, with force-majeure events limiting European volumes to 70% of contracts. The U.S. Producer Price Index for petrochemicals leaped 13.1% between December 2024 and March 2025 as ethylene exceeded 30 ¢/lb. Asian naphtha averaged USD 547/ton in April 2025, still 18% above the 2020–22 mean. Such swings drive formulators to shorten contract length and delay inventory builds, clipping 0.5 points from near-term CAGR.

Stricter Formaldehyde / VOC Caps

The EU ceiling of 0.062 mg/m³ formaldehyde forces panel producers to swap urea-formaldehyde for melamine or phenolic systems that cost 15–20% more. The U.S. Toxic Substances Control Act aligns with a 0.09 ppm limit on hardwood plywood. China’s draft GB 18580-2017 revision would pull the domestic threshold down to 0.080 mg/m³. Upgraded presses and abatement gear erode margins and remove 0.4 points from mid-term CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyurethane Dominance Anchored by Abrasion Resistance

Polyurethane commanded 60.14% of the Wood Coatings market in 2025 and will progress at a 3.82% CAGR through 2031, owing to ≥2H pencil hardness and optical clarity essential for mass-timber interiors. Acrylics are witnessing rising demand and are on the back of better UV stability and easy waterborne blending. Nitrocellulose and polyester coatings face a margin squeeze from higher phthalic anhydride prices. Emerging blocked-isocyanate one-packs based on vanillin show 12-month pot life and deblock at 120 °C, mapping neatly onto infrared ovens now common in Vietnamese factories. Acrylic-urethane hybrids captured 9% of the waterborne subsegment in 2025 and could reach 14% by 2031 as they help formulators meet the EU Ecolabel VOC <30 g/L target.

Regulatory stick is speeding the shift. The EU BAT reference for wood treatment mandates closed-loop solvent recovery for nitrocellulose, an upgrade that costs EUR 200,000–500,000 per booth. Polyurethane players reply with systems stable at room temperature yet curing fully during a 15-minute bake, matching throughput at Indonesian and Indian RTA plants. Demand for biobased polyols, able to replace up to 50% of petrochemical content, is rising among buyers pursuing LEED v4 credits, placing smaller Brazilian and Indian formulators on the radar of global OEMs.

By Technology: Solvent-Borne Incumbency Challenged by Waterborne Momentum

Solvent-borne lines delivered 78.12% of the Wood Coatings market volume in 2025, owing to fast dry and legacy equipment. Waterborne finishes, however, are forecast to enjoy a 4.35% CAGR through 2031, the highest among technologies, because they satisfy Directive 2004/42/EC and CARB limits on VOC. UV-cured products will climb as mass-timber builders demand cures under 10 seconds, while powder coatings account for a marginal share because MDF struggles at 180 °C cure.

Switching to waterborne requires stainless piping, bigger compressors, and longer flash zones that stretch oven time to 35–45 minutes. Asian Paints invested INR 5 billion in a Telangana plant in 2024, with 40% dedicated to waterborne production. Nippon Paint scaled Indonesian and Vietnamese capacity with inline viscosity control to hit IKEA’s <250 g/L VOC rule. UV-cured acrylates cost 25–35% more than solvent-borne polyurethanes yet eliminate oven energy and shrink floor space by 30%, an advantage not lost on German door makers chasing energy efficiency labels.

By Application: Furniture Segment Anchored by APAC Export Surge

Furniture and fixtures absorbed 69.34% of the Wood Coatings market volume in 2025 and are set to expand at a 3.75% CAGR to 2031, underpinned by Vietnam’s USD 16.3 billion export base and planned jump to USD 18 billion in 2025. Doors and windows are witnessing increased wood coatings consumption owing to steady North American housing starts and Europe’s Renovation Wave goal to retrofit 35 million dwellings by 2030. The cabinet application is anticipated to report significant gains in the near future as U.S. kitchen remodels hit USD 203 billion in 2024.

Composite decking, trims, and moldings are witnessing rising demand as UV-resistant topcoats protect color stability. Thailand’s 14.46% output jump and Indonesia’s 52.62% wooden share keep Southeast Asian plants humming. India’s RTA tide further tilts specifications toward fast-cure waterborne polyurethanes, reinforcing the application mix’s sensitivity to residential construction cycles.

Geography Analysis

Asia-Pacific accounted for 56.68% of the Wood Coatings market size in 2025 and is projected to rise at a 3.91% CAGR through 2031. China’s CNY 535.52 billion (USD 73.9 billion) furniture revenue and USD 54.932 billion export haul show coastal plants absorbing resin inflation via automation. Vietnam, India, and Indonesia benefit from 40–50% lower labor costs than Guangdong, and India’s Production Linked Incentive scheme rebates 4–6% of incremental domestic furniture sales, enticing coatings makers to co-locate near Ahmedabad and Pune.

Wood coatings demand in North America is witnessing considerable gains as U.S. remodeling stays elevated and Canada maintains 240,000 annual housing starts. Mexican furniture exports to the United States reached USD 4.8 billion in 2024, up 9% year-over-year, underscoring nearshoring momentum.

Europe accounted for a considerable market size and is anticipated to register considerable gains in the near future. Germany, France, Italy, and the United Kingdom account for 62% of regional demand, and the Renovation Wave program anchors spending through 2030. Brazil’s housing recovery drives South America's wood coatings market growth, while the Middle East and Africa’s demand is rising as Saudi Arabia’s Vision 2030 real-estate surge fuels demand for fire-retardant wood coatings.

Competitive Landscape

The wood coating market is moderately consolidated, with key players such as AkzoNobel, PPG Industries, Sherwin-Williams, and Asian Paints leveraging extensive product portfolios and global distribution networks to dominate furniture OEM and architectural channels. In contrast, smaller regional players focus on sustainability-driven niches, addressing market gaps often overlooked by larger competitors. The adoption of digitalization, including cloud-based formulation management and augmented-reality spray training, is transforming the industry by reducing time-to-market for new color programs. Buyers prioritize suppliers that ensure regulatory compliance, maintain supply chain reliability, and deliver robust design support, driving continuous investments in service capabilities across the wood coatings sector.

Wood Coatings Industry Leaders

The Sherwin-Williams Company

PPG Industries Inc.

Akzo Nobel N.V.

Nippon Paint Holdings Co., Ltd.

Asian Paints

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: PPG inaugurated a 25,000 t/y waterborne plant in Rayong, Thailand, to serve Southeast Asian furniture exporters.

- January 2024: Asian Paints commissioned an INR 5 billion Telangana site that dedicates 40% capacity to waterborne wood coatings.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the wood coatings market as the global consumption of liquid or powder formulations applied by spray, brush, roller, curtain, or UV line that protect or decorate solid wood substrates such as furniture, flooring, cabinets, doors, and architectural joinery. The base year for sizing is 2025, when Mordor analysts estimate 3.42 million tons of coatings were shipped worldwide.

Scope exclusion: finishes designed only for wood-plastic composites or MDF paper overlays are outside this assessment.

Segmentation Overview

- By Resin Type

- Polyurethane

- Acrylic

- Nitrocellulose

- Polyester

- Others

- By Technology

- Water-borne

- Solvent-borne

- UV-Cured

- Powder Coatings

- By Application

- Furniture and Fixtures

- Doors and Windows

- Cabinets

- Other Applications (including Floors, Decks, and Molding Products)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- South Africa

- Nigeria

- Egypt

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then interviewed formulators, furniture OEM buyers, and regional distributors across Asia-Pacific, North America, and Europe, followed by short surveys with independent applicators. These conversations clarified average selling prices, resin substitution pace, and real-world adoption of water-borne lines, enabling us to fine-tune assumptions drawn from secondary material.

Desk Research

We initiated desk work with trade-flow data from UN Comtrade, coating-grade resin output tables from the European Chemical Industry Council, and annual furniture production statistics from FAO Forestry. Regulations and VOC limits were pulled from the U.S. EPA, China's GB/T 9755, and REACH notices, which helped us frame technology shifts. Company 10-Ks, investor decks, and reputable trade journals such as Coatings World filled product-level price and capacity gaps, while D&B Hoovers supplied cross-checks on revenue splits. Paid databases, Dow Jones Factiva for news runs and Questel for recent radiation-cure patent counts, rounded out trend signals. The sources named are illustrative; many additional public and paid references were consulted throughout the build.

Market-Sizing & Forecasting

We applied a top-down production and trade reconstruction that starts with regional furniture, flooring, and millwork output, matches it with typical coating coverage rates, and is subsequently balanced through selective bottom-up checks such as sampled ASP × volume invoices. Key variables include polyurethane resin pricing, residential renovation indices, solvent-borne to water-borne penetration ratios, GDP-linked furniture demand elasticity, and regional VOC caps, all of which feed our multivariate regression forecast. Where granular shipment data were missing, usage coefficients from primary calls bridged the gaps before the final roll-up.

Data Validation & Update Cycle

Outputs pass an anomaly screen against independent import statistics and quarterly earnings signals. A senior analyst reviews variances, and reports refresh each year, with interim updates if raw material shocks or rule changes alter the baseline.

Why Mordor's Wood Coatings Baseline Commands Reliability

Published figures often diverge because research groups pick different base years, measure in value versus volume, or assume contrasting resin price paths.

Key gap drivers include unit of measurement, inclusion of industrial joinery, aggressiveness of technology shift scenarios, and refresh cadence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 3.42 million tons (2025) | Mordor Intelligence | - |

| USD 12.74 billion (2024) | Global Consultancy A | Reports value not volume, includes composite deck stains, updates every two years |

| USD 11.80 billion (2024) | Industry Journal B | Uses historical ASP escalation only, excludes UV-cured powders, limited primary validation |

The comparison shows that Mordor's carefully aligned scope, annual refresh, and dual validation steps deliver a balanced, transparent baseline that decision-makers can retrace to clear variables and repeatable logic.

Key Questions Answered in the Report

How large is the Wood Coatings market in volume terms?

The Wood Coatings market size is estimated at 3.54 million tons in 2026 and is projected to reach 4.23 million tons by 2031.

Which resin type leads volumes?

Polyurethane holds the top spot with 60.14% share in 2025, driven by abrasion resistance and clarity.

Which technology is growing fastest?

Waterborne systems are the swiftest, slated for a 4.35% CAGR through 2031 as regulators tighten VOC limits.

Why is Asia-Pacific dominant?

Asia-Pacific houses the bulk of global furniture manufacturing, giving it 56.68% of volumes in 2025 and the fastest regional growth.

What is the main regulatory headwind?

Stricter caps on formaldehyde, VOC, and pending PFAS restrictions raise compliance costs and slow product rollouts.

Page last updated on: