China Quick Commerce Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

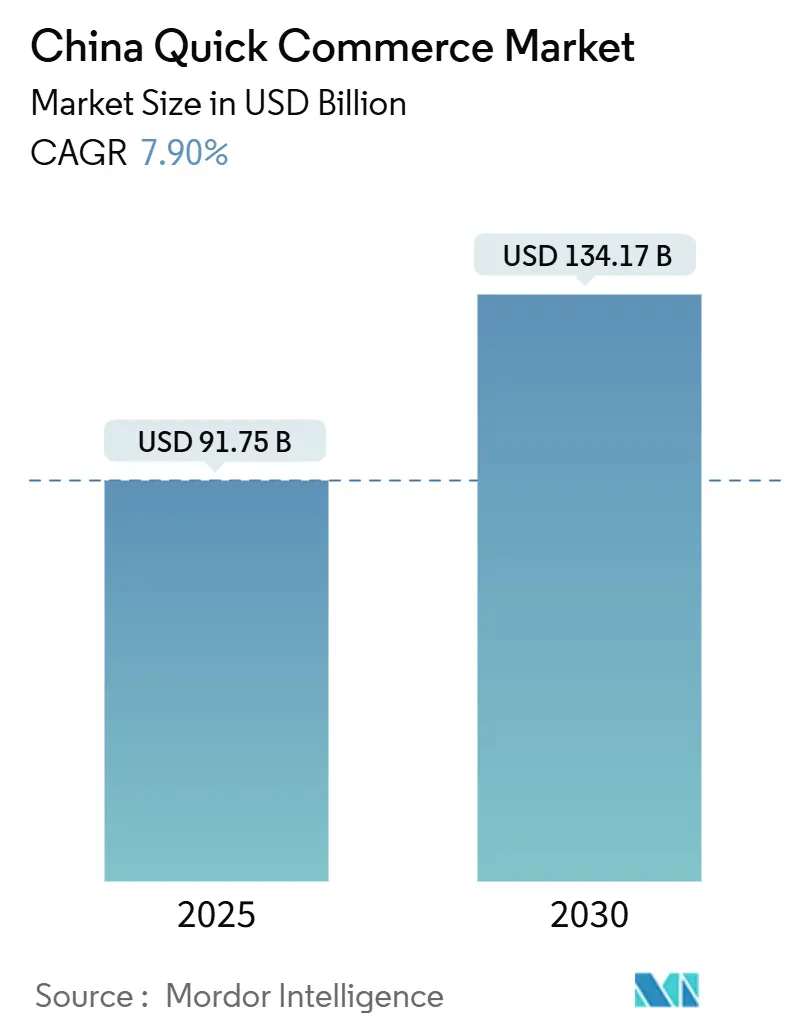

| Market Size (2025) | USD 91.75 Billion |

| Market Size (2030) | USD 134.17 Billion |

| Growth Rate (2025 - 2030) | 7.90% CAGR |

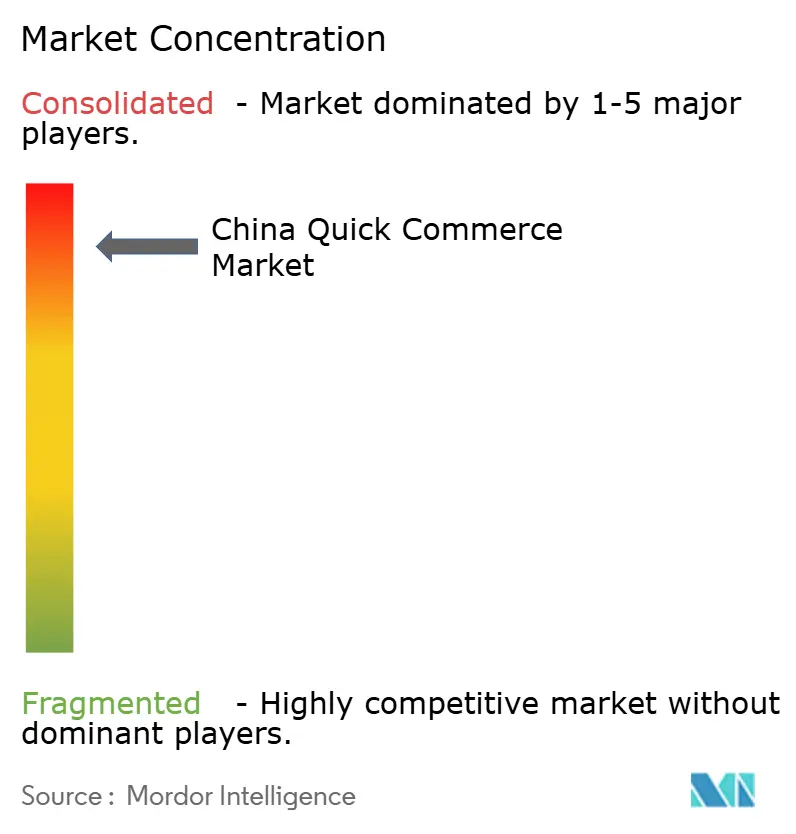

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Quick Commerce Market Analysis by Mordor Intelligence

The China Quick Commerce Market size is estimated at USD 91.75 billion in 2025, and is expected to reach USD 134.17 billion by 2030, at a CAGR of 7.90% during the forecast period (2025-2030).

This projection captures the transition from pandemic-era necessity toward structural consumer behavior, where an ultra-dense network of dark stores, artificial-intelligence pricing engines, and government-sponsored instant-retail pilots re-align the entire retail value chain. Adoption accelerates as sub-30-minute delivery promises become baseline expectations, platform operators roll out vertically integrated cold-chain assets, and local governments harmonize data-security regulations to streamline cross-border logistics. Intensifying platform rivalry drives capital deployment into robotics and drone delivery, while urbanization strategies that target a 70% national rate by 2030 expand the addressable consumer base. At the same time, new data-security rules effective January 2025 clarify cross-border data flows, de-risking international expansion initiatives.

Key Report Takeaways

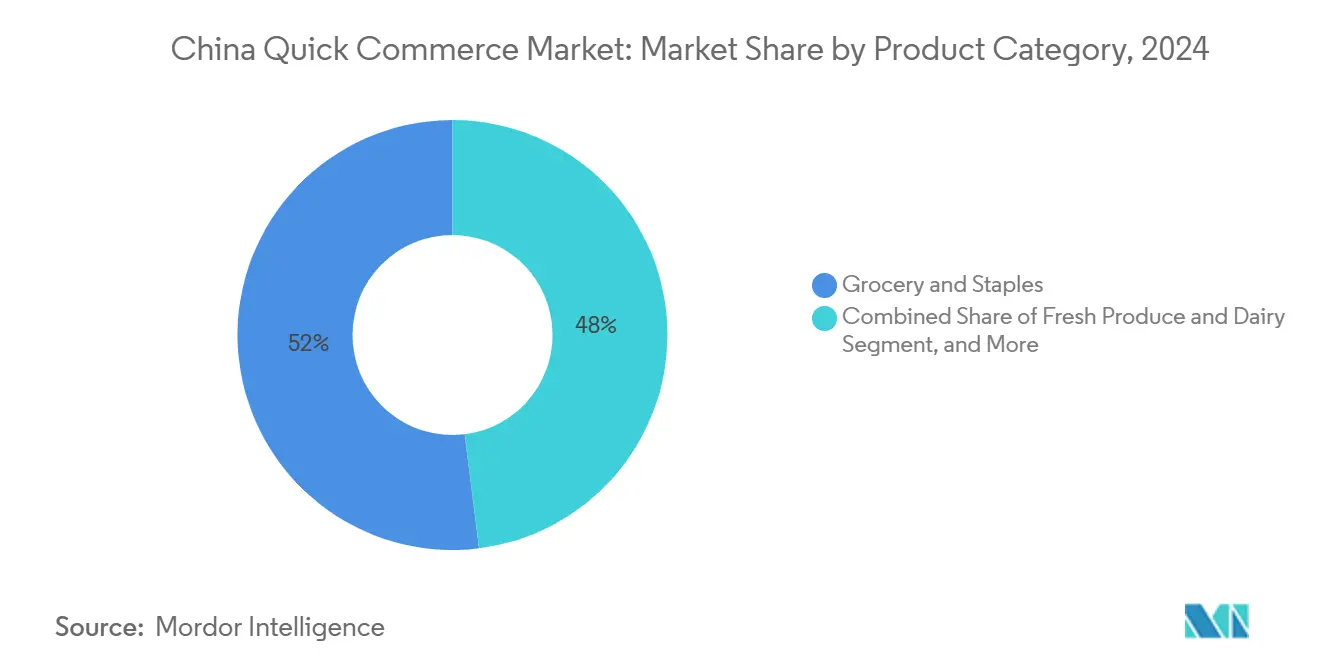

- By product category, Grocery and Staples held 51.96% of the China quick commerce market share in 2024, whereas Electronics and Accessories is projected to expand at a 7.43% CAGR through 2030.

- By delivery-time promise, sub-10-minute orders captured 54.86% share of the China quick commerce market size in 2024, while the 11–30-minute window is forecast to advance at a 7.88% CAGR.

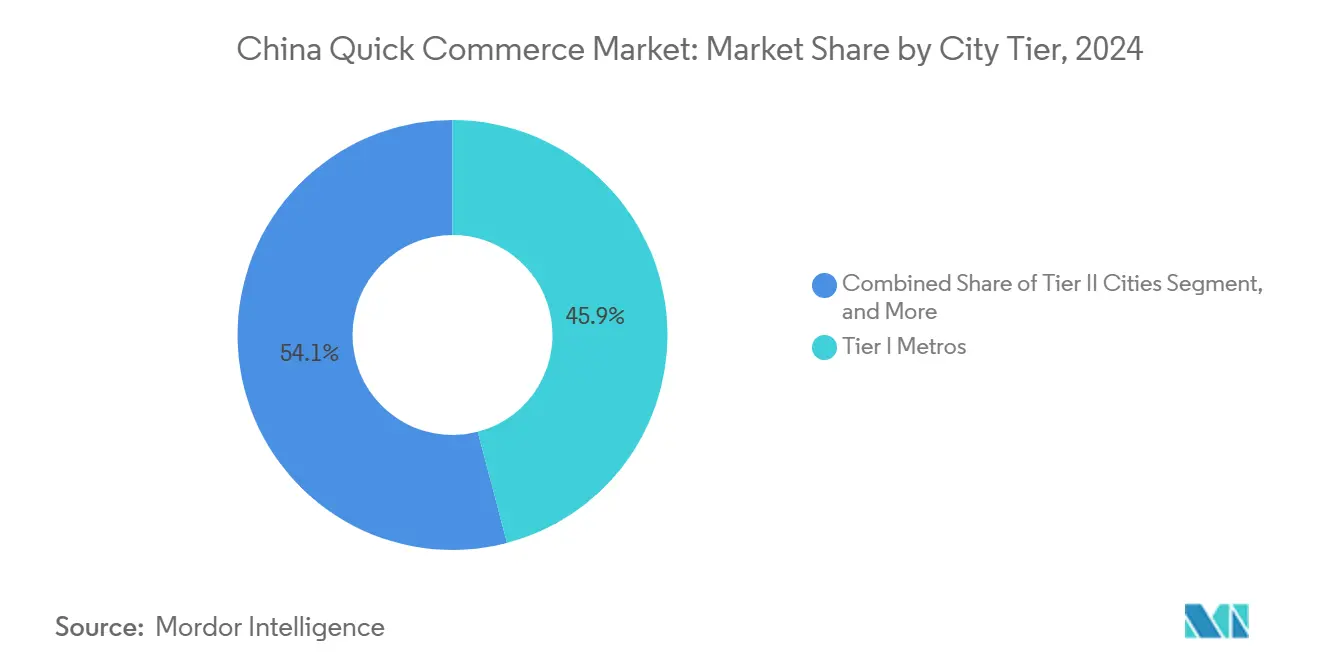

- By city tier, Tier I metros controlled 45.93% revenue in 2024, but Tier II cities lead growth at an 8.07% CAGR to 2030.

- By province, East Chinna holds 36.73% revenue in 2024, and West and Central China is expected to growth at an 7.03% CAGR to 2030.

China Quick Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-dense dark-store networks reduce last-mile costs | +1.2% | Tier I metros, expanding to Tier II cities | Medium term (2-4 years) |

| Gen-AI-powered dynamic pricing boosts conversion | +0.8% | National, with early gains in East and South China | Short term (≤ 2 years) |

| Government-led 'Instant Retail' pilots in 6 provinces | +1.5% | East China, South China, select pilot regions | Long term (≥ 4 years) |

| FMCG brands shifting promo budgets to sub-30-min channels | +0.9% | National, concentrated in urban centers | Medium term (2-4 years) |

| On-demand prescription delivery after e-prescription liberalization | +0.6% | National, with faster adoption in developed regions | Long term (≥ 4 years) |

| Rural live-streaming + instant delivery combos | +0.4% | West and Central China, rural regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ultra-Dense Dark-Store Networks Reduce Last-Mile Costs

Dark-store clusters place inventory within 3 km of consumer catchments, lowering fulfillment costs by 30–40% while shrinking average delivery time to under 15 minutes.[1]Money Department of Guangzhou Daily, “Yuhu Cold-Chain Center Fully Operational,” ycwb.com Meituan already operates more than 6,000 flash-express warehouses across 200 cities, supported by AI-enabled inventory rotation that delivers 85% turnover, far surpassing traditional retail’s 60%. JD.com’s 7Fresh chain broadened the model with 20 new Tianjin hybrid stores that combine consumer front ends with micro-fulfillment space. Cold-chain investments ensure quality in fresh categories; Guangzhou’s Yuhu complex reaches 124,000-ton capacity and has attracted over 400 tenants, illustrating public-private alignment. These assets underpin the China quick commerce market by hardwiring speed and freshness into the supply chain, sealing consumer loyalty even as subsidy-driven promotions fade.

Gen-AI-Powered Dynamic Pricing Boosts Conversion

Real-time price engines ingest demand signals, competitor moves, and consumer click-streams to recalibrate SKUs in milliseconds. Alibaba’s AI-infused 1688 storefront improves conversion for small sellers through automated assortment decisions, while reinforcement-learning models on Tmall outperform human pricing in both revenue and profit lift.[2]Yiming Hu et al., “Dynamic Pricing on E-commerce Platform with Deep Reinforcement Learning,” arxiv.org Regulatory guardrails prohibit discriminatory personalized prices, yet national policy still encourages algorithmic efficiency, allowing platforms to capture incremental margin without breaching consumer-protection norms.[3]Sun Chang, “China’s Regulatory Framework for Dynamic Pricing,” redfame.com As pricing algorithms mature, shopper tolerance for modest premium charges in exchange for guaranteed immediacy climbs, further fortifying monetization pathways for the China quick commerce market.

Government-Led “Instant Retail” Pilots in 6 Provinces

Central and provincial agencies sponsor instant-retail zones that bundle logistics subsidies, AI-computing grants, and data-flow sandboxes. The MIIT blueprint calls for global leadership in quick-commerce-enabling infrastructure by 2027 through partnerships among academia, industry, and public bodies. Anhui’s program earmarks funds for large-scale GPU clusters dedicated to retail AI workloads. Consumption-stimulus vouchers proved catalytic; Shanghai’s USD 70 million campaign triggered USD 1.68 billion in incremental spending, validating policy as a demand accelerant. These pilots reduce regulatory ambiguity, streamline permitting, and unlock municipal data assets, all of which compress time-to-scale for operators expanding the China quick commerce market.

FMCG Brands Shift Promo Budgets to Sub-30-Minute Channels

Fast-moving consumer-goods majors moved 35% of digital promotion spend to quick commerce in 2024, up from 18% in 2023, chasing higher repeat rates and better SKU-level attribution. Snack specialist Three Squirrels posted RMB 2.2 billion in Douyin live-commerce revenue after pivoting toward value SKUs aligned with impulse buying windows. Master Kong maintains 4 million distribution points but now overlays predictive trade-promotion optimization to speak directly to micro-markets during evening peak demand. Such brand realignment lifts paid-media monetization for platform operators and sustains overall order density, reinforcing the flywheel that powers the China quick commerce market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cost of rider social security and benefits | -1.8% | National, acute in Tier I | Short term (≤ 2 years) |

| Traffic congestion charges in big-city downtowns | -0.7% | Tier I metro cores | Medium term (2-4 years) |

| Spoilage risks in fresh products at micro-warehouses | -0.5% | Nationwide fresh segments | Medium term (2-4 years) |

| Local data laws restricting logistics IoT systems | -0.3% | National, varied by province | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cost of Rider Social Security and Benefits

Full social-insurance coverage for China’s 200 million gig-economy workers elevates operating costs. Meituan projects USD 1.4 billion in incremental annual outlays once coverage completes in 2025, while JD.com has already begun paying contributions. Average rider wages climbed 12% year-on-year to USD 1,740 monthly in 2025, outpacing white-collar growth. Platforms must absorb expenses or pass them through as delivery-service fees, risking order-frequency elasticity, particularly for low-ticket grocery baskets that dominate the China quick commerce market.

Traffic Congestion Charges in Big-City Downtowns

Beijing and Shanghai pilot congestion fees that limit freight vehicle access during peak hours. Similar schemes abroad cut emissions, yet in dense Chinese cores they force suburban warehousing and longer lead routes, diluting sub-10-minute promise feasibility. Studies suggest offsetting carbon gains hinge on integrated public-transport upgrades, timelines that stretch several years. For operators, congestion-related detours add cost and hamper fulfillment-center utilization, tempering short-term profit expansion in the China quick commerce market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Grocery Dominance Faces Electronics Disruption

Grocery and Staples generated 51.96% of the China quick commerce market size in 2024 on the back of unavoidable household demand, frequent replenishment, and high basket stickiness. Dark-store placement next to large residential estates corrals volume, ensuring 85% + SKU availability for daily essentials. Electronics and Accessories, though a mere sliver five years ago, is advancing at a 7.43% CAGR, energizing overall category mix. Instant-need use-cases phone chargers, ear buds before commutes, last-minute gaming peripherals align ideally with promise windows under 30 minutes. Fresh Produce and Dairy benefit from superior cold-chain nodes; Guangzhou’s 124,000-ton facility alone cuts spoilage to 1.4% from 7%, unlocking per-order gross-margin gains of 4-6 points. Snacks and Beverages ride live-commerce; Kuaishou handled 1.4 billion agri-orders in 2024, half of them dispatched via rapid fulfilment.

Beyond 2025, Electronics threatens to erode Grocery’s hold as platforms bundle device-repair services and extend interest-free payment options, raising ticket values yet maintaining rapid turn. Category diversification also insulates platforms from grocery’s razor-thin margins, shifting revenue from traffic monetization toward cross-sell profits. Compliance complexities loom: OTC-pharma skus must meet e-prescription rules dating from 2022, while meal-kit ingredients face stricter batch-tracking. Bridging regulatory gaps and enhancing cold-chain transparency will dictate category-level growth rates within the broader China quick commerce market.

By Delivery Time Promise: Sub-10-Minute Leadership Challenged by Balanced Speed

Sub-10-minute orders claimed 54.86% of the China quick commerce market share in 2024, energizing consumer fascination with instant gratification. Yet delivery-economics stress becomes evident; labor and tokenized rider incentives balloon for every additional minute shaved from service windows. Operators now pivot toward the 11–30-minute promise, which is expanding at a 7.88% CAGR, because it allows consolidated multi-drop routes that sustain margin even at lower average order prices. Drone corridors Badaling Great Wall alone processed 300,000 orders provide marketing sizzle but remain niche, reserved for scenic or isolated micro-markets.

As adoption broadens into Tier II cities with more diffuse geography, balanced-speed models dominate. ByteDance’s consolidation of Douyin Supermarket into its one-hour fulfillment product signals an industry shift toward operational sanity. Data showing 92% on-time performance in 20-minute windows versus 61% in 10-minute windows confirms consumers trade a few minutes for reliability. AI fleet-routing, hybrid locker networks, and sidewalk robots further compress variance, making 15-20 minutes the likely equilibrium for the China quick commerce market.

By City Tier: Metro Concentration Yields to Tier II Expansion

Tier I metros amassed 45.93% of 2024 revenue because of population density, mature payment ecosystems, and superior logistics nodes. Saturation, however, drives platforms inland; Tier II cities are set to grow at 8.07% CAGR through 2030. JD Logistics’ “local-warehouse” push into third-tier prefectures slashed lead times from two days to same-day for more than 85% of SKUs, lifting daily order volumes by 20%. Smaller cities bring higher per-drop distances, yet lower real-estate prices permit larger hybrid dark stores that consolidate grocery, general merchandise, and local fresh produce under one roof.

Government urbanization targets 70% by 2030 mean an additional 80 million consumers shift into urban clusters over five years. Their consumption patterns leapfrog toward mobile-first grocery delivery, bypassing large-format hyper-markets entirely. Rural revitalization grants ensure express-delivery coverage down to village level, setting a stepping-stone for eventual quick-commerce roll-outs. Ultimately, geographic diversification hedges platform exposure to congestion fees and wage inflation in saturated metros, cementing nationwide resilience for the China quick commerce market.

Geography Analysis

East China retained 36.73% revenue share in 2024 on the back of Shanghai-anchored cold-chain density and port-adjacent processing hubs. Freshippo’s first-ever annual profit in 2025 emerged chiefly from store format refinements and East China route-density gains. South China contributes significant volume by leveraging Shenzhen-driven manufacturing clusters; cross-border SKUs traverse new e-commerce customs zones in under two hours, a speed unattainable just two years earlier. Its twin-city policy with Hong Kong also incubates AI-driven logistics and accelerates GO-GLOBAL plays as Meituan’s USD 1 billion Brazil entry illustrates.

North China functions as the policy crucible. Drone-delivery pilots obtain early waivers in Beijing suburbs, and same-city freight ITS data feed into national standards committees. Here, quick-commerce players refine compliance models for personal-data handling before rolling updates nationwide, an advantage in navigating the Network Data Security Regulation. West and Central China outpace all regions with a 7.03% CAGR thanks to express-delivery village coverage and burgeoning consumer spend. Academic research on digital empowerment of litchi farmers shows specialty-crop incomes rise 30%, funneling rural money into instant-delivery channels and bringing fresh farm output to urban consumers within hours.

Regional disparity, however, requires nuanced operating models: mountainous Western districts lean on hub-and-spoke cross-dock centers, whereas Pearl-River Delta relies on micro-warehouses every 1.5 km. Compliance with provincial IoT data rules diverges, necessitating localized encryption gateways in Sichuan yet open APIs in Zhejiang. Balancing regulatory heterogeneity, infrastructural variance, and shifting consumption power will define regional winners in the China quick commerce market.

Competitive Landscape

Competition remains moderately concentrated; the top five platforms are estimated to capture just above 60% of GMV, positioning the market at an oligopolistic yet contestable stage. Meituan wields its 760-million-user super-app to cross-sell grocery, pharmacy, and local services, underpinned by the nation’s largest on-demand fleet. JD.com scales hybrid warehouse-store assets, extending its fulfillment prowess into instant grocery, while deepening investments in humanoid robotics that promise long-term cost compression. Alibaba converges Taobao Shangou and Ele.me, achieving 60 million promotional-period orders and inserting local commerce deep within its retail ecosystem.

ByteDance, an insurgent adjacent to social video, integrates Douyin’s algorithmic discovery with rapid delivery, converting viral demand into 30-minute basket-checkouts. Its traffic reservoir challenges incumbents paid-advertising economics. Walmart, unable to match domestic platforms’ rider scale, opts for partnership; its 2024 tie-up with Meituan grants store-level inventory visibility and last-mile reaches unfeasible in-house. Emerging specialists attack niches: cold-chain robotics company Guangdong 10+ enhances freezer warehouse throughput; autonomous vehicle startups pilot sidewalk bots across university campuses.

Regulation exerts dual forces raising operational barriers through labor mandates yet lowering data-transfer friction via uniform national guidelines. Operators that can monetize AI and automation while securing compliance will tilt the battlefield. Competitive vigor, product-mix shifts, and geographic broadening together uphold steady growth for the China quick commerce market amid margin pressures.

China Quick Commerce Industry Leaders

Beijing Sankuai Technology Co., Ltd. (Meituan)

Alibaba Group Holding Ltd. (Ele.me, Freshippo, and Taobao Shangou)

PDD Holdings Inc. (Pinduoduo Kuai Huo)

Yonghui Superstores Co., Ltd.

JD.com, Inc. (JD Daojia and JD Shop Now)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: JD.com and Meituan jointly invested in embodied-AI robotics startups to automate warehouse and customer-service tasks.

- May 2025: Alibaba’s Freshippo recorded its first annual profit and announced plans for nearly 100 new stores in lower-tier cities.

- April 2025: Alibaba upgraded the AI-powered 1688 platform to automate product selection and dynamic pricing for SMEs.

- December 2024: Walmart partnered with Meituan to expand digital-commerce reach in China.

China Quick Commerce Market Report Scope

| Grocery and Staples |

| Fresh Produce and Dairy |

| Snacks and Beverages |

| Personal Care and OTC Pharma |

| Home and Cleaning Supplies |

| Electronics and Accessories |

| Pet Care |

| Flowers and Gifts |

| Other Product Categories |

| Less than 10 Minutes |

| 11–30 Minutes |

| 31–60 Minutes |

| Tier I Metros |

| Tier II Cities |

| Tier III and Below |

| East China |

| South China |

| North China |

| West and Central China |

| By Product Category | Grocery and Staples |

| Fresh Produce and Dairy | |

| Snacks and Beverages | |

| Personal Care and OTC Pharma | |

| Home and Cleaning Supplies | |

| Electronics and Accessories | |

| Pet Care | |

| Flowers and Gifts | |

| Other Product Categories | |

| By Delivery Time Promise | Less than 10 Minutes |

| 11–30 Minutes | |

| 31–60 Minutes | |

| By City Tier | Tier I Metros |

| Tier II Cities | |

| Tier III and Below | |

| By Province | East China |

| South China | |

| North China | |

| West and Central China |

Key Questions Answered in the Report

How large is the China quick commerce market in 2025?

The market stands at USD 91.75 billion in 2025 and is projected to reach USD 134.17 billion by 2030, growing at a 7.9% CAGR.

Which product category dominates rapid-delivery orders in China?

Grocery and Staples lead with 51.96% share of 2024 value, driven by necessity purchases and high order frequency.

What delivery-promise window is growing fastest?

The 11–30-minute segment is expanding at a 7.88% CAGR, balancing consumer speed expectations with operational efficiency.

Why are Tier II cities strategic for quick-commerce platforms?

Rising disposable income and new logistics infrastructure push Tier II revenue growth to an 8.07% CAGR, outpacing saturated Tier I metros.

Page last updated on: