Recycled Construction Aggregates Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

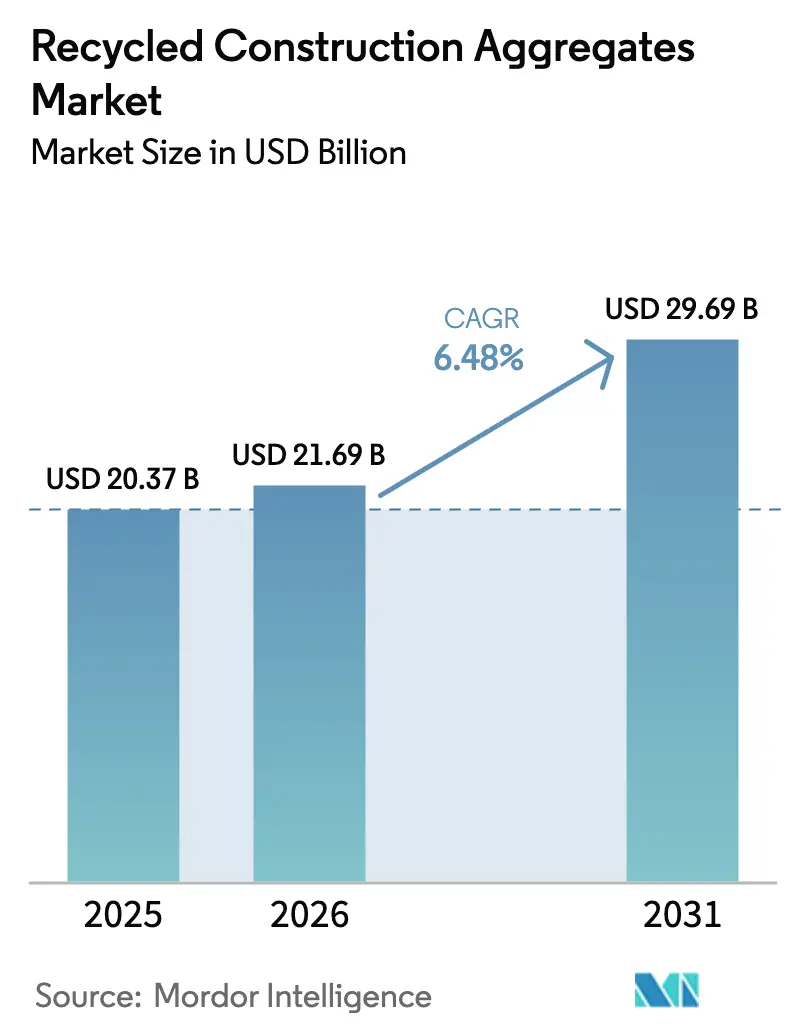

| Market Size (2026) | USD 21.69 Billion |

| Market Size (2031) | USD 29.69 Billion |

| Growth Rate (2026 - 2031) | 6.48% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recycled Construction Aggregates Market Analysis by Mordor Intelligence

The Recycled Construction Aggregates Market size was valued at USD 20.37 billion in 2025 and is estimated to grow from USD 21.69 billion in 2026 to reach USD 29.69 billion by 2031, at a CAGR of 6.48% during the forecast period (2026-2031). Regulatory mandates are digitizing waste tracking, imposing aggregate levies, and tightening circular-economy targets. These actions are shortening payback periods for mobile crushing fleets and carbon-mineralization lines. The widening cost gap between virgin stone and recycled material, amplified by rising diesel and carbon taxes, is positioning the recycled construction aggregates market as a mainstream procurement choice for infrastructure and residential projects. Carbon-negative aggregates, which generate emissions credits, are creating dual revenue streams. Additionally, AI-enabled crushers are consistently delivering gradations at a lower cost, addressing historical quality gaps. These converging forces are attracting strategic investments from global cement majors and private equity, leading to accelerated capacity additions in Europe, Asia-Pacific, and North America.

Key Report Takeaways

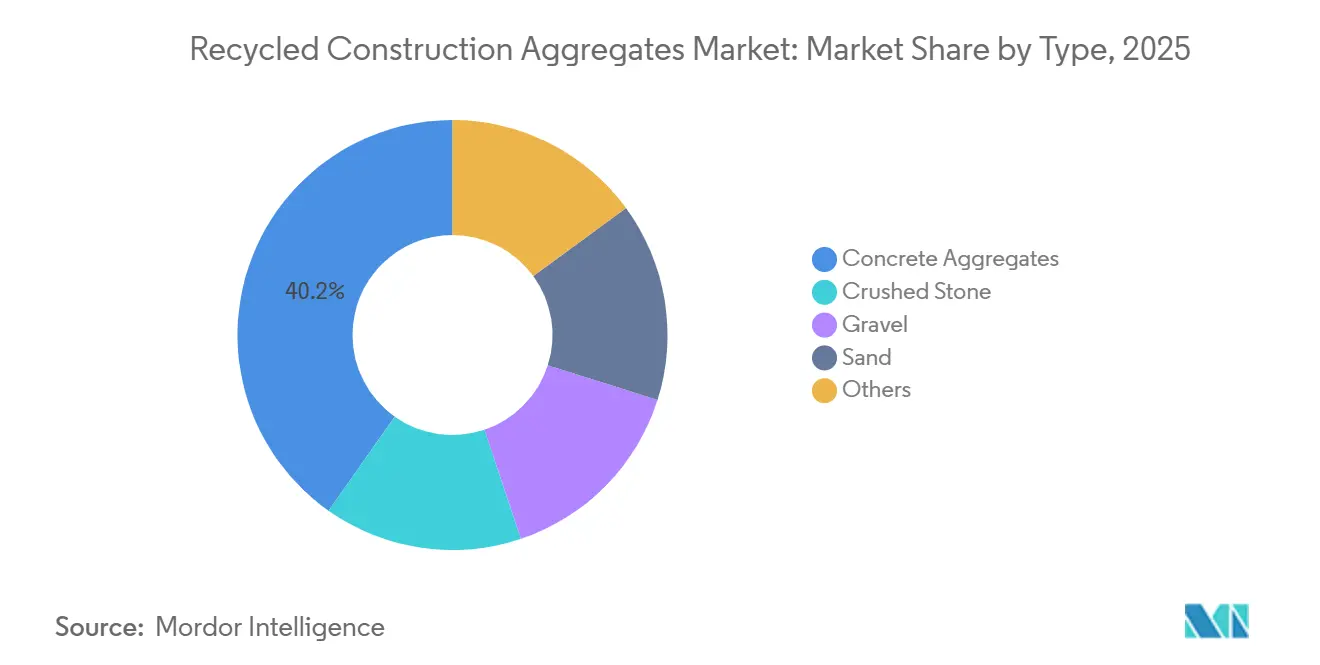

- By type, concrete aggregates led with 40.22% of the recycled construction aggregates market share in 2025 and will increase at a 6.67% CAGR from 2026 to 2031.

- By application, infrastructure commanded a 47.77% share of the recycled construction aggregates market size in 2025, while residential construction is projected to expand at a 7.11% CAGR from 2026 to 2031.

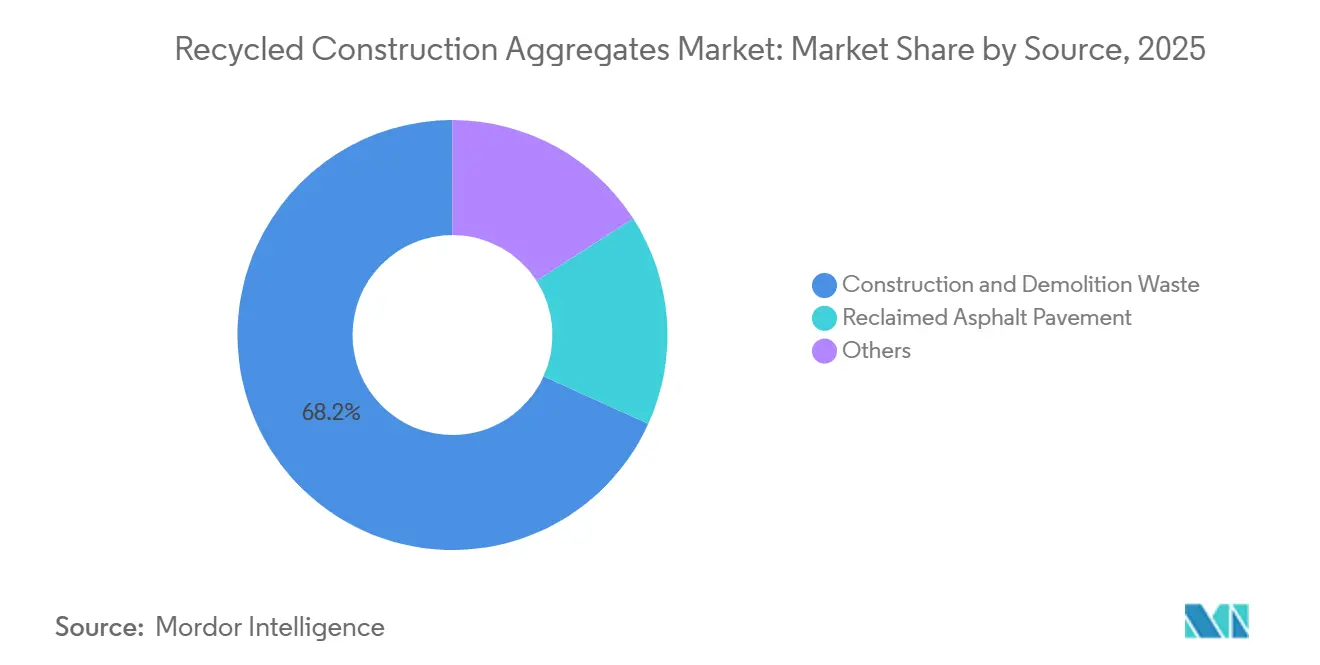

- By source, construction and demolition waste supplied 68.22% of the recycled construction aggregates market size in 2025; reclaimed asphalt pavement is advancing at a 6.89% CAGR from 2026 to 2031.

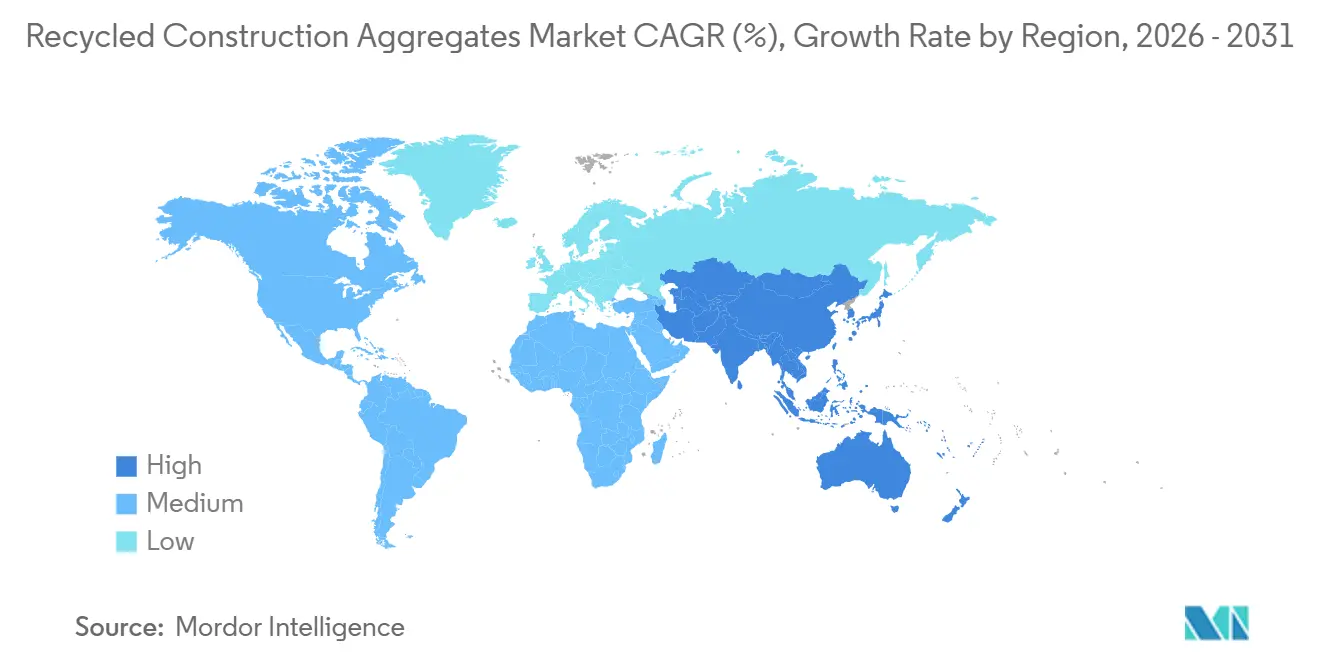

- By geography, Europe held a 36.69% share of the recycled construction aggregates market in 2025, whereas the Asia-Pacific is anticipated to record a 7.12% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Recycled Construction Aggregates Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital construction and demolition-waste tracking mandates | +1.2% | Europe, China, India | Short term (≤ 2 years) |

| Government circular-economy targets tighten | +1.5% | Global, with early gains in EU, China, ASEAN | Medium term (2-4 years) |

| Cost gap narrows vs. virgin aggregates as quarry diesel levies rise | +1.3% | Europe, UK, Canada | Medium term (2-4 years) |

| Carbon-mineralised aggregates earn negative-emission credits | +0.9% | North America, Europe, Australia | Long term (≥ 4 years) |

| AI-optimised mobile crushers cut processing cost/ton ≥18% | +1.1% | Global, spill-over to MEA and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital Construction and Demolition-Waste Tracking Mandates

Satellite tracking and electronic manifests are effectively curbing informal dumping, steering debris towards licensed recyclers. The European Union's Digital Waste Shipment System, operational since May 2026, empowers customs officers to intercept non-compliant cross-border shipments, levying fines for each infraction[1]European Commission, “Digital Waste Shipment System,” europa.eu. China's Solid Waste Action Plan, initiated in January 2026, mandates Beidou tracking for trucks hauling over 5 tonnes of construction debris. Simultaneously, India's Construction and Demolition Waste Management Rules, unveiled in April 2026, elevate extended-producer-responsibility targets, pushing for full compliance by 2029. These regulations bolster feedstock transparency, reduce financing risks for new plants, and accelerate the market's adoption of recycled construction aggregates, especially in regions previously reliant on informal supply chains.

Government Circular-Economy Targets Tighten

Starting in 2027, Saudi Arabia will require public projects to source a portion of their aggregates from recycled materials. In Mexico, the Circular Economy Law, effective in 2026, links producer responsibilities to deposit-return schemes for construction materials. Scotland has implemented a rule stating that if recycled materials are available within a 50-kilometer radius, the use of virgin stone for road repairs is prohibited. This regulation has led to a significant reservation of municipal asphalt demand. These mandates not only broaden the market for recycled construction aggregates but also encourage investments in capacity, particularly in previously overlooked regions.

Cost Gap Narrows vs. Virgin Aggregates as Diesel Levies Rise

Quarry operating costs are increasing due to aggregate taxes and carbon pricing. In Scotland, the levy has made recycled materials cheaper per tonne compared to virgin stone. In Canada, the rising carbon tax is driving up diesel costs for quarrying operations. In United States metropolitan areas, as quarry depletion leads to longer haul distances, recycled concrete aggregates are being sold at lower prices. This pricing undercuts virgin stone and strengthens the market for recycled construction aggregates, particularly in public works contracts.

Carbon-Mineralised Aggregates Earn Negative-Emission Credits

Technologies that embed captured CO₂ into crushed concrete are turning waste into a valuable asset for climate mitigation. Mobile units sequester CO₂ by the tonne while simultaneously enhancing compressive strength. Plants in Switzerland, along with a pilot in Finland, earn carbon credits for every tonne of CO₂ they remove. This premium pricing aids in offsetting their higher capital expenditures. These dual revenue streams not only strengthen project economics but also encourage broader acceptance in the market for recycled construction aggregates.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Perceived structural-grade performance gap vs. natural stone | -0.8% | India, South Korea, Southeast Asia | Medium term (2-4 years) |

| Sparse recycling infrastructure outside Tier-1 Asia-Pacific metros | -0.6% | ASEAN, India Tier-2/3 cities | Short term (≤ 2 years) |

| Trace-metal contamination spikes disposal cost for RAP blends | -0.4% | North America, Australia, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Perceived Structural-Grade Performance Gap vs. Natural Stone

Design codes often restrict the use of recycled aggregates in load-bearing mixes. In India, the use of recycled coarse aggregates is limited to the M25 concrete. South Korea, on the other hand, imposes a design strength limit when the coarse recycled aggregate surpasses a specific threshold[2]Bureau of Indian Standards, “IS 383 Aggregates Specification,” bis.gov.in. Due to a lack of long-term performance data, structural engineers remain skeptical about the quality of these aggregates. This skepticism has hindered the widespread adoption of recycled construction aggregates, especially in high-rise buildings and bridge projects.

Sparse Recycling Infrastructure Outside Tier-1 Asia-Pacific Metros

Coastal megacities are home to the majority of crushing plants. In Medan, Indonesia, and provincial cities across Thailand, contractors face a challenge: trucking materials over distances exceeding 200 km. This logistical hurdle reduces the cost advantages of recycling. By 2030, ASEAN nations may need to invest significantly in new facilities to meet diversion targets. Without such investments, the market for recycled construction aggregates could remain under-penetrated in key residential areas across the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Concrete Aggregates Anchor Structural Demand

In 2025, concrete aggregates held a dominant 40.22% share of the recycled construction aggregates market, with projections indicating a robust 6.67% CAGR through the forecast period of 2026–2031. Carbonation-curing lines enhance the 28-day compressive strength, enabling recycled materials to effectively replace virgin basalt in EN 206-certified structural mixes. While crushed stone finds its application in road bases with lenient tolerances, recycled gravel is the preferred choice for permeable pavements, ensuring compliance with Europe’s stormwater regulations. High-fines sand encounters supply challenges due to air-classification upgrades, which not only inflate processing costs but also hinder its market penetration.

Selective demolition, impact crushers, and air separators have become focal points for investments. These enhancements guarantee adherence to UNI 11531-1:2024 standards, particularly for flakiness and Los-Angeles abrasion thresholds, rendering them suitable for structural-grade concrete. Heidelberg Materials has integrated carbonation into its production line at a Polish facility. On the other hand, Holcim’s strategic acquisitions in 2024 have amplified its capacity, with a clear focus on concrete aggregates designed for low-carbon binders. Such advancements in equipment are set to bolster the recycled construction aggregates market, especially within the precast and ready-mix domains, over the forecast period of 2026–2031.

By Application: Infrastructure Leads, Residential Accelerates

In 2025, public works mandates in France, South Korea, and Saudi Arabia, which emphasized sourcing recycled materials within a 50 km radius of the site, increased the infrastructure's share to 47.77% of the recycled construction aggregates market. In the United Kingdom, a trial on the A47 highway validated the use of high levels of recycled asphalt for wearing courses. This success prompted a shift in specifications, advocating for High-RAP (Reclaimed Asphalt Pavement) blends across the nation's highways.

Looking ahead, residential demand is projected to grow at a compound annual growth rate (CAGR) of 7.11% during the forecast period of 2026–2031. This growth is largely attributed to Germany mandating recycled content in non-load-bearing walls and screeds. South Korean municipal codes have also expanded diversion quotas to include apartment blocks. While commercial and industrial projects are increasingly adopting recycled aggregates for parking decks and landscaping, developers of Class-A offices remain cautious. Their preference for virgin stone, influenced by image considerations, slightly limits the market's adoption of recycled aggregates in premium urban towers.

By Source: C&D Waste Dominates, RAP Gains Momentum

In 2025, global feedstock saw a significant contribution of 68.22% from construction and demolition debris, driven largely by rapid urban redevelopment efforts in China and India. In a bid to boost the recycled construction aggregates market, prefecture-level cities in China mandated digitized manifests and satellite tracking, aiming for a 50% utilization rate by 2027.

Reclaimed asphalt pavement, bolstered by advancements in warm-mix technology, is poised to grow at a rate of 6.89% CAGR (2026-2031). While a substantial amount was utilized, stockpiles still retained significant latent capacity. Over the next five years, innovations in leachate management and the adoption of low-temperature mixing techniques are expected to play a crucial role in tapping into this stock, thereby amplifying RAP's contribution to the recycled construction aggregates market supply.

Geography Analysis

In 2025, Europe accounted for 36.69% of global revenue. In Scotland, a levy on aggregates has widened the recycled discount compared to virgin stone. The European Union's Digital Waste Shipment System mandates the real-time reporting of cross-border waste, effectively closing loopholes that have historically disadvantaged local recyclers. Germany mandates the use of recycled content in the non-structural elements of its building code. France prioritizes recycled materials for municipal road orders when they are locally available. The United Kingdom now allows a significant percentage of Reclaimed Asphalt Pavement (RAP) in surface layers. These measures collectively strengthen the market for recycled construction aggregates in high-value civil works.

The Asia-Pacific region is set to achieve a 7.12% compound annual growth rate (CAGR) during the forecast period of 2026–2031. India's extended producer responsibility targets are expected to increase significantly between 2026 and 2029. In China, prefectures are mandated to achieve resource utilization goals by 2027, a directive supported by Beidou monitoring. Indonesia, Vietnam, and Malaysia have integrated diversion clauses into their annual infrastructure spending. However, inland markets still lack sufficient crushing capacity, presenting greenfield opportunities for investors aiming to expand the footprint of the recycled construction aggregates market beyond tier-1 hubs.

North America is benefiting from the Infrastructure Investment and Jobs Act, along with carbon pricing that enhances the competitiveness of recycled materials. Canada's rising carbon tax is projected to increase quarry diesel prices. In 2023, the United States achieved significant savings by utilizing Reclaimed Asphalt Pavement (RAP) instead of virgin materials. Mexico's 2026 Circular Economy Law, which combines deposit-return schemes with a waste-valorization park in Tula, positions the nation as a burgeoning hub for the recycled construction aggregates market. While South America, the Middle-East, and Africa are still in their infancy, Brazil and Saudi Arabia showcase robust policy momentum. This indicates potential growth in the medium term, provided they overcome financing challenges and address the low prices of virgin stone.

Competitive Landscape

The recycled construction aggregates market remains moderately consolidated. Mid-tier players in the North American market are witnessing higher average selling prices. This surge is largely attributed to infrastructure investments straining local supplies, prompting these players to invest in on-site crushing to bolster their reserves. There are untapped opportunities in Tier-2 cities across the Asia-Pacific region, which currently lack fixed recycling plants, and in carbon-negative precast elements. As standards tighten globally - with India enforcing IS 383, Italy introducing UNI 11531-1:2024, and Singapore setting a 1 percent contamination limit - capital is increasingly being directed towards selective demolition, air classification, and carbonation curing. This shift underscores the evolving perception of recycled aggregates, transitioning from mere landfill diversions to becoming mainstream inputs in structural applications.

Recycled Construction Aggregates Industry Leaders

HOLCIM

Heidelberg Materials

CEMEX S.A.B. de C.V.

CRH

Vulcan Materials Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Breedon Group opened waste-recovery sites at Ashbury and Costessey, each processing construction and demolition waste debris into road-base and concrete aggregates, expanding circular-materials coverage across East Anglia and the Midlands.

- July 2025: Cemex has delivered nearly 35,000 m³ of Vertua concrete, made from recycled aggregates, for the new Caen University Hospital. This sustainable project, focused on reducing environmental impact, utilized concrete delivered from Cemex's Caen Blainville production facility.

Global Recycled Construction Aggregates Market Report Scope

Recycled Construction Aggregates (RCAs) are processed, inorganic, and mineral materials obtained from previously used construction projects, industrial byproducts, or demolition waste. These materials are crushed, screened, and cleaned to serve as sustainable alternatives to natural aggregates, reducing the reliance on newly extracted sand, gravel, and stone.

The construction aggregates market is segmented by type, application, source, and geography. By type, the market is segmented into crushed stone, gravel, sand, concrete aggregates, and others. By application, the market is segmented into residential, commercial, infrastructure (roads, bridges, rail), and industrial. By source, the market is segmented into construction and demolition waste, reclaimed asphalt pavement, and others (slag, foundry sand, etc.). The report also covers the market size and forecasts for the market in 17 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| Crushed Stone |

| Gravel |

| Sand |

| Concrete Aggregates |

| Others |

| Residential |

| Commercial |

| Infrastructure (roads, bridges, rail) |

| Industrial |

| Construction and Demolition Waste |

| Reclaimed Asphalt Pavement |

| Others (slag, foundry sand, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Crushed Stone | |

| Gravel | ||

| Sand | ||

| Concrete Aggregates | ||

| Others | ||

| By Application | Residential | |

| Commercial | ||

| Infrastructure (roads, bridges, rail) | ||

| Industrial | ||

| By Source | Construction and Demolition Waste | |

| Reclaimed Asphalt Pavement | ||

| Others (slag, foundry sand, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global demand for recycled construction aggregates become by 2031?

The recycled construction aggregates market size is projected to reach USD 29.69 billion by 2031 from USD 21.69 billion in 2026, reflecting a 6.48% CAGR (2026-2031).

Which product type dominates sales today?

Concrete aggregates held 40.22% of 2025 revenue, benefiting from carbonation-curing protocols that lift compressive strength for structural concrete.

Where is the fastest geographic growth expected?

Asia-Pacific is forecast to post the quickest 7.12% CAGR (2026-2031) as India, China, and ASEAN nations enforce aggressive diversion mandates.

What policy tools most influence adoption?

Aggregates levies, carbon taxes on quarry diesel, and digital waste-tracking systems collectively shorten payback periods for recycling infrastructure.

How are negative-emission credits changing project economics?

Carbon-mineralized aggregates that lock away CO₂ can earn USD 80–130 per tonne of verified removal, creating a second revenue stream that funds advanced processing lines.

Which companies are leading consolidation?

HOLCIM, Heidelberg Materials, CEMEX S.A.B. de C.V., CRH, and Vulcan Materials Company are the leading players.

Page last updated on: