Quick Commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 213.59 Billion |

| Market Size (2031) | USD 303.42 Billion |

| Growth Rate (2026 - 2031) | 20.62% CAGR |

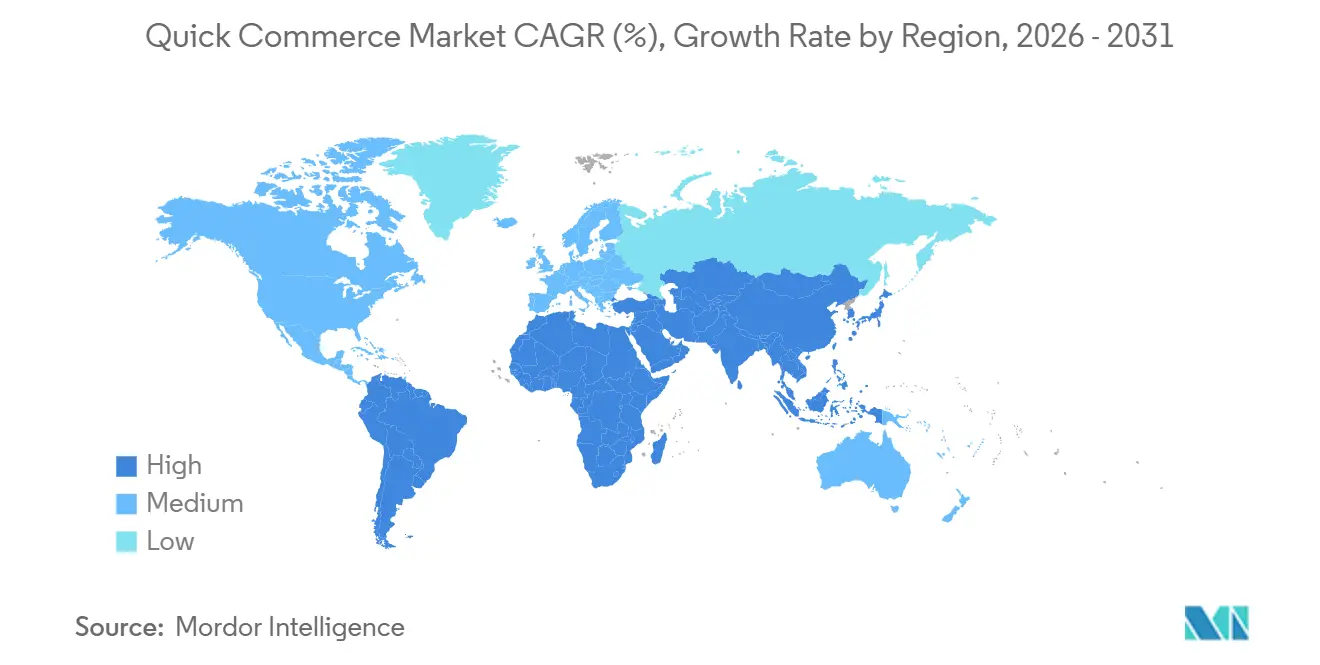

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

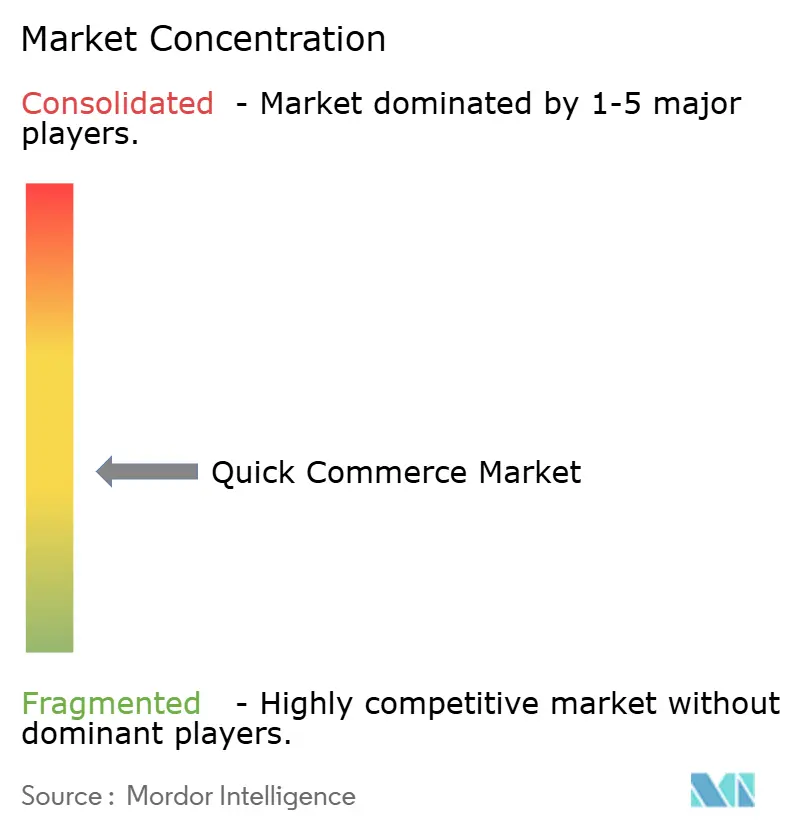

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Quick Commerce Market Analysis by Mordor Intelligence

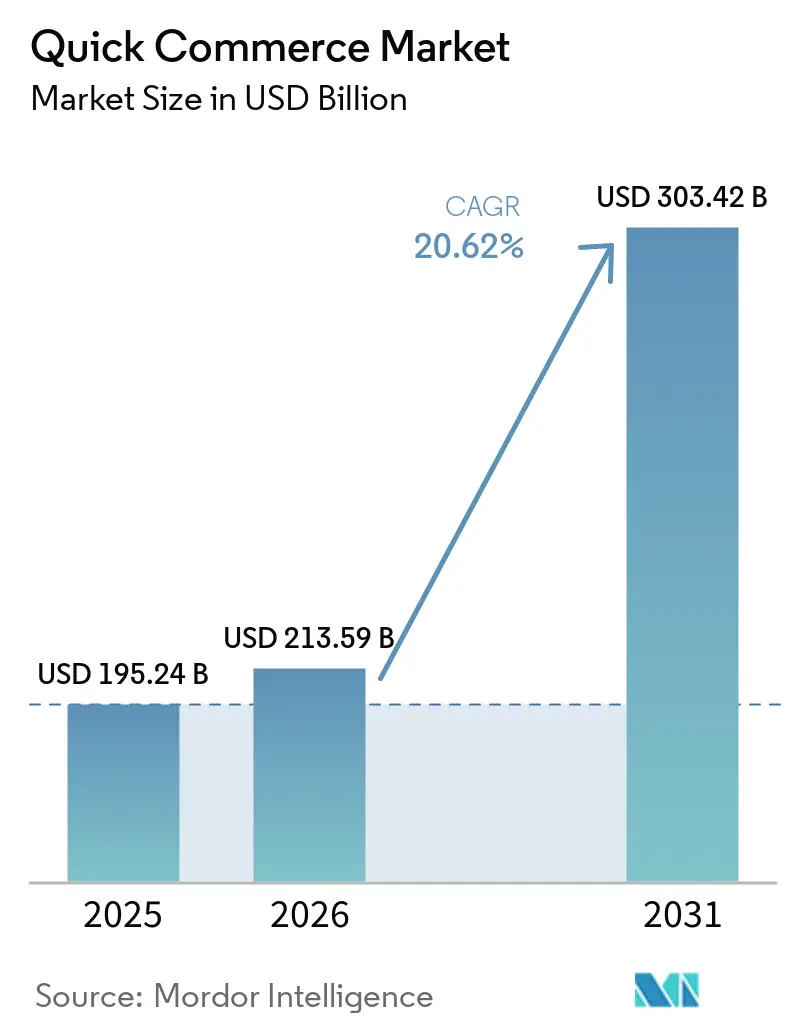

The quick commerce market size is projected to expand from USD 195.24 billion in 2025 and USD 213.59 billion in 2026 to USD 303.42 billion by 2031, registering a CAGR of 20.62% between 2026 to 2031. This pace remains ahead of broader digital commerce and points to a structural shift in how households buy daily essentials. Growth is being supported by denser dark-store networks and stronger route planning, which now allow platforms to keep sub-30-minute delivery promises at cost levels that were hard to sustain before 2022. Fill-in shopping remains the core use case because small, urgent replenishment orders fit urban routines and make delivery fees easier to justify, especially in dual-income households. Competition is moving beyond speed alone, as retail media, assortment expansion, and selective city penetration are becoming central to margin improvement in the quick commerce market. Regulatory pressure on gig work and dark-store land use still slows expansion in some regions, but rising urbanization, smartphone use, and convenience-led purchasing continue to widen the customer base for the quick commerce market.

Key Report Takeaways

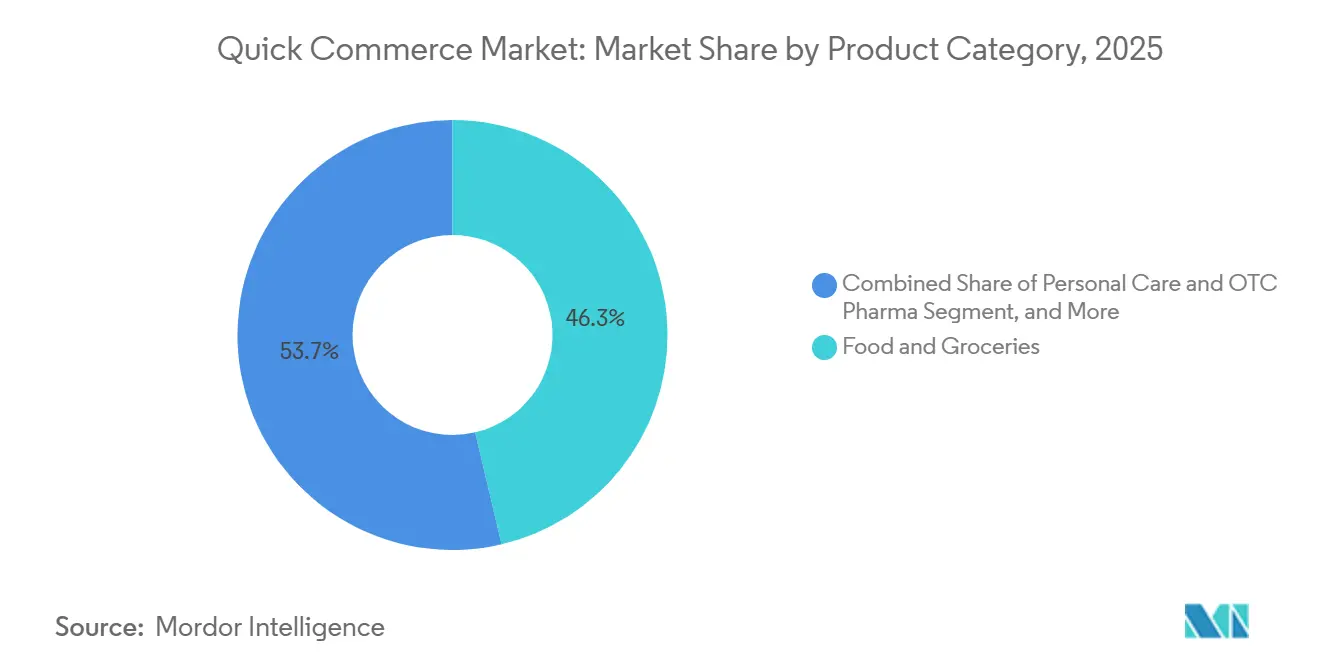

- By product category, food and groceries held 46.34% of the quick commerce market share in 2025, while personal care and OTC pharma is forecast to expand at a 21.34% CAGR through 2031.

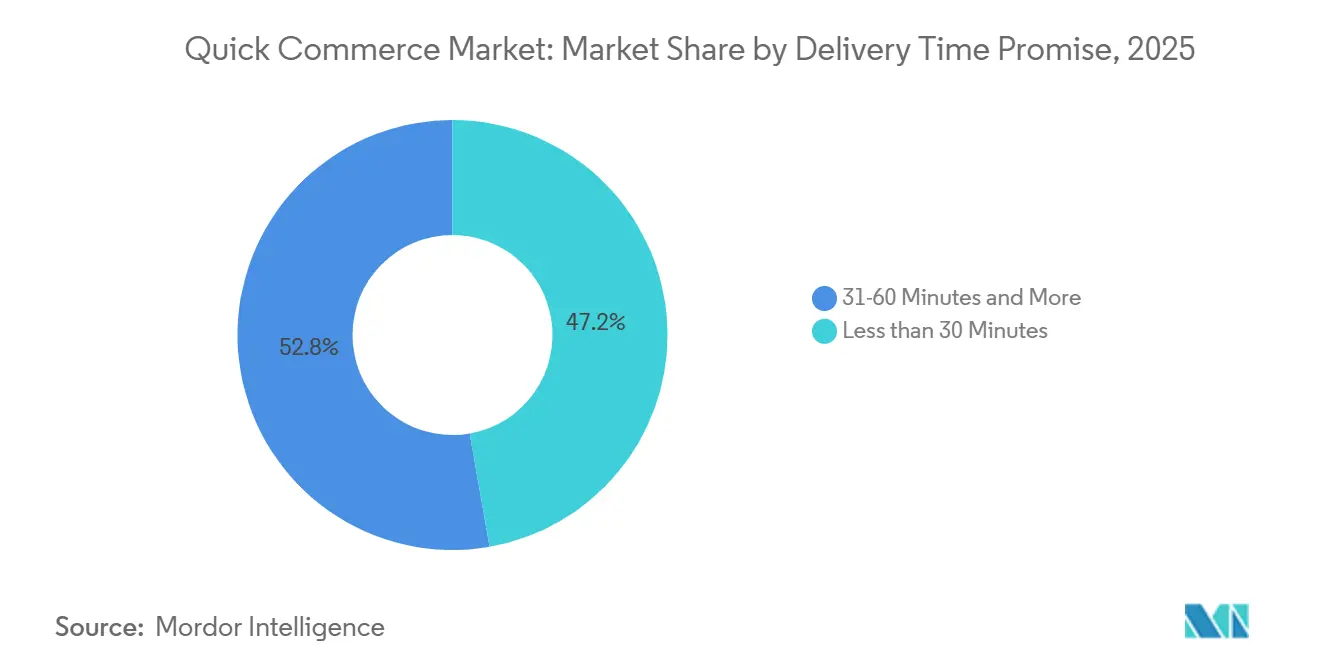

- By delivery time promise, the less than 30 minutes segment accounted for 47.24% of the quick commerce market size in 2025, while the 31-60 minutes segment is projected to grow at a 21.23% CAGR through 2031.

- By geography, Asia-Pacific held 39.34% of the quick commerce market share in 2025 and is also the fastest-growing regional segment at a 21.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Quick Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Immediate Convenience and Fill-In Shopping | +4.2% | Global | Short term (≤ 2 years) |

| Dark-Store and Micro-Fulfillment Network Expansion | +3.5% | Asia-Pacific core, spill-over to Europe and North America | Medium term (2-4 years) |

| Mobile-First Ordering and Cashless Checkout Adoption | +2.4% | Global, strongest in Asia-Pacific and Middle East Africa | Short term (≤ 2 years) |

| Category Expansion Beyond Grocery Missions | +2.1% | Global, Asia-Pacific leading, spill-over to Europe and North America | Medium term (2-4 years) |

| Retail Media Income Offsetting Delivery Economics | +1.6% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Backroom Automation Enabling Second-Wave City Profitability | +0.9% | Asia-Pacific core, spill-over to Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Immediate Convenience and Fill-In Shopping

Immediate availability has become a standard expectation in dense urban areas, and that shift is raising repeat usage in the global quick commerce market. Consumers often use these apps for missing ingredients, baby care items, household basics, or late-night top-up needs rather than for full weekly baskets. That pattern lowers price comparison because the trigger is urgency, not basket optimization. Dual-income households are placing a clearer value on time saved, which helps platforms retain fee-paying demand even when offline alternatives remain cheaper. As long as service reliability stays high, this behavior supports recurring orders and stronger customer lifetime value in the quick commerce market.

Dark-Store and Micro-Fulfillment Network Expansion

Dark-store expansion remains one of the clearest scale levers in the global quick commerce market. Eternal said Blinkit ended Q4 FY2026 with 2,243 active stores and is targeting 3,000 by March 2027, which shows that leading operators are still prioritizing network depth. Amazon India also committed INR 2,800 crore (USD 337 million) to expand Amazon Now to more than 1,000 micro-fulfillment centers across 100 cities, reinforcing the same direction of travel. A denser store grid shortens delivery distance, lowers breach risk, and improves inventory availability within tight service windows. That is why store buildout continues even when payback periods remain uneven across cities in the quick commerce market.

Mobile-First Ordering and Cashless Checkout Adoption

Mobile-first design has become a core growth engine for the quick commerce market because ordering, payment, and reordering now happen within a very short decision window. India's National Payments Corporation reported that real-time transaction volumes surpassed 130 billion in FY2024-25, which shows how ready the payment layer is for fast repeat purchasing.[1]National Payments Corporation of India, “NPCI Annual Report 2024-25,” NPCI, npci.org.in When checkout is almost frictionless, platforms can lift repeat orders, improve basket completion, and encourage impulse add-ons. This makes app design, one-tap reorders, and smart notifications as important as delivery speed. Operators that combine fast payments with strong personalization are therefore taking a larger share of incremental order flow in the quick commerce market.

Category Expansion Beyond Grocery Missions

Category expansion is widening the economic base of the quick commerce market beyond urgent grocery trips. Zepto added more than 5,000 electronics SKUs, including Apple products, by March 2025, showing that platforms want higher-value baskets from the same delivery network. Wolt added more than 3,000 new non-food venue partnerships in the second half of 2025, and non-restaurant orders represented 20% of its total order mix, which points to the same shift in a different operating model.[2]Wolt Enterprises Oy, “Non-Food Venue Expansion, 3,000+ New Partners in H2 2025,” Wolt Newsroom, explore.wolt.com These categories tend to raise average order values and reduce the dependence on grocery-only demand cycles. They also create new advertising inventory for brands, which gives platforms another way to improve contribution margins in the quick commerce market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Last-Mile Cost and Thin Basket Economics | -2.8% | Global | Short term (≤ 2 years) |

| Gig-Worker Regulation and Dark-Store Zoning Scrutiny | -1.7% | Europe, Asia-Pacific, North America | Medium term (2-4 years) |

| Supplier Trade-Term Pushback on Always-On Promotions | -1.2% | Global | Medium term (2-4 years) |

| Curbside Enforcement and Rider Safety Rules Stretching SLAs | -0.6% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Last-Mile Cost And Thin Basket Economics

Last-mile cost remains the main structural brake on the quick commerce market. In India, sub-30-minute operators were reported to carry logistics expenses equal to 19% to 25% of GMV, far above the level for slower 2-hour models. CNBC TV18 also reported estimated delivery cost floors of INR 95-100 (USD 1.1-1.2) per order and suggested that breakeven requires average order values near INR 750 (USD 9.0) under current rider cost structures. Blinkit's positive adjusted EBITDA in Q4 FY2026 shows that improvement is possible, but that outcome depended on scale, density, retail media support, and careful geographic selection. Until basket values move higher on a wider base, unit economics will continue to limit how fast the quick commerce market can scale across lower-density cities.

Gig-Worker Regulation And Dark-Store Zoning Scrutiny

Regulation is becoming more important for the quick commerce market because labor rules and dark-store permits are tightening at the same time. India's Social Security Central Rules 2026, notified in May 2026, introduced a 1% to 2% welfare levy on platform aggregators. Karnataka's platform law brought a 1% transaction fee and wider expectations around grievance handling and transparency, while Malaysia's Gig Workers Act 2025 took effect on March 31, 2026, with minimum earnings and social security provisions. At the same time, zoning restrictions in France and Amsterdam narrowed the site pool for dark stores in dense residential areas. These rules do not stop growth, but they do slow rollouts, raise compliance costs, and make cross-border operating models harder to standardize in the quick commerce market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Non-Grocery Verticals Reshape the Margin Profile

Food and groceries accounted for 46.34% of the quick commerce market size in 2025, which confirms that staple replenishment is still the entry point for most users. The segment benefits from frequent purchase cycles and routine household demand, so it remains the traffic anchor for the quick commerce market. Fresh produce and dairy deepen retention because they push operators to invest in cold-chain capable micro-fulfillment and tighter quality control. Snacks, beverages, and home cleaning items also fit well with the fill-in mission, and they raise basket values without adding much operational complexity. This mix explains why grocery-led platforms can widen frequency first and then layer in higher-margin categories over time.

Personal care and OTC pharma is projected to grow at a 21.34% CAGR through 2031, making it the fastest-growing product category in the quick commerce market. Zepto launched 10-minute medicine delivery in August 2025, which shows how operators are moving from convenience-led positioning to more routine health-related demand. The same network can also support flowers, gifts, and other occasion-led purchases, which gives platforms more use cases without a separate fulfillment buildout. Electronics and accessories add another layer because they lift order values and improve advertising potential for branded sellers. As non-grocery selection widens, the quick commerce market gains a healthier margin mix and less reliance on pure grocery missions.

By Delivery Time Promise: Extended Windows Gain Share as Networks Expand

The less than 30 minutes segment held 47.24% of the quick commerce market size in 2025, which shows that speed still shapes consumer choice in the category. This tier works best in dense urban districts where store catchments are small and order volumes are high enough to support labor and rent. For the quick commerce market, the segment also acts as a switching barrier because a fast and reliable promise is hard for slower entrants to match. Large platforms therefore keep investing in route design, rider availability, and inventory placement to protect this advantage. The financial challenge is that the same promise usually carries the highest cost intensity.

The 31-60 minutes segment is projected to grow at a 21.23% CAGR through 2031, making it the fastest-growing delivery window in the quick commerce market. This reflects the entry of large grocery operators with existing fulfillment assets and the expansion of pure-play platforms into cities where sub-30-minute economics are still developing. DoorDash said its non-restaurant verticals, which often sit closer to this delivery window, were expected to turn gross-profit positive in the second half of 2026. Instacart also introduced Caper Carts with NVIDIA Jetson modules in March 2026, showing that platforms can compete through smarter shopping and personalization rather than speed alone. As a result, the quick commerce market is likely to support both ultrafast and extended-window models, but the capital logic differs between them.

Geography Analysis

Asia-Pacific held 39.34% of the quick commerce market share in 2025 and is set to expand at a 21.54% CAGR through 2031, which keeps the region at the center of the global quick commerce market. China remains the scale anchor because Meituan, Alibaba, and JD.com already operate large logistics and merchant ecosystems that support rapid local fulfillment. The region is also seeing aggressive promotional competition, with Alibaba and JD.com each earmarking RMB 10 billion (USD 1.4 billion) for subsidies and incentives as platforms defend frequency and order volume. In India, rapid network rollout by Blinkit, Zepto, Swiggy Instamart, and Amazon Now is pushing the quick commerce market beyond top metros and into a wider set of cities.

North America represents a more measured but financially important part of the quick commerce market, with platforms increasingly focused on grocery profitability rather than growth at any cost. In the United States, Instacart reported Q1 2026 GTV of USD 10.288 billion, up 13% year on year, and adjusted EBITDA of USD 300 million at a 29% margin, which underlines the strength of its operating model. DoorDash completed its Deliveroo acquisition in October 2025 for GBP 2.9 billion (USD 3.86 billion), linking U.S. scale with operations across the United Kingdom, France, Italy, Belgium, Ireland, Singapore, Hong Kong, the UAE, and Australia. Europe has tighter zoning and labor scrutiny, so the quick commerce market there is more exposed to permit constraints and compliance-driven cost inflation. That pressure is favoring operators with stronger balance sheets and making it harder for smaller standalone entrants to hold urban share in Western Europe.

The Middle East is becoming one of the most concentrated regional pockets in the quick commerce market, led by Talabat's strong grocery and retail momentum. Talabat said grocery and retail GMV rose 45% in Q4 2025, and the company opened a 22,405 square meter distribution center in Cairo with capacity for 1.6 million items a day, giving it a larger operating base for Egypt and nearby markets. South America remains earlier in development, with Brazil and Colombia showing the clearest activity through multi-vertical platforms such as Rappi, while cold-chain and density constraints still limit broader rollout. Africa is still nascent, but urban growth and rising digital payments keep the long-term case for the quick commerce market intact even though current order economics remain tight in many cities.

Competitive Landscape

The global quick commerce market is regionally concentrated but globally fragmented, because leadership is strong inside national or regional clusters rather than across the full world map. Meituan in China, Blinkit in India, DoorDash in the United States, and Talabat in the Middle East each hold leading positions in their core geographies, but none has established a dominant worldwide grip. This structure keeps rivalry high, since traditional grocers, delivery specialists, and tech-led startups are all pursuing the same household spending on everyday items. It also means the quick commerce market rewards local density, merchant coverage, and execution more than simple global scale.

Three strategic themes are standing out in the quick commerce market, fulfillment control, audience monetization, and software productivity. DoorDash's acquisition of Deliveroo in October 2025 is a clear example of cross-border scale building, because it widened the company's geographic network in one move. Amazon India's commitment to more than 1,000 micro-fulfillment centers for Amazon Now shows the same push toward tighter infrastructure ownership and faster coverage buildout. Retail media is becoming more important at the same time, because platforms with large order volumes can sell brand placement and sponsored discovery inside their apps. That extra income matters in the quick commerce market because it helps offset high delivery costs without depending only on higher consumer fees.

Technology is now a central differentiator in the quick commerce market as service speed becomes easier to match. Instacart's March 2026 rollout of Physical AI Caper Carts connected in-store behavior with digital recommendations, while DoorDash said two-thirds of its software code is now AI generated, which points to faster feature deployment and lower engineering overhead.[3]DoorDash, Inc., “Q1 2026 Earnings Results,” DoorDash Investor Relations, ir.doordash.com Smaller regional players can still compete by bundling delivery into super-app ecosystems or by focusing on underpenetrated cities and higher-margin categories. Even so, the quick commerce market is moving toward a clear divide between operators that can fund dense networks and regulatory compliance, and operators that struggle to scale beyond a limited urban footprint.

Quick Commerce Industry Leaders

Meituan

JD.com, Inc.

DoorDash, Inc.

Delivery Hero SE

Maplebear Inc. (Instacart)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Zepto (KiranaKart Technologies Private Limited) received SEBI approval for an IPO with an issue size of INR 11,000-12,000 crore (approximately USD 1.3-1.45 billion), with the listing expected between July and September 2026. The approval provides the first high-profile public-market benchmark valuation for a pure-play q-commerce dark-store operator globally, with implications for comparable valuations across the sector.

- April 2026: Eternal Limited (parent of Blinkit) reported Q4 FY2026 results, with network order value of INR 14,386 crore (approximately USD 1.73 billion), up 95.4% year-on-year, and adjusted EBITDA turning positive at INR 37 crore (approximately USD 4.4 million) for the second consecutive quarter. The milestone establishes Blinkit as the first pure-play q-commerce dark-store operator to demonstrate sustained profitability at scale.

- April 2026: Amazon India announced an investment of INR 2,800 crore (approximately USD 337 million) to expand Amazon Now to over 100 cities, targeting a network exceeding 1,000 micro-fulfillment centers. The commitment positions Amazon as the most aggressive new infrastructure entrant in Indian q-commerce since the segment's formation.

- October 2025: DoorDash, Inc. completed the acquisition of Deliveroo for GBP 2.9 billion (USD 3.86 billion), adding operations in the United Kingdom, France, Italy, Belgium, Ireland, Singapore, Hong Kong, the UAE, and Australia to its platform. The combined entity represents one of the broadest geographic q-commerce footprints assembled under a single corporate structure.

Global Quick Commerce Market Report Scope

The Quick Commerce Market is experiencing significant growth, driven by companies specializing in ultra-fast delivery services. These businesses primarily focus on fulfilling online orders for groceries, convenience items, and household essentials, often delivering within a timeframe of less than 30 minutes.

The Quick Commerce Market Report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, and Other Product Categories), Delivery Time Promise (Less than 30 Minutes and 31-60 Minutes and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Grocery and Staples |

| Fresh Produce and Dairy |

| Snacks and Beverages |

| Personal Care and OTC Pharma |

| Home and Cleaning Supplies |

| Electronics and Accessories |

| Pet Care |

| Flowers and Gifts |

| Other Product Categories |

| Less than 30 Minutes |

| 31-60 Minutes and More |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Product Category | Grocery and Staples | |

| Fresh Produce and Dairy | ||

| Snacks and Beverages | ||

| Personal Care and OTC Pharma | ||

| Home and Cleaning Supplies | ||

| Electronics and Accessories | ||

| Pet Care | ||

| Flowers and Gifts | ||

| Other Product Categories | ||

| By Delivery Time Promise | Less than 30 Minutes | |

| 31-60 Minutes and More | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the quick commerce market in 2026?

The quick commerce market stands at USD 213.59 billion in 2026 and is forecast to reach USD 303.42 billion by 2031 at a 20.62% CAGR.

Which region leads global demand for instant delivery services?

Asia-Pacific led in 2025 with 39.34% share and is also the fastest-growing region with a 21.54% CAGR through 2031.

Which product category is expanding the fastest on quick commerce platforms?

Personal care and OTC pharma is the fastest-growing product category, projected to expand at 21.34% CAGR through 2031.

Why are 31-60 minute delivery windows gaining traction?

This tier is growing at 21.23% CAGR because it fits the economics of larger grocery operators and helps pure-play platforms expand into lower-density cities more efficiently.

What remains the main profitability challenge for operators?

Last-mile cost is still the biggest constraint, especially when basket values remain low and sub-30-minute delivery pushes logistics expenses well above slower delivery models.

Which companies are shaping competitive moves in 2025 and 2026?

Meituan, Blinkit, DoorDash, Talabat, Amazon Now, Instacart, and Gopuff are shaping competition through acquisitions, network expansion, AI deployment, and fresh funding activity.

Page last updated on: