Indonesia Quick Commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

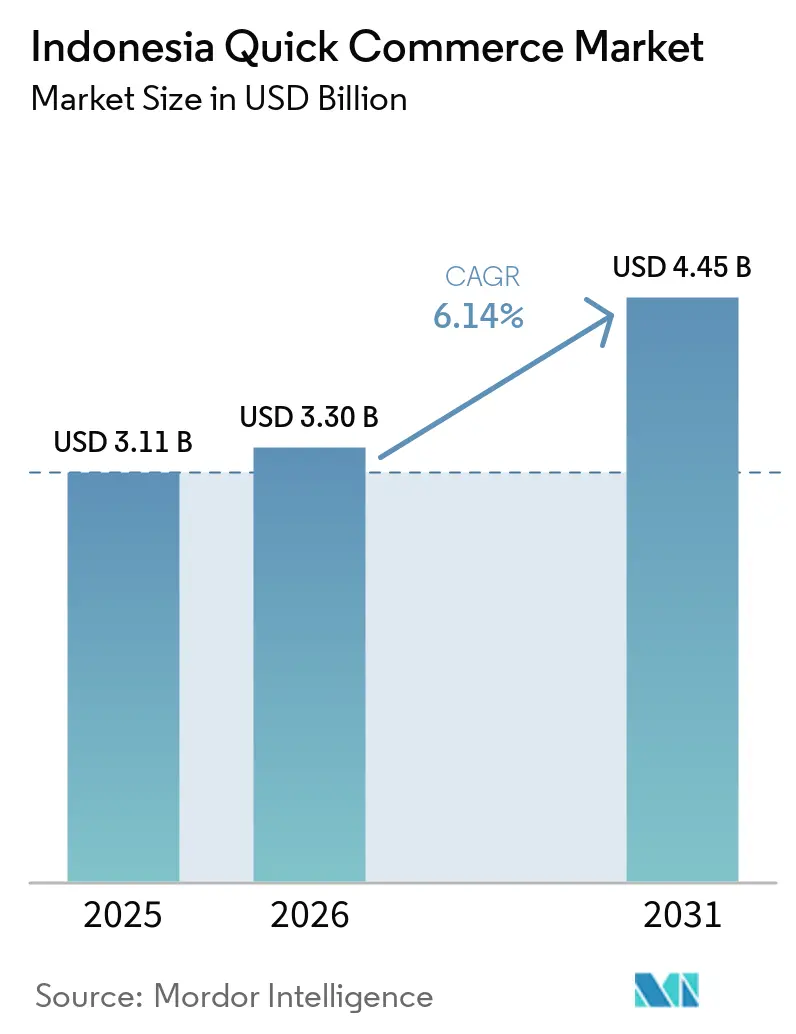

| Base Year Market Size (2025) | USD 3.11 Billion |

| Market Size (2026) | USD 3.30 Billion |

| Market Size (2031) | USD 4.45 Billion |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

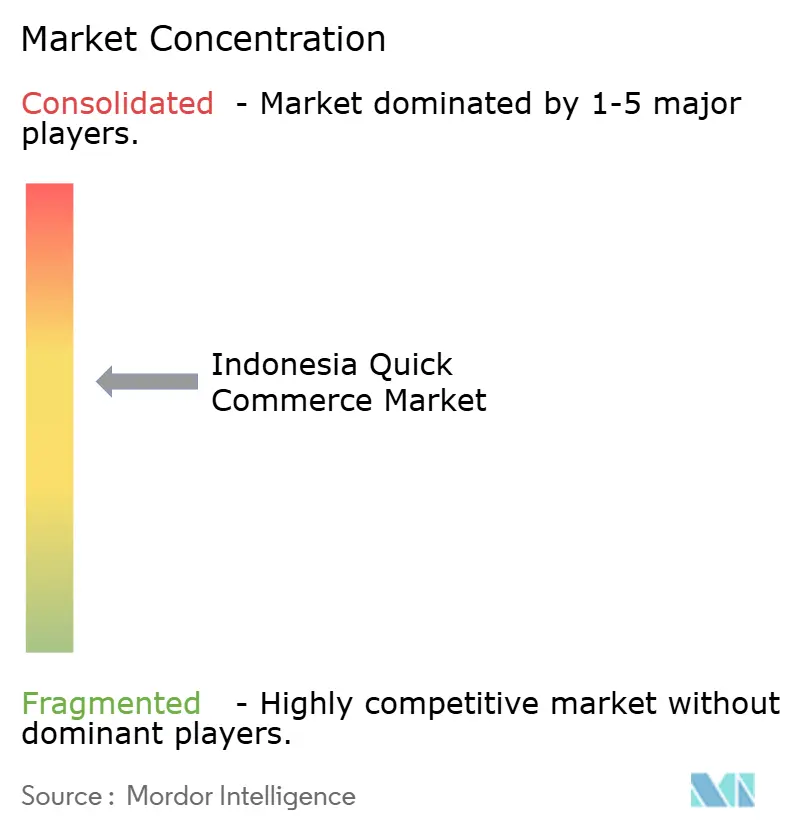

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Quick Commerce Market Analysis by Mordor Intelligence

The Indonesia quick commerce market size is expected to increase from USD 3.11 billion in 2025 to USD 3.30 billion in 2026 and reach USD 4.45 billion by 2031, growing at a CAGR of 6.14% over 2026-2031. The Indonesian quick commerce market is supported by wider mobile-first payment adoption, a broader dark-store footprint outside Jakarta, and super-app ecosystems that now treat instant delivery as a standard service. The country’s digital economy scale is giving Indonesia a fast-growing e-commerce market with a larger, denser demand base across groceries, daily essentials, and time-sensitive household purchases. The Indonesia quick commerce market is also moving out of its earlier subsidy-heavy phase, and operators are now placing more weight on order quality, repeat use, and route efficiency than on raw transaction growth alone. This shift is changing competition across the Indonesia quick commerce market, because scale alone is no longer enough without strong retention, disciplined fulfillment costs, and tighter assortment planning. At the same time, cold-chain constraints outside Java and rising last-mile labor costs are keeping the Indonesian quick commerce market selective about where and how it expands.

Key Report Takeaways

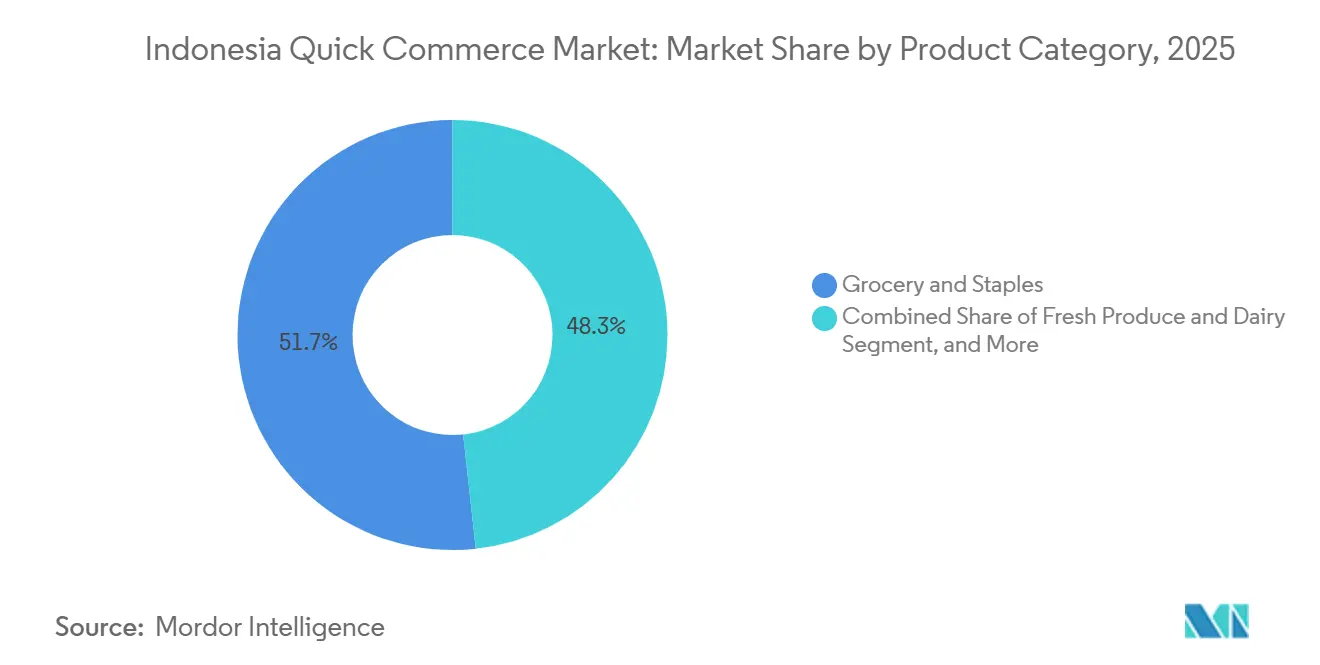

- By product category, grocery and staples led the indonesia quick commerce market with 51.72% in 2025, while pet care is projected to expand at a 6.45% CAGR through 2031.

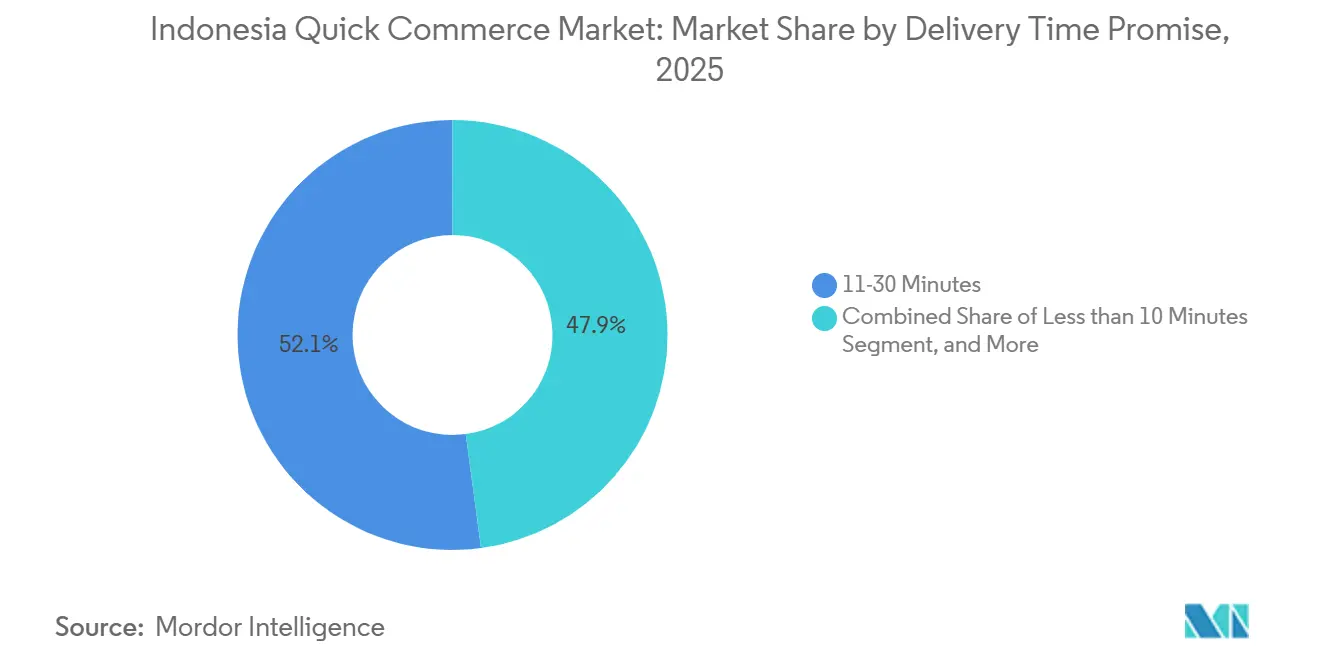

- By delivery time promise, the 11-30 minute window held a 52.11% share in 2025, while the less than 10 minutes segment is projected to grow at a 6.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Quick Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Platforms Integrating 15-Minute Fulfillment Options | +2.0% | Tier I metros, Jakarta, Surabaya, Bandung, expanding to Tier II | Short term (≤ 2 years) |

| Accelerated Urban Middle-Class Adoption of Digital Payments | +1.8% | National, with concentrated gains in Jakarta, Surabaya, Medan, Bali | Short term (≤ 2 years) |

| Expansion of Dark Store Networks Across Tier II Cities | +1.3% | Tier I core, spill-over to Tier II, Semarang, Makassar, Palembang, Balikpapan | Medium term (2-4 years) |

| On-Demand Grocery Partnerships With Modern Trade Chains | +1.0% | National, with early gains in Jakarta, Surabaya, Bandung, Medan | Medium term (2-4 years) |

| Mobile Data Costs Falling Below IDR 5,000 (USD 0.28)/GB | +0.6% | National, with highest impact in Tier II and Tier III cities | Medium term (2-4 years) |

| Growing Investor Appetite For Hyperlocal Logistics Start-Ups | +0.4% | Jakarta and Jabodetabek core, spill-over to Sumatra, Kalimantan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Platforms Integrating 15-Minute Fulfillment Options

The Indonesia quick commerce market is changing because leading super-apps are now placing fast fulfillment inside the main checkout flow instead of treating it as a separate service. Shopee’s instant delivery rollout was available in more than 50 cities, and orders using faster delivery options rose by more than 35% year over year in Q3 2025.[1]Sea Limited, “Third Quarter 2025 Results Investor Briefing,” Sea Limited, sea.com GrabMart also expanded quickly, with management stating that the business grew 1.7x faster than GrabFood in 2025 and increased its user base by 30% year over year. Grab also stated that users who bought groceries and food within the same ecosystem showed 1.5x higher frequency and 1.5x higher spend, which shows why platform bundling matters in the Indonesia quick commerce market. This changes competition because the main fight is moving toward the app interface, where one wallet, one rider pool, and one cart can lift order values without adding a separate customer acquisition burden. Smaller stand-alone operators therefore have less room to win on breadth and are more likely to focus on narrower needs such as fresh, specialty care, or fast pharmacy delivery.

Accelerated Urban Middle-Class Adoption of Digital Payments

The Indonesia quick commerce market is also benefiting from a payment system that is becoming easier to use at both the consumer and merchant levels. Bank Indonesia reported that QRIS transactions reached 13.66 billion in 2025, and total digital payment transactions rose by 39.2% year over year to 14.26 billion transactions.[2]Bank Indonesia, “Payment System Statistics - QRIS and Digital Transaction Data,” Annual Payment System Report, bi.go.id Bank Indonesia also reported 59.53 million QRIS users and 42.75 million merchants at the end of 2025, with around 90% of those merchants classified as micro, small, and medium enterprises. This wider merchant base gives the Indonesia quick commerce market a denser network for local sourcing, vendor settlement, and repeat neighborhood fulfillment. It also strengthens wallet-led loyalty loops, because consumers who keep payments, rewards, and delivery inside the same app usually reorder faster and with less friction. Bank Indonesia’s 2026 payment growth outlook remained strong, with one widely cited estimate pointing to 29.7% growth, which supports further cashless use in the Indonesia quick commerce market.

Expansion of Dark Store Networks Across Tier II Cities

The Indonesia quick commerce market is gaining a wider operational base as dark store and store-conversion models spread beyond the main metro core. Alfamart operated 50 dark stores by 2025 and said it would double that number in 2026, using underperforming store space as a lower-cost conversion route instead of building every site from scratch. Alfagift reached 25 million members by early 2026, while online sales rose from 6% of total revenue in December 2024 to 8% in 2025. This matters because incumbent minimarket chains enter the Indonesia quick commerce market with existing leases, power supply, and ambient inventory already in place, which lowers buildout friction. Indomaret also planned 1,000 new stores across Indonesia by year-end 2025, with clear attention on eastern Indonesia, which shows that physical network expansion is still shaping the future of the Indonesia quick commerce market. As a result, tier II city growth is likely to rely less on pure dark store duplication and more on hybrid store-backed fulfillment models that fit local demand density and lower-capex expansion.

On-Demand Grocery Partnerships with Modern Trade Chains

Partnerships with modern trade chains are helping the Indonesia quick commerce market add more assortment without forcing every operator to carry the full inventory burden alone. BlibliFresh expanded its Pasti Cepat service in 2025 across Jakarta, Depok, Tangerang, and Bekasi, using broader fulfillment points while working with Segari on premium fresh curation. This model is important because fresh goods and daily essentials need trust, consistency, and availability as much as speed, especially in the Indonesia quick commerce market where repeat use depends heavily on staples and household replenishment. Established retail chains also bring refrigeration, compliance routines, and shelf-life control that many smaller operators would struggle to build quickly. The U.S. Department of Commerce noted that cold-chain capacity remains uneven across Indonesia, which makes partnerships with structured retail operators even more valuable for scaling perishables.[3]International Trade Administration, “Indonesia Cold Chain Industry,” U.S. Department of Commerce, trade.gov The result is a hybrid supply model in which platforms handle demand capture and convenience while chain partners reduce sourcing risk and improve fulfillment reliability in the Indonesia quick commerce market. That balance is especially useful outside dense urban cores, where inventory mistakes and product spoilage can damage margins faster than late delivery times.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Rider Churn Due To Gig-Economy Competition | -1.5% | National, concentrated in Jakarta, Surabaya, Bandung, Medan | Short term (≤ 2 years) |

| Rising Last-Mile Labor Costs From Minimum-Wage Hikes | -1.2% | National, with highest impact in DKI Jakarta and surrounding areas | Short term (≤ 2 years) |

| Limited Cold-Chain Infrastructure Outside Java | -0.8% | Outer islands, Kalimantan, Sulawesi, Papua, Nusa Tenggara | Long term (≥ 4 years) |

| Regulatory Uncertainty On Instant Delivery Traffic In Residential Zones | -0.4% | Tier I metros, Tier II cities, Jakarta, Surabaya, Bali | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Rider Churn Due to Gig-Economy Competition

Rider churn remains one of the clearest operating risks in the Indonesia quick commerce market because service quality depends on rider availability at the exact hour and location where demand spikes. A Kompas Research and Development survey covering 482 drivers across 17 provinces found that 57.5% saw partner status as financially harmful, and 83.6% said revenue-sharing arrangements felt unfair. The same survey also found that many active drivers were thinking about exit, which shows why retention remains unstable even when platform demand is strong. This puts the Indonesia quick commerce market in a difficult position, because higher incentives protect fulfillment levels but weaken margins, while lower incentives reduce cost pressure but raise the risk of late delivery and canceled orders. Indonesia’s regulatory approach is also tightening, and the 8% commission cap referenced in discussions around Presidential Regulation No. 27/2026 limits how platforms balance payouts and take rates. Platforms are trying to respond with better dispatch tools, incentive redesign, and seasonal bonuses, but those steps do not fully remove the income instability that drives churn in the Indonesia quick commerce market.

Rising Last-Mile Labor Costs from Minimum-Wage Hikes

The Indonesia quick commerce market is also facing direct cost pressure from higher wage floors in the cities where order volumes are most concentrated. Indonesia’s provincial minimum wage rose by 6.5% in 2025, and Jakarta’s minimum wage reached IDR 5,396.7 (USD 337). This matters because dense urban corridors do not always translate into lower delivery costs, since congestion and idle time can raise the true cost of each completed order in the Indonesian quick commerce market. A study of GrabBike drivers in Jakarta found that the compensation structure explained 89.8% of the variation in driver performance, linking labor economics directly to fulfillment consistency. As a result, operators are pushing harder on route optimization, subscription programs, and vehicle efficiency in order to protect order economics without reducing service quality. The pressure is strongest in Jakarta and nearby areas, where labor competition is intense and the Indonesian quick commerce market cannot easily lower service expectations without risking customer churn.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Staples Anchor Revenue While Pet Care Leads Growth

Grocery and staples held 51.72% of the Indonesia quick commerce market share in 2025, which made staple replenishment the clearest repeat-use case for daily ordering. This category remains the core of the Indonesia quick commerce market because households reorder rice, cooking oil, eggs, packaged foods, and other basics more often than discretionary goods. That repeat cycle gives scaled operators better visibility into basket patterns, which helps them place inventory closer to demand and improve rider routing over time. Fresh produce and dairy, snacks and beverages, and personal care and OTC pharma sit in the next operating tier, but each one places a different burden on storage, picking, and compliance. Home and cleaning supplies and electronics and accessories remain smaller within the Indonesia quick commerce market because they are bought less often and usually do not carry the same urgency as food and everyday essentials.

Pet care is projected to expand at a 6.45% CAGR from 2026 to 2031, making it the fastest-growing product line in this part of the Indonesia quick commerce industry. The growth case is tied to rising urban pet ownership, especially among younger households in tier I metros that already use app-based delivery for routine household needs. This creates a useful overlap for the Indonesia quick commerce market, because recurring pet food orders can be bundled with staple baskets and then supported by automatic reminders or subscription-style offers. Flowers and gifts remain smaller in absolute value, but they can produce stronger order values during seasonal peaks such as Lebaran, Christmas, and Valentine’s Day. Personal care and OTC pharma also offer growth, but operators that want to scale these categories in the Indonesia quick commerce market need stronger compliance discipline, cleaner sourcing, and tighter storage controls than standard grocery-led models require.

By Delivery Time Promise: The 11-30 Minute Window Holds the Core Demand Pool

The 11-30 minute delivery window accounted for 52.11% of the Indonesia quick commerce market size in 2025, which shows that many shoppers value dependable convenience more than extreme speed. This pattern reflects a practical trade-off, because a slightly longer wait often gives consumers lower delivery fees and broader product choice. It also fits the geography of the Indonesia quick commerce market, where many suburban and peri-urban orders sit too far from a dark store to support ultra-fast delivery on a consistent basis. In those areas, the 11-30 minute promise is not a compromise so much as the working standard that balances service quality and cost. The 31-60 minutes and more category still matters as well, especially for store-backed models where staff pick orders from existing minimarket shelves while also serving walk-in shoppers.

The less than 10 minutes segment is projected to expand at a 6.78% CAGR from 2026 to 2031, making it the fastest-growing delivery-time bracket in the Indonesia quick commerce market. Its momentum is strongest in dense urban neighborhoods where dark stores can hold enough stock close to consumers and where rider dispatch is easier to manage. In practice, the Indonesia quick commerce market is using ultra-fast delivery as a habit-building tool, because the first few high-speed orders can pull customers deeper into a broader grocery, payment, and loyalty ecosystem. Once those routines are established, platforms can cross-sell slower categories and improve basket economics without relying on constant discounts. Growth in this segment will still depend on traffic management, zoning discipline, and the ability of operators to sustain fast delivery promises without raising fulfillment costs too sharply.

Geography Analysis

Java remained the core geography of the Indonesia quick commerce market in 2026, with Greater Jakarta contributing the largest provincial base and setting the operating standard for the rest of the country. The island combines stronger road infrastructure, deeper QRIS merchant coverage, and a large urban workforce with spending power that supports frequent household reorders. This is also where O2O fulfillment is most developed, as store-backed delivery hubs and dedicated dark stores operate side by side across the Jabodetabek corridor. Secondary Javanese cities are also becoming more relevant, and Yogyakarta was identified as one of Grab’s faster-growing local markets in 2025, showing that student and young professional demand is broadening the reach of the Indonesia quick commerce market.

Sumatra forms the next major operating zone in the Indonesia quick commerce market, anchored by cities such as Medan, Palembang, and Pekanbaru. Super-app platforms have already built delivery footprints there, which means the base layer for groceries and convenience-led reorders is now in place. The larger constraint is cold-chain depth, because fresh produce and dairy remain harder to scale where storage and temperature control are limited outside the main urban centers. Operators that build reliable refrigerated fulfillment earlier in Sumatra could secure an advantage in the Indonesia quick commerce market that will be difficult for later entrants to match quickly.

Eastern Indonesia, which includes Kalimantan, Sulawesi, Papua, Maluku, and Nusa Tenggara, is still the youngest entry zone, but it is moving faster than many operators expected. Grab’s 2025 consumer reporting highlighted Jayapura as its highest-growth local market, with growth of 53% year over year from a low base. The same reporting also pointed to the role of GrabKios and other digital access points in widening service reach across remote locations, which matters because demand often appears before full retail and logistics depth is available. Internet access and smartphone use continued to widen in 2025, which gives the Indonesia quick commerce market a stronger consumer base even in more dispersed island geographies. Indomaret’s plan to push further into eastern Indonesia suggests that modern trade buildout is still a leading indicator for future quick delivery adoption in these markets.

Competitive Landscape

The Indonesia quick commerce market is moderately concentrated, with Go-To through GoMart, Grab through GrabMart, and Shopee using existing logistics, payments, and app traffic to hold the strongest positions. This structure gives the Indonesia quick commerce market a clear scale bias, because large rider fleets, wallet systems, and food-delivery traffic can all be shared across adjacent services. Shopee’s model shows how powerful this can be, as Sea reported that faster delivery options gained more than 35% year over year in Q3 2025 and that instant delivery is being layered into a much broader commerce ecosystem. At the same time, the Indonesian quick commerce market still leaves room for specialists such as Astro in dense urban pockets where assortment quality and delivery certainty matter as much as app reach. The common thread across the Indonesia quick commerce market is that winning now depends less on subsidy-led scale and more on retention, basket expansion, and fulfillment discipline.

A potential Grab-GoTo combination would narrow the field further and could push the Indonesia quick commerce market closer to a duopoly structure if it goes ahead. Even without a deal, the main platforms already compete by bundling groceries with food delivery, ride-hailing, and digital payments rather than by treating quick delivery as a stand-alone service. Alfamart’s decision to double its dark store count in 2026 while lifting the online share of revenue to 8% in 2025 shows that physical retail chains are also becoming more assertive in the Indonesia quick commerce market. That hybrid model is important because a dense store network can become a fulfillment asset that rivals and even complements super-app scale in selected local zones.

AI, routing, and cost-control tools are becoming more important across the Indonesia quick commerce market as platforms move away from growth-at-all-costs behavior. Grab stated that grocery users who also buy food show 1.5x higher order frequency and 1.5x higher spend, which supports more personalized cross-sell and loyalty strategies. Operators are also looking at route optimization, electric vehicle partnerships, and subscription programs to offset labor pressure while keeping service levels intact. The clearest whitespace in the Indonesia quick commerce market remains fresh and temperature-sensitive delivery in tier II and outer-island locations, where no operator has yet built a strong, scalable lead.

Indonesia Quick Commerce Industry Leaders

PT Indomarco Prismatama

PT GoTo Gojek Tokopedia Tbk

PT Grab Teknologi Indonesia

PT Shopee International Indonesia

PT Bukalapak.com Tbk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Shopee had hiked service fees for its "Gratis Ongkir Ekstra" program in Indonesia. Effective May 2, 2026, rates had surged from 6% to 8% for regular-size products and reached 9.5% for special-size items. This adjustment had pushed effective seller take rates on the platform closer to 20-25% of post-discount sales.

- May 2026: The Indonesian government introduced regulatory proposals for Presidential Regulation No. 27 of 2026, which would cap platform-to-driver revenue at 8%. The policy aims to improve driver welfare and safety standards within the on-demand logistics sector.

- February 2026: Dash Electric, an Indonesia-based electric vehicle logistics startup, had partnered with Sayurbox and had clinched a SAGANA seed investment. Co-funded by Fondation Botnar, the Radical Fund, and Schneider Electric Energy Access Asia, the investment aimed to expand Dash's EV-as-a-Service model, enabling quick commerce operators to cut delivery fuel costs.

- January 2026: Gojek launched a new subscription-based service in Indonesia, offering users unlimited free deliveries and exclusive discounts on its platform. This initiative aimed to strengthen customer loyalty and increase user retention in the highly competitive quick commerce market.

Indonesia Quick Commerce Market Report Scope

The report focuses on analyzing the quick commerce market in Indonesia, which refers to the rapid delivery of goods and services, typically within 30 minutes to a few hours. This market encompasses various product categories, including groceries, personal care items, and other daily essentials, delivered through digital platforms. The study examines market dynamics, trends, growth drivers, challenges, and competitive landscape, providing insights into the forecast period and the factors influencing market growth.

The Indonesia Quick Commerce Market Report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, and More), and Delivery Time Promise (Less than 10 Minutes, 11-30 Minutes, 31-60 Minutes and More). The Market Forecasts are Provided in Terms of Value (USD).

| Grocery and Staples |

| Fresh Produce and Dairy |

| Snacks and Beverages |

| Personal Care and OTC Pharma |

| Home and Cleaning Supplies |

| Electronics and Accessories |

| Pet Care |

| Flowers and Gifts |

| Other Product Categories |

| Less than 10 Minutes |

| 11-30 Minutes |

| 31-60 Minutes and More |

| By Product Category | Grocery and Staples |

| Fresh Produce and Dairy | |

| Snacks and Beverages | |

| Personal Care and OTC Pharma | |

| Home and Cleaning Supplies | |

| Electronics and Accessories | |

| Pet Care | |

| Flowers and Gifts | |

| Other Product Categories | |

| By Delivery Time Promise | Less than 10 Minutes |

| 11-30 Minutes | |

| 31-60 Minutes and More |

Key Questions Answered in the Report

What is the current size and projection of quick commerce in Indonesia?

The Indonesia quick commerce market stood at USD 3.30 billion in 2026 and is expected to reach USD 4.45 billion by 2031.

How fast is quick commerce expected to grow in Indonesia through 2031?

Growth is projected at a 6.14% CAGR from 2026 to 2031, which reflects a shift toward more disciplined and efficiency-led expansion.

Which product category brings in the most revenue?

Grocery and staples led with 51.72% share in 2025, making everyday replenishment the main demand engine.

Which delivery speed do Indonesian shoppers prefer most?

The 11-30 minute window led with 52.11% share in 2025, showing that many users favor a balance between speed, cost, and assortment.

Where is the next wave of expansion likely to come from?

Tier III cities and below are projected to grow the fastest at 6.87% CAGR, although operators are likely to scale there through hybrid store-backed models rather than pure dark stores.

How are leading platforms trying to improve profitability?

Major players are leaning on bundled services, route optimization, wallet-led retention, subscription models, and selective dark-store expansion instead of relying mainly on subsidies.

Page last updated on: