Infant Formula Ingredients Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

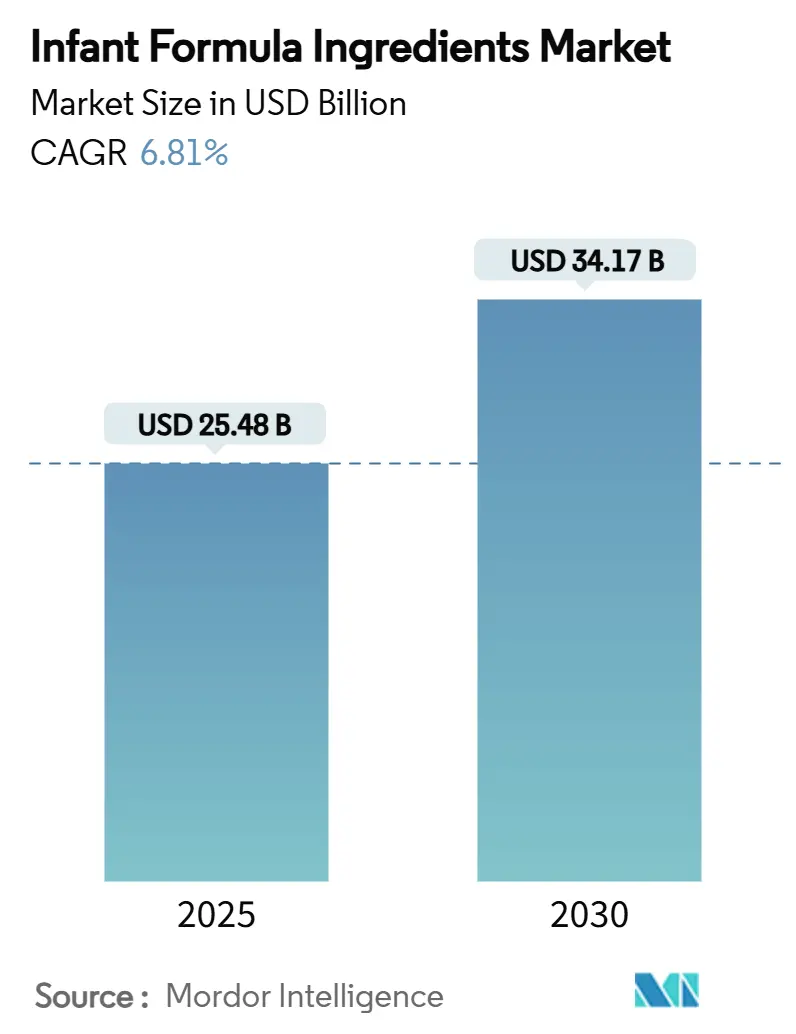

| Market Size (2025) | USD 25.48 Billion |

| Market Size (2030) | USD 34.17 Billion |

| Growth Rate (2025 - 2030) | 6.81% CAGR |

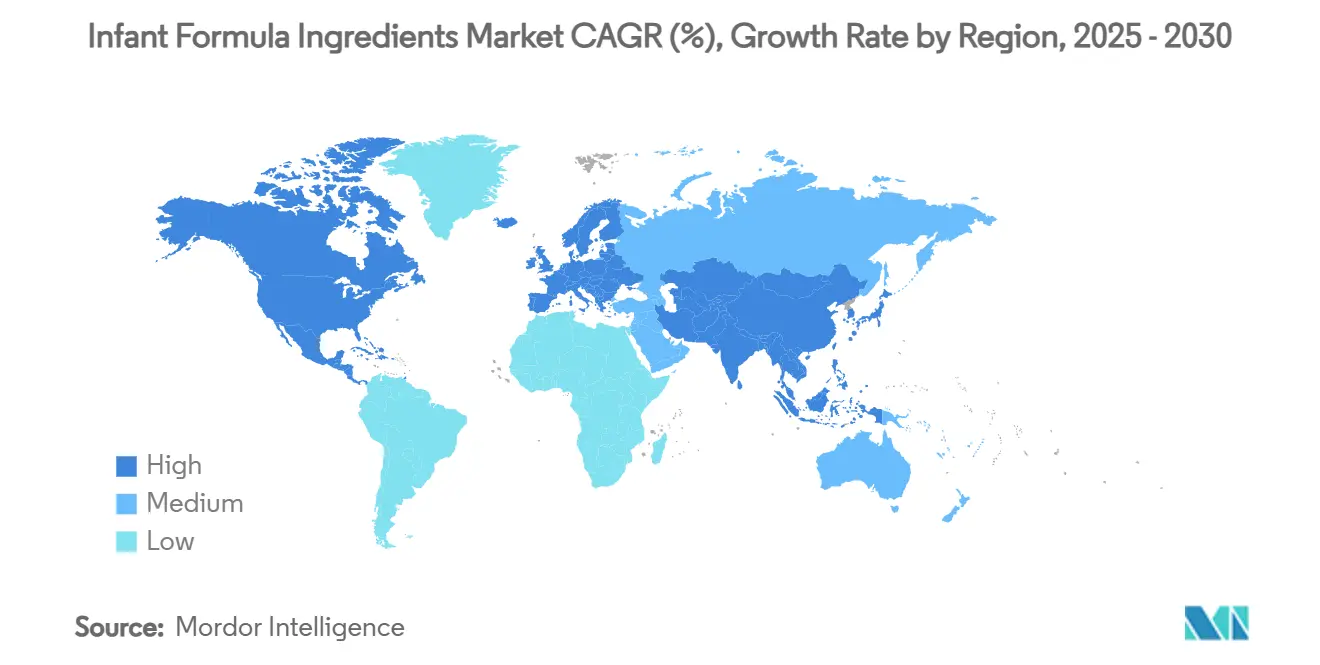

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Infant Formula Ingredients Market Analysis by Mordor Intelligence

The infant formula ingredients market size reached USD 25.48 billion in 2025 and is projected to grow to USD 34.17 billion by 2030, at a CAGR of 6.81% during the forecast period. The market growth is driven by regulatory updates, advancements in precision-fermentation technology, and increasing consumer preference for functional nutrition. The demand for functional ingredients has increased as parents seek formula products that closely mimic human breast milk composition and provide enhanced nutritional benefits. In May 2025, the US Food and Drug Administration (FDA) initiated its first comprehensive review of infant formula nutrient standards since 1998, which may result in stricter ingredient requirements while supporting innovation[1]Source: Federal Register, "Infant Formula Nutrient Requirements; Request for Information," federalregister.gov. This regulatory review aims to ensure formula products meet current nutritional science standards and incorporate the latest research findings on infant development. Human-identical milk oligosaccharides (HMOs) manufactured through precision fermentation have received regulatory approvals in the United States, Europe, and China, enhancing the availability of functional ingredients. These HMOs contribute to infant immune system development, gut health, and cognitive function, making them valuable components in modern infant formula products.

Key Report Takeaways

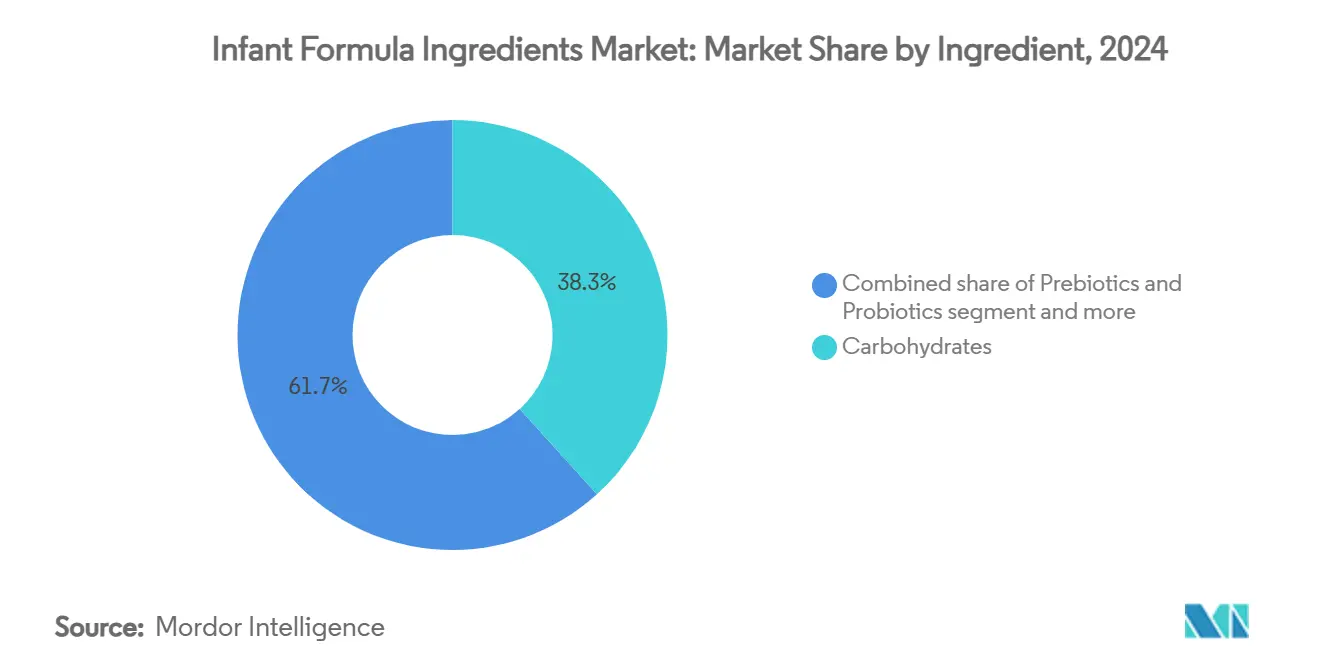

- By ingredient, carbohydrates captured 38.27% of infant formula ingredients market share in 2024, while prebiotics and probiotics are projected to grow at an 8.25% CAGR to 2030.

- By source, cow milk retained 68.46% of the infant formula ingredients market in 2024; goat milk is forecast to post a 9.93% CAGR between 2025 and 2030.

- By form, powder accounted for 74.33% of 2024 revenue, whereas liquid and semi-liquid formats are expected to expand at a 7.59% CAGR through 2030.

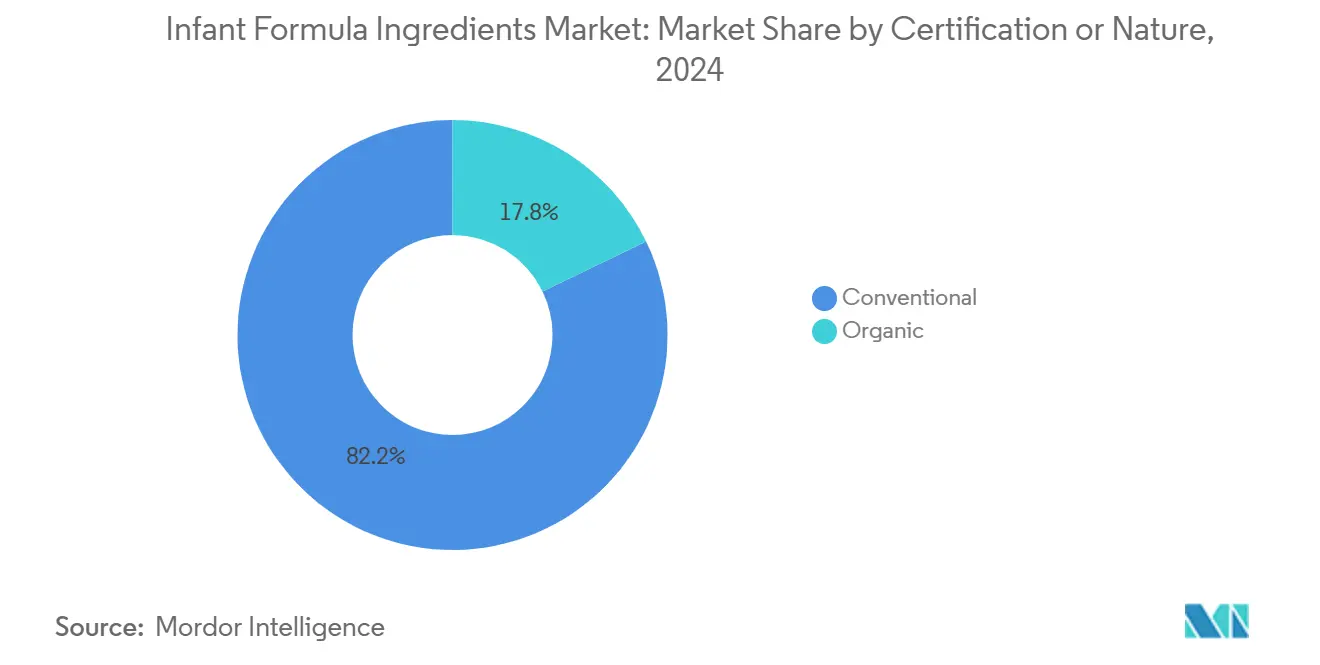

- By certification/nature, conventional products led with an 82.17% share in 2024; the organic segment is on track for a 9.45% CAGR through 2030.

- By application, standard infant formula (stage 1) commanded 46.19% in 2024, while specialty formulas will accelerate at a 9.88% CAGR to 2030.

- By geography, Asia-Pacific dominated with 53.15% of 2024 revenue and is projected to outpace peers at a 9.62% CAGR by 2030.

Global Infant Formula Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising parental awareness of infant nutrition | +1.2% | Global, with early gains in Asia-Pacific and Europe | Medium term (2-4 years) |

| Demand for functional and specialty ingredients | +1.5% | North America and Europe core, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Government-funded fortification mandates | +0.8% | Asia-Pacific core, emerging markets in Middle East and Africa and Latin America | Short term (≤ 2 years) |

| Clean label and organic ingredient trends | +0.9% | North America and Europe, premium segments in Asia-Pacific | Medium term (2-4 years) |

| Commercialisation of precision-fermented HMOs | +1.1% | Global, with regulatory leadership in United States and Europe | Long term (≥ 4 years) |

| Growing demand for multifunctional infant formula ingredients | +0.7% | Global, with innovation centers in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Parental Awareness of Infant Nutrition

Parents' growing understanding of nutrition and increased access to digital health platforms are driving significant changes in consumer behavior, particularly in their demand for detailed transparency in ingredient formulations and nutrient absorption data. This trend is especially prominent in Asia-Pacific markets, where comprehensive government health campaigns consistently emphasize the critical role of early nutrition in cognitive development and overall child health. Parents are now actively seeking ingredients that go beyond basic nutritional requirements, with particular emphasis on gut health components such as prebiotics, probiotics, and human milk oligosaccharides (HMOs) that closely match breast milk composition. The World Health Organization's 2025 digital marketing regulations have substantially increased requirements for ingredient transparency, compelling manufacturers to provide extensive scientific research to support their health claims. This heightened consumer awareness and demand for scientific validation is fundamentally reshaping product development strategies, as companies invest significantly in comprehensive clinical studies to validate their premium products and differentiate themselves in the market.

Demand for Functional and Specialty Ingredients

The infant formula ingredients market is experiencing growth due to increased demand for functional and specialty ingredients. This growth stems from parents' heightened focus on infant health, immunity, and developmental nutrition. Parents' increasing awareness of early-life nutrition's impact on long-term physical and cognitive development has prompted manufacturers to develop formulas that more closely match human breast milk composition. This has increased the use of specialized ingredients, including prebiotics, probiotics, human milk oligosaccharides (HMOs), omega-3 fatty acids (DHA/ARA), nucleotides, and bioactive proteins. Consumer preferences have shifted from basic nutritional requirements to formulas offering digestive, immune, and cognitive benefits. This shift has intensified research and development in biofunctional ingredients that replicate breast milk's immunological and nutritional properties. Premium formula products in both developed and emerging markets are increasingly incorporating ingredients such as HMOs and lactoferrin, which support gut microbiota development and immune defense.

Government-Funded Fortification Mandates

Government food fortification programs are expanding globally, with WHO guidelines emphasizing micronutrient supplementation as a public health imperative for infant development. China implemented 50 new food safety standards in March 2025, including mandatory choline requirements and enhanced vitamin and mineral specifications, directly impacting ingredient demand patterns. The Food Fortification Initiative's recommendations for iron, folic acid, and vitamin supplementation are gaining adoption in emerging markets, increasing demand for specialized ingredient blends. India's FSSAI regulations specify nutritional requirements for imported infant foods, while Indonesia's BPOM framework requires comprehensive microbiological and chemical testing. These regulatory frameworks have significant impact in regions with high malnutrition rates, where government procurement programs establish consistent demand volumes.

Clean Label and Organic Ingredient Trends

The demand for clean label formulations is influencing ingredient sourcing strategies, as manufacturers remove artificial additives in favor of minimally processed alternatives that preserve nutritional value. The organic infant formula market is growing rapidly due to consumers' readiness to pay higher prices for certified organic ingredients that support sustainability. The European Food Safety Authority's (EFSA) 2024 safety reassessment of guar gum (E 412) in infant foods identified risks related to toxic element exposure, leading manufacturers to explore natural thickening alternatives[2]Source: EFSA, "Re-evaluation of guar gum (E 412) as a food additive in foods for infants below 16 weeks of age and follow-up of its re-evaluation as food additive for uses in foods for all population groups," efsa.onlinelibrary.wiley.com. This increased regulatory oversight has encouraged the use of plant-based functional ingredients, including pectin and inulin, which offer prebiotic benefits without synthetic components. Clean label requirements also influence processing techniques, with companies developing gentle extraction methods that maintain bioactive compounds while ensuring safety compliance. Natural preservation systems and technologies for stabilizing bioactive ingredients are emerging from the convergence of clean label requirements and functional benefits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying advocacy for breastfeeding as the optimal choice | -1.8% | Global, with strongest impact in developed markets | Long term (≥ 4 years) |

| Food allergy and intolerance prevalence | -0.6% | North America and Europe, emerging concerns in Asia-Pacific | Medium term (2-4 years) |

| Stringent regulatory scrutiny and compliance costs | -0.9% | Global, with highest impact in regulated markets | Short term (≤ 2 years) |

| Price sensitivity in ingredient sourcing | -0.4% | Emerging markets, cost-conscious segments globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intensifying Advocacy for Breastfeeding as the Optimal Choice

Global breastfeeding advocacy has intensified through coordinated WHO and UNICEF initiatives, with the 2025 resolution on digital marketing regulation specifically targeting formula companies' online promotional strategies. The International Code of Marketing of Breast-milk Substitutes implementation has achieved widespread adoption, with 144 countries incorporating code provisions into national legislation, creating regulatory barriers for formula marketing[3]Source: International Breastfeeding Journal, "Outcomes of implementing the International Code of Marketing of Breast-milk Substitutes as national laws: a systematic review," internationalbreastfeedingjournal.biomedcentral.com. The Baby Friendly Initiative's expansion across healthcare systems is creating institutional barriers to formula promotion, while digital marketing restrictions limit companies' ability to reach new parents through online channels. Climate advocacy has introduced environmental arguments against formula use, with carbon footprint calculations showing significant emissions from commercial milk formula production and distribution. These advocacy efforts are particularly effective in developed markets where breastfeeding rates correlate with education levels and healthcare access, creating headwinds for premium formula segments.

Stringent Regulatory Scrutiny and Compliance Costs

The 2022 United States formula crisis has resulted in stricter regulatory requirements, with agencies implementing enhanced safety protocols and comprehensive supply chain monitoring procedures. The FDA's Operation Stork Speed now requires manufacturers to submit detailed risk management plans, while additional testing requirements for heavy metals and contaminants increase operational costs across operations. EFSA's novel food assessment procedures for HMOs maintain rigorous safety evaluation standards, significantly impacting product launch timelines and development costs. Companies developing innovative ingredients face substantial challenges when navigating multiple jurisdictions with different approval processes and extensive documentation requirements. For novel ingredients, regulatory compliance costs account for 15-20% of total product development expenses, creating significant entry barriers for smaller biotechnology companies and providing established companies with regulatory expertise a competitive advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient: Precision Fermentation Reshapes Traditional Categories

Carbohydrates held the largest market share at 38.27% in 2024, driven by lactose demand from traditional formula manufacturers. The prebiotics and probiotics segment is projected to grow at 8.25% CAGR through 2030. In the protein segment, precision fermentation technology enables the production of human casein micelles, which offer improved digestibility and nutrient absorption compared to bovine proteins. The vitamins and minerals segment growth is supported by government fortification mandates, particularly in emerging markets where micronutrient deficiency regulations require enhanced supplementation.

Human Milk Oligosaccharides (HMOs) show significant growth potential, as precision fermentation enables large-scale production of complex oligosaccharides. The "Others" segment includes bioactive ingredients that command higher prices due to their functional benefits. In 2024, EFSA's streamlined assessment procedures for human-identical compounds have accelerated regulatory approvals for novel ingredients, enabling biotechnology companies to compete with traditional suppliers through enhanced functionality and sustainability.

By Source: Goat Milk Gains Regulatory Momentum

Cow milk maintained its dominant position in the source segment with 68.46% market share in 2024, supported by established supply chains and processing infrastructure. Goat milk alternatives recorded the highest growth rate at 9.93% CAGR, following FDA approvals for brands like Kendamil and Kabrita in the US market. The protein hydrolysates segment continues to expand as manufacturers address food allergy concerns. Arla Foods received FDA approval for specialized hydrolysates that improve allergy management and gut comfort in infant formulas.

Soy-based alternatives maintain consistent demand in markets with high lactose intolerance, though their growth remains limited by consumer preference for animal-derived proteins. Regulatory frameworks continue to evolve for new protein sources, as demonstrated by Australia and New Zealand's approval of genetically modified E. coli for 2'-fucosyllactose production in infant formulas. This approval indicates increasing acceptance of biotechnology-derived ingredients. Following the 2022 formula crisis, companies are implementing source diversification strategies to enhance supply chain resilience.

By Form: Liquid Formats Gain Convenience Premium

Powder formulations maintained market leadership with 74.33% share in 2024, benefiting from cost efficiency and extended shelf life characteristics that appeal to both manufacturers and consumers, while liquid and semi-liquid formats demonstrated accelerated growth at 7.59% CAGR, driven by convenience preferences and supply chain optimization strategies. The powder segment's dominance reflects manufacturing economics and distribution advantages, particularly in emerging markets where refrigeration infrastructure limitations favor shelf-stable products.

However, liquid formats are gaining traction in developed markets where convenience commands premium pricing and parents prioritize ready-to-use solutions. Manufacturing innovations in liquid processing are addressing traditional limitations, with companies investing in aseptic packaging technologies that extend shelf life while maintaining nutritional integrity. Supply chain considerations favor liquid formats in regions with reliable cold chain infrastructure, while powder alternatives remain essential for markets with distribution challenges and cost sensitivity.

By Certification/Nature: Organic Growth Accelerates

Conventional formulations dominated with 82.17% market share in 2024, reflecting cost considerations and established manufacturing processes, while organic alternatives achieved robust 9.45% CAGR growth, driven by consumer willingness to pay premiums for certified organic ingredients that align with sustainability values. The organic segment benefits from clean label trends and environmental consciousness, with brands like HiPP achieving carbon neutrality for organic product lines through renewable energy adoption and regenerative farming practices.

Regulatory frameworks increasingly support organic certification, with EFSA maintaining stringent standards for organic ingredient approval while streamlining assessment procedures for established suppliers. The conventional segment maintains advantages in cost efficiency and ingredient availability, particularly for specialized functional ingredients that may not have organic alternatives. Manufacturing scalability remains a constraint for organic ingredients, with supply chain limitations creating price volatility that affects market growth potential in cost-sensitive segments.

By Application: Specialty Formulas Drive Innovation

Standard infant formula (Stage 1) holds the largest market share at 46.19% in 2024, serving healthy full-term infants. Specialty formulas exhibit the highest growth rate at 9.88% CAGR, reflecting increased awareness of specific nutritional and medical requirements. Follow-on formula (Stage 2) and growing-up milk (Stage 3) segments address distinct nutritional needs at different developmental stages, enabling ingredient suppliers to develop targeted formulations. The specialty formula category includes hypoallergenic, anti-reflux, and medical nutrition products.

These command higher prices due to their therapeutic properties and specialized production processes. Manufacturers are advancing specialty formula development through precision fermentation technologies, producing human-identical proteins that target specific medical conditions more effectively than conventional options. Specialty formulas face stringent regulatory requirements for safety assessment and clinical validation. While these requirements create market entry barriers, they also protect established manufacturers' market positions. The segment maintains consistent demand through healthcare professional endorsements and insurance coverage in certain markets, despite premium pricing compared to standard formulas.

Geography Analysis

Asia-Pacific dominates the global infant formula ingredients market with a 53.15% share in 2024 and is projected to grow at 9.62% CAGR through 2030. North America represents a mature market with established regulatory frameworks. The 2022 formula crisis prompted increased investments in supply chain resilience and regulatory modernization. The FDA's comprehensive nutrient review initiative in May 2025 suggests potential specification changes that may affect ingredient demand patterns, while Operation Stork Speed enhances safety protocols and monitoring requirements.

The United States and Canada show increased consumer demand for hypoallergenic, organic, and specialty formulas due to growing parental awareness of food sensitivities and functional nutrition. Ingredient manufacturers are developing plant-based proteins, non-GMO sources, and bioactive components to address these requirements. Europe maintains regulatory oversight through EFSA's assessment procedures for novel ingredients, with human-identical milk oligosaccharides receiving multiple approvals in 2024. The region's emphasis on sustainability and clean label formulations increases demand for organic and precision-fermented ingredients.

Latin America shows growth potential, driven by improving birth rates in Brazil and Mexico, and increasing urbanization that enhances access to modern retail and healthcare. Government nutrition programs and public-private partnerships improve early-life nutrition awareness, benefiting formula manufacturers. The market is moving toward fortified formulas with functional proteins, essential fatty acids, and prebiotics to address micronutrient deficiencies and gut health. The Middle East and Africa market continues to develop, supported by rising incomes, urbanization, and women's workforce participation, resulting in increased demand for infant nutrition products.

Competitive Landscape

The infant formula ingredients market demonstrates moderate fragmentation, with a fragmentation level of 4 out of 10, creating significant opportunities for specialized suppliers and biotechnology companies to challenge established players through advanced technological innovation and comprehensive regulatory expertise. Major dairy companies, including FrieslandCampina, Fonterra, and Arla Foods, maintain their strong market positions through well-established integrated supply chains and sophisticated processing capabilities.

The competitive environment is primarily influenced by complex regulatory approval timelines and extensive clinical validation capabilities, with companies making substantial investments in scientific research and documentation to support premium product positioning strategies in the global marketplace. The market's moderate concentration level creates substantial opportunities in specialized segments such as HMOs, protein hydrolysates, and bioactive compounds, where stringent regulatory barriers effectively protect existing market positions while simultaneously reducing competitive intensity across the industry.

New market entrants are successfully gaining market share by emphasizing their strong sustainability credentials and superior functional benefits, while established companies actively respond through strategic acquisitions and increased investments in internal research and development initiatives to maintain their competitive advantage.

Infant Formula Ingredients Industry Leaders

-

FrieslandCampina Ingredients

-

Fonterra Co-operative Group Limited

-

Arla Foods amba

-

Glanbia plc

-

DSM-Firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Royal FrieslandCampina is investing EUR 50 million to upgrade its whey processing facilities in the Netherlands. The company will allocate EUR 30 million to Workum for converting whey byproducts into Whey Protein Concentrate (WPC) by 2026. This upgrade will replace the existing gas-powered evaporator, reducing CO₂ emissions by 6,800 tons annually and conserving 350,000 m³ of water. The remaining EUR 20 million investment in Gerkesklooster will optimize whey processing for infant nutrition and implement a new milk reception system. These improvements will enhance protein recovery, with operations scheduled to begin by mid-2026.

- October 2024: DSM-Firmenich introduced a dry form of vitamin A for infant nutrition products. The product, "Dry Vit A Palmitate for Early Life Nutrition," represents an advancement in infant nutrition technology, improving nutrient delivery for formula-fed infants worldwide.

- May 2023: Arla Foods Ingredients launched Lacprodan Alpha-50, an alpha-lactalbumin-rich whey protein ingredient for low-protein infant formulas. The product contains 90% alpha-lactalbumin protein, enabling manufacturers to reduce total protein content while maintaining nutritional quality and better matching human breast milk composition. This development addresses health concerns regarding the relationship between high infant protein intake, accelerated weight gain, and obesity risk in later life.

Global Infant Formula Ingredients Market Report Scope

| Carbohydrates |

| Fats and Oils |

| Proteins |

| Vitamins and Minerals |

| Prebiotics and Probiotics |

| Human Milk Oligosaccharides (HMOs) |

| Others |

| Cow Milk |

| Goat Milk |

| Soy |

| Protein Hydrolysates |

| Others |

| Powder |

| Liquid and Semi-Liquid |

| Conventional |

| Organic |

| Standard Infant Formula (Stage 1) |

| Follow-On Formula (Stage 2) |

| Growing-Up Milk (Stage 3) |

| Specialty Formula |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Ingredient | Carbohydrates | |

| Fats and Oils | ||

| Proteins | ||

| Vitamins and Minerals | ||

| Prebiotics and Probiotics | ||

| Human Milk Oligosaccharides (HMOs) | ||

| Others | ||

| By Source | Cow Milk | |

| Goat Milk | ||

| Soy | ||

| Protein Hydrolysates | ||

| Others | ||

| By Form | Powder | |

| Liquid and Semi-Liquid | ||

| By Certification/Nature | Conventional | |

| Organic | ||

| By Application | Standard Infant Formula (Stage 1) | |

| Follow-On Formula (Stage 2) | ||

| Growing-Up Milk (Stage 3) | ||

| Specialty Formula | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the infant formula ingredients market?

The infant formula ingredients market size stood at USD 25.48 billion in 2025 and is projected to reach USD 34.17 billion by 2030

Which region leads global demand?

Asia-Pacific accounted for 53.15% of 2024 revenue and is expected to grow at a 9.62% CAGR, driven by regulatory standardization and rising birth expectations in China

Which ingredient segment is expanding fastest?

Prebiotics and probiotics are the fastest, forecast to advance at an 8.25% CAGR through 2030 as parents focus on gut health

How are precision-fermented HMOs influencing product development?

Commercial-scale fermentation of HMOs delivers human-identical oligosaccharides that enrich formulas with breast-milk-like prebiotic benefits and are increasingly approved across major markets

Page last updated on: