Rapid Prototyping Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

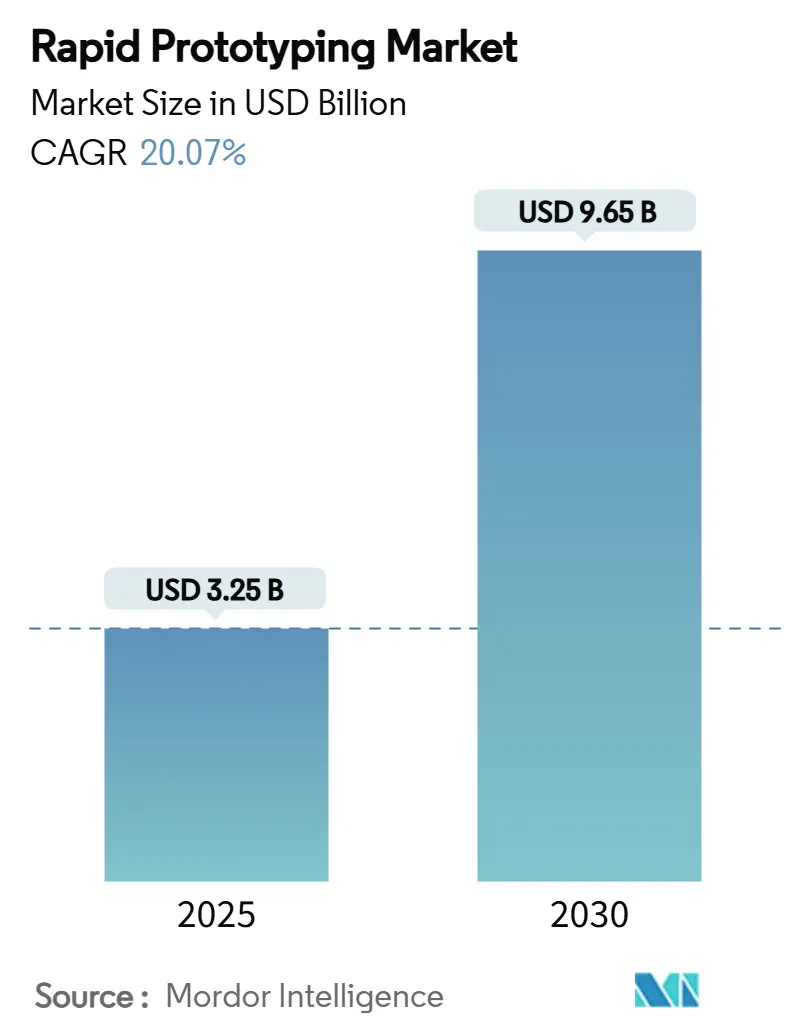

| Market Size (2025) | USD 3.25 Billion |

| Market Size (2030) | USD 9.65 Billion |

| Growth Rate (2025 - 2030) | 20.07% CAGR |

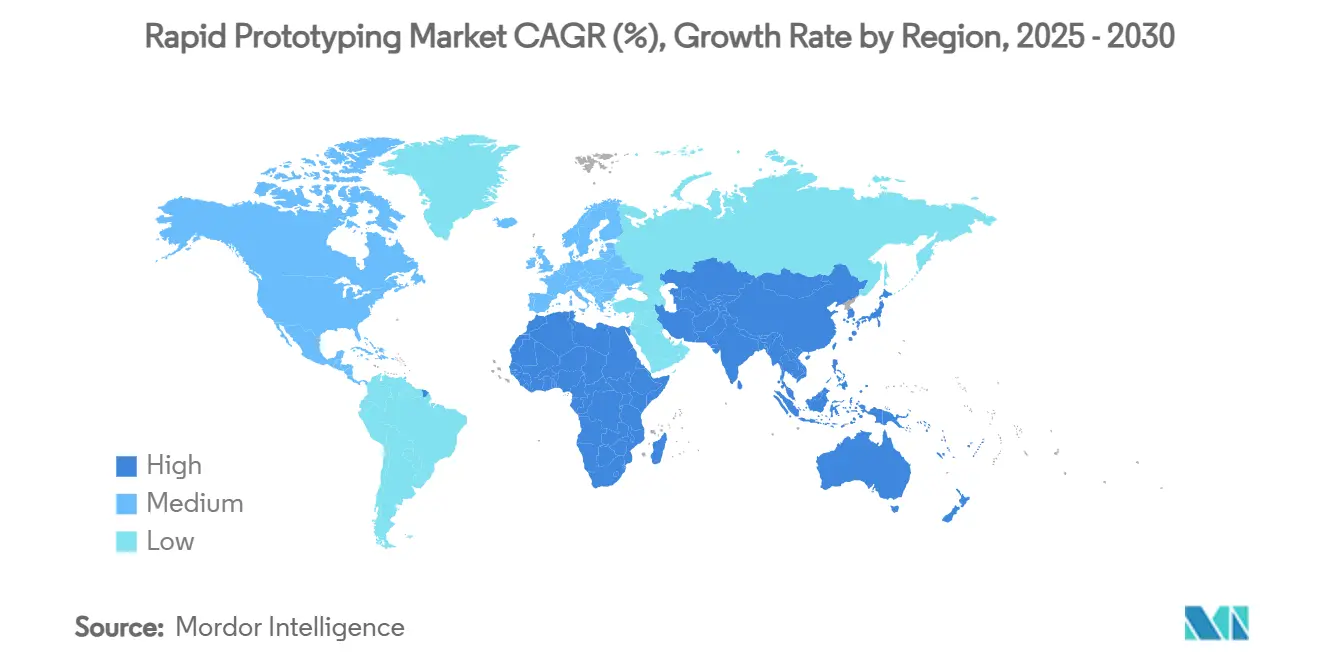

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Rapid Prototyping Market Analysis by Mordor Intelligence

The rapid prototyping market size stands at USD 3.25 billion in 2025 and is projected to reach USD 9.65 billion by 2030, advancing at a 20.07% CAGR. This rapid prototyping market momentum comes from the maturing of additive manufacturing, the roll-out of digital thread workflows, and record levels of public funding for advanced production capacity. Producers are replacing stand-alone prototyping labs with integrated cells that support short-run production, slashing design cycles and tooling budgets. Competitive gaps now revolve around software interoperability, validated material portfolios, and the ability to run multiple builds in parallel. Vendors that offer closed-loop quality control and traceable data trails attract regulated customers that must document each process step. As a result, platform providers able to combine printers, materials, and cloud analytics are moving further ahead of single-product rivals.

Key Report Takeaways

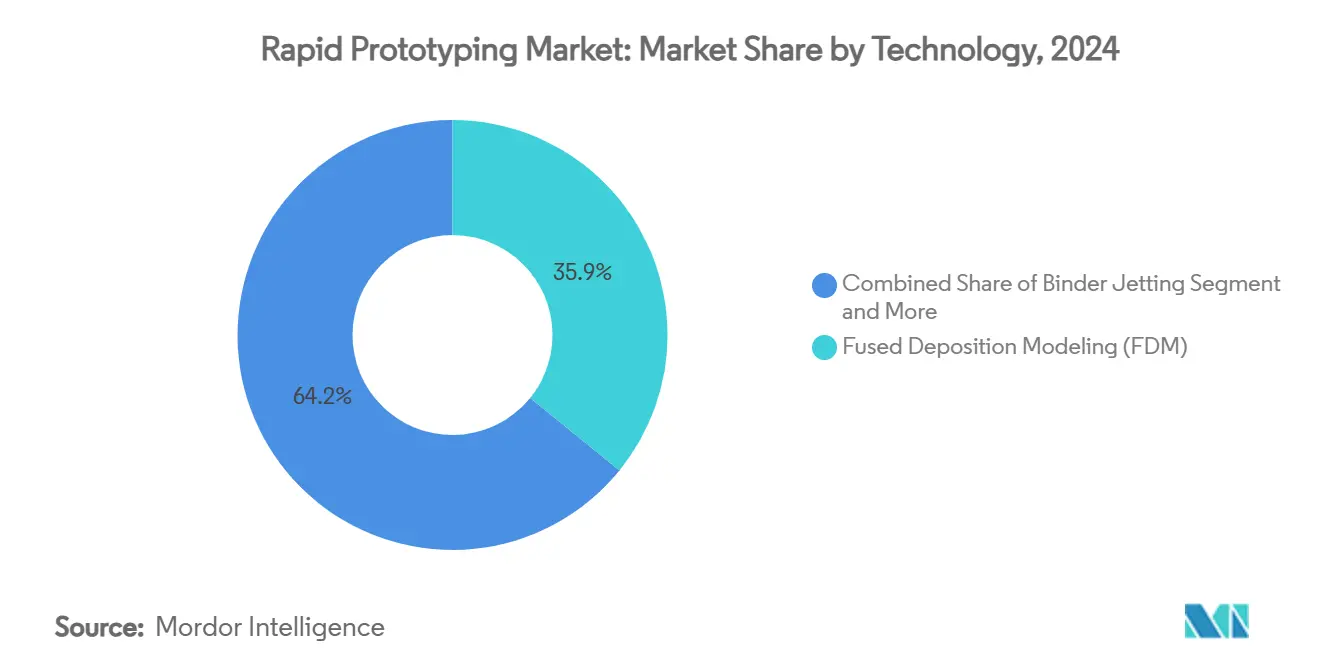

- By technology, Fused Deposition Modeling led with 35.85% rapid prototyping market share in 2024, while Binder Jetting is forecast to grow at 25.76% CAGR through 2030.

- By material type, polymers accounted for 47.02% of the rapid prototyping market size in 2024; metals are poised to expand at a 22.87% CAGR between 2025-2030.

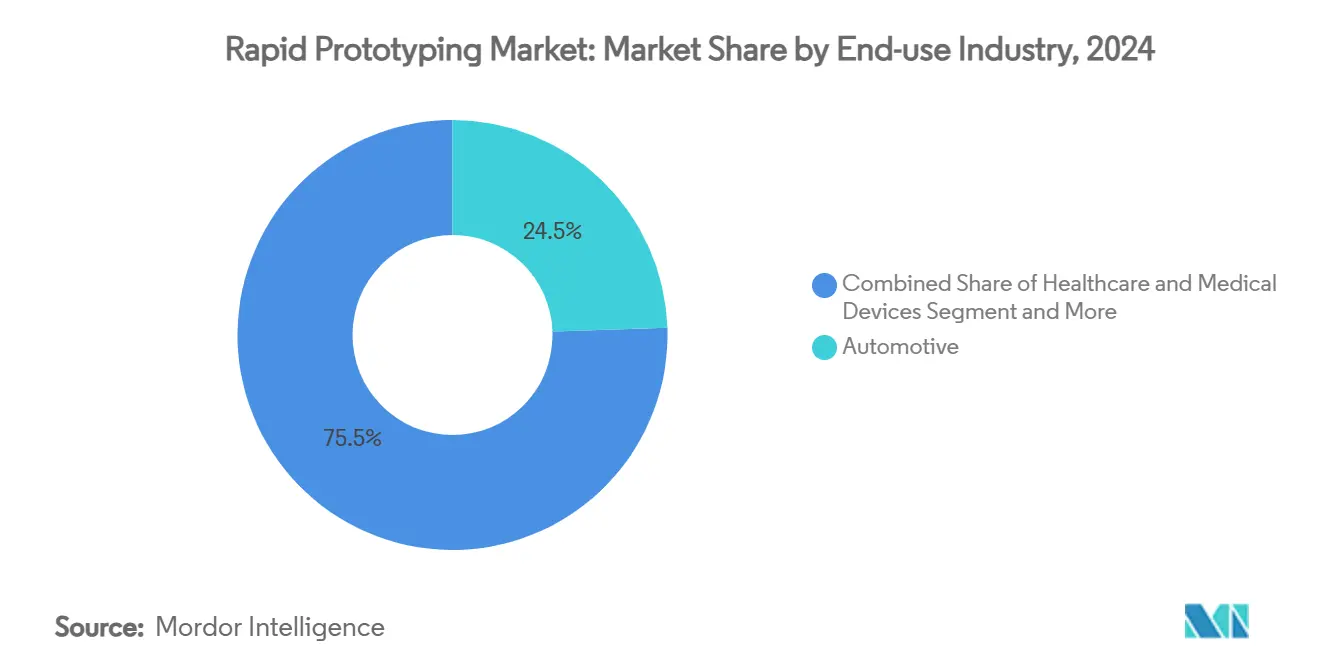

- By end-use industry, automotive held 24.46% revenue share in 2024, whereas healthcare is projected to rise at a 24.75% CAGR to 2030.

- By service type, prototype development services captured 38.76% of the rapid prototyping market size in 2024, while low-volume production parts will advance at a 23.37% CAGR during the same period.

- By region, North America led with 38.67% revenue share in 2024; Asia-Pacific is expected to post the fastest 24.02% CAGR to 2030.

Global Rapid Prototyping Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost and time compression through additive prototyping | +4.2% | Global, strong in North America & EU | Short term (≤ 2 years) |

| Falling polymer AM material prices | +3.1% | Global, strongest in APAC hubs | Medium term (2-4 years) |

| Government-aerospace AM funding surge | +2.8% | North America & EU, selective APAC | Medium term (2-4 years) |

| Digital thread adoption across design-to-print workflow | +3.5% | Global, led by North America industry | Long term (≥ 4 years) |

| AI-driven generative design integration | +2.9% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Bio-sourced materials for sustainable prototypes | +2.1% | EU leadership, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost and time compression through additive prototyping

Enterprises that substitute tool-free builds for traditional machining shrink development calendars from months to weeks. The U.S. Air Force awarded USD 8.7 million to Relativity Space for research that demonstrates defense demand for shorter iteration loops. Atlas Copco achieved 30% lower costs and a 92% lead-time cut after shifting key parts to in-house polymer printing. Automated build prep and AI scheduling widen the gap by raising machine utilization and keeping quality inside specification. Benefits are most visible on lattice-based cooling channels and conformal fixtures that are impossible to mill. Companies now view the capability as a competitive necessity when launching complex products.

Falling polymer AM material prices

Volume economies, recycling loops, and new feedstocks continue to push polymer costs down. HP's PA 12 S offers an 85% re-usability rate, lowering part cost without compromising finish. [1]HP Inc., "HP Unveils Disruptive New Material for 3D Polymers Production," press.hp.com Price trackers show softer engineering thermoplastic markets through 2024, reflecting oversupply and muted demand. Cellulose-based powders from MIT present plant-derived alternatives that reduce petrochemical exposure. Powder re-conditioning lets operators reclaim unused feedstock, closing the cost gap with injection-molded prototypes. Lower inputs open the rapid prototyping market to mid-tier firms that previously relied on external model shops.

Government–aerospace AM funding surge

Public agencies are channeling grants toward lightweight flight hardware. The U.S. Department of Energy earmarked USD 33 million for smart manufacturing, while the UK reserved GBP 100 million (USD 127 million) for greener aviation.[2]U.S. Department of Energy, “33 Million in Funding Available To Advance Smart Manufacturing Technologies,” energy.govAmerica Makes distributed USD 2.1 million to material-qualification projects that underpin certified aerospace parts. Such funding raises the baseline for process control and propels buying cycles for large-format metal printers.

Digital thread adoption across design-to-print workflow

Model-based definitions and IoT machine data now travel on a single thread, trimming hand-offs. MIT’s cross-industry maturity study links thread implementation to measurable productivity gains. Stratasys’ GrabCAD IoT captures real-time sensor data and remote diagnostics, helping operators solve issues before scrap accumulates. Integrated GD&T annotations further remove interpretation errors, especially on high-tolerance assemblies. Continuous feedback accelerates closed-loop improvements and strengthens compliance documentation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of industrial systems | -2.8% | Global, strongest in emerging markets | Short term (≤ 2 years) |

| Skilled-labor shortage for AM & hybrid CNC | -2.1% | North America & EU, spreading to APAC | Medium term (2-4 years) |

| Emerging bans on fine-polymer powders | -1.4% | EU lead, possible global adoption | Long term (≥ 4 years) |

| IP leakage and cyber-risk in cloud CAD sharing | -1.7% | Global, acute in defense and aerospace | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High capital cost of industrial systems

Metal printers and hybrid mills can exceed USD 1 million per cell, delaying orders when budgets tighten. Desktop Metal’s Q1 2024 revenue of USD 40.6 million highlighted cautious spending. Stratasys likewise reported a 13.6% sales drop in Q3 2024 as customers extended decision cycles. Service models and leasing reduce entry barriers, but full return on investment still depends on continuous machine loading.

Emerging bans on fine-polymer powders

The European Chemicals Agency seeks stricter limits on respirable silica, pushing vendors to certify closed powder loops. The U.S. EPA now requires 90-day notifications for any substance forming particles under 50 µm. [3]Environmental Protection Agency, “Significant New Use Rules on Certain Chemical Substances,” federalregister.gov Compliance adds filtration and monitoring costs, weighing on smaller service bureaus.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Binder Jetting disrupts FDM dominance

FDM commanded a 35.85% share of the rapid prototyping market in 2024 owing to low printer prices and robust polymer choices. Yet Binder Jetting will advance at a 25.76% CAGR as it prints metals, ceramics, and composites without warping. Improved silicon-carbide green densities of 1.87 g/cm³ at 60 µm layers underline progress in high-temperature materials. Dual-material jets simplify support removal, reducing post-processing labor. Powder-bed fusion retains an edge for aerospace super-alloys, but binder systems gain momentum in tooling inserts and pump components requiring infiltrated steel.

Second-generation Digital Light Processing targets dental aligners where layer lines must be invisible. Selective Laser Sintering persists in nylon housings and latticed footwear midsoles. Vacuum casting and CNC machining still cover oversized prototypes or parts with embedded electronics. Overall, rapid prototyping market adoption now follows a multi-technology toolkit that aligns cost, tolerance, and surface quality with the intended life cycle.

By Material Type: Metals challenge polymer supremacy

Polymers captured 47.02% of 2024 revenue, bolstered by ABS, PLA, and elastomer blends for conceptual models. Metal powders, however, are set for a 22.87% CAGR through 2030 as aerospace and healthcare demand fully dense parts. Steel coil prices between USD 800-1,000 per ton keep stainless feedstock attractive, while aluminum trades at USD 2,500-3,000 per metric ton and supports lightweight brackets. Recycling sieves, vacuum degassing, and plasma spheroidization techniques extend powder life and curb waste.

Copper and titanium remain premium due to challenging thermals but find niches in heat exchangers and implants. Composite pellets incorporating carbon fiber push stiffness-to-weight ratios beyond die-cast magnesium. Bio-based resins and flexible photopolymers enter medical wearables, signaling a diversified palette that aligns properties with regulatory and performance constraints.

By End-use Industry: Healthcare disrupts automotive leadership

Automotive accounted for 24.46% of 2024 spending, utilizing polymers for quick jigs and vents plus metals for turbo housings. Healthcare is forecast to post a 24.75% CAGR as patient-matched implants pass FDA De Novo reviews and predetermined change plans speed design updates. The restor3d total talus implant, formed from individual CT data, illustrates the value of bespoke parts.

Aerospace benefits from government backing and stringent buy-to-fly ratios that favor lattice infill. Consumer electronics apply micro-SLA for tight housing tolerances, while industrial machinery employs on-demand spares to cut warehouse inventory. Construction’s move toward 3D-printed walls opens a fringe but rising application, particularly in regions facing skilled bricklayer shortages.

By Service Type: Production parts reshape prototyping focus

Prototype development services held 38.76% of the rapid prototyping market in 2024, but low-volume production parts will outpace at 23.37% CAGR as tolerance and certification barriers fall. Protolabs posted USD 126.2 million Q1 2025 revenue even as traditional prototyping slowed, reflecting demand for end-use builds. Online quoting engines and distributed partner networks allow customers to place metal, polymer, and sheet-metal orders through a single portal.

Functional tooling fills the bridge between prototype and mass production, especially for injection-molding test shots. Design and engineering service bundles now include DFAM (design for additive manufacturing) consults that cut weight and consolidate assemblies. Concept modeling remains essential at early stages, yet its revenue share continues to decline as companies skip directly to production-grade iterations.

Geography Analysis

North America led with 38.67% of 2024 sales thanks to defense budgets and a dense aerospace supplier base. The U.S. Air Force’s contract with Relativity Space and America Makes’ USD 2.1 million project pool reinforce a priority on certified metal printing. Canada adds niche capability in cold-spray metal repair, and Mexico offers cost-effective electronics casting, completing a continental value chain.

Europe maintains balanced growth across Germany, the United Kingdom, France, and Italy, each leveraging historic industrial bases. The UK earmarked GBP 100 million (USD 127 million) for greener aviation, and the EU’s Clean Aviation fund allocated EUR 154 million (USD 174 million) in 2024 to low-carbon flight demonstrators. Strength in regulatory frameworks shapes material R&D toward recyclability and low-toxicity powders. Spain’s automotive clusters and Italy’s luxury-goods mold shops show rising demand for flexible tooling.

Asia-Pacific is the fastest-growing region with a 24.02% CAGR. Chinese firms raised 6.4 billion yuan in 2022, and new implementation opinions aim at global standards by 2025. India accelerates via the EOS-Godrej aerospace alliance that dovetails with Make in India policy. Japan and South Korea focus on dental and electronics niches, while Australia exploits mining R&D for wear-resistant alloy powders.

Middle East & Africa and South America remain emerging plays. UAE universities run pilot houses printed from local sand, whereas Brazil investigates bio-composite feedstocks for agricultural machinery repairs. Infrastructure and skills gaps temper uptake, but resource extraction industries create demand for on-site spare parts that bypass long import queues.

Competitive Landscape

Market fragmentation is moderate: top printer makers exceed USD 1 billion in annual revenue yet face niche challengers in materials, software, and AI optimization. Ecosystem platforms by Stratasys, EOS, and HP pair proprietary resins with closed-loop firmware, increasing customer switching costs. Binder-jet start-ups specialize in refractory metals, while software firms deploy in-process tomography and machine learning to compress qualification cycles.

Service bureaus evolve into hybrid manufacturers offering machining, molding, and inspection under one roof. Protolabs’ shift toward production demonstrates this trajectory, as does Materialise’s decision to unlock Magics APIs for customized workflows. Patent filings for vacuum-assisted extrusion and laser-ablated bound metal deposition indicate sustained R&D activity that can erode current process hierarchies.

AI start-ups targeting build-failure prediction or automatic orientation compete for the same slice of software budgets as incumbent MES vendors. Sustainability innovators leverage bio-derived powders to address European restrictions on microplastics, winning pilot projects in packaging and sports gear. Overall, differentiation centers on validated workflows, regulatory ready materials, and data-rich quality systems.

Rapid Prototyping Industry Leaders

-

Stratasys Ltd.

-

3D Systems Corporation

-

Materialise NV

-

Proto Labs, Inc.

-

EOS GmbH Electro Optical Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: EOS and Godrej Enterprises Group formed a partnership to deploy large-format multi-laser systems for India’s aerospace supply chain.

- March 2025: Stratasys partnered with Boeing, Northrop Grumman, and the U.S. Air Force to qualify Antero 800NA and 840CN03 for mission-critical parts.

- February 2025: Stratasys secured a USD 120 million equity injection from Fortissimo Capital to support expansion.

- January 2025: America Makes awarded USD 2.1 million to projects on material qualification, sustainability, and production optimization.

Global Rapid Prototyping Market Report Scope

| Fused Deposition Modeling (FDM) |

| Stereolithography (SLA) |

| Selective Laser Sintering (SLS) |

| Digital Light Processing (DLP) |

| Binder Jetting |

| CNC Machining |

| Vacuum Casting |

| Rapid Injection Molding |

| Polymers | Thermoplastics |

| Photopolymers | |

| Metals | Aluminum |

| Titanium | |

| Stainless Steel | |

| Ceramics | |

| Composites |

| Automotive |

| Aerospace and Defense |

| Healthcare and Medical Devices |

| Consumer Electronics |

| Industrial Machinery |

| Construction |

| Education and Research |

| Prototype Development Services |

| Tooling and Functional Prototyping |

| Conceptual Modeling |

| Low-volume Production Parts |

| Design and Engineering Services |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Technology | Fused Deposition Modeling (FDM) | ||

| Stereolithography (SLA) | |||

| Selective Laser Sintering (SLS) | |||

| Digital Light Processing (DLP) | |||

| Binder Jetting | |||

| CNC Machining | |||

| Vacuum Casting | |||

| Rapid Injection Molding | |||

| By Material Type | Polymers | Thermoplastics | |

| Photopolymers | |||

| Metals | Aluminum | ||

| Titanium | |||

| Stainless Steel | |||

| Ceramics | |||

| Composites | |||

| By End-use Industry | Automotive | ||

| Aerospace and Defense | |||

| Healthcare and Medical Devices | |||

| Consumer Electronics | |||

| Industrial Machinery | |||

| Construction | |||

| Education and Research | |||

| By Service Type | Prototype Development Services | ||

| Tooling and Functional Prototyping | |||

| Conceptual Modeling | |||

| Low-volume Production Parts | |||

| Design and Engineering Services | |||

| by Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the rapid prototyping market by 2030?

It is forecast to reach USD 9.65 billion, reflecting a 20.07% CAGR over 2025-2030.

Which technology is growing fastest within rapid prototyping?

Binder Jetting is expected to post the highest 25.76% CAGR through 2030 due to multi-material capability.

Why is healthcare demand rising for rapid prototyping?

FDA pathway reforms and personalized implant needs drive a 24.75% CAGR, making healthcare the fastest-growing vertical.

Which region is forecast to expand most quickly?

Asia-Pacific is set for a 24.02% CAGR as China and India scale local manufacturing and attract public funding.

How are material prices influencing adoption?

Declining polymer costs and improved powder recycling are lowering per-part expenses, enabling wider market access.

What main factor restrains rapid prototyping growth?

The high upfront cost of industrial metal systems remains the largest barrier, especially for small manufacturers.

Page last updated on: