3D CAD Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 12.47 Billion |

| Market Size (2030) | USD 16.25 Billion |

| Growth Rate (2025 - 2030) | 5.45% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

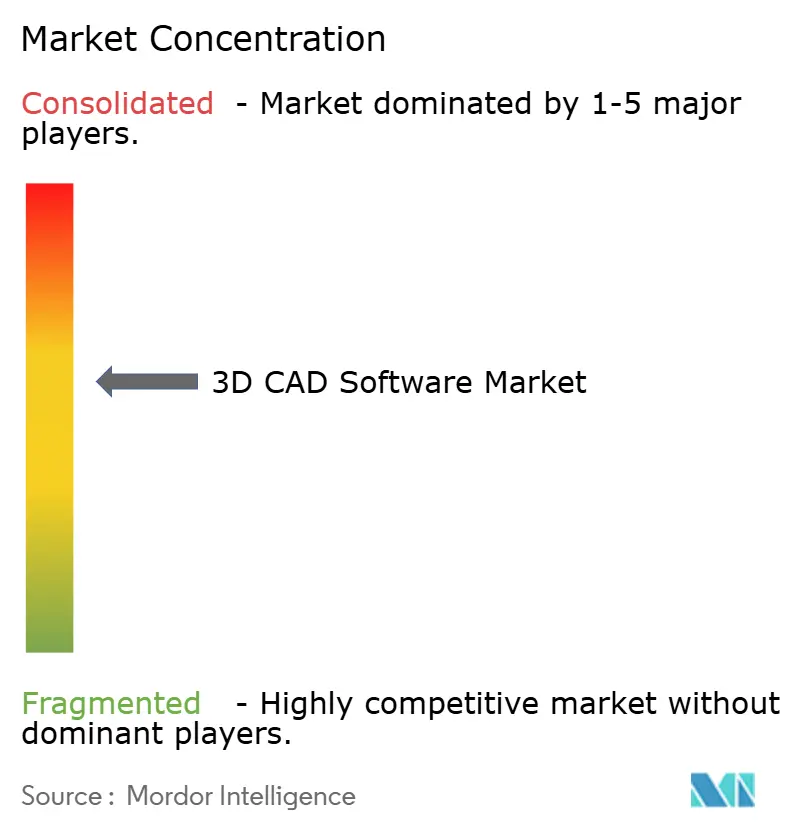

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

3D CAD Software Market Analysis by Mordor Intelligence

The 3D CAD software market size reaches USD 12.47 billion in 2025 and is forecast to climb to USD 16.25 billion by 2030 at a 5.45% CAGR, reinforcing the segment’s steady expansion amid manufacturing digitalization and cloud migration tailwinds. Enterprises are gravitating toward subscription-based, cloud-native platforms to reduce capital outlay, improve collaboration and shorten design-to-manufacture cycles. AI-driven generative workflows, tighter links between CAD and enterprise PLM, and additive-ready modeling tools are reshaping competitive dynamics. Vendors are responding with integrated ecosystems that bundle design, simulation and data-management capabilities, while end users focus on virtual prototyping to curb physical testing costs. Regional growth differentials remain pronounced: North America sustains leadership through early adoption, but Asia-Pacific shows the fastest trajectory as China, Japan and India accelerate factory modernization and workforce upskilling.

Key Report Takeaways

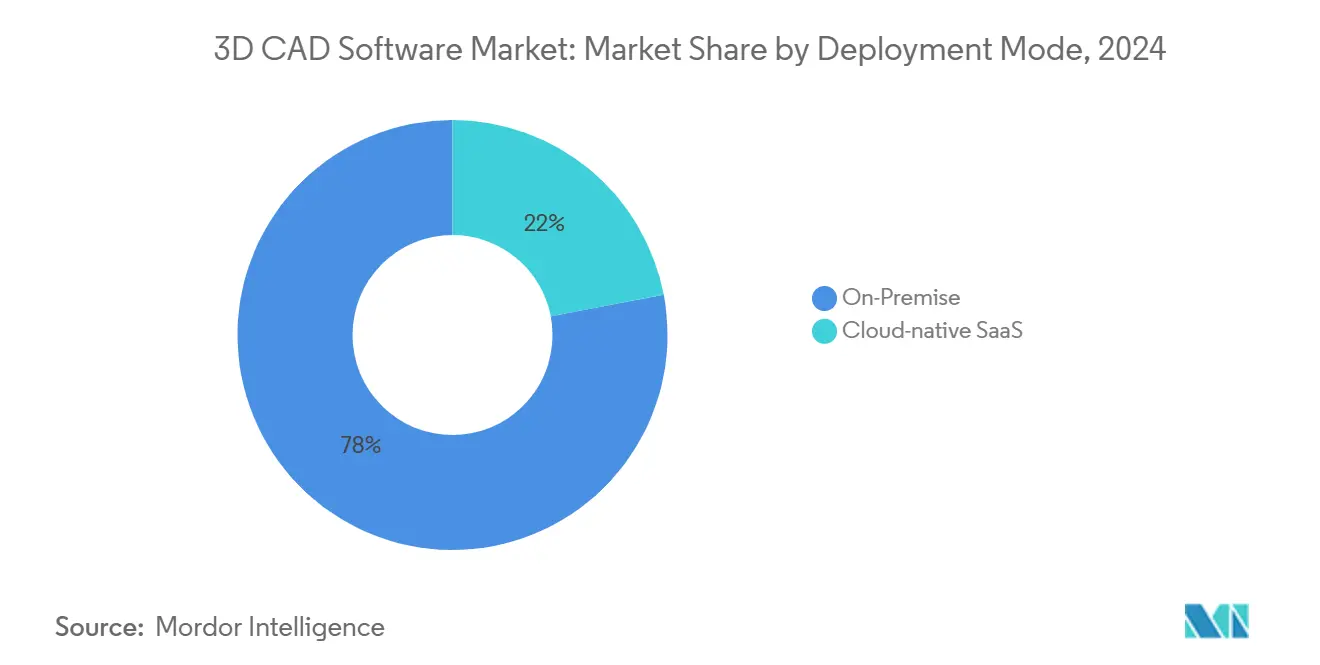

- By deployment mode, on-premises installations held 78.0% of 3D CAD software market share in 2024, whereas cloud-native SaaS deployments are poised to expand at 7.11% CAGR through 2030

- By end-use industry, industrial equipment and machinery led with 27.0% revenue share in 2024; healthcare and medical devices are forecast to post the quickest 6.47% CAGR through 2030

- By application, 3D modeling and drafting accounted for 58.0% of the 3D CAD software market size in 2024, while generative design advanced at a 6.67% CAGR through 2030

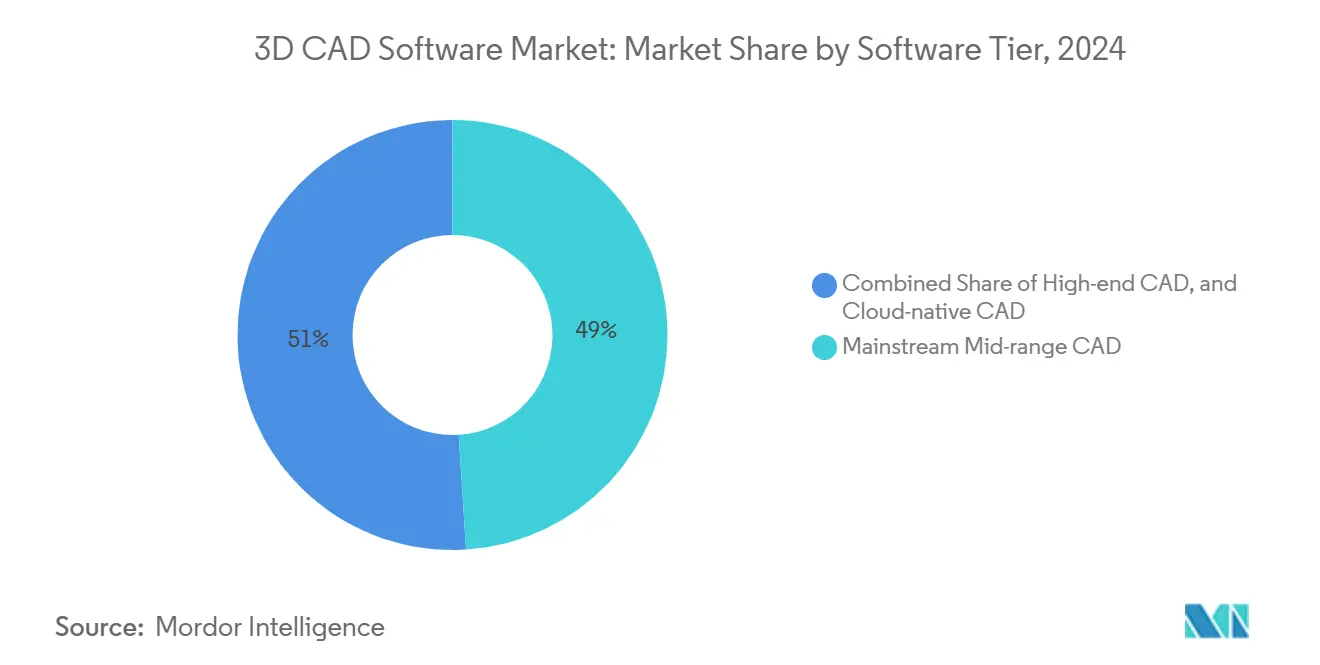

- By software tier, mainstream mid-range CAD captured 49.0% share in 2024; cloud-native CAD is projected to log the highest 7.37% CAGR to 2030

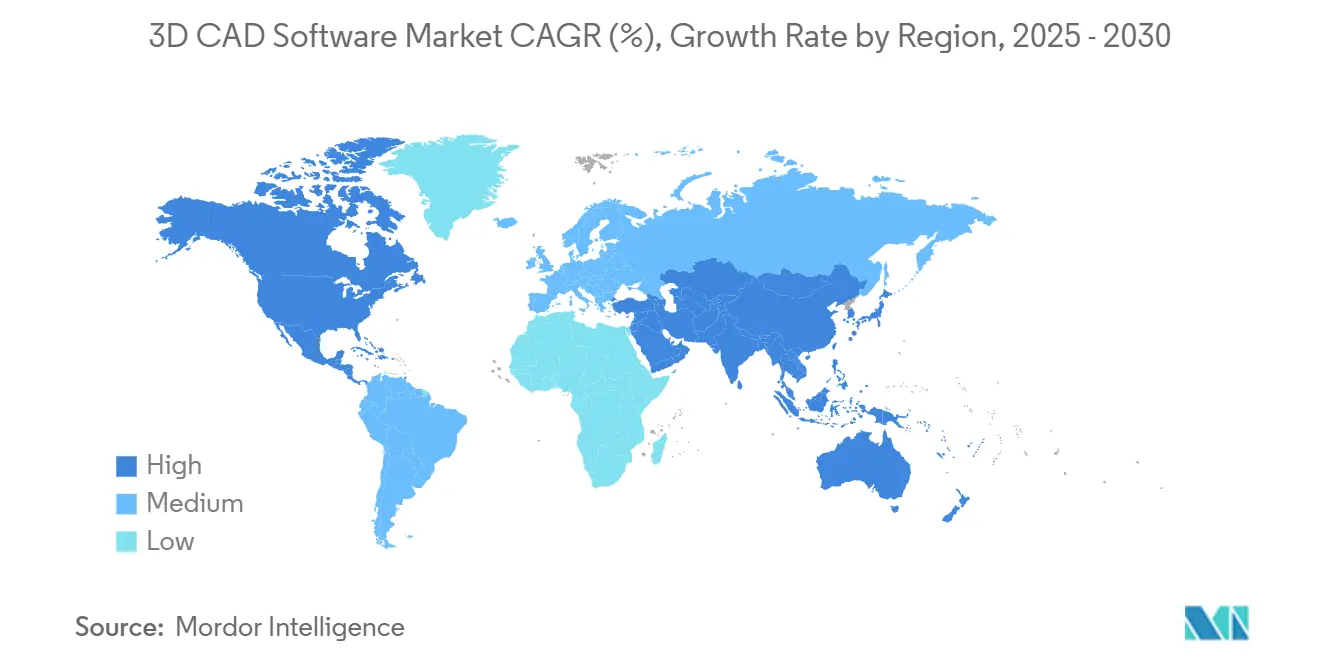

- By geography, North America commanded 32.0% share in 2024, but Asia-Pacific records the fastest 5.82% CAGR through 2030

Global 3D CAD Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising shift to cloud-based CAD subscriptions | +1.2% | Global, with early adoption in North America and European Union | Medium term (2-4 years) |

| Demand for virtual prototyping in additive manufacturing | +0.9% | Asia Pacific core, spill-over to North America | Medium term (2-4 years) |

| Integration of CAD with enterprise PLM digital thread | +0.8% | Global, concentrated in automotive and aerospace hubs | Long term (≥ 4 years) |

| Cost-out initiatives via model-based definition (MBD) | +0.7% | North America and European Union, expanding to Asia Pacific | Medium term (2-4 years) |

| AI-driven generative design in space and defence programs | +0.6% | North America and European Union, selective Asia Pacific markets | Long term (≥ 4 years) |

| Sustainability compliance via virtual-twin verification | +0.5% | European Union leading, North America following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising shift to cloud-based CAD subscriptions

Organizations migrate to cloud-native platforms to eliminate local server upkeep, gain real-time design access and streamline software updates. In September 2024, PTC and AWS demonstrated how browser-based platforms address file-locking challenges and lower ownership costs. CFOs favor predictable operating-expense models that replace large perpetual-license purchases. Adoption momentum is strongest among small and mid-size manufacturers now able to access high-end capabilities without datacenter investment. Security remains a board-level concern, prompting tools such as HALOCAD and Secude’s zero-trust wrappers that safeguard design IP in transit and at rest. Vendor responses include SOC 2 credentials and region-specific data-residency controls that ease compliance in regulated industries.

Demand for virtual prototyping in additive manufacturing

Additive processes move from prototyping to limited-series production, fueling demand for CAD platforms that embed Design-for-Additive-Manufacturing checks. In 2024, surveyed firms increased 3D-printing volumes, citing cycle-time savings and waste reduction. Fusion 360, Creo and SOLIDWORKS now integrate topology optimization and lattice generation that tailor parts to printer envelopes and material behaviors. Healthcare pioneers use these functions to create personalized implants, trimming development time from month to week. Aerospace adopters such as Neural Concept leverage GPU-accelerated solvers to evaluate thousands of lightweight concepts in minutes, replacing iterative physical trials with full-digital validation.

Integration of CAD with enterprise PLM digital thread

Manufacturers extend CAD data into unified PLM backbones to support continuous traceability, version control and downstream analytics. Tesla’s Dassault Systèmes implementation shows how a single source of design truth accelerates change management while preserving regulatory records.[1]WordPress, “Tesla Motors PLM Implementation with Dassault Systèmes,” plmphilosophy483489853.wordpress.com Aras reports 50% year-over-year growth in SaaS PLM deals, indicating rising appetite for cloud delivery that aligns with CAD subscriptions. Integrated platforms connect design to manufacturing execution and IoT feedback loops, enabling closed-loop optimization that underpins Industry 4.0 roadmaps. Regulated sectors gain measurable benefits as PLM ensures end-of-the-end audit trails, design history files and electronic signatures.

AI-driven generative design in space and defense programs

Defense primes and space agencies pilot AI engines that propose weight-optimized components within envelope and load constraints. PhysicsX’s LGM-Aero reduces aircraft concept generation from months to hours, unlocking novel airframe geometries unattainable through manual iteration.[2]PhysicsX, “Introducing LGM-Aero GenAI for Aero Engineering,” physicsx.ai NASA’s adoption of generative models reveals mass savings that translate into mission fuel reductions. The University of Illinois deepSPACE tool can yield hundreds of viable alternatives in a single run while embedding cost metrics for early trade-off analysis. Regulatory scrutiny slows broad rollout, but pilot successes are converting skeptics as validation workflows mature.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ownership of high-end CAD suites | -0.8% | Global, particularly impacting Small Medium Enterprises | Short term (≤ 2 years) |

| Cyber-security concerns around cloud CAD | -0.6% | Global, acute in regulated industries | Medium term (2-4 years) |

| Shortage of power-user CAD talent | -0.5% | Global, severe in Asia Pacific emerging markets | Long term (≥ 4 years) |

| Auto-sector licence renewal slowdown | -0.4% | Global automotive hubs, concentrated in European Union and North America | Short term (≤ 2 years |

| Source: Mordor Intelligence | |||

High total cost of ownership of high-end CAD suites

While subscription pricing improves cash flow, elevated seat rates and mandatory maintenance plans keep lifetime costs high. A Siemens NX license starts near USD 9,000, and SOLIDWORKS Premium subscriptions top USD 3,240 annually.[3]Hawk Ridge Systems, “SOLIDWORKS Buying Guide 2025,” hawkridgesys.com Users also budget for GPU-rich workstations and periodic hardware upgrades every two to six years. These outlays strain SME budgets and prompt evaluation of lower-cost cloud alternatives.

Cyber-security concerns around cloud CAD

Design files represent crown-jewel IP, and breaches can undermine long-term competitiveness. Recent Autodesk advisories on unauthorized account access heightened vigilance.[4]Autodesk, “Security Advisories – User Accounts,” autodesk.com Defense suppliers must comply with CMMC controls that mandate granular encryption and audit logging. Solutions like Onshape bake AES-256 encryption and SOC 2 Type II attestations into their offerings, yet some sectors still require on-premises repositories until assurance frameworks gain further trust.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Migration Accelerates Despite Legacy Dominance

On-premises deployments controlled 78.0% revenue in 2024, buoyed by entrenched file-based workflows and perceived sovereignty benefits. However, the 3D CAD software market is seeing subscription-first buying policies, and the cloud-native cohort is set for a 7.11% CAGR. Large aerospace OEMs maintain local servers for classified programs, yet mid-size suppliers shift toward browser-based platforms that eliminate VPN bottlenecks. Siemens’ NX X cloud licensing showcases full-featured CAD delivered on demand, letting teams spin up or down seats as project loads fluctuate. For many SMEs, cloud CAD’s reduced support burden outweighs concerns, spawning a balanced hybrid landscape likely to persist through the decade.

Over 2025-2030 cloud adoption will add multi-tenant analytics, AI-powered design suggestions and automated compliance checks, closing feature gaps with high-end desktops. Subscription telemetry will help vendors push iterative enhancements without disruptive version jumps. Conversely, organizations bound by ITAR or defense-specific regulations will continue investing in hardened on-premises vaults and air-gapped workstations, ensuring that the 3D CAD software market retains a two-track delivery model through 2030.

By End-Use Industry: Healthcare Innovation Drives Growth Beyond Industrial Leadership

Industrial equipment manufacturers held 27.0% of the 3D CAD software market share in 2024 as complex, high-tolerance machinery relies on parametric modeling for component interchangeability. Yet healthcare and medical devices outpace all peers with a 6.47% CAGR, spurred by personalized implants, surgical planning and fast-track FDA approvals that embrace virtual twins. Aerospace and defense investment in AI-driven optimization tightens the race, while automotive renewals taper amid electrification cost controls.

From 2025 onward, hospitals will create in-house design labs to customize patient-specific guides, widening healthcare’s footprint. Industrial firms will adopt model-based definitions to automate downstream machining, preserving revenue but ceding relative momentum. As additive materials mature for end-use parts, collaboration between medical OEMs and service bureaus will further expand healthcare’s contribution to overall 3D CAD software market size.

By Application: Generative Design Emerges as Growth Catalyst

Traditional 3D modeling and drafting contributed 58.0% of 2024 revenue, anchoring the everyday tasks of assembly creation and detailing. The generative design segment, though nascent, is slated for the highest 6.67% CAGR thanks to maturing machine-learning algorithms that interrogate vast design spaces within minutes. Simulation-integrated modeling increasingly blurs lines: designers validate stress, modal and thermal outcomes inside the CAD window, accelerating sign-off.

Through 2030, cloud compute elasticity will mainstream generative design beyond early aerospace use. Consumer-electronics firms will leverage AI to shave grams and reduce tooling cycles. Simulation and analysis modules, bolstered by GPU-accelerated solvers, will capture higher attach rates as subscription bundles make once-premium capabilities standard. Additive-manufacturing preparation tools—orientation, support-generation and lattice libraries—will convert prototypes into production layouts, rounding out a holistic workflow inside a single pane.

By Software Tier: Cloud-Native Solutions Challenge Traditional Hierarchies

Mainstream mid-range suites controlled 49.0% revenue in 2024 by balancing price and capability. Yet cloud-native platforms like Onshape and SOLIDWORKS Cloud are projected to log a 7.37% CAGR, propelled by frictionless deployment and automatic version management. High-end desktop giants retain niche dominance in deep simulation, complex surface modeling and industry-specific toolsets, but their price premium invites scrutiny.

In the coming five years, vendors will blur tiers, bundling PDM, simulation and rendering into single entitlements. Community app stores will extend functionality via low-code plugins, letting mid-range users access specialized workflows formerly reserved for elite suites. As browser-based kernels mature, the 3D CAD software market will judge products less on installation footprint and more on AI-assisted productivity, ecosystem reach and API openness.

By Geography: Asia-Pacific Acceleration Challenges North American Leadership

North America owns 32.0% revenue, backed by aerospace and defense primes and early cloud uptake. Asia-Pacific, by contrast, leads in growth at 5.82% CAGR as governments champion smart factory initiatives and indigenous software stacks. China funds domestic CNC and CAD integration to reduce export-control exposure. Japan’s manufacturing-first philosophy demands tight CAM-CAD fusion, giving rise to specialized workflows distinct from Western counterparts. India’s engineering-services exporters increasingly adopt cloud tools to collaborate with global clients in real time.

Europe maintains moderate expansion driven by stringent eco-design directives that push digital-twin validation. South America and the Middle East steadily adopt BIM-linked CAD as infrastructure booms but remain smaller slices of overall 3D CAD software market size. Currency volatility and skills gaps limit near-term upside, yet localized training and cloud datacenters are building a foundation for gradual acceleration.

Geography Analysis

North America started 2025 with 32.0% revenue and will likely track a 5.82% CAGR through 2030. Mature aerospace, automotive and medical-device clusters generate consistent license renewals, while SaaS rollouts offer incremental upside. Large enterprises widen platform footprints rather than add new seats, so vendor focus shifts to upselling AI modules and simulation bundles. Canada’s reseller consolidation—such as GoEngineer’s CAD MicroSolutions deal—bolsters cross-border customer support and nurtures mid-market cloud adoption.

Asia-Pacific’s faster 5.82% CAGR stems from capacity expansion and policy incentives. China’s pivot to high-value manufacturing elevates demand for advanced surface modeling, tolerance analysis and cyber-secure collaboration. Local developers invest in home-grown kernels to avoid license dependencies. Japan’s CAM-centric workflows encourage deep shop-floor feedback loops that require bidirectional CAD/CAM data structures. In October 2024, India's AEC and medical device sectors are integrating BIM and CAD systems through partnerships between Nemetschek India and MicroGenesis, with a target of 15-20% domestic market share by 2026.

Europe balances stable demand with regulatory-driven upgrades. Automotive OEMs embed life-cycle CO₂ calculations into design dashboards to comply with EU taxonomy rules. Aerospace Tier-1s expand digital-thread pilots that couple CAD models to IoT-equipped production lines, aligning with long-term sustainability targets. Brexit logistics complexities drive multi-site data-hosting strategies, prompting UK firms to negotiate hybrid cloud contracts that meet both GDPR and export-control mandates. EMEA vendors emphasize continuous security validation to assuage privacy and IP transfer concerns.

Competitive Landscape

The 3D CAD software market exhibits moderate concentration as the top five players—Dassault Systèmes, Autodesk, Siemens, PTC and Hexagon—lean on platform breadth and cross-selling muscle. Recent megadeals underscore a race toward AI-native, cloud-centric portfolios: In March 2025, Siemens closed a USD 10.6 billion takeover of Altair, fortifying simulation depth and HPC scale. In February 2025, Dassault's acquisition of Contentserv strengthens its product-experience management operations, marking a transition from computer-aided design (CAD) to value-chain management.

Autodesk's recurring revenue highlights how subscription saturation strengthens cash stability, supporting reinvestment in AI assistants and generative algorithms. PTC deepens AWS ties to accelerate Onshape performance and integrate cloud PLM, chasing a unified SaaS suite play. Hexagon absorbs Geomagic to mesh scan-data workflows with metrology solutions, catering to in-process inspection use cases.

Emerging challengers differentiate via specialized engines: PhysicsX focuses on aircraft generative design, Neural Concept targets GPU-accelerated CFD surrogates, and CADDi monetizes design-intelligence insights for supply-chain optimization. Strategic partnerships—NVIDIA with Siemens, Microsoft with Hexagon—inject AI compute and cloud reach, further heightening the bar for innovation. Patent filings cluster around geometry-kernel acceleration, cloud collaboration and generative optimization, suggesting sustained investment pressure on incumbents.

3D CAD Software Industry Leaders

Dassault Systèmes SE

Autodesk Inc.

Siemens Industry Software Inc.

PTC Inc.

Hexagon AB (MSC Software & Bricsys)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Siemens completed its USD 10.6 billion acquisition of Altair Engineering, adding AI-powered simulation breadth

- February 2025: Dassault Systèmes’ Centric Software bought Contentserv for EUR 220 million, strengthening PXM capabilities

- February 2025: Autodesk posted 12% Q4 FY2025 revenue growth to USD 1.64 billion and announced a restructuring impacting 1,350 roles

- January 2025: GoEngineer bought CAD MicroSolutions, expanding SOLIDWORKS and 3D-printing coverage in Canada

- December 2024: Hexagon AB purchased 3D Systems’ Geomagic software for USD 123 million, enriching scan-to-CAD workflows

- October 2024: Dassault Systèmes released SOLIDWORKS 2025 with AI-assisted command prediction and automatic drawings

- October 2024: Bechtle AG acquired DriveWorks Ltd. to enlarge design-automation reach in the UK

Global 3D CAD Software Market Report Scope

| On-Premise |

| Cloud-native SaaS |

| Industrial Equipment and Machinery |

| Aerospace and Defence |

| Automotive and Transportation |

| Consumer Electronics |

| Healthcare and Medical Devices |

| Architecture, Engineering and Construction (AEC) |

| 3D Modelling and Drafting |

| Simulation and Analysis |

| Generative Design |

| Additive-Manufacturing Preparation |

| Mainstream Mid-range CAD |

| High-end CAD |

| Cloud-native CAD |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Kuwait | |

| Bahrain | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Deployment Mode | On-Premise | |

| Cloud-native SaaS | ||

| By End-Use Industry | Industrial Equipment and Machinery | |

| Aerospace and Defence | ||

| Automotive and Transportation | ||

| Consumer Electronics | ||

| Healthcare and Medical Devices | ||

| Architecture, Engineering and Construction (AEC) | ||

| By Application | 3D Modelling and Drafting | |

| Simulation and Analysis | ||

| Generative Design | ||

| Additive-Manufacturing Preparation | ||

| By Software Tier | Mainstream Mid-range CAD | |

| High-end CAD | ||

| Cloud-native CAD | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Kuwait | ||

| Bahrain | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the 3D CAD software market in 2030?

It is expected to reach USD 16.25 billion, reflecting a 5.45% CAGR between 2025 and 2030.

Which deployment mode is growing the fastest?

Cloud-native SaaS platforms are forecast to expand at 7.11% CAGR as companies favor subscription access and real-time collaboration.

Why is healthcare adopting 3D CAD tools quickly?

Personalized implants, regulatory traceability and additive manufacturing workflows push healthcare-device makers toward advanced cloud-enabled design suites.

How are vendors integrating AI into design workflows?

Leading platforms embed generative algorithms that propose weight-optimized shapes, automate routine commands and tie simulation directly to modeling.

What security measures protect CAD data in the cloud?

Providers apply SOC 2 certifications, AES-256 encryption, zero-trust access controls and region-specific data-residency options to safeguard intellectual property.

Page last updated on: