France Quick Commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

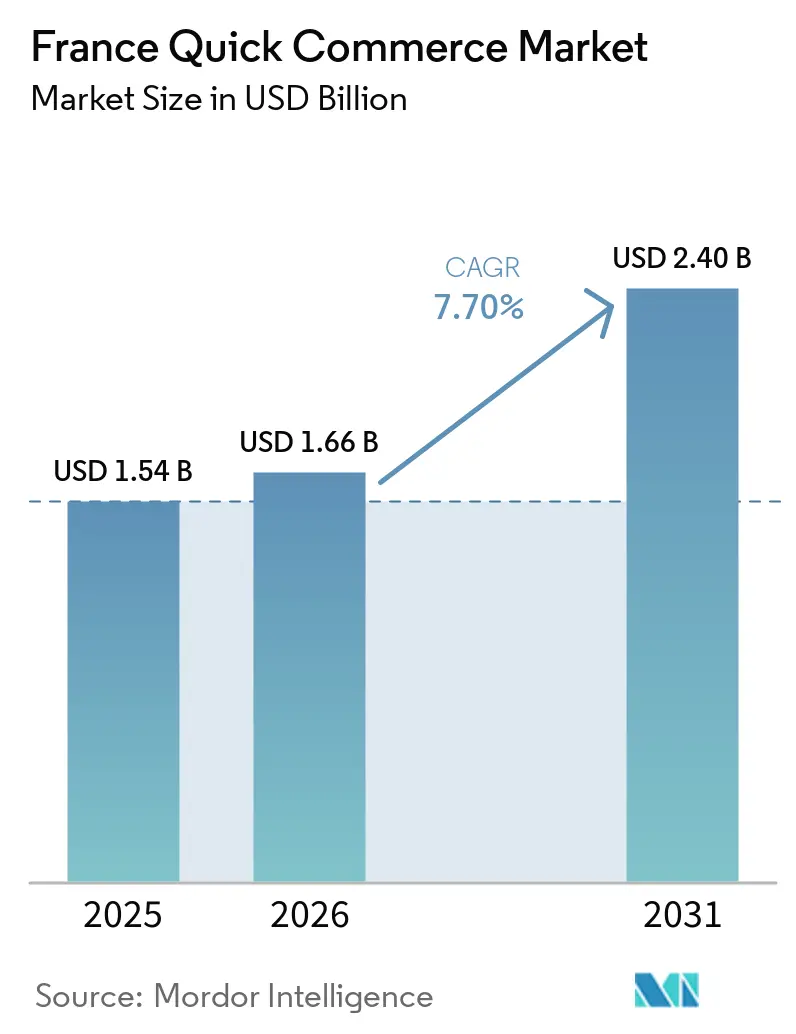

| Base Year Market Size (2025) | USD 1.54 Billion |

| Market Size (2026) | USD 1.66 Billion |

| Market Size (2031) | USD 2.40 Billion |

| Growth Rate (2026 - 2031) | 7.70% CAGR |

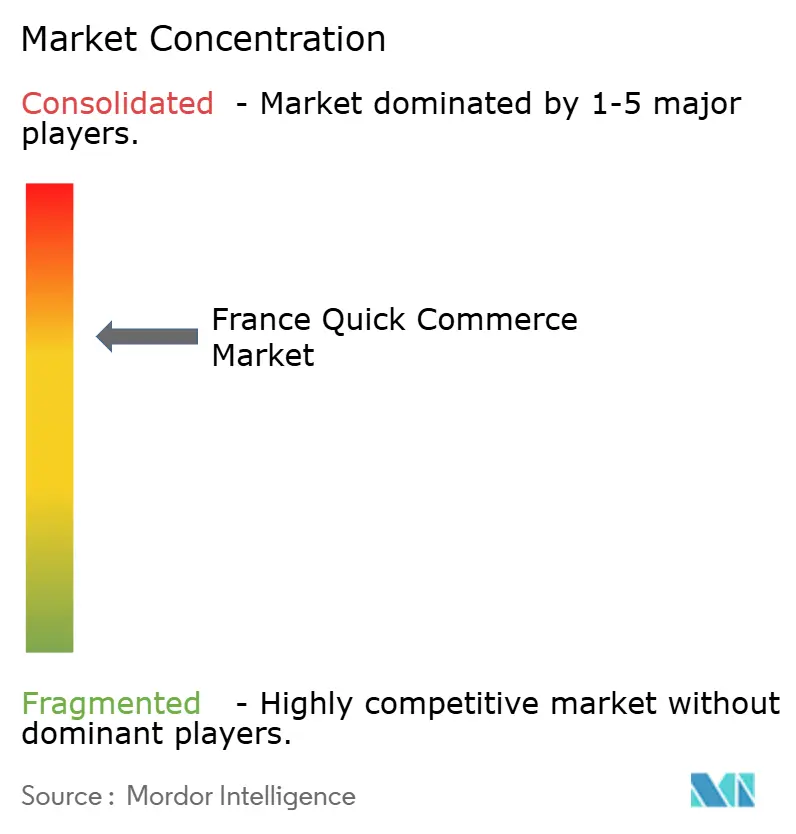

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Quick Commerce Market Analysis by Mordor Intelligence

The France quick commerce market size is expected to increase from USD 1.54 billion in 2025 to USD 1.66 billion in 2026 and reach USD 2.40 billion by 2031, growing at a CAGR of 7.7% over 2026-2031. A wave of exits by venture-funded pure-plays during 2023-2024 re-shaped the competitive field as traditional grocery chains and multi-category delivery platforms absorbed demand. Regulatory clarification that re-classified urban dark stores as warehouses, combined with persistent inflation and rising last-mile costs, tilted scale advantages toward retailers that already own real estate and inventory. Partnerships between Carrefour, Casino, Monoprix, Auchan, and leading platforms have become the dominant operating model, while Amazon’s January 2026 tie-up with Chronodrive signals deeper integration of retailer stock files with third-party logistics. Inflation of 2.7% year-on-year in April 2026 has placed fresh emphasis on operational efficiency and minimum-order thresholds, yet consumer willingness to pay premiums for emergency items continues to underpin demand for ultra-fast fulfillment.

Key Report Takeaways

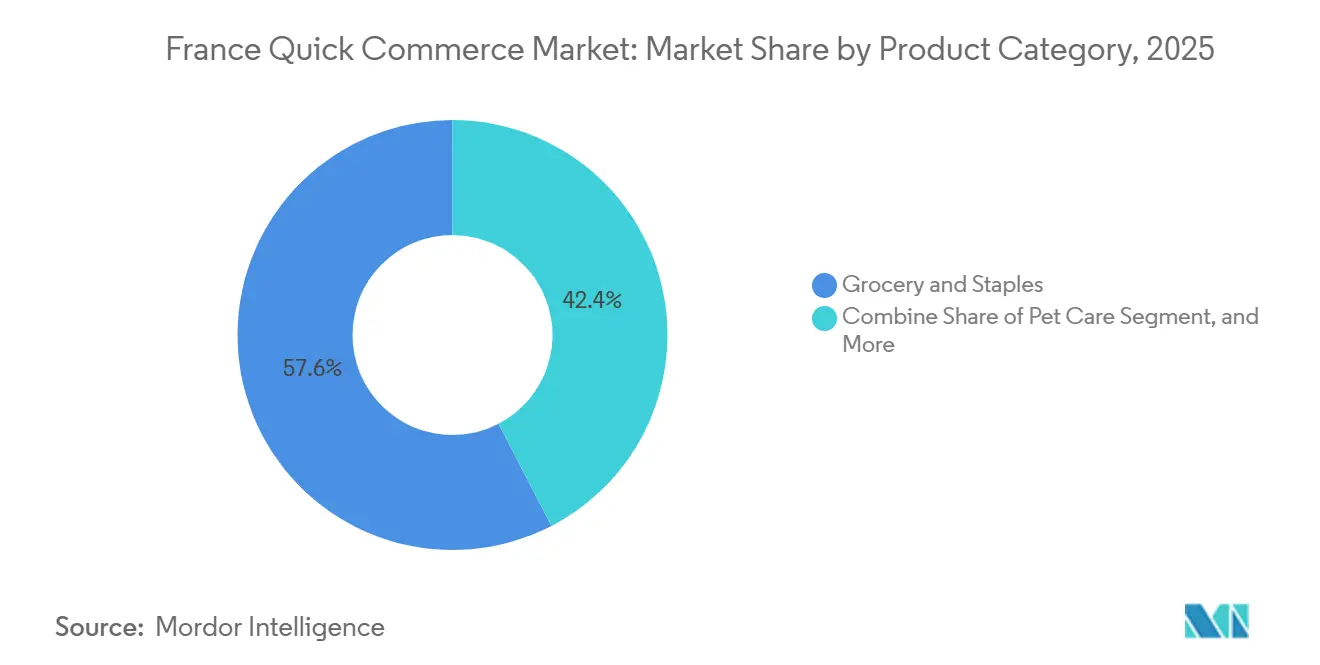

- By product category, Grocery and Staples accounted for 57.61% of the France quick commerce market share in 2025, whereas Pet Care is advancing at a 7.96% CAGR through 2031.

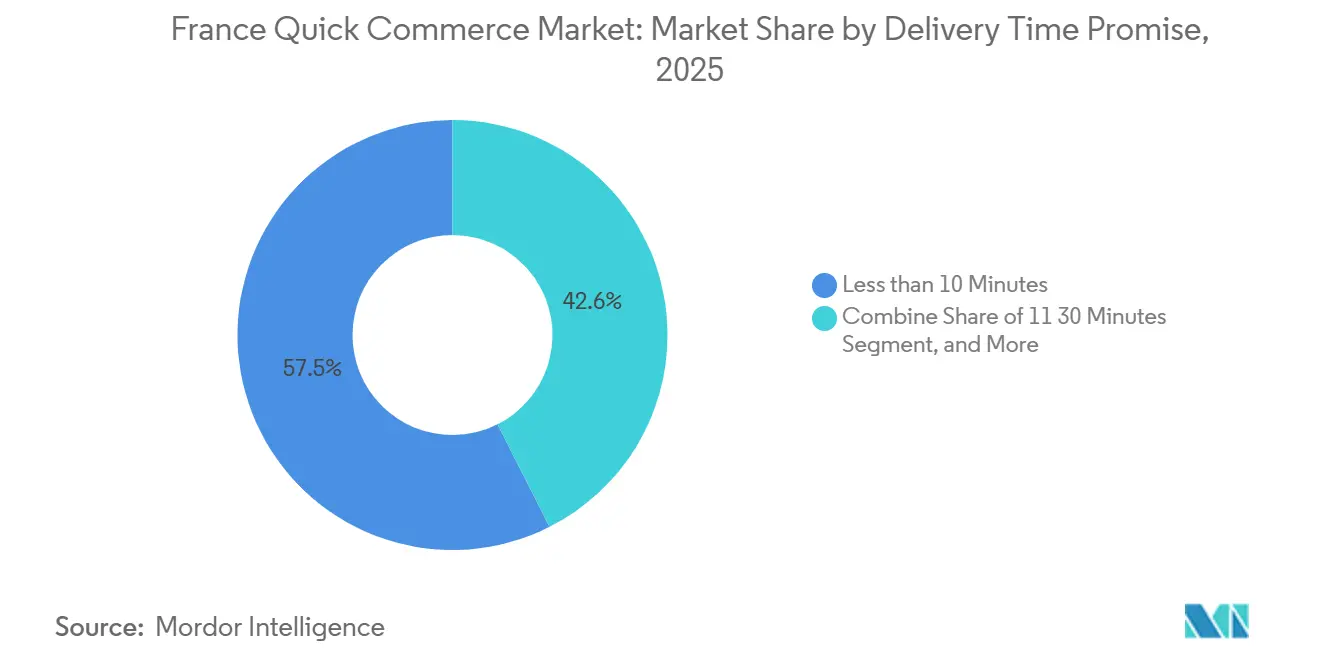

- By delivery time promise, the 11-30 Minutes window led with 57.45% revenue share in 2025, while the Less than 10 Minutes tier is projected to expand at an 8.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Quick Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Consumer Demand for Ultrafast Delivery Convenience | +2.1% | National focus on Paris, Lyon, Marseille, Bordeaux, Toulouse | Short term (≤ 2 years) |

| Expansion of Dark Store Networks Across Major French Cities | +1.4% | Tier I metros and early Tier II hubs | Medium term (2-4 years) |

| Integration of AI-Driven Demand Forecasting to Reduce Spoilage | +1.2% | Île-de-France and Auvergne-Rhône-Alpes lead | Medium term (2-4 years) |

| Rising Partnerships Between Quick Commerce and Traditional Retailers | +1.8% | National retailer networks | Short term (≤ 2 years) |

| Regulatory Incentives for Electric Cargo Bike Adoption in Urban Logistics | +0.9% | Paris, Lyon, Marseille, Toulouse | Long term (≥ 4 years) |

| Increasing Penetration of Mobile Wallet Payments Among Gen Z Consumers | +0.8% | Urban centers nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Demand For Ultrafast Delivery Convenience

Time-pressed households in dense French cities increasingly choose speed over price when purchasing everyday goods, an effect reinforced by mobile wallet adoption that exceeds 82% among 16-24-year-olds. DPD’s 2025 Baromètre showed 37% of shoppers abandon online baskets if delivery windows appear lengthy, validating the value that rapid fulfillment adds to the France quick commerce market. Uber Eats now reaches 530-plus agglomerations, proving that demand for near-instant delivery is no longer restricted to Paris-Lyon-Marseille but extends into midsized towns where courier density can still support sub-30-minute service.

Expansion Of Dark Store Networks Across Major French Cities

After a regulatory reset in 2023 classified dark stores as warehouses, retailers began integrating micro-fulfillment zones within existing stores to comply with zoning while preserving speed. Carrefour’s Sprint format and Monoprix’s 200-store Uber Eats network illustrate how compliant dark-store-in-store models sustain the France quick commerce market without fresh real-estate outlays.[1]Conseil d’État, “Ruling on Dark Store Classification,” conseil-etat.fr Picnic’s planned Q4 2026 launch in Lyon further confirms that disciplined dark-store deployment remains viable when aligned with municipal plans and anchored in positive unit economics.

Integration Of AI-Driven Demand Forecasting To Reduce Spoilage

Chronodrive cut perishables waste by 8% and saved USD 0.79 million annually after installing AI forecasting that links weather, local events, and sales data, directly lifting gross margins. Carrefour’s adoption of smart-shelf labels delivers real-time inventory visibility, a critical enabler of profitable rapid delivery, and underscores how predictive analytics is becoming table-stakes for players that expect sustained participation in the France quick commerce market.[2]Auchan Retail, “Chronodrive AI Demand Forecasting Case Study,” auchan.fr

Rising Partnerships Between Quick Commerce And Traditional Retailers

Retailer-platform alliances such as Carrefour-Uber Eats and Amazon-Chronodrive sidestep the capital burden of standalone courier fleets by fusing existing store inventory with marketplace logistics. Amazon’s nationwide 2-hour service launched in January 2026 demonstrates that hybrid models can achieve national reach immediately, challenging pure online grocers and reinforcing retailer dominance inside the France quick commerce market. These partnerships are fluid; Picnic’s 2025 switch from Système U to Intermarché shows suppliers compete fiercely for platform volume.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Profitability Challenges Due to High Last-Mile Costs | -1.6% | National, acute in Tier II-Tier III markets | Medium term (2-4 years) |

| Intensifying Municipal Restrictions on Urban Micro-Warehouses | -1.3% | Paris, Lyon, Marseille, Bordeaux, Toulouse | Short term (≤ 2 years) |

| Shortage of Qualified Delivery Riders in Smaller Cities | -0.7% | Tier II-Tier III and rural peripheries | Long term (≥ 4 years) |

| Consumer Price Sensitivity Amid Inflationary Pressures | -1.1% | Nationwide middle-income segment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Profitability Challenges Due To High Last-Mile Costs

Courier wages averaging EUR 17 (USD 19) per hour translate into USD 4.80-7.68 per drop when riders only complete three deliveries hourly. With typical delivery fees sitting below USD 2.30, most operators run sustained losses, and four venture-funded entrants shut down between 2023-2024. Survivors now impose higher order minimums and stretch windows to 2 hours to batch drops, yet profitability outside dense metros remains elusive, limiting expansion of the France quick commerce market.[3]UFC-Que Choisir, “Inflation Monitor April 2026,” quechoisir.org

Intensifying Municipal Restrictions On Urban Micro-Warehouses

In 2023, Paris implemented significant measures to regulate dark stores, initiating 25 enforcement actions that resulted in the closure or conversion of approximately 80% of these ultra-fast delivery hubs. These actions followed the enactment of Decree n°2023-195, which granted French cities the authority to reclassify dark stores as warehouses. This regulatory shift has had a profound impact on the quick commerce landscape in France. Similarly, Lyon and Marseille have adopted comparable regulations, which have strengthened the position of established grocers operating compliant storefronts. These measures have effectively raised capital barriers for potential new entrants, thereby limiting competition and slowing the spatial expansion of the quick commerce market in France.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Grocery Staples Lead, Pet Care Accelerates

Grocery and Staples held 57.61% revenue in 2025, acting as the trip-builder for cross-selling higher-margin items that lift the overall French quick commerce market size at the basket level. Fresh Produce and Dairy contributes rising turnover as consumers shift from weekly stock-ups to daily top-ups for perishables, leveraging the channel’s same-day freshness. Snacks and Beverages thrive on impulse demand, while Personal Care and OTC Pharma benefit from the willingness to pay premiums to avoid late-night pharmacy trips. Electronics, Flowers and Gifts, and other niche categories command smaller shares but deliver superior margins because customers value immediate gratification.

Pet Care is forecast to grow at a 7.96% CAGR, the strongest of any category, driven by subscription models for recurrent deliveries and rising preference for premium local pet food. Zooplus’ February 2026 purchase of JMT pushed combined turnover over USD 169 million and underscored consolidation momentum. The France quick commerce market share attributable to Pet Care is set to widen as owners increasingly treat pets as family and accept higher delivery fees for reliable just-in-time supply.

By Delivery Time Promise: 11-30 Minutes Balances Scale And Cost

The 11-30 Minutes delivery window is projected to contribute 57.45% of the 2025 market value, primarily due to its ability to facilitate multi-order batching. This operational efficiency enables couriers to maintain productivity levels exceeding three deliveries per hour. Leading players such as Carrefour Sprint, Uber Eats, and Deliveroo have aligned their strategies within this time frame to ensure economic sustainability while preserving the core value proposition of quick delivery services.

The Less than 10 Minutes delivery segment, although currently representing a smaller share of the market, is anticipated to experience the fastest growth, with a compound annual growth rate (CAGR) of 8.10%. Market operators are repositioning this segment as a premium service tier, targeting time-sensitive needs such as forgotten dinner ingredients or critical baby products. Delivery fees within this segment, ranging from USD 6 to USD 9, are structured to offset the additional labor costs required for ultra-fast fulfillment. This pricing strategy supports the growth of the quick commerce market in France, enabling expansion in the ultra-fast delivery segment without the need for significant discounting, thereby ensuring long-term market sustainability.

Geography Analysis

Paris and the wider Île-de-France captured the bulk of 2025 sales, leveraging 12.3 million residents, high disposable income, and the legacy footprint of early dark stores. After legal reclassification, Carrefour, Monoprix, and Franprix quickly re-purposed storefronts into micro-fulfillment nodes that align with zoning codes, ensuring the France quick commerce market remains robust even as pure-plays exit. Monoprix covers every arrondissement with 1-hour delivery on baskets above EUR 60 (USD 70.54), while Franprix offers zero-fee service on orders over EUR 50 (USD 58.79).

Lyon, Marseille, Bordeaux, and Toulouse anchor Tier II momentum. Picnic’s Q4 2026 entry into Lyon and Uber Eats’ penetration of more than 530 agglomerations showcase a pivot from density to breadth that is widening the France quick commerce market. Low-emission-zone incentives of up to USD 2,486 per electric cargo bike, funded jointly by Paris and national programs, lower operating costs and align sustainability goals with growth targets.

Smaller cities and rural belts remain restrained by weaker courier supply and consumer preference for drive-through pick-up. Yet DPD survey data confirm that 95% of shoppers still chase free-shipping thresholds, suggesting latent demand is present once service levels align with price expectations. As store networks densify and logistics software improves routing, the France quick commerce market is expected to extend deeper into lower-density areas over the long run.

Competitive Landscape

Following the withdrawal of Getir, Gorillas, Flink, and Gopuff during 2023-2024, the French quick commerce market has witnessed a significant shift in leadership. Prominent players such as Carrefour, Casino, Monoprix, Auchan, E.Leclerc, and Intermarché have emerged as key competitors, each leveraging partnerships with Uber Eats or Deliveroo to strengthen their market presence. Carrefour, in particular, has demonstrated its operational scale, with its network of 830 stores processing over 1 million orders within a single quarter. This achievement highlights the critical role that established grocers play in shaping the dynamics of the quick commerce market in France. Furthermore, Amazon's national launch of Chronodrive in January 2026 introduced a robust two-hour delivery service, further intensifying competition and raising the stakes for market participants.

Technology-driven innovations and strategic partnerships remain central to the competitive strategies employed by market players. For instance, Chronodrive's implementation of artificial intelligence (AI) to minimize spoilage has resulted in annual savings of nearly USD 0.79 million, which can be redirected toward further investments. Similarly, Carrefour's deployment of smart shelves provides real-time inventory data, enabling dynamic pricing strategies that enhance operational efficiency.

Meanwhile, niche platforms such as Kwez and Picky are capitalizing on localized differentiation by offering curated product assortments and delivery services within less than an hour. Additionally, bouquet specialists like LAMOU PARIS and Florajet have successfully monetized the urgency associated with gifting by charging premium rates for their services. Municipal zoning regulations, which restrict the conversion of new warehouses, inherently benefit established players with compliant storefronts. This regulatory environment contributes to a moderately concentrated yet highly competitive quick commerce market in France, where incumbents leverage their existing infrastructure to maintain a competitive edge.

France Quick Commerce Industry Leaders

Getir France SAS

Carrefour SA (Carrefour Sprint)

Gopuff (incl. Dija legacy)

Flink SE (incl. Cajoo)

Frichti SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: In Spain, Carrefour and Just Eat have ramped up their collaboration, now promising a swift 30-minute delivery for 4,500 Carrefour products. This move underscores the adaptability of the successful French collaboration model. Both companies view this expansion as a tactical step to bolster their e-commerce footprint, aiming to deliver groceries more swiftly and conveniently.

- April 2026: Deliveroo France and Uber Eats faced a labor complaint alleging exploitation of riders, highlighting ongoing scrutiny of gig-economy employment models.

- April 2026: Lidl opened 21 new stores across five major cities, enlarging its physical footprint and laying groundwork for possible platform partnerships.

- February 2026: Zooplus acquired JMT, lifting combined turnover above USD 169 million and consolidating the fast-growing pet-care segment.

France Quick Commerce Market Report Scope

The France Quick Commerce Market refers to the rapidly growing segment of the retail and e-commerce industry that focuses on ultra-fast delivery of consumer goods, typically within 30 minutes to a few hours, leveraging technology-driven platforms, localized warehouses, and efficient logistics networks.

The France Quick Commerce Market Report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, and Other Product Categories), Delivery Time Promise (Less than 10 Minutes, 11-30 Minutes, 31-60 Minutes and More). The Market Forecasts are Provided in Terms of Value (USD).

| Grocery and Staples |

| Fresh Produce and Dairy |

| Snacks and Beverages |

| Personal Care and OTC Pharma |

| Home and Cleaning Supplies |

| Electronics and Accessories |

| Pet Care |

| Flowers and Gifts |

| Other Product Categories |

| Less than 10 Minutes |

| 11-30 Minutes |

| 31-60 Minutes and More |

| Tier I Metros |

| Tier II Cities |

| Tier III and Below |

| By Product Category | Grocery and Staples |

| Fresh Produce and Dairy | |

| Snacks and Beverages | |

| Personal Care and OTC Pharma | |

| Home and Cleaning Supplies | |

| Electronics and Accessories | |

| Pet Care | |

| Flowers and Gifts | |

| Other Product Categories | |

| By Delivery Time Promise | Less than 10 Minutes |

| 11-30 Minutes | |

| 31-60 Minutes and More | |

| By City Tier | Tier I Metros |

| Tier II Cities | |

| Tier III and Below |

Key Questions Answered in the Report

What is the current France quick commerce market size and its growth outlook to 2031?

The France quick commerce market size stands at USD 1.54 billion in 2025, is projected at USD 1.66 billion in 2026, and is forecast to reach USD 2.40 billion by 2031, translating to a 7.7% CAGR over 2026-2031.

Which product category is the largest revenue contributor in French quick commerce?

Grocery and Staples led with 57.61% market share in 2025 as frequent top-up use and broad assortments anchor most baskets.

Which delivery time segment is growing the fastest?

The Less than 10 Minutes segment is forecast to advance at an 8.10% CAGR through 2031 after pivoting to a premium-priced, ultra-fast service tier.

How are regulations impacting dark store operations?

Decree n°2023-195 classifies dark stores as warehouses, letting cities restrict them; Paris opened 25 enforcement cases in 2023, pushing operators to embed micro-fulfillment inside compliant retail stores.

Why are partnerships between grocers and delivery platforms accelerating?

Alliances such as Carrefour-Uber Eats and Amazon-Chronodrive let retailers tap external courier fleets and digital reach without heavy capital outlays, aligning speed with sustainable margins.

What is driving the surge in pet-care deliveries?

Subscription services for recurring pet food and a consumer shift toward premium local brands are fueling a 7.96% CAGR in Pet Care, the fastest-growing quick-commerce category.

Page last updated on: