Fire-Retardant Treated Wood Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

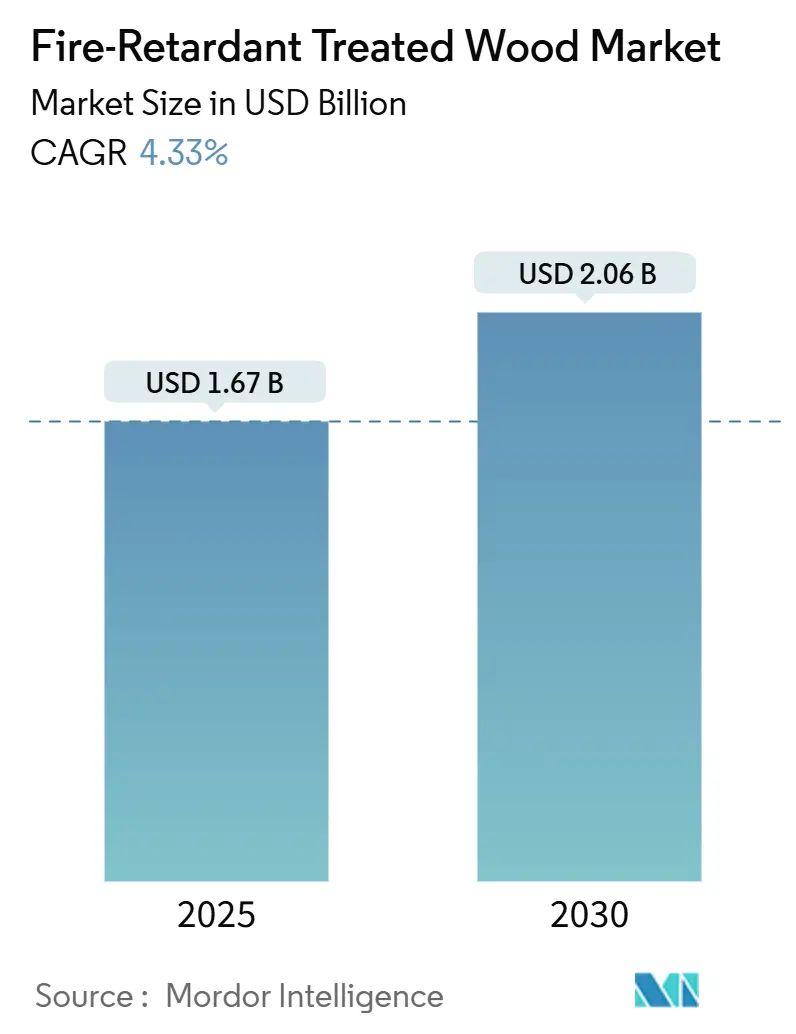

| Market Size (2025) | USD 1.67 Billion |

| Market Size (2030) | USD 2.06 Billion |

| Growth Rate (2025 - 2030) | 4.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fire-Retardant Treated Wood Market Analysis by Mordor Intelligence

The Fire-Retardant Treated Wood Market size is estimated at USD 1.67 billion in 2025, and is expected to reach USD 2.06 billion by 2030, at a CAGR of 4.33% during the forecast period (2025-2030).

Solid demand stems from regulatory tightening, wildfire-driven insurance requirements, and improving treatment chemistries. Commercial builders prefer the material because it pairs code compliance with cost-effective installation, while mass-timber architects increasingly specify it to safeguard taller wooden structures. In parallel, building-code harmonization across major economies lowers certification costs, which enhances cross-border tendering opportunities and accelerates the adoption curve. Finally, the ongoing shift toward climate-adapted infrastructure positions the fire-retardant treated wood market as an indispensable component of resilient construction portfolios.

Key Report Takeaways

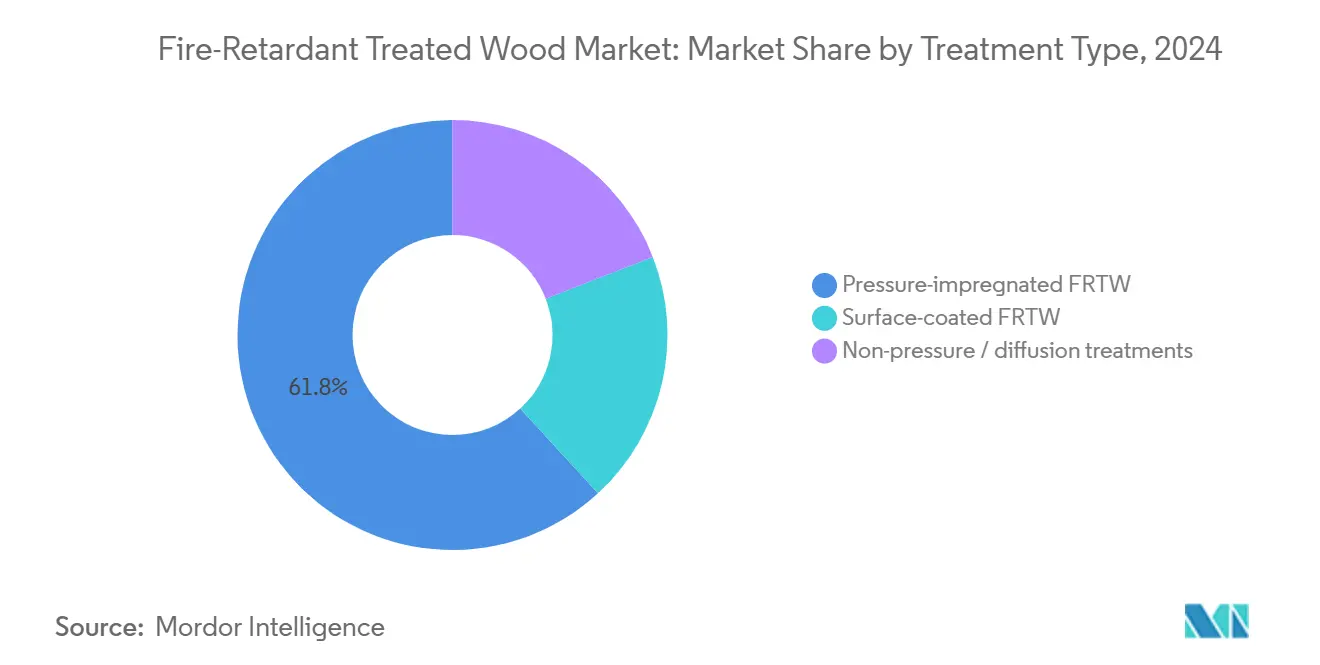

- By treatment type, pressure-impregnated wood led with 61.83% of the Fire-retardant Treated Wood market share in 2024; surface-coated products are poised for the fastest 4.68% CAGR to 2030.

- By product type, plywood captured 46.71% share of the Fire-retardant Treated Wood market size in 2024, while other product types are projected to expand at a 4.75% CAGR through 2030.

- By application, interior uses accounted for a 59.28% share of the Fire-retardant Treated Wood market size in 2024 and exterior applications are advancing at a 4.96% CAGR to 2030.

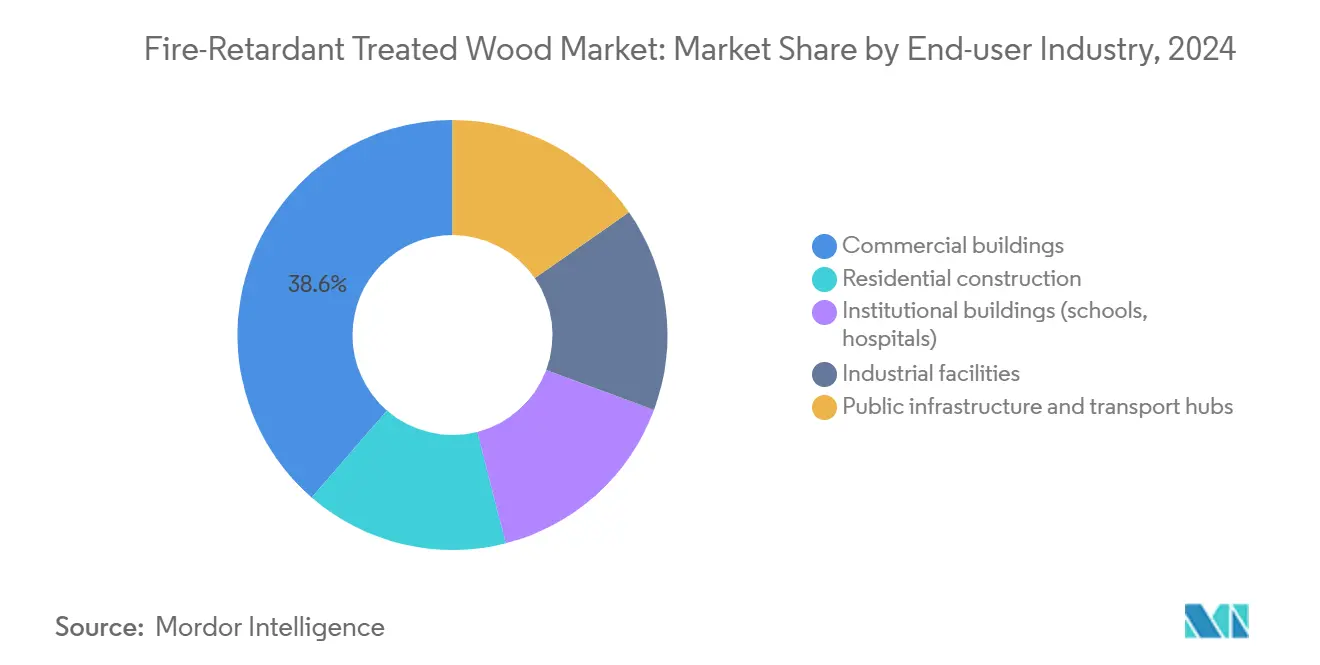

- By end-user industry, commercial buildings dominated with 38.65% revenue share in 2024; public infrastructure and transport hubs represent the fastest-growing segment at 5.18% CAGR through 2030.

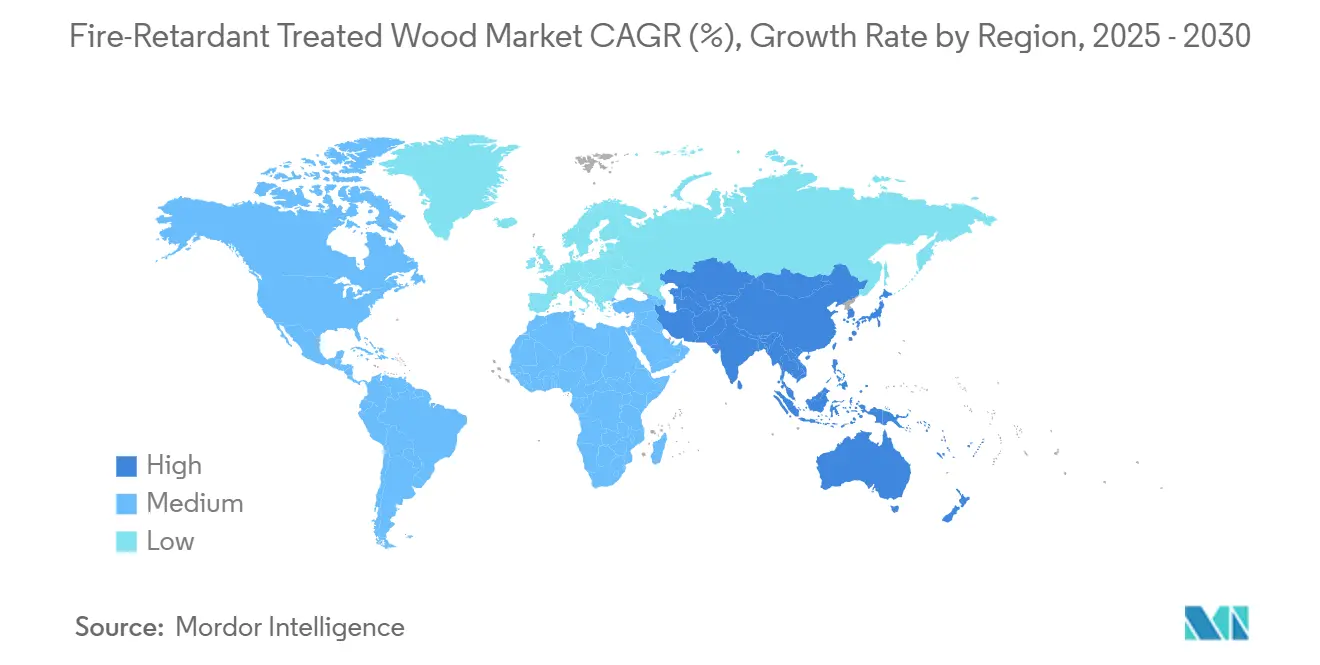

- By geography, North America commanded a 43.36% share in 2024, while Asia-Pacific is the most dynamic region at a 5.05% CAGR from 2025-2030.

Global Fire-Retardant Treated Wood Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Fire-safe Construction Materials | +1.2% | Global; North America & Europe concentrated | Medium term (2-4 years) |

| Strict Building Codes and Fire-safety Regulations | +1.5% | North America & EU primary; APAC emerging | Long term (≥ 4 years) |

| Increasing Use in Commercial and Institutional Buildings | +0.8% | Global; led by North America & APAC | Medium term (2-4 years) |

| Growth in Urban Infrastructure and Public-safety Initiatives | +0.6% | APAC core; spill-over to MEA | Long term (≥ 4 years) |

| Adoption in Off-site Modular Timber Construction Supply Chains | +0.3% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Fire-safe Construction Materials

Wildfire intensity in western North America and southern Europe reshapes specification practices, prompting jurisdictions to treat ignition resistance as mandatory rather than discretionary. California’s Chapter 7A now requires Class A materials in Wildland–Urban Interface zones, directly boosting demand among single-family and multifamily builders[1]California Department of Forestry and Fire Protection, “California Building Code Chapter 7A,” calfire.ca.gov. Insurers layer additional pressure by tying coverage to materials that reduce loss severity, turning fire-retardant-treated wood from a compliance cost into a premium-discount enabler. The United States trend reverberates internationally as Australia’s performance-based codes incorporate detailed fire-engineering pathways that frequently resolve in favor of impregnated solutions when risk audits prioritize life-safety over upfront cost. Manufacturers capitalize by launching code-specific offerings, TimberTech decking, for example, secured California State Fire Marshal approval, positioning FRTW as a differentiator across exterior product lines. The private sector’s pivot from reactive replacement to proactive risk mitigation ultimately enlarges the addressable Fire-retardant Treated Wood market.

Strict Building Codes and Fire-safety Regulations

The 2024 International Building Code clarified that only chemically impregnated products qualify as fire-retardant treated wood, closing loopholes that previously allowed surface-only coatings into occupancy-critical projects. NFPA 703 revisions 2023 introduced more rigorous field-retention and weathering tests, raising capital and technical barriers for new entrants while rewarding established formulations with proven third-party data. China’s GB 55037-2022 mandates, effective June 2023, bring the world’s largest construction economy closer to U.S. and EU benchmarks, opening a multi-billion-dollar channel for compliant products. Japan’s Ministry of Land, Infrastructure, Transport and Tourism now allows wooden structures to claim a 50-year service life, provided embedded FRTW maintains performance across periodic inspections, pushing specifiers toward premium treatments that resist chemical migration. Cross-border consistency reduces duplicative certification expenses for multinational developers, sustaining a steady CAGR contribution for the Fire-retardant Treated Wood market.

Increasing Use in Commercial and Institutional Buildings

Hospitals, governed by NFPA 99, require fire-retardant interiors in patient areas; global health-care construction outlays exceed USD 400 Billion annually, providing durable volume for compliant suppliers. School modernizations rely on FRTW to improve safe egress in multi-story expansions. Mass-timber skyscrapers such as Brock Commons prove that treated glulam and CLT can meet performance-based fire tests without sacrificing carbon credentials, prompting architects in North America and Japan to align structural innovation with stringent life-safety codes. Viance’s D-Blaze line, recently certified GREENGUARD Gold, solves earlier VOC concerns that had constrained use in sensitive occupancies, broadening addressable markets for low-emission interior assemblies. Comparative life-cycle costing shows that compliant FRTW subsystems often install faster and cheaper than non-combustible assemblies, supporting the topline of the fire-retardant treated wood market even in inflationary climates.

Growth in Urban Infrastructure and Public-safety Initiatives

Airport terminals like Helsinki and Portland International adopt architecturally exposed treated wood canopies, each triggering bespoke fire-modeling protocols that elevate global visibility for the category. Asia-Pacific government tenders now score bids on forward-facing resilience metrics, giving a premium to fire-retardant wood when thermal inertia and evacuation modeling validate performance. Utility operators such as Bonneville Power Administration have started wrapping wooden distribution poles with fire-activated mesh, demonstrating that FRTW can supplement rather than replace existing assets, which stretches supplier margins into the infrastructure segment. ASTM’s forthcoming pole-fire test standard institutionalizes that approach, making the specification process less discretionary across North America. As smart-city masterplans emphasize multi-hazard resilience, embedded fire-resistant timber becomes a go-to solution in landscape and street-furniture packages, adding a steady incremental layer to the fire-retardant treated wood market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Versus Non-treated Wood | -0.9% | Global; acute in price-sensitive markets | Medium term (2-4 years) |

| Limited Moisture-resistance in Exterior Applications | -0.4% | North America & Europe; humid zones | Long term (≥ 4 years) |

| Mislabeling Scandals Eroding Specifier Confidence | -0.2% | North America primary | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost Versus Non-treated Wood

Premiums of 25-40% over untreated lumber persist because impregnation requires additional kiln time, specialized autoclaves, and in-yard segregation, all of which raise carrying costs for distributors. When lumber indices spike, the absolute differential widens, encouraging contractors to value-engineer toward the legal minimum or pivot to steel framing if cost pass-through jeopardizes bid competitiveness. Emerging-market builders, already navigating currency risk, often view the premium as prohibitively high unless subsidized through insurance rebates. During late-2024 monetary tightening, commercial developers postponed envelope upgrades, illustrating price sensitivity despite regulatory momentum. These dynamics trim some growth potential from the fire-retardant treated wood market until economies of scale or alternative chemistries compress the cost delta.

Limited Moisture-resistance in Exterior Applications

Laboratory weathering shows that repeated wet-dry cycling can leach phosphates and borates, reducing time-to-ignition below code thresholds within three to five years in coastal climates. To counteract, specifiers must overlay paint or film-forming coatings, which adds upfront labor and ongoing maintenance. Some authorities restrict FRTW use on unprotected facades, curbing volumes in siding and soffits exactly where wildfire code push could otherwise generate upside. Manufacturers respond with silicone-modified surface sealants, yet long-term field data remain limited, tempering architects' confidence. Buyers may favor non-combustible fiber-cement or engineered stone, capping exterior share within the fire-retardant treated wood market without clear warranties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Pressure Methods Dominate Despite Surface Innovation

Pressure-impregnated solutions held 61.83% of 2024 revenue and continue to anchor structural applications. The Fire-retardant Treated Wood market size for pressure-treated categories will rise steadily as institutions refurbish legacy facilities that originally used older, less effective salts. While starting from a smaller base, surface-coated lines accumulate a 4.68% CAGR because new polymeric carrier systems now pass extended weathering tests, unlocking decks and soffits that previously required non-combustible panels. Over the forecast window, multi-factor product selection will pivot on compliance transparency and total installed cost rather than the binary impregnation versus surface debate, ensuring each treatment niche secures discrete but profitable lanes in the wider fire-retardant treated wood market.

Investment returns favor pressure networks because capex is amortized across volume utility poles, but surface innovators target higher margin refurbishment markets where aesthetic retention earns premiums. Promoters of diffusion and spray-on methods will focus on decorative ceilings and modular kiosks where structural contribution is secondary, allowing them to capture design-driven demand cycles. The net result is a segmented battlefield in which established incumbents protect commodity channels while agile entrants cherry-pick specialty use cases, collectively reinforcing an industry-wide CAGR even as internal mix shifts.

By Product Type: Plywood Leadership Faces Engineered Wood Challenge

Plywood delivered 46.71% 2024 revenue, benefiting from mature supply chains and proven fastener protocols. That said, the fire-retardant treated wood market share is gradually tilting toward engineered lumber and cross-laminated timber (CLT) panels propelled by mass-timber codes that authorize 18-story structures. Other product types enjoy a 4.75% CAGR as developers favor larger format panels that reduce onsite labor and accelerate schedules. Dimensional lumber contributes steady base load for light-frame exterior walls, whereas oriented strand board (OSB) faces substitution pressure from newer fire-rated sheathing that pairs gypsum and treated veneer in a single panel. Decking and fencing increments gain tailwinds from wildfire insurance rebates, especially in Colorado, Oregon, and British Columbia.

Competitive hierarchy hinges on the cost per square foot of fire-rated coverage. Plywood remains economical but loses design cachet to visually appealing cross-laminated timber (CLT) that supports exposed-beam aesthetics. Weyerhaeuser’s half-billion-dollar TimberStrand expansion signals faith in engineered formats, which combine structural capacity with built-in flame-spread indices suitable for open atriums. Long-term scenario modeling indicates plywood will retain plurality but cede a double-digit share to engineered alternatives by 2030 as architects seek carbon-storing yet code-compliant materials. As a result, product diversification strategies become pivotal for mills aiming to defend relevance within the evolving fire-retardant treated wood market.

By Application: Interior Dominance Challenged by Exterior Growth

Interior assemblies accounted for 59.28% 2024 demand, driven by life-safety codes prioritizing egress and structural integrity. Flooring systems and sub-floors rely on FRTW to delay burn-through beneath finish layers, while roof trusses employ it to safeguard fire service time. The Fire-retardant Treated Wood market size for interiors will expand with urban office renovation cycles. However, exterior uptake accelerates at 4.96% CAGR after California, New South Wales, and Greece advanced façade codes that require ignition resistance in high-risk zones. Recent polymeric sealants improve weather stability, so treated siding retains Class A ratings for a decade, making it viable for beachfront resorts.

Decking represents the bullet growth node as outdoor living budgets rise post-pandemic and homeowners leverage insurance credits by swapping combustible planks for approved FRTW. Pergolas, carports, and over-water boardwalks follow suit, though moisture-related warranty clauses still constrain full-scale adoption in tropical latitudes. Code officials remain vigilant about field cuts that expose untreated cores, resulting in specialized edge-treatment kits bundled with manufacturer warranties. Over time, exterior lines will chip away at interior dominance but will not overtake it by 2030, maintaining a healthy dual-engine dynamic for the entire fire-retardant treated wood market.

By End-user Industry: Commercial Leadership Amid Infrastructure Acceleration

Commercial complexes captured 38.65% 2024 revenue, anchored by office towers, retail malls, and data centers that integrate FRTW framing to optimize leasable heights without sacrificing fire walls. Institutional buyers, particularly education boards and health networks, reinforce baseline volumes, yet public infrastructure and transport hubs sprint ahead at 5.18% CAGR. The Fire-retardant Treated Wood market size for airport and rail concourse roofs climbs as architects flaunt timber’s aesthetics while compliance teams lock in performance via impregnation.

Industrial adoption remains episodic, focused on sectors with combustible process inputs that value char-forming properties. Residential uptake is fragmented because only a subset of municipalities mandates FRTW for single-family homes, though rising wildfire premiums are nudging adoption upward. The public works surge, exemplified by Portland International Airport’s 9-acre wooden diaphragm, signals an inflection where government procurement tilts toward carbon-beneficial materials that satisfy upgraded the National Fire Protection Association (NFPA)-category occupancy ratings. Consequently, the demand landscape broadens beyond speculative real-estate cycles, cushioning the fire-retardant treated wood market against macro volatility.

Geography Analysis

North America holds 43.36% of the global 2024 revenue. Intensified wildfire seasons, and insurer-driven retrofits secure a stable base for the region. Canadian code convergence simplifies cross-border supply, and utility-pole wrap programs add incremental volume.

Asia-Pacific is posting the strongest 5.05% CAGR as China’s GB 55037-2022 regulates Class B1 performance and Japan stretches timber service life to 50 years. ASEAN urbanization funnels demand into mid-rise hospitality and mixed-use complexes, with local mills importing Western impregnation technology.

Europe charts moderate growth on the back of carbon targets; Nordic nations lead, while southern markets lag due to fiscal austerity. South America and MEA contribute modestly; there are still formative regulatory frameworks, but infrastructure stimulus in Brazil and the United Arab Emirates signals future upside. Collectively, geographical diversification steadies the Fire-retardant Treated Wood market against localized housing or policy shocks.

Competitive Landscape

The Fire-Retardant Treated Wood market is moderately concentrated. Koppers Holdings, Viance, and Weyerhaeuser anchor the top tier through vertical integration, proprietary chemistry, and continent-spanning distribution. Koppers paid USD 100 Million for Brown Wood Preserving in 2024 to secure pole capacity in the Midwest, underlining inorganic growth tactics. Viance differentiates via DCOI-based UltraPole NXT, touting lower aquatic toxicity and 50-year limited warranties. New entrants gravitate toward eco-label-driven surface coatings as a market gap, but heavy R&D spend plus longer certification cycles raise competitive barriers. Long-term success favors suppliers who fuse chemical innovation with an airtight chain-of-custody, thus rebuilding trust after prior scandals and sustaining value capture in the Fire-retardant Treated Wood market.

Fire-Retardant Treated Wood Industry Leaders

Viance

Flameproof Company

Arxada

HOOVER TREATED WOOD PRODUCTS

Koppers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: T2EARTH, LLC unveiled OnWood Plywood, the latest eco-friendly wood product treated for fire retardancy (FRTW). OnWood, crafted without toxic chemicals, offers strength, Class A fire retardancy, and sustainability. This makes it a healthier, high-performing, and cost-effective choice for builders and developers in fire-prone areas.

- May 2025: Culpeper Wood Preservers, a manufacturer of pressure-treated lumber, is expanding its FlamePRO fire-retardant treated lumber product offerings into the Northeast region of the United States. The availability of Culpeper fire-treated wood will help serve the multifamily and commercial construction sectors across the region by making faster delivery times available.

Global Fire-Retardant Treated Wood Market Report Scope

| Pressure-impregnated FRTW |

| Surface-coated FRTW |

| Non-pressure / diffusion treatments |

| Plywood |

| Dimensional lumber |

| Oriented strand board (OSB) |

| Decking and fencing |

| Other Product Types (sheathing, siding, CLT panels) |

| Interior applications | Flooring and sub-flooring |

| Ceilings and roof trusses | |

| Wall partitions | |

| Exterior applications | Facades and cladding |

| Decks and patios | |

| Outdoor structures |

| Residential construction |

| Commercial buildings |

| Institutional buildings (schools, hospitals) |

| Industrial facilities |

| Public infrastructure and transport hubs |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Treatment Type | Pressure-impregnated FRTW | |

| Surface-coated FRTW | ||

| Non-pressure / diffusion treatments | ||

| By Product Type | Plywood | |

| Dimensional lumber | ||

| Oriented strand board (OSB) | ||

| Decking and fencing | ||

| Other Product Types (sheathing, siding, CLT panels) | ||

| By Application | Interior applications | Flooring and sub-flooring |

| Ceilings and roof trusses | ||

| Wall partitions | ||

| Exterior applications | Facades and cladding | |

| Decks and patios | ||

| Outdoor structures | ||

| By End-user Industry | Residential construction | |

| Commercial buildings | ||

| Institutional buildings (schools, hospitals) | ||

| Industrial facilities | ||

| Public infrastructure and transport hubs | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Fire-retardant Treated Wood market in 2025?

The Fire-retardant Treated Wood market size reached USD 1.67 Billion in 2025.

What is the projected CAGR through 2030?

The market is forecast to record a 4.33% CAGR between 2025 and 2030.

Which region grows the fastest?

Asia-Pacific leads with a 5.05% CAGR, propelled by China’s and Japan’s new fire-safety mandates.

Which treatment type holds the greatest share?

Pressure-impregnated wood dominates with 61.83% of 2024 revenue.

Why are exterior applications expanding quickly?

Wildfire mitigation rules and improved moisture-resistant coatings push exterior demand at a 4.96% CAGR.

Page last updated on: