Market Overview

| Study Period | 2020 - 2031 |

|---|---|

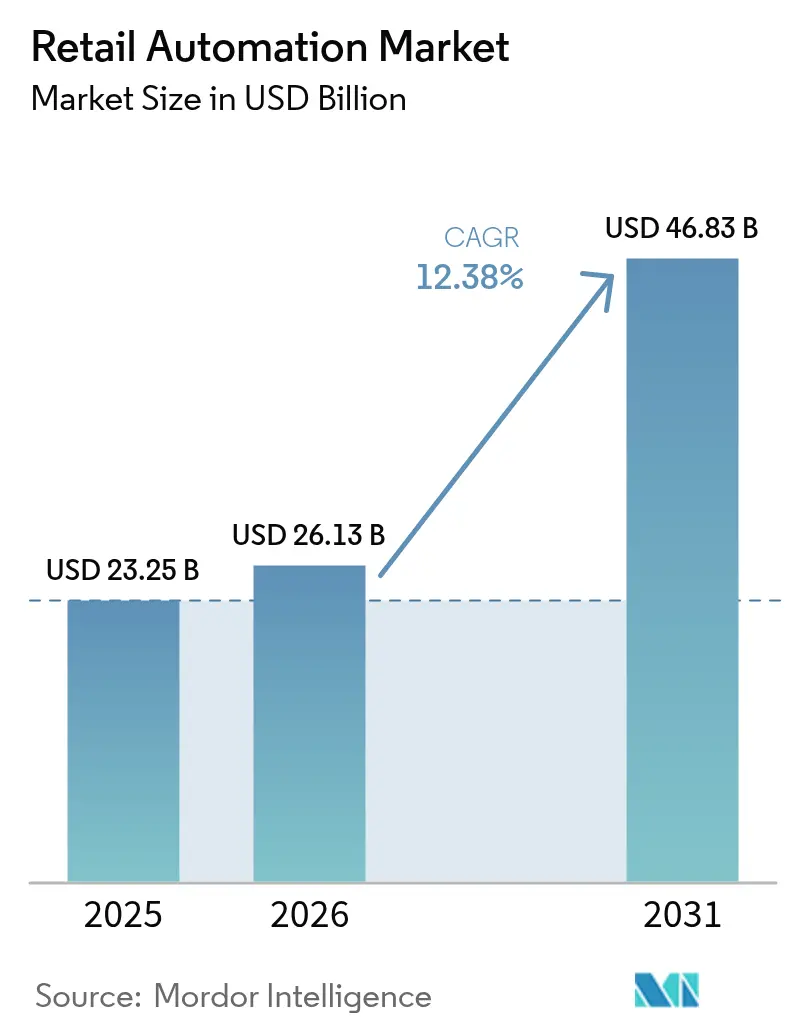

| Market Size (2026) | USD 26.13 Billion |

| Market Size (2031) | USD 46.83 Billion |

| Growth Rate (2026 - 2031) | 12.38% CAGR |

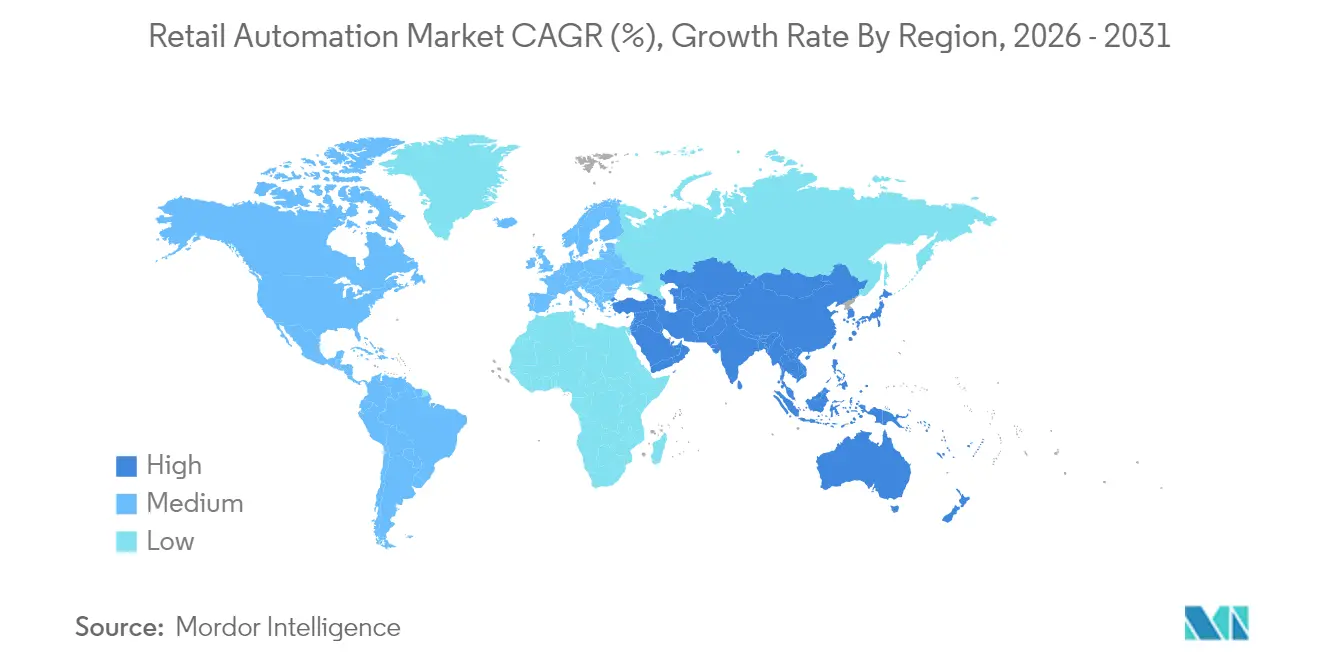

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Retail Automation Market Analysis by Mordor Intelligence

The retail automation market size is expected to grow from USD 23.25 billion in 2025 to USD 26.13 billion in 2026 and is forecast to reach USD 46.83 billion by 2031 at 12.38% CAGR over 2026-2031. Rapid adoption is being driven by retailers seeking higher operating efficiency, lower labor exposure, and seamless customer journeys. Front-of-house technologies such as self-checkout[1]Star Micronics, “Consumer Attitudes Toward Self-Checkout,” starmicronics.com and digital kiosks are expanding quickly, while edge-AI chips are opening new locations where limited connectivity once held back upgrades. Hardware continues to account for most current spending, yet cloud software and managed services are expanding faster as retailers favor subscription models that reduce capital outlay. Intensifying competition from e-commerce platforms is also pushing brick-and-mortar operators to automate order picking and last-mile fulfillment, creating fresh demand for micro-fulfillment centers, robotics, and real-time inventory systems.

Key Report Takeaways

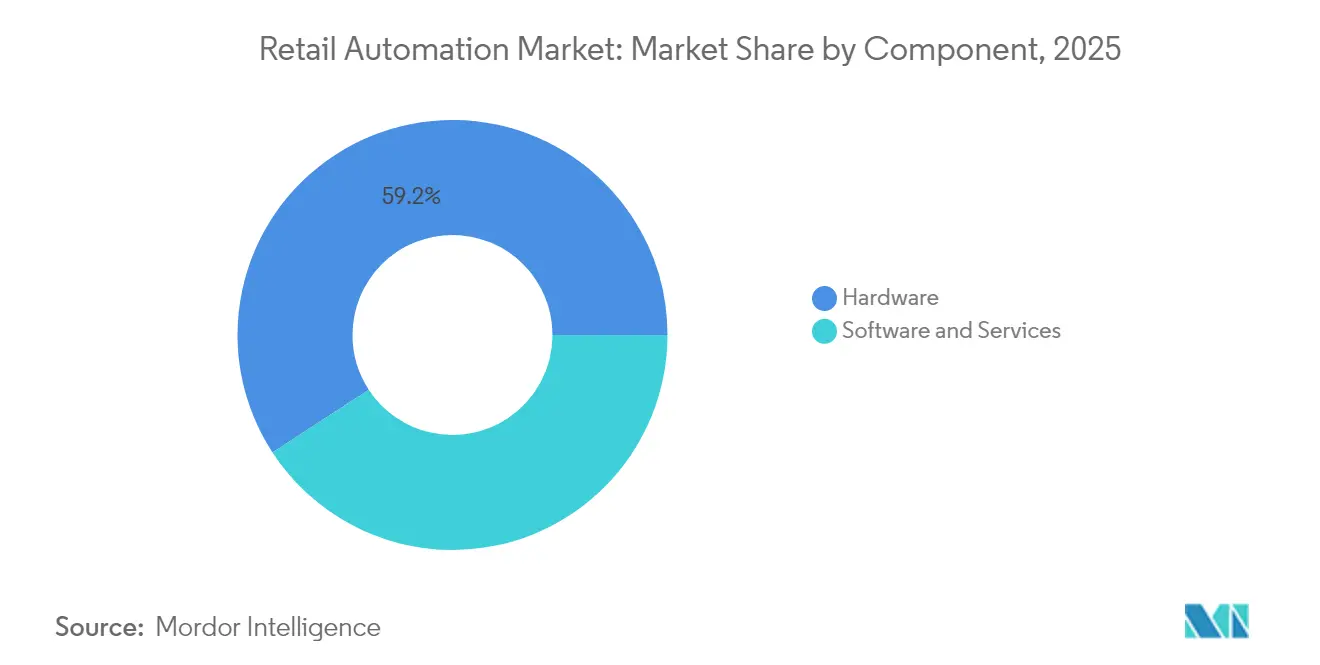

- By component, hardware commanded 59.20% of retail automation market share in 2025, while software and services are projected to expand at a 13.28% CAGR through 2031.

- By implementation, in-store front-of-house systems led with 57.35% of the retail automation market size in 2025; omnichannel fulfillment centers are advancing at 13.62% CAGR to 2031.

- By end-user, grocery retailers held 48.10% retail automation market share in 2025; the hospitality segment is forecast to grow at 13.31% CAGR.

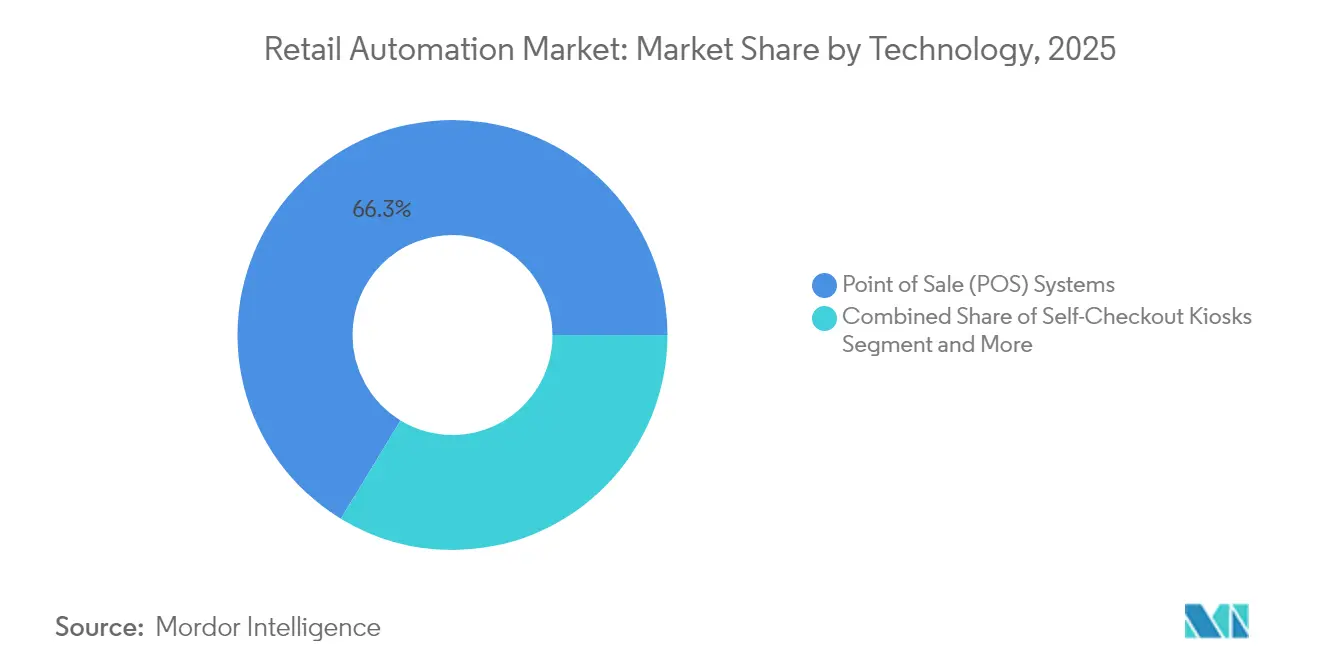

- By technology, POS systems dominated with 66.30% revenue share in 2025, while self-checkout kiosks are projected to rise at 13.73% CAGR.

- By store format, supermarkets accounted for 65.20% of the retail automation market size in 2025 and are expected to expand at 12.98% CAGR.

- By geography, North America led with 34.60% revenue share in 2025; Asia-Pacific is the fastest growing region at a projected 13.72% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Retail Automation Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for quality and fast service | +3.2% | North America, Europe, global urban hubs | Short term (≤ 2 years) |

| Growth and competition among retail and e-commerce players | +2.8% | Asia-Pacific, global tier-one cities | Medium term (2-4 years) |

| Labor shortages and wage inflation accelerating self-checkout adoption | +2.3% | North America, Europe, Australia, New Zealand | Medium term (2-4 years) |

| Retail-media monetization driving POS data integration | +1.9% | North America, Europe, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for quality and fast service

Shoppers increasingly value speed and accuracy over ancillary store attributes. Retailers upgrading to AI-driven checkout lanes report around 40% shorter transactions, which improves throughput at peak periods. Smaller chains are turning to modular POS bundles that scale in line with footfall. This modularity lowers barriers to entry, letting independents match service levels offered by national retailers. Higher satisfaction is turning into measurable loyalty gains, making store-wide automation a tactical priority for the next two years. The retail automation market is therefore experiencing sharper adoption cycles whenever customer wait times rise.

Growth and competition among retail and e-commerce players

Traditional stores face aggressive online rivals offering near-instant delivery and personalised promotions. Omnichannel commerce platforms that blend online and in-store inventory are becoming strategic. POS terminals are evolving into unified commerce hubs that process orders originating from websites, apps, or in-aisle QR codes. Retailers launching third-party marketplaces are creating new automation use cases, such as automated seller onboarding and fee reconciliation. Conversely, digital-first brands opening physical showrooms are deploying smart shelving and RFID to maintain the real-time stock accuracy they are accustomed to online. These intersecting models widen the addressable base of the retail automation market.

Labor shortages and wage inflation accelerating self-checkout adoption

Retail wages continue to climb faster than headline inflation, prompting chains to re-engineer staffing[2]Michele Dupré, “2025 Retail Trends Report,” Verizon, verizon.com. One attendant can now supervise four to six self-checkout stations, cutting front-end labor hours by up to 30%. Savings are redirected to service roles such as aisle advice and online order picking. This redeployment is changing staff skill requirements without eliminating headcount outright. The retail automation industry is responding with designs that feature predictive maintenance, antimicrobial screens, and ergonomic layouts that minimise compliance training.

Retail-media monetization driving POS data integration

In-store traffic is turning into a high-margin advertising asset. Retail media networks use live basket data to serve targeted promotions on kiosks, apps, and electronic shelf labels. Media revenue, often worth 5-7% of digital sales, is helping finance further automation, creating a self-reinforcing investment loop. Vendors are embedding ad-tech APIs into next-generation POS software so that inventory, pricing, loyalty, and advert serving operate on a single data layer. As a result, the retail automation market sees rising demand for analytics engines capable of billions of real-time impressions each year.

Restraints Impact Analysis of Retail Automation Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High hardware failure rates | -1.9% | Emerging markets, harsh environments | Short term (≤ 2 years) |

| Rising self-checkout fraud forcing rollout pauses | -1.3% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High hardware failure rates

Retail equipment often runs near-continuously in temperature-fluctuating, dust-heavy settings, leading to component fatigue. Self-checkout scanners exhibit higher downtime than staffed lanes, causing queue abandonment and service desk bottlenecks. Each outage minute can cost a high-volume supermarket thousands in missed revenue and brand erosion. Manufacturers are embedding ruggedised sensors and remote diagnostics, yet the problem remains acute in emerging markets lacking spare-part supply chains. These reliability issues dampen short-term ordering cycles and influence the retail automation market toward service-level-agreement contracts that shift maintenance risk to suppliers.

Rising self-checkout fraud forcing rollout pauses

Expanded self-service invites new types of shrinkage, from barcode switching to walk-aways. Incidents have risen sharply since 2019, prompting several large chains to slow planned installations while they evaluate AI vision, weight verification, and ID scanning add-ons. Shrinkage at self-checkout can reach 7% of sales compared with 0.3% for staffed lanes, eroding the labor savings that justified investment. Solution providers are integrating computer vision, edge-AI inference, and real-time intervention alerts. Until accuracy is proven, some retailers will cap self-service penetration, tempering near-term revenue growth for the retail automation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Retail Automation Market Segment Analysis

By Component:

Software Services Outpace Hardware GrowthHardware accounted for 59.20% of 2025 revenue as retailers installed POS devices, kiosks, and RFID gateways. However, software and services are forecast to outgrow hardware at 13.28% CAGR to 2031. The retail automation market size for software subscriptions is expanding as cloud deployment enables continuous feature updates rather than episodic hardware refreshes. Open-API hardware designs now let third-party developers plug in analytics, loyalty engines, and payment wallets, blurring traditional component lines.

Greater focus on data-driven operations is benefiting SaaS providers offering AI-powered forecasting and loss prevention. Managed service contracts bundle uptime guarantees, security patches, and predictive maintenance, shifting spending from capital to operating budgets. As retailers rationalise physical footprints, modular fixtures linked to cloud orchestration supply flexibility. Consequently, solution vendors that pair rugged hardware with scalable platforms are gaining share.

By End-User:

Grocery Dominance Amid Hospitality SurgeGrocery chains held 48.10% of 2025 revenue owing to high basket churn and thin margins that demand process efficiency. Micro-fulfillment systems, electronic shelf labels, and smart scales are central to this group’s automation roadmap. The retail automation market share of grocery is expected to remain significant, yet hospitality operators are posting the fastest gains at 13.31% CAGR. Quick-service restaurants are adding ordering kiosks, kitchen display systems, and robotic food prep to tackle wage pressure and speed expectations.

Hotels are deploying mobile check-in, digital keys, and service robots that deliver linens or room service trays, illustrating cross-sector technology spill-over. While general merchandise and specialty sectors automate inventory visibility, their growth pace is moderate relative to grocery and hospitality. Vendors tailoring solutions to sector-specific workflows will capture incremental opportunities as use cases broaden.

By Implementation:

Omnichannel Fulfillment Centers AccelerateCustomer-facing installations, such as self-checkout, held a 57.35% share in 2025 because they directly address queue times and upsell. Yet omnichannel fulfillment centers are the fastest-growing implementation, projected at 13.62% CAGR. The retail automation market size linked to micro-fulfillment is climbing as retailers convert back-of-store zones into automated pick stations that process online orders in under 30 minutes.

This reallocation of space reduces last-mile costs and supports same-day delivery pledges. Warehouses and back-store areas continue to adopt AMRs, automated sorters, and RFID portals, but growth lags behind front-of-house upgrades. Retailers integrating demand forecasting, order routing, and labor scheduling across all three zones report double-digit efficiency gains, reinforcing unified investment cycles.

By Technology:

Self-Checkout Kiosks Gain MomentumPOS platforms remained the bedrock with 66.30% revenue share in 2025, acting as the transactional system of record. Still, self-checkout kiosks are expanding at a 13.73% CAGR as shoppers value control and speed. Computer vision cameras and AI object recognition now cut mis-scans, while voice guidance improves accessibility. The retail automation market embraces RFID, barcode, and vision sensors to achieve item-level accuracy in mixed baskets.

Robotics and AMRs, though a smaller slice, are posting double-digit growth as costs fall and use cases mature. Brain Corp reports that store-friendly AMRs run 10 hours per charge and slot into existing cleaning or inventory routines, avoiding the ceiling-height constraints of drones. Over time, multi-sensor architectures linking kiosks, mobile apps, and shelf scanners will deliver end-to-end visibility from stockroom to checkout.

By Store Format:

Supermarkets Lead Automation AdoptionSupermarkets controlled 65.20% of 2025 spending and are projected to grow at 12.98% CAGR to 2031. High SKU volumes and perishables require granular inventory control. Smart shelves alert staff to out-of-stocks, while computer vision validates produce identification. The retail automation market size in the supermarket segment is set to widen as chains invest in voice-assisted navigation and augmented reality promotions that shorten trip time.

Hypermarkets pursue similar tools across larger footprints, emphasizing autonomous floor scrubbers and mobile picking carts. Convenience and fuel retailers focus on 24/7 unattended formats using computer-vision checkout and smart lockers. Department stores, with lower footfall frequency, allocate funds to interactive fitting mirrors and endless-aisle kiosks that integrate with e-commerce catalogs. Each format demands distinct user interfaces and device durability, steering solution design diversity.

Geography Analysis

North America Retail Automation Market

North America contributed 34.60% of 2025 revenue. High wages, early adoption culture, and strong vendor ecosystems underpinned leadership. Retailers are piloting computer-vision POS lanes expected to proliferate by 2026. Edge-AI processing inside scanners reduces latency and lessens reliance on data centers. Privacy regulations and shrinkage concerns temper unrestrained rollouts, but innovation pipelines remain healthy.

APAC Retail Automation Market

Asia-Pacific is the fastest-growing region at a 13.72% projected CAGR. China pioneers mobile wallet-only stores and robotic micro-warehouses, while India’s e-commerce surge fuels warehouse automation demand. Autonomous mobile robot penetration in regional facilities is forecast to climb from 27% to 92% within five years, underscoring the appetite for labor-saving devices. Rural expansion benefits from edge-AI chips that work in low-bandwidth sites, enlarging the retail automation market reach.

EMEA and South America Retail Automation Market

Europe holds a significant share, led by Western economies investing in energy-efficient systems and circular packaging. Eastern markets are catching up as wages rise and cross-border chains modernize. Strict data-protection rules shape computer-vision deployments, pushing vendors to implement on-device anonymization. South America and the Middle East, and Africa, though smaller today, exhibit strong long-term potential. Brazil’s reforming tax environment encourages cash-to-digital migration, while Gulf states fund smart-city retail projects that bundle logistics automation and contactless payment infrastructure.

Regulatory Landscape

Retail automation deployments are increasingly shaped by overlapping rules on AI transparency, transaction integrity, and labor impacts. In the European Union, the EU AI Act (Regulation (EU) 2024/1689) introduces a risk-based compliance framework for AI systems used in retail contexts, including disclosure obligations under Article 50 for certain AI interactions effective February 2, 2025, and documentation expectations referenced through EU AI Act technical requirements (including Annex IV documentation elements). These provisions affect computer-vision checkout, conversational assistants in kiosks, and analytics used for in-store decisioning.

In the United States and the United Kingdom, requirements are more fragmented but still affect store systems and POS governance. The UK government advanced measures in 2025 to address Electronic Sales Suppression in EPOS systems, emphasizing unalterable transaction logs and certification-oriented controls that increase compliance demands on POS software providers and integrators. In the US, state-level initiatives such as California SB-1446 introduce advance notice and workforce engagement obligations before implementing consequential workplace technology, while Rhode Island enacted staffing requirements tied to self-checkout lanes with an effective date of January 1, 2027. For retailers participating in SNAP, USDA Food and Nutrition Service guidance and 7 CFR 274.3 reinforce certification and approval expectations for automation that touches EBT processing and related interfaces, pushing vendors toward auditable workflows, privacy controls, and bias-aware design where AI is used in customer or eligibility-adjacent processes.

Value Chain Analysis

The retail automation value chain begins with component suppliers (scanners, cameras, RFID/barcode modules, edge compute, and payment peripherals) that feed OEMs and platform vendors packaging POS, kiosks, electronic shelf labels, and robotics into deployable store and fulfillment solutions. System integrators and managed service providers then run site surveys, address network readiness, manage device enrollment, apply cybersecurity hardening, and maintain ongoing uptime commitments, which matters given 24/7 store operations and the market shift toward subscription software and service bundles. Hardware still represents most current spending (59.20% share in 2025), but deployment economics increasingly reflect software layers such as loss-prevention analytics, orchestration, and remote monitoring.

Downstream, retailers and wholesalers operationalize automation across front-of-house checkout, back-store inventory workflows, and omnichannel fulfillment nodes, with data pipelines linking transactions, shelf availability, and picking execution. Recent partnerships and scale programs also show vendors tightening integration across the chain: Carrefour and Vusion expanded smart-store deployments in France (connected shelf labels and in-store intelligence), while Walmart Mexico expanded rollout of Vusion EdgeSense across formats, reflecting demand for store-level data capture to support inventory accuracy and labor scheduling. In distribution and micro-fulfillment, Associated Wholesale Grocers selected Symbotic for high-density end-to-end automation at its Gulf Coast Division Support Center. Retailers are also exploring new robot form factors, including Catalyst Brands partnering with Figure AI to deploy humanoid robotics for sorting and packing at a Reno, Nevada facility, and Colruyt Group with KION launching an R&D center for next-generation supply chain robotics, reinforcing the feedback loop between deployment and product design.

Competitive Landscape

The top five providers hold just above 30% of global revenue, indicating moderate concentration. NCR Corporation, Diebold Nixdorf, Zebra Technologies, Honeywell International, and Toshiba Global Commerce Solutions differentiate through broad portfolios and global service networks. NCR Voyix is moving production of self-checkout hardware to Ennoconn, freeing capital for its cloud platform, a sign that suppliers are prioritizing software valuation over fabrication scale[3]NCR Voyix Corporation, “Form 8-K: Manufacturing Outsourcing Agreement,” sec.gov.

Hardware specialists are partnering with AI software start-ups to embed analytics at the edge. Zebra’s Aurora suite links vision-guided robotics with AMRs, reflecting demand for single-vendor stacks that cut integration time. Acquisitions target robotics orchestration, predictive maintenance, and computer vision. Regional integrators compete on deployment speed and local regulations, fragmenting share beneath the global top tier.

Retailers prefer vendors able to supply end-to-end coverage spanning checkout, inventory, and fulfillment. This creates pressure on niche providers to align with ecosystems or specialise further. White-space opportunities remain in emerging markets where legacy infrastructure is thin. As edge-AI chips and 5G mature, late-adopting regions could leapfrog to advanced architectures, resetting competitive positioning in the retail automation market.

Retail Automation Industry Leaders

Datalogic S.P.A

Diebold Nixdorf, Incorporated

ECR Software Corporation

Emarsys eMarketing Systems AG

Fiserv Inc.

- *Disclaimer: Major Players sorted in no particular order

Retail Automation Market Companies Covered in this Report

- Datalogic S.p.A

- Diebold Nixdorf Inc.

- NCR Corporation

- Honeywell International Inc.

- Toshiba Tec Corp.

- Fujitsu Ltd.

- Zebra Technologies Corp.

- Posiflex Technology Inc.

- RapidPricer B.V.

- Fiserv Inc.

- Oracle Corp. (Retail Solutions)

- SAP SE (Retail Automation)

- ECR Software Corp.

- Emarsys (SAP subsidiary)

- SES-imagotag SA

- Pricer AB

- Avery Dennison Corp. (RFID)

- Checkpoint Systems Inc.

- PTC Inc. (Retail AR/IoT)

- KUKA AG (Retail Robotics)

Market Opportunities and Future Outlook

Opportunity is expanding where retailers can convert in-store and fulfillment automation into a unified execution layer that improves inventory accuracy, reduces shrink, and supports omnichannel service levels. Shelf digitization and store intelligence are moving from isolated pilots into broader trials, illustrated by Tesco testing Simbe Robotics Tally robots for automated shelf scanning and gap detection in 2026. This points to whitespace for vendors that can connect shelf data with replenishment, pricing, and order-routing systems. At the same time, retailer scrutiny around fraud at self-checkout is driving demand for embedded loss-prevention capabilities, with vendors increasingly placing edge-AI features inside scanners and checkout devices rather than relying on higher-latency cloud processing.

Large capital programs in automated fulfillment and distribution are also widening the addressable deployment base for robotics, orchestration software, and managed services. Amazon announced a USD 750 million investment for a robotics fulfillment center in North Maclean, Queensland, and separately committed more than EUR 10 billion to modernize and expand European robotics and delivery networks, indicating continued build-outs that pull through automation hardware, warehouse control software, and integration services. In Asia, Sheng Siong announced an S$520 million investment in a new distribution center, reinforcing demand for high-throughput automation beyond North America and Western Europe. As retailer IT and operations teams push for interoperable, production-grade automation, programs such as MACH Alliance Agent Ready (with an initial cohort of accredited providers in 2026) offer a practical route for solution selection and integration, creating opportunities for vendors that can demonstrate multi-system compatibility across POS, shelf systems, and fulfillment automation.

Recent Industry Developments in Retail Automation Market

- June 2026: Datalogic launched the Falcon X60/65 ultra-rugged mobile computer for retail and logistics environments. The release expands Datalogic's device portfolio for store and back-of-store workflows where durability and continuous scanning matter, supporting broader automation deployments across inventory, replenishment, and picking processes.

- May 2025: Zebra Technologies unveiled the Aurora VGR Assistant and Zebra Symmetry Fulfillment to link vision-guided robots with AMRs for retail picking workflows. The launch strengthens end-to-end orchestration across fulfillment tasks, addressing retailer demand for integrated robotics stacks that reduce integration time across omnichannel operations.

- March 2024: Diebold Nixdorf introduced Vynamic Connection Points 7, the next generation of its multivendor self-service software. The update reinforces multivendor interoperability and centralized management, helping large operators standardize monitoring, security updates, and service performance across diverse self-service endpoints.

Retail Automation Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers spending on retail automation solutions that reduce manual effort across store and retail backroom workflows, including hardware, software, and related services used to run daily retail operations.

Scope exclusions: We exclude pure e-commerce platform fees, generic marketing automation tools, and non-retail material handling equipment.

Segments Covered in This Report

- By Component

- Hardware

- Software and Services

- By End-User

- Grocery

- General Merchandise

- Hospitality

- By Implementation

- In-store Front-of-house

- Back-store / Warehouse

- Omnichannel Fulfilment / Micro-fulfilment Centers

- By Technology

- Point of Sale (POS) Systems

- Self-Checkout Kiosks

- Radio-Frequency Identification (RFID)/Barcode

- Robotics/Autonomous Mobile Robots (AMR)

- By Store Format

- Supermarkets

- Hypermarkets

- Convenience/Fuel

- Department Stores

- By Geography

- North America

- United States

- Canada

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market structure and to anchor the model to measurable retail activity. We relied on public sources such as US Census Bureau retail trade releases, Bureau of Labor Statistics wage and productivity series, Eurostat retail and labor datasets, World Bank macro indicators, and OECD digital economy and productivity metrics.

We also reviewed company annual reports, investor presentations, product brochures, and retailer announcements to understand rollout patterns for self-checkout, RFID, electronic shelf labels, and store analytics. In a few places, we used paid subscriptions for company financials and intelligence, patent lookups, and shipment-level trade signals to cross-check import intensity for key hardware categories. The sources listed here are illustrative only, and many other public documents and datasets were also used to collect, verify, and clarify inputs.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with retailers, system integrators, automation solution providers, and component makers, so assumptions could be tested where public data is thin. Respondent input helped clarify how rollout pace differs by store format and how software subscription mix changes during replacements. We covered demand conditions across APAC, EMEA, and the Americas, and we revisited key questions when adoption rates or pricing expectations differed by store format and deployment style.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 19% | APAC: 47% |

| Mid tier: 54% | Functional/Unit leaders: 21% | EMEA: 31% |

| Smaller Players: 20% | Managers: 60% | Americas: 22% |

Market-Sizing & Forecasting

The sizing model starts with a top-down build where retail activity and store footprint signals are reconstructed into an addressable demand pool, and then translated into annual spending for automation. To keep the totals realistic, we corroborate the outcome with selective bottom-up approximations using sampled vendor revenues, channel checks, and typical ASP multiplied by rollout volumes for major solution types.

Inputs used in the model include the installed base of retail outlets and distribution points, labor cost pressure and staffing availability, self-checkout penetration trends, RFID and barcode adoption levels, electronic shelf label rollout intensity, and capital spending cycles tied to store refurbishments. When a data point is missing for a country or a smaller store format, we bridge the gap using proxy indicators like organized retail share and comparable deployment rates from similar markets, followed by a check with expert feedback.

For forecasting, scenario analysis is used to reflect different adoption speeds, followed by an exponential smoothing step on pricing and shipment trends so short-term volatility does not distort the path. The final forecast is then aligned to what primary respondents expect on rollout timing, replacement cycles, and software subscription mix shifts.

Data Validation & Update Cycle

Outputs are validated through triangulation across multiple angles, including consistency checks versus retail sales growth, store count movements, and known deployment milestones in major markets. Large variances are flagged and reviewed, and the model is re-run when key assumptions like adoption rates, pricing progression, or service attach rates show inconsistent behavior across regions.

Before sign-off, a second analyst reviews the logic, calculations, and any judgment-based overrides, and follow-up calls are triggered when a number cannot be explained by a clear demand indicator. Reports are refreshed annually, and interim updates are made when material events shift adoption patterns or pricing, with a final pre-delivery review to ensure clients receive the most current view.

Mordor Intelligence's Retail Automation Market Market Size Versus Other Published Estimates

Published market sizes for retail automation can differ even when the topic name looks the same, because each publisher draws the line around what gets counted and which year is treated as the current reference point. Differences also show up when pricing is modeled as one blended average versus being tied to separate hardware, software, and service mix changes.

Pure e-commerce platform fees sit outside Mordor Intelligence's scope, which can reduce totals versus estimates that bundle broader digital commerce software along with in-store and backroom automation spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 26.13 B (2026) | |

| Global Consultancy A | USD 30.51 B (2025) | Uses an earlier current year and a wider technology bucket that can group additional warehouse material-handling systems and adjacent store hardware into one total, which lifts the reported size. |

| Industry Publisher B | USD 28.62 B (2024) | Uses a longer forecast window and a broader definition by component and vertical, and the public summary does not clarify exclusions like e-commerce platform fees or how services are separated from software. |

The spread in values is mostly explained by scope and timing, followed by how mixed bundles are priced and converted into USD for the stated year. By keeping the count tied to measurable retail rollout activity and clearly separated solution buckets, the estimate remains easier to repeat and to pressure-test when adoption assumptions change.

Key Questions Answered in the Report

What is the current value of the retail automation market?

The retail automation market stands at USD 26.13 billion in 2026.

How fast is the market expected to grow through 2031?

The market is projected to expand at a 12.38% CAGR, reaching USD 46.83 billion by 2031.

Which region is growing fastest?

Asia-Pacific is forecast to post a 13.72% CAGR between 2026 and 2031, the highest among all regions.

What technology segment is expanding most quickly?

Self-checkout kiosks are expected to rise at a 13.73% CAGR due to labor pressures and shopper preference for quick transactions.

Which end-user segment leads adoption?

Grocery accounts for 48.10% of 2025 revenue thanks to high transaction volumes and tight margins that favor efficiency gains.

Why are retailers integrating retail media with POS data?

Retail media monetization provides an additional 5-7% of e-commerce sales in high-margin advertising revenue, offsetting automation costs while enhancing targeted promotions.

Page last updated on: