Data Preparation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.05 Billion |

| Market Size (2031) | USD 16.84 Billion |

| Growth Rate (2026 - 2031) | 15.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Preparation Market Analysis by Mordor Intelligence

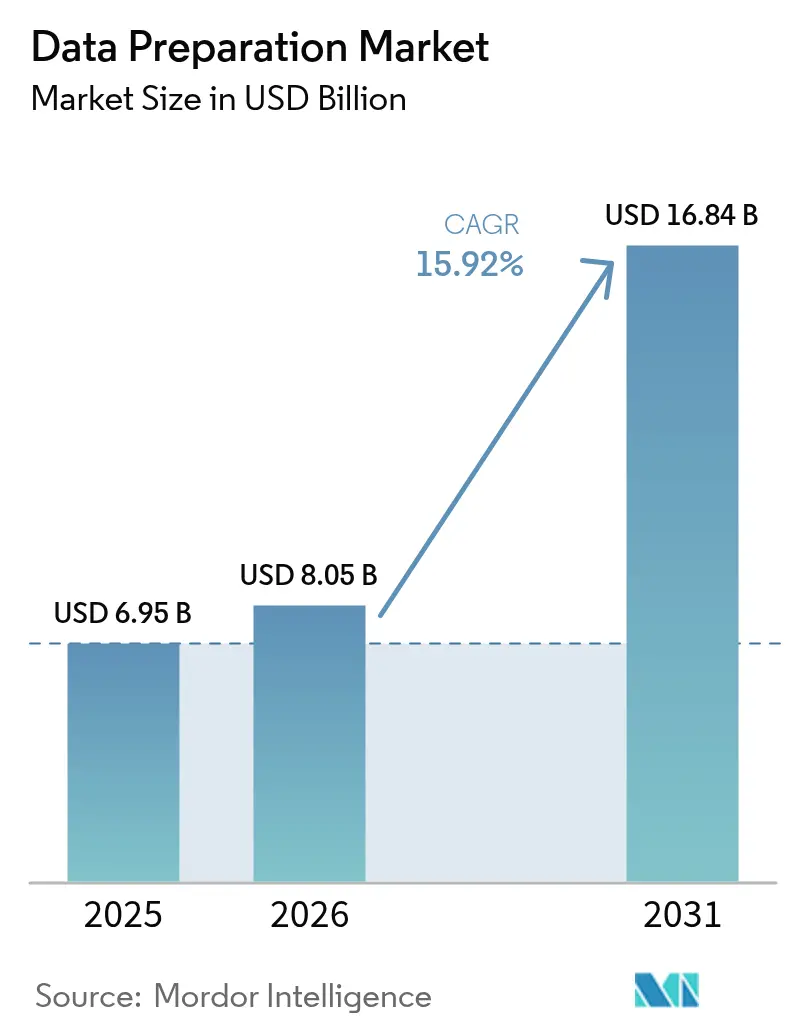

The data preparation market size is expected to grow from USD 6.95 billion in 2025 to USD 8.05 billion in 2026 and is forecast to reach USD 16.84 billion by 2031 at 15.92% CAGR over 2026-2031. This expansion mirrors the surge in AI-ready infrastructure as enterprises embed generative AI into day-to-day workflows; adoption has reached 83% of organizations in China and full production roll-outs in 24% of United States companies[1]SAS Institute, “AI Adoption Barometer 2024,” sas.com. Proliferating data-governance programs, now present in 71% of organizations compared with 60% in 2023, reinforce spending on systematic data preparation tools. Deployment choices continue to diverge: on-premises solutions controlled 65.7% of 2024 revenue, while cloud deployments are scaling fastest at 17.8% CAGR, a pattern shaped by sovereign-cloud regulations such as Vietnam’s Data Law, effective July 2025, that restrict cross-border transfers. Large enterprises held 68.9% revenue share in 2024, yet small and medium enterprises (SMEs) show the strongest momentum at 18.1% CAGR as low-code analytics and consumption-based pricing lower entry barriers. Data-ingestion modules retained the top 24.3% slice of 2024 revenue; however, governance-centric solutions are rising fastest at 17.3% CAGR, pushed by greenhouse-gas-reporting mandates emerging from the EU Corporate Sustainability Reporting Directive. IT and telecommunications contributed the largest 22.8% vertical share in 2024, while healthcare and life sciences climbed at a 16.8% CAGR through 2030 as AI enters diagnosis, patient-workflow and life-science research and development. Regionally, North America led with 37.1% revenue in 2024, yet Asia-Pacific will outpace all others at 17.5% CAGR, underpinned by expanding data-center capacity—12,206 MW active and 14,338 MW in development. Mergers and acquisitions activity signals intensifying competition: Salesforce agreed to purchase Informatica for USD 8 billion in May 2025, and Alteryx was taken private for USD 4.4 billion in March 2024.

Key Report Takeaways

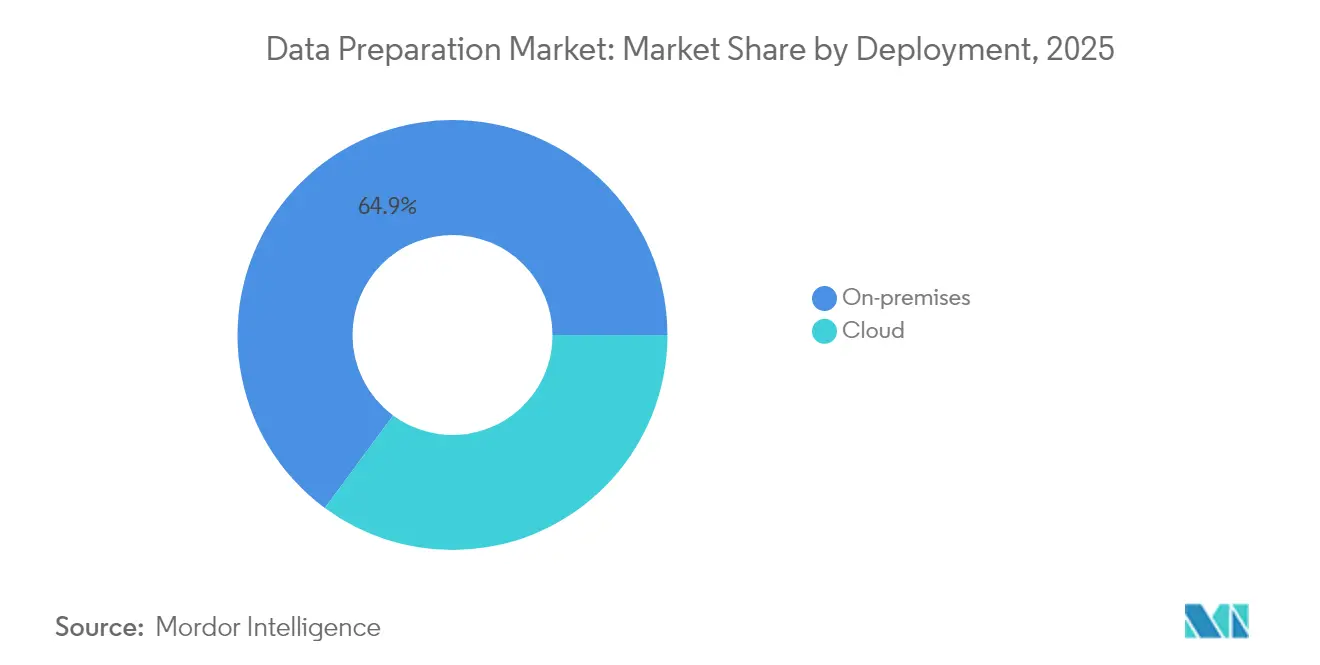

- By deployment, on-premises platforms held 64.88% of the data preparation market share in 2025; cloud models are forecast to expand at a 17.12% CAGR through 2031.

- By enterprise size, large organizations led with 68.05% revenue share in 2025, while SMEs are advancing at an 17.62% CAGR to 2031.

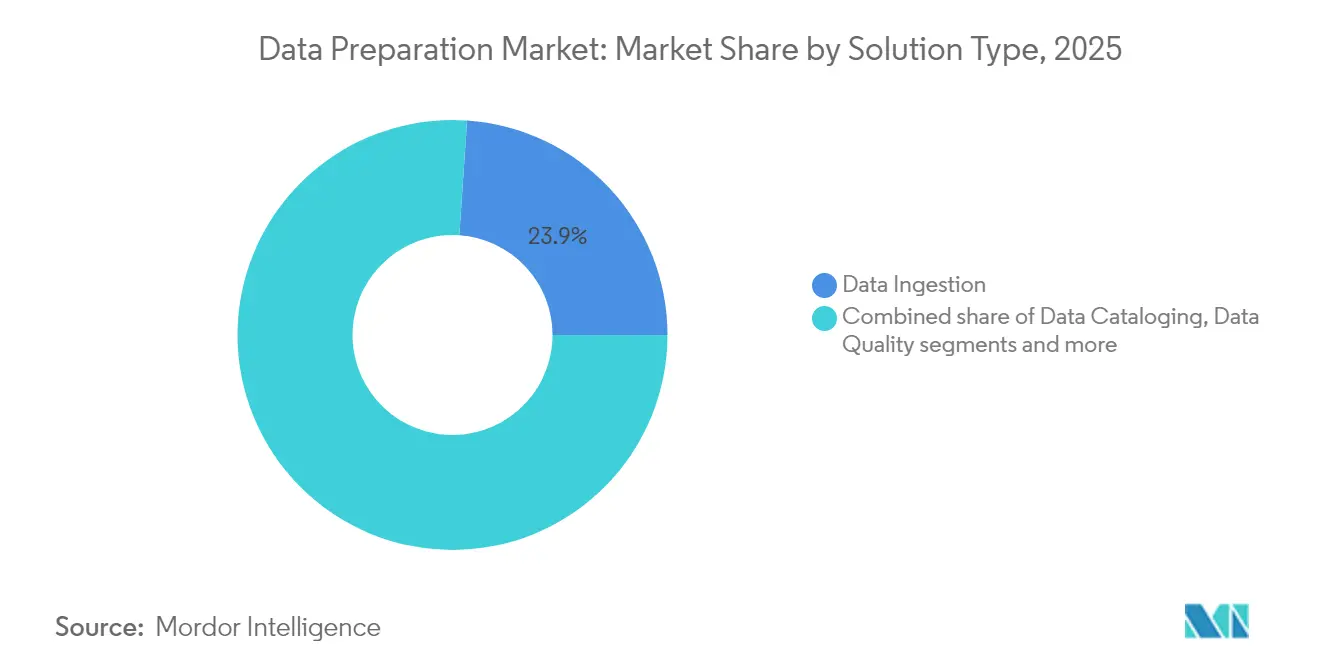

- By solution type, data ingestion captured 23.92% of 2025 revenue; data governance solutions are set to grow at 16.74% CAGR to 2031.

- By end-user vertical, IT and telecommunications accounted for 22.35% of 2025 sales; healthcare and life sciences post the quickest 16.31% CAGR through 2031.

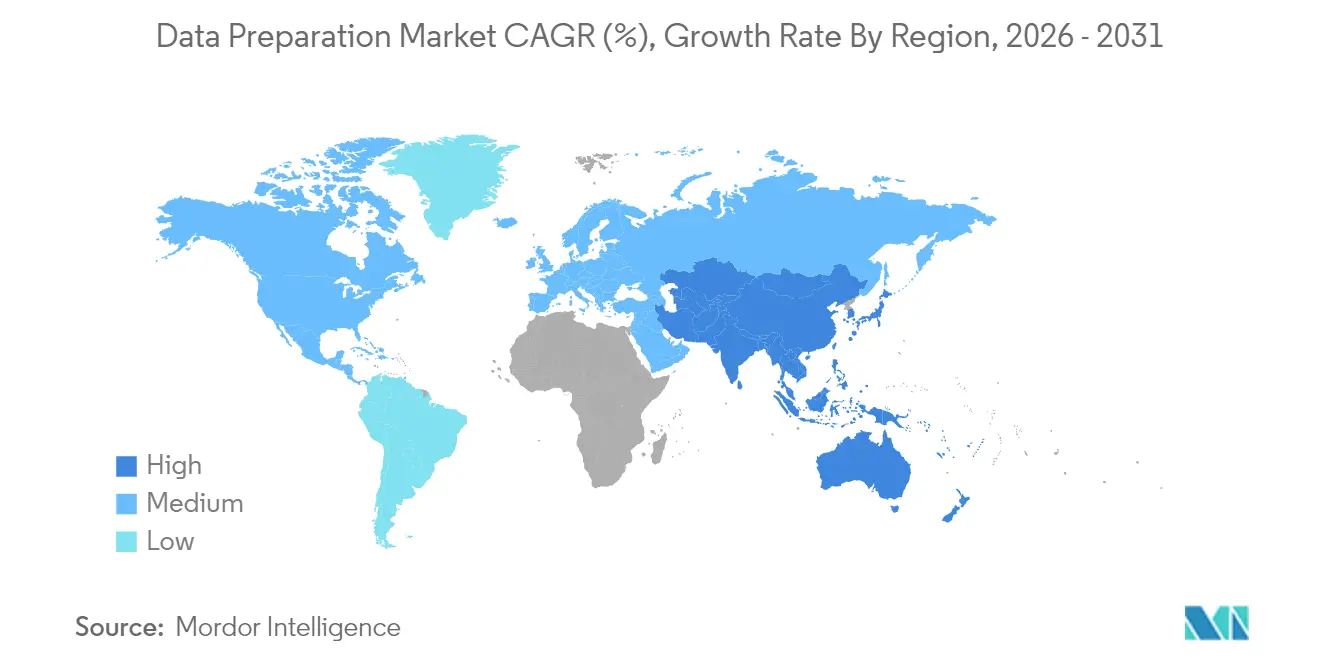

- By geography, North America commanded 36.62% revenue share in 2025; Asia-Pacific shows the strongest 16.98% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Preparation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low-/no-code self-service analytics tools | +3.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Cloud adoption by SME analytics teams | +2.8% | Global, with Asia-Pacific highest growth | Short term (≤ 2 years) |

| GenAI copilots inside data-prep workflows | +3.5% | North America and Asia-Pacific core, spill-over to Europe | Medium term (2-4 years) |

| Vendor bundling into data-fabric suites | +2.1% | Global, enterprise focus in developed markets | Long term (≥ 4 years) |

| Vertical-specific AI data-prep pipelines | +2.4% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Sovereign-cloud regulation and repatriation | +1.8% | Asia-Pacific and Europe, regulatory focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Shift to Low-/No-Code Self-Service Analytics Tools

Low-code interfaces are redefining the data preparation market by enabling business specialists to build pipelines via drag-and-drop designs rather than scripts. Google Cloud’s BigQuery data preparation illustrates the trend, offering AI guidance that cleans, profiles and transforms data with natural-language prompts[2]Google Cloud, “Introducing BigQuery Data Preparation,” cloud.google.com. The approach reduces reliance on scarce data engineers, shortens development cycles and aligns analytics delivery with domain expertise. GenAI-powered augmentation is spreading quickly; industry forecasts suggest nearly all BI platforms will embed GenAI by 2026. Adoption, however, requires diligent governance to keep proliferating citizen-built flows aligned with enterprise quality and security standards.

Surging Cloud Adoption Among SME Analytics Teams

SMEs are scaling cloud-native pipelines to close capability gaps with larger rivals, driving incremental demand across Asia-Pacific where 60% of firms plan AI language-model implementation by 2025. Cloud elasticity and consumption pricing let smaller firms avoid capital expenses while accessing advanced data-prep functions. UK research shows sub-1% of SMEs exploit big-data analytics today, underscoring runway as cost and complexity hurdles fall. Yet skills shortages persist; managed service providers are stepping in to configure pipelines and enforce compliance, particularly around emerging data-localization rules.

Integration of GenAI Copilots Inside Data-Prep Workflows

Seventy-five percent of organizations intend to fund GenAI within twelve months, making AI copilots central to transformation strategies. Copilots automate tedious profiling, suggest optimal joins and flag anomalies, compressing the 94% of project time traditionally spent on cleaning. Natural-language interaction lowers the expertise threshold, though automated outputs must still pass governance gates that track lineage and validate accuracy. Investment momentum is highest in data-intensive verticals such as telecom and finance, where even marginal time savings yield material ROI.

Vendor Bundling of Data-Prep Modules into Broader Data-Fabric Suites

Acquisitions such as Salesforce-Informatica illustrate consolidation toward unified fabrics housing catalog, quality, lineage and orchestration. The strategy simplifies integration overhead by delivering an end-to-end workspace from ingest to BI, improving consistency across multi-cloud estates. However, the all-in-one push raises vendor-lock-in risks and limits plug-and-play agility. Enterprises are evaluating standards such as OpenLineage and Apache Arrow to preserve optionality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skills gap for data-governance configuration | -2.3% | Global, acute in emerging markets | Medium term (2-4 years) |

| High TCO of multi-cloud data pipelines | -1.9% | North America and Europe | Short term (≤ 2 years) |

| Escalating data-sovereignty penalties | -1.4% | Asia-Pacific and Latin America | Medium term (2-4 years) |

| Compute-intensive jobs face carbon quotas | -1.1% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skills Gap for Complex Data-Governance Configuration

Nearly one-third of CIOs cite data-management complexity as a critical obstacle, and shortages of governance specialists delay the rollout of scalable pipelines[3]Lenovo and IDC, “AI Readiness Study 2024,” lenovo.com. The challenge intensifies where legislation such as California’s climate-disclosure rule mandates automated capture of Scope 1-3 emissions. Emerging markets face deeper shortages as academic programs lag, pushing firms toward external consultants and managed-service contracts that inflate deployment budgets.

Steep Total Cost of Ownership for Multi-Cloud Data Pipelines

A majority of multicloud programs miss ROI targets as integration, replication and monitoring expenses rise faster than forecast. Region-specific storage mandated by localization laws further inflates spend as firms duplicate infrastructure across zones. Operational overhead can exceed 25% of aggregate cloud budgets once security and lineage tools are added, pressuring mid-market buyers to compromise between architectural elegance and affordability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Acceleration Balances On-Premises Dominance

The data preparation market size for on-premises platforms totaled USD 4.51 billion in 2025, translating to 64.88% data preparation market share, a reflection of enterprise demand for direct control amid tougher localization rules. Vietnam’s Data Law and India’s Digital Personal Data Protection Rules reinforce on-prem and sovereign-cloud models that keep sensitive records within national borders. Cloud services, though smaller, are projected to compound at 17.12% through 2031 as SMEs and digitally native units prioritize agility. In North America, hybrid blueprints predominate, fusing local clusters for regulated data with hyperscale reservoirs for lower-risk workloads. Cloud providers respond with dedicated regional instances and encrypted-key control to offset compliance fears, widening adoption beyond traditional tech hubs as smaller cities gain direct-connect fiber.

The economic calculus hinges on workload variability: steady ETL batches and predictable enrichment jobs remain on-prem due to licensing amortization, while bursty AI inference and citizen-developer sandboxes migrate to pay-as-you-go clouds. Over half of multinationals are expected to run sovereign-cloud instances by 2029, creating demand for seamless policy enforcement across private, public and edge nodes. Vendors now emphasize unified control planes that propagate data-quality rules and lineage graphs no matter the substrate.

By Enterprise Size: SMEs Propel Future Upside Despite Large-Company Lead

Large corporations generated USD 4.73 billion revenue in 2025, equal to 68.05% of the data preparation market, supported by dedicated governance teams and global footprints. Their spend skew favors platform bundles that integrate catalog, lineage and observability into existing data fabrics. Conversely, SMEs contributed USD 2.22 billion yet will outgrow other cohorts at 17.62% CAGR, lifting the data preparation market size for SME solutions to a projected USD 5.02 billion by 2031. Consumption billing and automated schema-detection reduce capital obstacles, enabling regional retailers, fintechs and SaaS start-ups to achieve parity with incumbents.

A Small Business Institute Journal survey shows 70% of U.S. SMEs acknowledge analytics value, but only a minority has in-house talent to execute end-to-end pipelines. Low-code cloud workbenches and managed-service ecosystems fill gaps, while industry associations offer modular training to accelerate citizen usage. Challenges persist in developing policy frameworks that map to emerging AI-act obligations, creating openings for channel partners specializing in compliance overlays.

By Solution Type: Governance Gains Speed as Ingestion Retains the Crown

Data ingestion retained a commanding 23.92% of 2025 revenue, underlining the foundational need to collect structured, semi-structured and unstructured feeds for downstream refinement. Yet governance modules will post the quickest 16.74% CAGR, reflecting the regulatory pivot toward audit-ready ESG and AI-ethics disclosures. The data preparation market size for governance tools is forecast to reach USD 3.74 billion by 2031. Integrated metadata-driven catalogs now attach automated policy checks, making lineage visualizations central to risk management. Synthetic-data generators embed privacy safeguards while expanding AI training sets, helping firms meet minimization requirements without degrading model accuracy.

Adjacent categories—quality, wrangling, enrichment—are coalescing into single UI layers. Product roadmaps prioritize context-aware suggestions that learn preferred business rules and propose standardization patterns. Vendors court partner ecosystems to package vertical templates, such as healthcare HL7-FHIR normalizers or financial FIX-protocol mappers, boosting time-to-value and reinforcing switching costs.

By End-User Vertical: Healthcare Surges While IT and Telecom Stays on Top

IT and telecommunications booked USD 1.55 billion in 2025, equating to 22.35% of the data preparation market, fueled by 5G roll-outs that generate telemetry requiring rapid cleansing and enrichment. Operators lean on AI to optimize network utilization and predict churn, driving spend on high-throughput pipeline automation. Healthcare and life sciences, at USD 1,018 million in 2025, will climb fastest at 16.31% CAGR as hospitals digitize patient pathways and pharmaceutical firms orchestrate multi-omics datasets for drug discovery. The data preparation industry faces strict HIPAA, GDPR and upcoming EU AI Act stipulations that elevate governance modules to must-have status.

Banking, financial services and insurance (BFSI) sectors adopt GenAI for fraud detection and hyper-personalized advice—China already logs 83% organizational usage—placing heavy emphasis on explainability and lineage to satisfy supervisory boards. Retailers deploy customer-graph enrichment to feed recommendation APIs and measure Scope 3 emissions, linking transactional records with supplier audits to meet emerging sustainability pledges. Government programs harness open-data portals and internal dashboards for evidence-based policy, although budget ceilings and procurement cycles elongate project timelines.

Geography Analysis

North America’s USD 2.54 billion spend in 2025 reflected 36.62% data preparation market share, an outcome of early AI experimentation and dense vendor ecosystems. California’s climate-disclosure statute compels companies above USD 1 billion revenue to publish Scope 1-3 emissions, reinforcing governance-tool demand across the continent. Multinationals headquartered elsewhere yet active in the United States must still report, extending influence beyond borders. Canada advances parallel frameworks through Bill C-27’s Consumer Privacy Protection Act, while Mexico’s data-localization proposals are prompting hybrid-cloud blueprints for cross-border maquiladora supply chains. The region’s investment focus has pivoted from initial ingestion capabilities to advanced observability and automated remediation that reduce operational toil.

Asia-Pacific is the fastest climber, expanding 16.98% annually as public-cloud growth surpasses other regions. China’s 83% GenAI adoption manifests in aggressive pipeline modernization, while South Korea and Japan allocate national AI funds to health-record digitization and smart-factory programs. Vietnam’s Data Law and India’s DPDP Rules trigger data-residency layers within multinational stacks, increasing on-prem edge deployments and stimulating demand for integrated policy engines. Australian enterprises face new Critical Infrastructure Security obligations that require real-time anomaly detection in upstream data-prep stages. Meanwhile, Singapore’s IMDA grants push SMEs to cloud services, reinforcing the region’s mass-market momentum.

Europe posts steady mid-teens growth as ESG mandates drive “report-ready” pipeline investments. The EU Corporate Sustainability Reporting Directive forces roughly 50,000 firms to log greenhouse-gas metrics using consistent taxonomies, elevating data catalog and quality tooling to the executive agenda. Germany and France lead spend, though momentum accelerates in Italy and Spain as Recovery and Resilience Facility grants underwrite digital-transition projects. The EU AI Act requires transparency, bias monitoring and human-oversight logs, deepening the need for secure lineage archives that span edge nodes and hyperscaler zones. Eastern European states ramp local-cloud capacity to keep citizen data domestic, encouraging partnerships between regional telcos and global hyperscalers.

Value Chain Analysis

The data preparation value chain begins with upstream data sources, including enterprise apps such as ERP/CRM, operational databases, IoT/telemetry, logs, documents, and third-party datasets, plus the infrastructure that stores and processes them, such as on-prem data platforms and cloud warehouses and lakehouse storage. Data ingestion and connectivity form the first execution chokepoint, where managed connectors, API governance, and change-data-capture patterns shape how quickly teams can onboard new sources and keep pipelines stable. Recent platform moves toward larger connector libraries, for example Databricks Lakeflow Connect expanding to 100+ native managed connectors in June 2026, point to sustained demand to reduce brittle third-party integration and ongoing maintenance overhead.

Midstream stages cover profiling, cleansing, transformation, enrichment, and metadata capture, including catalog, lineage, and policy, which convert raw data into analysis-ready assets for downstream BI, ML, and GenAI workloads. AI-assisted preparation is increasingly embedded as a horizontal capability across suites, for example Microsoft Research released Data Formulator 0.7 in May 2026 as an open-source, AI-powered approach to streamline transformations and reduce repetitive manual data handling, while governance and quality controls operate as gating functions for regulated use cases. Downstream participants include analytics and visualization tools, ML platforms, data-product marketplaces, and managed service partners that operationalize DataOps practices (versioning, CI/CD, observability) and compliance controls across hybrid and sovereign-cloud footprints, with distribution primarily through SaaS subscriptions, hyperscaler marketplaces, and enterprise license bundles tied to broader data-fabric stacks.

Competitive Landscape

Consolidation is reshaping the vendor map. Salesforce’s USD 8 billion agreement to buy Informatica underscores the pivot toward full-suite fabrics combining ingest, governance, catalog and AI-assisted analytics under one commercial license. The move answers Microsoft and Oracle bundles and locks a broad customer base into Salesforce’s Agentforce platform. Private-equity appetite remains high: Clearlake Capital and Insight Partners took Alteryx private for USD 4.4 billion, accelerating its transition to cloud-native SaaS and GenAI copilots. IBM, Microsoft and Oracle extend footprints with horizontal releases that integrate lineage observability and automated remediation into broader AI studios, while Google Cloud doubles down on BigQuery data preparation.

Disruptors focus on AI-first architectures. Scale AI raised USD 1 billion Series F funding as Meta invested USD 14.3 billion and tapped CEO Alexandr Wang to head a new super-intelligence lab. Claud-native start-ups such as Prophecy emphasize visual pipelines and MIGRATION Copilot that ports legacy ETL code to Spark and Snowpark, appealing to enterprises modernizing mainframe workloads. Vertical specialists emerge: Tamr for life-sciences entity resolution, Precisely for ESG metrics alignment, and One Data for data-product marketplaces.

Competitive intensity heightens around differentiation levers: automated data-quality remediation, embedded privacy-enhancing computation, and domain templates that assure regulators. Price competition remains moderate because buyers prize reduced risk and compliance readiness over lowest cost, though freemium tiers from open-source entrants exert pressure at the lower end of the SME market.

Data Preparation Industry Leaders

Informatica LLC

IBM Corporation

SAS Institute Inc.

Microstrategy Inc.

Tableau Software, LLC (Salesforce.com Inc.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunity is tightening around products that make data preparation directly usable inside AI agent and RAG workflows, particularly when unstructured content such as documents, PDFs, tickets, emails, and call transcripts needs to be transformed into governed, queryable context. IBM framed this workflow explicitly with OpenRAG for watsonx.data in March 2026, and follow-on enhancements that add risk assessment and privacy management capabilities through StoredIQ InstaScan within Cloud Pak for Data in June 2026. Together, these releases suggest buyer pull for packaged, compliant preparation steps rather than bespoke scripts.

A second area of whitespace is headless, in-situ data preparation and governance that plugs into enterprise AI tooling without forcing data movement or a single front-end UI. Informatica highlighted this in May 2026 with headless data management for AWS, and it also deepened collaboration with Microsoft to make Model Context Protocol servers available within Microsoft Foundry. As organizations standardize on lakehouse patterns and open table formats such as Apache Iceberg and Delta Lake across hybrid environments, vendors that provide portable metadata, lineage, and policy controls across these runtimes have room to expand, especially where localization and audit needs push buyers to keep sensitive datasets in-country while still enabling self-service preparation and governed sharing.

Recent Industry Developments

- June 2026: IBM announced enhancements to Cloud Pak for Data that incorporate StoredIQ InstaScan capabilities for rapid risk assessment and data privacy management. The update improves how enterprises scan, classify, and prepare sensitive datasets before sharing or AI use, tightening the linkage between data preparation and compliance workflows.

- May 2026: Informatica introduced headless data management for AWS and expanded its agent-oriented capabilities by making Model Context Protocol servers and CLAIRE Agent skills available through AWS AI surfaces such as the AWS Agent Registry. This move connects data preparation, governance, and quality functions with emerging AI agent architectures where data stays in place across cloud services.

- May 2024: Clearlake Capital and Insight Partners completed the USD 4.4 billion take-private of Alteryx. The transaction supported a faster shift toward cloud-native delivery and accelerated product iteration around automation and AI-assisted data preparation features.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The data preparation market is counted as the revenue earned from software and related subscriptions used to ingest, profile, clean, transform, and publish data so it can be used for analytics, dashboards, and machine learning.

Scope exclusions: We exclude pure-play data integration runtimes, ETL appliances, and one-off professional services work that ends as custom scripting.

Segmentation Overview

- By Deployment

- On-premises

- Cloud

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Solution Type

- Data Ingestion

- Data Cataloging

- Data Quality

- Data Governance

- Data Wrangling

- Data Enrichment

- By End-user Vertical

- BFSI

- Healthcare and Life Sciences

- Retail and e-Commerce

- Manufacturing and Industrial

- IT and Telecommunications

- Government and Public Sector

- Others (Energy, Education, Media)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries and create the first set of demand and supply signals before the model was built. We relied on public sources such as the US Bureau of Labor Statistics, the US Census Bureau, Eurostat, OECD digital economy datasets, and World Bank ICT indicators to understand digital spend direction and hiring intensity around data roles.

To connect those macro indicators to this market, we reviewed SEC filings and annual reports, investor presentations, product documentation on company websites, and reputable press coverage of platform updates and acquisitions. When needed, we used paid subscriptions for company financials and intelligence, news and financials, and patent databases to cross-check product positioning and revenue reporting patterns. These examples are not exhaustive, and we also referenced other public and paid sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were run with software providers, cloud and channel partners, system integrators, and buyer-side data leaders who manage analytics and governance programs. We used these inputs to confirm which offerings get purchased as data preparation versus adjacent tools, validate typical pricing movements, and pressure-test adoption by industry and region before the demand totals were finalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 46% |

| Mid tier: 54% | Functional/Unit leaders: 34% | EMEA: 30% |

| Smaller Players: 15% | Managers: 53% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where enterprise software and data management spend is filtered into a data-prep demand pool using adoption signals and usage intensity. Once that structure is in place, we use selective bottom-up approximations, such as sampled vendor revenues, channel checks on subscription bundles, and an ASP x active-user style logic. We then adjust totals only where the gap is explainable.

Key model inputs include cloud migration pace for analytics stacks, growth in data volumes and the share of semi-structured data, governance and compliance program rollout, the shift from IT-led to self-service data workflows, and typical subscription pricing behavior (including packaging changes across seats, capacity, and feature tiers). Forecasts rely on scenario analysis supported by expert views on AI-assisted preparation features, budget cycles, and the pace of consolidation activity. Where bottom-up evidence is incomplete, we use conservative penetration assumptions and recheck them against hiring, software budget indicators, and provider revenue mix disclosures.

Data Validation & Update Cycle

Checks are applied at multiple points so the final number aligns with real-world signals. We compare outputs against independent indicators such as software spending direction, provider revenue mix commentary, and regional cloud adoption patterns, then investigate any large variances before sign-off.

If an outlier is found, we revisit assumptions, and when needed we trigger interview follow-ups to confirm whether a scope item was misclassified or a pricing change was temporary. Reports are refreshed annually, with interim updates when major events materially shift demand or supply. Before delivery, we run a final analyst pass so the view reflects the latest public information and the most recent validated assumptions.

Mordor Intelligence's Data Preparation Market Sizing Compared With Other Published Estimates

It is common to see different market values published for data preparation, even when the topic name sounds the same. The gaps usually come from how each study draws the line between data preparation and nearby software categories, plus differences in the year used, currency timing, and how subscriptions are treated.

Some publishers combine data preparation with broader ETL, data integration, or professional services revenue, while others focus only on tools and recurring subscriptions. The spread can also be driven by how bundles are handled, whether cloud and on-prem pricing are normalized, and whether forecasts assume aggressive adoption of AI-assisted features or a more gradual buyer ramp. By keeping professional services out and counting platform revenue only when the primary job is profiling, cleansing, and transforming data for downstream analytics, the 2025 total lands at USD 6.95 B under the scope used by Mordor Intelligence.

Across the 2025 comparison, the differences are largely explainable by scope rules and timing, rather than a change in underlying demand signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.95 B (2025) | |

| Global Consultancy A | USD 7.01 B (2024) | Uses a tools-only view with a 2024 base year, and the scope description does not clarify exclusions for integration runtimes or bundled adjacent modules, which can shift totals depending on vendor packaging. |

| Industry Publisher B | USD 6.50 B (2024) | Uses a 2024 base year and provides limited detail on what is included beyond broad deployment and enterprise segments, which can undercount subscription expansions tied to governance-centric and AI-assisted prep features. |

Taken together, the comparison mainly shows that year choice and scope rules create most of the variance, not a disagreement about demand direction. Our approach stays traceable because each assumption is tied back to adoption signals, pricing logic, and interview validation, which makes the final market value easier to reproduce and update.

Key Questions Answered in the Report

What is the current size of the data preparation market?

The data preparation market is valued at USD 8.05 billion in 2026.

How fast is the data preparation market expected to grow?

Revenue is forecast to rise at a 15.92% CAGR, reaching USD 16.84 billion by 2031.

Which deployment model is expanding fastest?

Cloud-based deployments are scaling at 17.12% CAGR, driven by SME adoption and AI workload elasticity.

Why are data governance tools gaining momentum?

Global sustainability and AI regulations require transparent lineage, quality and ESG reporting, pushing governance modules to a 16.74% CAGR.

Which region will post the strongest growth?

Asia-Pacific is projected to lead with a 16.98% CAGR, supported by digital-transformation programs and sovereign-cloud investments.

How are mergers and acquisitions shaping competition?

Large suites are forming through deals such as Salesforce-Informatica and the Alteryx take-private, consolidating ingest, catalog and governance under unified platforms.

Page last updated on: