UX Design Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

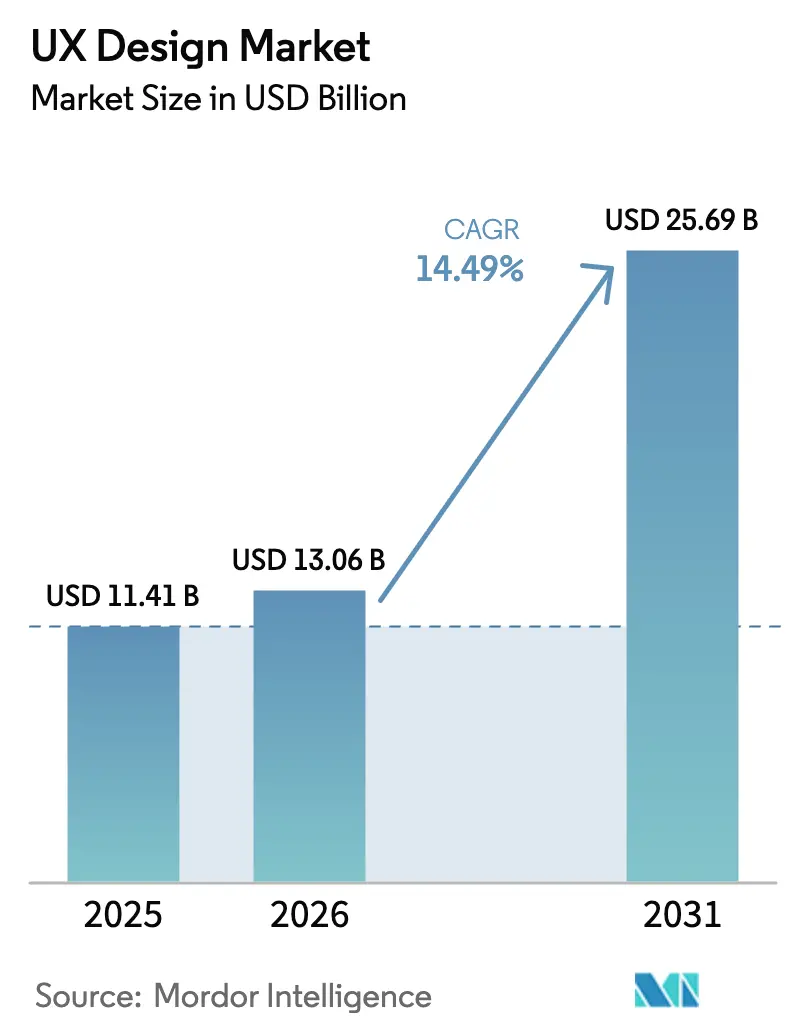

| Market Size (2026) | USD 13.06 Billion |

| Market Size (2031) | USD 25.69 Billion |

| Growth Rate (2026 - 2031) | 14.49% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UX Design Market Analysis by Mordor Intelligence

The UX design market size is expected to grow from USD 11.41 billion in 2025 to USD 13.06 billion in 2026 and is forecast to reach USD 25.69 billion by 2031 at 14.49% CAGR over 2026-2031. Enterprises now treat UX as a core strategic lever, a shift underscored by Microsoft’s USD 70.1 billion Q3 FY25 revenue, where demand for AI-enabled cloud experiences required sophisticated interfaces. Alphabet recorded USD 90.2 billion in Q1 2025 revenue as Google Cloud’s AI-enhanced services expanded 28%, reinforcing the same pattern. Cloud deployment retains a 65.98% market foothold, mirrored by 18.20% forecast growth as distributed teams favor collaborative, browser-based design environments. Large enterprises hold 70.45% share but still post a healthy 16.43% CAGR, while small and medium businesses accelerate UX spending to stay competitive. Industry demand is most intense in BFSI, which commands 28.52% share, yet retail and ecommerce stand out with an 18.40% CAGR, linking better experience design directly to conversion gains.

Key Report Takeaways

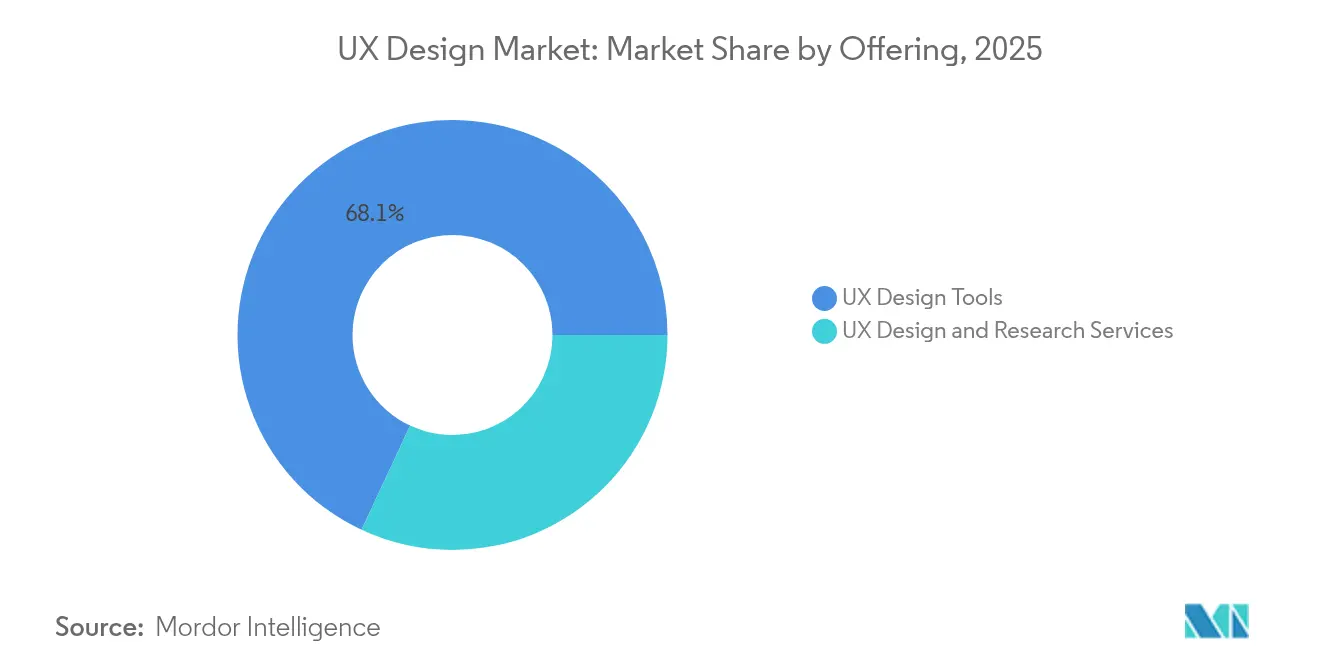

- By offering, tools accounted for 68.05% of UX design market share in 2025 and are expanding at a 16.12% CAGR through 2031.

- By enterprise size, large enterprises held 69.80% of UX design market share in 2025, while small and medium enterprises are catching up yet still trail the 16.05% CAGR posted by large organizations.

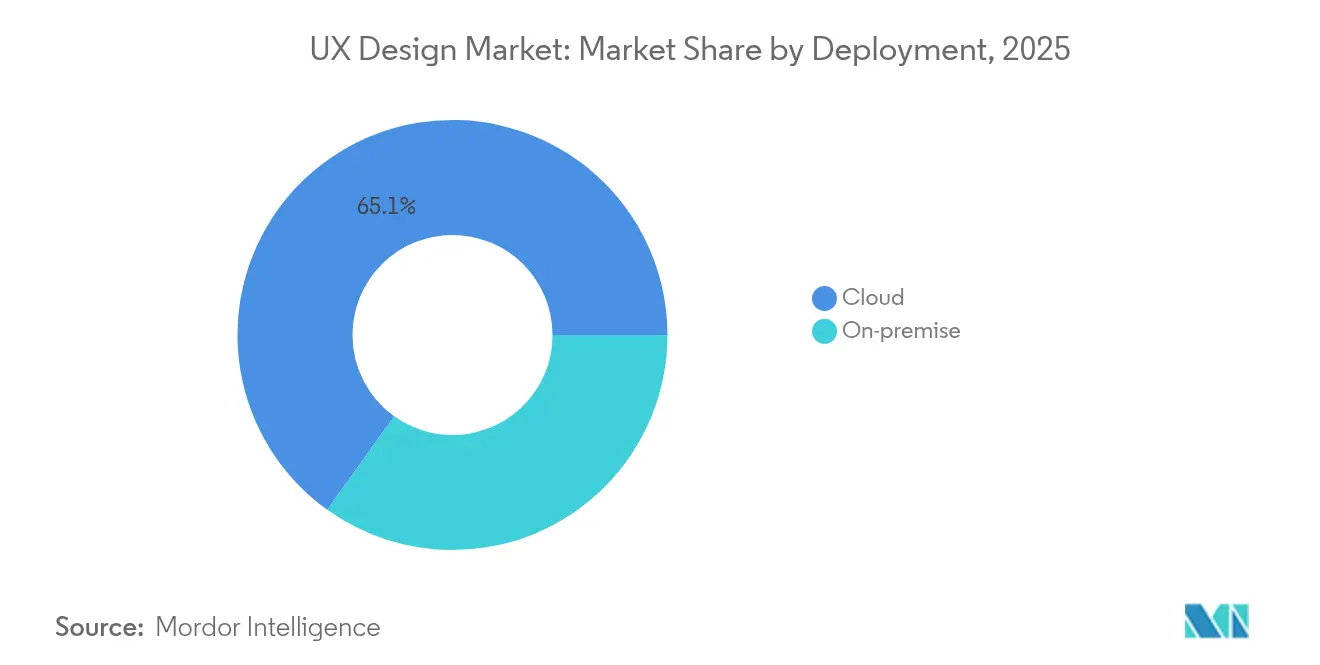

- By deployment model, the cloud segment captured 65.10% of UX design market size in 2025 and is projected to grow at an 17.45% CAGR to 2031.

- By industry, BFSI led with 28.10% revenue share in 2025; retail and ecommerce are forecast to expand at an 17.92% CAGR through 2031.

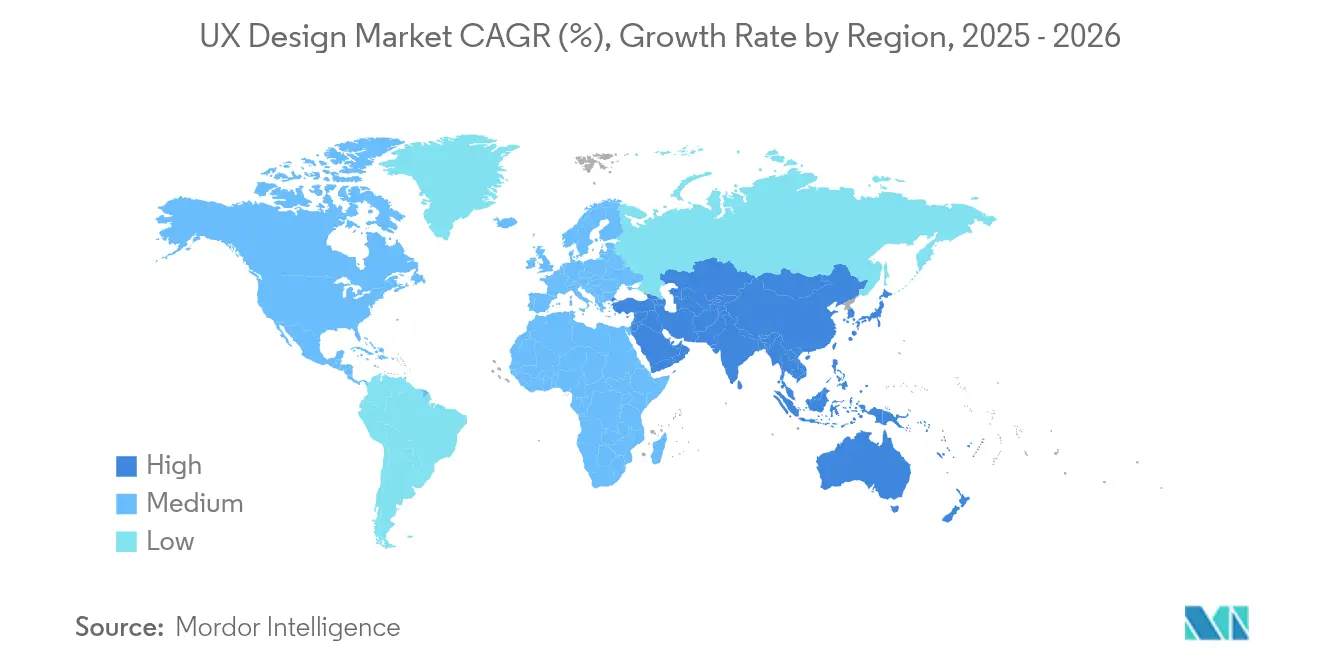

- By geography, North America commanded 43.75% of UX design market size in 2025, while Asia-Pacific is set to post the fastest 19.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of UX Design Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of mobile and web applications | +3.2% | Global (strongest in Asia-Pacific) | Medium term (2-4 years) |

| Accelerating digital-transformation spend on CX | +4.1% | North America and EU, spreading to Asia-Pacific | Short term (≤ 2 years) |

| Proliferation of SaaS and e-commerce platforms | +2.8% | Global, tech hubs | Medium term (2-4 years) |

| Technological advancements (AI, AR/VR, IoT) | +3.5% | North America and EU, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Inclusive-accessibility design mandates | +1.9% | EU and North America | Short term (≤ 2 years) |

| GenAI-driven design automation | +2.7% | Global, tech-forward firms | Medium term (2-4 years) |

| Rising adoption of mobile and web applications | +3.2% | Global (strongest in Asia-Pacific) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Digital-Transformation Spend on CX

Enterprises now budget an average USD 33 million for customer-experience technology, and a significant portion flows directly into UX initiatives. TEKsystems highlights UX as a critical skills gap, signaling that demand for design talent outstrips supply. Retail studies show effective UX can lift conversions 400%, while 89% of customers leave after poor experiences.[1]Retail TouchPoints, “Why UX Drives 400% Conversion Gains,” retailtouchpoints.com This budget prioritization widens the performance gap between design-mature firms and laggards.

Technological Advancements (AI, AR/VR, IoT)

Thirty-five percent of SaaS vendors already embed AI, with 42% planning adoption to personalize interfaces and automate layout decisions.[2]Selleo, “AI Adoption in SaaS 2025 Survey,” selleo.com Figma’s AI-driven “vibe-coding” converts plain-language briefs into production-ready code, shortening design-to-dev cycles. IoT growth adds context-aware screens that must adapt to changing environments, while Microsoft’s updated design system shows how AI outputs can coexist with user agency.

Proliferation of SaaS and E-commerce Platforms

Global SaaS revenues are on track for USD 195 billion, driving a competitive focus on superior interfaces over feature parity. Executives at 79% of e-commerce firms cite user-experience tech as a top investment priority.[3]Integrio Systems, “Digital Transformation Spending Trends 2025,” integrio.netVertical SaaS solutions require domain-specific UX, and low-code ecosystems amplify demand for reusable design libraries that keep citizen developers on brand.

GenAI-Driven Design Automation Reducing Time-to-Market

UserTesting’s AI Insight Summary processed 30,000 study videos and saved 9,500 analyst hours, proving measurable productivity gains. ProtoPie’s USD 21 million Series B funds AI prototyping that large clients such as Google already pilot. Research from Jakob Nielsen suggests AI could expand the UX workforce from 3 million to 10 million by 2034 because automation lowers entry barriers while elevating strategic design roles.

Restraints Impact Analysis of UX Design Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High costs and budget constraints | −2.1% | Global (heavier in emerging markets) | Short term (≤ 2 years) |

| Shortage of skilled UX professionals | −1.8% | Global, acute in Asia-Pacific | Medium term (2-4 years) |

| Algorithmic bias and ethics concerns in AI design tools | −0.9% | EU and North America | Long term (≥ 4 years) |

| Data-privacy rules limiting in-product analytics | −1.2% | EU first, spreading globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Costs and Budget Constraints

App-interface projects cost USD 6,000 in India versus USD 48,000 in North America, making ROI harder to justify for SMEs in resource-constrained economies. In Japan, 52.2% of firms report unclear UX returns, mainly due to measurement skill shortages. Inflationary pressures since 2024 also push decision-makers to delay discretionary spend even when UX links directly to retention.

Shortage of Skilled UX Professionals

Indeed tracked an 89% drop in UX research postings from 2022 peaks, yet demand remains elevated, creating a paradox. Only 4.2% of open roles target entry-level talent, escalating salary brackets to USD 120,000–168,000 in key hubs. Emerging markets suffer most as local education pipelines lag, forcing a reliance on costly expatriate specialists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

UX Design Market Segment Analysis

By Offering:

Tools Dominate Service RevenueTools held 68.05% of UX design market share in 2025 and posted a 16.12% CAGR, underscoring how software now eclipses consulting in value capture. Internal design teams gravitate to cloud-native suites that support synchronous editing, version control, and AI-assisted component generation. Figma alone reports that 75% of surveyed designers rely on its platform, with 85% of users outside the United States. Service providers retain relevance for regulated industries where compliance expertise is critical, yet even these engagements increasingly bundle software licenses with strategic advisory.

Demand for automated tooling increases as AI inserts accessibility checks, responsive-layout generators, and code handoff directly into design canvases. As a result, enterprises shift CapEx from hourly consulting fees to recurring subscriptions. Consulting firms respond by emphasizing change-management, governance, and enterprise-wide design-system deployment. This hybrid model balances automated efficiency with human oversight for mission-critical projects.

By End-user Enterprise Size:

Large Enterprises Lead InvestmentLarge enterprises controlled 69.80% of UX design market size in 2025 and continued to advance at a 16.05% CAGR through 2031, reflecting their deeper pockets and regulatory exposure. Global brands like Citigroup employ federated design systems spanning hundreds of applications, driving demand for robust governance features. SMEs, while resource-limited, invest steadily as low-code commerce engines make UX table stakes.

Design maturity correlates with key metrics: companies with well-defined design ops report higher Net Promoter Scores and lower churn. Subscription-based “design-as-a-service” models now package senior oversight, junior execution, and platform access at predictable monthly costs, enabling SMEs to secure enterprise-grade experiences without ballooning payroll. Nevertheless, constrained budgets keep SME projects narrowly focused on near-term conversion gains.

By Deployment:

Cloud Platforms Enable CollaborationCloud deployments represented 65.10% of UX design market share in 2025 and are growing at an 17.45% CAGR. Browser-based suites enable real-time co-creation across time zones, a must-have since remote work became standard. Microsoft’s Fluent framework shows how cloud-resident tokens propagate consistent UI across Windows, web, and mobile properties.

AI features flourish in the cloud, where vendors can train models on anonymized usage telemetry to refine pattern suggestions. Even security-conscious banks now adopt hybrid modes: sensitive data remains on-premise while design review sessions occur in encrypted cloud workspaces. Improved compliance certifications—SOC 2 Type II, ISO 27001, GDPR—further quell objections.

By End-user Industry:

BFSI Leads, Retail AcceleratesBFSI captured 28.10% of UX design market share in 2025 as banks race to digitize commoditized services. Accessibility mandates and fintech competition force continuous interface upgrades to retain customers. Retail and ecommerce post the swiftest 17.92% CAGR, since even small UX gains can materially lift cart-to-purchase ratios.

Healthcare directs rising spend to patient-facing portals where clarity and trust are paramount. Clinical workflows also benefit as intuitive dashboards cut cognitive load. Media and entertainment refines content discovery algorithms, and telecom operators streamline self-service portals to slash call-center costs. Emerging IoT-heavy verticals—from smart homes to industrial automation—introduce multimodal requirements that push UX beyond the screen.

Geography Analysis

Metropolitan North America UX Design Market

North America accounted for 43.75% of UX design market size in 2025. Technology heavyweights invest aggressively in RandD, and the Americans with Disabilities Act obliges digital accessibility across both public and private sectors. Microsoft alone generated USD 42.4 billion in cloud revenue that depends on refined interface coherence. Venture capital ecosystems clustered around San Francisco, Seattle, Toronto, and Austin funnel capital into next-generation design tooling startups.

APAC UX Design Market

Asia-Pacific is projected to post the fastest 19.10% CAGR. Digital-first consumers in India, Indonesia, and Australia push local enterprises to adopt real-time collaborative design suites, with Figma reporting a 46% jump in regional tool investment over five years. Yet skills shortages persist: 52.2% of Japanese firms cite unclear ROI on UX due to measurement challenges. Government initiatives, such as India’s Digital Public Infrastructure program, earmark funds for design-centric public services, thereby nurturing a new talent pipeline.

Broader European Markets

Europe maintains steady growth on the back of the European Accessibility Act, enforced from June 2025, which requires WCAG 2.1 AA compliance or face penalties up to EUR 1 million. Switzerland voluntarily aligns with the directive, widening the addressable market for compliance specialists. Data-privacy culture shapes UX in the region: cookie-consent flows, granular user-controls, and algorithm-explainability features are now standard. Design vendors differentiate by building privacy-by-design templates that satisfy GDPR while preserving personalization opportunities.

Competitive Landscape

The UX design market remains moderately fragmented. Software vendors such as Adobe, Figma, and Sketch consolidate share through network effects and plugin ecosystems. Figma filed confidentially for an IPO after surpassing USD 600 million ARR, illustrating how cloud collaboration disrupts desktop incumbents. Adobe’s acquisition of Figmable strengthens its research analytics, positioning the Creative Cloud suite to address end-to-end experience workflows.

AI is the defining battleground: platforms incorporate generative layout suggestions, automated color-contrast checks, and natural-language component search. Contentsquare’s merger with Hotjar and subsequent knot-up with UserTesting creates an integrated insights stack that competes head-to-head with full-service agencies. Traditional consultancies evolve into hybrid models that pair design leadership with proprietary toolkits, ensuring relevance against SaaS-first entrants.

White-space opportunities persist in accessibility-focused automation, domain-specific component libraries, and design governance dashboards tracking token usage across codebases. Startups addressing these niches often secure strategic funding or exit via acquisition once they prove synergy with larger platform roadmaps. Vendor roadmaps increasingly prioritize open APIs and design-system interoperability to lock in enterprise clients seeking seamless handoff between design and development.

UX Design Industry Leaders

Figma Inc.

Adobe Inc.

Sketch

InVisionApp Inc.

Axure Software Solutions

- *Disclaimer: Major Players sorted in no particular order

UX Design Market Companies Covered in this Report

- Intellectsoft

- UXtweak

- UXPressia

- Userlytics Corporation

- Playbook UX LLC

- 1thing Design and Innovation Pvt Ltd

- Aufait UX

- ProCreator Solutions Pvt Ltd

- Eleken Design Ltd

- Clay Global LLC

- Figma Inc.

- Adobe Inc. (Adobe XD)

- InVisionApp Inc.

- Bohemian Coding (Sketch)

- Axure Software Solutions

- Balsamiq Studios

- UserTesting Inc.

- Hotjar Ltd

- Optimal Workshop Ltd

- Maze Design Inc.

Recent Industry Developments in UX Design Market

- June 2025: Figma introduced Code Layers in Figma Sites, letting creators add interactions and animations with manual or AI-generated code.

- May 2025: Figma launched Figma Make, an AI tool that builds layouts from library assets using user-defined style rules.

- January 2025: Adobe acquired Figmable to integrate advanced UX research analytics across Creative Cloud applications.

- December 2024: InVision confirmed a full shutdown, selling its Freehand white-boarding tool to Miro.

Global UX Design Market Report Scope

UX design centers on crafting products and services that prioritize user satisfaction and ease of use. By delving deep into user behaviors and needs, designers forge interactions that resonate intuitively. From inception to launch, the focus remains steadfast on aligning with user goals and expectations. The ultimate aim is to create products that are not just functional but also easy to navigate, ensuring a smooth user journey. Given its holistic approach, UX design draws from various fields, with experts often hailing from visual design, programming, psychology, and interaction design backgrounds.

The market is defined by the revenue accrued through the sale of UX Design by various players across the globe. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The UX design market is segmented by enterprise size (small & medium enterprises and large enterprises), deployment (cloud and on-premise), and geography (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Segmentation Overview

| UX Design Tools |

| UX Design and Research Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Cloud |

| On-premise |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Retail and eCommerce |

| Media and Entertainment |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Offering | UX Design Tools | ||

| UX Design and Research Services | |||

| By End-user Enterprise Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By Deployment | Cloud | ||

| On-premise | |||

| By End-user Industry | IT and Telecom | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Retail and eCommerce | |||

| Media and Entertainment | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the UX design market?

The UX design market reached USD 13.06 billion in 2026.

How fast is the UX design market expected to grow?

It is forecast to rise at a 14.49% CAGR to USD 25.69 billion by 2031 over 2026-2031.

Which segment holds the largest share of the UX design market?

Design tools lead with 68.05% of 2025 revenue.

Which region will grow the fastest?

Asia-Pacific is projected to expand at a 19.10% CAGR through 2031.

Why are cloud deployments growing so rapidly?

Cloud platforms enable real-time collaboration and integrate AI features, driving an 17.45% CAGR for the cloud segment.

Page last updated on: