Reclaimed Rubber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

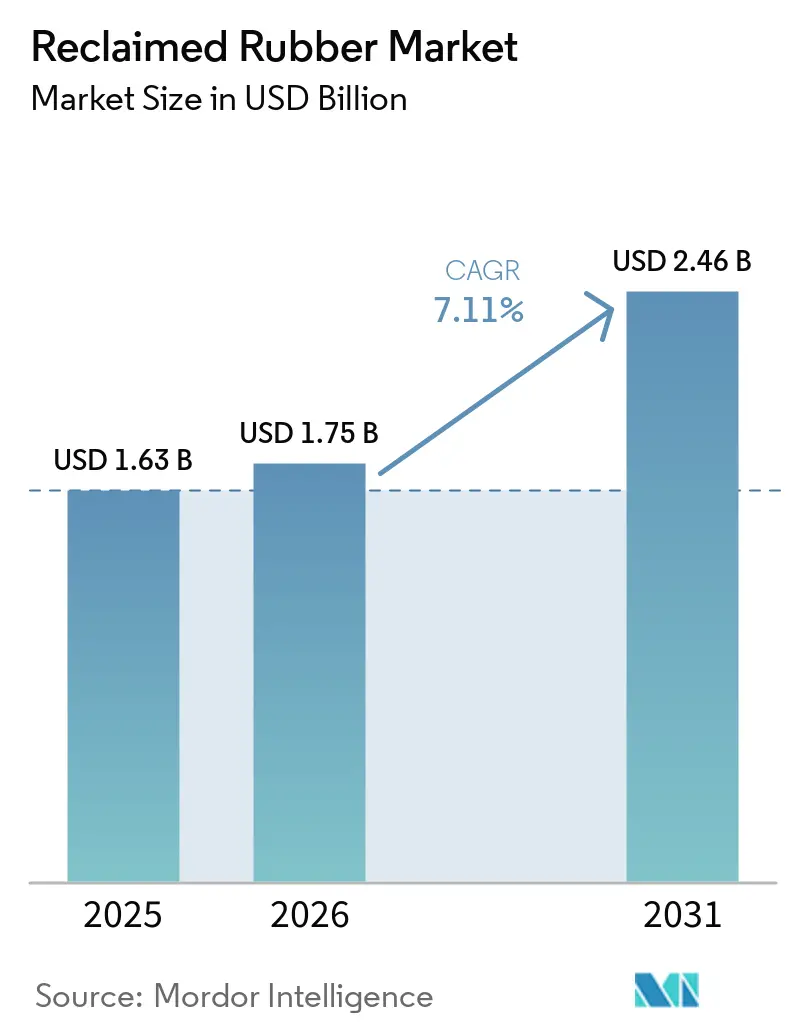

| Market Size (2026) | USD 1.75 Billion |

| Market Size (2031) | USD 2.46 Billion |

| Growth Rate (2026 - 2031) | 7.11% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

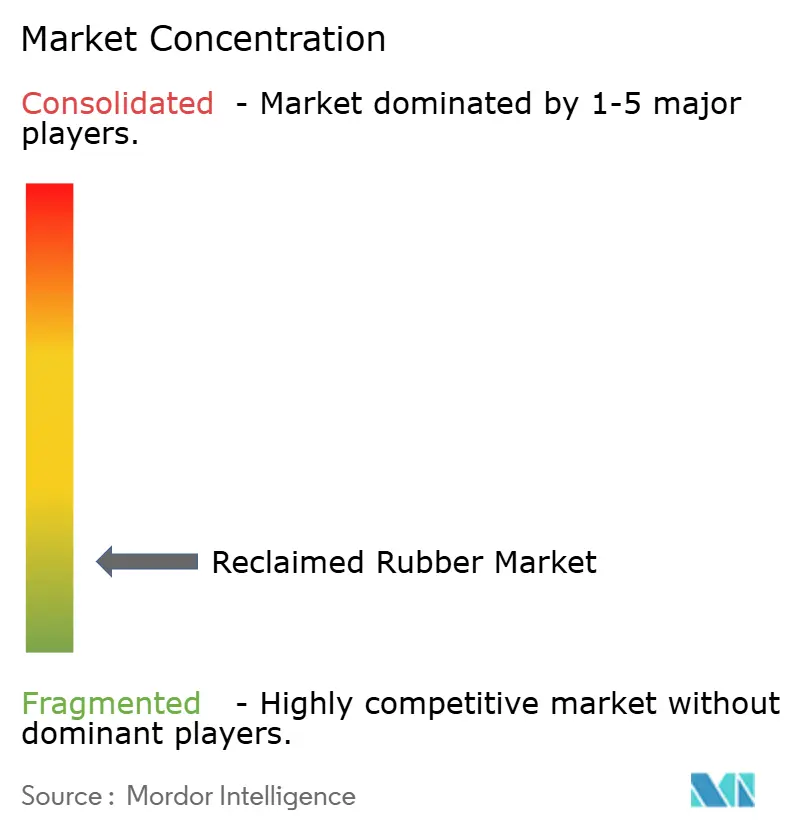

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Reclaimed Rubber Market Analysis by Mordor Intelligence

The Reclaimed Rubber Market size is projected to expand from USD 1.63 billion in 2025 and USD 1.75 billion in 2026 to USD 2.46 billion by 2031, registering a CAGR of 7.11% between 2026 to 2031. Momentum stems from mounting raw-material inflation, stricter disposal rules for end-of-life tires, and continuous advances in devulcanisation that close the quality gap with virgin rubber. Whole tire reclaim (WTR) remains the backbone of global output, while chemical processes expand fastest as OEMs ask for higher-grade recyclate in premium applications. Regionally, Asia-Pacific dominates demand and supply because the world’s largest tire manufacturing base sits next to the planet’s deepest pool of scrap tires, giving processors an unrivalled cost edge. Tightening producer-responsibility schemes in India, China, and the European Union lock in a steady pipeline of feedstock, nudging the reclaimed rubber market toward structural rather than cyclical growth.

Key Report Takeaways

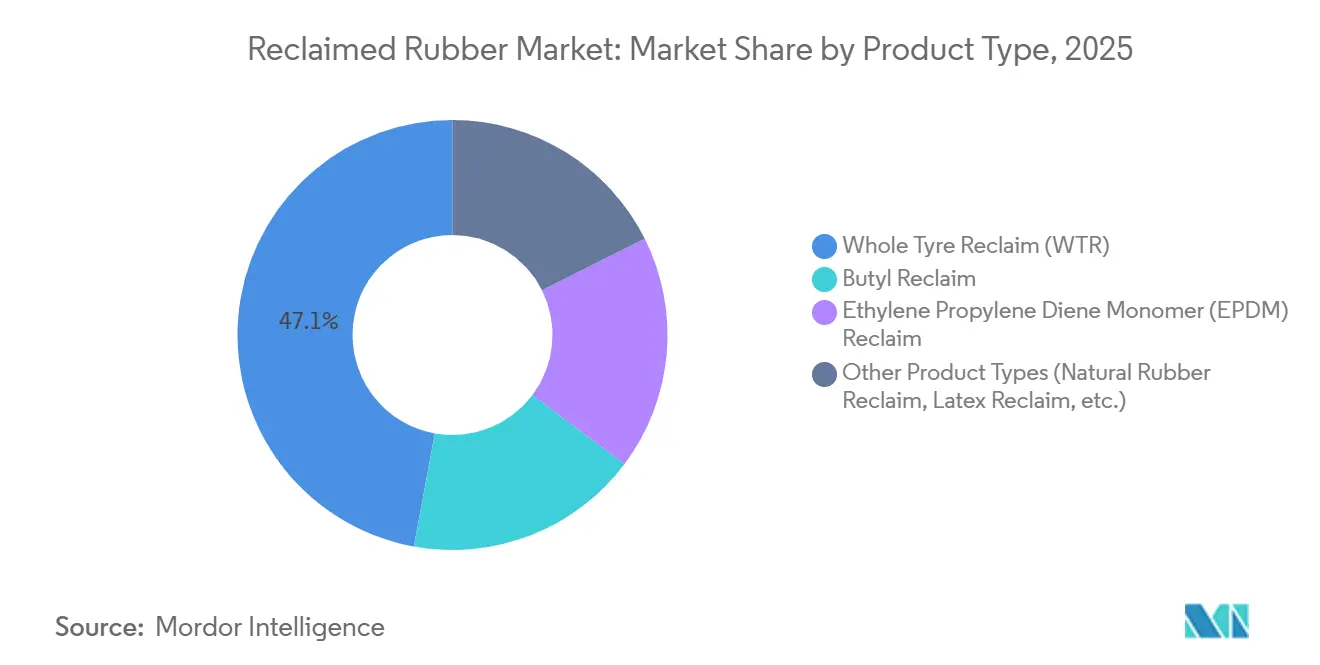

- By product type, consumer-friendly WTR led with 47.21% of reclaimed rubber market share in 2025 and is advancing at a 7.69% CAGR from 2026-2031.

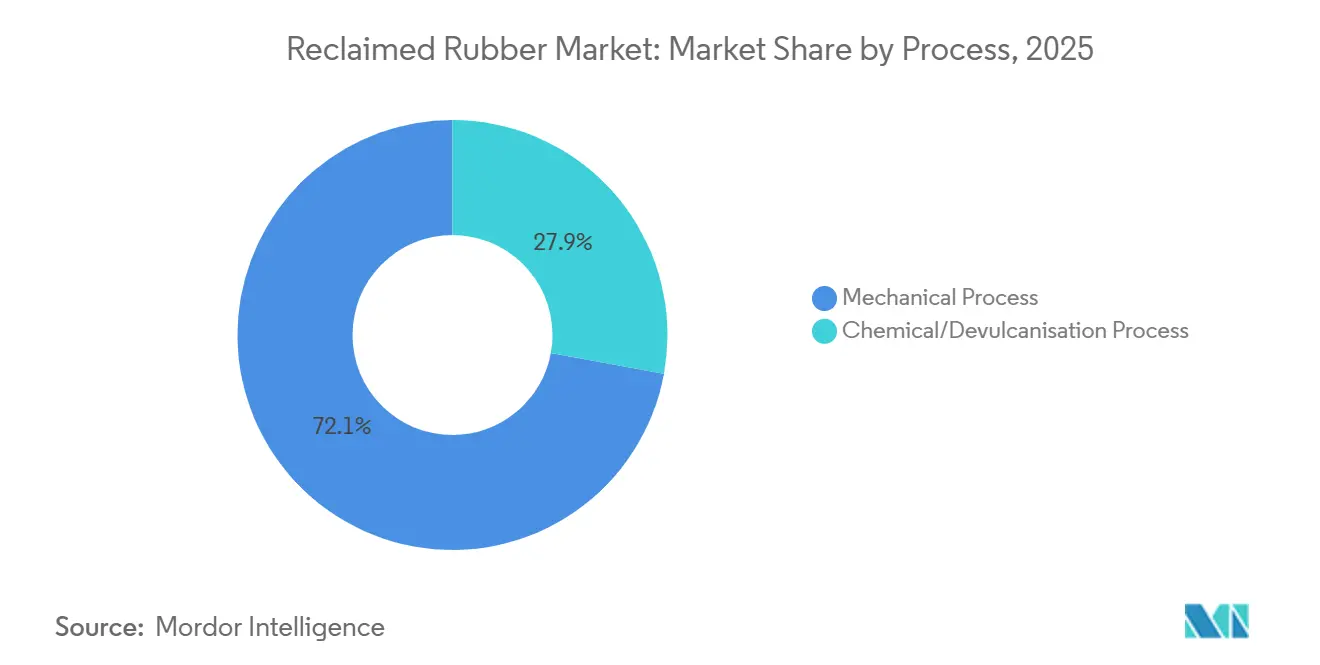

- By process, mechanical methods accounted for 72.11% of the reclaimed rubber market size in 2025, while chemical/devulcanisation is forecast to expand at 7.77% CAGR from 2026-2031.

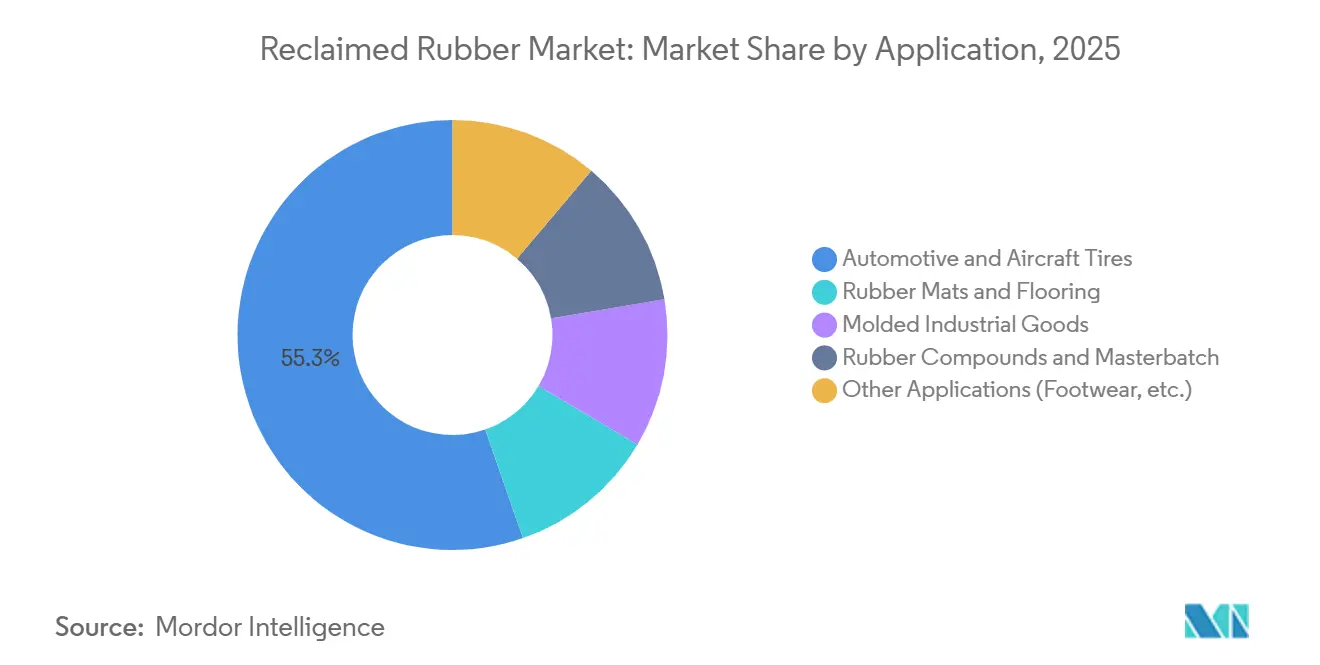

- By application, automotive tires captured 55.32% of revenue in 2025 and posted the highest 7.89% CAGR through 2031 as OEM sustainability mandates intensify.

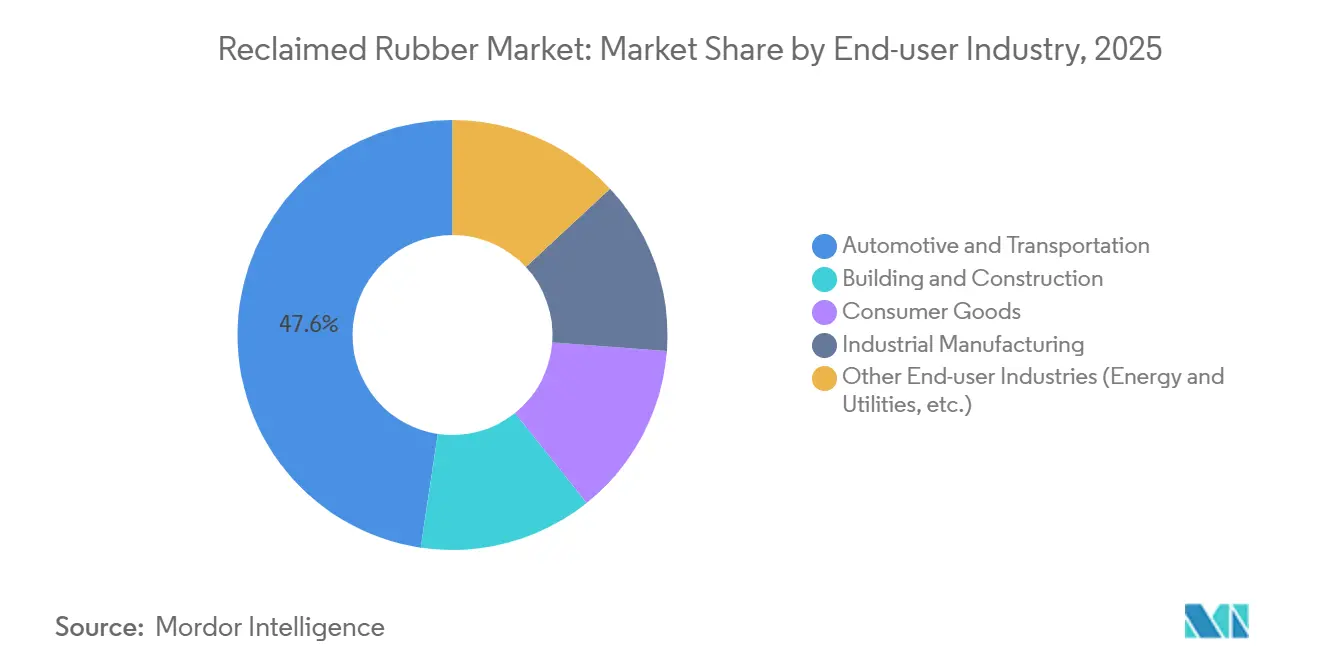

- By end-user industry, automotive and transportation held 47.63% share of the reclaimed rubber market size in 2025 and is projected to rise at an 8.03% CAGR between 2026-2031.

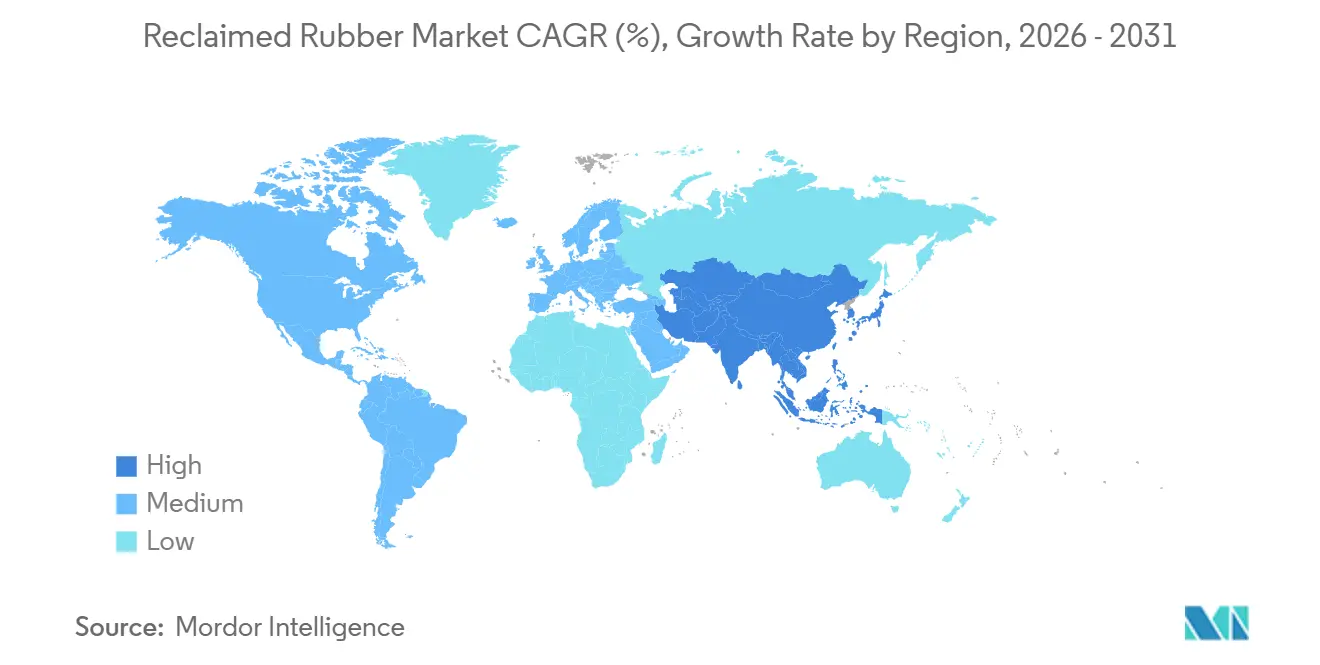

- By geography, Asia-Pacific commanded 46.22% of the reclaimed rubber market share in 2025 and records the quickest 7.88% CAGR from 2026-2031, driven by China’s 450 million-ton waste-rubber utilisation target.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Reclaimed Rubber Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-effective sustainable substitute for virgin rubber | +1.8% | Global, highest adoption in Asia-Pacific and Europe | Medium term (2-4 years) |

| Global waste-tire regulations accelerating recycling mandates | +1.5% | Global, led by EU, China, select US states | Short term (≤ 2 years) |

| OEM recycled-content targets for premium tire lines | +1.3% | North America, Europe, premium Asia-Pacific | Medium term (2-4 years) |

| Rapid devulcanization scale-up slashing energy use | +1.0% | Global, early adoption in Europe and Japan | Long term (≥ 4 years) |

| Renewable-fuel co-processing driving feedstock demand | +0.9% | Europe, North America, emerging Asia-Pacific cement sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost-Effective Sustainable Substitute for Virgin Rubber

In 2024-2025, reclaimed rubber showcased a significant cost advantage, being priced 30-50% lower than both virgin natural and synthetic elastomers. While natural rubber prices hovered between USD 1,800-2,100 per ton, whole tire reclaim was available at a more modest USD 800-1,200. This structural price gap arises because reclaimed rubber sidesteps both agricultural risk premiums and the volatility associated with petrochemical feedstocks. Tier-2 automotive suppliers have begun integrating 20-40% reclaimed content into products like floor mats, mud flaps, and dampers, all while adhering to ISO 9001 quality standards. In a notable move, Toyoda Gosei introduced weather-stripping featuring 20% recycled content for the Toyota RAV4 in December 2025, underscoring the material's validated performance. Over in the construction sector, REGUPOL is making waves by processing 115 million pounds of scrap rubber each year[1]REGUPOL, “Recycled Rubber Flooring Solutions,” REGUPOL.COM. Their efforts have led to a 40% reduction in material costs for flooring that meets ASTM D5603 impact standards, compared to using virgin EPDM. Additionally, with the EU Emissions Trading System expanding to cover waste incineration, carbon-pricing schemes are increasingly favoring reclaimed materials. This is largely due to the environmental benefit: diverting just 1 ton of tires from landfills can prevent the release of approximately 2.5 tons of CO₂-equivalent emissions.

Global Waste-Tire Regulations Accelerating Recycling Mandates

In 2024-2025, binding legislation converted voluntary corporate initiatives into enforceable mandates. The EU Waste Shipment Regulation 2024/1157 requires member states to focus on material recycling instead of energy recovery. Ireland's Extended Producer Responsibility (EPR) program, implemented in January 2025, obligates tire producers to fund collections and achieve a 90% recovery target by 2027. In China, certified recyclers receive a 70% VAT rebate and must use recycled content in non-critical tire compounds. This regulatory push has driven the establishment of facilities such as Yichang Hengdali's 100 kiloton per annum plant, which began operations in December 2024. California's SB 876 law requires a 5% crumb-rubber minimum in state-funded road asphalt, increasing demand for mechanical reclaim. Processors with ISO 14001 and ISCC PLUS certifications gain preferred-supplier status, while non-compliant operators face potential exclusion.

OEM Recycled-Content Targets for Premium Tire Lines

Global tire brands are making bold commitments to incorporate recycled materials. Michelin aims to use 100% renewable or recycled inputs by 2050. In 2022, it produced its first passenger tire with 45% sustainable content. Through partnerships with Enviro and Antin, Michelin is eyeing a pyrolysis capacity of 1 million tons per annum in Europe by the end of the decade. Continental's UltraContact NXT boasts up to 65% recycled and renewable materials, with a goal of reaching 40% across its portfolio by 2030. Bridgestone is targeting 70% sustainable components in its commercial truck tires, bolstered by its development of guayule latex. Achieving these ambitious targets hinges on high-purity reclaim and recovered carbon black, creating a premium pricing tier that benefits advanced processors.

Rapid Devulcanization Technology Scale-Up Slashing Energy Use

Commercial operations now utilize microwave, ultrasonic, and mechanochemical devulcanization, reducing energy demands to 1.2 kWh/kg compared to the 2.5-3.0 kWh/kg required by traditional autoclaves. In Japan and South Korea, ultrasonic systems achieve 85-90% tensile retention, with module costs below USD 0.8 million for a 5 tons per day output, resulting in payback periods of less than three years. The Xiangcheng Sanshan plant in China, operational since September 2025, uses twin-screw mechanochemical devulcanization to produce 50 kilotons of EPDM reclaim annually, addressing demand in roofing and automotive applications. KRAIBURG TPE has leveraged this advancement to develop a thermoplastic elastomer with 73% recycled content, meeting OEM standards for interior trims.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Variability in feedstock quality disrupting compound consistency | -0.7% | Global, acute where collection is informal | Short term (≤ 2 years) |

| Odor and VOC compliance limits for consumer goods | -0.5% | Europe and North America, emerging Asia-Pacific | Medium term (2-4 years) |

| Competition from bio-based elastomers in high-performance uses | -0.4% | North America and Europe premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Variability in Feedstock Quality Disrupting Compound Consistency

End-of-life tires, laden with mixed polymer ratios, steel belts, and road contaminants, face scrutiny upon arrival. Up to 15% of this incoming material gets downgraded or outright rejected due to excessive metal or chemical residues. To counteract this variability, downstream compounders resort to extra stabilizers, which inflate costs by an additional 5-8% and erode the economic advantage of reclamation. Automotive OEMs, adhering to Ford's FLTM BN 108-01 standard, mandate a tensile strength exceeding 10 MPa and an elongation surpassing 300%. This stipulation restricts reclaim loadings to below 30% unless manufacturers can guarantee high-purity streams. In 2022, China's tire-recovery rate stood at 52.73%, lagging behind the global average. This shortfall underscores the challenges posed by informal collection networks, which amplify quality risks. While investments in near-infrared sorting promise to mitigate this heterogeneity, they come at a steep price, demanding up to USD 0.5 million in capital per line.

Odor and VOC Compliance Limits for Consumer-Facing Goods

Residual sulfur compounds and aromatics emit odors that exceed the EU's 0.5% VOC limit for indoor rubber products[2]European Chemicals Agency, “REACH VOC Limits,” ECHA.EUROPA.EU. Meanwhile, Germany's AgBB guideline further tightens this limit to 0.3% specifically for flooring materials. Implementing secondary purification methods, such as solvent washing or thermal desorption, not only raises processing costs by 8-12% but also prolongs cycles by as much as two days. Footwear brands set an odor intensity cap at 2.5 on a 5-point hedonic scale. Achieving this threshold proves challenging without encapsulation, which can reduce tensile strength by 10-15%. As a result, the reclaimed rubber market finds its opportunities constrained, particularly in indoor and consumer applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Whole Tyre Reclaim (WTR) Dominance Drives Innovation

In 2025, Whole Tire Reclaim (WTR) accounted for 47.12% of the reclaimed rubber market. Projections indicate steady growth, with an expected CAGR of 7.69% through 2031. This growth is supported by the mechanical grinding process, which requires a relatively low capital investment of USD 2-5 million for a capacity of 10 kilotons per year. WTR's diverse polymer blend is utilized in vibration dampers, mud flaps, and floor mats. These applications help Tier-2 suppliers achieve cost reductions required by OEMs while maintaining compliance with ISO 9001 standards.

The demand for butyl and EPDM reclaims is increasing, driven by their use in roofing membranes and automotive weather-seals, which are shifting away from virgin-only material specifications due to carbon-reduction mandates. EPDM reclaim, priced 15-20% higher than WTR, uses devulcanization processes to meet the ozone-aging requirements necessary for single-ply roofing. High-Tech Reclaim and Swani Rubber supply these specialty grades to industrial compounders. As microwave and mechanochemical methods continue to improve, they are narrowing the performance gap with virgin polymers, which is expanding the range of potential end markets.

By Process: Mechanical Methods Lead, but Devulcanization Gains on Energy Efficiency

In 2025, mechanical grinding accounted for 72.11% of the market share due to its capability to process mixed feedstock and its energy requirement of 0.8-1.2 kWh/kg. In December 2025, Liberty Tire expanded its North Carolina facility with a USD 1.4 million investment, increasing capacity by 3.3 kilotons per year as part of its incremental growth strategy.

The chemical devulcanization segment is projected to grow at a CAGR of 7.77%, supported by the demand from OEMs for higher-purity feedstock used in premium tires. Microwave units in this segment consume 1.2-1.8 kWh/kg of energy while retaining up to 90% of tensile strength. Xiangcheng Sanshan's 50 kilotons per year plant in Henan reflects China's focus on advancing reclaim technology. Equipment in this segment now offers payback periods of less than three years, and reclaimed rubber used in premium applications achieves a 10-15% price premium compared to mechanical grades.

By Application: Automotive Tires Anchor Demand, Industrial Goods Diversify

In 2025, automotive and aircraft tires accounted for 55.32% of the total demand, and this segment is projected to grow at a CAGR of 7.89% through 2031. Major players like Michelin, Continental, and Bridgestone are channeling high-purity reclaimed materials into treads, not only to meet recycled-content targets but also to advocate for specifications that prioritize devulcanized grades over mechanical crumb. Rubber mats and flooring, historically dependent on styrene-butadiene crumb, now integrate color-stabilized WTR for playground surfacing, boosting indoor-air quality compliance. Molded industrial goods such as dock fenders and mining screens exploit reclaimed rubber’s damping traits to outlast virgin equivalents in abrasive settings.

Rubber compounds and masterbatch suppliers blend proprietary compatibilizers that let converters swap in 40–50% reclaim without process adjustments, catalyzing penetration into seals, bushings, and conveyor belts. Footwear brands source high-tensile natural-rubber reclaim for outsoles, cutting material cost while aligning with consumer eco-labels.

By End-User Industry: Automotive and Transportation Lead, Construction Expands

In 2025, the automotive and transportation sectors accounted for 47.63% of reclaimed rubber consumption. This share is poised to increase, driven by the demand from electric vehicle (EV) manufacturers for lightweight, high-purity reclaimed parts, particularly for vibration control. Ford has begun integrating reclaimed blends into key components like baffles, seals, and gaskets across its major platforms. Thanks to advancements in compatibilizers, the reclaimed rubber industry is successfully supplying these components, ensuring they meet original equipment manufacturer (OEM) standards for tensile strength and aging.

Building and construction integrates high-density crumb into rubberized concrete overlays, reducing thermal cracking and traffic noise. Seismic isolation bearings using EPDM reclaim expand in Japan and Chile, where earthquake codes tighten. Consumer-goods firms insert reclaim into yoga mats, pet products, and tool grips, leveraging marketing stories around tire-to-table circularity. Industrial manufacturing blends reclaim into conveyor belts that run at moderate temperatures, gaining cost savings without sacrificing tear resistance. Energy utilities apply antioxidant-treated reclaim in cable-sheathing compounds to meet flame-retardancy norms. This multi-industry adoption insulates the reclaimed rubber market from single-sector downturns and reinforces steady long-term growth.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 46.22% of global revenue, projections indicate a growth rate of 7.88% CAGR extending to 2031. In 2024, China's recycled-tire volume reached 9 million tons, marking a 20% year-on-year increase, supported by a newly introduced 70% VAT rebate for certified processors. Provinces such as Hubei and Shandong expanded their capacities by over 150 kilotons annually during 2024-2025. Meanwhile, India's Swani Rubber and Thailand's Green Rubber Energy are increasing specialty and pyrolysis lines to address demand in automotive corridors.

North America maintains a significant position. Federal infrastructure funding of USD 1.2 billion is allocated to waste-to-energy projects, influencing feedstock pricing. At the same time, state regulations, such as California's SB 876, support the market for crumb-rubber asphalt. In 2023, the U.S. processed 240 million out of 300 million scrap tires, converting 75 million to ground rubber and utilizing 96 million for energy. Canada and Mexico, both part of the USMCA automotive chain, contribute an additional 15-18% to the regional demand.

Europe's contributions are shaped by mandatory take-back and Extended Producer Responsibility (EPR) frameworks. Genan, with a grinding capacity of 400 kilotons per year, operates across Denmark, Portugal, and Germany, and is advancing textile-fraction valorization. Michelin's pyrolysis initiative in Sweden serves as a model for a closed-loop recovered carbon black supply, integrated into European tire manufacturing plants. EU policies aim to increase the average recycled raw material content beyond 23% by 2030, indicating a rise in demand for high-spec reclaim.

In South America, Brazil enforces manufacturer take-back, while Argentina introduced its first rubber-modified highway section, incorporating 10% tire powder, in October 2025. The Middle East and Africa, present potential for growth. Both Saudi Arabia and South Africa are considering the implementation of landfill bans and green public procurement regulations.

Competitive Landscape

The reclaimed rubber market remains fragmented. Leading the pack are Michelin, Genan Holding A/S, GRP Ltd., Liberty Tire Recycling, and Rolex Reclaim Pvt. Ltd. In 2024, Genan reported a 9% revenue uptick, reaching EUR 63.7 million, driven by robust demand. The company has innovatively turned once-waste textile fibers into a monetizable asset, cleaning and pelletizing them for geotextiles, thus diversifying its income. Liberty Tire, aiming to fortify its dominance in mechanical-crumb rubber, showcased its strategy with a USD 1.4 million investment in North Carolina, made in December 2025.

Tech-savvy players are vying for premium tire contracts. Mitsubishi Chemical is venturing into devulcanized EPDM for high-voltage EV seals, harnessing its proprietary polymer science to meet OEM durability standards. Marubeni's strategic move, investing USD 7 million for a 32% stake in Green Rubber Energy, underscores the importance of pyrolysis assets, which seamlessly blend carbon-black recovery with tire-pyrolysis oil sales.

Certification and traceability set suppliers apart. In July 2025, HANWA secured ISCC PLUS and ISCC EU certifications, subsequently backing a Thai pyrolysis plant with a capacity of 100 kilotons per year. KRAIBURG TPE, utilizing devulcanized feedstock, produces TPEs with 73% recycled content. These TPEs not only meet automotive interior air quality standards but have also landed contracts with European clients. However, smaller processors lacking ISO 14001 certification or consistent batch quality may find themselves relegated to less lucrative civil engineering markets.

Reclaimed Rubber Industry Leaders

GRP LTD.

Rolex Reclaim Pvt. Ltd.

Liberty Tire Recycling

Genan

MICHELIN

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Liberty Tire Recycling added 3.3 kilotons per year of mechanical crumb capacity at its North Carolina site through a USD 1.4 million upgrade.

- December 2025: Toyoda Gosei commercialized weather-stripping with 20% recycled rubber for the Toyota RAV4, confirming reclaim’s viability in durability-critical seals.

Global Reclaimed Rubber Market Report Scope

Reclaimed rubber is a sustainable material produced by devulcanizing and processing waste rubber products, such as used tires and tubes, back into a reusable raw material. It acts as a cost-effective, environmentally friendly alternative to virgin rubber, offering high elasticity and durability for industrial applications like tire manufacturing, mats, and automotive parts.

The market is segmented by product type, process, application, and end-user industry. By product type, the market is segmented into whole tire reclaim (WTR), butyl reclaim, ethylene propylene diene monomer (EPDM) reclaim, and other product types (including natural rubber reclaim and latex reclaim). By process, the market is segmented into mechanical process and chemical/devulcanisation process. By application, the market is segmented into automotive and aircraft tires, rubber mats and flooring, molded industrial goods, rubber compounds and masterbatch, and other applications (including footwear). By end-user industry, the market is segmented into automotive and transportation, building and construction, consumer goods, industrial manufacturing, and other end-user industries (including energy and utilities). The report also covers the market size and forecasts for reclaimed rubber in 19 countries across the world. For each segemnt market sizing and forecasts are provided in terms of value (USD).

| Whole Tire Reclaim (WTR) |

| Butyl Reclaim |

| Ethylene Propylene Diene Monomer (EPDM) Reclaim |

| Other Product Types (Natural Rubber Reclaim, Latex Reclaim, etc.) |

| Mechanical Process |

| Chemical/Devulcanisation Process |

| Automotive and Aircraft Tires |

| Rubber Mats and Flooring |

| Molded Industrial Goods |

| Rubber Compounds and Masterbatch |

| Other Applications (Footwear, etc.) |

| Automotive and Transportation |

| Building and Construction |

| Consumer Goods |

| Industrial Manufacturing |

| Other End-user Industries (Energy and Utilities, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Whole Tire Reclaim (WTR) | |

| Butyl Reclaim | ||

| Ethylene Propylene Diene Monomer (EPDM) Reclaim | ||

| Other Product Types (Natural Rubber Reclaim, Latex Reclaim, etc.) | ||

| By Process | Mechanical Process | |

| Chemical/Devulcanisation Process | ||

| By Application | Automotive and Aircraft Tires | |

| Rubber Mats and Flooring | ||

| Molded Industrial Goods | ||

| Rubber Compounds and Masterbatch | ||

| Other Applications (Footwear, etc.) | ||

| By End-user Industry | Automotive and Transportation | |

| Building and Construction | ||

| Consumer Goods | ||

| Industrial Manufacturing | ||

| Other End-user Industries (Energy and Utilities, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will the reclaimed rubber market be by 2031?

It is projected to reach USD 2.46 billion by 2031, expanding at a 7.11% CAGR from 2026 to 2031.

Which product category leads reclaimed-rubber demand?

Whole Tire Reclaim held 47.12% market share in 2025 and remains the dominant grade through 2031.

What is driving reclaimed-rubber uptake in automotive tires?

Automaker recycled-content mandates and tire-maker pledges, such as Michelin’s and Continental’s, are boosting high-purity reclaim use in premium treads.

Which region grows fastest for reclaimed rubber?

Asia-Pacific shows the highest regional CAGR at 7.88%, lifted by Chinese tax incentives and capacity additions.

Page last updated on: