GCC Quick Commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

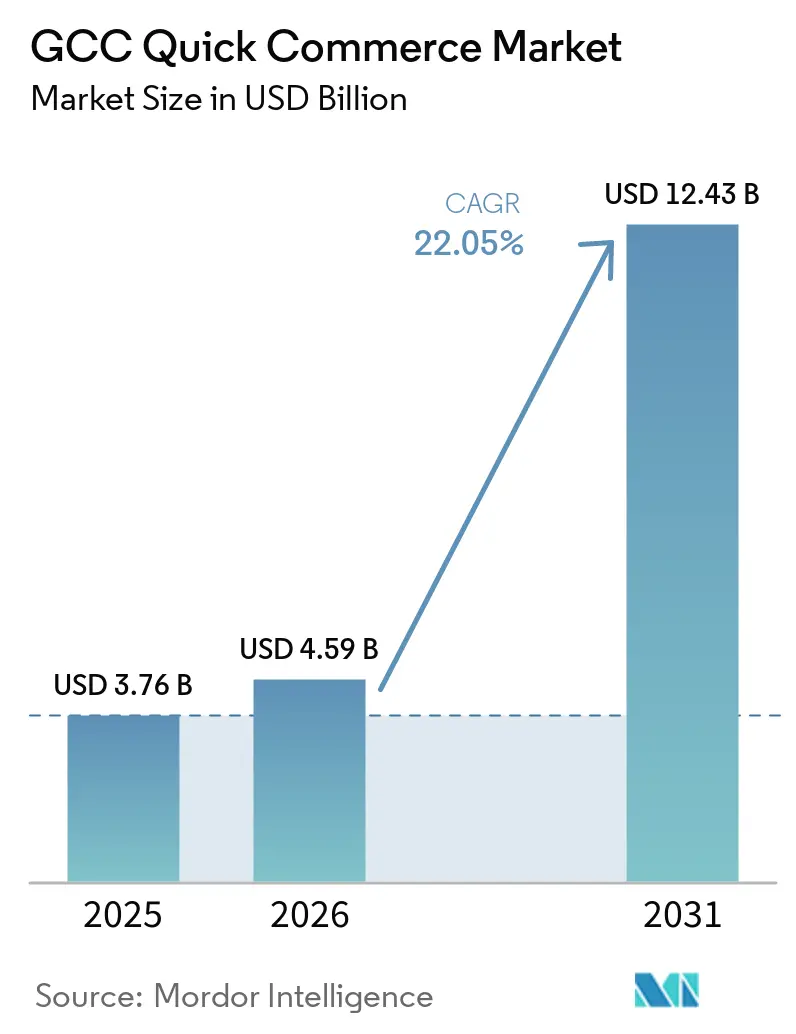

| Base Year Market Size (2025) | USD 3.76 Billion |

| Market Size (2026) | USD 4.59 Billion |

| Market Size (2031) | USD 12.43 Billion |

| Growth Rate (2026 - 2031) | 22.05% CAGR |

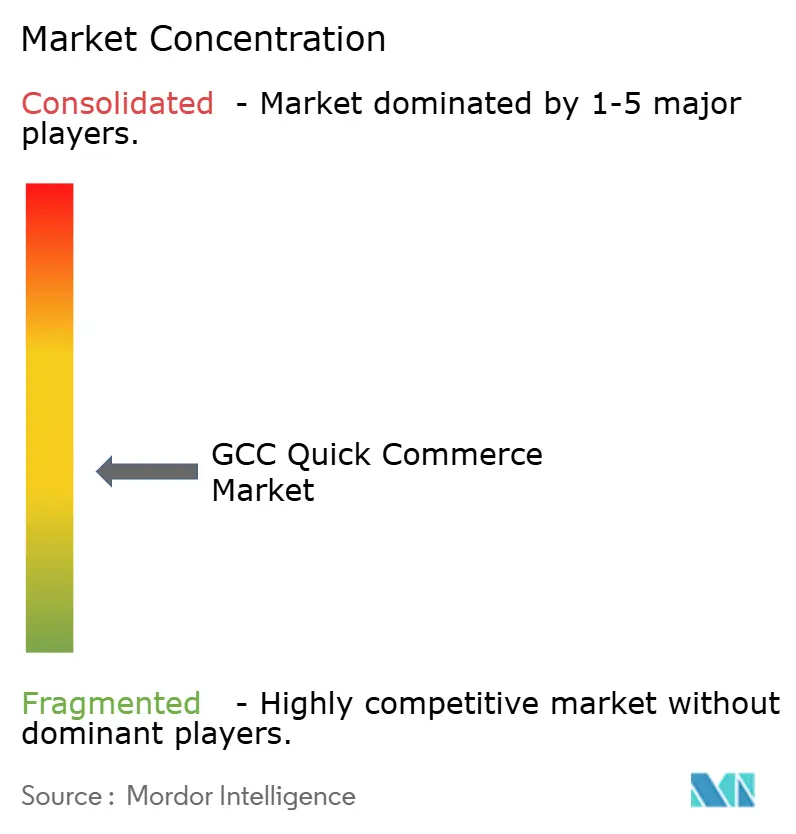

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Quick Commerce Market Analysis by Mordor Intelligence

The GCC Quick Commerce Market size is projected to expand from USD 3.76 billion in 2025 and USD 4.59 billion in 2026 to USD 12.43 billion by 2031, registering a CAGR of 22.05% between 2026 and 2031. The GCC quick commerce market is expanding from a strong base of smartphone use, urban concentration, and digital-first buying behavior that makes rapid delivery part of regular household purchasing. Saudi Arabia set the pace in 2025 with 54.76% of regional demand, and that lead gave it the deepest platform activity, the widest dark store buildout, and the strongest influence on service standards across neighboring markets. Government spending on transport and logistics is improving the physical network that supports fast fulfillment, while rising comfort with digital payments is reducing checkout friction and helping platforms convert small, urgent, and repeat orders more efficiently. The GCC quick commerce market is also widening beyond core grocery missions as operators push into discretionary categories, secondary cities, and cross-market operating models that improve inventory planning and route execution. Competition remains intense, but the direction of travel is clearer than before, with the GCC quick commerce market increasingly favoring scaled ecosystems that can absorb investment cycles, defend delivery speed, and spread data advantages across multiple cities and countries.

Key Report Takeaways

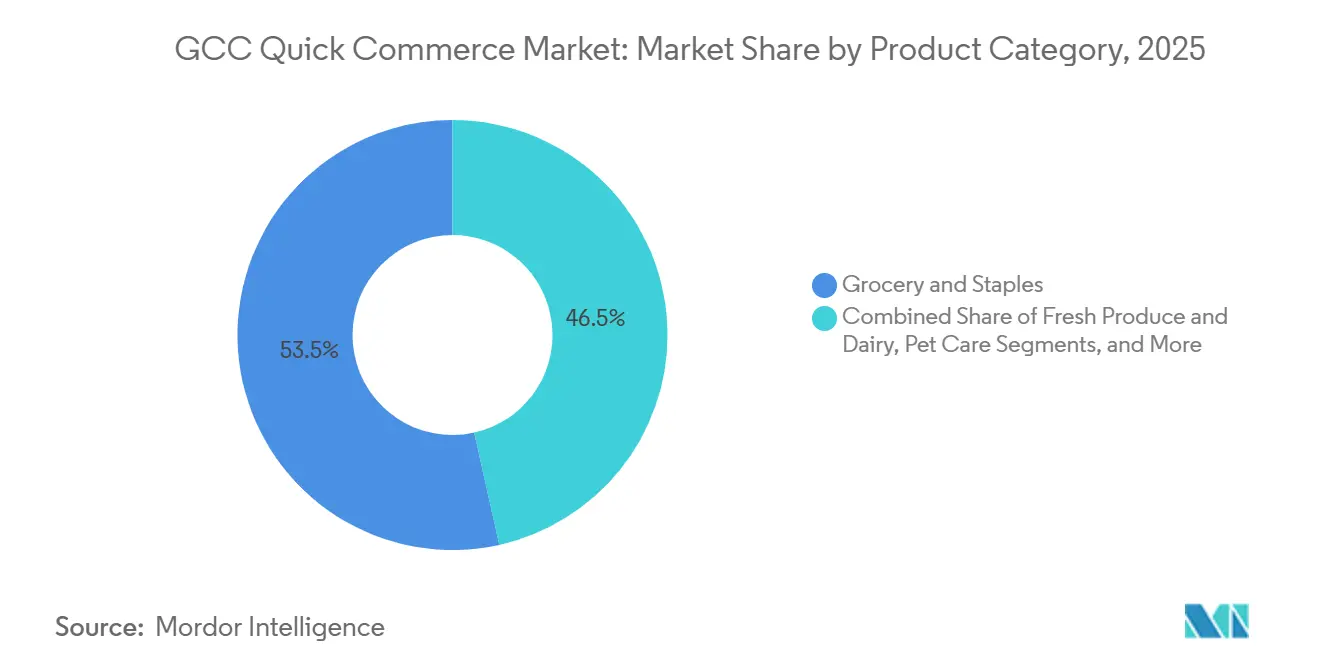

- By product category, grocery and staples led the GCC quick commerce market with 53.48% market share in 2025, while pet care is forecast to expand at a 22.45% CAGR through 2031.

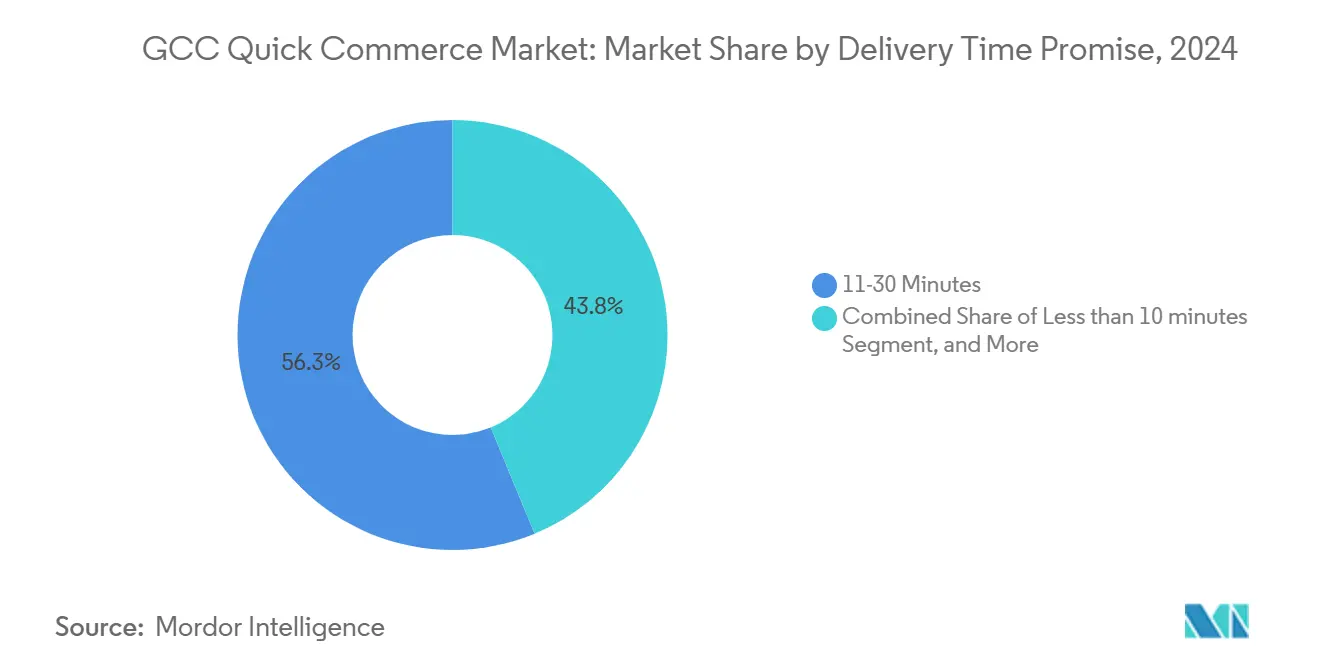

- By delivery time promise, 11-30 minutes held 56.25% share in 2025, while less than 10 minutes is projected to grow at a 22.57% CAGR through 2031.

- By country, Saudi Arabia held 54.76% share in 2025, while Qatar is forecast to expand at a 22.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC Quick Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Smartphone Penetration and Digital Payments | +5.2% | Global, led by United Arab Emirates and Saudi Arabia | Short term (≤ 2 years) |

| High Disposable Income and Demand for Convenience | +4.8% | United Arab Emirates, Saudi Arabia, Qatar, Kuwait | Short term (≤ 2 years) |

| Government Investments in Logistics Infrastructure | +4.1% | GCC-wide, concentrated in Saudi Arabia and UAE | Medium term (2-4 years) |

| Expansion of Dark-Store Networks by Retail Conglomerates | +3.5% | Tier I metros across Saudi Arabia, UAE, and Qatar | Short term (≤ 2 years) |

| Integration of High-Temperature Delivery Robots | +2.3% | Saudi Arabia, UAE core metro zones | Medium term (2-4 years) |

| Cross-Border Digital Nomad Inflow Boosting On-Demand Consumption | +1.4% | UAE, Saudi Arabia, with spill-over to Qatar and Bahrain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Smartphone Penetration and Digital Payments

Mobile use in the Gulf Cooperation Council (GCC) has moved beyond an adoption story and into a condition that supports constant app-based buying. The UAE had 21.9 million active mobile connections by early 2025, and Saudi Arabia had 48.1 million, while smartphone adoption exceeded 95% in both markets.[1]Google and Visa, “State of Commerce, Search and Spend Decoded UAE and Saudi Arabia, 2024-2025,” Think with Google, thinkwithgoogle.com Consumer behavior matched that level of access, with 67% of UAE consumers using mobile devices for their most recent retail purchase in 2025, the highest rate recorded in Visa and PYMNTS Intelligence tracking. For the GCC quick commerce market, this means discovery, checkout, and reorder behavior increasingly happen inside the same device session, which shortens decision time and supports higher order frequency. It also helps the GCC quick commerce market because digital payment habits remove friction from low-ticket and impulse baskets that might otherwise be abandoned. As a result, the GCC quick commerce market benefits from a customer base that is already comfortable with app navigation, stored cards, and repeat digital purchases.

High Disposable Income and Demand for Convenience

Household spending power in the richer GCC markets supports a delivery model built on urgency rather than large planned baskets. Consumers in the UAE, Saudi Arabia, Qatar, and Kuwait are more willing to pay for time savings, which gives fast delivery a daily use case instead of an occasional premium service. The region also has a young urban population profile, and that keeps app-led shopping tied closely to convenience, immediacy, and routine top-up behavior. Climate reinforces this pattern because extreme summer heat makes physical grocery trips less attractive and pushes more replenishment orders into digital channels. That effect is especially visible when households need staples, snacks, beverages, or care products without delaying until a weekly stock-up trip. In practice, the GCC quick commerce market gains from a demand base that values speed, availability, and low-effort ordering as part of normal city life.

Government Investments in Logistics Infrastructure

Public investment is strengthening the transport backbone that quick commerce needs to promise short delivery windows at scale. GCC governments collectively invested USD 110 billion in logistics infrastructure in 2024, and Saudi Arabia accounted for more than USD 74 billion of that total. In March 2026, the GCC Customs Union Authority activated a logistics fast-track route with priority lanes between major ports and airports, supported by advance cargo data exchange and customs relief for essential goods including food and perishables. These measures matter to the GCC quick commerce market because they shorten inbound replenishment cycles and make leaner dark store inventory models easier to sustain. They also improve the case for expansion beyond top metro zones because stock movement becomes more predictable across cities and borders. Over time, the GCC quick commerce market stands to gain from lower replenishment friction, better regional coordination, and stronger economics in secondary service areas.

Expansion of Dark-Store Networks by Retail Conglomerates

Dark stores are becoming a core piece of retail infrastructure rather than a side experiment. Talabat said in May 2026 that it had raised its full-year 2026 investment plan to USD 120 million, with a clear focus on growing talabat mart density and strengthening supply chain capabilities. ADNOC Distribution and noon formalized a strategic partnership in April 2025 to place noon Minutes fulfillment hubs inside ADNOC’s network of 551 service stations and 373 Oasis convenience stores across the UAE.[2]ADNOC Distribution, “ADNOC Distribution and noon Enter Strategic Partnership to Redefine Quick-Commerce Convenience and Speed,” ADNOC Distribution, adnocdistribution.ae Amazon also entered the UAE format in October 2025 with Amazon Now, using Emirates Post offices as micro-fulfillment hubs through its partnership with 7X and supporting grocery supply through LuLu in the UAE. This pattern matters because firms with an existing physical footprint can expand faster and at a lower capital cost than operators building every node from the ground up. The GCC quick commerce market is therefore shifting toward players that combine software, delivery density, and legacy real estate assets into a single operating system.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Customer Acquisition Costs Eroding Unit Economics | -2.8% | GCC-wide, most acute in United Arab Emirates and Saudi Arabia | Short term (≤ 2 years) |

| Regulatory Caps on Delivery Riders' Working Hours | -1.9% | GCC-wide, Qatar leads with WBGT-based thresholds | Medium term (2-4 years) |

| Limited Cold-Chain Capacity for Extreme Heat Deliveries | -1.4% | Saudi Arabia, United Arab Emirates, Oman, secondary effect in Qatar and Kuwait | Medium term (2-4 years) |

| Dependence on Expatriate Labor Vulnerable to Visa Reforms | -1.1% | Saudi Arabia, United Arab Emirates, Kuwait | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Customer Acquisition Costs Eroding Unit Economics

Customer acquisition remains a core financial pressure point because most major operators are still trying to defend frequency, retention, and visibility at the same time. In large GCC cities, several platforms target the same consumer base, which keeps discounting and loyalty incentives active even when operators want to improve margins. That makes it harder for smaller firms to match delivery fee promotions, free trials, and membership perks without weakening their economics. The strongest response has been a shift toward subscription programs and ecosystem-led retention, where recurring fees can offset part of the pressure from order-level promotions. Even so, the burden falls unevenly across the field, and the GCC quick commerce market increasingly rewards platforms that already have scale and repeat-use households. This is one of the clearest reasons the GCC quick commerce market is consolidating around fewer well-funded ecosystems.

Regulatory Caps on Delivery Riders' Working Hours

Heat-related work rules limit rider availability during some of the busiest hours of the day in the Gulf summer. Human Rights Watch documented in 2025 that Saudi Arabia enforced a noon-to-3pm summer ban, the UAE applied a 12:30pm-to-3pm restriction, and Qatar used a wet-bulb globe temperature threshold of 32.1°C for outdoor work.[3]Human Rights Watch, “Gulf States, Protect Workers from Extreme Heat,” Human Rights Watch, hrw.org These protections are important for worker safety, but they also compress delivery capacity when afternoon demand remains high. Platforms must therefore build larger rider pools and more complex shift structures to protect service levels, which adds labor and coordination cost. The impact is not temporary because climate exposure returns every summer and affects operating models across multiple GCC markets. For the GCC quick commerce market, this keeps fulfillment speed tied not only to demand density and technology, but also to labor rules that directly shape daily supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Grocery and Staples Lead While Pet Care Expands Fastest

Grocery and staples held 53.48% of the GCC quick commerce market share in 2025, which kept the category at the center of platform traffic and repeat use. This position reflects how closely immediate delivery fits household replenishment for food, beverages, and everyday essentials. Talabat reported that its grocery and retail GMV grew 45% year over year in Q4 2025 and rose from 27% to 32% of total platform GMV, which showed that leading operators were still widening their retail mix rather than defending a fixed grocery base. Fresh produce and dairy, snacks and beverages, and personal care and OTC pharma remain important because each serves a separate mission, with planned restocking, impulse use, and urgent need all feeding order volume. The GCC quick commerce market therefore continues to rely on grocery as the anchor that brings users back often enough for broader cross-category monetization.

Pet care is forecast to grow at a 22.45% CAGR through 2031, making it the fastest product segment in the GCC quick commerce market size outlook. Growth in this category is tied less to a sudden jump in pet ownership and more to a stronger preference for premium food, hygiene, and care products that consumers want replaced quickly when stock runs low. Electronics and accessories also matter because they bring higher basket values and fit urgent replacement or gift-led buying occasions. Flowers and gifts serve a similar event-driven role, especially in business-heavy markets such as Dubai and Doha where professional and social gifting is more frequent. Home and cleaning supplies remain smaller in basket value, but they support steady reordering between larger grocery missions, which helps the GCC quick commerce industry deepen customer retention across routine household needs.

By Delivery Time Promise: Mid-Speed Delivery Holds the Base While Ultra-Fast Windows Gain Ground

The 11-30 minutes segment accounted for 56.25% of the GCC quick commerce market size in 2025, which made it the leading service promise across the region. This range sits at the point where operational reliability and customer expectations are most aligned. Platforms can support it with dense dark store placement, limited but relevant assortments, and dispatch models that avoid the cost stress of constant sub-10-minute commitments. The 31-60 minutes and more tier still serves an important role because it allows expanded SKU depth and gives operators a practical way to enter less dense districts before fully tightening delivery windows. The GCC quick commerce market has therefore settled on 11-30 minutes as the benchmark that many operators use to balance speed, availability, and cost discipline.

Less than 10 minutes is projected to grow at a 22.57% CAGR through 2031, which makes it the fastest-moving promise within this segment. That rise reflects how the fastest operators are using automation trials, tighter zone mapping, and denser hub networks to compress delivery times in selected urban pockets. It also shows that consumer expectations are not static, because the success of one platform’s speed standard quickly becomes a reference point for rivals in the same city. In the GCC quick commerce market, sub-10-minute delivery is still more selective than universal, but it is already reshaping how companies think about hub spacing, picking speed, and traffic routing. Over time, the window is likely to remain concentrated in the most favorable districts, while still influencing service design across the broader network.

Geography Analysis

Saudi Arabia held 54.76% of the GCC quick commerce market share in 2025, which made it the clear regional center of gravity. Its scale stems from a large urban consumer base, a broad platform presence, and the deepest dark-store footprint in the GCC. Competition in the Kingdom is active, with Talabat, Noon Minutes, HungerStation, Jahez, and Ninja all shaping service expectations across major cities. Saudi logistics policy is also improving the backdrop for expansion, with broader transport modernization and regional customs coordination supporting faster replenishment and better coverage beyond the biggest metro zones. The UAE contributed a smaller share of total value, but it remained a leading test bed for innovation, with Amazon Now launching 15-minute delivery in Dubai and Abu Dhabi and the ADNOC-noon partnership turning existing forecourt assets into fulfillment nodes.

Qatar is forecast to expand at a 22.77% CAGR through 2031, the fastest national pace in the GCC quick commerce market size outlook. Doha’s compact urban geography helps, as shorter delivery supports higher-order density and better route efficiency than in more sprawling city formats. Strong household purchasing power and maturing digital buying habits also support higher frequency and smoother checkout behavior. Jahez’s July 2025 agreement to acquire a 76.56% stake in Snoonu for USD 245 million, valuing the platform at QAR 1.16 billion (USD 320 million), showed how seriously scaled operators view Qatar’s demand trajectory. Kuwait follows a similar affluence-led pattern, but fragmentation among large platforms has kept the path to consolidation and margin improvement less direct.

Oman and Bahrain contributed smaller shares of regional value, but both remain relevant to cross-border expansion planning. Oman’s logistics sector handled more than 143 million tonnes of cargo in 2025, and land transport revenue increased 18%, which points to better connectivity for store replenishment and inbound goods movement. Operators with existing networks in Saudi Arabia, the UAE, or Kuwait can extend technology, sourcing, and operating playbooks into these smaller markets with limited incremental overhead. Oman’s Port Community System is scheduled for 2026, and that should further improve document flow across ports, airports, dry ports, and free zones for supply chains serving this market.

Competitive Landscape

The Gulf Cooperation Council quick commerce market remained fragmented in headline terms in 2025, but it was already consolidating in practice around 4 or 5 scaled ecosystems. Talabat stood out because it reported full-year 2025 GMV of USD 9.5 billion and an adjusted EBITDA margin of 6.5%, which showed that regional scale can produce a workable earnings profile in this format. That matters because the Gulf Cooperation Council quick commerce market is no longer being shaped only by delivery speed, but also by who can fund logistics density, absorb promotions, and keep customer retention high through subscriptions and cross-category breadth. The result is a field where smaller platforms can still win niche demand, but scaled operators set the commercial pace.

Strategic moves in 2025 and 2026 showed how leading companies are trying to widen their advantage. Talabat completed the acquisition of InstaShop in March 2025, and the company said the combined pro forma 2024 grocery and retail GMV exceeded USD 2.5 billion after the deal. Jahez then moved deeper into cross-border expansion by agreeing to acquire a majority stake in Snoonu, which gave it a stronger position in Qatar after earlier building activity in Saudi Arabia, Bahrain, and Kuwait. Amazon took a different route by entering with an asset-light model that reused postal and retail infrastructure instead of building a proprietary fulfillment network from zero. ADNOC Distribution’s alliance with noon showed a similar logic because established service station assets can be converted into quick commerce nodes faster than greenfield sites can be rolled out.

White-space opportunities remain strongest in non-grocery retail, Tier II cities, and service models that can support urgent business replenishment as well as household demand. Pharmacy, beauty, flowers, electronics, and other event-led or urgent-use categories still offer room for deeper assortment and stronger repeat behavior beyond the grocery core. Smaller operators such as Barq, YallaMarket, and ElGrocer are therefore more likely to defend vertical or local positions than to challenge the largest ecosystems across the full Gulf Cooperation Council footprint. The Gulf Cooperation Council quick commerce market is moving toward a structure where scale, infrastructure partnerships, and category breadth matter more than speed claims alone, and that raises the likelihood of further consolidation over the medium term.

GCC Quick Commerce Industry Leaders

Jahez International Company

Talabat UAE Company LLC

HungerStation LLC

Noon UAE Grocery Delivery LLC

Careem Networks FZ-LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Talabat reported Q1 2026 GMV of USD 2.7 billion, up 19% year-on-year, with GCC GMV of USD 2.1 billion representing 79% of the total. The company raised its full-year 2026 investment plan to USD 120 million, focused on scaling talabat mart dark store density and strengthening its talabat pro subscription program across 8 markets.

- April 2026: ADNOC Distribution and Noon celebrated one year of formalizing a strategic partnership through a memorandum of understanding to establish Noon Minutes fulfillment hubs within ADNOC's network of 551 service stations and 373 Oasis convenience stores across the UAE. The partnership integrates AI-powered logistics and the ADNOC Rewards loyalty program with noon's delivery network.

- March 2026: Talabat reported Q1 2026 GMV of USD 2.7 billion, up 19% year-on-year, with GCC GMV of USD 2.1 billion representing 79% of the total. The company raised its full-year 2026 investment plan to USD 120 million, focused on scaling talabat mart dark store density and strengthening its talabat pro subscription program across 8 markets.

- October 2025: Amazon launched Amazon Now, a 15-minute delivery service, in Dubai and Abu Dhabi, converting Emirates Post offices into micro-fulfillment hubs through a partnership with 7x, and partnering with LuLu for grocery supply in the UAE and with Al Othaim in Saudi Arabia. This represents a shift from Amazon's centralized warehouse model to a hyper-local partnership approach.

GCC Quick Commerce Market Report Scope

The GCC Quick Commerce Market is a rapidly expanding industry segment that specializes in ultra-fast delivery services, typically ensuring the delivery of groceries, food, and everyday essentials within minutes to a few hours of order placement.

The GCC Quick Commerce Market is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, and Other Product Categories), Delivery Time Promise (Less than 10 Minutes, 11-30 Minutes, and 31-60 Minutes and More), and Country (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, and Bahrain). The Market Forecasts are Provided in Terms of Value (USD).

| Grocery and Staples |

| Fresh Produce and Dairy |

| Snacks and Beverages |

| Personal Care and OTC Pharma |

| Home and Cleaning Supplies |

| Electronics and Accessories |

| Pet Care |

| Flowers and Gifts |

| Other Product Categories |

| Less than 10 Minutes |

| 11-30 Minutes |

| 31-60 Minutes and More |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Product Category | Grocery and Staples |

| Fresh Produce and Dairy | |

| Snacks and Beverages | |

| Personal Care and OTC Pharma | |

| Home and Cleaning Supplies | |

| Electronics and Accessories | |

| Pet Care | |

| Flowers and Gifts | |

| Other Product Categories | |

| By Delivery Time Promise | Less than 10 Minutes |

| 11-30 Minutes | |

| 31-60 Minutes and More | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

What is the current size of the GCC quick commerce market and how fast is it growing?

The GCC quick commerce market was valued at USD 3.76 billion in 2025 and is forecast to reach USD 12.43 billion by 2031, growing at a 22.05% CAGR during 2026-2031.

Which product category leads demand across GCC quick commerce platforms?

Grocery and staples led demand with 53.48% share in 2025 because rapid delivery fits routine household replenishment better than most other categories.

Which delivery promise is most widely used in the GCC?

The 11-30 minutes window held the largest share at 56.25% in 2025 because it balances speed, operational feasibility, and customer expectations.

Which country is the largest opportunity in the GCC region?

Saudi Arabia led the region with 54.76% share in 2025, supported by platform scale, urban demand concentration, and strong logistics investment.

Which country is growing the fastest through 2031?

Qatar is projected to record the fastest growth at a 22.77% CAGR through 2031, helped by Doha's compact geography and strong consumer purchasing power.

What is driving competition among leading quick commerce platforms in the GCC?

Competition is being shaped by dark store density, infrastructure partnerships, cross-border expansion, and acquisitions such as Talabat-InstaShop and Jahez-Snoonu, while operators also push subscriptions and broader retail assortments.

Page last updated on: