Halal Ingredients Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

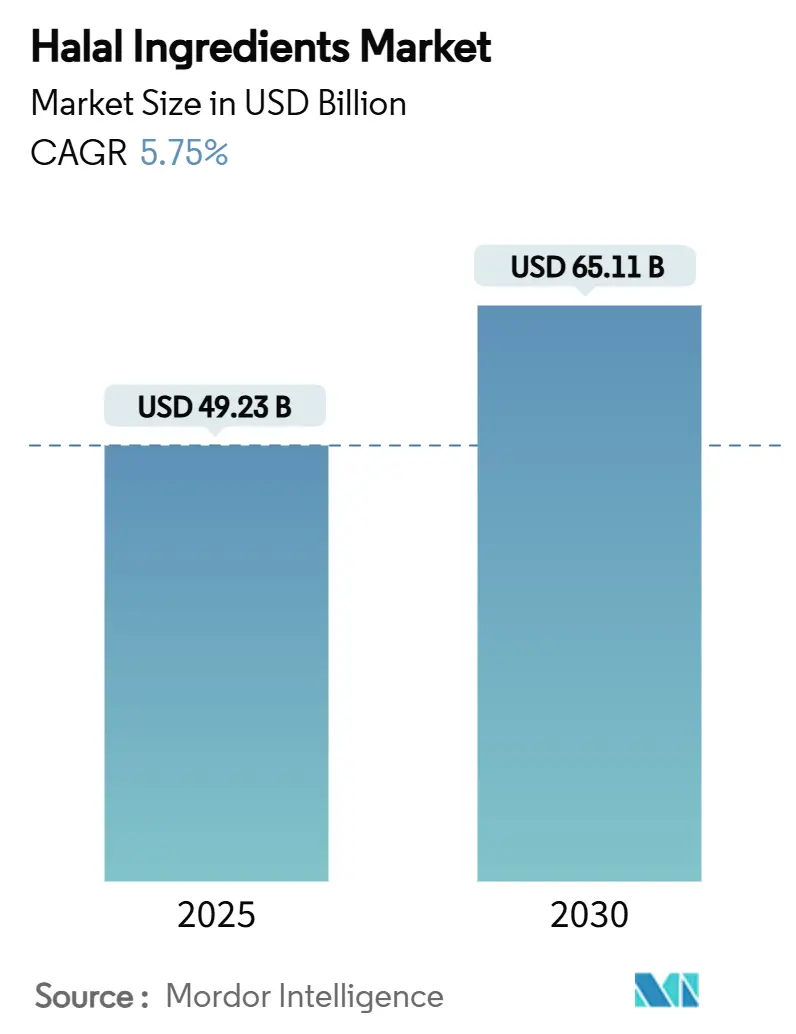

| Market Size (2025) | USD 49.23 Billion |

| Market Size (2030) | USD 65.11 Billion |

| Growth Rate (2025 - 2030) | 5.75% CAGR |

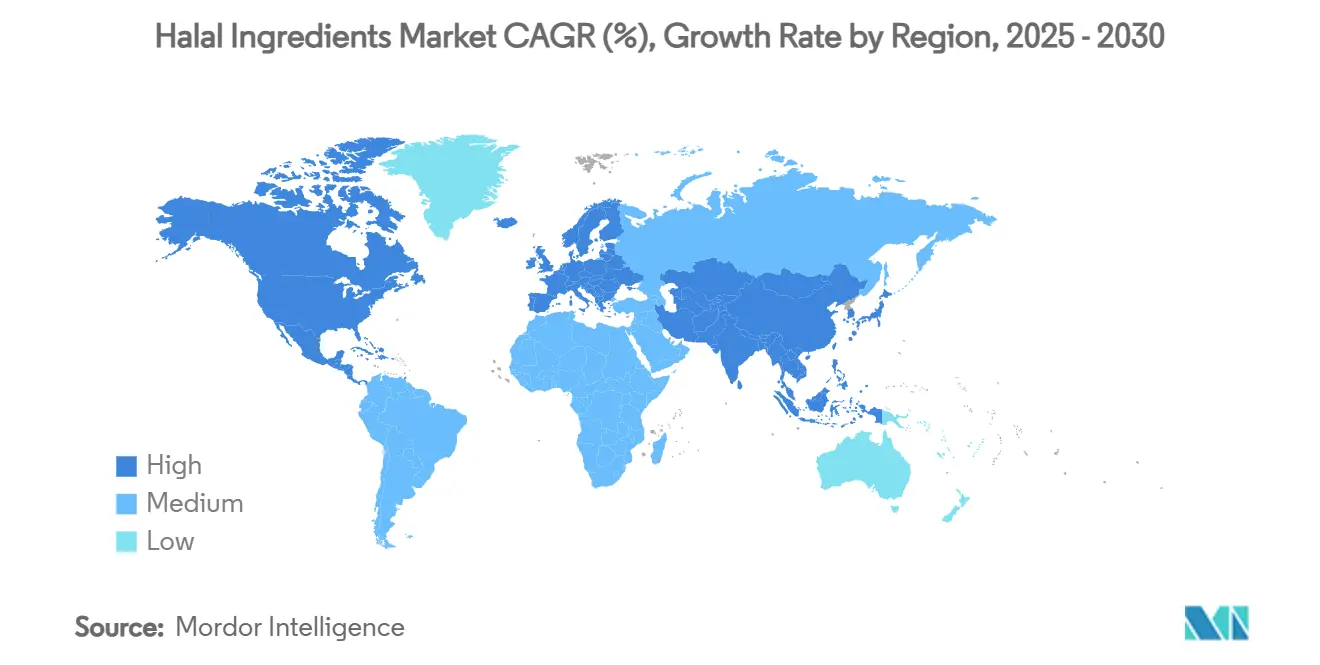

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Halal Ingredients Market Analysis by Mordor Intelligence

The halal ingredients market size reached USD 49.23 billion in 2025 and is expected to grow to USD 65.11 billion by 2030, at a CAGR of 5.75%. This growth is driven by demographic expansion, regulatory requirements, and increasing consumer preference for ethically sourced products. Key regulatory developments include Indonesia's mandatory halal certification framework implemented in October 2024, Saudi Arabia's adoption of GSO 2055-1:2015 standards, and streamlined accreditation processes in export-focused countries[1]Source: U.S. Department of Agriculture, "Indonesia: Indonesia Confirms Extension for Mandatory Halal Certification for Imported Food and Beverage Products and Annulment of Apostille Requirement," fas.usda.gov. The integration of blockchain technology improves supply chain transparency, while advancements in fermentation techniques expand the range of compliant enzymes and proteins. North America leads in market volume due to early consumer adoption, while the Asia-Pacific region shows the highest growth rate, supported by new regulations. The market exhibits moderate competition, with established multinational companies leveraging their research and development capabilities and global distribution networks, while specialized firms capture market opportunities through microbial innovations and clean-label products.

Key Report Takeaways

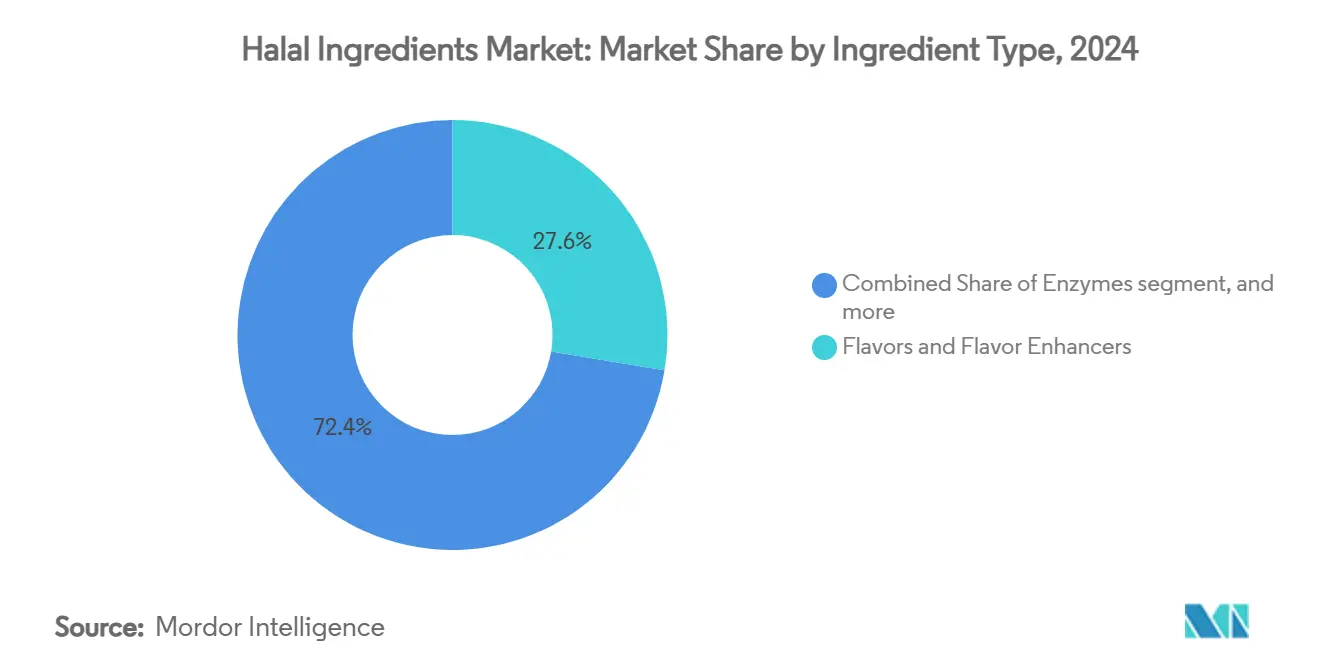

- By ingredient type, flavors and flavor enhancers led with 27.63% of the halal ingredients market share in 2024, while enzymes are projected to grow at a 7.59% CAGR through 2030.

- By source, plant-based inputs accounted for 64.11% of the halal ingredients market size in 2024, whereas microbial sources are set to expand at an 8.31% CAGR between 2025-2030.

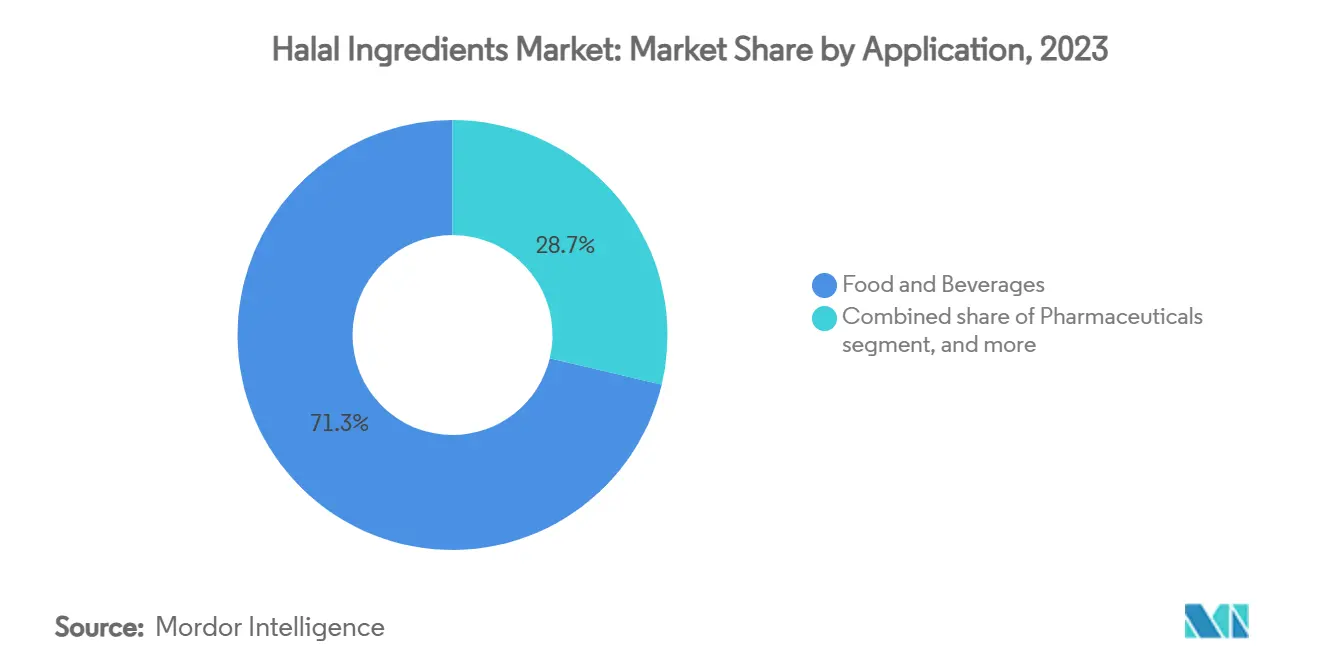

- By application, food and beverages captured 71.28% revenue in 2024; pharmaceuticals are poised for the fastest growth at 9.23% CAGR to 2030.

- By geography, North America held 48.52% of global value in 2024; Asia-Pacific is forecast to register an 8.57% CAGR from 2025-2030.

Global Halal Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of halal-processed foods and packaged goods | +1.2% | Global, with concentration in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Rising global muslim population | +1.8% | Global, with highest impact in Asia-Pacific, North America, Europe | Long term (≥ 4 years) |

| Halal-aligned "clean label" positioning | +0.9% | North America and Europe primarily, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Mandatory halal certification rollouts in indonesia and Saudi Arabia | +1.1% | Asia-Pacific core, spill-over to global trade | Medium term (2-4 years) |

| Rapid growth of halal Cosmetics formulating bases | +0.7% | Asia-Pacific, Middle East, expanding to North America | Medium term (2-4 years) |

| Enhanced auditing and traceability requirements | +0.8% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Halal-Processed Foods and Packaged Goods

The halal ingredients market is experiencing significant growth due to increasing demand for halal-certified processed and packaged foods. Rising incomes, urbanization, and changing consumer lifestyles, particularly among young muslim consumers, are increasing the demand for convenient, ready-to-eat halal products, including snacks, confectionery, bakery items, beverages, and frozen meals. This shift in consumption patterns is compelling manufacturers to reformulate their products using certified halal ingredients to serve the expanding global halal consumer base. The increase in processed food consumption extends beyond muslim-majority markets. Ayana Bio's 2023 "Ultra-Processed Food Pulse" survey reveals that 82% of U.S. adults regularly consume ultra-processed foods, highlighting these products' significance in contemporary diets[2]Source: AyanaBio, "Survey Data Reveals Two-Thirds of American Adults Would Eat More and Pay More for Ultra-processed Foods that Include More Nutritious Ingredients," ayanabio.com. Food manufacturers are responding to health, ethical, and religious dietary preferences by incorporating halal-certified ingredients, even in regions with smaller muslim populations, thus expanding the global demand for halal ingredients.

Rising Global Muslim Population

The global muslim population growth is driving the expansion of the halal ingredients market. The increasing muslim population has created higher demand for halal-compliant foods, beverages, and personal care products. Manufacturers in the food, nutraceutical, and cosmetic industries are responding by incorporating halal-certified ingredients to meet consumer requirements and expand their market presence. This shift has led to significant investments in halal certification processes, ingredient sourcing, and production facilities to ensure compliance with Islamic dietary laws. Indonesia and Pakistan represent significant markets, each comprising approximately 12% of the global muslim population, with 243 million and 241 million muslims, respectively[3]Source: World Population Review, "Muslim Population by Country 2025," worldpopulationreview.com. These large consumer markets are increasing the demand for halal-certified ingredients, including emulsifiers, flavors, and functional proteins, making halal compliance essential for global market growth. The growing awareness of halal requirements among consumers has also influenced multinational companies to reformulate their products and establish dedicated halal production lines to serve these markets effectively.

Halal-Aligned "Clean Label" Positioning

The alignment of halal certification with clean-label trends has created a market opportunity where religious compliance meets consumer demand for transparency and natural ingredients. This alignment allows halal ingredient suppliers to serve both muslim and non-muslim consumers, expanding their market reach. Companies are developing innovative solutions, such as Cargill's partnership with ENOUGH for mycoprotein production, to create plant-based alternatives to animal-derived ingredients. Natural preservation methods, including cultured sugars and fermentation-based acidulants, meet both halal requirements and consumer preferences for recognizable ingredients. According to the Islamic Services of America, non-Muslim consumers increasingly choose halal-certified products, associating them with quality and ethical production[4]Source: Islamic Services of America, "Halal in the Modern World: Balancing Tradition and Contemporary Living," isahalal.com. This market positioning enables ingredient manufacturers to implement premium pricing strategies while expanding their presence, especially in North American and European markets where clean-label preferences are significant. The approach has been successful in categories such as natural sweeteners, plant-based proteins, and organic preservatives, where halal compliance aligns with consumer expectations for minimal processing and ingredient transparency.

Mandatory Halal Certification Rollouts in Indonesia and Saudi Arabia

Indonesia's implementation of Government Regulation No. 42 of 2024, which mandates halal certification for food and beverage products, has established a regulatory framework that other muslim-majority countries are implementing. The regulation uses a phased implementation approach, requiring medium and large companies to comply by October 2024, while micro and small enterprises have until 2026. This structured approach enables comprehensive market transformation while considering industry capacity limitations. Saudi Arabia has implemented GSO 2055-1:2015 standards for halal food requirements across the supply chain, creating unified regulations that support trade within the Gulf Cooperation Council. These mandatory certification requirements have fundamentally changed ingredient sourcing practices, with suppliers investing significantly in compliance infrastructure and certification processes to maintain market access. The regulations have also accelerated technology adoption, particularly blockchain-based traceability systems, as companies work to demonstrate comprehensive compliance to regulatory authorities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of unified global halal standards | -0.8% | Global, with highest impact on international trade | Long term (≥ 4 years) |

| Regulatory and labeling variability between export markets | -0.6% | Export-dependent regions: Asia-Pacific, Middle East | Medium term (2-4 years) |

| Limited consumer awareness in non-muslim markets | -0.4% | North America, Europe, Latin America | Short term (≤ 2 years) |

| Complex and costly certification processes | -0.7% | Global, with highest impact on SMEs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Unified Global Halal Standards

The lack of unified international halal standards creates significant market barriers, as certification bodies across jurisdictions interpret Islamic dietary laws differently. In Canada, the fragmented certification landscape demonstrates this issue, where the absence of a central regulatory authority has resulted in consumer trust concerns, even though the Canadian Food Inspection Agency mandates halal labeling. Multinational ingredient suppliers face operational challenges due to multiple competing standards, requiring them to comply with various certification requirements across markets, which increases costs and delays product launches. The diverse requirements, including Malaysia's JAKIM standards, Indonesia's HAS 23000 criteria, and other national frameworks, create a complex regulatory environment that impedes international trade. Small ingredient suppliers are particularly affected, as they often lack the resources to obtain multiple certifications, which restricts their market access. The standardization issues also affect new ingredient categories, where modern processing methods and biotechnology applications require interpretation of traditional halal principles, resulting in varied rulings from certification bodies. The industry recognizes the need for international standardization to reduce compliance costs and support market growth.

Complex and Costly Certification Processes

The intricate nature of halal certification procedures creates substantial barriers for ingredient manufacturers, particularly smaller enterprises lacking dedicated compliance resources. The certification process requires initial approval and continuous compliance monitoring, with facilities required to maintain separate processing areas for halal and non-halal products, implement comprehensive traceability systems, and undergo regular audits. Ingredient suppliers serving multiple markets face significant challenges in meeting varied documentation requirements, testing protocols, and renewal procedures across different jurisdictions. The costs of certification extend beyond fees to include facility modifications, staff training, supply chain audits, and ongoing compliance monitoring, creating significant financial barriers that can restrict market participation and limit investment in innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Enzymes Drive Biotechnology Shift

Flavors and flavor enhancers held the largest market share at 27.63% in 2024, due to their widespread use across food applications from bakery products to beverages. Enzymes recorded the highest growth rate with a 7.59% CAGR (2025-2030), supported by advancements in halal-compliant enzyme production through biotechnology and increased demand for natural processing aids. The growth in the enzyme segment indicates the industry's shift toward biotechnology solutions, particularly in microbial enzyme production for halal alternatives. Sweeteners maintain a strong market position as manufacturers adopt halal-certified alternatives to traditional sugar substitutes, while chemically-modified fibers provide new sweetening options matching sugar's taste profile. Acidulants and preservatives benefit from clean-label trends, with cultured preservation methods meeting both halal requirements and natural ingredient preferences.

Starches and proteins experience increased competition from new alternatives, while fats and oils show stable demand despite sustainability concerns. Emulsifiers and colorants benefit from the regulatory approval of plant-based options, and antioxidants gain prominence as manufacturers implement natural preservation methods. The ingredient type segmentation demonstrates industry shifts toward biotechnology integration, clean-label formulation, and sustainable sourcing practices, with enzyme innovations combining halal compliance and technological progress.

By Source: Microbial Innovation Challenges Plant Dominance

Plant-based ingredients hold the largest market share at 64.11% in 2024, due to their natural halal compliance and alignment with clean-label trends. Plant-derived ingredients inherently meet halal requirements without extensive certification processes. Microbial sources are growing at the highest rate with an 8.31% CAGR, supported by advancements in fermentation technology and increased regulatory acceptance. The growth in microbial ingredients stems from improvements in precision fermentation and cellular agriculture, which enable the production of complex ingredients traditionally derived from animals.

Animal-based (halal-slaughtered) ingredients remain essential for specific applications but face increased environmental concerns. Synthetic ingredients show varying levels of acceptance based on application type and regional preferences. Microbial innovations in protein production, enzyme manufacturing, and bioactive compounds provide halal alternatives to conventional ingredients while offering potential cost and environmental benefits. While plant-based sources maintain advantages in consumer perception and regulatory acceptance, microbial alternatives are gaining market presence through enhanced functionality in specific applications.

By Application: Pharmaceuticals Accelerate Beyond Food Dominance

Food and beverages applications hold a dominant 71.28% market share in 2024, representing the primary consumer of halal ingredients across bakery, dairy, beverages, and meat products. This segment's dominance reflects its extensive ingredient requirements, ranging from preservation to flavor enhancement across multiple food categories. The pharmaceuticals segment demonstrates the highest growth rate at 9.23% CAGR, driven by increased muslim consumer demand for halal-compliant healthcare products and enhanced regulatory requirements for ingredient transparency. The cosmetics and personal care segment experiences growth due to regulatory changes, particularly in Indonesia, where halal certification for cosmetics becomes mandatory by October 2026.

In the food and beverages segment, bakery and confectionery applications require substantial ingredient volumes, particularly enzymes, emulsifiers, and preservatives. Dairy and desserts manufacturing depends on halal-certified cultures and stabilizers, while the beverages category requires natural flavoring compounds and acidulants. Meat and meat products processing focuses on preservatives and processing aids that maintain halal compliance throughout production. The expansion of halal lifestyle products generates ingredient demand across multiple categories, prompting suppliers to develop specialized formulations for non-food applications that meet halal compliance standards.

Geography Analysis

North America holds the dominant market share at 48.52% in 2024, supported by well-established supply chains, regulatory frameworks, and widespread acceptance of halal products across diverse consumer segments. Asia-Pacific demonstrates the highest growth potential with an 8.57% CAGR, driven by substantial muslim populations, favorable government policies, and increasing middle-class consumption. Europe shows consistent growth due to expanding muslim demographics and standardized regulations, while the Middle East and Africa benefit from traditional halal consumption and government support for halal industry development.

Regional market characteristics vary significantly. North America emphasizes premium products and clean-label compliance, while Asia-Pacific prioritizes volume growth and regulatory adherence. Indonesia's implementation of mandatory halal certification has established a regulatory benchmark, influencing other Southeast Asian markets and increasing demand for certified ingredients. Established markets focus on product premiumization and innovation, while emerging markets prioritize market access and compliance requirements. Asia-Pacific suppliers who demonstrate compliance with multiple certification standards gain advantages in cross-regional trade, establishing the region as a key manufacturing center for halal ingredients.

Europe, the Middle East, and Africa present distinct market characteristics. Europe's halal ingredients market growth is primarily driven by increasing muslim populations in countries like France, Germany, and the UK, alongside growing awareness among non-muslim consumers about halal product quality. The region's regulatory harmonization efforts have streamlined certification processes, facilitating trade across borders. The Middle East and Africa maintain strong traditional halal consumption patterns, with countries like Saudi Arabia, UAE, and Egypt implementing comprehensive halal standards. These regions benefit from established certification bodies, religious oversight, and increasing investments in halal food processing infrastructure.

Competitive Landscape

The halal ingredients market shows high fragmentation, creating opportunities for both multinational corporations and specialized halal-focused suppliers. This fragmentation stems from diverse ingredient categories, regional certification requirements, and varying consumer preferences across global markets. Major companies, such as Cargill Incorporated, Archer-Daniels-Midland Company, and Kerry Group plc, utilize their global supply chains and research and development capabilities to develop halal-compliant ingredients.

Companies that demonstrate comprehensive traceability and certification compliance gain competitive advantages, with blockchain technology emerging as a key differentiator in supply chain transparency. The market shows increased investment in biotechnology, particularly in fermentation technologies and microbial ingredient production, to address halal compliance requirements. Growth opportunities exist in pharmaceutical and cosmetic applications, where demand for halal-certified ingredients is increasing but supply remains limited.

New market entrants are focusing on specialized segments such as halal enzymes, plant-based alternatives, and blockchain-enabled traceability solutions. These companies compete with established players through technological innovation and specialized market knowledge. The market has evolved from primarily focusing on compliance to emphasizing innovation, with technology adoption becoming both a competitive advantage and an entry barrier for smaller companies without digital infrastructure.

Halal Ingredients Industry Leaders

-

Cargill, Incorporated

-

Archer-Daniels-Midland Company

-

Kerry Group plc

-

International Flavors & Fragrances Inc.

-

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Archer Daniels Midland (ADM) opened a 3,000 m² facility in the Lagos Free Trade Zone, near Lekki Deep Sea Port. The facility serves as a regional center for human and animal nutrition, as well as carbohydrate solutions businesses. Located in a business-friendly environment, it supports innovation, collaboration, and distribution throughout West Africa, serving livestock, aquaculture, pet-food markets, and human-food applications.

- August 2024: Cargill launched its first sugar-confectionery blending facility in Southeast Asia at its Pandaan site in East Java, Indonesia. The blending plant combines modified starches, sweeteners, pectin, and carrageenan to create sugar confectionery products with textures designed for Asian consumers. The facility focuses on developing regional specialty solutions while meeting requirements for nature-derived ingredients and halal certification.

- June 2023: Kerry introduced Tastesense™ Advanced, a taste solution for low- and zero-sugar food and beverages. This plant-derived alternative to sugar and stevia enables up to 80% sugar reduction while providing clean sweetness and enhanced mouthfeel without off-notes. The solution reduces carbon emissions by 30% and water usage by 45%. It is non-GMO and available in kosher, halal, and vegan-compliant formats to meet consumer demand for healthier, naturally sweetened products.

- February 2023: Palsgaard completed an EUR 18 million expansion at its Zierikzee factory in the Netherlands, increasing its global PGPR (polyglycerol polyricinoleate) production capacity from 5,750 MT to 11,500 MT annually. PGPR, a plant-based co-emulsifier, is used in chocolate manufacturing to control flow, reduce viscosity, and facilitate the molding process. It also serves in margarine and bakery products to lower fat content and improve texture. The company's PGPR products are palm-free, non-GMO, and meet halal and kosher standards.

Global Halal Ingredients Market Report Scope

| Flavors and Flavor Enhancers |

| Sweeteners |

| Acidulants and Preservatives |

| Hydrocolloids and Stabilizers |

| Starches and Proteins |

| Fats and Oils |

| Enzymes |

| Emulsifiers |

| Colorants |

| Antioxidants |

| Others |

| Plant-based |

| Animal-based (Halal slaughtered) |

| Microbial |

| Synthetic |

| Food and Beverages | Bakery and Confectionery |

| Dairy and Desserts | |

| Beverages | |

| Meat and Meat Products | |

| Soups, Sauces, and Dressings | |

| Other Applications | |

| Cosmetics and Personal Care | |

| Pharmaceuticals | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Ingredient Type | Flavors and Flavor Enhancers | |

| Sweeteners | ||

| Acidulants and Preservatives | ||

| Hydrocolloids and Stabilizers | ||

| Starches and Proteins | ||

| Fats and Oils | ||

| Enzymes | ||

| Emulsifiers | ||

| Colorants | ||

| Antioxidants | ||

| Others | ||

| By Source | Plant-based | |

| Animal-based (Halal slaughtered) | ||

| Microbial | ||

| Synthetic | ||

| By Application | Food and Beverages | Bakery and Confectionery |

| Dairy and Desserts | ||

| Beverages | ||

| Meat and Meat Products | ||

| Soups, Sauces, and Dressings | ||

| Other Applications | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the halal food ingredients market?

The halal food ingredients market size stands at USD 49.23 billion in 2025 and is projected to reach USD 65.11 billion by 2030.

Which region is growing fastest?

Asia-Pacific posts the highest forecast growth, with an 8.57% CAGR driven by Indonesia’s mandatory certification regime and rising disposable incomes.

Which ingredient type is gaining the most momentum?

Enzymes lead growth, expanding at a 7.59% CAGR as microbial fermentation replaces animal-derived inputs.

Why are pharmaceuticals attracting attention?

Muslim consumers increasingly demand fully halal-compliant medicines, propelling the pharmaceutical application segment at a 9.23% CAGR.

Page last updated on: