Plywood Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

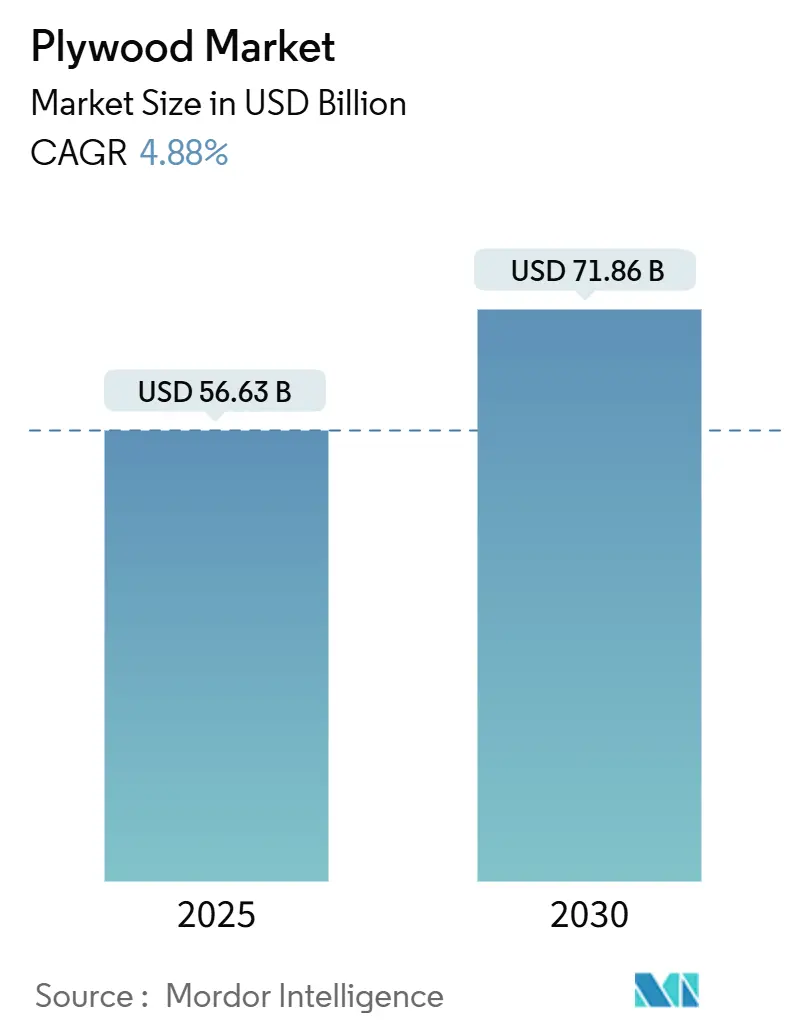

| Market Size (2025) | USD 56.63 Billion |

| Market Size (2030) | USD 71.86 Billion |

| Growth Rate (2025 - 2030) | 4.88% CAGR |

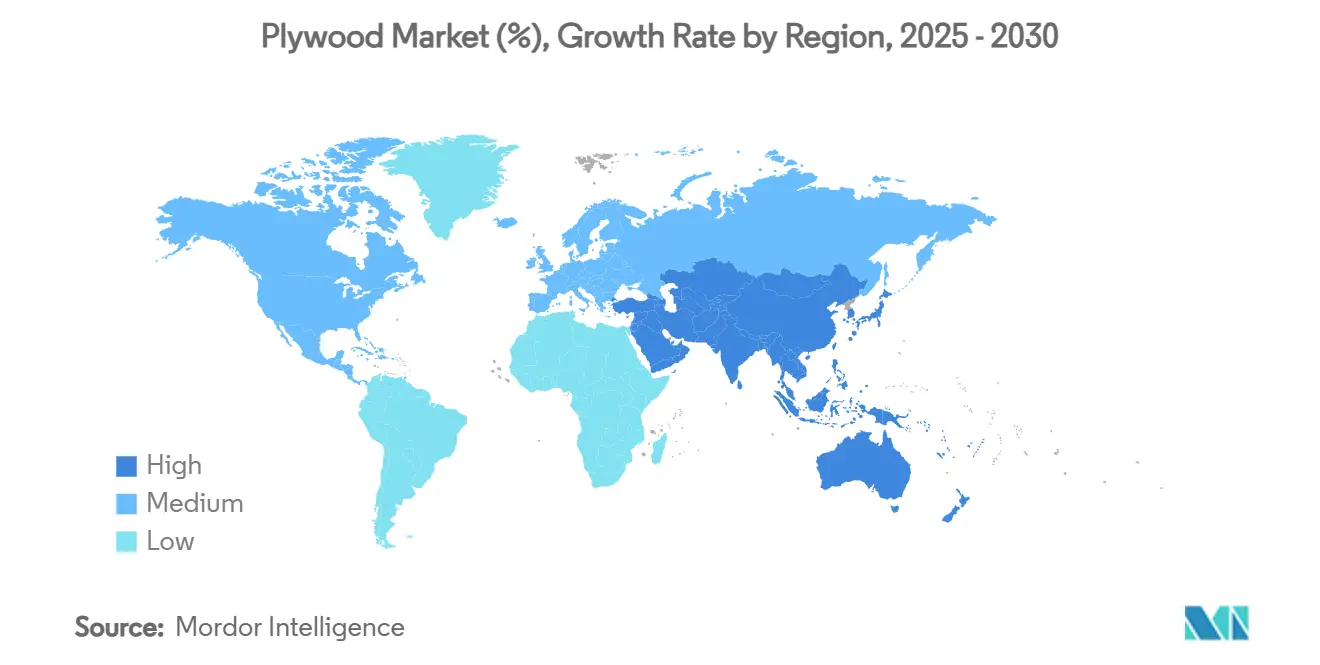

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

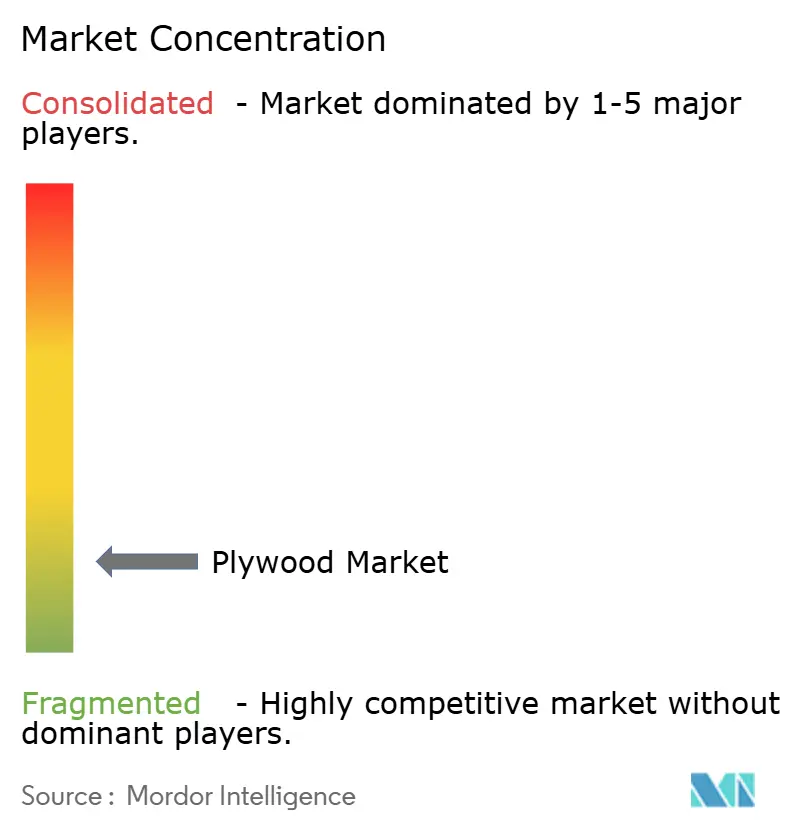

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plywood Market Analysis by Mordor Intelligence

The Plywood Market size is estimated at USD 56.63 billion in 2025, and is expected to reach USD 71.86 billion by 2030, at a CAGR of 4.88% during the forecast period (2025-2030).

Construction activity in developing nations, modular building uptake, and rising furniture demand continue to outweigh competitive pressure from OSB panels and tighter environmental rules. Expansive public‐sector projects in Asia–Pacific and the Gulf states, fire‐safety focused product innovation, and the shift from single-use plastics to reusable wood packaging further strengthen the plywood market outlook. At the same time, looming carbon-border taxes and stricter traceability requirements motivate producers to upgrade supply chains and cut emissions, laying a pathway for higher-margin certified products. Competitive intensity remains high as regional mills scale up capacity and larger players deploy AI-driven production systems to improve yields and pare costs.

Key Report Takeaways

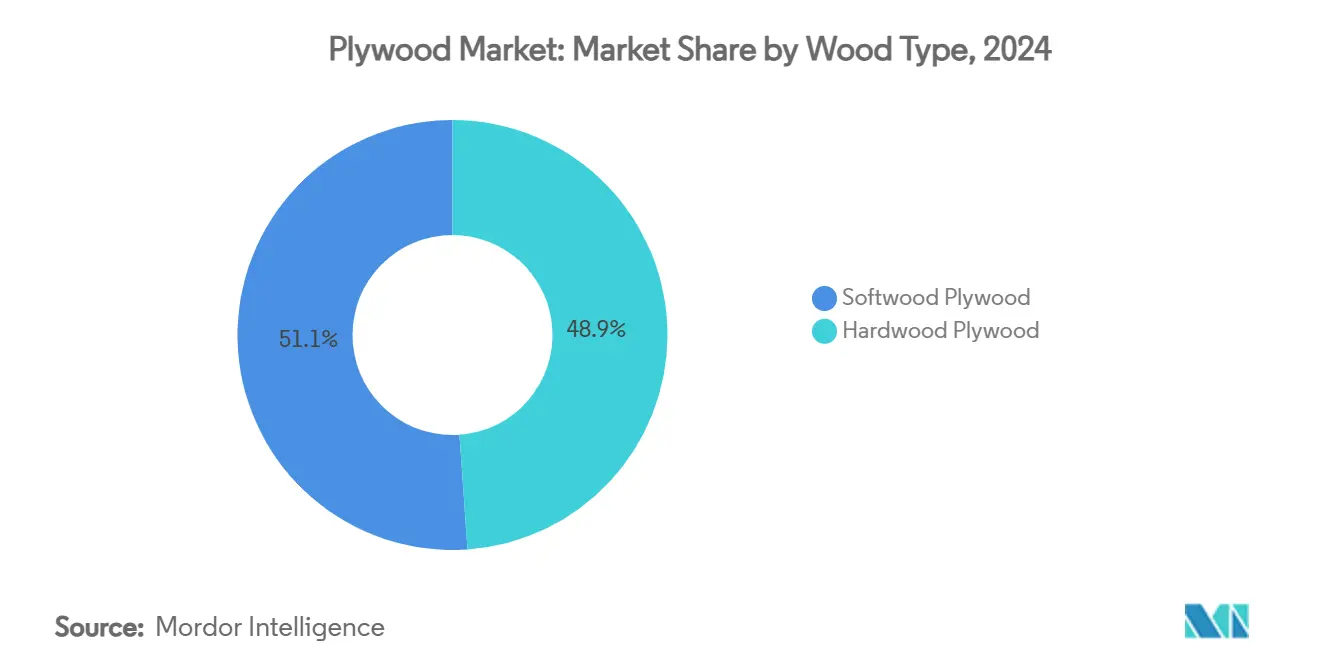

- By wood type, softwood plywood led with 51.12% of plywood market share in 2024 and enjoys the fastest expansion at 6.12% CAGR through 2030.

- By grade, MR grade remained dominant at 33.35% revenue share in 2024; fire-resistant grade is set to grow quickest at 6.32% CAGR to 2030.

- By application, furniture captured 37.72% share of the plywood market size in 2024, while paneling and cladding advance at a 5.66% CAGR to 2030.

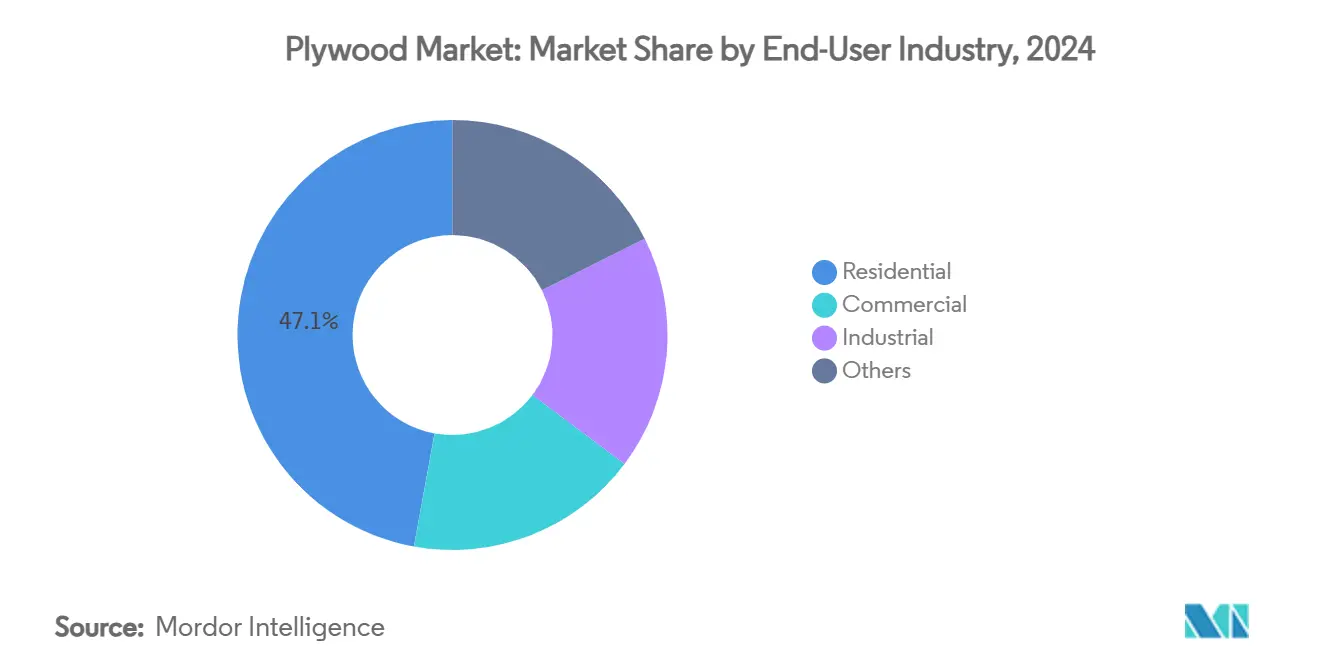

- By end user, residential construction accounted for 47.13% demand in 2024; the industrial segment shows the highest CAGR at 5.78% through 2030.

- By geography, Asia–Pacific dominated the plywood industry with a 57.12% share in 2024, whereas the Middle East & Africa segment is projected to post the fastest 5.62% CAGR to 2030.

Global Plywood Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming construction spending in emerging economies | +1.2% | Asia–Pacific; Middle East & Africa | Medium term (2-4 years) |

| Furniture and interior décor demand surge | +0.9% | Global, strongest in Asia–Pacific | Short term (≤ 2 years) |

| Adoption of modular/off-site building methods | +0.7% | North America and EU, spreading to Asia–Pacific | Long term (≥ 4 years) |

| Shift from one-way plastics to plywood in industrial packaging | +0.5% | Europe and North America | Medium term (2-4 years) |

| Fire-retardant bio-adhesive formulations for mass-timber high-rises | +0.4% | North America and EU urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Booming Construction Spending in Emerging Economies

Saudi Arabia’s Vision 2030 programme alone earmarks more than USD 1.25 trillion for buildings and infrastructure, pushing demand for formwork, interiors, and temporary structures that rely on cost-efficient plywood . Similar public investment pipelines across India, Indonesia, and Vietnam sustain sizeable order books for regional mills. Plywood intensity per construction dollar remains higher in emerging markets than in developed economies, amplifying volume growth. Suppliers that can guarantee on-time delivery and uniform quality are positioned to lock in long-term contracts for mega-projects.

Furniture & Interior Decor Demand Surge

Regional veneer hubs such as Gujarat report brisk sales as middle-income consumers favor natural finishes, spurred by price-inflated laminates and shifting aesthetic trends. The resulting plywood uptake spans cabinets, wardrobes, and built-ins, aided by moisture-resistant cores and fire-retardant overlays that satisfy apartment fire codes. Asian exporters capture additional upside from global e-commerce furniture sales, which prefer flat-packed plywood components for lighter shipping weight.

Adoption of Modular/Off-Site Building Methods

Factory-built classrooms, hospitals, and multi-family units increasingly deploy standardized plywood for sheathing and sub-assemblies. In the EU, wood-framed construction has grown to 11% of building activity, while the UK records more than 50% wood usage in new homes. Dimensional stability, predictable strength, and ease of machining make plywood well suited to precision off-site fabrication. Automated CNC routing lines further elevate material yield and cut installation time on site.

Shift From One-Way Plastics to Plywood in Industrial Packaging

Circular-economy directives in Europe reward reusable transit packaging. Durable plywood crates now replace disposable plastics for heavy machinery exports, offering multiple trip cycles and reduced landfill fees. Logistics firms also remarket empty crates as raw material, boosting residual value and lowering total cost of ownership compared with one-and-done corrugated or polymer solutions within the plywood industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental compliance and deforestation curbs | -0.8% | EU and North America first, global later | Short term (≤ 2 years) |

| OSB and alternative panels gaining share | -0.6% | North America initially, spreading worldwide | Medium term (2-4 years) |

| Carbon-border tariffs raising export costs | -0.4% | China-EU; Asia-US trade lanes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Environmental Compliance & Deforestation Curbs

The EU Deforestation Regulation, entering force 30 December 2025, obliges plywood importers to furnish GPS-level provenance and legality proofs, exposing non-compliant shipments to substantial fines and border rejection [1]European Commission, “Regulation (EU) 2023/1115 on Deforestation-Free Supply Chains,” ec.europa.eu. Mills face additional audit costs, while smallholders lacking certification risk losing access to premium markets. Global brands often extend the strictest rule set across their full supply chains, effectively globalizing EU-style due diligence and compressing margins for unverified suppliers in the plywood industry.

OSB & Alternative Panels Gaining Share

Capacity additions and broader code acceptance accelerate substitution. Fibre cement and magnesi um oxide boards, registering 18–20% annual growth in India, further encroach on traditional plywood domains, especially where termite resistance is pivotal.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Wood Type: Softwood Plywood Extends Structural Lead

Softwood grades captured a 51.12% plywood industry share in 2024 and are forecast to post a 6.12% CAGR to 2030, supported by mass-timber buildings and standardized framing needs. The plywood market size for softwood reached USD 28.9 billion in 2025, mirroring surging demand for sheathing, roofing, and wall bracing panels in North America and Europe. Dimensional stability, lighter weight, and cost competitiveness underpin the appeal for modular factories that value quick machining and consistent nail-holding power. Hardwood variants dominate aesthetic furniture, cabinetry, and specialty vehicle interiors where grain, color, and surface smoothness justify premiums. Still, softwood boards gain share in mid-range furniture as digital printing and overlay films can replicate hardwood visuals on pine or spruce cores.

Second-generation fire-retardant binders allow softwood to enter Class A wall assemblies. D-Blaze-treated pine studs and panels now meet stringent US model code criteria, opening doors to 6- to 12-story mixed-use projects previously restricted to steel joists. Mills leverage AI scanners to grade veneer defects faster, trimming reject rates and improving recovery. Over the outlook period, certified plantation spruce and pine widen the softwood edge in countries enforcing deforestation curbs.

By Grade Type: Fire-Resistant Innovation Leads Growth

MR grade sustained the largest share at 33.35% in 2024 due to its broad application window in furniture carcasses, partitions, and cabinetry. Yet the fire-resistant category commands the highest 6.32% CAGR as regulators raise safety bars for high-occupancy structures. The plywood market size for fire-resistant panels is projected to reach USD 12.6 billion by 2030, up from USD 8.6 billion in 2025, indicating strong pull from commercial real estate. Chemical suppliers refine intumescent coatings that char at lower temperatures, cutting smoke density and allowing extra evacuation time. Class A-rated panels are increasingly specified for hotel corridors, school auditoria, and transport hubs that require stringent flame-spread thresholds.

BWR and BWP boards cater to semi-exposed and fully wet spaces such as balconies and kitchen counters, respectively. Structural grade plywood competes head-to-head with OSB in load-bearing floors; however, higher screw-holding capacity and moisture cycling resilience afford plywood a niche where builders demand premium performance. Continuous hot-press lines with vacuum-assisted resin penetration raise bond quality and enable thinner plies without sacrificing strength.

By Application: Paneling & Cladding Accelerate

Construction remained the single-largest demand center, though paneling and cladding registered the fastest 5.66% CAGR through 2030. Architects cite biophilic design goals and carbon reduction targets as key motivators for choosing wood façades over steel or PVC. The plywood industry size for façade systems is forecast to double across office retrofits and education facilities adopting exposed wood themes. Furniture applications, while mature, continue to account for 37.72% of 2024 volumes as modular storage and flat-pack wardrobes dominate urban apartments.

Packagers increasingly switch to plywood crates for heavy machinery, leveraging 10-plus reuse cycles and strong resistance to puncture compared with corrugated solutions. Automotive manufacturers adopt thin-veneer sandwich panels for delivery van flooring, lowering kerb weight and thereby improving fuel economy. Machine-learning models, such as the Random Forest veneer predictor with 76% accuracy, optimize feedstock usage and support expanding plywood penetration across diverse applications.

By End-User Industry: Industrial Gains Momentum

Residential building still represented 47.13% of 2024 plywood orders, mainly subflooring, kitchens, and wardrobes. Nonetheless, industrial consumers show the fastest 5.78% CAGR as companies retreat from single-use plastics and metals. Reusable plywood boxes now carry electronics, auto components, and pharmaceuticals across long supply chains. Film-faced concrete formwork rated for 10 pours wins share on high-rise job sites, reducing waste and labour. Commercial fit-out demand remains healthy for offices, retail, and hospitality, where plywood’s acoustic and tactile properties add user appeal. The plywood industry continues to diversify as specialty grades serve cold storage insulation backing, rail interiors, and marine decking.

Geography Analysis

Asia–Pacific dominated with 57.12% of 2024 demand as China, India, and Southeast Asia sustained high construction activity and robust furniture manufacturing. Vietnam’s first-half 2025 wood export value of USD 8.21 billion, a 8.9% year-on-year rise, shows resilience despite a 46% US duty, producers quickly redirected shipments to South Korea, Japan, and the EU . India’s organised panel players benefit from urban housing and a government-backed 100-smart-cities mission; many are adding calibrating sanders and hot presses to supply premium calibrated plywood.

The Middle East & Africa segment exhibits the fastest projected 5.62% CAGR through 2030. Saudi Arabia alone controls 39% of MENA construction value, with more than USD 1.5 trillion of unawarded projects mid-pipeline [2]Source: Saudi Ministry of Finance, “Budget Statement 2025,” mof.gov.sa. NEOM, Red Sea Global, and countless hospitality ventures demand vast volumes of formwork and interior panel products. Local governments encourage mill investments to reduce import dependence, while new logistics corridors—such as the UAE-India food corridor—enhance plywood distribution speed across Gulf Cooperation Council states, boosting growth in the plywood industry.

North America retains a sizeable albeit mature market where OSB dominates new single-family housing starts. Yet certified plywood wins in multifamily, remodel, and premium cabinetry. Mills in the US Pacific Northwest and Canada deploy waste-wood biomass boilers and AI edge defect scanners to boost energy efficiency and margin. In Europe, wood-based construction’s 11% share of total building starts is double the global average, driven by subsidies for low-carbon materials and public procurement guidelines favouring FSC-certified panels. Builders value chain-of-custody documentation to comply with the EU Deforestation Regulation, cementing a market for verified plywood.

Competitive Landscape

The plywood industry remains fragmented globally, though regional consolidation accelerates as capital costs and environmental compliance burdens rise. In Asia–Pacific, thousands of family-owned mills feed domestic builders and modest export contracts, keeping price competition intense. Contrast that with North America, where a handful of integrated forest products groups, led by Weyerhaeuser and Georgia-Pacific, control major veneer resources and automated board lines. European suppliers such as UPM and Metsä Wood focus on certified spruce plywood for structural and decorative use, differentiating on sustainability labels and engineered surface finishes.

Technology adoption is a key battleground. Weyerhaeuser’s AI-enabled optimisation at oriented strand facilities cuts raw-material waste by 5% and lifts press throughput. Finnish mills trial machine-vision veneer sorters paired with predictive maintenance analytics that reduce unexpected downtime. Chinese producers invest in continuous hot-press lines capable of curating thinner plies at higher speeds, supporting mid-market furniture exporters seeking calibrated thickness tolerance.

Strategic investments in the plywood industry also target sustainability. Companies commit to science-based emission targets and procure renewable electricity, positioning themselves favourably once carbon-border taxes bite. Bio-based adhesive innovators collaborate with panel makers to scale soy-ligin or lignin-phenol hybrid resins that lower formaldehyde emissions. Meanwhile, several ASEAN mills pursue listings or joint ventures to fund re-plantation programmes and secure long-term fibre. M&A activity picked up in late 2024 when two Indian mid-tier firms merged to pool distribution networks and meet inventory credit guidelines imposed by new goods-and-services tax rules.

Plywood Industry Leaders

Weyerhaeuser Company

Georgia-Pacific

West Fraser Timber Co.

UPM

SVEZA Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Weyerhaeuser committed USD 500 million to construct a new TimberStrand facility in Arkansas, doubling engineered-wood capacity to 10 million cubic feet annually.

- May 2024: Century Plyboards launched “Century Cubicles,” a modular restroom and locker system built around moisture-resistant plywood panels.

Global Plywood Market Report Scope

| Softwood Plywood |

| Hardwood Plywood |

| Tropical Plywood |

| Aircraft Plywood |

| Decorative Plywood |

| Flexible Plywood |

| Other Types |

| Furniture |

| Construction |

| Flooring |

| Paneling and Cladding |

| Transport (Automotive, Marine, etc.) |

| Packaging |

| Other Applications |

| Residential |

| Commercial |

| Industrial |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Softwood Plywood | |

| Hardwood Plywood | ||

| Tropical Plywood | ||

| Aircraft Plywood | ||

| Decorative Plywood | ||

| Flexible Plywood | ||

| Other Types | ||

| By Application | Furniture | |

| Construction | ||

| Flooring | ||

| Paneling and Cladding | ||

| Transport (Automotive, Marine, etc.) | ||

| Packaging | ||

| Other Applications | ||

| By End-user Industry | Residential | |

| Commercial | ||

| Industrial | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current plywood market size and growth rate?

The plywood market size stood at USD 56.63 billion in 2025 and is projected to expand at a 4.88% CAGR to USD 71.86 billion by 2030.

Which region dominates plywood consumption?

Asia–Pacific led with a 57.12% share in 2024, propelled by large-scale construction and furniture exports.

Why is fire-resistant plywood growing so fast?

Stricter building codes for high-rise safety and advances in intumescent technology drive a 6.32% CAGR for fire-resistant grades.

How are environmental rules affecting plywood trade?

The EU Deforestation Regulation and upcoming carbon-border taxes raise compliance costs, pressuring high-emission suppliers to modernise or re-route exports.

Page last updated on: