United Kingdom Quick Commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

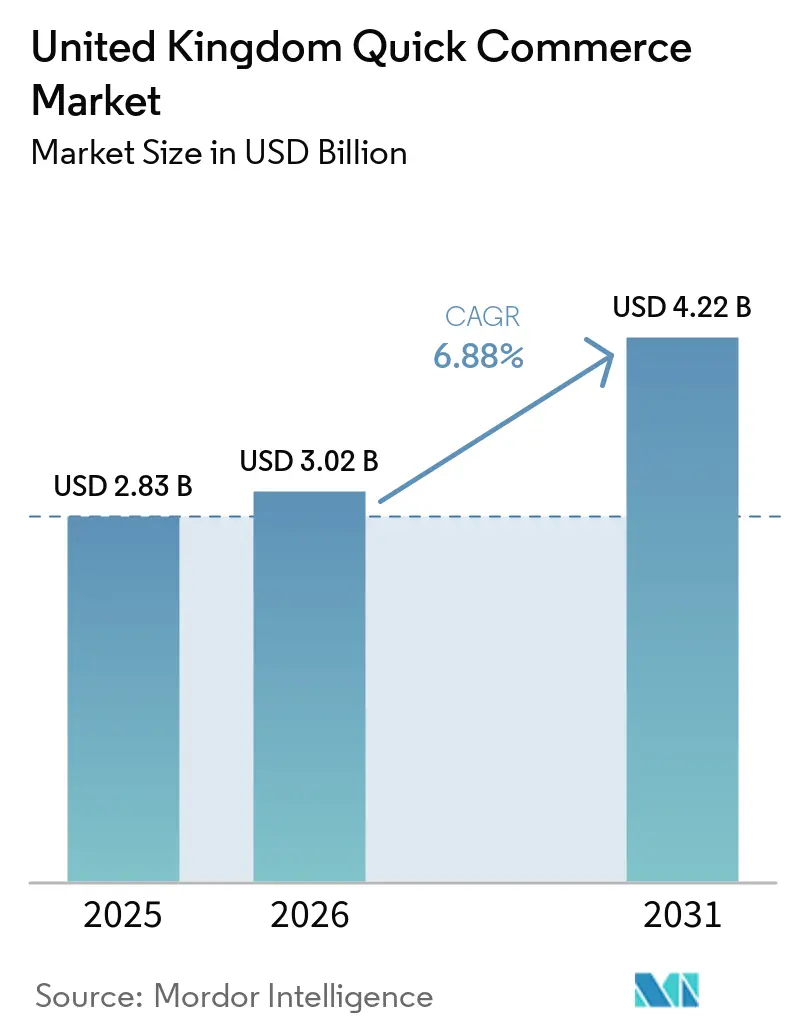

| Base Year Market Size (2025) | USD 2.83 Billion |

| Market Size (2026) | USD 3.02 Billion |

| Market Size (2031) | USD 4.22 Billion |

| Growth Rate (2026 - 2030) | 6.88% CAGR |

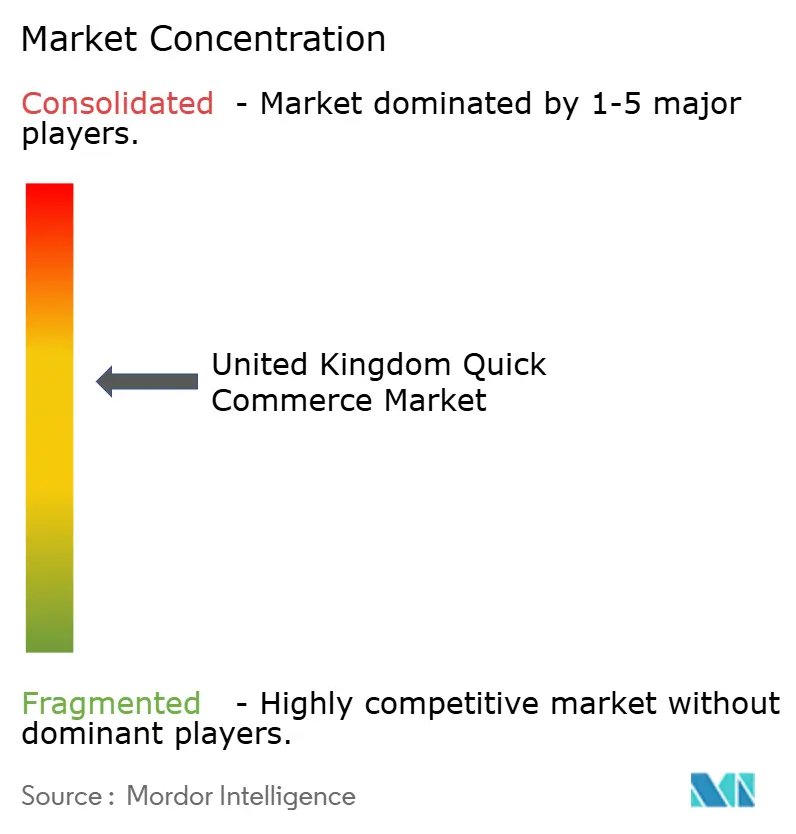

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Quick Commerce Market Analysis by Mordor Intelligence

The United Kingdom (UK) quick commerce market size was valued at USD 2.83 billion in 2025 and estimated to grow from USD 3.02 billion in 2026 to reach USD 4.22 billion by 2031, at a CAGR of 6.88% during the forecast period (2026-2031). The UK remained the third-largest e-commerce economy globally, and this scale helped quick commerce move from a venture-led experiment into an embedded retail channel. Consumer habits formed during the 2020-2021 lockdown period stayed in place through 2025, and repeat ordering became a stronger growth driver than first-time user addition. The channel is now being shaped by order-frequency growth, denser retailer-led fulfillment, and a broader use case that goes beyond emergency grocery purchases to routine top-up missions and selected non-food buying. Grocery-retailer-led fulfillment models give incumbent chains a clear structural advantage because they can use existing stores, supply chains, and labor networks instead of building fully dedicated dark-store estates from scratch. Even so, the United Kingdom quick commerce market still faces cost pressure from worker compliance rules, urban delivery charges, and packaging obligations, which means long-term gains will depend on reliability, route efficiency, and disciplined category expansion rather than subsidy-led share capture.

Key Report Takeaways

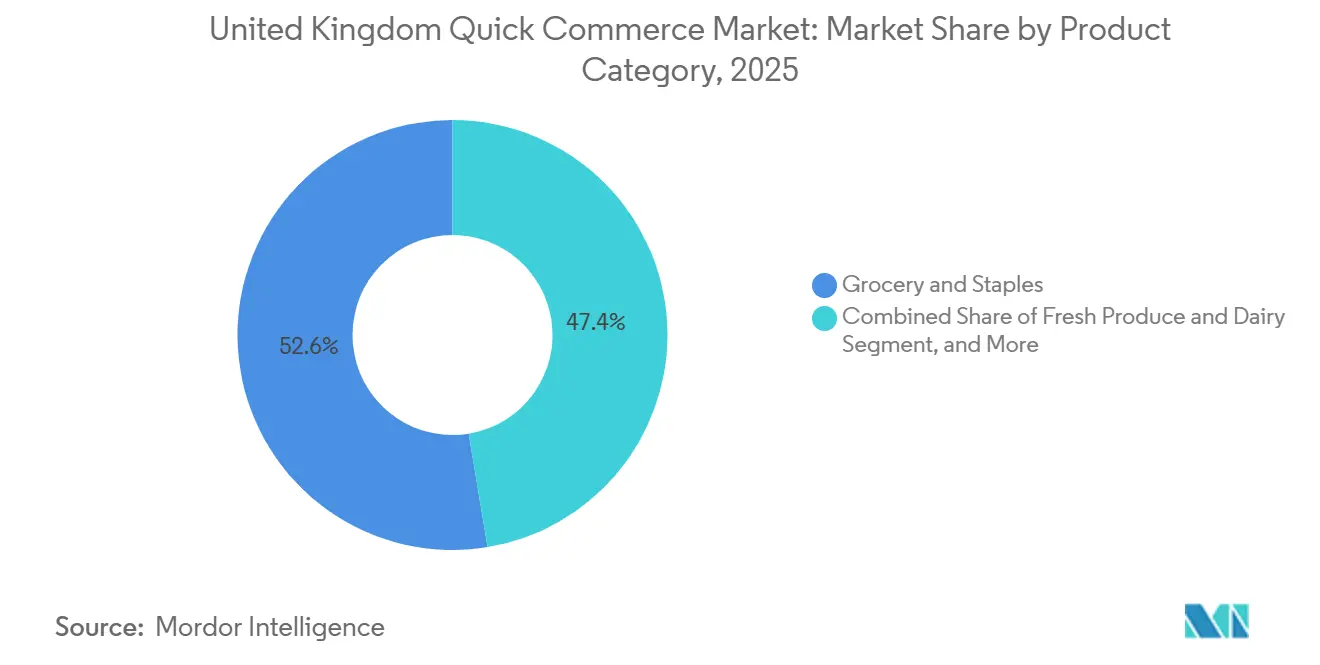

- By product category, Grocery and Staples held 52.61% of market value in 2025, while Electronics and Accessories is forecast to expand at a 7.10% CAGR through 2031.

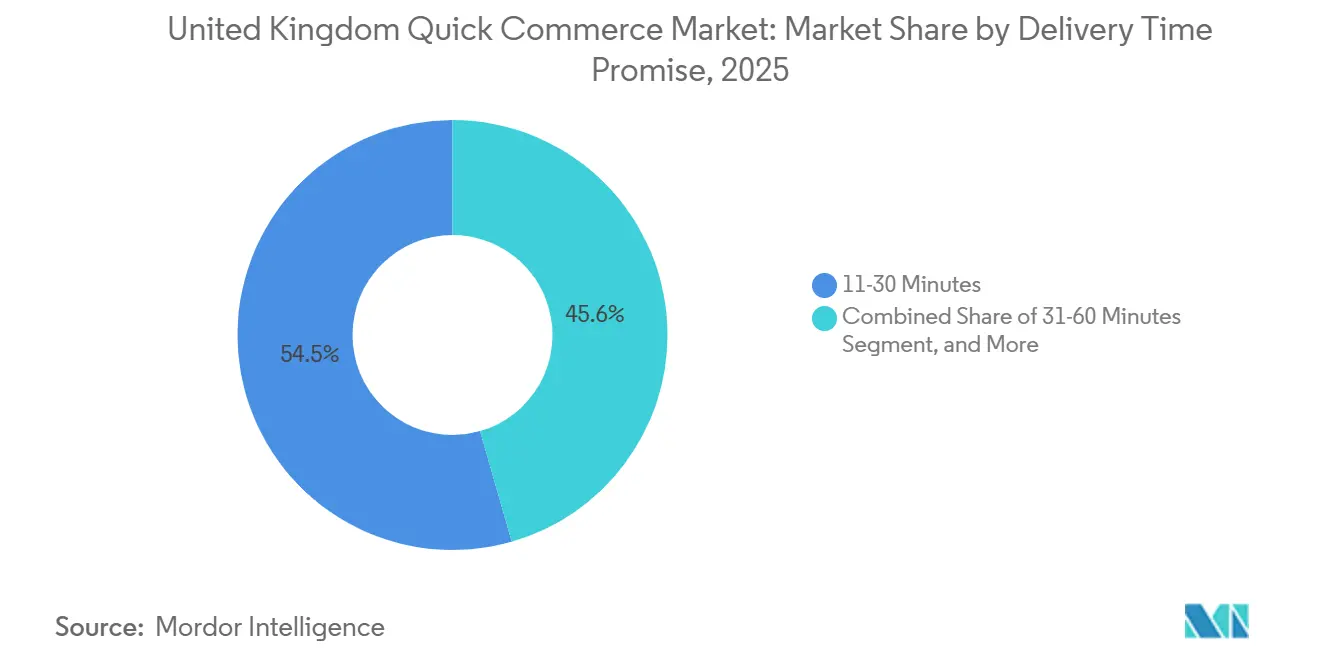

- By delivery time promise, the 11-30 Minutes segment accounted for 54.45% of market value in 2025, while the Less than 10 Minutes segment is projected to grow at a 7.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Quick Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Consumer Demand for Hyper-Convenience in Urban Centers | +1.5% | London, Manchester, Birmingham, with spillover to Leeds and Glasgow | Short term (≤ 2 years) |

| Expansion of Dark-Store Networks by Major Grocery Chains | +1.3% | Greater London core, expanding to Tier II metros | Medium term (2-4 years) |

| Integration of AI-Driven Demand Forecasting Reducing Stock-Outs | +1.1% | Platform operations with strongest deployment focus in the United Kingdom | Medium term (2-4 years) |

| Rising Penetration of 5G Smartphones Accelerating Mobile-First Ordering | +0.8% | Urban England and Northern Ireland, with slower progression in rural Scotland and Wales | Short term (≤ 2 years) |

| Venture Capital Infusion into Last-Mile Logistics Start-Ups | +0.4% | London-led expansion with wider national ambitions | Medium term (2-4 years) |

| Partnerships With Residential Real-Estate Operators for Lobby Micro-Fulfillment | +0.3% | Dense London boroughs, with early moves in Manchester and Leeds | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Demand For Hyper-Convenience In Urban Centers

Urban density remained the clearest demand driver for the UK quick commerce market, and that demand extended well beyond the narrow pandemic-user cohort. Survey work from March 2026 showed that 67% of British adults were aware of rapid grocery delivery services, while convenience at 47% and speed at 43% were the main reasons for use. The same survey also showed that 38% of active users were willing to switch providers for better delivery options, which points to service quality as a core retention lever. Usage widened across age groups as well, with Gen Z penetration reaching 66% in 2024, while the average basket value rose from GBP 30 (USD 38.4) to GBP 40 (USD 51.2) between 2021 and 2024. That change suggests that many shoppers now use the United Kingdom quick commerce market for planned convenience spending rather than one-off impulse orders. Co-op's goal of capturing close to one-third of the store-to-door rapid delivery space by 2027, supported by a GBP 1 million (USD 1.3 million) first-year investment in the Peckish platform, reflects that broader behavior shift across urban convenience retail.[1]Deliveroo plc, “Interim Financial Report H1 2025,” Deliveroo plc, dpd-12774-s3.s3.eu-west-2.amazonaws.com

Expansion Of Dark-Store Networks By Major Grocery Chains

The expansion of dark-store capacity by grocery incumbents is reshaping the United Kingdom quick commerce market through asset reuse rather than pure new-build rollout. Tesco's Whoosh service operated from 1,600 stores, including 180 large-format sites, and reached more than 70% of United Kingdom households by early 2026, while sales rose 47% year over year in the 19 weeks ending January 3. This model is structurally important because store-based rapid fulfillment avoids the annual lease burden of a standalone dark store, which the input placed at more than GBP 500,000 (USD 640,000). Amazon also moved more decisively into this model when it launched Amazon Now from a purpose-built Southwark dark store in January 2026 and then added Battersea and Lewisham while securing at least 4 more sites. Tesco's acquisition of 5 former Amazon Fresh sites after Amazon shut all 14 of its United Kingdom Fresh stores in September 2025 showed how quickly physical assets can be recycled across competing retail networks. The result is a planning environment in which existing retailers can scale faster and with less regulatory friction than pure-play operators that still need separate change-of-use approvals.

Integration Of AI-Driven Demand Forecasting Reducing Stock-Outs

Artificial intelligence moved from trial use to operating infrastructure across the UK quick commerce market during 2025 and 2026. Iceland Foods completed the rollout of Invent.ai's forecasting and replenishment platform across all SKUs and more than 1,000 stores and distribution centers in April 2026, with the system using seasonality, promotions, new launches, and one-off events to improve replenishment decisions.[2]Invent.ai, “Iceland Partners With Invent.ai to Transform Inventory and Replenishment Operations,” Invent.ai, invent.ai Waitrose also expanded AI-led forecasting through Blue Yonder, and the approach brought local store behavior and seasonal demand into stock planning, which supports better order accuracy for rapid delivery. This matters because reliability is becoming as important as speed in the United Kingdom quick commerce market, especially when a missing item can disrupt a full top-up order. The operators that can hold strong SKU-level visibility are better placed to sustain the 8-plus orders per rider-hour that support viable economics in dense areas. Ocado's on-grid fulfillment benchmark of more than 30 million processed items in 2024, 99.7% order accuracy, and pick latency below 2 seconds showed why technology depth remains a durable competitive edge.

Rising Penetration Of 5G Smartphones Accelerating Mobile-First Ordering

The growth of 5G has started to shape buying behavior in the United Kingdom quick commerce market rather than just support network access. As of July 2025, 5G accounted for 28% of all United Kingdom mobile connections, up 9 percentage points from a year earlier, while urban areas recorded 29% 5G connection rates compared with 19% in rural locations. Full 5G standalone coverage from at least one mobile network operator reached 83% of the country, and outdoor 5G coverage from at least one operator reached 97% in 2025.[3]Ofcom, “Nations Report 2025,” Ofcom, ofcom.org.uk Mobile commerce accounted for 61.9% of United Kingdom e-commerce value in 2024, which shows how strongly shoppers already default to smartphone-based purchasing for routine and urgent needs. Lower latency and faster loading matter in the United Kingdom quick commerce market because time-sensitive orders are more exposed to app drop-off and checkout abandonment than standard e-commerce baskets. Better mobile connectivity also improves live inventory visibility between the app and the fulfillment point, which lowers the risk of cancellations caused by stock mismatches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Burn Rates and Path-to-Profitability Challenges | -1.2% | National, affecting all platform models operating in the United Kingdom | Short term (≤ 2 years) |

| Regulatory Uncertainty Around Gig-Worker Employment Status | -0.9% | National, with stronger enforcement exposure in London and major cities | Medium term (2-4 years) |

| Rising Urban Congestion Charges Increasing Delivery Costs | -0.7% | Greater London core, with spillover to clean air charging zones in other cities | Short term (≤ 2 years) |

| Consumer Backlash Against Single-Use Packaging Waste | -0.4% | National, with earlier adoption in London, Bristol, and Edinburgh | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Burn Rates And Path-To-Profitability Challenges

Profitability remains one of the clearest operating constraints on the United Kingdom quick commerce market, even after the most aggressive subsidy phase faded. Gopuff's United Kingdom business reduced its pre-tax loss from GBP 93.8 million (USD 120.1 million) to GBP 51.6 million (USD 66.0 million) in 2023, while revenue rose from GBP 42.8 million (USD 54.8 million) to GBP 78.1 million (USD 100 million), yet cumulative losses since entry still exceeded GBP 187 million (USD 239.4 million). Deliveroo showed the other side of the picture when it recorded its first full year of profitability in 2024, with GBP 2.9 million (USD 3.7 million) profit on GBP 7.4 billion gross transaction value. That result came mainly from better stacked-order efficiency and lower marketing spend, rather than from a broad margin reset in rapid grocery. Platform margins also remain under pressure because large grocery partners can negotiate harder on commissions as they scale. In less dense parts of the United Kingdom quick commerce market, breakeven still depends on maintaining 8 or more orders per rider-hour, and that threshold remains difficult to protect when order density weakens.

Regulatory Uncertainty Around Gig-Worker Employment Status

Worker classification remains one of the biggest policy risks facing the United Kingdom quick commerce market. The legal backdrop was already shaped by the Uber BV v Aslam ruling, and the government increased pressure in January 2025 by warning gig operators about worker misclassification. The Home Office then opened a consultation in October 2025 to extend mandatory right-to-work checks to gig-economy and zero-hours workers, including delivery riders, and the proposal closed in December 2025. The associated impact assessment placed the business cost at GBP 90 million (USD 115.2 million) in present value over 10 years, while individual check costs ranged from GBP 1.79 (USD 2.3) to GBP 8.32 (USD 10.6) depending on verification method. Non-compliance penalties can reach GBP 60,000 per illegal worker, which adds direct financial risk to labor-intensive platform models. The wider concern is that added documentation burdens may reduce rider availability during evening and weekend peaks, which would hurt service reliability at the exact points when customer demand is strongest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Non-Food Verticals Are Expanding Faster Than Core Grocery

Grocery and Staples accounted for 52.61% of the United Kingdom quick commerce market share in 2025, which confirmed that emergency and top-up grocery missions still formed the core demand base. Electronics and Accessories is the fastest-growing product segment in the United Kingdom quick commerce market, with a projected 7.10% CAGR from 2026 to 2031. That growth reflects a change in purchase behavior as urban consumers increasingly apply instant-delivery expectations to chargers, earphones, and other small but high-urgency items. Deliveroo said its retail proposition added around 2,000 partner sites in 2024, and the retail vertical delivered double-digit gross transaction value growth in the second half of the year. Personal Care and OTC Pharma also gained momentum as Boots expanded its on-demand service through Deliveroo and Uber Eats to 500 United Kingdom stores by September 2025 and offered more than 10,000 products with delivery times as short as 30 minutes.

Fresh Produce and Dairy, Snacks and Beverages, and Home and Cleaning Supplies continued to add meaningful volume around the grocery core of the United Kingdom quick commerce market. These categories work well because they can be picked within the same pathways as staple grocery orders, which helps lift average basket value without the same level of extra cost. Pet Care and Flowers and Gifts stayed smaller in scale, but both serve a useful role because they carry stronger margins and lower return rates than many other non-food categories. Pet Care is especially relevant because recurring replenishment patterns can support better customer lifetime value and stronger repeat behavior. Procurement and fulfillment standards for fresh categories also continued to matter more as operators tried to protect quality while expanding the category mix.

By Delivery Time Promise: The 11-30 Minutes Window Remains The Economic Core

The 11-30 Minutes window accounted for 54.45% of the United Kingdom quick commerce market size in 2025, which shows that the mainstream service proposition still sits in the sub-hour range rather than at the extreme end of instant delivery. This window matches the practical efficiency frontier because a dark store serving an average 1.8-kilometer rider radius in a dense urban setting can support around 8 deliveries per rider-hour. The Less than 10 Minutes segment is still the fastest-moving part of the United Kingdom quick commerce market and is projected to expand at a 7.22% CAGR through 2031. That momentum is tied to robotic picking systems that can reduce assembly time from 2-5 minutes to less than 90 seconds. It is also tied to AI routing tools that have reduced estimated delivery-time variance from 7 minutes to 3 minutes on optimized routes.

The 31-60 Minutes and More segment grew more slowly, but it did not lose relevance within the United Kingdom quick commerce market. Tesco Whoosh broadened the use case for this window in October 2025 when it introduced full-basket scheduled same-day delivery through car and van courier partners. Amazon Now also entered London with a stated 30-minute promise, which reinforces sub-hour delivery as the entry point for wider grocery adoption rather than a niche premium offer. Cost pressure still matters in this tier because Transport for London raised the Congestion Charge to GBP 18 (USD 23.0) per day from January 2, 2026, which strengthened the case for electric cargo bikes and micro-hubs that avoid central-zone vehicle exposure.

Geography Analysis

In 2025, Tier I metros accounted for a significant portion of the market value, underscoring the United Kingdom's quick commerce market's reliance on urban hubs, particularly London. London's dominance stemmed from its high population density, affluent inner-boroughs, and a robust delivery infrastructure established in recent years. The city boasted a confluence of delivery networks, including DoorDash, Deliveroo, Uber Eats, Gopuff, Amazon Now, Tesco Whoosh, and Zapp, offering consumers unparalleled delivery choices. Amazon Now's expansion from Southwark to Battersea and Lewisham in early 2026 emphasized London's role as the trendsetter for new operational models.

From now until 2031, major cities in England and Scotland, excluding London, are poised to drive the expansion of the UK's quick commerce market. Cities like Birmingham, Manchester, Leeds, Sheffield, and Bristol are emerging as the next competitive hotspots, striking a favorable balance between urban density and operational ease, unlike central London. Morrisons Now demonstrated that supermarket-led rapid fulfillment can thrive in Tier II areas, utilizing its store network for nationwide one-hour delivery, sidestepping the dark-store challenges of the capital. Co-op, with its extensive convenience store network, expanded its online grocery access to target a majority of the UK population. By early 2026, Tesco Whoosh had extended its services to a substantial portion of households, indicating that in these cities, the challenge lies more in achieving sufficient order density for rider operations than in coverage.

While Northern Ireland boasted widespread outdoor 5G coverage from at least one operator in 2025, Wales lagged significantly, highlighting the uneven digital readiness in the UK's quick commerce landscape. Scotland is emerging as a key investment hub, evident from Aldi's significant 2025 initiative, which incorporated micro-fulfillment and e-cargo bike trials into a broader convenience strategy. Urban density outside Cardiff remains sparse, suggesting a slower pace for Wales. However, the platform-aggregator model offers a viable entry into Welsh towns via established supermarket outlets. The current geographic trend indicates a market still anchored by London, yet increasingly bolstered by retailer-led expansions in regional cities and their surrounding areas.

Competitive Landscape

The United Kingdom quick commerce market is moving from a fragmented venture-led phase into a more concentrated structure shaped by grocery incumbents, multi-vertical platforms, and a small group of dark-store specialists. Tesco, Co-op, Sainsbury's, and Morrisons represent the retailer-led group, while DoorDash and Deliveroo, Uber Eats, and Just Eat represent the multi-vertical platform layer. Gopuff, Zapp, and Amazon Now make up the specialist or hybrid end of the field, although each is pursuing a different operating model. The exit of Getir in April 2024 and the earlier wind-down of Gorillas reduced fragmentation and shifted available demand toward operators with stronger balance sheets and broader infrastructure.

Consolidation accelerated in October 2025 when DoorDash completed its GBP 2.9 billion (USD 3.7 billion) acquisition of Deliveroo, combining Deliveroo's rider network of around 130,000 in the United Kingdom with DoorDash's dispatch and machine-learning capabilities. Deliveroo's 2024 report also showed a 50% year-over-year improvement in stacking efficiency and a 3% reduction in rider wait time, which suggests that technology and operating discipline matter as much as raw scale in the United Kingdom quick commerce market. Tesco took a different route by using store-based fulfillment and expanding Whoosh to 1,600 stores, which let it extend reach without taking on the full fixed-cost burden of a dedicated dark-store model. Gopuff signaled another strategic path when it raised USD 250 million in November 2025 to support AI, consumer experience, and infrastructure expansion rather than pure discount-led growth. Zapp took the opposite stance by narrowing its focus to premium customers in affluent inner-London zones.

The main white-space opportunities in the United Kingdom quick commerce market now sit in Tier III cities, higher-margin non-food categories such as pharmacy and electronics, and retail media monetization. Smaller operators that cannot consistently hit the 8-orders-per-rider-hour threshold remain under pressure to partner, consolidate, or leave. Compliance burdens from packaging rules, labor checks, and urban road charging could reinforce the advantage of grocery incumbents because those companies already have broader compliance systems in place. This leaves the United Kingdom quick commerce market more consolidated than it was during the subsidy era, but still open enough for differentiated operators to grow if they control costs and protect service quality.

United Kingdom Quick Commerce Industry Leaders

Gopuff

Deliveroo plc (Hop)

Tesco plc (Whoosh)

Zapp

Amazon.com Inc. (Amazon Fresh)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Amazon launched Amazon Now dark stores in Battersea and Lewisham, London, with at least 4 additional UK sites secured, offering 30-minute grocery and household essentials delivery, the service operates across 35 product categories and is available to both Prime and non-Prime customers, signaling Amazon's recommitment to a dark-store fulfillment model after closing its Amazon Fresh physical stores.

- April 2026: Iceland Foods completed the rollout of Invent.ai's AI forecasting and replenishment platform across all SKUs and 1,000-plus UK stores and distribution centers, automating replenishment decisions in real time, the system incorporates seasonality, promotions, and one-off event variables, with the stated objective of minimizing stockouts and reducing lost sales.

- February 2026: Tesco's Whoosh rapid delivery service reported a 47% year-on-year sales increase in the 19 weeks ending January 3, 2026, attracting over 250,000 new customers, the service operates from 1,600 UK stores and now reaches more than 70% of UK households via partners including Uber Eats, Just Eat Go, and Stuart.

- January 2026: London's Congestion Charge increased from GBP 15 (USD 19.2) to GBP 18 (USD 23.0) per day effective January 2, 2026, the first increase since 2020, with the pre-existing EV exemption replaced by a 50% discount for electric vans registered for Auto Pay, directly increasing last-mile delivery operating costs for all platforms serving central London.

United Kingdom Quick Commerce Market Report Scope

The Quick Commerce Market in the United Kingdom is experiencing significant growth, driven by companies specializing in ultra-fast delivery services. These businesses primarily focus on fulfilling online orders for groceries, convenience items, and household essentials, often delivering within a timeframe of less than 30 minutes.

The United Kingdom Quick Commerce Market Report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care, Home Supplies, Electronics, Pet Care, and Flowers and Gifts), Delivery Time Promise (Less Than 10 Minutes, 11-30 Minutes, and 31-60 Minutes). The Market Forecasts are in Value (USD).

| Grocery and Staples |

| Fresh Produce and Dairy |

| Snacks and Beverages |

| Personal Care and OTC Pharma |

| Home and Cleaning Supplies |

| Electronics and Accessories |

| Pet Care |

| Flowers and Gifts |

| Other Product Categories |

| Less than 10 Minutes |

| 11-30 Minutes |

| 31-60 Minutes and More |

| By Product Category | Grocery and Staples |

| Fresh Produce and Dairy | |

| Snacks and Beverages | |

| Personal Care and OTC Pharma | |

| Home and Cleaning Supplies | |

| Electronics and Accessories | |

| Pet Care | |

| Flowers and Gifts | |

| Other Product Categories | |

| By Delivery Time Promise | Less than 10 Minutes |

| 11-30 Minutes | |

| 31-60 Minutes and More |

Key Questions Answered in the Report

What is the current and forecast value of the United Kingdom quick commerce market?

The United Kingdom quick commerce market was valued at USD 2.83 billion in 2025, is estimated at USD 3.02 billion in 2026, and is projected to reach USD 4.22 billion by 2031 at a 6.88% CAGR.

Which product category leads sales in rapid delivery across the United Kingdom?

Grocery and Staples remained the largest category with a 52.61% value share in 2025, which shows that top-up and emergency grocery missions still anchor demand.

Which delivery window is growing the fastest in the United Kingdom?

Less than 10 Minutes is the fastest-growing delivery promise, with a projected 7.22% CAGR through 2031, even though 11-30 Minutes remains the largest segment by current value.

Why are grocery retailers gaining an edge over pure-play operators?

Large chains can use existing stores, supply chains, and labor systems as fulfillment infrastructure, which lowers fixed costs and supports wider coverage than dark-store-only models.

What are the main risks facing rapid delivery operators in the United Kingdom?

The biggest risks are worker compliance costs, path-to-profitability pressure, urban road charges, and packaging regulation, all of which can squeeze already thin per-order margins.

Page last updated on: