Germany Quick Commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

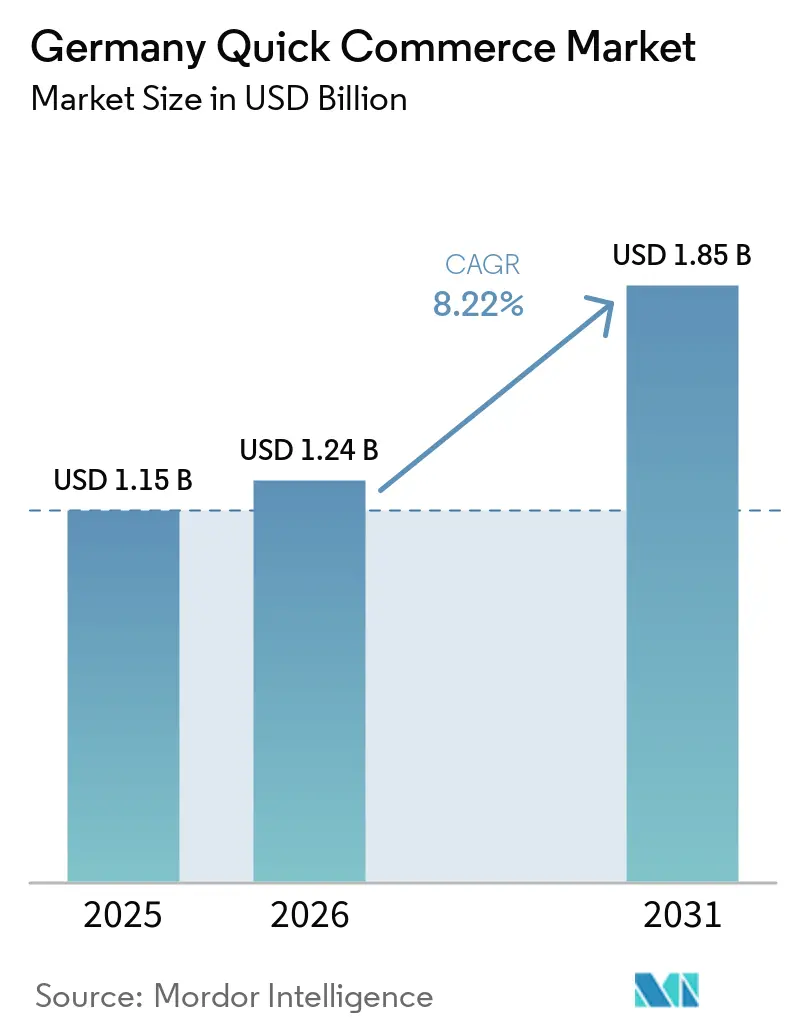

| Base Year Market Size (2025) | USD 1.15 Billion |

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 1.85 Billion |

| Growth Rate (2026 - 2031) | 8.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Quick Commerce Market Analysis by Mordor Intelligence

The Germany quick commerce market size is expected to increase from USD 1.15 billion in 2025 to USD 1.24 billion in 2026 and reach USD 1.85 billion by 2031, growing at a CAGR of 8.22% over 2026-2031. The market entered 2026 with a clearer path to durable growth, because operators are now focusing more on contribution margins, order density, and delivery efficiency than on rapid network expansion. The exits of Getir and Gorillas from Germany in May 2024 removed overlapping dark store capacity and an estimated EUR 560 million, USD 607 million, in competing gross merchandise value from the field, which left the remaining operators in a more disciplined setting. That consolidation reduced the pressure of subsidy-driven competition and improved the economics outlook for the surviving platforms. Demand conditions still support further growth, because Germany has dense urban clusters, a broad base of dual-income households, and younger consumers who increasingly view sub-30-minute delivery as a normal retail option. The next phase of the Germany quick commerce market will depend on which operators can pair convenience with cost control, while retail partnerships, automation, and broader category reach continue to shape expansion.

Key Report Takeaways

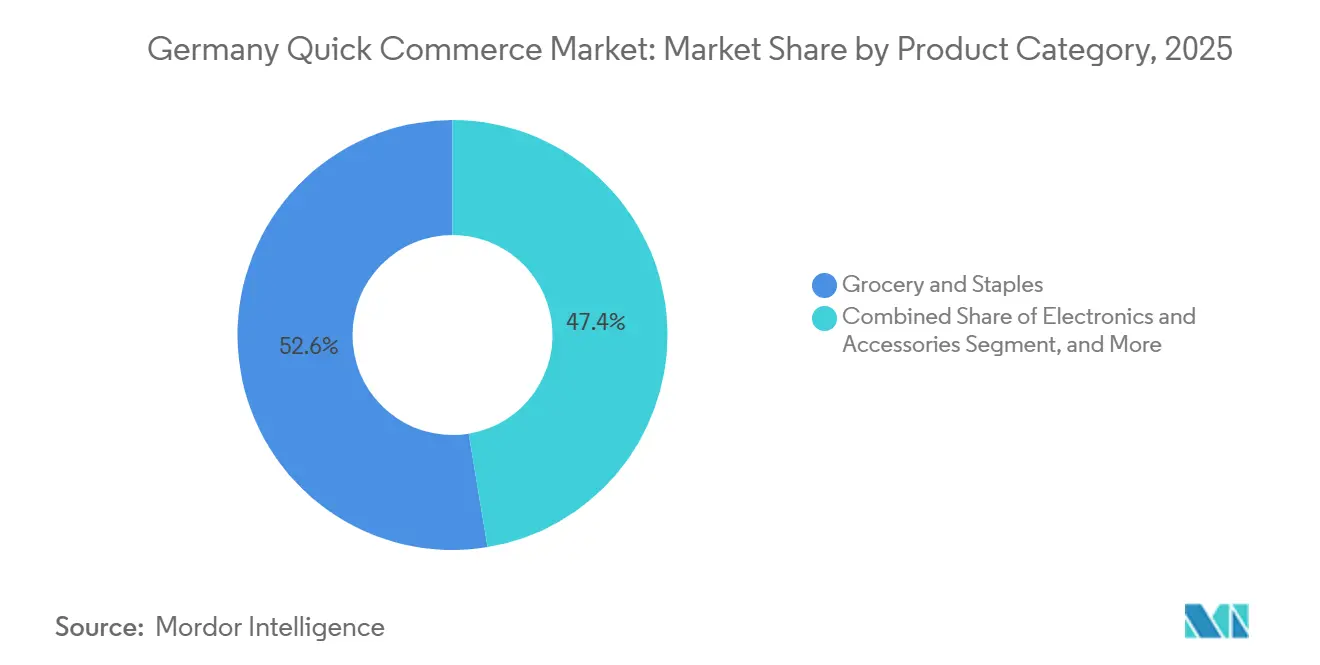

- By product category, Grocery and Staples held 52.61% share in 2025, while Electronics and Accessories is forecast to expand at an 8.54% CAGR through 2031.

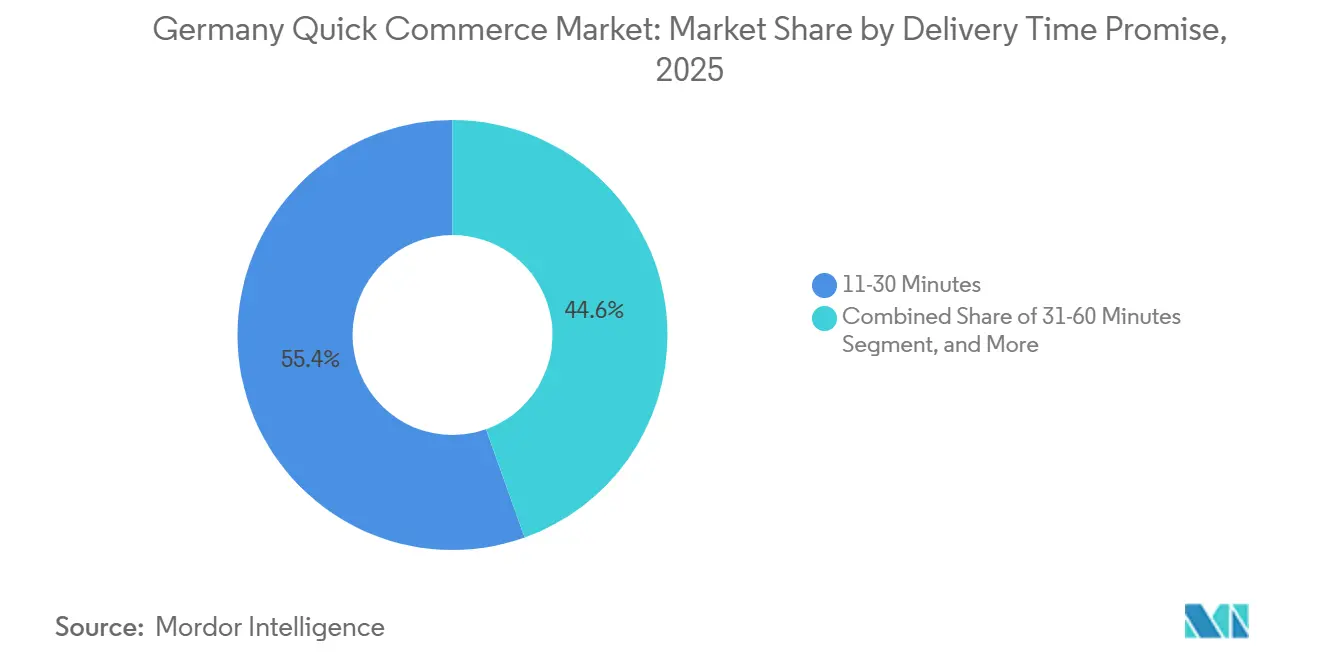

- By delivery time promise, the 11-30-minute tier held 54.45% of Germany quick commerce market share in 2025, while the less than 10-minute segment is forecast to grow at an 8.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Quick Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Convenience Among Dual-Income Households | +2.5% | National, most acute in Berlin, Munich, Hamburg, Frankfurt, and Cologne metropolitan areas | Long term (≥ 4 years) |

| Growing Urban Millennial and Gen Z Population in Major Cities | +2% | National, concentrated in Tier I Metros with spill-over to Tier II cities | Medium term (2-4 years) |

| Increasing Venture Capital and Corporate Funding for Quick Commerce | +1.5% | National, with capital deployment anchored in Berlin-based operators and Hamburg and Munich-area distribution infrastructure | Medium term (2-4 years) |

| Strategic Partnerships Between Quick Commerce Platforms and Supermarket Chains | +0.8% | National, with early gains in cities where Flink and REWE cooperate, 40+ cities via Lieferando | Medium term (2-4 years) |

| Municipal Subsidies for Electric Cargo Bikes That Reduce Delivery Costs | +0.5% | Major urban centers, federal program national in scope, municipal supplements concentrated in Stuttgart, Berlin, Hamburg, and Cologne | Short term (≤ 2 years) |

| Adoption of AI-Driven Micro-Fulfillment Centers to Optimize Order Picking | +0.4% | Asia-Pacific core spill-over, primarily Berlin, Munich, and the Frankfurt area where automated fulfillment centers are already live | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand For Convenience Among Dual-Income Households

Dual-income households remain the most dependable demand base for the Germany quick commerce market. Germany’s Federal Statistical Office reported that couples with children spent an average of EUR 658 (USD 703), per month on food, beverages, and tobacco in 2025 when both partners were in paid employment, which was materially above the national household average.[1]Federal Statistical Office, “Type of Household Consumption Expenditure,” Federal Statistical Office, destatis.de That spending profile matters because these households are not using delivery only for occasional convenience, they are shifting recurring household tasks into paid services. The same pattern is stronger in larger urban households, where time pressure is higher and daily routines are more compressed. This produces more frequent orders, steadier basket formation, and better utilization of neighborhood fulfillment assets. As the Germany quick commerce market becomes more disciplined, operators with dense urban coverage are better placed to convert this repeat demand into more stable unit economics.

Growing Urban Millennial And Gen Z Population In Major Cities

Millennial and Gen Z consumers are reshaping the order mix in the Germany quick commerce market. The user base in these age groups is more comfortable with app-based grocery shopping and more willing to treat fast delivery as a routine purchase channel rather than an occasional service. Their demand is also broader than the early grocery-only model, because younger users increasingly add beauty, household, pet, and small electronics purchases to the same platform journey. That widens the revenue opportunity without requiring the same increase in delivery infrastructure. The importance of this shift is not only higher order frequency, but also better cross-category monetization from the same customer base. In practical terms, this makes younger urban customers central to category expansion and to the next stage of Germany quick commerce market growth.

Increasing Venture Capital And Corporate Funding For Quick Commerce

Capital availability has remained a meaningful support for the Germany quick commerce market, even after the broader venture slowdown. Flink raised USD 150 million in September 2024 and then secured another USD 100 million in March 2026 in a Prosus-led round that valued the company at USD 900 million, which showed renewed investor confidence in operators with a clearer route to disciplined growth. Picnic also raised EUR 430 million (USD 460 million), in November 2025 to expand infrastructure in Eastern and Southern Germany.[2]Prosus, “Prosus Leads US Dollars 100 Million Funding Round in Flink,” Prosus, prosus.com Germany’s wider start-up environment still matters, because the market raised EUR 7.6 billion (USD 8.1 billion), in 2024 financing and the WIN Initiative is targeting EUR 12 billion (USD 14 billion) in venture ecosystem investment by 2030. The pattern is different from 2021, because capital is now being directed toward automation, route efficiency, and fulfillment performance rather than headline land grabs. That change supports the Germany quick commerce market by favoring operators that can prove profitability at the hub level.

Strategic Partnerships Between Quick Commerce Platforms And Supermarket Chains

Platform and supermarket alliances are changing how the Germany quick commerce market is organized. REWE and Lieferando launched an express grocery service in September 2024 across more than 40 German cities, with Flink handling logistics from its dark store network and making more than 3,000 REWE products available within 45 minutes. Amazon and Knuspr expanded their partnership in Germany through early 2025, making Knuspr’s range available to all Amazon customers in Berlin, Rhine-Main, and Munich, not only to Prime members.[3]Amazon Germany, “Knuspr auf Amazon.de: Schnelle Lieferung Frischer Lebensmittel,” About Amazon Deutschland, aboutamazon.de These arrangements help platforms secure broader assortments and stronger retail credibility, while chains gain access to convenience-led demand without building the same last-mile network from scratch. They also reduce procurement friction, which is important in a model where margin discipline matters more than speed alone. The result is a more connected operating model in which the Germany quick commerce market increasingly sits between digital platforms, supermarket supply chains, and localized fulfillment networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Last-Mile Logistics Costs Eroding Unit Economics | -1.8% | National, with sharpest impact in high-density Tier I Metros where rider wages, hub rents, and drop density challenges converge | Long term (≥ 4 years) |

| Intensifying Regulatory Scrutiny on Dark Stores in Residential Areas | -1.2% | National, with enforcement activity most visible in Berlin, regulatory influence extends to Hamburg and Munich as dark store densities increase | Medium term (2-4 years) |

| Rising Competition From Supermarket Click-And-Collect Models | -0.8% | National, concentrated in cities where REWE Abholservice and Picnic operate, compliance factors linked to omnichannel retail infrastructure | Medium term (2-4 years) |

| Limited Cold-Chain Capacity For Fresh Produce In Micro Fulfillment Hubs | -0.5% | National, most binding in Tier II and Tier III cities where automated multi-temperature micro-fulfillment infrastructure is absent | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Last-Mile Logistics Costs Eroding Unit Economics

Last-mile delivery remains the most persistent operating challenge in the Germany quick commerce market. HHL Leipzig Graduate School of Management research cited by Handelsdaten showed average quick commerce delivery costs of EUR 6.80 (USD 7.96) per order against average revenues of EUR 5.18 (USD 6.06), leaving an operational loss of EUR 1.63 (USD 1.17) per drop before warehousing and marketing costs are added. The regulatory backdrop is also becoming more expensive, because the EU Platform Work Directive entered into force in December 2024 and Germany must transpose it into national law by December 2, 2026, which raises the risk of full payroll obligations for riders. Wolt’s earlier shift to a hybrid labor model in Germany increased fixed labor costs by 17%, which illustrates how quickly delivery economics can tighten when labor rules change. The real constraint is not only wages, but also order density, because operators still need 500 to 1,000 daily orders per dark store to approach profitability. That threshold can be reached in central Berlin, but it is harder to sustain in Tier II and Tier III cities where demand is more dispersed.

Intensifying Regulatory Scrutiny On Dark Stores In Residential Areas

Dark store regulation is becoming a more visible restraint on the Germany quick commerce market. A peer-reviewed study published in Standort documented 57 dark store facilities within Berlin’s S-Bahn ring as of 2023 and found that close to 40% were in residential or mixed-use areas, which intensified conflicts over rider traffic, noise, and public space. The study also called for clearer planning treatment under Germany’s building law, because micro-fulfillment hubs still sit between retail and industrial classifications. German cities have not imposed blanket bans like some Dutch municipalities, but complaints and selective enforcement already show how permitting risk can slow network rollout. That matters most in the neighborhoods that operators prefer, because dense residential zones usually offer the strongest order potential. If zoning becomes tighter in Berlin, Hamburg, and Munich, site selection and expansion timelines across the Germany quick commerce market will become more complicated and more expensive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Grocery Dominates, But Discretionary Segments Accelerate

Grocery and Staples held 52.61% share of the Germany quick commerce market size in 2025, which confirmed that daily household replenishment remained the main reason consumers used these services. The category supports repeat ordering and relatively predictable basket formation, which makes it the most manageable starting point for dark store assortment planning. Fresh Produce and Dairy remains the key adjacent category because operators need fresh baskets to deepen household reliance on the platform. Picnic’s Oberhausen fulfillment center, opened in August 2025 with EUR 150 million (USD 160.5 million), in investment, uses 1,500 autonomous robots across 3 temperature zones from -18°C to +20°C and can process up to 33,000 orders per day, which showed that fresh grocery fulfillment at scale is operationally achievable. Electronics and Accessories is forecast to grow at the fastest 8.54% CAGR from 2026 to 2031, which points to a broader use case developing inside the Germany quick commerce industry.

Snacks and Beverages, Personal Care and OTC Pharma, and Home and Cleaning Supplies continue to sit in the middle of the mix because they fit short-notice replenishment needs and usually travel well through existing last-mile networks. Pet Care, Flowers and Gifts, and Other Product Categories remain smaller, but they matter because they raise basket value and improve order economics without requiring the same cold-chain complexity. Wolt’s nationwide partnership with Fressnapf in 2026 showed how platforms are using specialist retail brands to widen the product mix and keep customers inside the same app environment. Across the Germany quick commerce industry, the category shift is less about abandoning grocery and more about layering higher-value discretionary purchases onto an already established convenience habit.

By Delivery Time Promise: 30-Minute Standard Holds, Ultra-Fast Tier Gains Ground

The 11-30-minute segment commanded 54.45% of Germany quick commerce market share in 2025, which showed that the half-hour promise had become the practical service standard. This timing tier works because it lets operators cover a wider radius from each site and makes it easier to improve drop density. Flink’s network of around 160 urban hubs and an average basket size above EUR 45 (USD 48), reflects the operating logic behind this model, where speed is balanced against a viable order value. The 31-60-minute tier remains important for operators such as Picnic, whose scheduled route model traded some speed for a lower-cost structure and helped the company approach EUR 600 million (USD 641 million), in German net sales in 2024. In the Germany quick commerce market, this means the standard offer is now less about maximum speed and more about repeatable convenience at a workable cost.

The less than 10-minute segment is projected to expand at an 8.64% CAGR from 2026 to 2031, even after the withdrawal of the earliest ultra-fast players. That projected growth reflects a different model from the 2021-2022 phase, because newer execution depends more on forecasting tools, robotic picking, and tighter inventory control than on dense store duplication. Knuspr deployed AI robotics from Sereact at its Berlin fulfillment center in late 2025, with each robot processing up to 600 items per hour and the site targeting up to 10,000 daily orders. A January 2024 academic study found that extending lead times from 15 to 60 minutes could reduce costs by up to 57%, which suggests that operators able to preserve speed without absorbing those costs will hold a meaningful advantage in the Germany quick commerce market.

Geography Analysis

Tier I metros dominate the Germany quick commerce market, with a significant share concentrated in cities like Berlin, Munich, and Hamburg. Berlin leads in network density, with numerous dark stores identified within the S-Bahn ring, and a majority of these stores are located in close proximity to competitors, indicating comprehensive inner-city coverage. Studies highlight that dark store placement aligns with districts having stronger purchasing power, which underscores Berlin's central role in the market. Federal support for electric cargo bikes also plays a crucial role at the city level, as Germany’s subsidy program covers a portion of acquisition costs for commercially operated e-cargo bikes, providing a boost to sustainable logistics. Munich and the Rhine-Main corridor have also strengthened their positions, supported by Knuspr’s focus on profitability and its use of robotics in key locations to enhance operational efficiency.

estern Germany has emerged as a highly competitive region for mid-market expansion. Picnic’s strategic hubs and distribution centers support a growing network that aims to bring a significant portion of households within reach in the coming years. Cologne benefits from the collaboration between REWE and Flink, while Hamburg remains a contested market with competition from REWE’s express services, Wolt Market, and Knuspr’s regional expansion efforts. An analysis published in late 2025 revealed that shopping trips by public transport in Germany’s largest cities are significantly higher than the national average, providing delivery platforms with a structural advantage in dense urban areas where reliance on private cars is lower. These factors make western urban corridors strategically vital, combining population density, retail infrastructure, and consumer behavior conducive to app-based replenishment.

Eastern and Southern Germany are less developed in terms of market penetration but represent clear targets for the next investment cycle in the Germany quick commerce market. Picnic’s expansion into cities like Dresden, Leipzig, and Munich, along with Knuspr’s development near Schönefeld to enhance Berlin postal code coverage, demonstrates how operators are extending their reach beyond the initial urban cores. The average exchange rate between the euro and the US dollar used in this analysis remains the basis for financial figures reported for 2024.

Competitive Landscape

Germany’s quick commerce market is moderately concentrated after the 2024 exits of Getir and Gorillas, with Flink leading among pure-play operators while Picnic, Knuspr, REWE, and platform-led models continue to apply meaningful competitive pressure. The market is not dominated by one company, which keeps pricing, fulfillment speed, and category breadth under constant pressure. Strategy has clearly split into 2 models, with asset-light aggregators such as Wolt and Lieferando monetizing partner networks, while vertically integrated operators such as Flink and Picnic keep tighter control over inventory and picking. That divide matters because control over fulfillment can improve reliability, but it also requires higher capital commitment. The Germany quick commerce market is therefore competitive not only in customer acquisition, but also in the choice between platform coordination and owned infrastructure.

The main white-space areas still sit in cold-chain-enabled fresh and frozen delivery outside the top 5 cities, retail media tied to high-frequency order flows, and business supply for small offices and local shops. Flink’s move into Next Day and No Rush alongside its 30-minute core offer showed that operators are widening convenience tiers instead of treating speed as the only point of differentiation. REWE’s Drive and Go pilot and Lidl’s Click and Collect testing showed that established grocers are also reducing friction in ways that can compete with rapid delivery on selected missions. Rohlik Group’s decision to position its Veloq logistics software as a separate licensing proposition also suggested that algorithmic fulfillment is becoming a stronger source of competitive advantage than network density alone. The pending December 2026 transposition deadline for EU platform work rules adds another layer of pressure, because more automation can help operators offset the cost of tighter labor obligations.

Several recent moves show how competition is evolving in practice. Flink’s March 2026 USD 100 million funding round led by Prosus gave the company room for selective hub openings and further operating investment after a difficult valuation period. Picnic’s August 2025 opening of the Oberhausen center and its November 2025 funding round strengthened its ability to scale fresh grocery fulfillment in Germany with a more automated backbone. Amazon and Knuspr broadened their partnership in February 2025, which increased Knuspr’s reach through a high-traffic digital storefront in Berlin, Rhine-Main, and Munich. These moves keep the Germany quick commerce market intense, because each leading player is strengthening a different lever, funding, automation, retail access, or local fulfillment depth.

Germany Quick Commerce Industry Leaders

Flink SE

Getir Germany GmbH

Gorillas Technologies GmbH

Wolt Enterprises Deutschland GmbH

Uber Eats Germany GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Flink SE closed a USD 100 million growth financing round led by Prosus, with participation from existing investors and new backer Btomorrow Ventures, BAT's corporate venture arm, at a post-round valuation of USD 900 million. Funds are earmarked for targeted hub openings in selected German regions through 2026 and operational investments in the Netherlands.

- March 2026: Picnic announced it is on track to surpass EUR 1 billion (USD 1.07 billion), in German revenue in 2026, with the March 2026 launch in Munich adding to coverage in Dresden and Leipzig, entered in 2025. Picnic projects that 40% of German households will be within its delivery range by end-2026.

- February 2026: Flink relaunched on Wolt's platform in Germany, with stores live in Berlin-Mitte and Tempelhof-Schöneberg, reversing its late-2024 consolidation onto Lieferando exclusively. Flink simultaneously explored using its rider fleet for Uber Eats restaurant deliveries as a third-party logistics subcontractor to improve rider utilization.

- February 2026: REWE and Cimcorp completed automation of REWE's fresh food supply chain at its Oranienburg logistics center, which distributes fruit and vegetables to over 370 supermarkets and 580 shops in greater Berlin, processing approximately 29,000 units daily.

Germany Quick Commerce Market Report Scope

The Germany Quick Commerce Market is witnessing substantial growth, driven by companies specializing in the rapid delivery of online orders. These companies primarily focus on groceries, convenience items, and household essentials, catering to the increasing demand for faster and more efficient delivery services. Orders are often fulfilled within a 30-minute timeframe, which has become a key differentiator in this market. The convenience offered by such services is reshaping consumer behavior and driving competition among market players. This trend highlights the growing importance of speed and reliability in the e-commerce landscape.

The Germany Quick Commerce Market Report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, Other Product Categories), Delivery Time Promise (Less than 10 Minutes, 11-30 Minutes, 31-60 Minutes and More). The Market Forecasts are Provided in Terms of Value (USD).

| Grocery and Staples |

| Fresh Produce and Dairy |

| Snacks and Beverages |

| Personal Care and OTC Pharma |

| Home and Cleaning Supplies |

| Electronics and Accessories |

| Pet Care |

| Flowers and Gifts |

| Other Product Categories |

| Less than 10 Minutes |

| 11-30 Minutes |

| 31-60 Minutes and More |

| By Product Category | Grocery and Staples |

| Fresh Produce and Dairy | |

| Snacks and Beverages | |

| Personal Care and OTC Pharma | |

| Home and Cleaning Supplies | |

| Electronics and Accessories | |

| Pet Care | |

| Flowers and Gifts | |

| Other Product Categories | |

| By Delivery Time Promise | Less than 10 Minutes |

| 11-30 Minutes | |

| 31-60 Minutes and More |

Key Questions Answered in the Report

What is the current and forecast size of Germany quick commerce?

The Germany quick commerce market size stands at USD 1.24 billion in 2026 and is forecast to reach USD 1.85 billion by 2031, growing at an 8.22% CAGR over 2026-2031.

Which product category leads spending on rapid delivery platforms in Germany?

Grocery and Staples led in 2025 with a 52.61% share, because repeat food and household replenishment remains the core use case for fast delivery services.

Which delivery window do German consumers prefer most?

The 11-30-minute promise led with 54.45% share in 2025, showing that customers value fast service, but still within a model operators can run more efficiently.

Why did profitability improve after 2024 consolidation?

The exits of Getir and Gorillas removed overlapping dark store capacity and heavy subsidy pressure, which improved the operating setting for the remaining players.

Which companies are shaping competition in Germany?

Flink leads among pure-play operators, while Picnic, Knuspr, REWE, Wolt, and Lieferando shape competition through funding, automation, supermarket partnerships, and broader category reach.

Page last updated on: