Japan Quick Commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

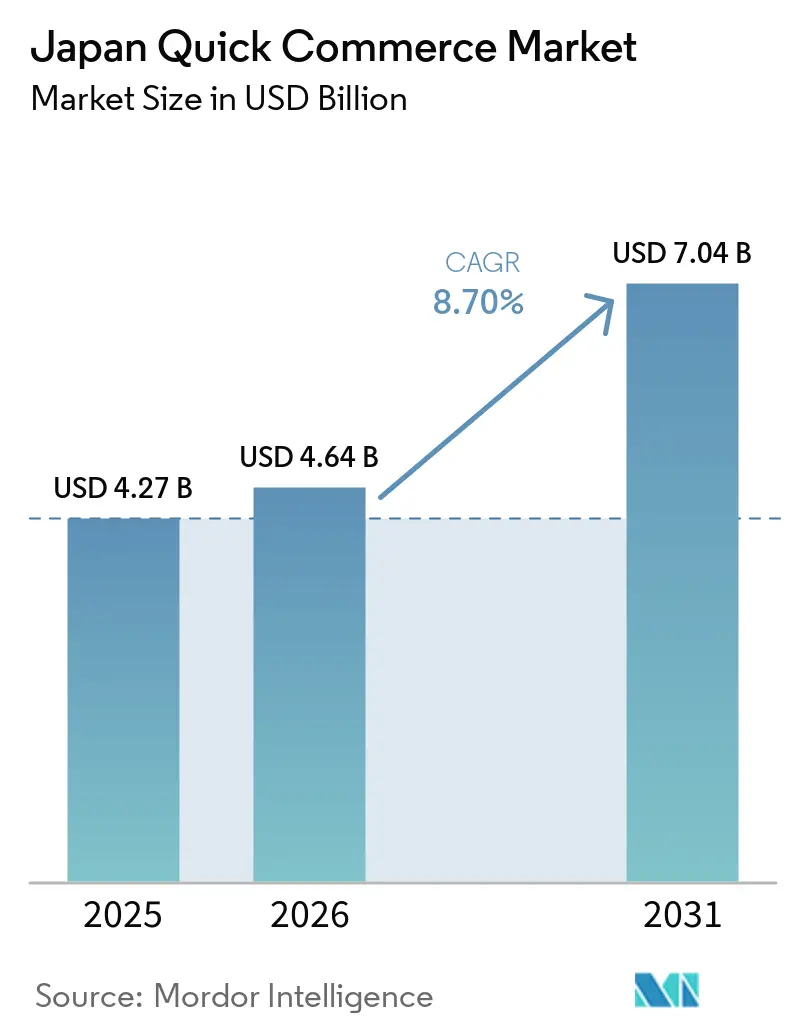

| Base Year Market Size (2025) | USD 4.27 Billion |

| Market Size (2026) | USD 4.64 Billion |

| Market Size (2031) | USD 7.04 Billion |

| Growth Rate (2026 - 2031) | 8.70% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Quick Commerce Market Analysis by Mordor Intelligence

The Japan quick commerce market was valued at USD 4.27 billion in 2025 and is forecast to reach USD 7.04 billion by 2031, expanding at a CAGR of 8.70% over the 2026-2031 period. The market is supported by Japan's dense urban form, its wide convenience store base, and a logistics culture built around reliable everyday retail fulfillment. Convenience-led purchasing has become the core demand pattern, as single-person households and dual-income families increasingly use rapid delivery for routine replenishment rather than occasional emergency orders. Grocery-led frequency still anchors volume, but faster growth in electronics and accessories shows that immediate replacement purchases are widening the addressable order mix. Retailer-led fulfillment models are also strengthening the market by using existing store networks and reducing dependence on pure third-party delivery economics. Even so, the Japan quick commerce market faces limits from rising last-mile cost, labor shortages, and tight urban fulfillment space, which means operators with route density, automation, and real estate access remain in the strongest position.

Key Report Takeaways

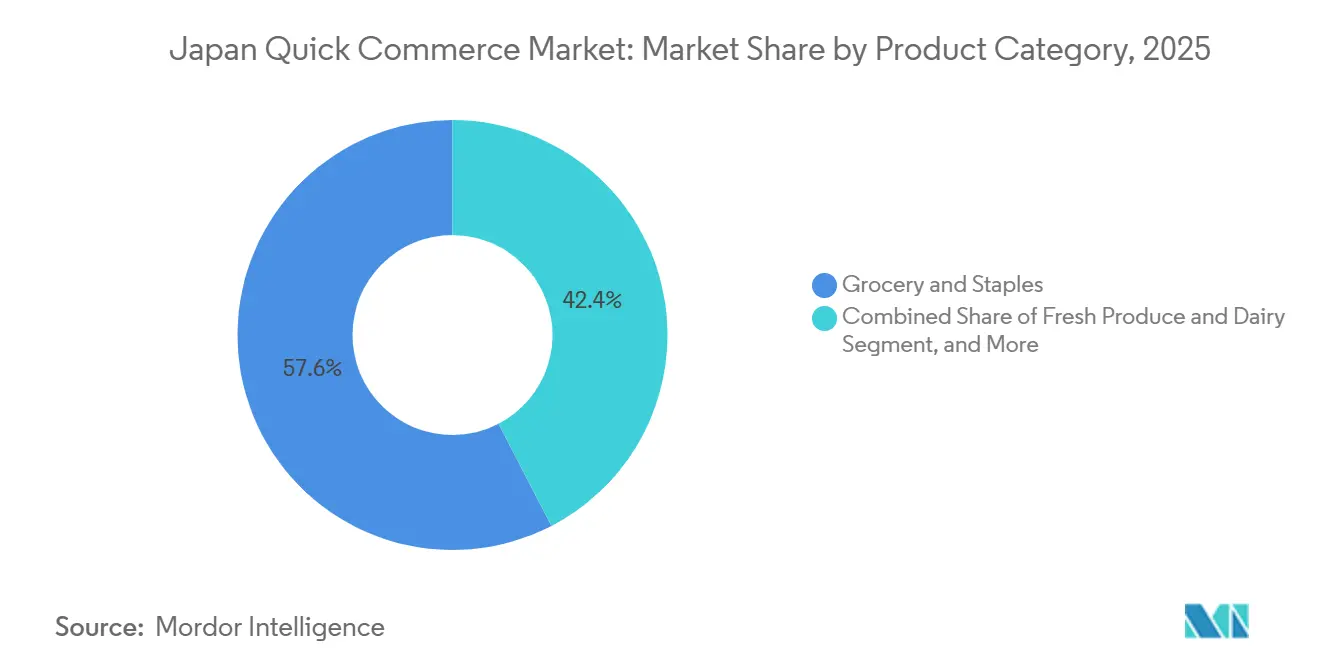

- By product category, grocery and staples held 57.61% of market value in 2025, while electronics and accessories is projected to expand at a CAGR of 7.96% through 2031.

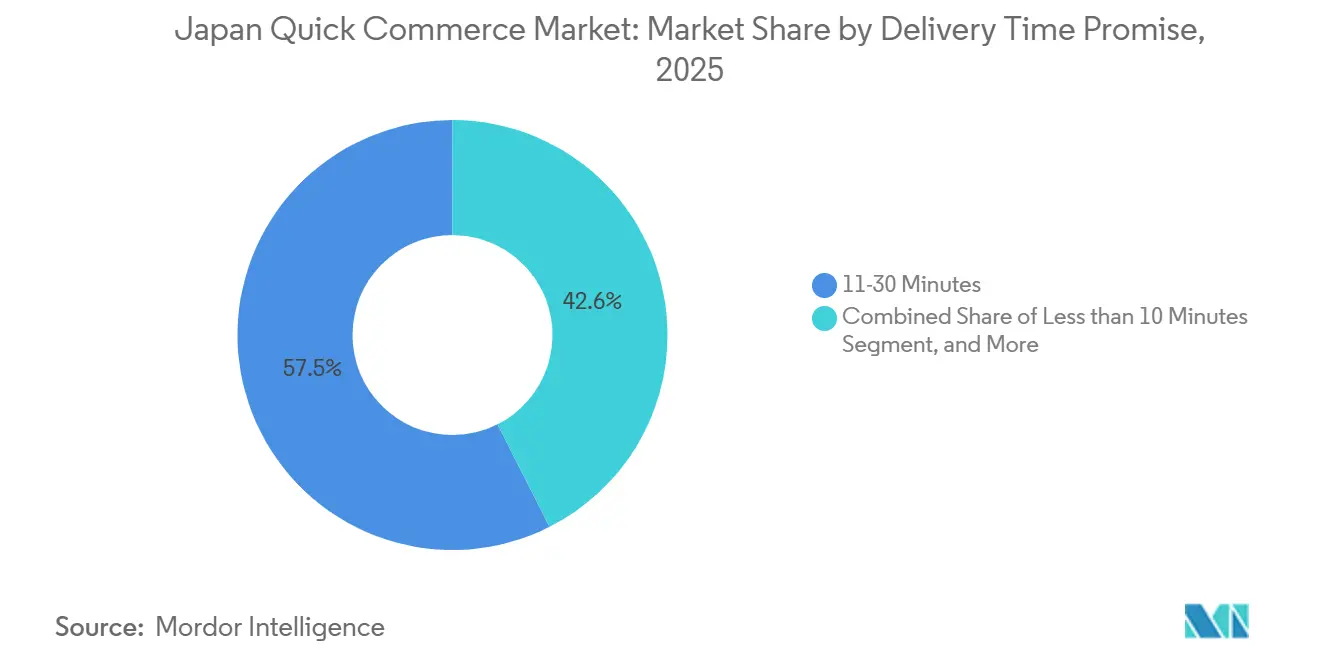

- By delivery time promise, the 11-30-minute tier accounted for 57.45% of market value in 2025, while the less than 10 minutes tier is forecast to grow at a CAGR of 8.10% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Quick Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Convenience-First Purchasing Behavior | +2.5% | National, with highest intensity in Tokyo 23 wards and the Osaka Namba-Umeda corridor | Short term (≤ 2 years) |

| Rapid Expansion of Dark Stores in Urban Japan | +1.8% | Tier I metros, with spillover into Tier II cities | Medium term (2-4 years) |

| Aging Population Demanding Home Delivery Solutions | +1.3% | National, with high relevance in Greater Tokyo suburbs and aging regional communities | Long term (≥ 4 years) |

| Rising Cashless Payment Adoption Enabling Seamless Checkout | +0.9% | National, with stronger adoption in urban areas | Medium term (2-4 years) |

| Deployment of Sidewalk Delivery Robots in Pilot Zones | +0.6% | Tokyo, Nagoya, and Kyoto pilot corridors | Long term (≥ 4 years) |

| Retail Media Monetization Within Quick Commerce Apps | +0.4% | National, led by large app ecosystems and convenience retail networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Convenience-First Purchasing Behavior

Urban households in Japan increasingly use fast delivery for daily needs rather than only for restaurant meals. A February 2026 survey of single-person households in the Tokyo metropolitan area found that 34.5% used delivery services multiple times per month, and daily necessities made up 51.8% of ordered categories while food delivery accounted for 14.1%. That buying pattern matters for the Japan quick commerce market because it favors platforms that can carry bulky, routine, and top-up items with dependable availability instead of only meal orders. METI reported that household expenditure on food, beverages, and alcohol rose 2.6% year over year in 2024 and was 5.7% above 2022 levels, which supports steady replenishment demand in the categories most suited to rapid delivery.[1]Ministry of Economy, Trade and Industry, “FY2024 E-Commerce Market Survey,” Ministry of Economy, Trade and Industry, meti.go.jp Operators that match assortment to top-up grocery, household essentials, and personal care are better placed to capture repeat orders in the Japan quick commerce market than those that treat grocery as an add-on to food delivery.

Rapid Expansion of Dark Stores in Urban Japan

Dark stores are becoming more important in the Japan quick commerce market because speed alone is not enough if stock accuracy is weak. Purpose-built fulfillment sites can hold broader assortments and maintain tighter inventory visibility than a live retail floor, which improves order completion and lowers substitution risk. AEON and Ocado announced a third automated customer fulfillment center in Kuki-Miyashiro, following the first site in Chiba and a second center planned for Hachioji, which shows continued investment in automation-led grocery fulfillment.[2]Eloise Hill, “Ocado Unveils Third Customer Fulfilment Centre with Aeon,” Retail Gazette, retailgazette.co.uk That build-out supports a model in which labor productivity and pick accuracy improve as volume scales across dense urban catchments. The Japan quick commerce market therefore gives an advantage to operators that secured logistics assets early and can connect fulfillment speed with reliable SKU depth.

Aging Population Demanding Home Delivery Solutions

Japan's aging profile is creating a long-duration demand base for the Japan quick commerce market. The Cabinet Office showed that people aged 65 and over accounted for around 30% of the population, and that share is set to rise further over time. Seven and i Holdings said 7NOW had reached all 47 prefectures by February 2025 and framed the service around diverse shopping needs, including people who face grocery access difficulty.[3]Seven and i Holdings, “7NOW Meets Your Diverse Shopping Needs,” Seven and i Holdings, 7andi.com A care manager survey published in April 2025 also showed clear demand for faster household delivery among older users, including a strong preference for orders that arrive within 1 hour. As a result, the Japan quick commerce market is not only tied to urban convenience spending, it is also linked to an expanding access need among seniors and mobility-constrained households.

Rising Cashless Payment Adoption Enabling Seamless Checkout

Cashless adoption is reducing a basic friction point for the Japan quick commerce market, which is payment speed at the moment of order confirmation. METI stated that Japan's cashless payment ratio reached 58.0% of consumer spending in 2025, totaling JPY 162.7 trillion (USD 1.05 trillion), and code payments rose 22.6% year over year to JPY 16.6 trillion (USD 0.10 trillion) across 13.5 billion transactions. The same data showed an average code-payment ticket of around JPY 1,200 (USD 7.70), which aligns closely with convenience-led small basket behavior that is common in fast delivery use cases. Nikkei Asia also reported that credit card payments overtook cash as the main household payment method for the first time, which points to a broader shift in consumer readiness for app-based ordering. This matters for the Japan quick commerce market because higher digital payment comfort supports faster checkout, stronger repeat usage, and smoother app-led promotions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Last-Mile Logistics Cost Per Order | -1.2% | National, with the greatest strain in lower-density Tier II and Tier III zones | Medium term (2-4 years) |

| Intensifying Competition Compressing Margins | -0.9% | National, with the sharpest pressure in Tokyo and Osaka | Short term (≤ 2 years) |

| Labor Shortages in Urban Logistics | -0.7% | National, especially in suburban delivery corridors and smaller cities | Long term (≥ 4 years) |

| Municipal Restrictions on Micro-Fulfillment Center Zoning | -0.5% | Tier I metros, especially Tokyo, Osaka, and Nagoya | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Last-Mile Logistics Cost Per Order

Last-mile economics remain one of the main limits on the Japan quick commerce market. The Japan Institute of Logistics Systems reported that the retail sector logistics cost ratio rose to 6.38% of sales in 2024, the highest level in at least 20 years for that category. The burden is heavier for quick delivery because order values are smaller, pick cycles are shorter, and the service promise leaves less room to spread cost across routes. METI also reported an urban redelivery rate of 11.6% in October 2024, which shows that failed or repeated delivery attempts still add cost in dense areas. This means the Japan quick commerce market rewards operators that can raise route density, improve forecasting, and limit failed handoffs rather than those that compete only on discounting.

Intensifying Competition Compressing Margins

Competition in the Japan quick commerce market has shifted away from simple expansion and toward capital discipline and operational scale. DoorDash announced on February 25, 2026 that it would wind down Wolt operations in Japan and other markets, and Wolt then ceased operations in Japan in March 2026. That exit left Uber Eats Japan and Demae-can with a stronger position in food delivery, but it did not remove pressure in grocery and daily necessities where retailer-led and dark-store-led formats still compete on different economics. Seven-Eleven Japan is building a model that uses store infrastructure and app traffic, while other operators still depend more heavily on paid acquisition and delivery density to protect margins. The result is a Japan quick commerce market where scale helps, but the underlying business model now matters just as much as order growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Grocery Anchors Frequency as Electronics Reshapes Basket Value

Grocery and staples held 57.61% of the market in 2025, which made the category the core volume engine of the Japan quick commerce market. That leadership came from repeat purchase behavior rather than premium pricing, because households use fast delivery for top-up missions that happen several times a week. Single-person households and working couples rely on grocery for urgent replenishment, and that steady cadence supports the route density needed to keep fulfillment costs under control. Fresh produce and dairy, snacks and beverages, and home and cleaning supplies all add natural basket extensions that make a grocery-led order more viable for operators.

Electronics and accessories is forecast to grow at a 7.96% CAGR through 2031, which makes it the fastest-rising product category in the Japan quick commerce market. METI reported that household expenditure on home appliances, AV equipment, and computer peripherals rose 3.5% year over year in 2024 and stood 15.7% above 2019 levels. That pattern supports demand for replacement items such as cables, chargers, and small accessories, where delivery speed can matter more than price. METI also showed growth in cosmetics and pharmaceutical spending, which supports adjacent expansion into personal care and OTC products that can lift order value without moving far from the Japan quick commerce industry's daily-need mission.

By Delivery Time Promise: The 11-30-Minute Window Sets the Base Standard

The 11-30-minute segment accounted for 57.45% of the Japan quick commerce market size in 2025, which shows where commercial scale currently sits. This delivery window works because it balances picker accuracy, assortment depth, and customer expectations in dense city neighborhoods. Seven-Eleven Japan said its 7NOW service was available through 70% of its more than 20,000 stores by March 2026, and the service targets delivery in as little as 20 minutes, which supports this middle band at national scale. In practical terms, the Japan quick commerce market has settled around this band because it is fast enough to feel immediate while still allowing dependable fulfillment across thousands of SKUs.

The less than 10 minutes segment is projected to expand at an 8.10% CAGR through 2031, making it the fastest-growing time promise in the Japan quick commerce market. Rakuten expanded robot delivery in Tokyo in February 2025 with Avride robots and a wider operating area across Harumi and nearby districts, which shows how dense service zones can push fulfillment times lower in selected neighborhoods. Rakuten later highlighted strong repeat behavior in its unmanned delivery service, which suggests that very short delivery windows can create habit when the service is reliable. The slower 31-60-minute and longer tiers still matter for larger baskets and regulated categories, but sub-10-minute service is setting the pace for premium convenience in the Japan quick commerce market.

Geography Analysis

Tier I metros accounted for a significant portion of the value in 2025, and that concentration has made the Japan quick commerce market heavily centered on Greater Tokyo and other dense urban corridors. Greater Tokyo remains the main proving ground because it combines population density, high convenience store penetration, and a customer base that is comfortable with app-led ordering. Rakuten stated its unmanned delivery service had expanded significantly in Tokyo's Harumi area by late 2025, which shows how selected districts can support repeated rapid delivery usage at the neighborhood scale. Rakuten also expanded that network in early 2025 with Avride robots and wider service coverage across Harumi, Tsukishima, and Kachidoki. Tokyo's role in the Japan quick commerce market is therefore not just about scale, it is also about being the first zone where operators test new delivery formats under live commercial conditions.

The Kansai region forms the second major zone for the Japan quick commerce market because Osaka's mix of dense residential and commercial districts can support service economics similar to Tokyo in selected areas. Osaka also benefits from the wider national move toward cashless payments, which helps app-based retail and food orders move through quickly. Nagoya has emerged as a meaningful test location as well. Aichi Prefecture announced a public-road autonomous delivery demonstration in Nagoya's Sakae district that ran across several weekdays from late 2025 into early 2026, covering multiple delivery routes with the ROBO-HI DeliRo robot. This kind of trial matters because the Japan quick commerce market needs proof that automation can work in live urban settings beyond the capital.

Coverage outside the largest metropolitan areas follows a different logic in the Japan quick commerce market. Demand there is tied less to instant urban convenience and more to shrinking local retail access, older populations, and weaker physical shopping options. Seven and i Holdings' move to bring 7NOW to all prefectures by early 2025 showed that partner-store-led coverage can reach much farther than a dark-store-only model. The Japan Times also reported on the Minami-Osawa robot pilot in Hachioji, which highlighted how autonomous delivery can support communities where topography and aging demographics make physical shopping harder. As a result, the Japan quick commerce market is geographically split between dense city economics and a broader access-led opportunity that will depend more on automation, existing store networks, and lower-cost coverage models.

Competitive Landscape

The Japan quick commerce market has become more concentrated in food-led delivery, but it remains more mixed across grocery, household essentials, and specialty categories. DoorDash's February 2026 decision to wind down Wolt operations in Japan, followed by Wolt's March exit, showed how difficult the market had become for operators without enough scale or structural advantage. Uber Eats Japan and Demae-can have strengthened their position in food delivery, but they are not the only competitive reference point because the Japan quick commerce market also includes retailer-led networks and dark-store-led models. That mix keeps the broader market from being fully locked into a single platform structure.

One important strategic move came from Seven-Eleven Japan, which completed 7NOW expansion across all 47 prefectures by February 2025 and then launched 7NOW Mobile Order nationwide in April 2026 for in-store pickup of freshly prepared products. This gave Seven-Eleven a retailer-led route into the Japan quick commerce market that depends on store infrastructure and repeat app usage rather than pure marketplace commissions. Rakuten made another strategic move when it brought Avride robots into commercial service in Tokyo in February 2025 after the underlying safety pathway had been cleared, strengthening its automation position in dense neighborhoods. AEON's continued build-out with Ocado adds a third pattern, which is automation-heavy grocery fulfillment designed to deepen basket quality and operational efficiency. These moves show that competition in the Japan quick commerce market is now being shaped by infrastructure depth and model design as much as by brand reach.

The market still leaves room for smaller and niche players, but that room is narrowing. Operators that lack logistics density, retail asset backing, or ecosystem traffic face more pressure as wage costs and fulfillment costs stay high. The Japan quick commerce market is also developing a regulatory threshold around automation, because firms that want to scale sidewalk robots need credible safety compliance and local operating experience. This favors established companies with capital, engineering depth, and existing commercial networks. In that setting, the likely winners in the Japan quick commerce market are the ones that can combine order density, trusted fulfillment, and a model that does not rely only on discount-driven customer acquisition.

Japan Quick Commerce Industry Leaders

Rakuten Group, Inc.

Uber Eats Japan, Inc.

Kuroneko Yamato Logistics Co., Ltd.

Demae-can Co., Ltd.

7-Eleven Japan Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Seven-Eleven Japan launched 7NOW Mobile Order nationwide on April 1, 2026, enabling customers to order freshly prepared items including fried foods and Seven Cafe Bakery products via the 7NOW app for in-store pickup in as little as 20 minutes. The company targets expansion to approximately 18,000 stores with this feature by the end of fiscal year 2026 and aims for JPY 120 billion (USD 0.77 billion) in annual 7NOW sales by February 2031.

- April 2026: AEON NEXT's online supermarket Green Beans opened the "Green Beans Park" brand experience lab and pickup spot on April 6, 2026, in conjunction with the grand opening of AEON Hachioji Takiyama, piloting a hybrid physical-digital model to integrate online grocery ordering with in-store consumer engagement.

- March 2026: Wolt ceased operations in Japan on March 4-5, 2026, following DoorDash's February 25, 2026 announcement to wind down Wolt and Deliveroo operations in four markets including Japan, Qatar, Singapore, and Uzbekistan. The exit consolidated approximately 90% of Japan's food-delivery segment between Uber Eats Japan and Demae-can, with Coupang's Rocket Now and KDDI's menu expected to absorb residual market share.

- November 2025: Rakuten Unmanned Delivery celebrated its first anniversary in Tokyo's Harumi area, having grown participating stores from 3 to 23, product range to over 8,000 items, households served from approximately 14,000 to over 34,000, and delivery locations from 62 to 188, with monthly orders more than doubling and repeat rates exceeding 50% as of November 2025.

Japan Quick Commerce Market Report Scope

The Quick Commerce Market in Japan represents a rapidly expanding segment within the country's retail and e-commerce industry. It is characterized by the provision of ultra-fast delivery services for consumer goods, typically within 30 minutes to a few hours. This market leverages advanced technology platforms, strategically positioned warehouses, and highly efficient logistics networks to meet consumer demand.

The Japan Quick Commerce Market Report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Pet Care, and Flowers and Gifts), Delivery Time Promise (Less Than 10 Minutes, 11-30 Minutes, and 31-60 Minutes). The Market Forecasts are Provided in Terms of Value (USD).

| Grocery and Staples |

| Fresh Produce and Dairy |

| Snacks and Beverages |

| Personal Care and OTC Pharma |

| Home and Cleaning Supplies |

| Electronics and Accessories |

| Pet Care |

| Flowers and Gifts |

| Other Product Categories |

| Less than 10 Minutes |

| 11-30 Minutes |

| 31-60 Minutes and More |

| By Product Category | Grocery and Staples |

| Fresh Produce and Dairy | |

| Snacks and Beverages | |

| Personal Care and OTC Pharma | |

| Home and Cleaning Supplies | |

| Electronics and Accessories | |

| Pet Care | |

| Flowers and Gifts | |

| Other Product Categories | |

| By Delivery Time Promise | Less than 10 Minutes |

| 11-30 Minutes | |

| 31-60 Minutes and More |

Key Questions Answered in the Report

What is the size of the Japan quick commerce market?

The Japan quick commerce market was valued at USD 4.27 billion in 2025 and is forecast to reach USD 7.04 billion by 2031, growing at an 8.70% CAGR over 2026-2031.

Which product category leads demand in Japan quick commerce?

Grocery and staples led the market with a 57.61% share in 2025 because repeat top-up purchases still drive the highest order frequency.

Which delivery speed band is most important in Japan?

The 11-30-minute window held 57.45% of value in 2025 because it balances speed, picking accuracy, and broad assortment availability.

Which city tier is growing fastest for rapid delivery services in Japan?

Tier II cities are projected to grow the fastest at an 8.05% CAGR through 2031 as operators extend coverage beyond saturated Tier I metros.

Why are convenience store chains important in this space?

Convenience store chains matter because they already have store density, local inventory, and customer traffic. That lets them scale delivery and pickup with lower new infrastructure spending.

What are the biggest challenges for operators in Japan?

The main challenges are high last-mile costs, margin pressure from competition, labor constraints, and the need to build efficient fulfillment density in urban areas.

Page last updated on: