Singapore Quick Commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

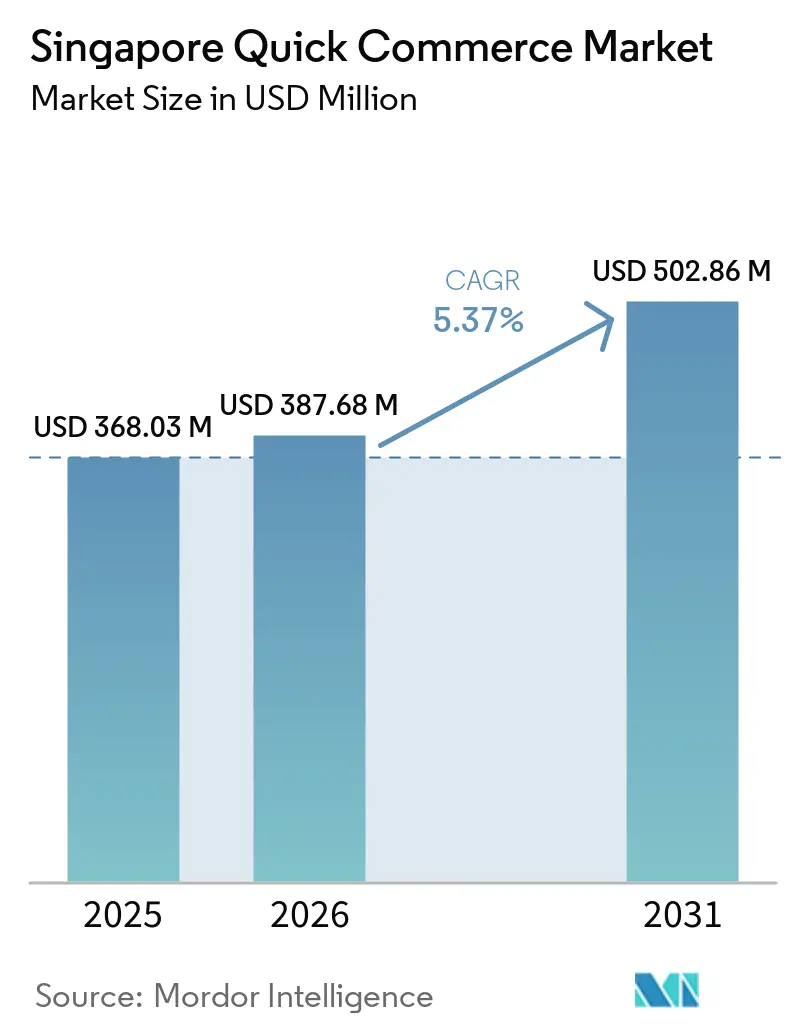

| Base Year Market Size (2025) | USD 368.03 Million |

| Market Size (2026) | USD 387.68 Million |

| Market Size (2031) | USD 502.86 Million |

| Growth Rate (2026 - 2031) | 5.37% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Quick Commerce Market Analysis by Mordor Intelligence

The Singapore quick commerce market size was valued at USD 368.03 million in 2025 and is estimated to grow from USD 387.68 million in 2026 to reach USD 502.86 million by 2031, at a CAGR of 5.34% during the forecast period (2026-2031). Growth is now driven less by subsidies and more by disciplined unit economics as operators prioritize density, cross-platform leverage, and fulfillment automation. Amazon Fresh and Deliveroo exited in early 2026, clearing volume for incumbents that can spread logistics costs across ride-hailing, payments, and e-commerce. Grab and Sea Limited’s Shopee are converting those structural advantages into higher order frequency, while traditional grocers deepen omnichannel reach through automated warehouses and dark stores. Super-app ecosystems, expanding cold-chain capacity, and government-backed digital-payments rails together form a robust demand flywheel that should sustain mid-single-digit annual expansion even as competitive intensity rises.

Key Report Takeaways

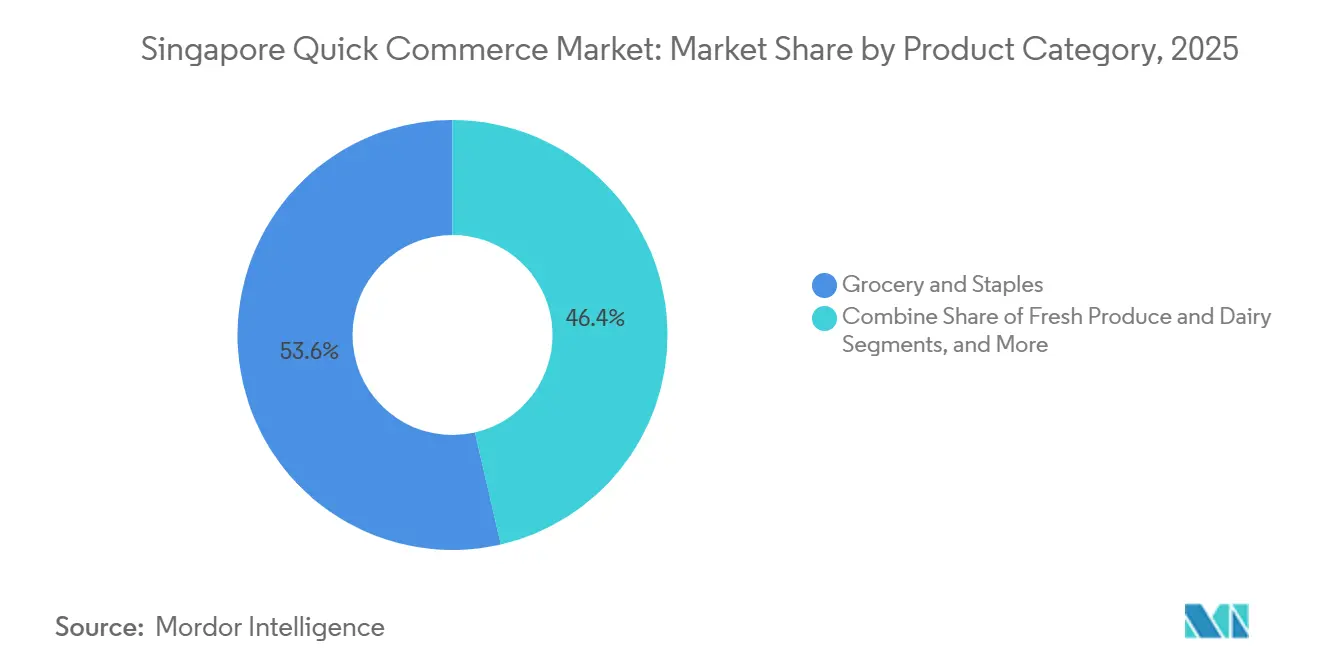

- By product category, Grocery and Staples led with 53.61% revenue share in 2025, whereas Fresh Produce and Dairy is projected to advance at a 5.88% CAGR to 2031.

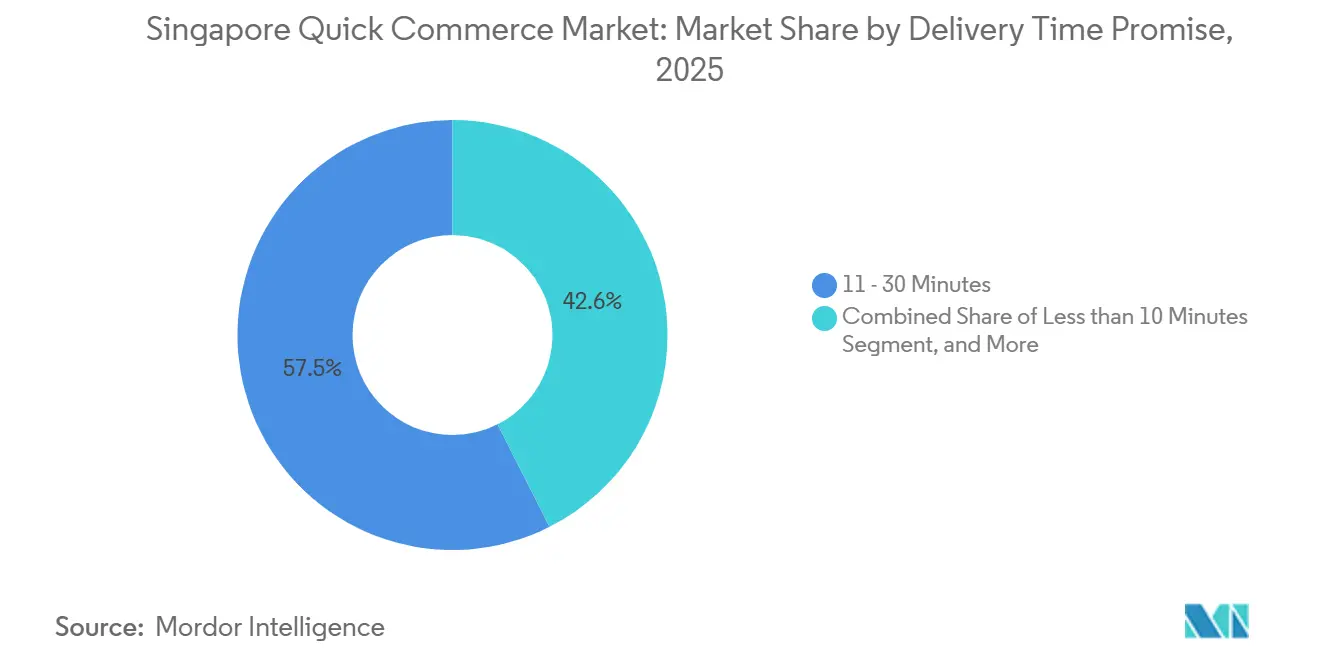

- By delivery time promise, the 11-30 Minutes tier commanded 57.45% of the Singapore quick commerce market share in 2025, while the Less than 10 Minutes segment is forecast to post a 5.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Quick Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Smartphone-Enabled on-Demand Culture | +1.5% | National, concentrated in Tier I Metros | Short term (≤ 2 years) |

| Expansion of Dark Store Networks Across Singapore | +1.3% | National, early density in Kallang, Yio Chu Kang, Tampines, Woodlands | Medium term (2-4 years) |

| Strategic Investments by Super Apps and E-Commerce Giants | +1.2% | National, spill-over to Johor-Singapore corridor | Medium term (2-4 years) |

| Government Support for Cashless Payments and Digitalization | +0.8% | National | Long term (≥ 4 years) |

| Emergence of AI-Driven Predictive Inventory Management | +0.6% | National, early adoption in Tier I dark stores | Medium term (2-4 years) |

| Cross-Border Micro-Fulfillment Hubs Serving Johor-Singapore Corridor | +0.4% | North Region and Johor Bahru | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation Of Smartphone-Enabled On-Demand Culture

Singapore records smartphone penetration near 165%, and mobile checkouts represent 85% of all e-commerce purchases. Such ubiquity has schooled households to treat instant fulfillment as default service, compressing the margin of error for delivery reliability. Surveys show 80% of residents expect same-day delivery and 61% want receipt within three hours, while half of Deliveroo users now order groceries, retail items, or gifts in addition to meals. Digital wallets covering 39% of e-commerce payments enable one-tap checkout, converting browsing impulses into incremental orders that lift frequency for the Singapore quick commerce market. Platforms that marry frictionless payment with predictive reorder prompts secure an outsized share of high-frequency baskets such as snacks or personal care.[1]Anchanto, “Singapore E-Commerce Market: Trends, Growth and Opportunities,” anchanto.com

Expansion Of Dark Store Networks Across Singapore

Micro-fulfillment nodes closed to foot traffic are mushrooming across dense residential pockets to shrink last-mile distances. Foodpanda’s Pandamart outlets in Kallang and Yio Chu Kang stock 5,000-plus SKUs and use AI to stage goods within two-kilometer radii, cutting average drop-times to below 25 minutes and reducing rider idle minutes by double digits. Lazada’s RedMart Now, launched in February 2026, leverages zoned facilities that bypass legacy store replenishment, promising 30-minute delivery in south-central and western districts. Singapore’s planners accelerate the trend by rezoning large brownfield sites such as Bukit Timah Turf City into mixed-use precincts where ground-level logistics can coexist with housing. Real-estate costs still loom large, but operators mitigate rents through higher order density, subscription programs, and automated picking that boost throughput per square foot, helping sustain profitable expansion of the Singapore quick commerce market.

Strategic Investments By Super Apps And E-Commerce Giants

Grab’s USD 600 million purchase of foodpanda Taiwan in March 2026 illustrates the region-wide scale economics now shaping competitive advantage. Order volume synergies stretch procurement discounts, while unified tech stacks spread algorithm and cloud costs across multiple countries. Shopee processed 4 billion orders in 4Q 2025, funneling parcel density into its SPX Express network that now achieves 90% next-day delivery domestically. These flywheels let super apps price grocery baskets close to, or even below, cost, using ad sales and fintech revenues for cross-subsidy. Stand-alone grocers respond with automation; for instance, FairPrice’s smart carts grew average basket value 80%. The cumulative pattern fortifies two-horse dominance inside the Singapore quick commerce market and narrows the path for venture-backed niche entrants.

Government Support For Cashless Payments And Digitalization

The city-state’s regulators have erected a seamless payments backbone that removes checkout friction from the Singapore quick commerce market. PayNow processed 1.2 billion transfers in 2025, while SGQR standardizes acceptance across 300,000 merchants. GovWallet onboards millions for digital disbursements, seeding consumer familiarity with in-app payments that operators immediately monetize through loyalty tie-ins. Smart Nation 2.0 opens public-sector APIs, transport, identity, housing, so platforms can weave personalized offers around commuter patterns or HDB block clusters. Strict data-protection rules ensure privacy, favoring well-capitalized incumbents with compliance teams over lightweight startups.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Real-Estate and Labor Costs Eroding Margins | -0.9% | National, acute in Central and Tier I zones | Short term (≤ 2 years) |

| Stringent Urban Traffic Regulations Limiting Delivery Windows | -0.7% | National, concentrated in CBD and restricted zones | Medium term (2-4 years) |

| Volatility in Venture Funding for Hyperlocal Startups | -0.5% | National | Short term (≤ 2 years) |

| Consumer Fatigue Toward Delivery App Promotions | -0.3% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Real-Estate And Labor Costs Eroding Margins

Industrial land in core logistics precincts commands premium leases that strain unit margins for micro-fulfillment operators. Sheng Siong spent SGD 520 million (USD 384.8 million) to relocate its automated warehouse to Sungei Kadut, illustrating the heavy capital now required merely to secure suitable floor area. Delivery riders earn SGD 8-12 (USD 5.92-8.88) per hour, and November 2025 safety rules mandate rest breaks and speed caps that trim deliveries per shift by up to 15%. Ultra-dense dark stores must book 150-200 daily orders just to break even under these cost conditions. The Singapore quick commerce market therefore tilts toward players with either multichannel scale or third-party logistics alliances that dilute fixed expenses across larger revenue pools.

Stringent Urban Traffic Regulations Limiting Delivery Windows

Commercial vans above 3,500 kilograms face expressway restrictions during peak periods, rerouting them onto arterial roads and extending cross-island trips by nearly 20 minutes. Separate rules cap e-bike speeds at 25 kilometers per hour and require riders to pause after four continuous hours, cutting the attainable drop count per shift. Restricted zones such as the CBD impose delivery surcharges that either erode operator margins or discourage consumer purchases. Platforms operating inside the Singapore quick commerce market therefore over-provision rider capacity in off-peak slots or invest in higher dark-store density to keep average travel times within promised windows.[2]Land Transport Authority, “Enhanced Safety Measures for Delivery Riders,” lta.gov.sg

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Grocery Anchors, Fresh Produce Accelerates

Grocery and Staples secured 53.61% of the Singapore quick commerce market in 2025, buoyed by frequent top-up purchasing patterns and a reliable inventory cycle that turns stock 15-20 times annually. The Deliveroo-Sheng Siong exclusive partnership placed more than 5,000 SKUs online with 24-hour access, proving that legacy grocers can lift reach without cannibalizing footfall. Fresh Produce and Dairy, though smaller, shows the highest momentum at a 5.88% CAGR through 2031; capacity gains stem from Ninja Van’s cold-chain fleet and from Pandamart XL sites that expanded chilled lines by 30%. Non-food niches offer margin upsides, OnePhone’s one-hour phone replacement service and ElectronicsCrazy’s three-hour urgent delivery monetize willingness to pay for speed on high-value, low-weight items. Pharmacies such as Glovida broaden the category mix by shipping over-the-counter products under Health Sciences Authority oversight, deepening consumer trust. Operators that integrate ambient, chilled, and frozen zones within a single facility can meet full-basket needs, increasing wallet share inside the Singapore quick commerce market size for multipurpose missions.

The breadth-versus-depth trade-off remains critical. Grocery ensures volume, perishables demand temperature precision, and impulse categories widen margins. Platforms mastering predictive slotting across these temperature bands elevate service reliability and become default household suppliers. Those lagging in cold-chain rigor or SKU breadth risk relegation to occasional-use status, limiting their share of the Singapore quick commerce market size.

By Delivery Time Promise: Mid-Speed Dominates, Ultra-Fast Gains

Deliveries pledged within 11-30 minutes captured 57.45% of spend in 2025, striking a balance between cost and consumer gratification. Algorithms such as Deliveroo’s Frank optimize rider dispatch during dinner peaks, while RedMart Now uses zoned facilities to stay within a half-hour promise across west and central districts. Ultra-fast fulfillment under 10 minutes, although nascent, is projected to grow at 5.92% CAGR thanks to dark stores positioned within two-kilometer order radii. The model thrives in central catchments exceeding 15,000 residents per square kilometer where daily order volumes surpass 200. Premium electronics, pharmacy refills, and gifting are also migrating into this hyper-local tier, widening revenue streams for the Singapore quick commerce market. The 31-60 minute bracket services bulk orders and lower-density suburbs, often via van fleets that accept longer lead times in exchange for higher average basket value.

The competitive path forward is flexible fulfillment. Operators that can dynamically route an order to the optimal node, dark store, retail outlet, or regional warehouse, based on customer urgency and item weight will defend market share more effectively than peers locked into a single speed tier. Compliance with speed caps and mandatory rider rest pauses intensifies the engineering challenge yet also widens the moat for platforms with sophisticated routing engines and dense node coverage.

Geography Analysis

Singapore’s compact 730-square-kilometer footprint means planning-area density replaces long-haul distance as the key geographic variable. Tier I Metros, Central Region, Downtown Core, and dense East and North-East districts, generated nearly three-fifths of 2025 gross merchandise value. These precincts combine subway connectivity, integrated retail, and robust office clusters that create lunch-time and late-night order peaks. The Greater Southern Waterfront and one-north technology hub continue to add condominium towers and co-working campuses that lift per-capita discretionary income, amplifying the Singapore quick commerce market’s urban heartland.

Tier II areas straddle cost and convenience. Bishan’s upcoming sub-regional center brings new municipal offices and transport links that will elevate daytime footfall, while Yio Chu Kang already hosts a Pandamart XL, signaling logistical viability. Transport corridors being extended under the Cross-Island Line will shave minutes off inter-suburb journeys, enabling dark-store clustering that maintains sub-30-minute promises without incurring CBD-level rents.

Tier III and below regions furnish the long-term upside. Woodlands stands out as the northern gateway feeding demand from Johor via the Rapid Transit System and bonded cross-border warehouses. Jurong Lake District, near the mega-port at Tuas, slowly evolves into a western commercial hub that could absorb dark-store capacity once rail extensions come online. Former Paya Lebar Air Base and Bukit Timah Turf City redevelopment will inject tens of thousands of new homes that future-proof order density. Consequently, geographic strategy must shadow phased infrastructure rollouts; those who lock in leases and permitting ahead of population inflows will enjoy structural cost advantages across the Singapore quick commerce market.

Competitive Landscape

Industry concentration is moderate, with Grab and Shopee together estimated above 60% share, leveraging ride-hailing, payments, fintech, and marketplace cross-traffic to squeeze per-order logistics cost. Their ecosystems recycle on-demand couriers across food, parcels, and grocery, achieving marginal-cost economics that recently forced Amazon Fresh and Deliveroo to leave. Grab’s March 2026 acquisition of foodpanda Taiwan spreads procurement contracts and machine-learning spend across multiple markets, while Shopee’s 4 billion quarterly orders push parcel volume into SPX Express routes that guarantee next-day island-wide coverage. Traditional retailers retaliate through capital-intensive automation: Sheng Siong’s USD 385 million Sungei Kadut warehouse underpins 120 stores at 15-plus inventory turns, and FairPrice’s AI-equipped smart carts lift in-store basket size by 80%.[3]The Business Times, “Sheng Siong to Relocate Warehouse to Sungei Kadut,” businesstimes.com.sg

White-space competition now emerges in cross-border fulfillment and high-ticket niches. DSV’s RedLion2 campus and the 103° Food Cold Zone allow chilled inventory to sit in lower-cost Johor while still meeting 60-90-minute service levels into northern Singapore, potentially eroding the central-warehouse advantage today enjoyed by incumbents. Electronics and gifts remain fragmented, with OnePhone and ElectronicsCrazy charging premium fees for one-hour or three-hour delivery that super-apps have yet to replicate at scale. Robotics startups such as ROLO Robotics and Cata target labor bottlenecks through automated picking and postal-code demand forecasting, offering incremental productivity gains that could be white-labeled to multiple retailers. Regulatory tailwinds, namely the Food Safety and Security Act’s stringent standards, raise entry barriers for lightly capitalized challengers yet also create opportunities for compliance-as-a-service offerings bundled with cold-chain tracking.

Singapore Quick Commerce Industry Leaders

Grab Holdings Inc.

Delivery Hero SE (foodpanda)

Sea Ltd. (Shopee, ShopeeFood)

Deliveroo plc

Amazon.com Inc. (Amazon Fresh, Prime Now)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Grab agreed to buy foodpanda Taiwan for USD 600 million, boosting regional procurement scale and reducing average fulfillment cost.

- March 2026: The 103° Food Cold Zone opened inside the Johor-Singapore Special Economic Zone, offering sustainable frozen-commodity storage 30-40% cheaper than Singapore equivalents.

- March 2026: Maersk inaugurated a USD 148 million automated logistics campus featuring robotic sortation and 24-hour customs clearance to strengthen Singapore’s role as a Southeast Asian fulfillment hub.

- March 2026: Deliveroo confirmed its departure from Singapore effective March 4, repatriating capital after 11 years in the market.

Singapore Quick Commerce Market Report Scope

The Singapore Quick Commerce Market refers to the rapidly growing segment of the retail and e-commerce industry in Saudi Arabia that focuses on ultra-fast delivery of consumer goods, typically within 30 minutes to a few hours, leveraging technology-driven platforms, localized warehouses, and efficient logistics networks.

The Singapore Quick Commerce Market Report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, and Flowers and Gifts), and Delivery Time Promise (Less Than 10 Minutes, 11-30 Minutes, and 31-60 Minutes). The Market Forecasts are Provided in Terms of Value (USD).

| Grocery and Staples |

| Fresh Produce and Dairy |

| Snacks and Beverages |

| Personal Care and OTC Pharma |

| Home and Cleaning Supplies |

| Electronics and Accessories |

| Pet Care |

| Flowers and Gifts |

| Other Product Categories |

| Less than 10 Minutes |

| 11-30 Minutes |

| 31-60 Minutes and More |

| By Product Category | Grocery and Staples |

| Fresh Produce and Dairy | |

| Snacks and Beverages | |

| Personal Care and OTC Pharma | |

| Home and Cleaning Supplies | |

| Electronics and Accessories | |

| Pet Care | |

| Flowers and Gifts | |

| Other Product Categories | |

| By Delivery Time Promise | Less than 10 Minutes |

| 11-30 Minutes | |

| 31-60 Minutes and More |

Key Questions Answered in the Report

What is the current Singapore quick commerce market size and how fast is it growing?

The Singapore quick commerce market size stood at USD 368.03 million in 2025 and is projected to rise to USD 502.86 million by 2031, expanding at a 5.34% CAGR, according to Mordor Intelligence.

Which product category is growing fastest within Singapore's instant retail segment?

Fresh Produce and Dairy leads growth with a forecast 5.88% CAGR through 2031, powered by new cold-chain capacity and larger refrigerated assortments.

Who are the dominant companies in Singapore's quick commerce space?

Grab and Shopee together command more than 60% of orders, leveraging super-app ecosystems that bundle mobility, payments, and marketplace traffic.

How are regulatory changes impacting delivery operations?

New food-safety standards and rider safety rules add compliance costs and cap rider speeds, pushing operators toward denser dark-store networks and automation.

What geographic areas offer the next wave of expansion potential?

Northern districts such as Woodlands and Jurong are primed for growth as new mixed-use towns, rail links, and cross-border logistics hubs come online.

Which technologies are most critical for quick commerce profitability?

AI-driven demand forecasting, robotic picking, and integrated digital-payment rails collectively reduce stockouts, labor costs, and checkout friction, bolstering margins.

Page last updated on: