Wood Preservatives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.17 Billion |

| Market Size (2031) | USD 3.94 Billion |

| Growth Rate (2026 - 2031) | 4.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

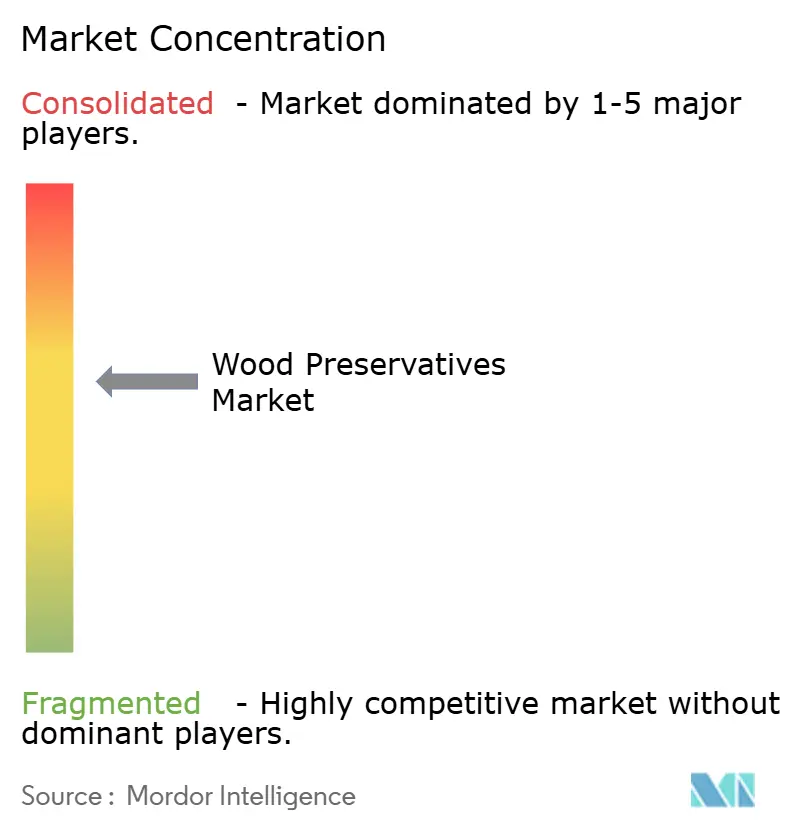

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wood Preservatives Market Analysis by Mordor Intelligence

The Wood Preservatives Market size is expected to grow from USD 3.03 billion in 2025 to USD 3.17 billion in 2026 and is forecast to reach USD 3.94 billion by 2031 at a 4.46% CAGR over 2026-2031. This moderate expansion is anchored by robust residential construction, active infrastructure renewal, and a steady pivot from oil-borne chemistries toward water-based copper systems. Regulatory agencies in North America and Europe have accelerated the retirement of chromated copper arsenate, pentachlorophenol, and creosote, which redirects demand to copper-azole, micronized-copper, and emerging bio-derived alternatives. Builders now favor preservatives that pair diminished aquatic toxicity with recycled-copper content, while utilities and rail operators complete multi-year testing programs to ensure field performance. Commodity copper pricing volatility continues to pressure margins, yet formulators offset the impact with recycled feedstocks, hedging strategies, and differentiated additive packages that limit leaching. The aggregate picture is a wood preservatives market navigating cost headwinds and compliance complexity without losing sight of the underlying demand for treated lumber in decking, fencing, utility poles, rail sleepers, and marine piles.

Key Report Takeaways

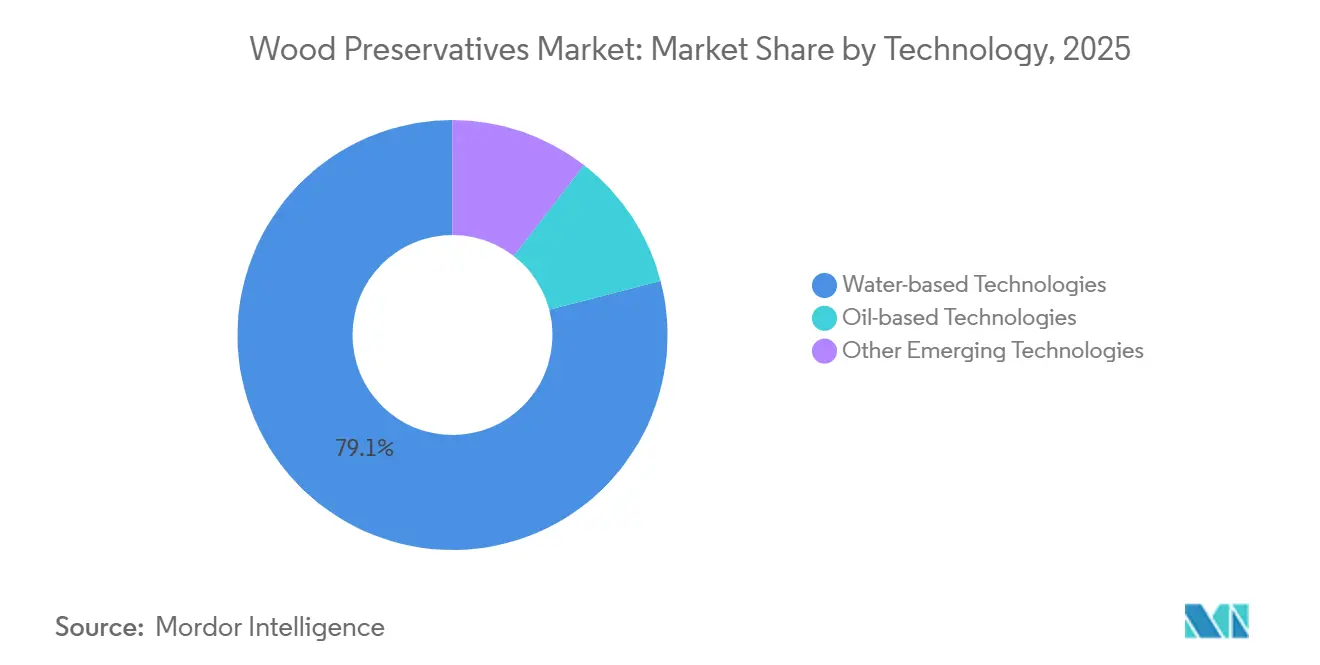

- By technology, water-based formulations captured 79.05% revenue in 2025, and the segment is set to grow at a 4.31% CAGR through 2031.

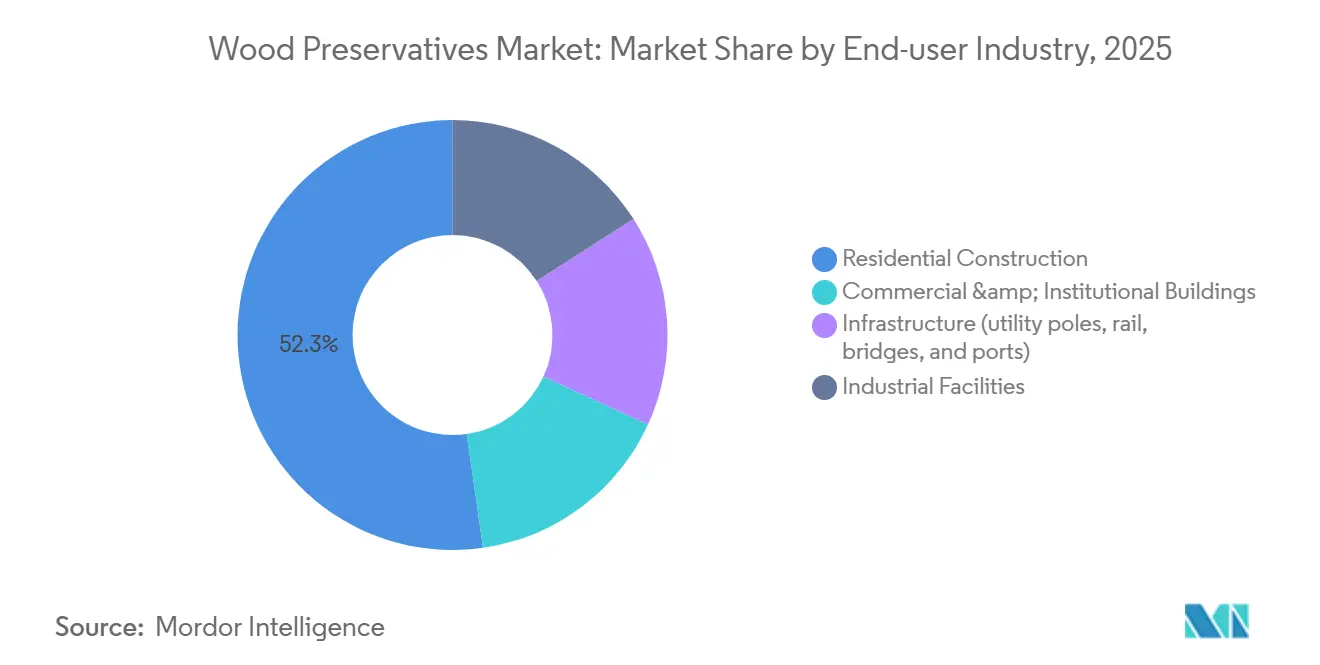

- By end-user industry, residential construction led with 52.26% of demand in 2025, while it also records the fastest trajectory at a 4.56% CAGR to 2031.

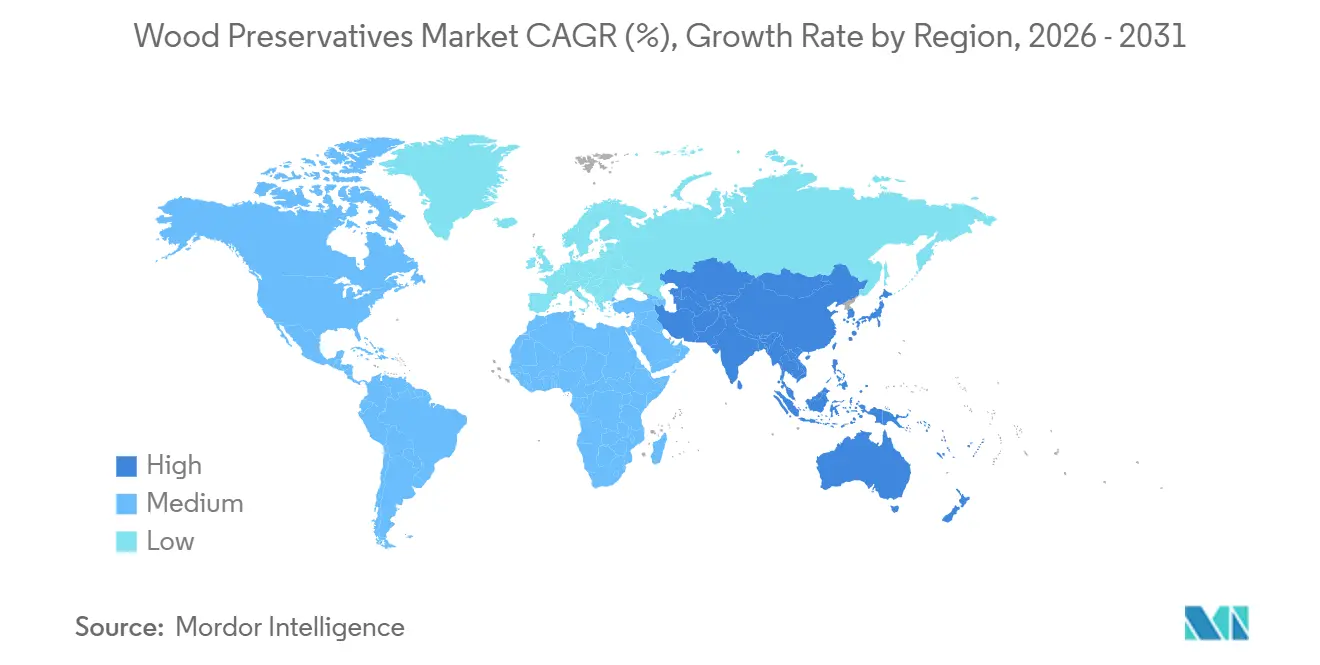

- By geography, North America held 36.14% of global revenue in 2025, whereas Asia-Pacific is forecast to advance at a 5.72% CAGR and outpace every other region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wood Preservatives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction boom in residential and infrastructure projects | +1.8% | Global, concentrated in Asia-Pacific and North America | Medium term (2–4 years) |

| Shift toward eco-friendly water-based and copper-based systems | +1.2% | North America and Europe, spillover to ASEAN and Latin America | Long term (≥ 4 years) |

| Growth in outdoor living (decking, fencing, landscaping) | +0.9% | North America, Europe, Australia | Short term (≤ 2 years) |

| Durability needs for utility poles, rail sleepers, marine piles | +0.7% | Global, emphasis on North America utilities and Asia-Pacific rail | Long term (≥ 4 years) |

| Emergence of carbon-negative mass-timber buildings | +0.5% | North America and Europe, pilot projects in Japan and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction Boom in Residential and Infrastructure Projects

Governments continue to channel sizable budgets into road, rail, and public works pipelines, and that spending dovetails with a rebound in single-family housing starts to lift preservative consumption across framing lumber, decking, and heavy timbers. India’s National Infrastructure Pipeline has earmarked USD 1.4 trillion through 2025, much of which specifies treated sleepers and bridge components[1]Government of India, “National Infrastructure Pipeline,” india.gov.in. China sustains legacy railway upgrades that draw on creosote and copper-chrome formulations even as property-sector headwinds persist. In the United States, completions for detached housing improved in 2025, while renovation spending on patios, pergolas, and privacy fences pushed demand for copper-azole and micronized-copper lumber. The driver adds 1.8 percentage points to the overall CAGR, with influence peaking in the medium term as infrastructure projects move from planning to execution.

Shift Toward Eco-Friendly Water-Based and Copper-Based Systems

Regulatory bans on pentachlorophenol and usage caps on chromated copper arsenate have accelerated the transition toward water-dispersible copper compounds. The US Environmental Protection Agency’s 2022 order ends pentachlorophenol by February 2027, forcing utility companies to certify copper naphthenate and micronized-copper poles. Micronized particles below 1 micron exhibit measurably lower leaching than dissolved copper salts, reducing aquatic toxicity without sacrificing fungicidal power. Arxada’s Preserve range achieves 96.1% recycled-copper content in CA-C and CA-B products, aligning preservative selection with circular-economy credits in green-building programs[2]Arxada, “Preserve CA-C Technical Data Sheet,” arxada.com. As European regulators classify copper with an aquatic M-factor of 10, innovators respond with encapsulated-release platforms that trim effective loading rates. The driver supplies a 1.2 percentage-point uplift to growth over the long run as standards in Asia-Pacific and Latin America converge on EU and U.S. norms.

Growth in Outdoor Living (Decking, Fencing, and Landscaping)

Household priorities shifted during the pandemic, and discretionary spending on outdoor amenities remains structurally higher than pre-2020. Pressure-treated southern yellow pine and Douglas fir still anchor most decks, with copper-azole delivering a 40-year service life that appeals to contractors. Fencing projects and garden borders specify lighter retention, yet they represent consistent volume in humid regions. Landscaping timbers for raised beds, retaining walls, and playgrounds add niche demand. This driver supplies a 0.9 percentage-point boost but is front-loaded, tapering as homeowners reach a new equilibrium in remodeling budgets.

Durability Needs for Utility Poles, Rail Sleepers, and Marine Piles

The United States maintains more than 130 million wood utility poles, and annual replacement cycles of 3% to 4% ensure a recurring market for preservatives. Rail corridors across India, China, and Southeast Asia continue to deploy creosote or copper-chrome sleepers, balancing cost against 25-year service lives. Marine piles in ports contend with saltwater immersion, marine borers, and ultraviolet degradation, which requires heavy copper loadings and co-biocides. Field validation extends adoption timelines but ultimately expands the accessible base for water-borne chemistries. The driver contributes 0.7 percentage points to the CAGR and operates across a long-term horizon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent bans or restrictions on CCA, PCP, creosote, and VOC limits | −1.1% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Volatility in copper and biocide feedstock prices | −0.6% | Global, pronounced in Asia-Pacific and Latin America | Medium term (2–4 years) |

| Fire-retardant CLT coatings reducing deep-soak demand | −0.4% | North America and Europe, emerging in Japan and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Bans or Restrictions on CCA, PCP, Creosote, and VOC Limits

The U.S. Environmental Protection Agency finalized pentachlorophenol’s cancellation in 2022, eliminating inventory by February 2027 and ending a seven-decade utility-pole standard. Chromated copper arsenate remains confined to restricted industrial uses under exacting disposal rules, while creosote faces parallel limits in the European Union’s Persistent Organic Pollutants Regulation. VOC caps in coatings push formulators toward water carriers that demand fresh R&D outlays. The EU Biocidal Products Regulation now screens out carcinogens, mutagens, endocrine disruptors, and very persistent, very mobile substances, extending timeframes and raising costs for every new active. Collectively, these actions shave 1.1 percentage points off the CAGR in the near term as phase-out dates collide with field-trial bottlenecks.

Volatility in Copper and Commodity Biocide Feedstock Prices

Copper traded between USD 8,500 and USD 10,000 per metric ton from 2024 to 2025, a range wide enough to buffet profit margins for micronized-copper and copper-azole producers. Treaters with fixed-price contracts are exposed to sudden price spikes, and while utilities accept some pass-through costs, builders and consumers resist increases, eroding volumes. Supplemental actives such as quaternary ammonium compounds and triazoles track petrochemical volatility, disadvantaging small formulators without hedging scale. The restraint removes 0.6 percentage points from CAGR, most evident in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Based Dominance Anchored by Copper Innovation

Water-based systems accounted for a commanding 79.05% share of the wood preservatives market in 2025 and are forecast to rise at a 4.31% CAGR through 2031. This leadership springs from micronized-copper particles that leach 30% to 50% less active ingredient than dissolved salts, thereby meeting tougher aquatic-toxicity thresholds. In 2025, the water-based portion represented the largest single component of the wood preservatives market size at USD 2.5 billion, and ongoing substitution away from oil-borne actives cements its trajectory. The residual share belongs to oil-borne chemistries, chiefly creosote and vegetable-oil blends, which face volume pressure as phase-out deadlines arrive in North America and the European Union. Yet creosote still claims relevance for rail sleepers and marine structures where high-retention, heavy-duty protection justifies elevated toxicity management.

Second-generation water-based offerings now integrate recycled-copper feedstocks that hedge price swings and burnish green-building credentials. Arxada’s Wolman E line leverages BARamine technology to stabilize copper azole and slow volatilization. Borate diffusions flourish in interior framing where low mammalian toxicity and adhesive compatibility trump weather durability. Bio-derived terpenes and nano-copper dispersions hover in pilot scale, their path impeded by multi-jurisdictional approvals. Over the forecast horizon, the water-based segment is expected to secure more share of wood preservatives market size, reflecting a decisive tilt toward chemistries that reconcile efficacy with environmental stewardship.

By End-User Industry: Residential Leadership Fueled by Outdoor Living

Residential projects supplied 52.26% of global volume in 2025, translating to the single largest slice of the wood preservatives market share. Pandemic-era home improvement raised the baseline for decking, fencing, and landscaping, and that momentum persists. The segment is on track to expand at a 4.56% CAGR, surpassing every other end-user cohort. Copper-azole remains the default for southern yellow pine decks, while borate diffusions gain share in indoor framing free from weather exposure.

Commercial and institutional builders follow in second position, using treated wood for façades, site furnishings, and sheltered load-bearing beams. Infrastructure users, utilities, railways, and marina operators require industrial-strength retentions and point to a durable revenue stream tied to cyclical replacement. The installed base of over 130 million poles in the United States alone ensures recurring treatment needs. Industrial sites round out demand with cooling-tower fills and chemical-resistant platforms that rely on reverse-treated timbers. Even as residential consumption leads the growth narrative, infrastructure remains a stabilizing anchor that insulates the wood preservatives industry from housing downturns.

Geography Analysis

North America generated 36.14% of global sales in 2025, underpinned by a mature installed base of utility poles and a housing stock that embraces pressure-treated lumber for exterior applications. US utilities continued field verification of copper naphthenate and micronized-copper poles ahead of the February 2027 pentachlorophenol sunset EPA.GOV. Canada’s forestry sector provides a reliable supply of preservative-grade lumber, while Mexico’s growing middle class sustains fencing and decking activity. Europe remains defined by stringent Biocidal Products Regulation scrutiny, which both inflates compliance costs and fosters innovation. Germany, France, and the United Kingdom account for the majority of European demand, and Arxada’s 2023 GB BPR authorization for Tanasote underscores the pathway for new copper-oil hybrids.

Asia-Pacific is on a faster track, poised to grow at a 5.72% CAGR as China and India concentrate infrastructure spending on rail and bridge programs that specify treated sleepers and load-bearing timbers. India’s National Infrastructure Pipeline draws heavily on treated wood to stretch budgets and accelerate project timelines. China’s coastal port expansions likewise depend on marine-grade pilings. Japan’s aging grid and rail infrastructure create steady replacement cycles even as the nation pioneers mass-timber mid-rise apartments. ASEAN economies favor cost-effective oil-borne preservatives, but environmental codes are tightening and will gradually channel demand toward water-based systems. South America’s outlook hinges on Brazil’s Minha Casa Minha Vida housing program and Argentina’s farm infrastructure expansion, while fiscal constraints moderate upside in the Middle East and Africa.

The combined dynamics yield a diversified demand map: North America and Europe present high-regulation, high-value environments; Asia-Pacific offers the strongest volume growth; Latin America, the Middle East, and Africa supply option value that hinges on macroeconomic stability.

Competitive Landscape

The Wood Preservatives market is moderately consolidated. Arxada’s fifth-generation Wolman E copper azole integrates 96.1% recycled copper and reduces volatile organic compounds in response to LEED and BREEAM scoring. Koppers Performance Chemicals booked USD 198.5 million in Q3 2024 revenue inside its Performance Chemicals division, reflecting stable sales to utilities and railways despite industrial softness. LANXESS continued portfolio pruning by divesting its iron-oxide pigments arm in 2024, sharpening focus on specialty chemicals. Overall, the competitive picture balances entrenched technology leaders with a fringe of innovative startups, producing a market where differentiation rests on compliance assurance, field data depth, and supply-chain resilience.

Wood Preservatives Industry Leaders

Koppers Performance Chemicals

LANXESS

Lonza

LANXESS

Viance

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: UBC Okanagan’s School of Engineering announced that its researchers, in their latest study, demonstrated that the Plastination technique can also be used on Western red cedar to make it stronger and protect the wood from water damage and decay. Plastination manages moisture in wood by replacing water in the cellular structure with a silicone compound.

- June 2025: MYLVA, a pest control company, enlisted TECNALIA experts to evaluate the effectiveness of its wood protection products against wood-boring insects. The assessment adhered to standards EN 46, EN 118, and EN 1390, and was conducted in TECNALIA's laboratories.

Global Wood Preservatives Market Report Scope

Wood preservatives help control wood degradation problems due to fungal rot or decay, sap stains, molds, or wood-destroying insects. Their usage helps increase a product's long-term resistance to attack by fungi, bacteria, insects, and marine borers.

The wood preservative market is segmented by technology, end-user industry, and geography. By technology, the market is segmented into water-based technologies, oil-based technologies, and other emerging technologies. By end-user industry, the market is segmented into residential construction, commercial and institutional buildings, infrastructure, and industrial facilities. The report also studies the wood preservatives market in 16 countries across major regions. For each segment, the market sizing and forecasts have been done based on value (USD).

| Water-based Technologies | Micronized Copper Systems |

| Chromated Copper Arsenate (legacy/phase-out markets) | |

| Borates (indoor use) | |

| Other Technologies (Bio-based and Nano-formulated Preservatives) | |

| Oil-based Technologies | Pentachlorophenol |

| Creosote | |

| Other Oil Based Technologies (Vegetable-oil Carriers and Hybrid Oils) | |

| Other Emerging Technologies |

| Residential Construction |

| Commercial and Institutional Buildings |

| Infrastructure (utility poles, rail, bridges, and ports) |

| Industrial Facilities |

| Asia-Pacifc | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology | Water-based Technologies | Micronized Copper Systems |

| Chromated Copper Arsenate (legacy/phase-out markets) | ||

| Borates (indoor use) | ||

| Other Technologies (Bio-based and Nano-formulated Preservatives) | ||

| Oil-based Technologies | Pentachlorophenol | |

| Creosote | ||

| Other Oil Based Technologies (Vegetable-oil Carriers and Hybrid Oils) | ||

| Other Emerging Technologies | ||

| By End-user Industry | Residential Construction | |

| Commercial and Institutional Buildings | ||

| Infrastructure (utility poles, rail, bridges, and ports) | ||

| Industrial Facilities | ||

| By Geography (Value) | Asia-Pacifc | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the wood preservatives market in 2026?

The wood preservatives market size reached USD 3.17 billion in 2026 and is expected to expand steadily through 2031.

What is the projected growth rate for wood preservatives through 2031?

The market is forecast to register a 4.46% CAGR between 2026 and 2031 as residential construction and infrastructure renewal offset regulatory headwinds.

Which technology dominates wood preservation today?

Water-based systems held 79.05% of revenue in 2025 thanks to micronized-copper innovation and favorable environmental profiles.

Why are utilities moving away from pentachlorophenol?

The United States Environmental Protection Agency ordered a full phase-out of pentachlorophenol by February 2027, directing utilities toward copper-based alternatives.

Which region is expected to grow fastest?

Asia-Pacific is set to outpace all regions with a 5.72% CAGR, driven by infrastructure investment in China and India.

Page last updated on: