Nut Ingredients Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

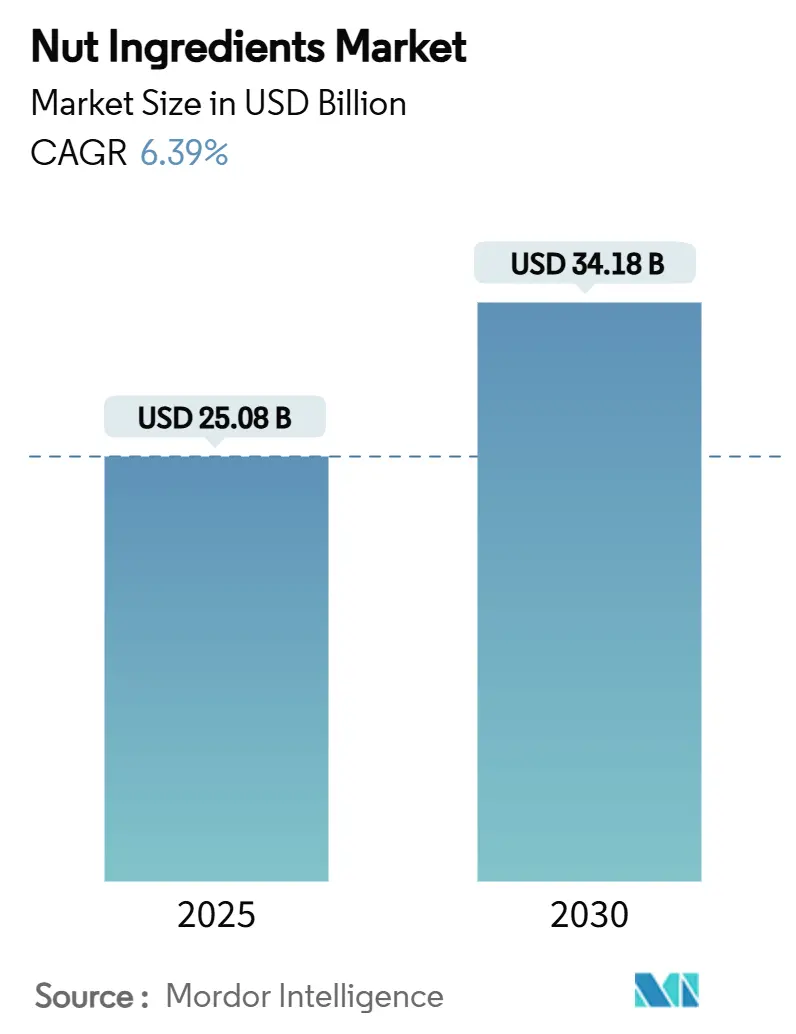

| Market Size (2025) | USD 25.08 Billion |

| Market Size (2030) | USD 34.18 Billion |

| Growth Rate (2025 - 2030) | 6.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Nut Ingredients Market Analysis by Mordor Intelligence

The nut ingredients market size is expected to grow from USD 25.08 billion in 2025 to USD 34.18 billion by 2030, registering a CAGR of 6.39% during the forecast period. This growth is fueled by increasing consumer preference for plant-based nutrition, the rise of clean-label products, and the demand for multifunctional ingredients that enhance both nutritional value and taste. Advancements in processing technologies, supported by significant R&D investments, are improving the functionality of nut powders, pastes, and oils, making them easier to incorporate into automated production systems. Nuts are also gaining popularity as natural sources of protein, healthy fats, and micronutrients, offering a competitive edge in reformulating snacks, bakery products, dairy alternatives, and meat substitutes. The competitive landscape remains moderately intense, with vertically integrated players leveraging economies of scale, supply chain control, and sustainability practices to manage costs and secure premium pricing in value-added applications.

Key Report Takeaways

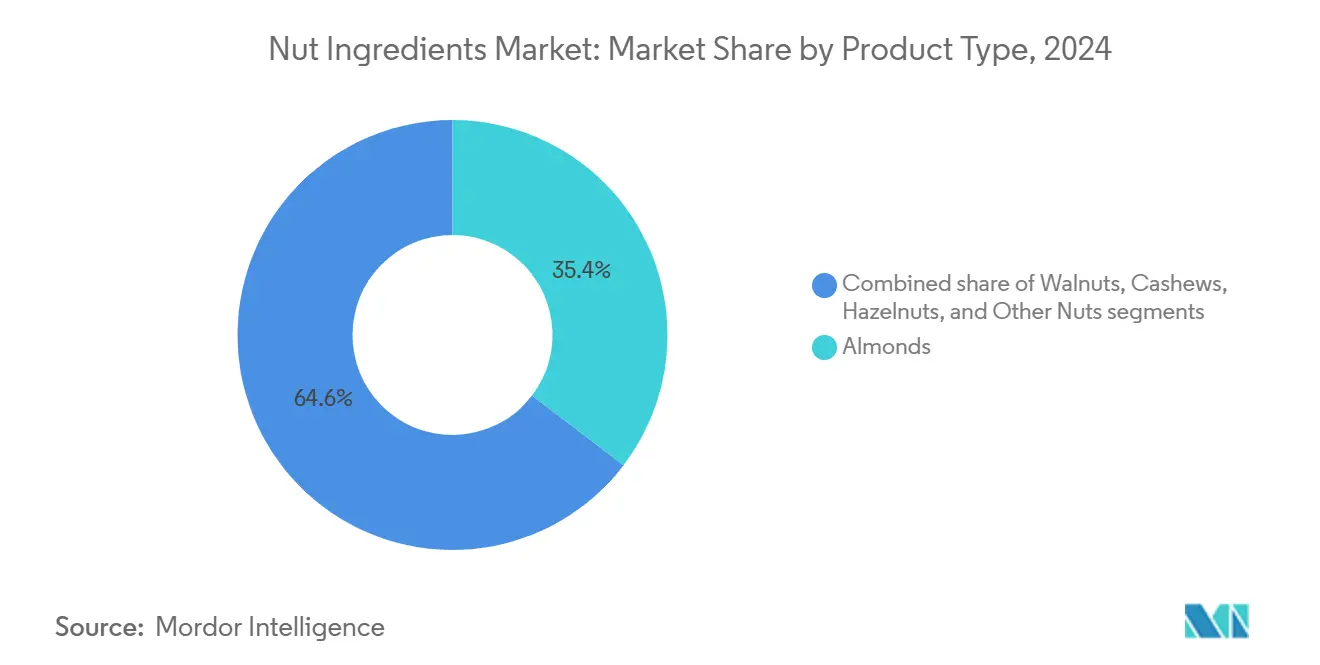

- By product type, almonds led with 35.36% of nut ingredients market share in 2024 while hazelnuts are forecast to register an 8.32% CAGR through 2030.

- By ingredient form, whole nuts captured 41.21% of the nut ingredients market size in 2024, whereas powdered formats are expanding at a 7.77% CAGR to 2030.

- By nature, the conventional segment commanded 91.33% of the nut ingredients market size in 2024, while organic variants represent the fastest trajectory at an 8.15% CAGR through 2030.

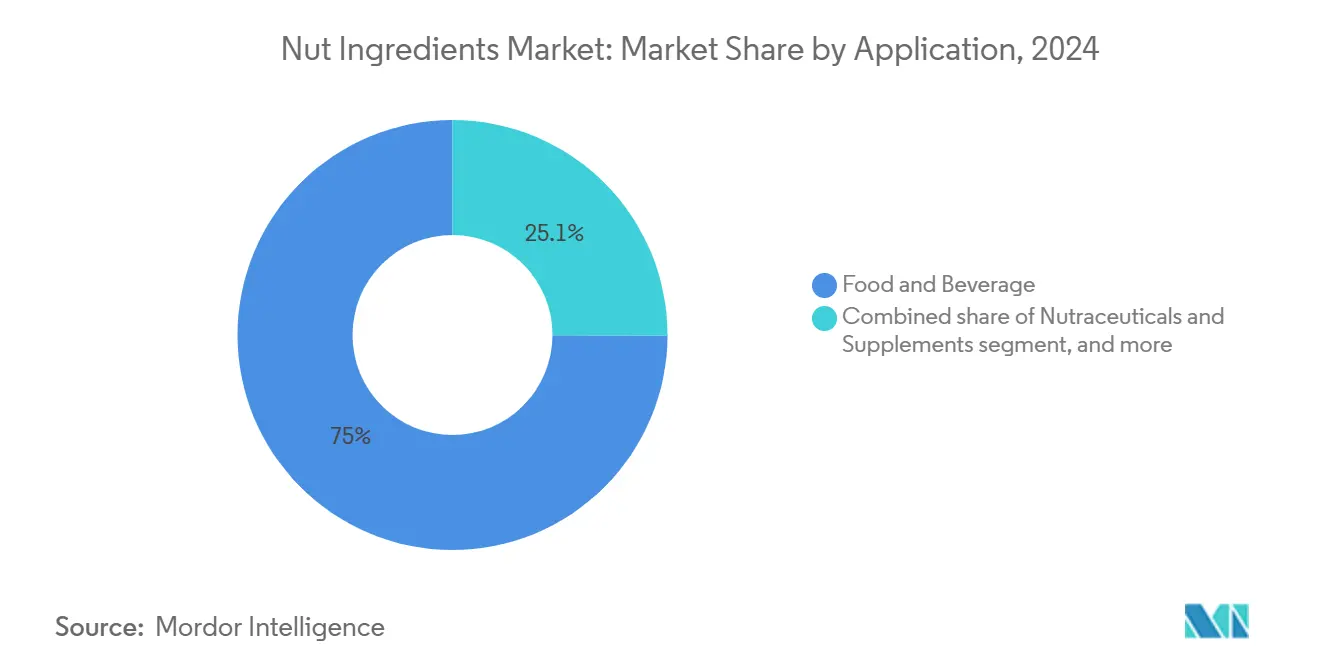

- By application, food and beverage accounted for 74.95% of nut ingredients market share in 2024; nutraceuticals and supplements are advancing at a 9.11% CAGR through 2030.

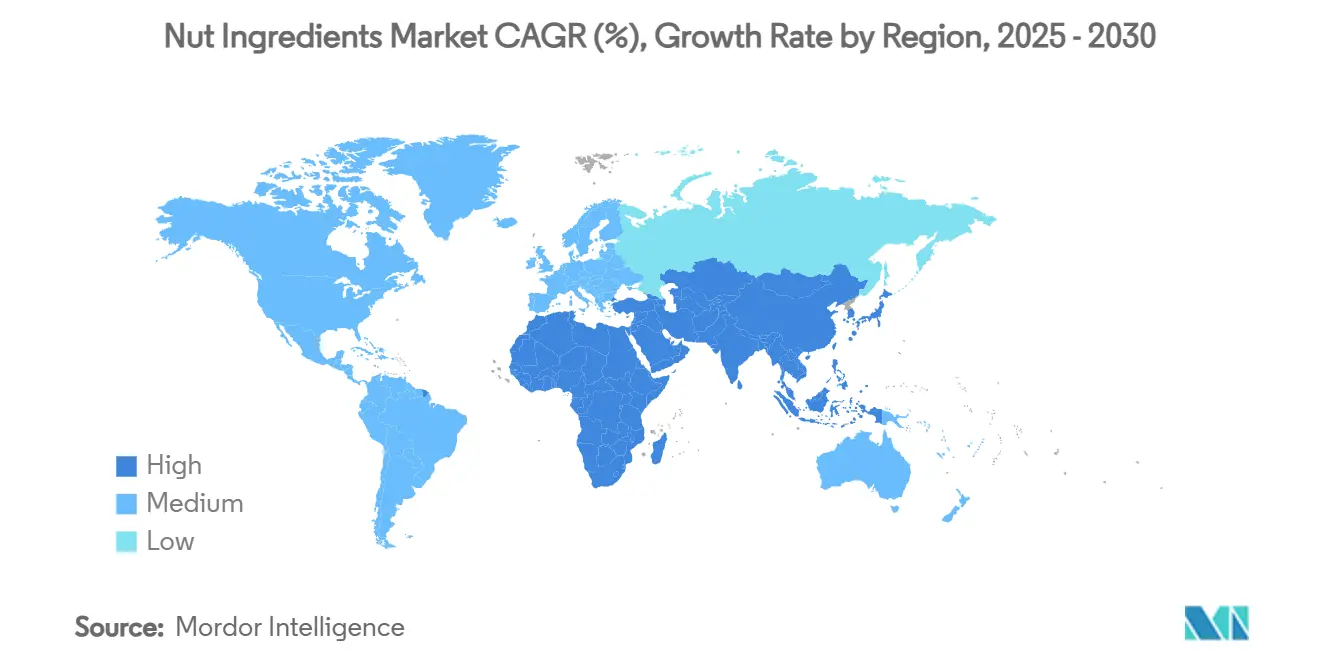

- By geography, Europe held 34.89% of nut ingredients market share in 2024 and Asia-Pacific is forecast to post the highest regional CAGR at 8.53% to 2030.

Global Nut Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer focus on nutritionally rich food | +1.5% | Global, with stronger adoption in North America & Europe | Medium term (2-4 years) |

| Multifunctionality of nuts | +1.2% | Global, particularly Asia-Pacific food processing hubs | Long term (≥ 4 years) |

| Premiumization in snacks, bakery and dairy | +0.8% | Europe & North America, expanding to urban Asia | Short term (≤ 2 years) |

| Nutrition-based product positioning and marketing | +0.6% | Global, led by developed markets | Medium term (2-4 years) |

| Advancements in food technology and processing | +0.4% | North America & Europe, technology transfer to Asia | Long term (≥ 4 years) |

| Innovation in product formulations | +0.3% | Global, concentrated in R&D centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing consumer focus on nutritionally rich food

Health-conscious consumers are transforming ingredient selection in food manufacturing, making nuts a preferred choice for their nutritional value and sensory appeal. The rising demand for plant-based proteins has boosted the use of nut ingredients in meat alternatives, with walnut-based formulations effectively mimicking the texture of animal proteins. Blue Diamond's almond protein powder exemplifies this trend, catering to clean-label developers seeking plant-based ingredients with superior amino acid profiles. Consumers' willingness to pay more for nutritionally enhanced products creates growth opportunities for manufacturers who can clearly highlight the health benefits of nut-derived ingredients. In nutraceuticals, nut oils are increasingly popular for their essential fatty acid profiles, supporting cardiovascular health claims. Advances in nutrition science and food technology are helping formulators enhance nut ingredient functionality while maintaining clean-label standards, meeting the needs of health-conscious consumers.

Multifunctionality of nuts

Food manufacturers are increasingly turning to nut ingredients, drawn by their versatility and the value they bring. Cashews, for instance, are not just creamy bases for dairy alternatives; they also fortify protein in nutritional bars and enhance texture in confections. Innovations in processing allow manufacturers to tap into multiple value streams from a single nut. Take hazelnut oil, for example: it's now a sought-after component in both luxury skincare products and high-heat cooking. This multifunctionality simplifies the supply chain for large-scale food processors, enabling them to meet diverse ingredient needs from a single source. Moreover, advanced processing techniques let manufacturers fine-tune nut ingredient properties, ensuring tailored functionality while preserving nutritional value. As food manufacturers grapple with margin pressures from commodity inflation, the economic efficiency of these multifunctional ingredients becomes paramount in their quest to optimize formulation costs.

Premiumization in snacks, bakery and dairy

Traditional food categories are increasingly using nut ingredients as a premium positioning strategy to stand out in competitive market segments and justify higher price points. For instance, Barry Callebaut incorporates wholesome nuts into multi-textural chocolate inclusions, reflecting the confectionery industry's shift toward more refined flavor profiles that support premium pricing. This premiumization trend is also evident in dairy alternatives, where nut ingredients are utilized to create products that not only meet but exceed conventional dairy standards in terms of nutrition and sensory appeal. In the artisanal bakery segment, nuts are strongly associated with craftsmanship and quality, enabling manufacturers to charge 20-30% higher prices compared to standard formulations. Additionally, advancements in nut processing, such as specialized roasting and seasoning techniques, allow brands to develop distinctive flavor profiles that enhance differentiation in the market. The effectiveness of premiumization strategies is further amplified when combined with transparent sourcing practices that emphasize quality and sustainability, resonating with consumer preferences for ethical and high-quality products.

Nutrition-based product positioning and marketing

Strategic marketing that emphasizes the nutritional and functional benefits of nut ingredients is driving growth in health-conscious consumer markets. Nuts, often referred to as "nutritional gold," are being utilized in innovative ways. Manufacturers are now extracting value from components like peanut skins, which are rich in antioxidants and suitable for functional food applications. Precision nutrition trends allow manufacturers to create targeted health solutions, such as omega-3-rich walnuts for heart health and protein-dense almonds for sports nutrition. The emerging nutricosmetics market bridges food and cosmetics, offering products that deliver both internal health and external beauty benefits. Effective marketing of these dual benefits enables premium pricing and expands market reach. Additionally, peer-reviewed research validating the health claims of nut ingredients strengthens marketing strategies and ensures compliance with health product regulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and price volatility | -0.7% | Global, acute in supply-constrained regions | Short term (≤ 2 years) |

| Growing allergen concerns | -0.5% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Regulatory and compliance challenges | -0.4% | Global, varying by jurisdiction | Long term (≥ 4 years) |

| Quality and shelf life issues | -0.3% | Global, critical in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High cost and price volatility

Food manufacturers relying on nut ingredients face significant margin pressures due to fluctuating commodity prices. Supply-demand imbalances have caused extreme volatility across nut categories. For instance, macadamia prices rose by 37% in 2024 as global demand exceeded production capacity, forcing manufacturers to either absorb higher costs or pass them on to consumers. Climate change has further intensified price volatility by causing unpredictable weather conditions that disrupt production and reduce yield consistency in key regions. Larger manufacturers mitigate these challenges through strategic inventory management and long-term supply contracts. However, smaller processors often lack the financial resources to manage sudden price spikes effectively. Emerging market manufacturers, who primarily compete on price, are particularly vulnerable to rising ingredient costs. While supply chain diversification can help manage price risks, the geographic concentration of nut production limits diversification opportunities for many manufacturers.

Growing allergen concerns

Food manufacturers are grappling with increasing challenges due to rising allergen awareness and stricter labeling requirements, which could limit market access for nut-based products. The FDA's 2022 allergen management guidelines demand robust traceability systems and cross-contamination prevention measures, driving up operational costs, especially for manufacturers handling multiple allergens[1]United States Food and Drug Administration, "Food Allergen Labeling and Consumer Protection Act of 2004 (FALCPA)", www.fda.gov. To mitigate litigation risks from allergen exposure, many manufacturers adopt conservative labeling practices, which can restrict product positioning and market reach. Shared manufacturing facilities face added complexities, as they require stringent cleaning protocols and dedicated production lines to manage cross-contamination risks effectively. While consumer education initiatives are improving awareness and supporting market growth, regulatory uncertainties deter manufacturers from exploring new nut ingredient applications. Advanced processing technologies that reduce allergenicity through protein modification offer potential solutions, but unclear regulatory approval processes in many regions remain a significant barrier.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Almonds Dominate While Hazelnuts Accelerate

In 2024, almonds hold a leading 35.36% market share, driven by California's advanced agricultural systems and efficient processing capabilities that cater to diverse applications. Blue Diamond Growers' almond protein powder highlights the segment's innovation, offering a superior amino acid profile compared to traditional plant proteins while maintaining clean-label standards. Almonds are highly versatile: whole almonds target premium snacks, sliced forms enhance bakery items, and powdered variants support protein fortification in nutraceuticals. Processing advancements enable multiple uses from a single almond variety, such as oil extraction for cosmetics and meal production for animal feed, ensuring maximum utilization and competitive pricing. With reliable supply chains and consistent quality, almonds remain the preferred choice for large-scale food manufacturers.

Hazelnuts are the fastest-growing product segment, with an 8.32% CAGR projected through 2030, supported by their expanding use in premium confectionery and improved processing technologies. The University of Rovira i Virgili's 2025 development of infrared technology enables real-time hazelnut quality assessment without opening packages, reducing costs and improving supply chain efficiency[2]University of Rovira i Virgili, "New Method Identifies Rancid Hazelnuts Without Removing Them From The Bag", www.urv.cat. Advanced equipment now achieves 80% peeling rates with 95% completeness, enhancing processing efficiency. Rising demand from chocolate manufacturers, such as Barry Callebaut incorporating hazelnuts into multi-textural chocolate inclusions, reflects their premium positioning. Additionally, hazelnut oil's high oleic acid content drives its use in cosmetics, offering superior skin conditioning and commanding premium pricing in personal care products.

By Ingredient Form: Whole Nuts Lead While Powders Gain Traction

In 2024, whole nuts hold a 41.21% market share, driven by consumer demand for minimally processed ingredients and manufacturers' preference for simpler handling. Proper storage extends their shelf life to 24 months for unopened containers, preserving both nutritional value and sensory quality. Whole nuts are cost-effective due to reduced processing complexity and lower equipment needs, appealing to both large-scale manufacturers and small producers. Advanced storage methods, such as controlled atmosphere and temperature management, ensure quality during long supply chain cycles. These nuts serve diverse uses, from visually appealing premium snacks to industrial food processing where they are further processed. Additionally, whole nuts resist oxidation better than processed forms, reducing rancidity risks during storage and transport.

The powdered nut segment is growing at a 7.77% CAGR through 2030, fueled by rising demand for ready-to-use ingredients in automated production systems. Improved grinding technologies now achieve precise particle sizes (40-60 mesh) while maintaining nutritional integrity, expanding their use in sensitive formulations. Powdered nuts offer uniform distribution and enhanced bioavailability, making them ideal for nutraceuticals where particle size impacts absorption and efficacy. Innovations in processing allow for controlled oil content, extending shelf life and maintaining flavor for specific applications. This growth aligns with industry trends toward ingredient standardization and supply chain efficiency, as powdered forms simplify handling, ensure consistent quality, and support automated dosing in large-scale production.

By Nature: Conventional Dominates While Organic Expands

In 2024, conventional nut ingredients hold a significant 91.33% market share, driven by established supply chains and cost advantages that cater to mainstream food manufacturers across various applications. Mature agricultural practices and efficient processing infrastructure ensure consistent quality at competitive prices. Economies of scale enable large processors to maintain affordability while meeting acceptable quality standards for mass-market needs. Companies like TreeHouse Foods highlight how conventional processors can enhance sustainability without organic certification, as seen in their goal to achieve 100% RSPO-certified palm oil by 2030. Well-established global distribution networks further reduce supply chain risks and ensure reliable sourcing for high-volume manufacturers. This stability supports market growth while organic alternatives work to strengthen their supply chains and processing capabilities.

Organic nut ingredients are growing rapidly, with an 8.15% CAGR projected through 2030. This growth is fueled by consumers willing to pay premiums for certified sustainable products and the expanding availability of organic food in retail. Regulatory frameworks ensure clear certification standards, protecting premium pricing through controlled supply chains and strict quality requirements. Innovations in organic processing, such as natural preservation methods using biopolymers and essential oils, address past challenges like functionality and shelf life without synthetic additives. Certification standards create entry barriers that protect established suppliers while ensuring high-quality products. The segment's growth reflects rising consumer awareness of sustainability and health benefits, with manufacturers leveraging organic credentials to justify 20-30% price premiums in premium food applications.

By Application: Food & Beverage Dominates While Nutraceuticals Surge

In 2024, food and beverage applications hold a significant 74.95% market share, covering subcategories like bakery, confectionery, dairy alternatives, and plant-based products. These applications capitalize on nuts' functional and nutritional benefits. The segment thrives due to established processing systems and consumer familiarity with nut-based ingredients. Bakery and confectionery lead premiumization trends, where nuts enhance both functionality and visual appeal. Advanced processing methods, such as oil roasting for flavor and shelf life or dry roasting for health-focused products, further boost innovation. Dairy alternatives, a rapidly growing subcategory, use cashew and almond bases to deliver creamy textures and plant-based protein, closely mimicking traditional dairy. This diversity strengthens the segment against market fluctuations and allows manufacturers to maximize ingredient use across various product lines.

Nutraceuticals and supplements are the fastest-growing segment, with a 9.11% CAGR projected through 2030. Rising consumer interest in preventive health and scientific validation of nuts' benefits, such as supporting heart and brain health, drive this growth. Nuts are rich in omega-3 fatty acids, antioxidants, and plant proteins, which support health claims backed by research. Processing advancements enable the extraction of bioactive compounds, like walnut-derived omega-3s, offering plant-based alternatives to fish oil with better oxidative stability. This segment commands premium pricing, often 40-60% higher than conventional food applications, due to targeted health benefits supported by clinical studies. Regulatory support for health claims further strengthens the competitive position of manufacturers who can validate their products' functional advantages.

Geography Analysis

In 2024, Europe holds the largest market share at 34.89%, driven by advanced food processing infrastructure and strong consumer demand for premium nut ingredients. The region benefits from proximity to Turkey, a key hazelnut producer, and its robust processing capabilities that support both local consumption and exports. Germany and the UK lead in consumption due to their thriving bakery and confectionery sectors, while Italy and France boost demand through artisanal food products emphasizing quality and origin. The Netherlands acts as a major distribution hub, leveraging its port and logistics infrastructure to serve the broader European market. Strict European organic certification standards enhance premium positioning, ensuring quality and consumer trust.

Asia-Pacific is the fastest-growing region, with a projected CAGR of 8.53% through 2030, fueled by economic growth and changing demographics. China drives regional expansion with rising urbanization and disposable incomes, increasing demand for premium food products influenced by Western nutrition trends. According to China's National Bureau of Statistics, the average annual per capita disposable income rose from 39,218 yuan in 2023 to approximately 41,300 yuan in 2024, reflecting growing purchasing power[3]National Bureau of Statistics of China, "Average Annual Per Capita Disposable Income Of Households In China From 1990 To 2024", www.stats.gov.cn.. The region's influence on global markets is evident in the "Dubai chocolate phenomenon," where high pistachio demand has caused supply shortages. India's growing food processing sector creates opportunities for nut ingredients in dairy alternatives and traditional sweets. Mature markets like Japan, Australia, and South Korea focus on quality and innovation, while Indonesia, Thailand, and Singapore offer growth potential due to expanding middle-class populations and exposure to global food trends.

North America remains a key market with established supply chains and a focus on convenience and nutrition. The U.S. benefits from California's almond and walnut production, which supports cost-efficient, high-quality supply chains for food manufacturers. Canada emphasizes premium and organic products, aligning with consumer preferences for natural and sustainable ingredients. Mexico is an emerging player, driven by its expanding food processing sector and integration with North American supply chains. In South America, Brazil and Argentina cater to local and export markets, particularly for nuts suited to tropical climates. The Middle East and Africa are smaller but growing markets, with the UAE serving as a distribution hub and South Africa providing processing capabilities for local and European markets.

Competitive Landscape

The nut ingredients market is moderately fragmented, with global leaders and regional suppliers competing across diverse product categories. Major players like Cargill, Olam, and Barry Callebaut maintain strong market positions through integrated supply chains and extensive product portfolios. Meanwhile, smaller companies capitalize on the growing demand for plant-based proteins, clean-label products, and functional nutrition by offering organic, specialty, and locally sourced options, contributing to market fragmentation.

Technological advancements are driving differentiation and efficiency in the market. Innovations in processing, such as automated macadamia processing systems with capacities of 500-1000 kg/h, enhance product functionality, improve consistency, and reduce costs, giving companies a competitive edge while supporting economies of scale.

Emerging opportunities lie in niche applications like nutricosmetics and advanced protein formulations. Smaller players can leverage these segments to establish a strong presence before larger competitors recognize and enter these markets.

Nut Ingredients Industry Leaders

-

Blue Diamond Growers

-

Olam Food Ingredients

-

Archer Daniels Midland Company (ADM)

-

Barry Callebaut AG

-

John B. Sanfilippo & Son Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: eatThis Superfood™ has launched its new line of Roasted Foxnuts (Makhana) in the United States. The brand, known for its commitment to natural, nutrient-rich snacking, introduces four unique flavor profiles: BBQ, Organic Mint, Sea Salt Caramel, and Chili.

- November 2024: KP Snacks, part of the Intersnack Group, has acquired Whole Earth Foods from Ecotone, marking a significant expansion into the nut butter market. Whole Earth, best known as the UK’s leading peanut butter brand with a strong footprint across Europe, brings both nut butters and soft drinks to the KP portfolio.

- September 2024: Dodan Foods has expanded its product line by launching a natural, creamy cashew butter made solely from premium cashew nuts. According to the brand, this new product is designed to offer a rich, velvety smooth texture with no additives or preservatives, appealing to health-conscious consumers seeking nutritious nut-based spreads.

- August 2024: Sitavatika launched a premium range of nuts and dry fruits, including cashew nuts, makhana, almonds, pistachios, and more, all carefully handpicked for discerning consumers. According to the brand, this expansion broadens its product portfolio beyond spices, reinforcing the brand’s reputation for delivering 100% pure, natural produce in the Indian market.

Global Nut Ingredients Market Report Scope

| Almonds |

| Walnuts |

| Cashews |

| Hazelnuts |

| Other Nuts |

| Whole |

| Sliced/Chopped |

| Roasted |

| Powders |

| Other Forms (Pastes, Oils) |

| Conventional |

| Organic |

| Food and Beverage | Bakery and Confectionery |

| Dairy Alternatives and Plant-Based Products | |

| Snacks | |

| Meat Alternatives | |

| Culinary and Seasonings | |

| Beverages and Nutritional Bars | |

| Nutraceuticals and Supplements | |

| Cosmetics and Personal Care | |

| Animal Feed and Pet Food |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Almonds | |

| Walnuts | ||

| Cashews | ||

| Hazelnuts | ||

| Other Nuts | ||

| By Ingredient Form | Whole | |

| Sliced/Chopped | ||

| Roasted | ||

| Powders | ||

| Other Forms (Pastes, Oils) | ||

| By Nature | Conventional | |

| Organic | ||

| By Application | Food and Beverage | Bakery and Confectionery |

| Dairy Alternatives and Plant-Based Products | ||

| Snacks | ||

| Meat Alternatives | ||

| Culinary and Seasonings | ||

| Beverages and Nutritional Bars | ||

| Nutraceuticals and Supplements | ||

| Cosmetics and Personal Care | ||

| Animal Feed and Pet Food | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the nut ingredients market in 2025?

The nut ingredients market size is USD 25.08 billion in 2025 with a forecast to reach USD 34.18 billion by 2030 at a 6.39% CAGR.

Which nut type generates the greatest revenue?

Almonds occupy 35.36% of global revenue, thanks to broad functionality in bakery, dairy alternatives, and nutritional powders.

What region is expanding fastest for nut ingredients?

Asia-Pacific shows the highest CAGR at 8.53% through 2030, driven by rising incomes, urbanization, and growing food-processing capacity.

Which ingredient form is gaining traction with manufacturers?

Powdered nut formats are advancing at a 7.77% CAGR because they integrate seamlessly into automated lines and deliver uniform dispersion.

Page last updated on: